Financial Analysis: Management Accounting Report for Unicorn Grocery

VerifiedAdded on 2019/12/18

|17

|5259

|251

Report

AI Summary

This report provides a detailed analysis of management accounting practices, focusing on a case study of Unicorn Grocery, a cooperative store in the UK. The report explores various aspects of management accounting, including its types, different reporting methods, and techniques of cost analysis to prepare income statements. It delves into absorption and marginal costing methods to calculate net profit. The report also examines the benefits of management accounting systems, planning tools for budgetary control, budget preparation and forecasting, and the adaptation of management accounting during financial problems. Furthermore, it discusses the role of management accounting in an organization and the accounting tools helpful in fixing financial issues, along with the role of financial reports for a company. The report provides income statements using both absorption and marginal costing methods, offering a comprehensive overview of financial analysis and decision-making processes within the context of the grocery business. The report is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

P1 Management accounting and its types. .................................................................................3

P2: Different methods of management accounting reporting. ...................................................4

Task 2...............................................................................................................................................6

P3 Techniques of cost analysis to prepare an income statement................................................6

M1 Benefits of management accounting systems......................................................................9

D1 Management accounting system and reporting.....................................................................9

TASK 3..........................................................................................................................................10

P4. Advantages and disadvantage of Planning Tools used for Budgetary Control.................10

M3. Preparation and forecasting of budget...............................................................................12

Task 4.............................................................................................................................................12

P5. Adaption of Management Accounting System during financial problem..........................12

M4: Role of Management Accounting in an organization........................................................13

D3. Accounting tools helpful in fixing financial problems.......................................................14

D2. Role of Financial Report for a Company...........................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

P1 Management accounting and its types. .................................................................................3

P2: Different methods of management accounting reporting. ...................................................4

Task 2...............................................................................................................................................6

P3 Techniques of cost analysis to prepare an income statement................................................6

M1 Benefits of management accounting systems......................................................................9

D1 Management accounting system and reporting.....................................................................9

TASK 3..........................................................................................................................................10

P4. Advantages and disadvantage of Planning Tools used for Budgetary Control.................10

M3. Preparation and forecasting of budget...............................................................................12

Task 4.............................................................................................................................................12

P5. Adaption of Management Accounting System during financial problem..........................12

M4: Role of Management Accounting in an organization........................................................13

D3. Accounting tools helpful in fixing financial problems.......................................................14

D2. Role of Financial Report for a Company...........................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

2

INTRODUCTION

Managerial accounting played an important role on the collection and generation of

various financial information and data form various functional department of the company. It is a

process of planning, analyses, interpretation and controlling all this information which can help

to make various decision making by the manager. There are various decision making at the

different level like strategic level, operational level and tactical level (Baldvinsdottir, Mitchell,

and Nørreklit, 2010). The accounting system is measure the performance of the organization in

an effective manner. The present report is based on the Unicorn grocery which is a cooperative

store in the United Kingdom. They provide a wide range of products to its customers which can

include fruits, breads, packed food items, tea and coffee, fresh juices and other departmental and

grocery products. The cited business unit is owned by democratic members and use a concept of

cooperative model of business. The organization structure of the business in participative which

can help to resolve a complex conflict in an effective manner. Apart from that the report also

provide the firm financial information which can help to make their decision more efficiently.

TASK 1

P1 Management accounting and its types.

Management accounting is the process in which certain management reports and accounts are

required to be made which will provide the organisation with accurate and timely statistical and

financial information. This information’s are required by the managers to take day to day and

short term decisions. These reports are basically prepared on monthly or weekly basis to be

provided to an organisations internal audiences. They show the amount of cash and sales revenue

and raw material and inventory, accounts receivables, outstanding debts and will also include

variance analysis, charts, etc. Management accounting mainly extends to three basic areas which

are strategic management, performance management and risk management (Bennett,Schaltegger,

and Zvezdov, 2013).

