Financial Resources Management Report: Victoria Babies Analysis

VerifiedAdded on 2020/07/23

|12

|2683

|37

Report

AI Summary

This report provides a comprehensive analysis of financial resources and business structures, focusing on the case of Victoria Babies, a small manufacturing concern. The report begins by examining different business structures, comparing general partnerships, Limited Liability Partnerships (LLPs), and Private Limited Liability Companies, ultimately recommending the conversion to an LLP. It then differentiates between management and financial accounting, outlining their respective purposes, audiences, and regulations. The report further details the three key financial statements: the income statement, balance sheet, and statement of cash flow, including an illustration of annual accounts. Finally, it identifies five key stakeholders—investors, suppliers, lenders, employees, and Her Majesty Revenue and Tax—and their respective information requirements, demonstrating how financial information informs their decision-making processes. The report concludes with a summary of the key findings and recommendations for Victoria Babies' financial management.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Different kind of business structure and their differences...........................................................1

TASK 2............................................................................................................................................2

Explain management and financial accounting...........................................................................2

Key difference between management and financial accounting..................................................2

TASK 3............................................................................................................................................4

Financial statements.....................................................................................................................4

Illustration of annual accounts.....................................................................................................5

Income statement......................................................................................................................5

Balance sheet............................................................................................................................5

Statement of cash flow.............................................................................................................6

TASK 4............................................................................................................................................7

Identify 5 stakeholders and their information requirement..........................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Different kind of business structure and their differences...........................................................1

TASK 2............................................................................................................................................2

Explain management and financial accounting...........................................................................2

Key difference between management and financial accounting..................................................2

TASK 3............................................................................................................................................4

Financial statements.....................................................................................................................4

Illustration of annual accounts.....................................................................................................5

Income statement......................................................................................................................5

Balance sheet............................................................................................................................5

Statement of cash flow.............................................................................................................6

TASK 4............................................................................................................................................7

Identify 5 stakeholders and their information requirement..........................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Financial management is about making solid plans and strategies for acquiring required

funds and assure its right utilization. It involves planning, organizing, allocation, monitoring as

well as controlling the money. Victoria Babies is a small sized manufacturing concern which is

specializes in producing innovative “Non Spill Toddler Bowl”. The current paper will investigate

different form of business structures and highlight key difference to select the best one.

Moreover, the report will clearly present three key statements and differentiate financial

accounting from managerial accounting. Lastly, important stakeholders and their information

requirement will be examined.

TASK 1

Different kind of business structure and their differences

According to the given case, Victoria Babies was set up as an Ordinary Partnership in

which her parents joined as partners with a total turnover of GBP400,000 in 2015. With the

immense growth, a venture capitalist keen to invest GBP 700,000 in its business which will help

the business to meet its capital requirement for expansion program. Thus, it need business to

change their structure either to Limited Liability Partnership or set up business as a Private

Limited Liability Company.

General or Ordinary Partnership: Partnership is simply a combination of two or more

people who take responsibility to run a business with putting their combined efforts and share

profit in set ratio. In this form, all the partners have unlimited liability towards lenders and

creditors (Ahmed and Manab, 2016). Moreover, they are liability for each other’s acts and

omission. Under the legal requirement, to set partnership, there is no need of registration.

Limited Liability Partnership: It is a form of partnership, in which, some partners limit

their liabilities. It does not means that other partner will be obliged for the misconduct and

negligence of copartner. It is different from general partnership because in this, partners have

limited liability. In order to become LLP, Victoria Babies need to incorporate the entity and also

need to follow LLP Act. At the same times, its benefits includes separate legal status, tax

transparency and others.

1 | P a g e

Financial management is about making solid plans and strategies for acquiring required

funds and assure its right utilization. It involves planning, organizing, allocation, monitoring as

well as controlling the money. Victoria Babies is a small sized manufacturing concern which is

specializes in producing innovative “Non Spill Toddler Bowl”. The current paper will investigate

different form of business structures and highlight key difference to select the best one.

Moreover, the report will clearly present three key statements and differentiate financial

accounting from managerial accounting. Lastly, important stakeholders and their information

requirement will be examined.

