Corporate Accounting Report: Financial Analysis of QEM and South32

VerifiedAdded on 2022/11/23

|15

|3479

|124

Report

AI Summary

This report presents a detailed analysis of corporate accounting practices, focusing on the financial performance of two companies: QEM Limited and South32. The analysis is based on the companies' annual reports, examining equity components, liabilities, and their changes over three financial years (2016, 2017, and 2018). The report investigates how these companies comply with laws and regulations. It further explores the advantages and disadvantages of different sources of finance, such as debt and equity, and their impact on organizational growth and financial stability. The study aims to assess the financial health and strategies of the selected companies, offering insights into their equity, liabilities, and overall financial positions, comparing QEM and South32.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

The report brings out an evaluation with the help of analysing two financial years for two

major companies named as QEM limited and South32. The report has used the annual reports

for the analysis to evaluate the equity, its elements, liabilities and its elements. The report has

analysed how compliance to laws and regulations differs from small proprietary

organisations, large proprietary organisations to the disclosing companies. Further, the report

determines the change in the items of equity and liability in the three financial years 2016,

2017, and 2018. Further, there is a discussion on. How effectively an organisation raise and

decide its source of finance.

The report brings out an evaluation with the help of analysing two financial years for two

major companies named as QEM limited and South32. The report has used the annual reports

for the analysis to evaluate the equity, its elements, liabilities and its elements. The report has

analysed how compliance to laws and regulations differs from small proprietary

organisations, large proprietary organisations to the disclosing companies. Further, the report

determines the change in the items of equity and liability in the three financial years 2016,

2017, and 2018. Further, there is a discussion on. How effectively an organisation raise and

decide its source of finance.

Contents

Introduction................................................................................................................................3

Part-A.........................................................................................................................................3

Part-B.......................................................................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................13

Introduction................................................................................................................................3

Part-A.........................................................................................................................................3

Part-B.......................................................................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

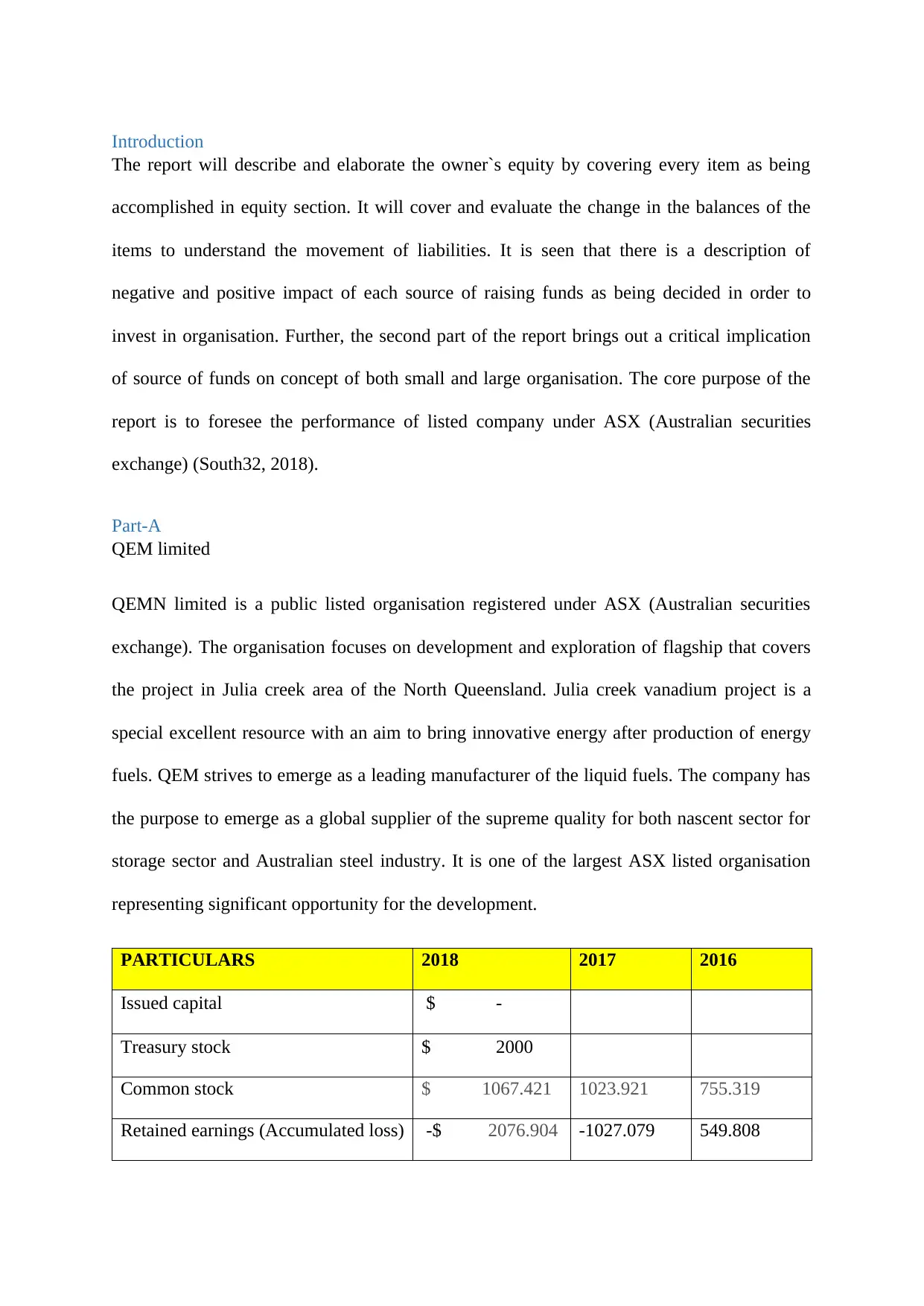

Introduction

The report will describe and elaborate the owner`s equity by covering every item as being

accomplished in equity section. It will cover and evaluate the change in the balances of the

items to understand the movement of liabilities. It is seen that there is a description of

negative and positive impact of each source of raising funds as being decided in order to

invest in organisation. Further, the second part of the report brings out a critical implication

of source of funds on concept of both small and large organisation. The core purpose of the

report is to foresee the performance of listed company under ASX (Australian securities

exchange) (South32, 2018).