Different types of management accounting systems:

Inventory control system: It is essential for a business organization is to maintained efficiency

in the company. The main aim of this system is to reducing time spend of inventory, monitor

time consumption and increase profitability of the company.

3

Managerial accounting played an important role on the collection and generation of

various financial information and data form various functional department of the company. It is a

process of planning, analyses, interpretation and controlling all this information which can help

to make various decision making by the manager. There are various decision making at the

different level like strategic level, operational level and tactical level (Baldvinsdottir, Mitchell,

and Nørreklit, 2010). The accounting system is measure the performance of the organization in

an effective manner. The present report is based on the Unicorn grocery which is a cooperative

store in the United Kingdom. They provide a wide range of products to its customers which can

include fruits, breads, packed food items, tea and coffee, fresh juices and other departmental and

grocery products. The cited business unit is owned by democratic members and use a concept of

cooperative model of business. The organization structure of the business in participative which

can help to resolve a complex conflict in an effective manner. Apart from that the report also

provide the firm financial information which can help to make their decision more efficiently.

TASK 1

P1 Management accounting and its types.

Management accounting is the process in which certain management reports and accounts are

required to be made which will provide the organisation with accurate and timely statistical and

financial information. This information’s are required by the managers to take day to day and

short term decisions. These reports are basically prepared on monthly or weekly basis to be

provided to an organisations internal audiences. They show the amount of cash and sales revenue

and raw material and inventory, accounts receivables, outstanding debts and will also include

variance analysis, charts, etc. Management accounting mainly extends to three basic areas which

are strategic management, performance management and risk management (Bennett,Schaltegger,

and Zvezdov, 2013).

Different types of management accounting systems:

Inventory control system: It is essential for a business organization is to maintained efficiency

in the company. The main aim of this system is to reducing time spend of inventory, monitor

time consumption and increase profitability of the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimisation system: - This is one of the most usable modal which helps to calculate the

demand of a product at different price level. The main aim of this approach is to setting up a

price of a product where maximum profit will be gained and demand of such product is to be

maintained. According to the various principles that there is a direct relation between price and

demand for a product. This is essential for a company to set their product price which is not too

much and should be affordable for a consumer with also provide profit out of them.

Cost accounting system: This is one of the most significant tool in the management accounting

related with the recording all operational and production activities. This approach is using in

variety of industries specially in the manufacturing sector. The main aim of this system to

identify cost of a product or services, cost planning and its effective control and record all

information for the managerial decision making. It will help to produce a product through

maximum utilization of organizational resources in order to achieve their targets.

P2: Different methods of management accounting reporting.

The management accounting reporting was prevalent in in the 18 century as well.

This many historian have said about this management accounting report in many different ways

according to their views from time to time .Basically this system of accounting was used by the

different industries in past decade. They did not had the advanced ideas about this management

accounting system. But in today's world this management accounting has evolved into a

dynamic and extremely important .Due to this management accounting on can be able to develop

his carrier in this field (Christ, and Burritt, 2013).The developing business is being able to do his

accounting work more easy and comfortable . The different method used in the management

accounting reporting can be explained as given below.

Performance report: This is important for every organization is to analyse and evaluate their

performance on regular basis. For this, they need to compare their past performance and

established target with the current figures. It will provide the actual position of the company and

they can carry out its work accordingly. For example, after evaluation of historical data manager

found that performance not up the mark. they can easily make corrective actions and improve in

the near future. For performance improvement manager can use variety of tools and helps to

increase staff motivation leads to increase productivity and profitability.

Inventory management report: This report related with the various information which required to

the top management in order to control inventory. The main aim of this report is to maintain a

4

demand of a product at different price level. The main aim of this approach is to setting up a

price of a product where maximum profit will be gained and demand of such product is to be

maintained. According to the various principles that there is a direct relation between price and

demand for a product. This is essential for a company to set their product price which is not too

much and should be affordable for a consumer with also provide profit out of them.