TASK 1

Different kind of business structure and their differences

According to the given case, Victoria Babies was set up as an Ordinary Partnership in

which her parents joined as partners with a total turnover of GBP400,000 in 2015. With the

immense growth, a venture capitalist keen to invest GBP 700,000 in its business which will help

the business to meet its capital requirement for expansion program. Thus, it need business to

change their structure either to Limited Liability Partnership or set up business as a Private

Limited Liability Company.

General or Ordinary Partnership: Partnership is simply a combination of two or more

people who take responsibility to run a business with putting their combined efforts and share

profit in set ratio. In this form, all the partners have unlimited liability towards lenders and

creditors (Ahmed and Manab, 2016). Moreover, they are liability for each other’s acts and

omission. Under the legal requirement, to set partnership, there is no need of registration.

Limited Liability Partnership: It is a form of partnership, in which, some partners limit

their liabilities. It does not means that other partner will be obliged for the misconduct and

negligence of copartner. It is different from general partnership because in this, partners have

limited liability. In order to become LLP, Victoria Babies need to incorporate the entity and also

need to follow LLP Act. At the same times, its benefits includes separate legal status, tax

transparency and others.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Private Limited Liability Company: It is small organization which cannot issue share to

public as these firms are not listed on any recognized stock exchange. They can offer and issue

share only to their friends, relatives and known members for fundraising (Garrison and et.al.,

2010). As its name, members have limited liability but it involves compliance with multiple of

laws, thus, it includes excessive legal formalities such as compliance with Company Act 2006

and registration. Still, there are number of benefits associated with this form of business structure

i.e. separate entity, tax benefits and full control.

Taking into account all the requirement, it is better to suggest Victoria Babies to convert

business into Limited Liability Partnership, because it involves comparatively less legal

requirement such as LLP Act and incorporation only. Moreover, it overcome the main drawback

of general partnership that is unlimited liability and also will be treated as a separate legal status

under the corporate law.

TASK 2

Explain management and financial accounting

Management accounting is concerned with preparation of internal business reports and

supply it to managers with the view to devise more effective and solid strategies which enable

the entity to achieve sustainable progress (Ahmed and Manab, 2016). Victoria Babies managers

will require sales, cost, inventory and other reports for business planning and decisions.

Unlike this, financial accounting is just aims at recording each and every financial

transaction of the undertaking in annual statements to know profitability and financial health of

the enterprise (Nam and Park, 2016). It includes recording, classifying, summarizing and

analyzing the final results.

Key difference between management and financial accounting

Basis of

difference

Financial accounting Management accounting

Purpose To know financial position and

operational performance of

Victoria Babies (Schipper, Francis

and Weil, 2017)

To devise better business plans,

decisive actions and make growth

strategies

2 | P a g e

public as these firms are not listed on any recognized stock exchange. They can offer and issue

share only to their friends, relatives and known members for fundraising (Garrison and et.al.,

2010). As its name, members have limited liability but it involves compliance with multiple of

laws, thus, it includes excessive legal formalities such as compliance with Company Act 2006

and registration. Still, there are number of benefits associated with this form of business structure

i.e. separate entity, tax benefits and full control.

Taking into account all the requirement, it is better to suggest Victoria Babies to convert

business into Limited Liability Partnership, because it involves comparatively less legal

requirement such as LLP Act and incorporation only. Moreover, it overcome the main drawback

of general partnership that is unlimited liability and also will be treated as a separate legal status

under the corporate law.

TASK 2

Explain management and financial accounting

Management accounting is concerned with preparation of internal business reports and

supply it to managers with the view to devise more effective and solid strategies which enable

the entity to achieve sustainable progress (Ahmed and Manab, 2016). Victoria Babies managers

will require sales, cost, inventory and other reports for business planning and decisions.

Unlike this, financial accounting is just aims at recording each and every financial

transaction of the undertaking in annual statements to know profitability and financial health of

the enterprise (Nam and Park, 2016). It includes recording, classifying, summarizing and

analyzing the final results.

Key difference between management and financial accounting

Basis of

difference

Financial accounting Management accounting

Purpose To know financial position and

operational performance of

Victoria Babies (Schipper, Francis

and Weil, 2017)

To devise better business plans,

decisive actions and make growth

strategies

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Statements Profit and loss statement

Balance sheet

Cash flow statement

Sales reports

Cost reports

Stock reports and others

Requirement It is legally mandatory because as

per Company Act, every private as

well as public company has to

create their accounts for every

financial year.