Part-A

QEM limited

QEMN limited is a public listed organisation registered under ASX (Australian securities

exchange). The organisation focuses on development and exploration of flagship that covers

the project in Julia creek area of the North Queensland. Julia creek vanadium project is a

special excellent resource with an aim to bring innovative energy after production of energy

fuels. QEM strives to emerge as a leading manufacturer of the liquid fuels. The company has

the purpose to emerge as a global supplier of the supreme quality for both nascent sector for

storage sector and Australian steel industry. It is one of the largest ASX listed organisation

representing significant opportunity for the development.

PARTICULARS 2018 2017 2016

Issued capital $ -

Treasury stock $ 2000

Common stock $ 1067.421 1023.921 755.319

Retained earnings (Accumulated loss) -$ 2076.904 -1027.079 549.808

The report will describe and elaborate the owner`s equity by covering every item as being

accomplished in equity section. It will cover and evaluate the change in the balances of the

items to understand the movement of liabilities. It is seen that there is a description of

negative and positive impact of each source of raising funds as being decided in order to

invest in organisation. Further, the second part of the report brings out a critical implication

of source of funds on concept of both small and large organisation. The core purpose of the

report is to foresee the performance of listed company under ASX (Australian securities

exchange) (South32, 2018).

Part-A

QEM limited

QEMN limited is a public listed organisation registered under ASX (Australian securities

exchange). The organisation focuses on development and exploration of flagship that covers

the project in Julia creek area of the North Queensland. Julia creek vanadium project is a

special excellent resource with an aim to bring innovative energy after production of energy

fuels. QEM strives to emerge as a leading manufacturer of the liquid fuels. The company has

the purpose to emerge as a global supplier of the supreme quality for both nascent sector for

storage sector and Australian steel industry. It is one of the largest ASX listed organisation

representing significant opportunity for the development.

PARTICULARS 2018 2017 2016

Issued capital $ -

Treasury stock $ 2000

Common stock $ 1067.421 1023.921 755.319

Retained earnings (Accumulated loss) -$ 2076.904 -1027.079 549.808

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

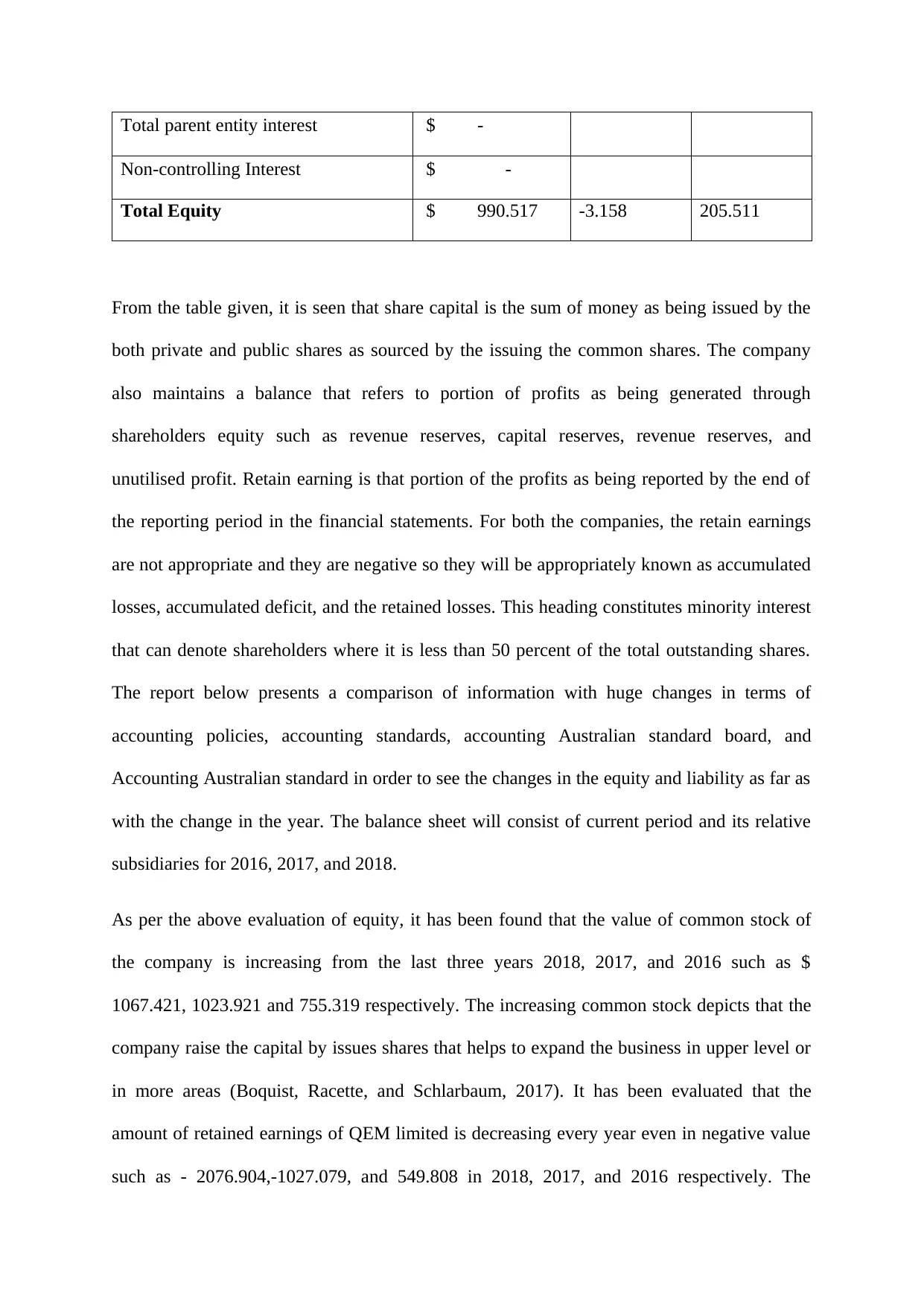

Total parent entity interest $ -

Non-controlling Interest $ -

Total Equity $ 990.517 -3.158 205.511

From the table given, it is seen that share capital is the sum of money as being issued by the