Cost accounting system: This is one of the most significant tool in the management accounting

related with the recording all operational and production activities. This approach is using in

variety of industries specially in the manufacturing sector. The main aim of this system to

identify cost of a product or services, cost planning and its effective control and record all

information for the managerial decision making. It will help to produce a product through

maximum utilization of organizational resources in order to achieve their targets.

P2: Different methods of management accounting reporting.

The management accounting reporting was prevalent in in the 18 century as well.

This many historian have said about this management accounting report in many different ways

according to their views from time to time .Basically this system of accounting was used by the

different industries in past decade. They did not had the advanced ideas about this management

accounting system. But in today's world this management accounting has evolved into a

dynamic and extremely important .Due to this management accounting on can be able to develop

his carrier in this field (Christ, and Burritt, 2013).The developing business is being able to do his

accounting work more easy and comfortable . The different method used in the management

accounting reporting can be explained as given below.

Performance report: This is important for every organization is to analyse and evaluate their

performance on regular basis. For this, they need to compare their past performance and

established target with the current figures. It will provide the actual position of the company and

they can carry out its work accordingly. For example, after evaluation of historical data manager

found that performance not up the mark. they can easily make corrective actions and improve in

the near future. For performance improvement manager can use variety of tools and helps to

increase staff motivation leads to increase productivity and profitability.

Inventory management report: This report related with the various information which required to

the top management in order to control inventory. The main aim of this report is to maintain a

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

minimum level of stock in warehouse which save their cost of acquisition and other operations

cost. If a business organization cannot manage such report they can facing huge loss and

mismanagement of financial resources. With the help of such costing technique EOQ and

activity based accounting can be determined in an appropriate manner.

Variable analyses report: In a production process, there are variety of expenses incurred in a unit.

These cost can be direct, indirect, fixed, variable etc. This report is related with the all variable

expenses of a product. Variable cost is including such variable which are change as per the level

of production in manufacturing a unit. This cost is very on product quantity which includes direct

labour, material cost, power and so on.

Job costing report: There are various business corporation where product and services are

produced on the basis of customer order, their specification. Basically, this involves a variety of

industries such as aircraft, car, ship building companies. A large number of employees working

in a unit which associated with a job and incurred a cost. These all expenses need to be added

and suck cost can be divided among total number of units are produced. This will help to identify

each job and their cost will also be control which leads to increase profit.

Absorption costing: It is a cost accounting approach which include all types of cost associated

with am product and service s such as fixed and variable. This is one of the best approach to

determine all kind of cost material, labour, machinery, overhead and inventory as well. Such

costing method allow a manager to provide the exact picture of cost and profit earned by the

company.

Managerial costing: This is another approach to calculating the profit earn by the business

organization. In this method all kind of variable cost including in the calculation. So that cost of

product will change on the basis of production. Of production of a product increase it will also

increase in the cost. On the other hand, if production is lower it will reduce the cost of a product.

Task 2

P3 Techniques of cost analysis to prepare an income statement.

Cost analyses is essential for each and every business organization in order to evaluate the all

data which can help to make their decision effective. There are various tools and approaches

which can be used by the cited business unit and design and create an income statement which

can be included margin and absorption cost methods in order to calculate net profit of the

company.

5

cost. If a business organization cannot manage such report they can facing huge loss and

mismanagement of financial resources. With the help of such costing technique EOQ and

activity based accounting can be determined in an appropriate manner.

Variable analyses report: In a production process, there are variety of expenses incurred in a unit.

These cost can be direct, indirect, fixed, variable etc. This report is related with the all variable

expenses of a product. Variable cost is including such variable which are change as per the level

of production in manufacturing a unit. This cost is very on product quantity which includes direct

labour, material cost, power and so on.

Job costing report: There are various business corporation where product and services are

produced on the basis of customer order, their specification. Basically, this involves a variety of

industries such as aircraft, car, ship building companies. A large number of employees working

in a unit which associated with a job and incurred a cost. These all expenses need to be added

and suck cost can be divided among total number of units are produced. This will help to identify

each job and their cost will also be control which leads to increase profit.