It is not a legal necessity, still, for

managerial requirement, all the

organizations are involved in it

(Ahmed and Manab, 2016).

Audience It includes external users i.e.

investors, lenders, suppliers, tax

agencies i.e. HMRC, government

and competitor as well.

Only internal audiences such as

managers, workforce, CEO, CFO,

departmental heads and others.

Regulations Victoria Babies accountant need to

use accounting principles (GAAP),

accounting and reporting standards

(IAS and IFRS) to record the

result of their monetary activities

(Nam and Park, 2016).

There is no regulations and standards

set for management accounting.

Frequency P&L can be prepared either

quarterly, semi-annually or

annually, but balance sheet must

be prepared at the closing date of

fiscal year.

It is an ongoing function and reports

are prepared as per managerial need

(Houtson, 2014).

Auditing Auditing the annual account is a

compulsion for Victoria Babies

It is not audited.

Focus It focuses on historical trading

functions, thus, it is a backward-

looking approach.

It focuses on analyzing existing

performance to predict future. Thus, it

is a forward looking method

(Macintosh and Quattrone, 2010).

3 | P a g e

Balance sheet

Cash flow statement

Sales reports

Cost reports

Stock reports and others

Requirement It is legally mandatory because as

per Company Act, every private as

well as public company has to

create their accounts for every

financial year.

It is not a legal necessity, still, for

managerial requirement, all the

organizations are involved in it

(Ahmed and Manab, 2016).

Audience It includes external users i.e.

investors, lenders, suppliers, tax

agencies i.e. HMRC, government

and competitor as well.

Only internal audiences such as

managers, workforce, CEO, CFO,

departmental heads and others.

Regulations Victoria Babies accountant need to

use accounting principles (GAAP),

accounting and reporting standards

(IAS and IFRS) to record the

result of their monetary activities

(Nam and Park, 2016).

There is no regulations and standards

set for management accounting.

Frequency P&L can be prepared either

quarterly, semi-annually or

annually, but balance sheet must

be prepared at the closing date of

fiscal year.

It is an ongoing function and reports

are prepared as per managerial need

(Houtson, 2014).

Auditing Auditing the annual account is a

compulsion for Victoria Babies

It is not audited.

Focus It focuses on historical trading

functions, thus, it is a backward-

looking approach.

It focuses on analyzing existing

performance to predict future. Thus, it

is a forward looking method

(Macintosh and Quattrone, 2010).