both private and public shares as sourced by the issuing the common shares. The company

also maintains a balance that refers to portion of profits as being generated through

shareholders equity such as revenue reserves, capital reserves, revenue reserves, and

unutilised profit. Retain earning is that portion of the profits as being reported by the end of

the reporting period in the financial statements. For both the companies, the retain earnings

are not appropriate and they are negative so they will be appropriately known as accumulated

losses, accumulated deficit, and the retained losses. This heading constitutes minority interest

that can denote shareholders where it is less than 50 percent of the total outstanding shares.

The report below presents a comparison of information with huge changes in terms of

accounting policies, accounting standards, accounting Australian standard board, and

Accounting Australian standard in order to see the changes in the equity and liability as far as

with the change in the year. The balance sheet will consist of current period and its relative

subsidiaries for 2016, 2017, and 2018.

As per the above evaluation of equity, it has been found that the value of common stock of

the company is increasing from the last three years 2018, 2017, and 2016 such as $

1067.421, 1023.921 and 755.319 respectively. The increasing common stock depicts that the

company raise the capital by issues shares that helps to expand the business in upper level or

in more areas (Boquist, Racette, and Schlarbaum, 2017). It has been evaluated that the

amount of retained earnings of QEM limited is decreasing every year even in negative value

such as - 2076.904,-1027.079, and 549.808 in 2018, 2017, and 2016 respectively. The

Non-controlling Interest $ -

Total Equity $ 990.517 -3.158 205.511

From the table given, it is seen that share capital is the sum of money as being issued by the

both private and public shares as sourced by the issuing the common shares. The company

also maintains a balance that refers to portion of profits as being generated through

shareholders equity such as revenue reserves, capital reserves, revenue reserves, and

unutilised profit. Retain earning is that portion of the profits as being reported by the end of

the reporting period in the financial statements. For both the companies, the retain earnings

are not appropriate and they are negative so they will be appropriately known as accumulated

losses, accumulated deficit, and the retained losses. This heading constitutes minority interest

that can denote shareholders where it is less than 50 percent of the total outstanding shares.

The report below presents a comparison of information with huge changes in terms of

accounting policies, accounting standards, accounting Australian standard board, and

Accounting Australian standard in order to see the changes in the equity and liability as far as

with the change in the year. The balance sheet will consist of current period and its relative

subsidiaries for 2016, 2017, and 2018.

As per the above evaluation of equity, it has been found that the value of common stock of

the company is increasing from the last three years 2018, 2017, and 2016 such as $

1067.421, 1023.921 and 755.319 respectively. The increasing common stock depicts that the

company raise the capital by issues shares that helps to expand the business in upper level or

in more areas (Boquist, Racette, and Schlarbaum, 2017). It has been evaluated that the

amount of retained earnings of QEM limited is decreasing every year even in negative value

such as - 2076.904,-1027.079, and 549.808 in 2018, 2017, and 2016 respectively. The

decreasing amount of retained earning depicts that the company decided to pay to its dividend

to the shareholders. The amount of total equity is increasing in the year 2018, which indicates

the positive sign for the company as it raises the capital from equity (Hasan, Hossain, and

Habib, 2015).