Absorption costing: It is a cost accounting approach which include all types of cost associated

with am product and service s such as fixed and variable. This is one of the best approach to

determine all kind of cost material, labour, machinery, overhead and inventory as well. Such

costing method allow a manager to provide the exact picture of cost and profit earned by the

company.

Managerial costing: This is another approach to calculating the profit earn by the business

organization. In this method all kind of variable cost including in the calculation. So that cost of

product will change on the basis of production. Of production of a product increase it will also

increase in the cost. On the other hand, if production is lower it will reduce the cost of a product.

Task 2

P3 Techniques of cost analysis to prepare an income statement.

Cost analyses is essential for each and every business organization in order to evaluate the all

data which can help to make their decision effective. There are various tools and approaches

which can be used by the cited business unit and design and create an income statement which

can be included margin and absorption cost methods in order to calculate net profit of the

company.

5

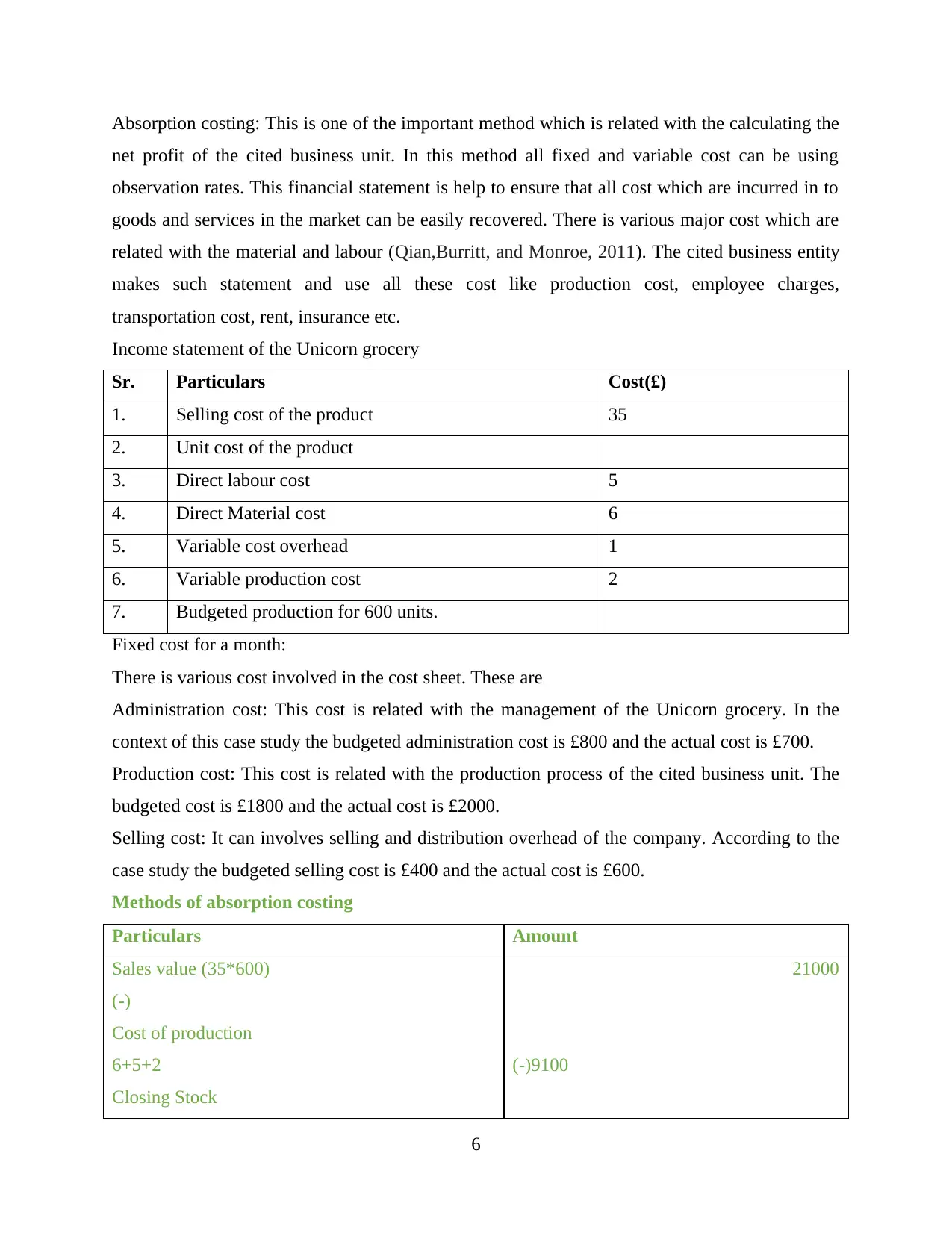

Absorption costing: This is one of the important method which is related with the calculating the

net profit of the cited business unit. In this method all fixed and variable cost can be using

observation rates. This financial statement is help to ensure that all cost which are incurred in to

goods and services in the market can be easily recovered. There is various major cost which are

related with the material and labour (Qian,Burritt, and Monroe, 2011). The cited business entity

makes such statement and use all these cost like production cost, employee charges,

transportation cost, rent, insurance etc.

Income statement of the Unicorn grocery

Sr. Particulars Cost(£)

1. Selling cost of the product 35

2. Unit cost of the product

3. Direct labour cost 5

4. Direct Material cost 6

5. Variable cost overhead 1

6. Variable production cost 2