3 | P a g e

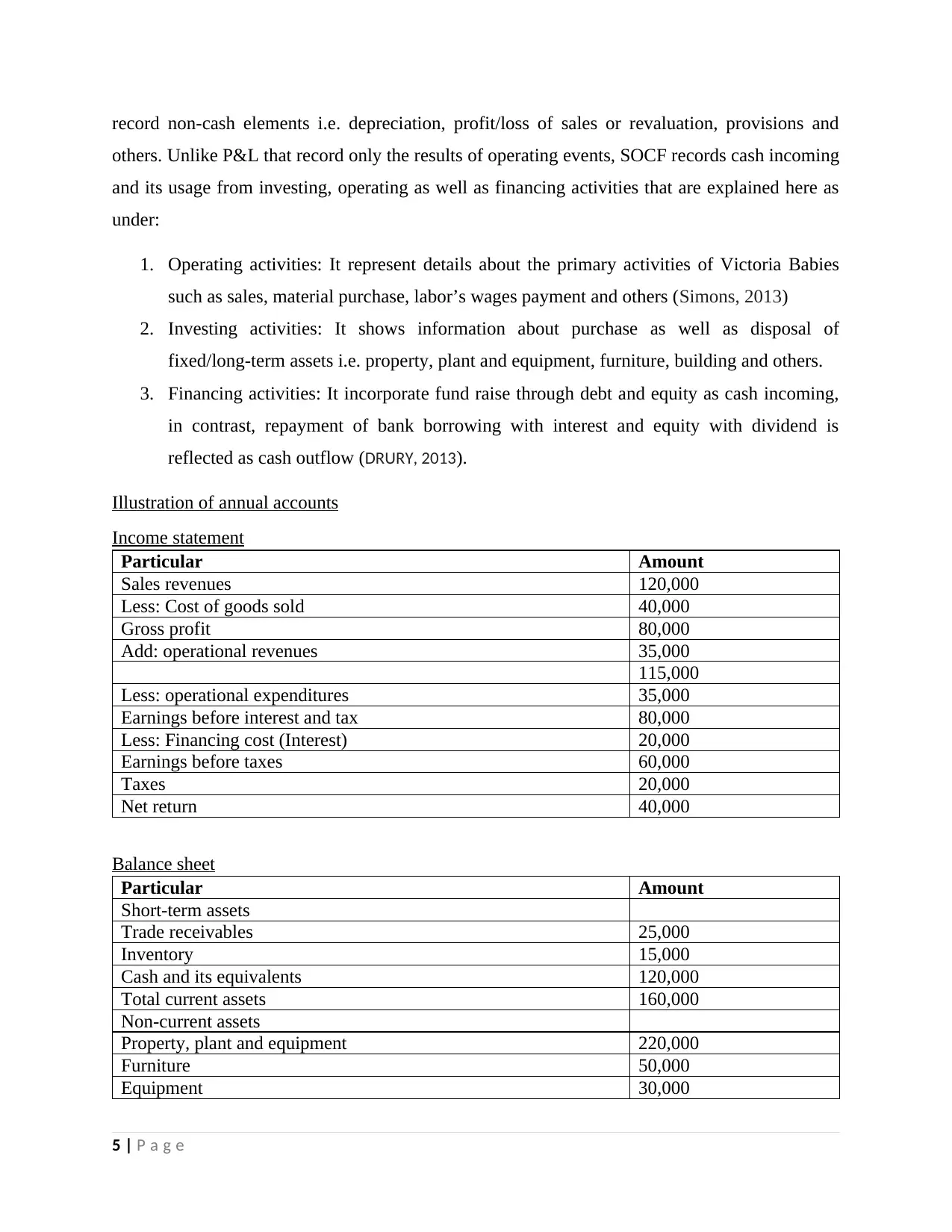

TASK 3

Financial statements

After change of the business structure of Victoria Babies to LLP, it is now legally

necessary for the enterprise to prepare and submit financial accounts. The three financial

statements that it will need to prepare to determine and assess their financial position are

discussed here as under:

Income statement: This is also called profitability or P&L statement which reveals

performance for a given reporting period. It incorporates two key elements that are revenues and

expenditures, first includes income received by entity whereas expenses are the payments,

spending or cost (Schipper, Francis and Weil, 2017). For instance, sales is recorded as income

which is subtracted from cost of sale along with the other direct expense to know gross profit,

excess of it over other indirect expenses i.e. staff salary, marketing and other is called net profit.

Victoria Babies need to prepare such statement following accrual basis of accounting, wherein,

transactions are recorded when they actually incurred. Thus, it only reports current year’s

expenditures and revenues to determine net return.

Balance sheet: It is also called statement of financial position because it presents

financial health of the entity. Assets, liabilities and equity are the three components or key

elements of balance sheet. Assets are the resources which is owned by Victoria Babies, liability

indicates business obligation towards others such as borrowings, lease, overdraft, payables etc.

whereas equity is the total money injected by owner (Zimmerman and Yahya-Zadeh, 2011). It needs

to be prepared at the closing date of financial year.

Accounting equation: Assets=Liabilities+equity

Equity= Assets – liabilities

Liabilities= Assets – equity

Statement of cash flow: This is another account which presents details about cash

movement only thus, it reports both increase and decrease in cash/bank balance of Victoria

Babies in a given period. In other words, it can be said that SOCF is based cash accounting

concept which records and incorporate all the details or transactions that either injected cash into

or results in outflow of cash and its equivalent (Garrison and et.al., 2010). Thus, it does not

4 | P a g e

Financial statements

After change of the business structure of Victoria Babies to LLP, it is now legally

necessary for the enterprise to prepare and submit financial accounts. The three financial

statements that it will need to prepare to determine and assess their financial position are

discussed here as under:

Income statement: This is also called profitability or P&L statement which reveals

performance for a given reporting period. It incorporates two key elements that are revenues and

expenditures, first includes income received by entity whereas expenses are the payments,

spending or cost (Schipper, Francis and Weil, 2017). For instance, sales is recorded as income

which is subtracted from cost of sale along with the other direct expense to know gross profit,

excess of it over other indirect expenses i.e. staff salary, marketing and other is called net profit.

