Accounting for Decision Making: Comparative Financial Analysis Report

VerifiedAdded on 2022/11/22

|24

|3018

|323

Report

AI Summary

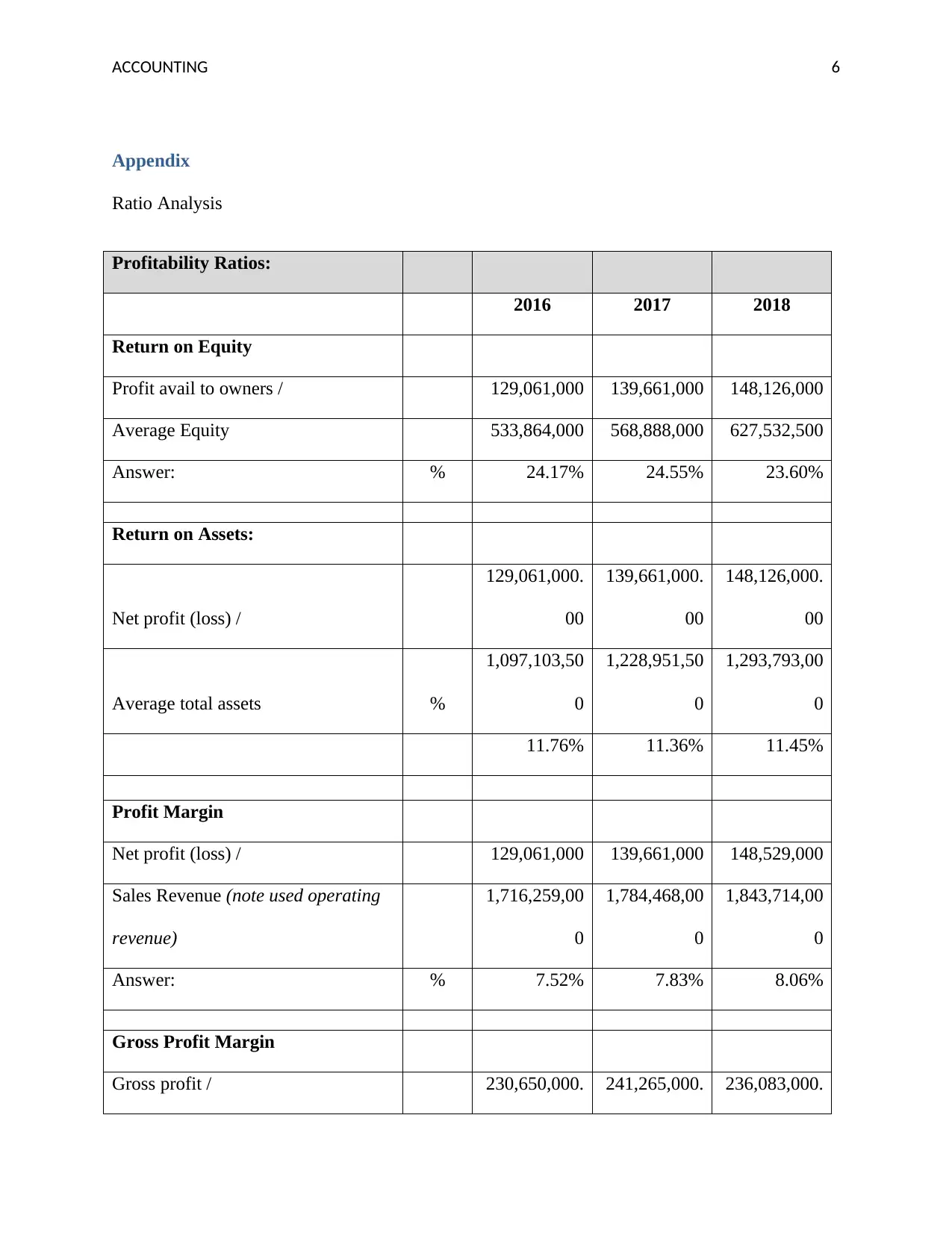

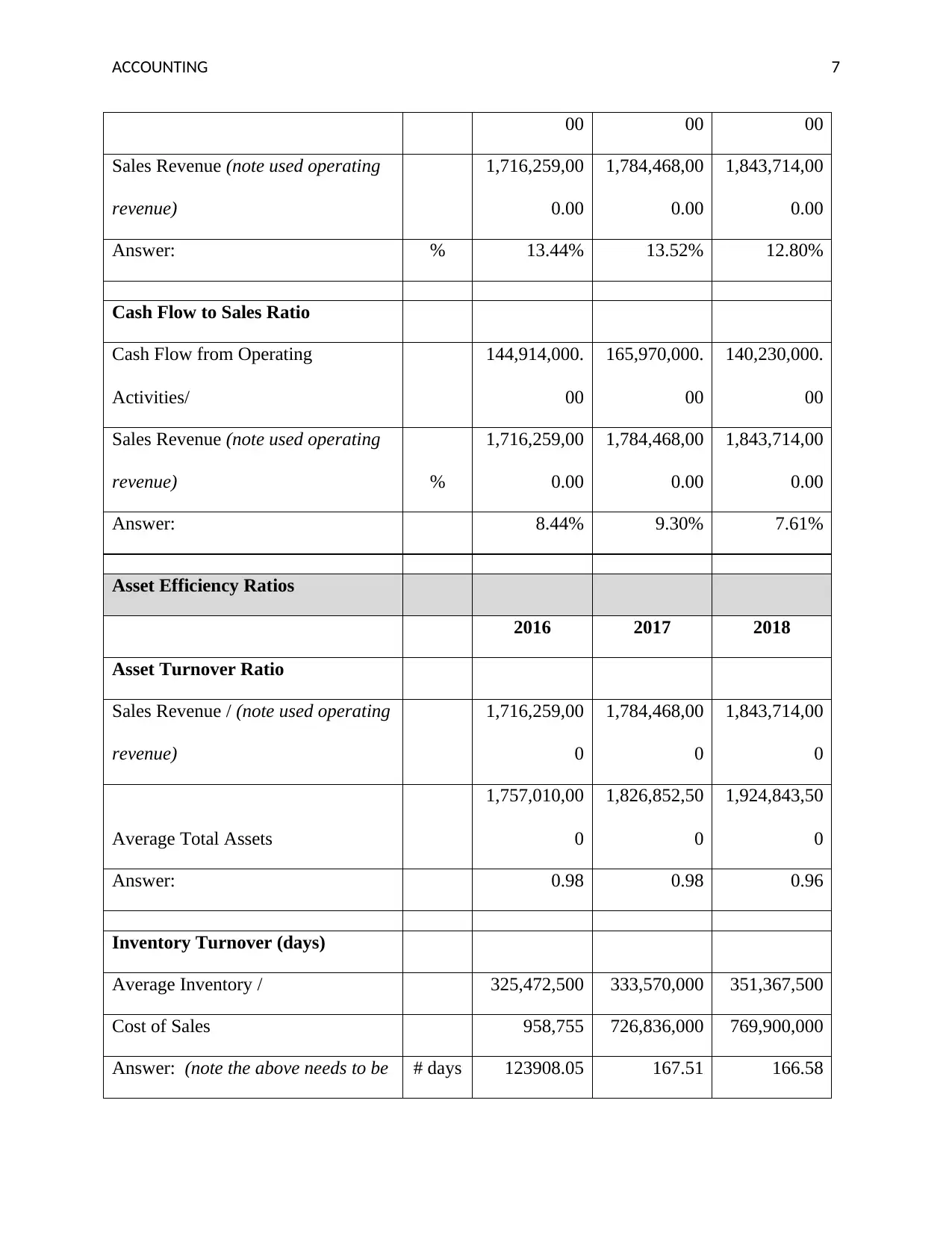