7. Budgeted production for 600 units.

Fixed cost for a month:

There is various cost involved in the cost sheet. These are

Administration cost: This cost is related with the management of the Unicorn grocery. In the

context of this case study the budgeted administration cost is £800 and the actual cost is £700.

Production cost: This cost is related with the production process of the cited business unit. The

budgeted cost is £1800 and the actual cost is £2000.

Selling cost: It can involves selling and distribution overhead of the company. According to the

case study the budgeted selling cost is £400 and the actual cost is £600.

Methods of absorption costing

Particulars Amount

Sales value (35*600)

(-)

Cost of production

6+5+2

Closing Stock

21000

(-)9100

6

net profit of the cited business unit. In this method all fixed and variable cost can be using

observation rates. This financial statement is help to ensure that all cost which are incurred in to

goods and services in the market can be easily recovered. There is various major cost which are

related with the material and labour (Qian,Burritt, and Monroe, 2011). The cited business entity

makes such statement and use all these cost like production cost, employee charges,

transportation cost, rent, insurance etc.

Income statement of the Unicorn grocery

Sr. Particulars Cost(£)

1. Selling cost of the product 35

2. Unit cost of the product

3. Direct labour cost 5

4. Direct Material cost 6

5. Variable cost overhead 1

6. Variable production cost 2

7. Budgeted production for 600 units.

Fixed cost for a month:

There is various cost involved in the cost sheet. These are

Administration cost: This cost is related with the management of the Unicorn grocery. In the

context of this case study the budgeted administration cost is £800 and the actual cost is £700.

Production cost: This cost is related with the production process of the cited business unit. The

budgeted cost is £1800 and the actual cost is £2000.

Selling cost: It can involves selling and distribution overhead of the company. According to the

case study the budgeted selling cost is £400 and the actual cost is £600.