Victoria Babies need to prepare such statement following accrual basis of accounting, wherein,

transactions are recorded when they actually incurred. Thus, it only reports current year’s

expenditures and revenues to determine net return.

Balance sheet: It is also called statement of financial position because it presents

financial health of the entity. Assets, liabilities and equity are the three components or key

elements of balance sheet. Assets are the resources which is owned by Victoria Babies, liability

indicates business obligation towards others such as borrowings, lease, overdraft, payables etc.

whereas equity is the total money injected by owner (Zimmerman and Yahya-Zadeh, 2011). It needs

to be prepared at the closing date of financial year.

Accounting equation: Assets=Liabilities+equity

Equity= Assets – liabilities

Liabilities= Assets – equity

Statement of cash flow: This is another account which presents details about cash

movement only thus, it reports both increase and decrease in cash/bank balance of Victoria

Babies in a given period. In other words, it can be said that SOCF is based cash accounting

concept which records and incorporate all the details or transactions that either injected cash into

or results in outflow of cash and its equivalent (Garrison and et.al., 2010). Thus, it does not

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

record non-cash elements i.e. depreciation, profit/loss of sales or revaluation, provisions and

others. Unlike P&L that record only the results of operating events, SOCF records cash incoming

and its usage from investing, operating as well as financing activities that are explained here as

under:

1. Operating activities: It represent details about the primary activities of Victoria Babies

such as sales, material purchase, labor’s wages payment and others (Simons, 2013)

2. Investing activities: It shows information about purchase as well as disposal of

fixed/long-term assets i.e. property, plant and equipment, furniture, building and others.

3. Financing activities: It incorporate fund raise through debt and equity as cash incoming,

in contrast, repayment of bank borrowing with interest and equity with dividend is

reflected as cash outflow (DRURY, 2013).

Illustration of annual accounts

Income statement

Particular Amount

Sales revenues 120,000

Less: Cost of goods sold 40,000

Gross profit 80,000

Add: operational revenues 35,000

115,000

Less: operational expenditures 35,000

Earnings before interest and tax 80,000

Less: Financing cost (Interest) 20,000

Earnings before taxes 60,000

Taxes 20,000

Net return 40,000

Balance sheet

Particular Amount

Short-term assets

Trade receivables 25,000

Inventory 15,000

Cash and its equivalents 120,000

Total current assets 160,000

Non-current assets

Property, plant and equipment 220,000

Furniture 50,000

Equipment 30,000

5 | P a g e

others. Unlike P&L that record only the results of operating events, SOCF records cash incoming

and its usage from investing, operating as well as financing activities that are explained here as

under:

1. Operating activities: It represent details about the primary activities of Victoria Babies

such as sales, material purchase, labor’s wages payment and others (Simons, 2013)

2. Investing activities: It shows information about purchase as well as disposal of

fixed/long-term assets i.e. property, plant and equipment, furniture, building and others.

3. Financing activities: It incorporate fund raise through debt and equity as cash incoming,

in contrast, repayment of bank borrowing with interest and equity with dividend is

reflected as cash outflow (DRURY, 2013).

