Financial Analysis Report: ABC Ltd. - Capital Budgeting Techniques

VerifiedAdded on 2021/06/17

|14

|1707

|49

Report

AI Summary

This report provides a financial analysis of ABC Ltd., focusing on capital budgeting techniques for project selection. It explores methods like Annual Worth, Present Worth, Internal Rate of Return, and Benefit/Cost analysis to evaluate investment options. The report delves into Net Present Value (NPV), Minimum Acceptable Rate of Return (MARR), and Equivalent Annual Cost calculations for machinery selection. It also discusses the gaps in Life Cycle Costing, which considers costs throughout a product's lifespan, and offers recommendations to improve benefit/cost analysis and risk management. The student analyzes various aspects of financial decision-making, including the importance of capital structure and risk assessment in investment strategies. The report provides valuable insights into financial analysis and its application in real-world business scenarios.

Running head: FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

Name of the Student:

Name of the University:

Author’s Note:

FINANCIAL ANALYSIS

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ANALYSIS

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................6

Answer to Question 3......................................................................................................................7

Answer to Question 4......................................................................................................................8

Answer to Question 5......................................................................................................................9

Introduction..................................................................................................................................9

Gaps in Life Cycle Costing..........................................................................................................9

Recommendations......................................................................................................................11

Reference.......................................................................................................................................13

FINANCIAL ANALYSIS

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................6

Answer to Question 3......................................................................................................................7

Answer to Question 4......................................................................................................................8

Answer to Question 5......................................................................................................................9

Introduction..................................................................................................................................9

Gaps in Life Cycle Costing..........................................................................................................9

Recommendations......................................................................................................................11

Reference.......................................................................................................................................13

2

FINANCIAL ANALYSIS

Answer to Question 1

The annual worth of the company represents the annual equivalent value of all cash

inflows and cash outflows of the alternatives options (2). This method is usually used for making

comparison between the viability of two projects. In this method only one life cycle of the

project is to be evaluated. Present worth is used to estimate the future cash inflows from a project

and is normally used in capital budgeting techniques. Internal Rate of Return is the rate at which

the present value of the cash inflows and cash outflows becomes zero (4).

Capital Investment decision are often based on the analysis of Annual Worth, Present

Worth and Internal rate of return. The annual worth of the projects helps the business in making

comparison between alternative projects with the proposed projects. The present worth of the

project is used by businesses to determine the present value of cash inflows which the business

can expect from the project (3). The IRR of the project determines the minimum rate of return

which the company needs to earn. These are important factors which are needed to be considered

while taking investment decisions.

FINANCIAL ANALYSIS

Answer to Question 1

The annual worth of the company represents the annual equivalent value of all cash

inflows and cash outflows of the alternatives options (2). This method is usually used for making

comparison between the viability of two projects. In this method only one life cycle of the

project is to be evaluated. Present worth is used to estimate the future cash inflows from a project

and is normally used in capital budgeting techniques. Internal Rate of Return is the rate at which

the present value of the cash inflows and cash outflows becomes zero (4).

Capital Investment decision are often based on the analysis of Annual Worth, Present

Worth and Internal rate of return. The annual worth of the projects helps the business in making

comparison between alternative projects with the proposed projects. The present worth of the

project is used by businesses to determine the present value of cash inflows which the business

can expect from the project (3). The IRR of the project determines the minimum rate of return

which the company needs to earn. These are important factors which are needed to be considered

while taking investment decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ANALYSIS