Methods of absorption costing

Particulars Amount

Sales value (35*600)

(-)

Cost of production

6+5+2

Closing Stock

21000

(-)9100

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

100*13

Variable cost

Contribution

Less

Variable sales expenses

600-1

Fixed Cost

Admin. & Selling

(700+600)

Total

(-)1300

(-)7800

13200

(-) 600

(-) 2000

(-)1300

9300

Net profit by using absorption costing

Particulars Amount

Sales

35*600

(-)

Cost of Production

Gross Profit

(-)

Cost (Fixed and variable)

Variable sales expenses

600*1

Adm. And Selling expenses

700+600

(-)

Over absorption fixed production overhead

21000

9600

11400

600

1300

(-) 100 (-)1800

9600

Marginal costing: This is another approach which is used by the various organizations in order to

differentiating between different cost such as fixed cost, variable cost, marginal cost and try to

7

Variable cost

Contribution

Less

Variable sales expenses

600-1

Fixed Cost

Admin. & Selling

(700+600)

Total

(-)1300

(-)7800

13200

(-) 600

(-) 2000

(-)1300

9300

Net profit by using absorption costing

Particulars Amount

Sales

35*600

(-)

Cost of Production

Gross Profit

(-)

Cost (Fixed and variable)

Variable sales expenses

600*1

Adm. And Selling expenses

700+600

(-)

Over absorption fixed production overhead

21000

9600

11400

600

1300

(-) 100 (-)1800

9600

Marginal costing: This is another approach which is used by the various organizations in order to

differentiating between different cost such as fixed cost, variable cost, marginal cost and try to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