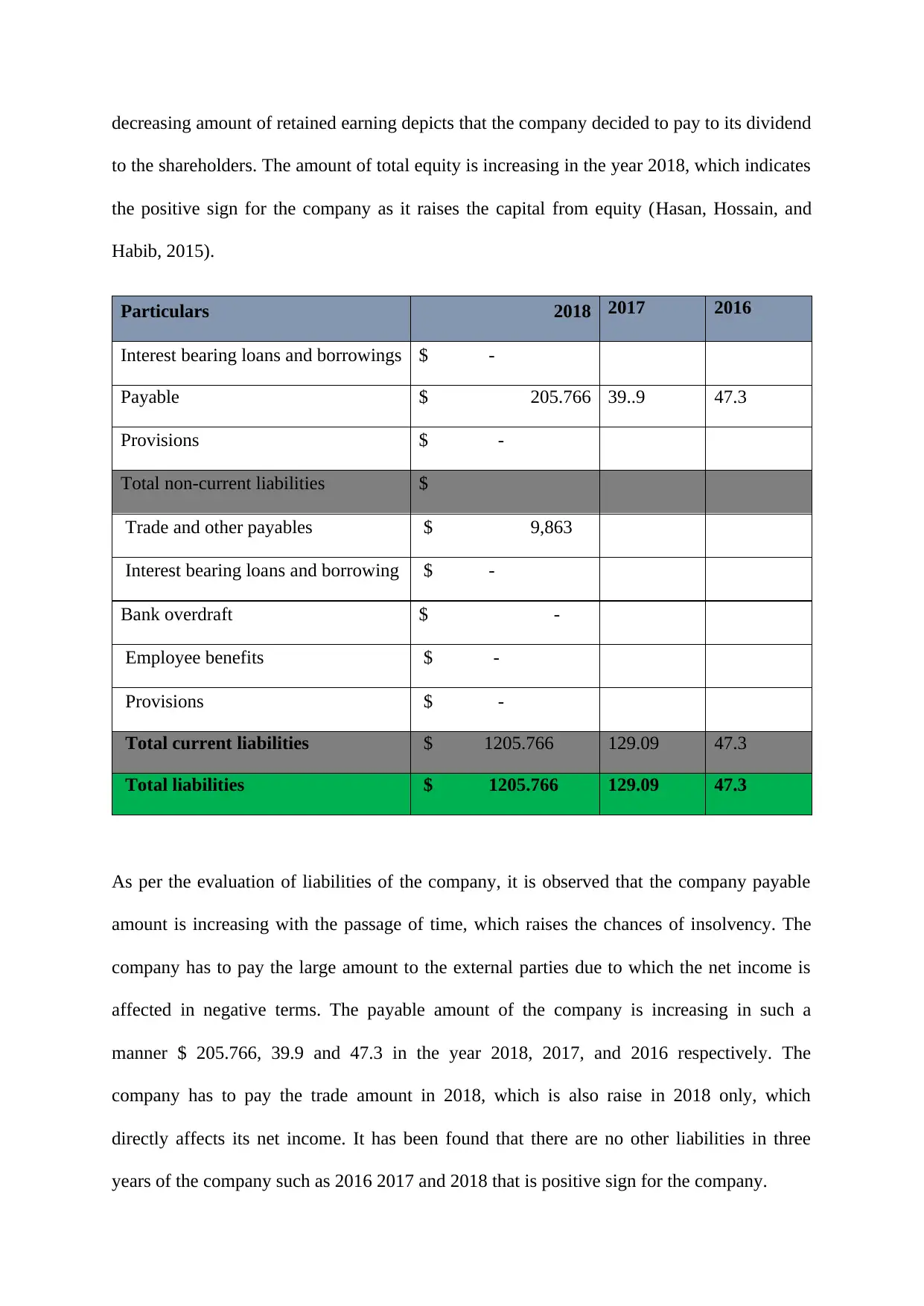

Particulars 2018 2017 2016

Interest bearing loans and borrowings $ -

Payable $ 205.766 39..9 47.3

Provisions $ -

Total non-current liabilities $

Trade and other payables $ 9,863

Interest bearing loans and borrowing $ -

Bank overdraft $ -

Employee benefits $ -

Provisions $ -

Total current liabilities $ 1205.766 129.09 47.3

Total liabilities $ 1205.766 129.09 47.3

As per the evaluation of liabilities of the company, it is observed that the company payable

amount is increasing with the passage of time, which raises the chances of insolvency. The

company has to pay the large amount to the external parties due to which the net income is

affected in negative terms. The payable amount of the company is increasing in such a

manner $ 205.766, 39.9 and 47.3 in the year 2018, 2017, and 2016 respectively. The

company has to pay the trade amount in 2018, which is also raise in 2018 only, which

directly affects its net income. It has been found that there are no other liabilities in three

years of the company such as 2016 2017 and 2018 that is positive sign for the company.

to the shareholders. The amount of total equity is increasing in the year 2018, which indicates

the positive sign for the company as it raises the capital from equity (Hasan, Hossain, and

Habib, 2015).

Particulars 2018 2017 2016

Interest bearing loans and borrowings $ -

Payable $ 205.766 39..9 47.3

Provisions $ -

Total non-current liabilities $

Trade and other payables $ 9,863

Interest bearing loans and borrowing $ -

Bank overdraft $ -

Employee benefits $ -

Provisions $ -

Total current liabilities $ 1205.766 129.09 47.3

Total liabilities $ 1205.766 129.09 47.3

As per the evaluation of liabilities of the company, it is observed that the company payable

amount is increasing with the passage of time, which raises the chances of insolvency. The

company has to pay the large amount to the external parties due to which the net income is

affected in negative terms. The payable amount of the company is increasing in such a

manner $ 205.766, 39.9 and 47.3 in the year 2018, 2017, and 2016 respectively. The

company has to pay the trade amount in 2018, which is also raise in 2018 only, which

directly affects its net income. It has been found that there are no other liabilities in three

years of the company such as 2016 2017 and 2018 that is positive sign for the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