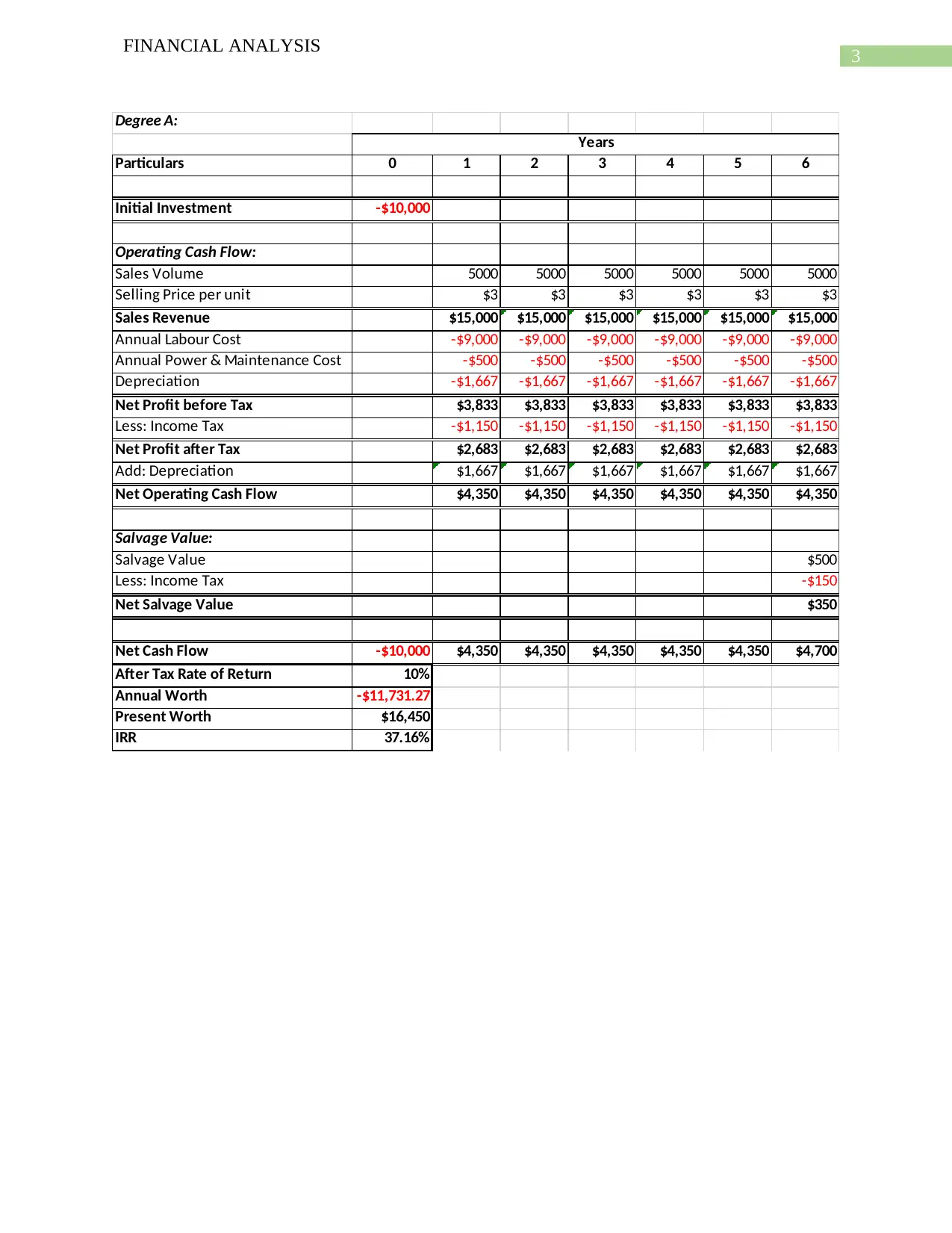

Degree A:

Particulars 0 1 2 3 4 5 6

Initial Investment -$10,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$9,000 -$9,000 -$9,000 -$9,000 -$9,000 -$9,000

Annual Power & Maintenance Cost -$500 -$500 -$500 -$500 -$500 -$500

Depreciation -$1,667 -$1,667 -$1,667 -$1,667 -$1,667 -$1,667

Net Profit before Tax $3,833 $3,833 $3,833 $3,833 $3,833 $3,833

Less: Income Tax -$1,150 -$1,150 -$1,150 -$1,150 -$1,150 -$1,150

Net Profit after Tax $2,683 $2,683 $2,683 $2,683 $2,683 $2,683

Add: Depreciation $1,667 $1,667 $1,667 $1,667 $1,667 $1,667

Net Operating Cash Flow $4,350 $4,350 $4,350 $4,350 $4,350 $4,350

Salvage Value:

Salvage Value $500

Less: Income Tax -$150

Net Salvage Value $350

Net Cash Flow -$10,000 $4,350 $4,350 $4,350 $4,350 $4,350 $4,700

After Tax Rate of Return 10%

Annual Worth -$11,731.27

Present Worth $16,450

IRR 37.16%

Years

FINANCIAL ANALYSIS

Degree A:

Particulars 0 1 2 3 4 5 6

Initial Investment -$10,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$9,000 -$9,000 -$9,000 -$9,000 -$9,000 -$9,000

Annual Power & Maintenance Cost -$500 -$500 -$500 -$500 -$500 -$500

Depreciation -$1,667 -$1,667 -$1,667 -$1,667 -$1,667 -$1,667

Net Profit before Tax $3,833 $3,833 $3,833 $3,833 $3,833 $3,833

Less: Income Tax -$1,150 -$1,150 -$1,150 -$1,150 -$1,150 -$1,150

Net Profit after Tax $2,683 $2,683 $2,683 $2,683 $2,683 $2,683

Add: Depreciation $1,667 $1,667 $1,667 $1,667 $1,667 $1,667

Net Operating Cash Flow $4,350 $4,350 $4,350 $4,350 $4,350 $4,350

Salvage Value:

Salvage Value $500

Less: Income Tax -$150

Net Salvage Value $350

Net Cash Flow -$10,000 $4,350 $4,350 $4,350 $4,350 $4,350 $4,700

After Tax Rate of Return 10%

Annual Worth -$11,731.27

Present Worth $16,450

IRR 37.16%

Years

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ANALYSIS

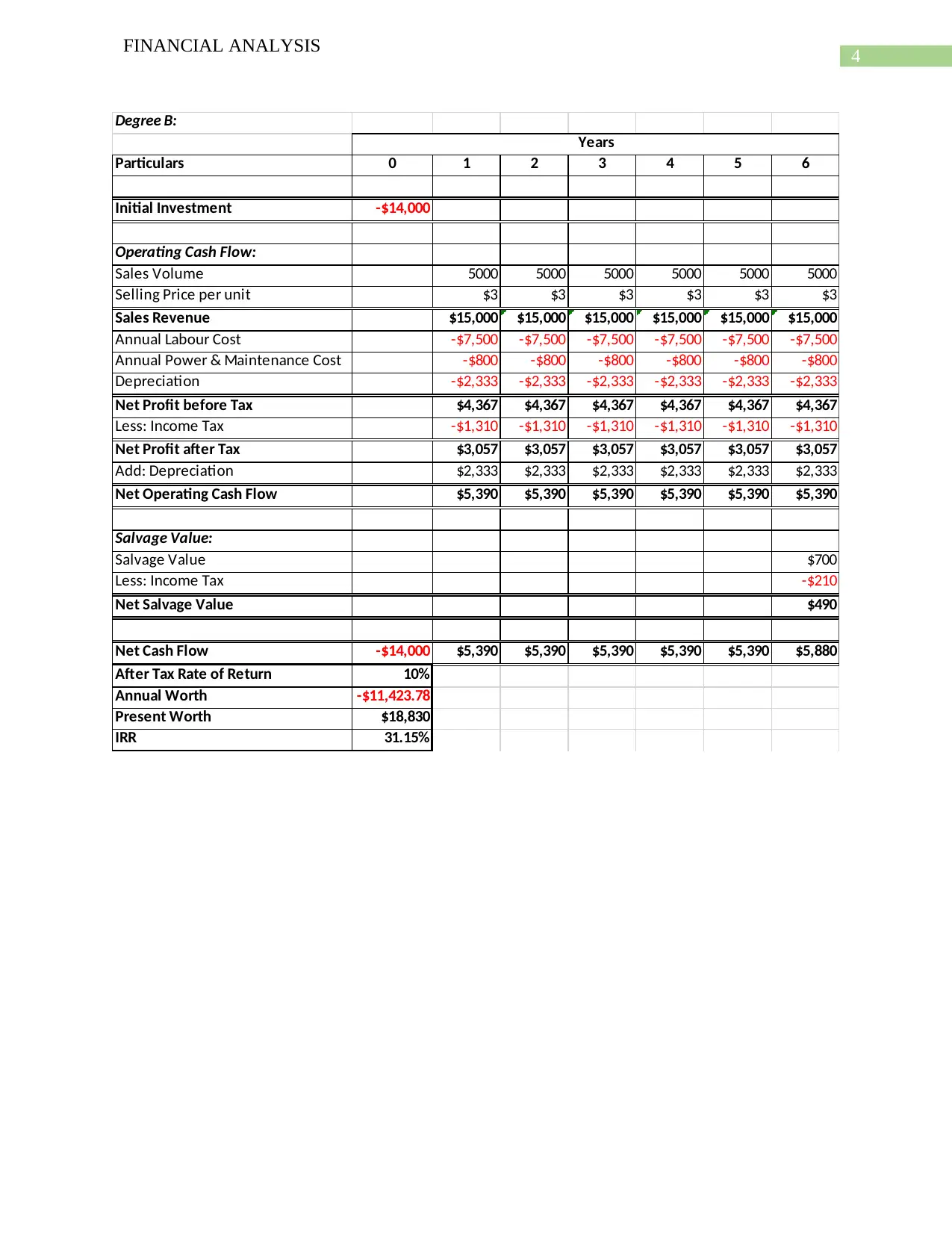

Degree B:

Particulars 0 1 2 3 4 5 6

Initial Investment -$14,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$7,500 -$7,500 -$7,500 -$7,500 -$7,500 -$7,500

Annual Power & Maintenance Cost -$800 -$800 -$800 -$800 -$800 -$800

Depreciation -$2,333 -$2,333 -$2,333 -$2,333 -$2,333 -$2,333

Net Profit before Tax $4,367 $4,367 $4,367 $4,367 $4,367 $4,367

Less: Income Tax -$1,310 -$1,310 -$1,310 -$1,310 -$1,310 -$1,310

Net Profit after Tax $3,057 $3,057 $3,057 $3,057 $3,057 $3,057

Add: Depreciation $2,333 $2,333 $2,333 $2,333 $2,333 $2,333

Net Operating Cash Flow $5,390 $5,390 $5,390 $5,390 $5,390 $5,390

Salvage Value:

Salvage Value $700

Less: Income Tax -$210

Net Salvage Value $490

Net Cash Flow -$14,000 $5,390 $5,390 $5,390 $5,390 $5,390 $5,880

After Tax Rate of Return 10%

Annual Worth -$11,423.78

Present Worth $18,830

IRR 31.15%

Years

FINANCIAL ANALYSIS

Degree B:

Particulars 0 1 2 3 4 5 6

Initial Investment -$14,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$7,500 -$7,500 -$7,500 -$7,500 -$7,500 -$7,500

Annual Power & Maintenance Cost -$800 -$800 -$800 -$800 -$800 -$800

Depreciation -$2,333 -$2,333 -$2,333 -$2,333 -$2,333 -$2,333

Net Profit before Tax $4,367 $4,367 $4,367 $4,367 $4,367 $4,367

Less: Income Tax -$1,310 -$1,310 -$1,310 -$1,310 -$1,310 -$1,310

Net Profit after Tax $3,057 $3,057 $3,057 $3,057 $3,057 $3,057

Add: Depreciation $2,333 $2,333 $2,333 $2,333 $2,333 $2,333

Net Operating Cash Flow $5,390 $5,390 $5,390 $5,390 $5,390 $5,390

Salvage Value:

Salvage Value $700

Less: Income Tax -$210

Net Salvage Value $490

Net Cash Flow -$14,000 $5,390 $5,390 $5,390 $5,390 $5,390 $5,880

After Tax Rate of Return 10%

Annual Worth -$11,423.78

Present Worth $18,830

IRR 31.15%

Years

5

FINANCIAL ANALYSIS

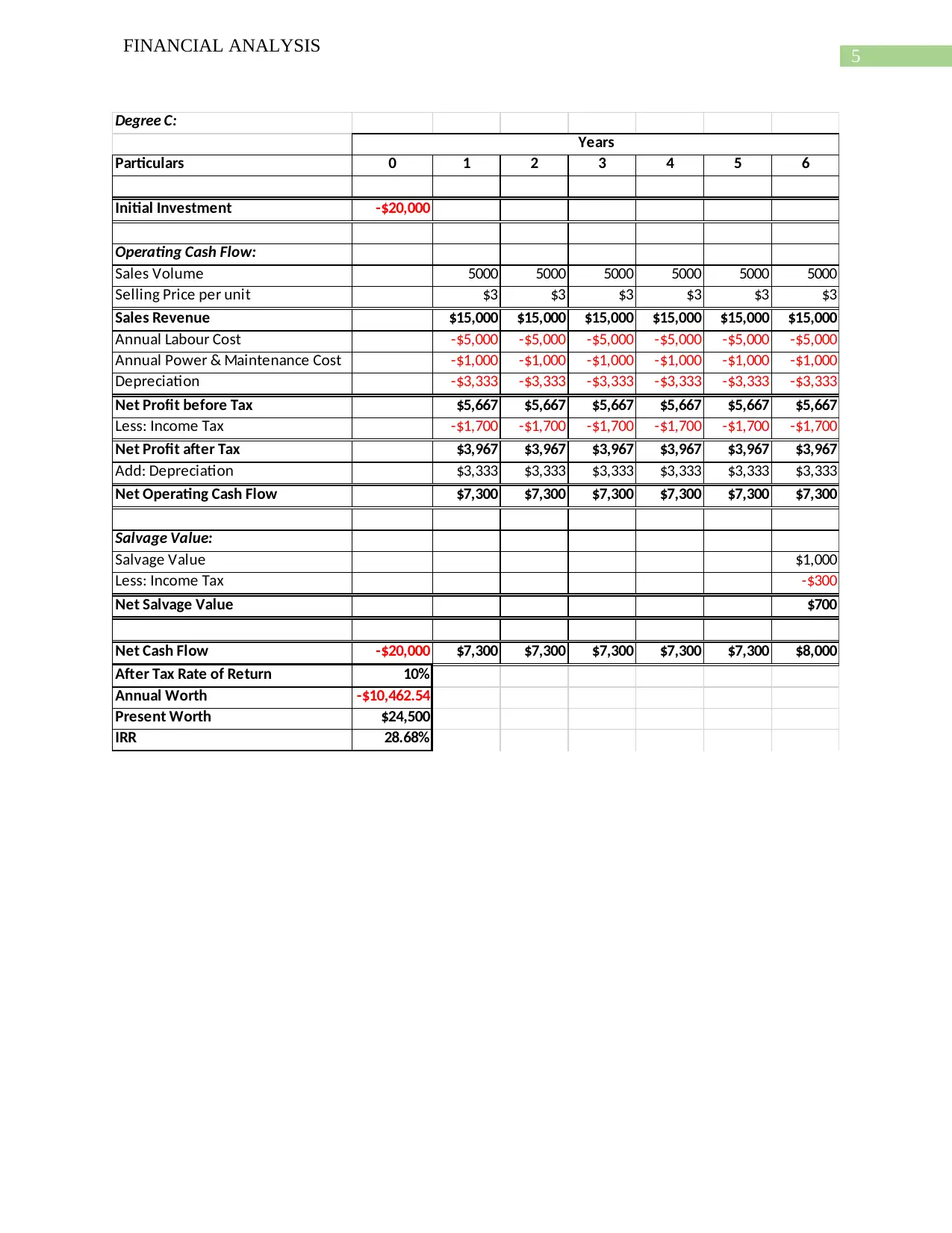

Degree C:

Particulars 0 1 2 3 4 5 6

Initial Investment -$20,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$5,000 -$5,000 -$5,000 -$5,000 -$5,000 -$5,000

Annual Power & Maintenance Cost -$1,000 -$1,000 -$1,000 -$1,000 -$1,000 -$1,000

Depreciation -$3,333 -$3,333 -$3,333 -$3,333 -$3,333 -$3,333

Net Profit before Tax $5,667 $5,667 $5,667 $5,667 $5,667 $5,667

Less: Income Tax -$1,700 -$1,700 -$1,700 -$1,700 -$1,700 -$1,700

Net Profit after Tax $3,967 $3,967 $3,967 $3,967 $3,967 $3,967

Add: Depreciation $3,333 $3,333 $3,333 $3,333 $3,333 $3,333

Net Operating Cash Flow $7,300 $7,300 $7,300 $7,300 $7,300 $7,300

Salvage Value:

Salvage Value $1,000

Less: Income Tax -$300

Net Salvage Value $700

Net Cash Flow -$20,000 $7,300 $7,300 $7,300 $7,300 $7,300 $8,000

After Tax Rate of Return 10%

Annual Worth -$10,462.54

Present Worth $24,500

IRR 28.68%

Years

FINANCIAL ANALYSIS

Degree C:

Particulars 0 1 2 3 4 5 6

Initial Investment -$20,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$5,000 -$5,000 -$5,000 -$5,000 -$5,000 -$5,000

Annual Power & Maintenance Cost -$1,000 -$1,000 -$1,000 -$1,000 -$1,000 -$1,000

Depreciation -$3,333 -$3,333 -$3,333 -$3,333 -$3,333 -$3,333

Net Profit before Tax $5,667 $5,667 $5,667 $5,667 $5,667 $5,667

Less: Income Tax -$1,700 -$1,700 -$1,700 -$1,700 -$1,700 -$1,700

Net Profit after Tax $3,967 $3,967 $3,967 $3,967 $3,967 $3,967

Add: Depreciation $3,333 $3,333 $3,333 $3,333 $3,333 $3,333

Net Operating Cash Flow $7,300 $7,300 $7,300 $7,300 $7,300 $7,300

Salvage Value:

Salvage Value $1,000

Less: Income Tax -$300

Net Salvage Value $700

Net Cash Flow -$20,000 $7,300 $7,300 $7,300 $7,300 $7,300 $8,000

After Tax Rate of Return 10%

Annual Worth -$10,462.54

Present Worth $24,500

IRR 28.68%

Years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ANALYSIS

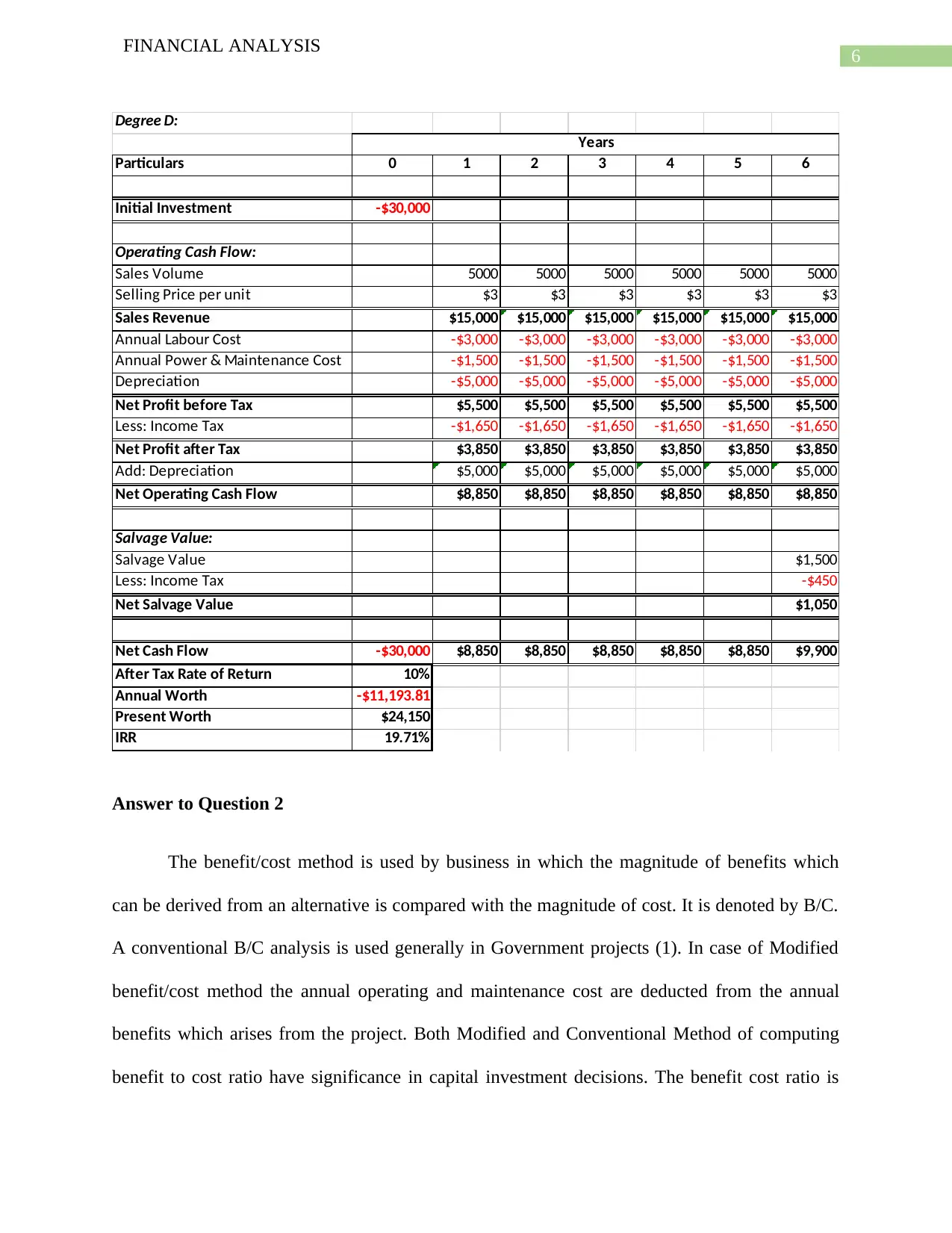

Degree D:

Particulars 0 1 2 3 4 5 6

Initial Investment -$30,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$3,000 -$3,000 -$3,000 -$3,000 -$3,000 -$3,000

Annual Power & Maintenance Cost -$1,500 -$1,500 -$1,500 -$1,500 -$1,500 -$1,500

Depreciation -$5,000 -$5,000 -$5,000 -$5,000 -$5,000 -$5,000

Net Profit before Tax $5,500 $5,500 $5,500 $5,500 $5,500 $5,500

Less: Income Tax -$1,650 -$1,650 -$1,650 -$1,650 -$1,650 -$1,650

Net Profit after Tax $3,850 $3,850 $3,850 $3,850 $3,850 $3,850

Add: Depreciation $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Net Operating Cash Flow $8,850 $8,850 $8,850 $8,850 $8,850 $8,850

Salvage Value:

Salvage Value $1,500

Less: Income Tax -$450

Net Salvage Value $1,050

Net Cash Flow -$30,000 $8,850 $8,850 $8,850 $8,850 $8,850 $9,900

After Tax Rate of Return 10%

Annual Worth -$11,193.81

Present Worth $24,150

IRR 19.71%

Years

Answer to Question 2

The benefit/cost method is used by business in which the magnitude of benefits which

can be derived from an alternative is compared with the magnitude of cost. It is denoted by B/C.

A conventional B/C analysis is used generally in Government projects (1). In case of Modified

benefit/cost method the annual operating and maintenance cost are deducted from the annual

benefits which arises from the project. Both Modified and Conventional Method of computing

benefit to cost ratio have significance in capital investment decisions. The benefit cost ratio is

FINANCIAL ANALYSIS

Degree D:

Particulars 0 1 2 3 4 5 6

Initial Investment -$30,000

Operating Cash Flow:

Sales Volume 5000 5000 5000 5000 5000 5000

Selling Price per unit $3 $3 $3 $3 $3 $3

Sales Revenue $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

Annual Labour Cost -$3,000 -$3,000 -$3,000 -$3,000 -$3,000 -$3,000

Annual Power & Maintenance Cost -$1,500 -$1,500 -$1,500 -$1,500 -$1,500 -$1,500

Depreciation -$5,000 -$5,000 -$5,000 -$5,000 -$5,000 -$5,000

Net Profit before Tax $5,500 $5,500 $5,500 $5,500 $5,500 $5,500

Less: Income Tax -$1,650 -$1,650 -$1,650 -$1,650 -$1,650 -$1,650

Net Profit after Tax $3,850 $3,850 $3,850 $3,850 $3,850 $3,850

Add: Depreciation $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Net Operating Cash Flow $8,850 $8,850 $8,850 $8,850 $8,850 $8,850

Salvage Value:

Salvage Value $1,500

Less: Income Tax -$450

Net Salvage Value $1,050

Net Cash Flow -$30,000 $8,850 $8,850 $8,850 $8,850 $8,850 $9,900

After Tax Rate of Return 10%

Annual Worth -$11,193.81

Present Worth $24,150

IRR 19.71%

Years

Answer to Question 2

The benefit/cost method is used by business in which the magnitude of benefits which

can be derived from an alternative is compared with the magnitude of cost. It is denoted by B/C.