Illustration of annual accounts

Income statement

Particular Amount

Sales revenues 120,000

Less: Cost of goods sold 40,000

Gross profit 80,000

Add: operational revenues 35,000

115,000

Less: operational expenditures 35,000

Earnings before interest and tax 80,000

Less: Financing cost (Interest) 20,000

Earnings before taxes 60,000

Taxes 20,000

Net return 40,000

Balance sheet

Particular Amount

Short-term assets

Trade receivables 25,000

Inventory 15,000

Cash and its equivalents 120,000

Total current assets 160,000

Non-current assets

Property, plant and equipment 220,000

Furniture 50,000

Equipment 30,000

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

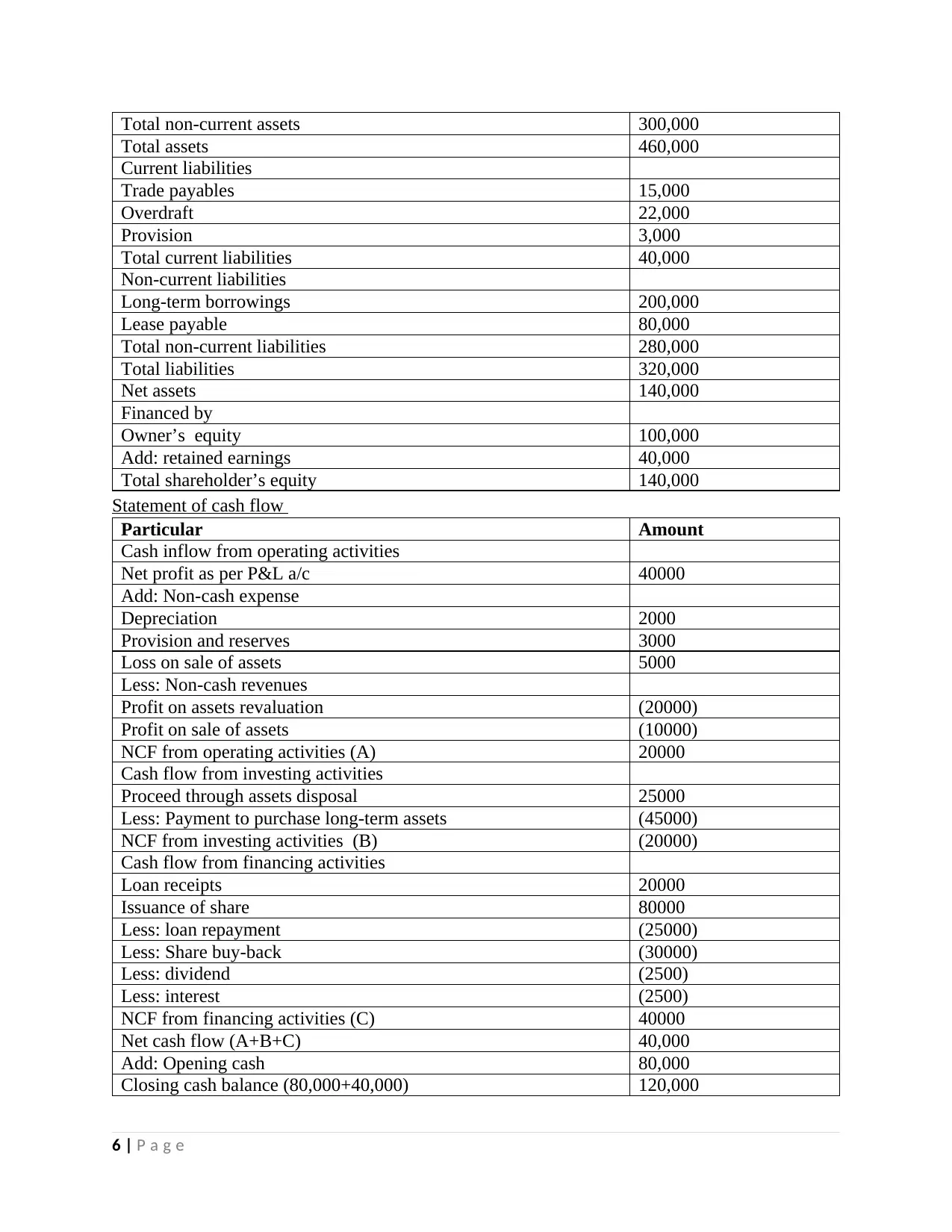

Total non-current assets 300,000

Total assets 460,000

Current liabilities

Trade payables 15,000

Overdraft 22,000

Provision 3,000

Total current liabilities 40,000

Non-current liabilities

Long-term borrowings 200,000

Lease payable 80,000

Total non-current liabilities 280,000

Total liabilities 320,000

Net assets 140,000

Financed by

Owner’s equity 100,000

Add: retained earnings 40,000

Total shareholder’s equity 140,000

Statement of cash flow

Particular Amount

Cash inflow from operating activities

Net profit as per P&L a/c 40000

Add: Non-cash expense

Depreciation 2000

Provision and reserves 3000

Loss on sale of assets 5000

Less: Non-cash revenues

Profit on assets revaluation (20000)