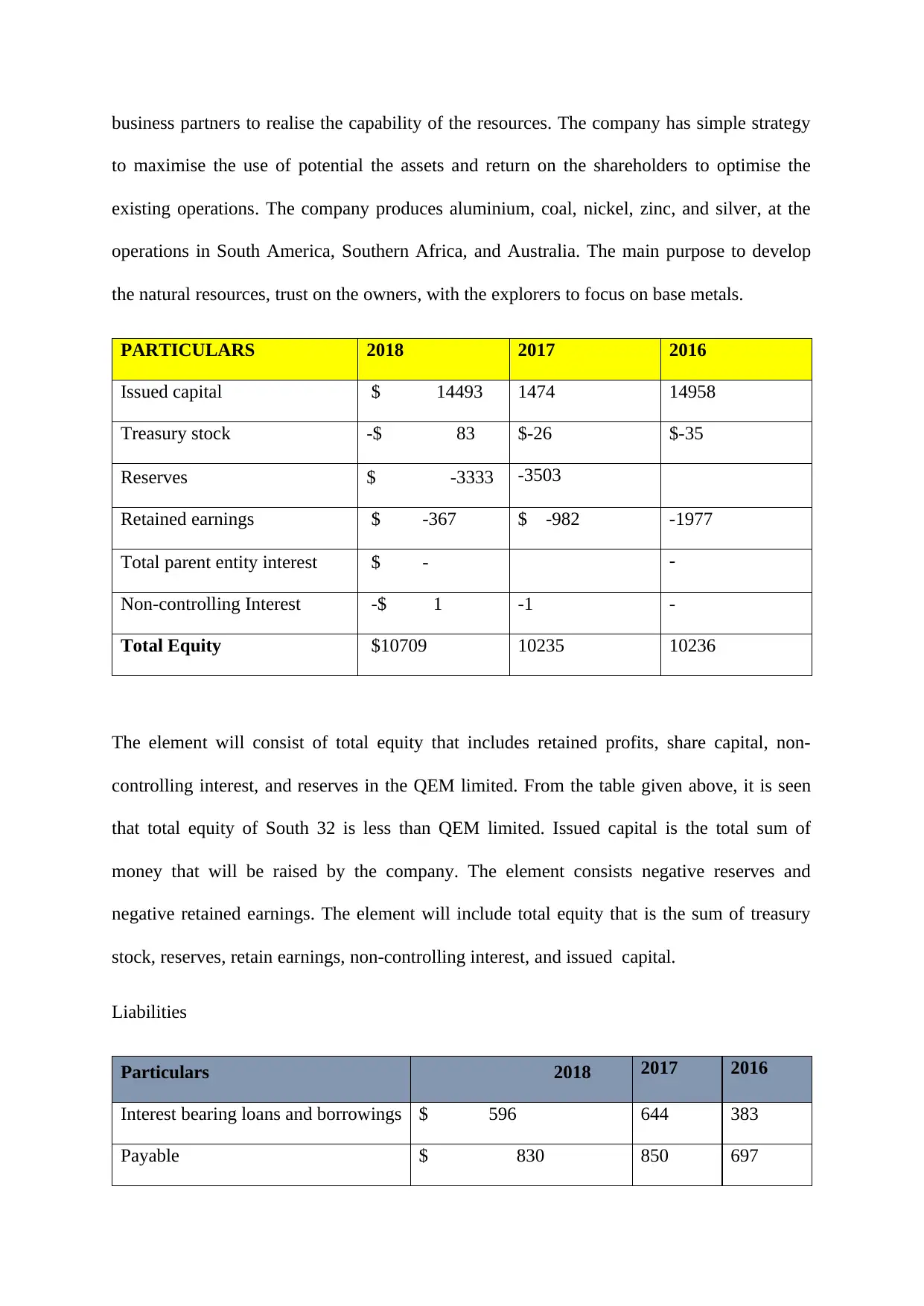

South 32

South 32 is an internationally diversified metal and mining organisation with premium

quality operations in South America, Southern Africa, and Australia. The main purpose of the

company is to make huge difference to develop natural resources, improvements in people`s

lives and especially for the generations to come. The company trust the owners and the

business partners to realise the capability of the resources. The company has simple strategy

to maximise the use of potential the assets and return on the shareholders to optimise the

existing operations. The company produces aluminium, coal, nickel, zinc, and silver, at the

operations in South America, Southern Africa, and Australia. The main purpose to develop

the natural resources, trust on the owners, with the explorers to focus on base metals

(South32, 2018).

The element will consist of total equity that includes retained profits, share capital, non-

controlling interest, and reserves in the QEM limited. It has been found that the total equity of

South 32 is increasing which indicates that the company raise the capital by issuing the shares

instead of liabilities (South32, 2018). The amount of retained earnings of the company is

declining every year with the negative amount, which indicates that the company pays the

dividend amount to its shareholders and the others payments are also increasing that the

organization has to pay (Geddes, 2017). The amount of retained earnings was declined in

such a manner $ -367, -98, -1977 in 2018, 2017, and 2016 respectively. It depicts that the

payments is reduces but still it face the issues in the coming future due to financial crisis

(Hau, and Lai, 2016).

By the evaluation of liabilities of South 32, It is observed that the non-current liabilities of the

company is huge in the year 2017 but it is decreasing in the year 2018 as the company raise

the capital by raising shares instead of borrowing money on liabilities. In the evaluation of

South 32 is an internationally diversified metal and mining organisation with premium

quality operations in South America, Southern Africa, and Australia. The main purpose of the

company is to make huge difference to develop natural resources, improvements in people`s

lives and especially for the generations to come. The company trust the owners and the

business partners to realise the capability of the resources. The company has simple strategy

to maximise the use of potential the assets and return on the shareholders to optimise the

existing operations. The company produces aluminium, coal, nickel, zinc, and silver, at the

operations in South America, Southern Africa, and Australia. The main purpose to develop

the natural resources, trust on the owners, with the explorers to focus on base metals

(South32, 2018).

The element will consist of total equity that includes retained profits, share capital, non-

controlling interest, and reserves in the QEM limited. It has been found that the total equity of

South 32 is increasing which indicates that the company raise the capital by issuing the shares

instead of liabilities (South32, 2018). The amount of retained earnings of the company is

declining every year with the negative amount, which indicates that the company pays the

dividend amount to its shareholders and the others payments are also increasing that the

organization has to pay (Geddes, 2017). The amount of retained earnings was declined in

such a manner $ -367, -98, -1977 in 2018, 2017, and 2016 respectively. It depicts that the

payments is reduces but still it face the issues in the coming future due to financial crisis

(Hau, and Lai, 2016).

By the evaluation of liabilities of South 32, It is observed that the non-current liabilities of the

company is huge in the year 2017 but it is decreasing in the year 2018 as the company raise

the capital by raising shares instead of borrowing money on liabilities. In the evaluation of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

total liabilities, it has been analysed that the amount of trade payable is decreasing in the year

2018 with the huge percentage which is beneficial for the company. In the year 2016, 2017,

and 2018, the amount of trade payable is $135, 850 and 697 respectively. The amount of total

liabilities is also decreasing in the year 2018 due to decreasing its whole liabilities which is

positive factor for the company (Johnston, 2018). The company create the provision account

in the year 2018 as it receivable ratio is increasing due to which it is in doubt for some

debtors that they does not provide money to them.