A conventional B/C analysis is used generally in Government projects (1). In case of Modified

benefit/cost method the annual operating and maintenance cost are deducted from the annual

benefits which arises from the project. Both Modified and Conventional Method of computing

benefit to cost ratio have significance in capital investment decisions. The benefit cost ratio is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ANALYSIS

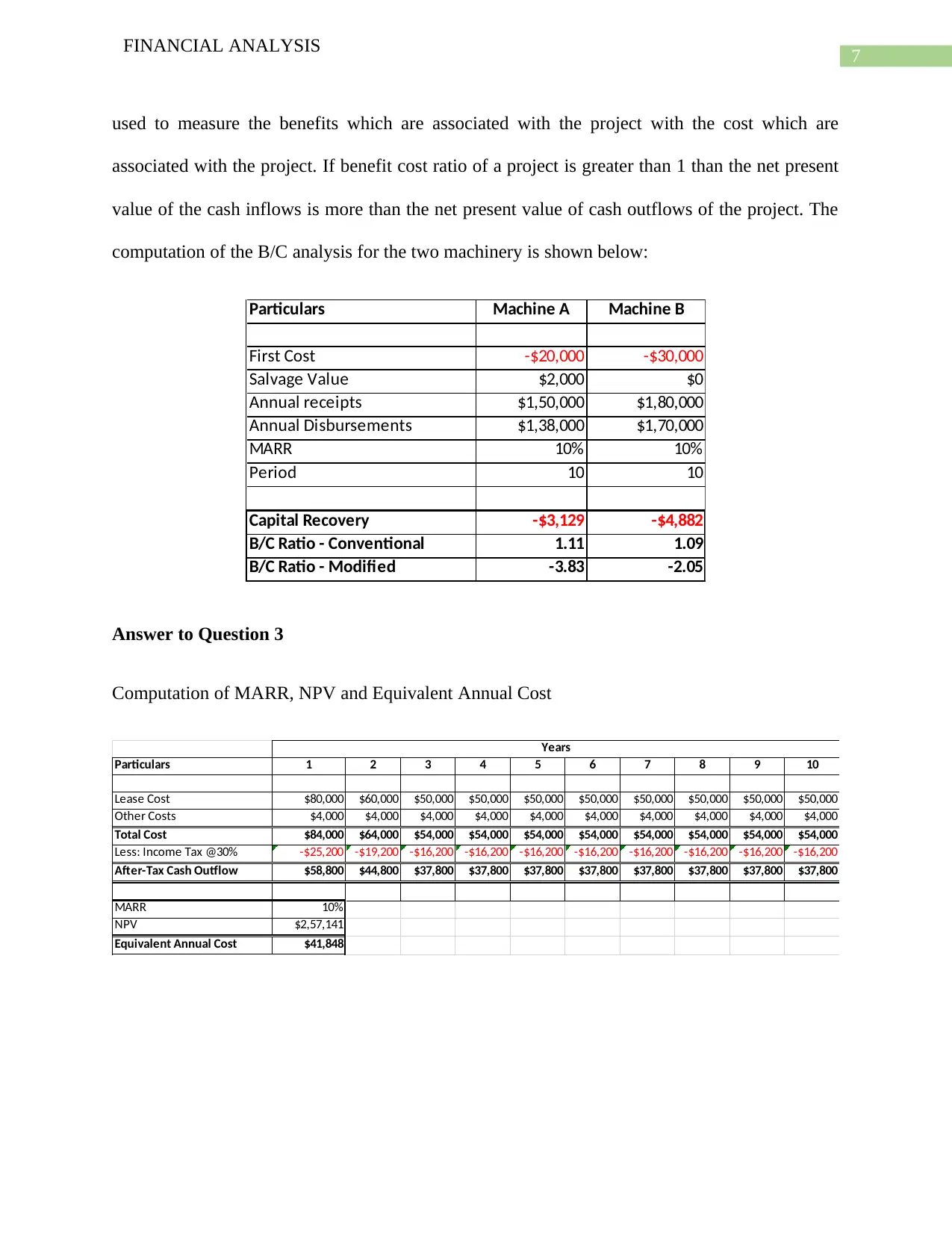

used to measure the benefits which are associated with the project with the cost which are

associated with the project. If benefit cost ratio of a project is greater than 1 than the net present

value of the cash inflows is more than the net present value of cash outflows of the project. The

computation of the B/C analysis for the two machinery is shown below:

Particulars Machine A Machine B

First Cost -$20,000 -$30,000

Salvage Value $2,000 $0

Annual receipts $1,50,000 $1,80,000

Annual Disbursements $1,38,000 $1,70,000

MARR 10% 10%

Period 10 10

Capital Recovery -$3,129 -$4,882

B/C Ratio - Conventional 1.11 1.09

B/C Ratio - Modified -3.83 -2.05

Answer to Question 3

Computation of MARR, NPV and Equivalent Annual Cost

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost $80,000 $60,000 $50,000 $50,000 $50,000 $50,000 $50,000 $50,000 $50,000 $50,000

Other Costs $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000

Total Cost $84,000 $64,000 $54,000 $54,000 $54,000 $54,000 $54,000 $54,000 $54,000 $54,000

Less: Income Tax @30% -$25,200 -$19,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200

After-Tax Cash Outflow $58,800 $44,800 $37,800 $37,800 $37,800 $37,800 $37,800 $37,800 $37,800 $37,800

MARR 10%

NPV $2,57,141

Equivalent Annual Cost $41,848

Years

FINANCIAL ANALYSIS

used to measure the benefits which are associated with the project with the cost which are

associated with the project. If benefit cost ratio of a project is greater than 1 than the net present

value of the cash inflows is more than the net present value of cash outflows of the project. The

computation of the B/C analysis for the two machinery is shown below:

Particulars Machine A Machine B

First Cost -$20,000 -$30,000

Salvage Value $2,000 $0

Annual receipts $1,50,000 $1,80,000

Annual Disbursements $1,38,000 $1,70,000

MARR 10% 10%

Period 10 10

Capital Recovery -$3,129 -$4,882

B/C Ratio - Conventional 1.11 1.09

B/C Ratio - Modified -3.83 -2.05

Answer to Question 3

Computation of MARR, NPV and Equivalent Annual Cost

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost $80,000 $60,000 $50,000 $50,000 $50,000 $50,000 $50,000 $50,000 $50,000 $50,000

Other Costs $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000

Total Cost $84,000 $64,000 $54,000 $54,000 $54,000 $54,000 $54,000 $54,000 $54,000 $54,000

Less: Income Tax @30% -$25,200 -$19,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200 -$16,200

After-Tax Cash Outflow $58,800 $44,800 $37,800 $37,800 $37,800 $37,800 $37,800 $37,800 $37,800 $37,800

MARR 10%

NPV $2,57,141

Equivalent Annual Cost $41,848

Years

8

FINANCIAL ANALYSIS

Answer to Question 4

Machine X:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Machine Cost -$20,000

Less: Trade-in- Allowance $0

Net Cost -$20,000

Annual Operating & Maintenance Cost -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000

Salvage Value $0

After-Tax Cash Outflow -$20,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000

MARR 10%

NPV -$5,20,919

Equivalent Annual Cost -$84,777

Years

Machine Y:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Machine Cost -$1,20,000

Less: Trade-in- Allowance $20,000

Net Cost -$1,00,000

Annual Operating & Maintenance Cost -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000

Salvage Value $30,000

After-Tax Cash Outflow -$1,00,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$40,000

MARR 10%

NPV -$4,71,412

Equivalent Annual Cost -$76,720

Years

Machine Z:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Machine Cost -$1,60,000

Less: Trade-in- Allowance $0

Net Cost -$1,60,000

Annual Operating & Maintenance Cost -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000

Salvage Value $50,000

After-Tax Cash Outflow -$1,60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$10,000

MARR 10%

NPV -$4,63,088

Equivalent Annual Cost -$75,365

Years

The above images show the calculations of NPV, MARR and Equivalent Annual Cost for

the three options of machine which the company has which are Machine X, Machine Y and

Machine Z. The NPV analysis of the three options are in negative which represents the costs of

the machine and analysis of such costs are based on such costs. The above calculations reveals

FINANCIAL ANALYSIS

Answer to Question 4

Machine X:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Machine Cost -$20,000

Less: Trade-in- Allowance $0

Net Cost -$20,000

Annual Operating & Maintenance Cost -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000

Salvage Value $0

After-Tax Cash Outflow -$20,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000 -$90,000

MARR 10%

NPV -$5,20,919

Equivalent Annual Cost -$84,777

Years

Machine Y:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Machine Cost -$1,20,000

Less: Trade-in- Allowance $20,000

Net Cost -$1,00,000

Annual Operating & Maintenance Cost -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000

Salvage Value $30,000

After-Tax Cash Outflow -$1,00,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$70,000 -$40,000

MARR 10%

NPV -$4,71,412

Equivalent Annual Cost -$76,720

Years

Machine Z:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Machine Cost -$1,60,000

Less: Trade-in- Allowance $0

Net Cost -$1,60,000

Annual Operating & Maintenance Cost -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000

Salvage Value $50,000

After-Tax Cash Outflow -$1,60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$60,000 -$10,000

MARR 10%

NPV -$4,63,088

Equivalent Annual Cost -$75,365

Years

The above images show the calculations of NPV, MARR and Equivalent Annual Cost for

the three options of machine which the company has which are Machine X, Machine Y and

Machine Z. The NPV analysis of the three options are in negative which represents the costs of

the machine and analysis of such costs are based on such costs. The above calculations reveals

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL ANALYSIS

that the Machine Z is the most favorable option which is available to the company as the NPV of

the cash outflows is lowest which is -$ 4,63,088.

Answer to Question 5

Introduction

The main purpose of this assignment is to analyze the projects selection process of ABC

ltd which is engaged in manufacturing activities. The company is planning to further expand the

business and thereby needs to invest in a machinery for which the management of the company

has options. For the purpose of selection of the options, the management will be applying capital

budgeting techniques which will be involving NPV analysis, payback period analysis,

profitability index analysis. The assignment also be commenting on the gaps which are there in

Life cycle costing technique and will also be recommending to ABC ltd as to how the business

can assess its risks better and improve the cost/benefit analysis of the business.

Gaps in Life Cycle Costing

Life cycle cost is a cost process which considers the actual cost and revenues which are

attributable to a product from the first use of the product till the product becomes obsolete. In

other words, life cycle cost technique follows the cost which are associated with the product over

the years or in other words over the life cycle of the project. the total cost of the product involves

all the costs which are costs which are related to planning, design, acquisition and support costs

and any other costs which are related to the product (5). Life cycle costing represents the total

cost of ownership in case of an asset and similarly will be including all the costs which will be

incurred over the life time of the asset. The method allows businesses to consider all the costs

which are incurred by the machinery for acquisition, maintenance, reimbursement or disposal

FINANCIAL ANALYSIS

that the Machine Z is the most favorable option which is available to the company as the NPV of

the cash outflows is lowest which is -$ 4,63,088.

Answer to Question 5

Introduction

The main purpose of this assignment is to analyze the projects selection process of ABC

ltd which is engaged in manufacturing activities. The company is planning to further expand the

business and thereby needs to invest in a machinery for which the management of the company

has options. For the purpose of selection of the options, the management will be applying capital

budgeting techniques which will be involving NPV analysis, payback period analysis,

profitability index analysis. The assignment also be commenting on the gaps which are there in

Life cycle costing technique and will also be recommending to ABC ltd as to how the business

can assess its risks better and improve the cost/benefit analysis of the business.