Profit on sale of assets (10000)

NCF from operating activities (A) 20000

Cash flow from investing activities

Proceed through assets disposal 25000

Less: Payment to purchase long-term assets (45000)

NCF from investing activities (B) (20000)

Cash flow from financing activities

Loan receipts 20000

Issuance of share 80000

Less: loan repayment (25000)

Less: Share buy-back (30000)

Less: dividend (2500)

Less: interest (2500)

NCF from financing activities (C) 40000

Net cash flow (A+B+C) 40,000

Add: Opening cash 80,000

Closing cash balance (80,000+40,000) 120,000

6 | P a g e

Total assets 460,000

Current liabilities

Trade payables 15,000

Overdraft 22,000

Provision 3,000

Total current liabilities 40,000

Non-current liabilities

Long-term borrowings 200,000

Lease payable 80,000

Total non-current liabilities 280,000

Total liabilities 320,000

Net assets 140,000

Financed by

Owner’s equity 100,000

Add: retained earnings 40,000

Total shareholder’s equity 140,000

Statement of cash flow

Particular Amount

Cash inflow from operating activities

Net profit as per P&L a/c 40000

Add: Non-cash expense

Depreciation 2000

Provision and reserves 3000

Loss on sale of assets 5000

Less: Non-cash revenues

Profit on assets revaluation (20000)

Profit on sale of assets (10000)

NCF from operating activities (A) 20000

Cash flow from investing activities

Proceed through assets disposal 25000

Less: Payment to purchase long-term assets (45000)

NCF from investing activities (B) (20000)

Cash flow from financing activities

Loan receipts 20000

Issuance of share 80000

Less: loan repayment (25000)

Less: Share buy-back (30000)

Less: dividend (2500)

Less: interest (2500)

NCF from financing activities (C) 40000

Net cash flow (A+B+C) 40,000

Add: Opening cash 80,000

Closing cash balance (80,000+40,000) 120,000

6 | P a g e

TASK 4

Identify 5 stakeholders and their information requirement

Stakeholder theory presents that companies have multiple of stakeholders who either directly or

indirectly interested in business success and progress. With reference to Victoria Babies, some of the

important stakeholders are presented here underneath:

Investors: Investors are the most important stakeholder who invest their money in an undertaking

with the objective to get something in return i.e. dividend, share value appreciation (Ahmed and Manab,

2016). Thus, they analyze Victoria Babies’s stock performance, profitability, dividend policy, rate of

dividend and earnings as well.

Suppliers: Victoria Babies produces “Non Spill Toddler Bowl”, thus, it will require material

for the purpose of manufacturing. Suppliers are those who gave their acceptance to supply

material on credit and thereby facilitate entity to pay later (Bhimani and et.al., 2013). They

evaluate that whether company had maintained a right balance between their current assets and

current liabilities or have enough liquid funds or not to satisfy deferred short-term obligations.

Lenders: In order to raise fund, company often contact banks and other financial

institution for borrowing. Lenders are the people who lend money to the organization and charge

either fixed or floating interest (Macintosh and Quattrone, 2010). They use Victoria Babies annual

reports to know solvency position, profitability, credit rating, cash management and ability to

bear financial burden which indicates its interest payment capability.

Employees: Workers are the most important assets of the firm because without their

presence, efforts and cooperation, Victoria Babies would not be able to grow in such a

competitive world. They are interested in business growth so as to get good salary, monetary

benefits i.e. incentive, bonus, reward and non-monetary advantage i.e. promotion, praise and

others.

Her Majesty Revenue and Tax: It is an independent tax collection agency who collects

corporate tax from the business unit. They use audited P&L to charge tax on net profitability to

collect right amount of tax.

7 | P a g e

Identify 5 stakeholders and their information requirement

Stakeholder theory presents that companies have multiple of stakeholders who either directly or

indirectly interested in business success and progress. With reference to Victoria Babies, some of the

important stakeholders are presented here underneath:

Investors: Investors are the most important stakeholder who invest their money in an undertaking

with the objective to get something in return i.e. dividend, share value appreciation (Ahmed and Manab,

2016). Thus, they analyze Victoria Babies’s stock performance, profitability, dividend policy, rate of

dividend and earnings as well.