As per the above analysis of both the companies, it is observed that the financial position of

South 32 is improving as compare to QEM Limited. It has been found that the South 32 has

less liability as compare to South 32. But as per the comparison of both the companies, QEM

has fewer amounts of total liabilities as compare to South 32. From the table given above, it

is seen that total equity of South 32 is less than QEM limited. Issued capital is the total sum

of money that will be raised by the company.

The liabilities section evaluates items of section through two parts named as total current

liabilities and noncurrent liabilities. The company only owns payables as their non-current

liabilities and trade and other payables as their current liabilities. Current liabilities are the

liabilities that will be paid in the duration of nearly 1 year. Non-current liabilities have the

elements that cannot be paid in less than one year. The company has no loan obligations, as

its operations are not being extended much.

South 32

South 32 is an internationally diversified metal and mining organisation with premium

quality operations in South America, Southern Africa, and Australia. The main purpose of the

company is to make huge difference to develop natural resources, improvements in people`s

lives and especially for the generations to come. The company trust the owners and the

2018 with the huge percentage which is beneficial for the company. In the year 2016, 2017,

and 2018, the amount of trade payable is $135, 850 and 697 respectively. The amount of total

liabilities is also decreasing in the year 2018 due to decreasing its whole liabilities which is

positive factor for the company (Johnston, 2018). The company create the provision account

in the year 2018 as it receivable ratio is increasing due to which it is in doubt for some

debtors that they does not provide money to them.

As per the above analysis of both the companies, it is observed that the financial position of

South 32 is improving as compare to QEM Limited. It has been found that the South 32 has

less liability as compare to South 32. But as per the comparison of both the companies, QEM

has fewer amounts of total liabilities as compare to South 32. From the table given above, it

is seen that total equity of South 32 is less than QEM limited. Issued capital is the total sum

of money that will be raised by the company.

The liabilities section evaluates items of section through two parts named as total current

liabilities and noncurrent liabilities. The company only owns payables as their non-current

liabilities and trade and other payables as their current liabilities. Current liabilities are the

liabilities that will be paid in the duration of nearly 1 year. Non-current liabilities have the

elements that cannot be paid in less than one year. The company has no loan obligations, as

its operations are not being extended much.

South 32

South 32 is an internationally diversified metal and mining organisation with premium

quality operations in South America, Southern Africa, and Australia. The main purpose of the

company is to make huge difference to develop natural resources, improvements in people`s

lives and especially for the generations to come. The company trust the owners and the

business partners to realise the capability of the resources. The company has simple strategy

to maximise the use of potential the assets and return on the shareholders to optimise the

existing operations. The company produces aluminium, coal, nickel, zinc, and silver, at the

operations in South America, Southern Africa, and Australia. The main purpose to develop

the natural resources, trust on the owners, with the explorers to focus on base metals.

PARTICULARS 2018 2017 2016

Issued capital $ 14493 1474 14958

Treasury stock -$ 83 $-26 $-35

Reserves $ -3333 -3503

Retained earnings $ -367 $ -982 -1977

Total parent entity interest $ - -

Non-controlling Interest -$ 1 -1 -

Total Equity $10709 10235 10236

The element will consist of total equity that includes retained profits, share capital, non-

controlling interest, and reserves in the QEM limited. From the table given above, it is seen

that total equity of South 32 is less than QEM limited. Issued capital is the total sum of

money that will be raised by the company. The element consists negative reserves and

negative retained earnings. The element will include total equity that is the sum of treasury

stock, reserves, retain earnings, non-controlling interest, and issued capital.

Liabilities

Particulars 2018 2017 2016

Interest bearing loans and borrowings $ 596 644 383

Payable $ 830 850 697

to maximise the use of potential the assets and return on the shareholders to optimise the

existing operations. The company produces aluminium, coal, nickel, zinc, and silver, at the

operations in South America, Southern Africa, and Australia. The main purpose to develop

the natural resources, trust on the owners, with the explorers to focus on base metals.

PARTICULARS 2018 2017 2016

Issued capital $ 14493 1474 14958

Treasury stock -$ 83 $-26 $-35

Reserves $ -3333 -3503

Retained earnings $ -367 $ -982 -1977

Total parent entity interest $ - -

Non-controlling Interest -$ 1 -1 -

Total Equity $10709 10235 10236

The element will consist of total equity that includes retained profits, share capital, non-

controlling interest, and reserves in the QEM limited. From the table given above, it is seen

that total equity of South 32 is less than QEM limited. Issued capital is the total sum of

money that will be raised by the company. The element consists negative reserves and

negative retained earnings. The element will include total equity that is the sum of treasury

stock, reserves, retain earnings, non-controlling interest, and issued capital.