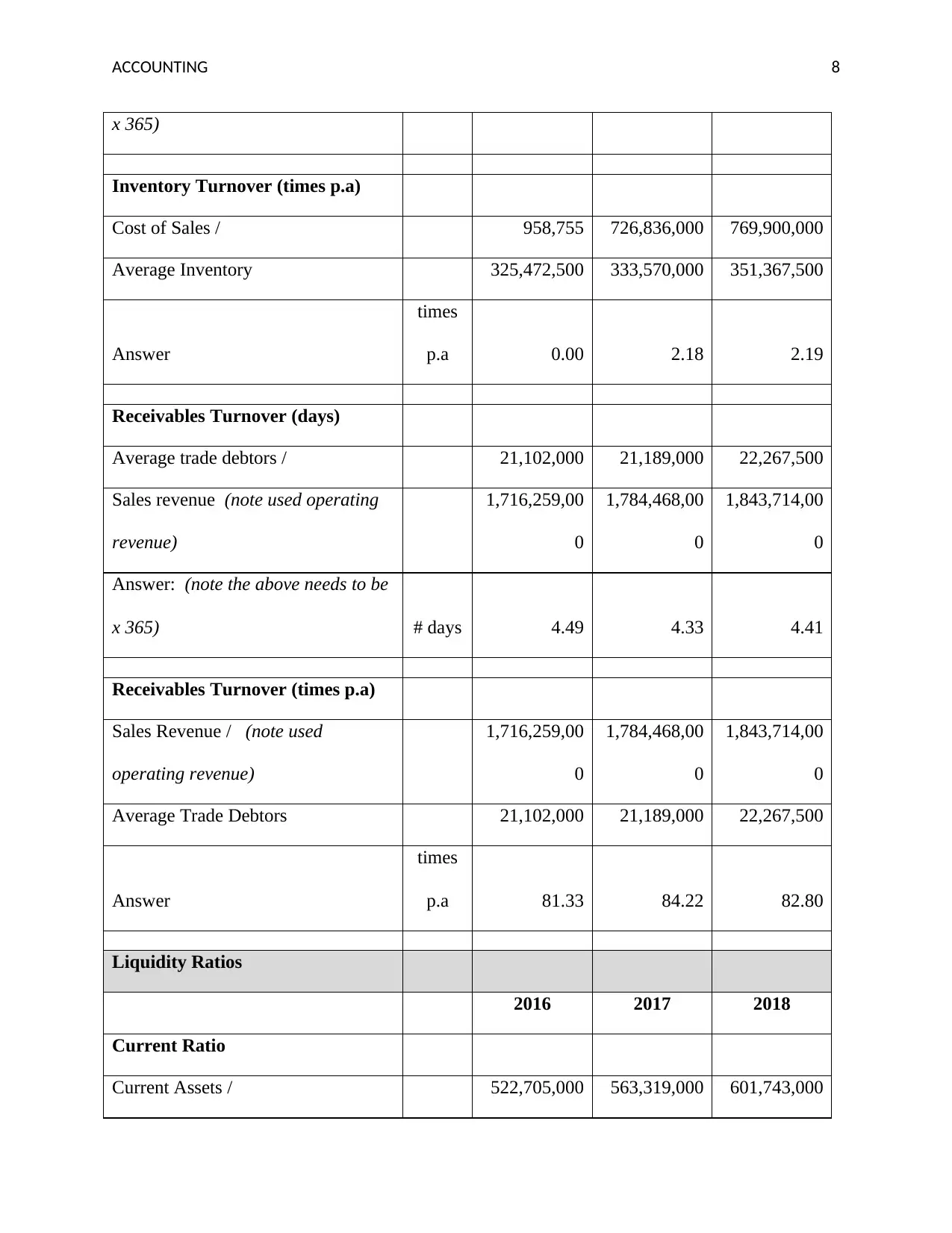

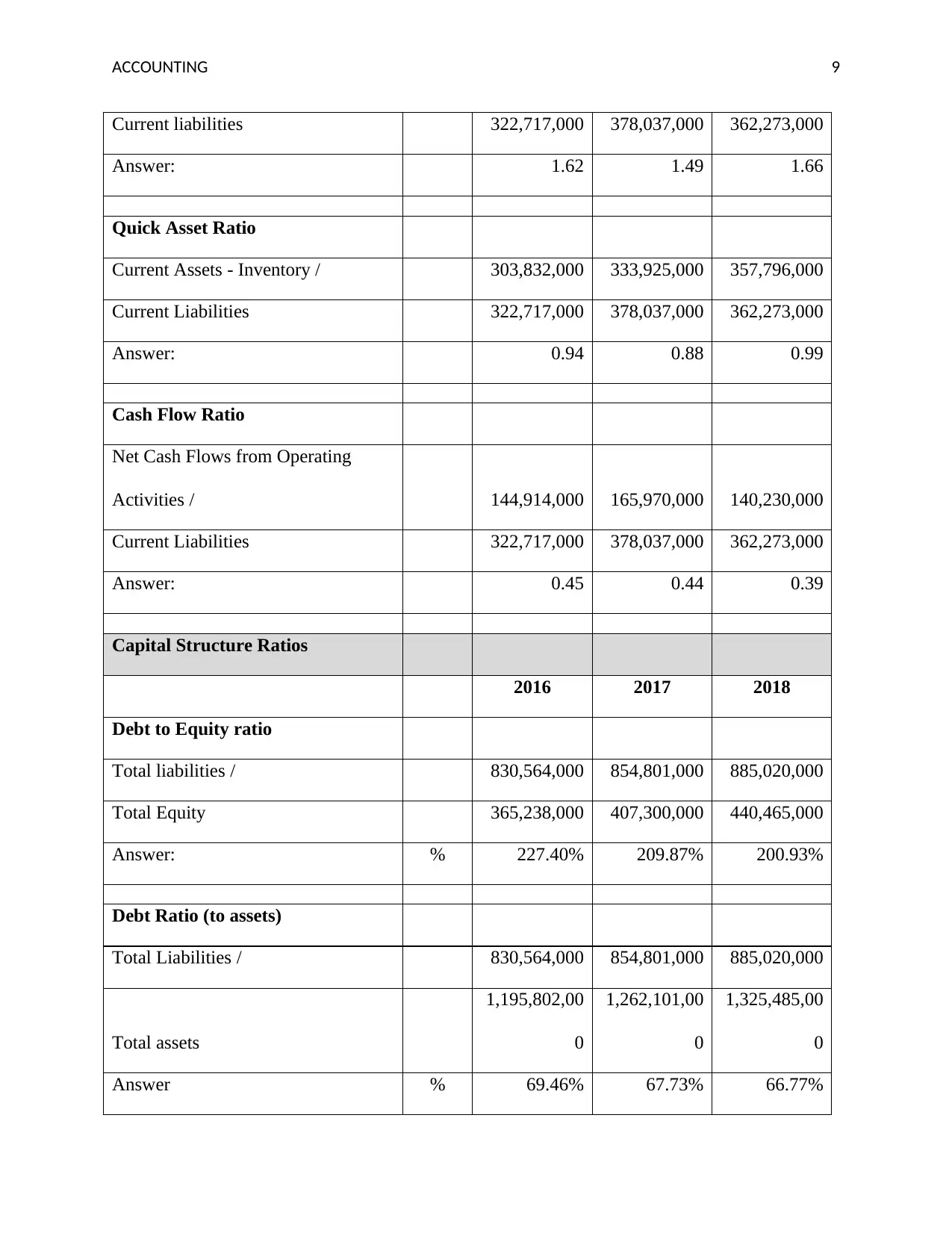

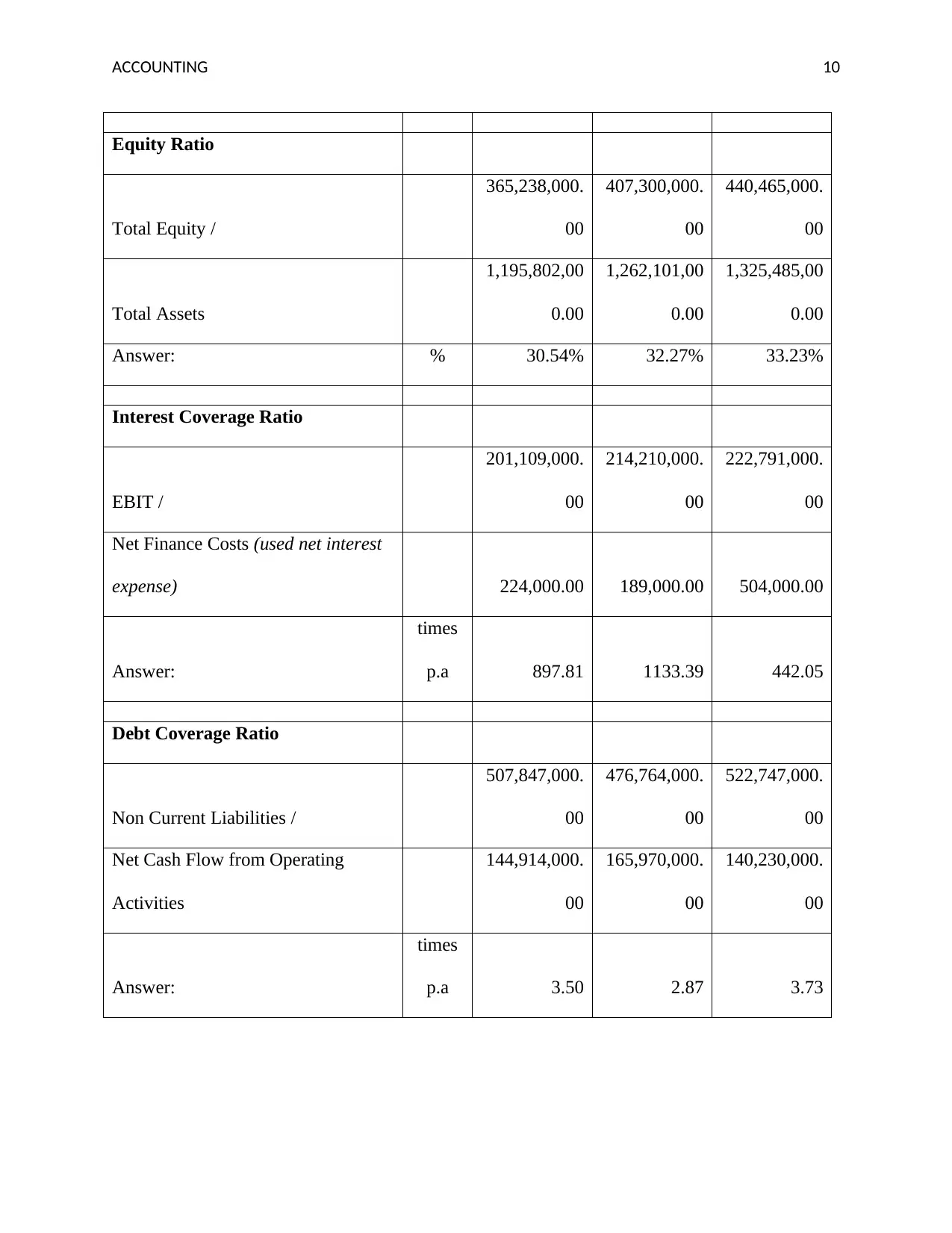

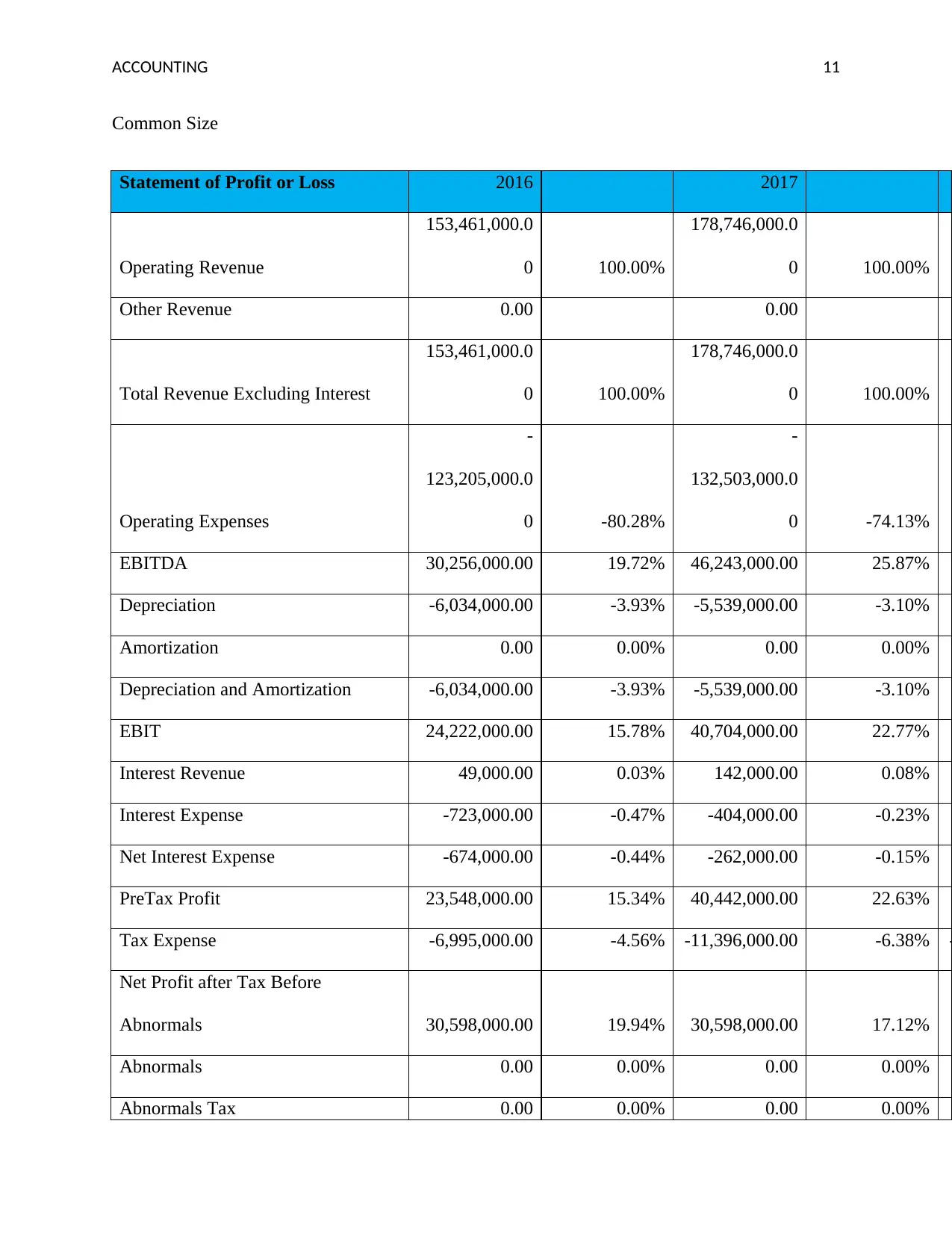

This report presents a comparative financial analysis of Dulux Group Limited and Lovisa Holdings Limited, focusing on their financial performance. The analysis includes a detailed examination of profitability ratios (Return on Equity, Return on Assets, Profit Margin, Gross Profit Margin, Cash Flow to Sales Ratio), asset efficiency ratios (Asset Turnover Ratio, Inventory Turnover, Receivables Turnover), liquidity ratios (Current Ratio, Quick Asset Ratio, Cash Flow Ratio), and capital structure ratios (Debt to Equity ratio, Debt Ratio, Equity Ratio, Interest Coverage Ratio). The study evaluates the companies' financial positions, highlighting trends and limitations, and provides recommendations based on the findings. The report utilizes data from the years 2016, 2017, and 2018 to conduct its comparative analysis and offers insights into the companies' strengths and areas for improvement.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.