Gaps in Life Cycle Costing

Life cycle cost is a cost process which considers the actual cost and revenues which are

attributable to a product from the first use of the product till the product becomes obsolete. In

other words, life cycle cost technique follows the cost which are associated with the product over

the years or in other words over the life cycle of the project. the total cost of the product involves

all the costs which are costs which are related to planning, design, acquisition and support costs

and any other costs which are related to the product (5). Life cycle costing represents the total

cost of ownership in case of an asset and similarly will be including all the costs which will be

incurred over the life time of the asset. The method allows businesses to consider all the costs

which are incurred by the machinery for acquisition, maintenance, reimbursement or disposal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL ANALYSIS

when the business wants to take a decision. In other words, life cycle costing method for an asset

considers the full cost implication of the asset before taking any decisions. The basic difference

between traditional method of costing and life cycle costing lies in time period for which cost is

considered. In case of traditional system of costing, costs are considered on the basis of calendar

year whereas in life cycle costing method, the cost and revenues which are associated with the

asset or product is traced through several calendar year which shows that life cycle costing is a

longer process and is much more wide.

Thus, from the above discussions it is clear that life cycle costing approach is carried out

by business so as to get a clear picture of the long-term picture of the cost and revenues

associated with the project. The advantage of using this costing method is that it enhances

control of the business over manufacturing costs. In addition to this, it is essential because it

keeps a track and measure of the costs of the product or asset at different stages of life of the

asset. In the case of ABC ltd, the company wants to implement life cycle costing techniques for

the ascertain and monitoring the costs which are associated with asset over the useful life of the

asset (6). However, there are certain gaps which are present in the life cycle costing technique

which are mentioned below in points form:

1. The technique of product life cycle costing spreads the expense or cost related with the

asset over the useful life of the asset which might not be accurate as initial cost which are

incurred on the asset at beginning of its life might be less than what the expenses are

incurred on the asset towards the end of the useful life of the asset.

2. It is important to monitor the continuous performance of the asset after implementation of

life cycle costing techniques as if proper monitoring is not maintained than the costs

associated with the asset will become more than the benefits.

FINANCIAL ANALYSIS

when the business wants to take a decision. In other words, life cycle costing method for an asset

considers the full cost implication of the asset before taking any decisions. The basic difference

between traditional method of costing and life cycle costing lies in time period for which cost is

considered. In case of traditional system of costing, costs are considered on the basis of calendar

year whereas in life cycle costing method, the cost and revenues which are associated with the

asset or product is traced through several calendar year which shows that life cycle costing is a

longer process and is much more wide.

Thus, from the above discussions it is clear that life cycle costing approach is carried out

by business so as to get a clear picture of the long-term picture of the cost and revenues

associated with the project. The advantage of using this costing method is that it enhances

control of the business over manufacturing costs. In addition to this, it is essential because it

keeps a track and measure of the costs of the product or asset at different stages of life of the

asset. In the case of ABC ltd, the company wants to implement life cycle costing techniques for

the ascertain and monitoring the costs which are associated with asset over the useful life of the

asset (6). However, there are certain gaps which are present in the life cycle costing technique

which are mentioned below in points form:

1. The technique of product life cycle costing spreads the expense or cost related with the

asset over the useful life of the asset which might not be accurate as initial cost which are

incurred on the asset at beginning of its life might be less than what the expenses are

incurred on the asset towards the end of the useful life of the asset.

2. It is important to monitor the continuous performance of the asset after implementation of

life cycle costing techniques as if proper monitoring is not maintained than the costs

associated with the asset will become more than the benefits.

11

FINANCIAL ANALYSIS

3. In case a business takes loan for purchase of asset and as per life cycle costing the loan

amount will be repaid over the useful life of the asset which means the company would

have to bear interest charges over the useful life of the asset which might not be a good

option.

4. The technique of life cycle costing assumes that the performance of the assets which is in

the initial years will not be same as the performance of the asset in the later years of the

useful life of the asset. This concept is not appropriate as such might not be the case and

therefore the costs assumption of the business might not be realistic

The above mention points are the various limitation or gaps which the techniques Life cycle

costing faces in comparison to traditional and other costing techniques.

Recommendations

The recommendations which can be given to the company for improving benefit/cost

analysis and risks of the business are given below:

1. The business needs to implement a proper capital structure so as to reduce the cost of

capital which signifies risks which are associated with the capital structure of the

business. The business needs to incorporate debt capital and equity capital in the capital

mix so as to attain a favorable balance in the capital structure.

2. The management of the company needs to conduct NPV analysis so as to ensure that the

assets which the management of the company intends to invest on has benefits which

exceeds the cost which is related to the asset. The management of the company

FINANCIAL ANALYSIS

3. In case a business takes loan for purchase of asset and as per life cycle costing the loan

amount will be repaid over the useful life of the asset which means the company would

have to bear interest charges over the useful life of the asset which might not be a good

option.

4. The technique of life cycle costing assumes that the performance of the assets which is in

the initial years will not be same as the performance of the asset in the later years of the

useful life of the asset. This concept is not appropriate as such might not be the case and

therefore the costs assumption of the business might not be realistic

The above mention points are the various limitation or gaps which the techniques Life cycle

costing faces in comparison to traditional and other costing techniques.

Recommendations

The recommendations which can be given to the company for improving benefit/cost

analysis and risks of the business are given below:

1. The business needs to implement a proper capital structure so as to reduce the cost of

capital which signifies risks which are associated with the capital structure of the

business. The business needs to incorporate debt capital and equity capital in the capital

mix so as to attain a favorable balance in the capital structure.

2. The management of the company needs to conduct NPV analysis so as to ensure that the

assets which the management of the company intends to invest on has benefits which

exceeds the cost which is related to the asset. The management of the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.