Liabilities

Particulars 2018 2017 2016

Interest bearing loans and borrowings $ 596 644 383

Payable $ 830 850 697

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

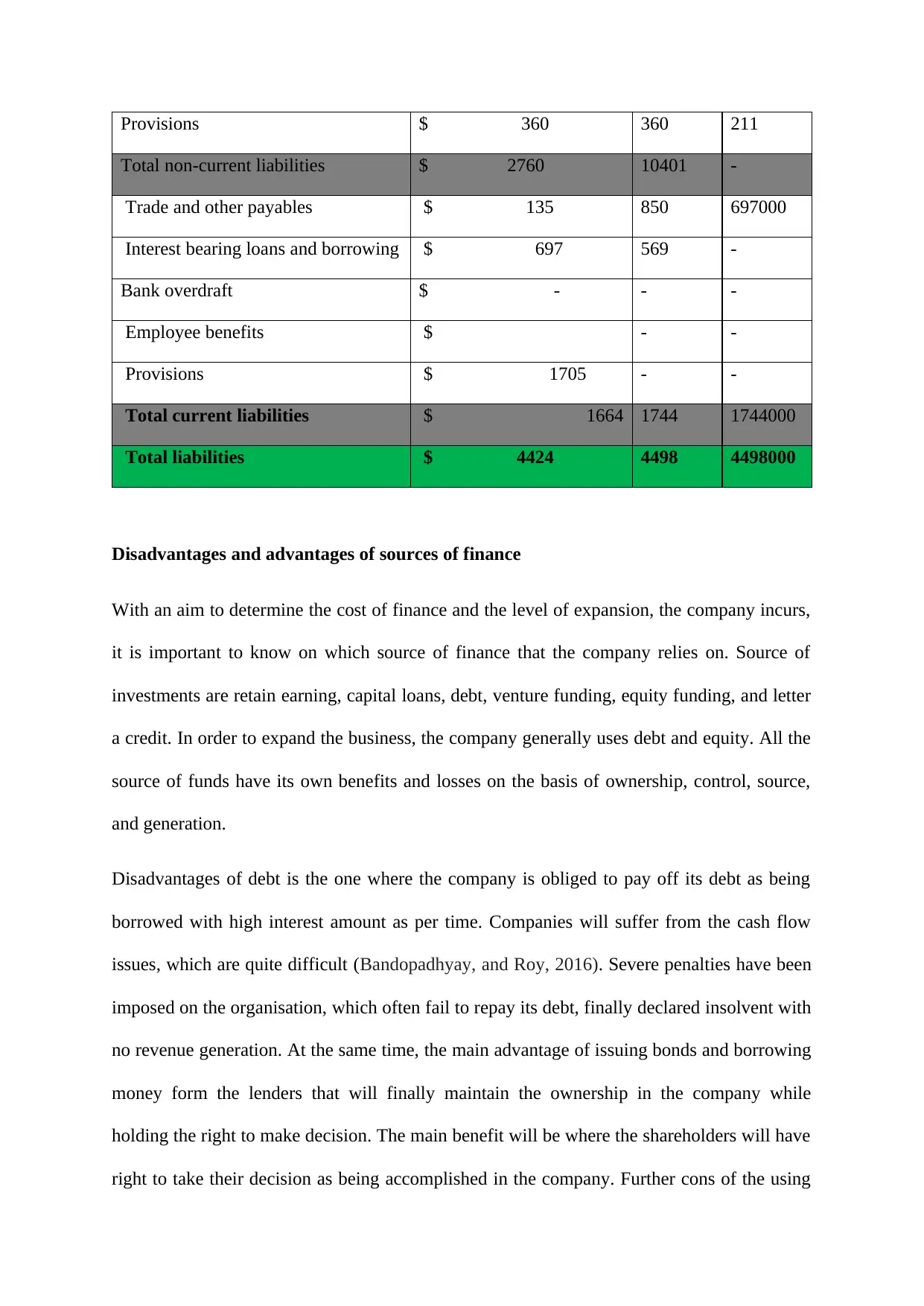

Provisions $ 360 360 211

Total non-current liabilities $ 2760 10401 -

Trade and other payables $ 135 850 697000

Interest bearing loans and borrowing $ 697 569 -

Bank overdraft $ - - -

Employee benefits $ - -

Provisions $ 1705 - -

Total current liabilities $ 1664 1744 1744000

Total liabilities $ 4424 4498 4498000

Disadvantages and advantages of sources of finance

With an aim to determine the cost of finance and the level of expansion, the company incurs,

it is important to know on which source of finance that the company relies on. Source of

investments are retain earning, capital loans, debt, venture funding, equity funding, and letter

a credit. In order to expand the business, the company generally uses debt and equity. All the

source of funds have its own benefits and losses on the basis of ownership, control, source,

and generation.

Disadvantages of debt is the one where the company is obliged to pay off its debt as being

borrowed with high interest amount as per time. Companies will suffer from the cash flow

issues, which are quite difficult (Bandopadhyay, and Roy, 2016). Severe penalties have been

imposed on the organisation, which often fail to repay its debt, finally declared insolvent with

no revenue generation. At the same time, the main advantage of issuing bonds and borrowing

money form the lenders that will finally maintain the ownership in the company while

holding the right to make decision. The main benefit will be where the shareholders will have

right to take their decision as being accomplished in the company. Further cons of the using

Total non-current liabilities $ 2760 10401 -

Trade and other payables $ 135 850 697000

Interest bearing loans and borrowing $ 697 569 -

Bank overdraft $ - - -

Employee benefits $ - -

Provisions $ 1705 - -

Total current liabilities $ 1664 1744 1744000

Total liabilities $ 4424 4498 4498000

Disadvantages and advantages of sources of finance

With an aim to determine the cost of finance and the level of expansion, the company incurs,

it is important to know on which source of finance that the company relies on. Source of

investments are retain earning, capital loans, debt, venture funding, equity funding, and letter

a credit. In order to expand the business, the company generally uses debt and equity. All the

source of funds have its own benefits and losses on the basis of ownership, control, source,

and generation.

Disadvantages of debt is the one where the company is obliged to pay off its debt as being

borrowed with high interest amount as per time. Companies will suffer from the cash flow

issues, which are quite difficult (Bandopadhyay, and Roy, 2016). Severe penalties have been

imposed on the organisation, which often fail to repay its debt, finally declared insolvent with

no revenue generation. At the same time, the main advantage of issuing bonds and borrowing

money form the lenders that will finally maintain the ownership in the company while

holding the right to make decision. The main benefit will be where the shareholders will have

right to take their decision as being accomplished in the company. Further cons of the using

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

debt as a financing source can be company is responsible to pay the main principle amount

along with the interest. Debt financing can affect the credit rating of the company.

On the other hand, equity has the advantage as it possess very low risk, as it does not have

any type of fixed payment. A person must has his own capital to start the business. The

company does not have any risk credit even when interest rate is relatively high. Repayment

of debt loans can lead reduction in the cash flows as needed to prosper the company. At the

same time, it does have many disadvantages inclusive of loss of control, conflicting

situations, and cost.