Suppliers: Victoria Babies produces “Non Spill Toddler Bowl”, thus, it will require material

for the purpose of manufacturing. Suppliers are those who gave their acceptance to supply

material on credit and thereby facilitate entity to pay later (Bhimani and et.al., 2013). They

evaluate that whether company had maintained a right balance between their current assets and

current liabilities or have enough liquid funds or not to satisfy deferred short-term obligations.

Lenders: In order to raise fund, company often contact banks and other financial

institution for borrowing. Lenders are the people who lend money to the organization and charge

either fixed or floating interest (Macintosh and Quattrone, 2010). They use Victoria Babies annual

reports to know solvency position, profitability, credit rating, cash management and ability to

bear financial burden which indicates its interest payment capability.

Employees: Workers are the most important assets of the firm because without their

presence, efforts and cooperation, Victoria Babies would not be able to grow in such a

competitive world. They are interested in business growth so as to get good salary, monetary

benefits i.e. incentive, bonus, reward and non-monetary advantage i.e. promotion, praise and

others.

Her Majesty Revenue and Tax: It is an independent tax collection agency who collects

corporate tax from the business unit. They use audited P&L to charge tax on net profitability to

collect right amount of tax.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the research, it can be concluded that Victoria Babies should convert or change

their existing structure of general partnership to LLP which involves less legal requirements in

comparison to Private Limited Liability Company. Moreover, there were three statements of

financial statements found that is income statement, cash flow statement and balance sheets

which is prepared following principles, accounting and reporting standards under financial

accounting. At the end, it is found that each of the stakeholders have different interest in the

business, therefore, they extract different set of information from the financial statements for the

purpose of decisions making.

8 | P a g e

From the research, it can be concluded that Victoria Babies should convert or change

their existing structure of general partnership to LLP which involves less legal requirements in

comparison to Private Limited Liability Company. Moreover, there were three statements of

financial statements found that is income statement, cash flow statement and balance sheets

which is prepared following principles, accounting and reporting standards under financial

accounting. At the end, it is found that each of the stakeholders have different interest in the

business, therefore, they extract different set of information from the financial statements for the

purpose of decisions making.

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ahmed, I. and Manab, N.A., 2016. Influence of Enterprise Risk Management Success Factors on

Firm Financial and Non-Financial Performance: A Proposed Model. International

Journal of Economics and Financial Issues. 6(3). pp.18-63.

Bhimani, A. and et.al., 2013. Introduction to Management Accounting. Pearson Higher Ed.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Garrison, R.H. and et.al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Nam, G. and Park, J.W., 2016. A new approach to evaluating earnings management

models. International Journal of Managerial and Financial Accounting. 8(3-4). pp.247-

269.

Schipper, K., Francis, J. and Weil, R., 2017. Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Schipper, K., Francis, J. and Weil, R., 2017. Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Simons, R., 2013. Performance Measurement and Control Systems for Implementing Strategy

Text and Cases: Pearson New International Edition. Pearson Higher Ed.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education. 26(1). pp.258-259.

Online

Houtson, G., 2014. Strategic Management Accounting. [Online]. Available through: <

http://smallbusiness.chron.com/examples-strategic-management-accounting-

18149.html>.

9 | P a g e

Books and Journals

Ahmed, I. and Manab, N.A., 2016. Influence of Enterprise Risk Management Success Factors on

Firm Financial and Non-Financial Performance: A Proposed Model. International

Journal of Economics and Financial Issues. 6(3). pp.18-63.

Bhimani, A. and et.al., 2013. Introduction to Management Accounting. Pearson Higher Ed.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Garrison, R.H. and et.al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Nam, G. and Park, J.W., 2016. A new approach to evaluating earnings management

models. International Journal of Managerial and Financial Accounting. 8(3-4). pp.247-

269.

Schipper, K., Francis, J. and Weil, R., 2017. Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Schipper, K., Francis, J. and Weil, R., 2017. Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Simons, R., 2013. Performance Measurement and Control Systems for Implementing Strategy

Text and Cases: Pearson New International Edition. Pearson Higher Ed.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education. 26(1). pp.258-259.

Online

Houtson, G., 2014. Strategic Management Accounting. [Online]. Available through: <

http://smallbusiness.chron.com/examples-strategic-management-accounting-

18149.html>.

9 | P a g e

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.