Part-B

This section will bring out a discussion on critical analysis on the concepts of small

proprietary organisation, large companies, and the disclosure reporting company-

Level of organisation operation determines proprietorship as bring limited by shares under

the Corporation Act, 2001 leading to compliance. As being limited by shares, if a company

operates in unlimited share capital that illustrates that it is being limited by guarantee with no

certain guarantee, these companies cannot be known as proprietary organisation. As per the

ASX and corporation act, certain rules and regulation has to be complied as per law

requirement (Alomari, Power, and Tantisantiwong, 2018). Small proprietary organisation will

include consolidated revenue, which will control the amount, which is less than12.5 million

dollars. South32 is a disclosing company where it will include payments to government in the

annual tax transparency and meeting the needs of voluntary disclosures initiatives. The

information technology system is subject to security breaches that finally results into theft,

security breaches, disclosures and the corrupted information (Alomari, Power, and

Tantisantiwong, 2018). The company effectively report and give disclosures for the process

recoveries for each of the coal operation. The report will set out statutory disclosures as being

required under the corporation act, as per the AASB (Australian accounting standards) in

along with the interest. Debt financing can affect the credit rating of the company.

On the other hand, equity has the advantage as it possess very low risk, as it does not have

any type of fixed payment. A person must has his own capital to start the business. The

company does not have any risk credit even when interest rate is relatively high. Repayment

of debt loans can lead reduction in the cash flows as needed to prosper the company. At the

same time, it does have many disadvantages inclusive of loss of control, conflicting

situations, and cost.

Part-B

This section will bring out a discussion on critical analysis on the concepts of small

proprietary organisation, large companies, and the disclosure reporting company-

Level of organisation operation determines proprietorship as bring limited by shares under

the Corporation Act, 2001 leading to compliance. As being limited by shares, if a company

operates in unlimited share capital that illustrates that it is being limited by guarantee with no

certain guarantee, these companies cannot be known as proprietary organisation. As per the

ASX and corporation act, certain rules and regulation has to be complied as per law

requirement (Alomari, Power, and Tantisantiwong, 2018). Small proprietary organisation will

include consolidated revenue, which will control the amount, which is less than12.5 million

dollars. South32 is a disclosing company where it will include payments to government in the

annual tax transparency and meeting the needs of voluntary disclosures initiatives. The

information technology system is subject to security breaches that finally results into theft,

security breaches, disclosures and the corrupted information (Alomari, Power, and

Tantisantiwong, 2018). The company effectively report and give disclosures for the process

recoveries for each of the coal operation. The report will set out statutory disclosures as being

required under the corporation act, as per the AASB (Australian accounting standards) in

regards to the remuneration payment to the non-executive payment. AASB and other more

authorities will finally avail reliefs for the large organisation. It was not availed to the large

organisation earlier, which include disclosing entities, guarantors of borrowings, large

organisations, and service licensee that operate under 319(4) of corporation law.

A huge proprietary organisation has been generally explained, as it requires preparation of

financial statements where AASIC issued number of instruments with certain amendments

inclusive of specific audited reports (Allen, Qian, and Xie, 2019).

Disclosing organisation always lead to preparation of the financial statements as being

required by the AAS (Australian Accounting Standards). It is quite important to register a

name of the company where it must register ABN, GSTIN number (Goods and service tax),

and tax filing number. Few changes have been regulated in the financial reporting in a year in

the preparation of organisation with employees with more than 100 in numbers, 50 million in

the consolidated revenues, and 25 million in the gross assets (Allen, Qian, and Xie, 2019).

QEM as well as south32 disclose its financial statements and they are registered under

incorporation Act and its related certification. The name of directors and its related person

will have to register under the AOA (Article of Association) and MOA (memorandum of

association), and finally comply with the legal needs of the company. The companies are

disclosing companies who disclose their financial data and maintain a level of transparency

so that it is an activity to release relevant data, which will affect the investment decision. It is

being considered by the SEC, which will include relevance to the management compensation,

operational results, and financial conditions. Composition of investment will include capital-

leasing obligation with the short term obligations as estimated (Allen, Qian, and Xie, 2019).

Conclusion

From the discussion, it can be inclusive of both companies, which are QEM limited, and

south32. The organisation has to maintain an appropriate and considerable source of funds as

authorities will finally avail reliefs for the large organisation. It was not availed to the large

organisation earlier, which include disclosing entities, guarantors of borrowings, large

organisations, and service licensee that operate under 319(4) of corporation law.

A huge proprietary organisation has been generally explained, as it requires preparation of

financial statements where AASIC issued number of instruments with certain amendments

inclusive of specific audited reports (Allen, Qian, and Xie, 2019).

Disclosing organisation always lead to preparation of the financial statements as being

required by the AAS (Australian Accounting Standards). It is quite important to register a

name of the company where it must register ABN, GSTIN number (Goods and service tax),

and tax filing number. Few changes have been regulated in the financial reporting in a year in

the preparation of organisation with employees with more than 100 in numbers, 50 million in

the consolidated revenues, and 25 million in the gross assets (Allen, Qian, and Xie, 2019).

QEM as well as south32 disclose its financial statements and they are registered under

incorporation Act and its related certification. The name of directors and its related person

will have to register under the AOA (Article of Association) and MOA (memorandum of

association), and finally comply with the legal needs of the company. The companies are

disclosing companies who disclose their financial data and maintain a level of transparency

so that it is an activity to release relevant data, which will affect the investment decision. It is

being considered by the SEC, which will include relevance to the management compensation,

operational results, and financial conditions. Composition of investment will include capital-

leasing obligation with the short term obligations as estimated (Allen, Qian, and Xie, 2019).

Conclusion

From the discussion, it can be inclusive of both companies, which are QEM limited, and

south32. The organisation has to maintain an appropriate and considerable source of funds as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.