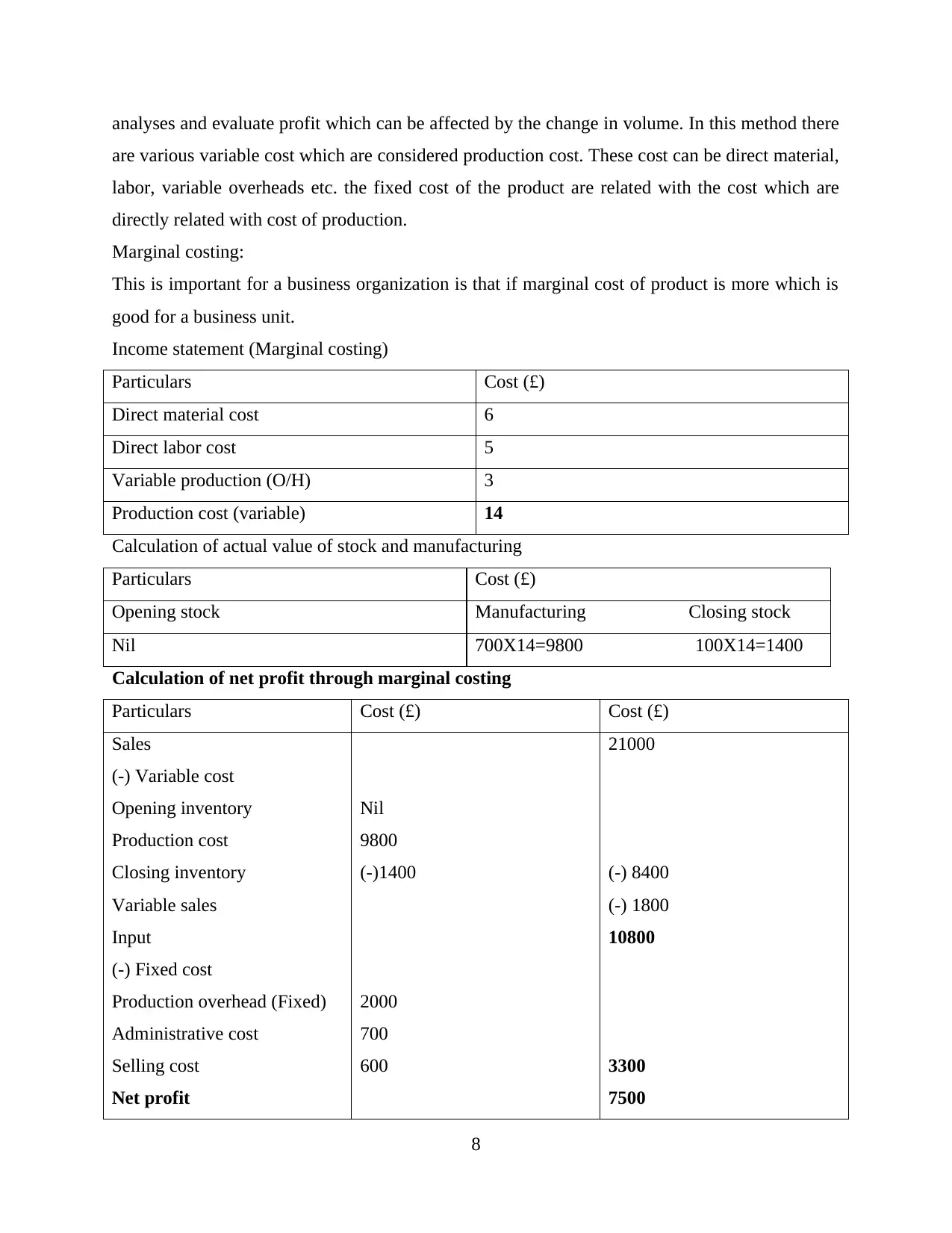

analyses and evaluate profit which can be affected by the change in volume. In this method there

are various variable cost which are considered production cost. These cost can be direct material,

labor, variable overheads etc. the fixed cost of the product are related with the cost which are

directly related with cost of production.

Marginal costing:

This is important for a business organization is that if marginal cost of product is more which is

good for a business unit.

Income statement (Marginal costing)

Particulars Cost (£)

Direct material cost 6

Direct labor cost 5

Variable production (O/H) 3

Production cost (variable) 14

Calculation of actual value of stock and manufacturing

Particulars Cost (£)

Opening stock Manufacturing Closing stock

Nil 700X14=9800 100X14=1400

Calculation of net profit through marginal costing

Particulars Cost (£) Cost (£)

Sales

(-) Variable cost

Opening inventory

Production cost

Closing inventory

Variable sales

Input

(-) Fixed cost

Production overhead (Fixed)

Administrative cost

Selling cost

Net profit

Nil

9800

(-)1400

2000

700

600

21000

(-) 8400

(-) 1800

10800

3300

7500

8

are various variable cost which are considered production cost. These cost can be direct material,

labor, variable overheads etc. the fixed cost of the product are related with the cost which are

directly related with cost of production.

Marginal costing:

This is important for a business organization is that if marginal cost of product is more which is

good for a business unit.

Income statement (Marginal costing)

Particulars Cost (£)

Direct material cost 6

Direct labor cost 5

Variable production (O/H) 3

Production cost (variable) 14

Calculation of actual value of stock and manufacturing

Particulars Cost (£)

Opening stock Manufacturing Closing stock

Nil 700X14=9800 100X14=1400

Calculation of net profit through marginal costing

Particulars Cost (£) Cost (£)

Sales

(-) Variable cost

Opening inventory

Production cost

Closing inventory

Variable sales

Input

(-) Fixed cost

Production overhead (Fixed)

Administrative cost

Selling cost

Net profit

Nil

9800

(-)1400

2000

700

600

21000

(-) 8400

(-) 1800

10800

3300

7500

8

M1 Benefits of management accounting systems

Enhances profitability: Engagement accounting exercises budgetary control and capital

budgeting which enables it to reduce the cost and increase the profitability.

Makes company more efficient: Management accounting is used as it evaluate company actual

performance with set performance and finds out the variance. There are specific budgetary

tools available to reduce or remove those variances hence making it more efficient.

Decision making simplified: Managerial decision making regarding financial statements is

simplified as management accounting provides weekly and monthly reports which enables

the managers in understanding about the available finance and the extra cost (Christ, and

Burritt,2013).

Enables control over fluctuation: Management accounting provides extra control over any future

fluctuation in market or financial resources. As it has provision of emergency funds and also

it studies fund flow in detail.

Enhances Cost transparency: Company is able to analyse the total cost and expenditure in all the

weekly and monthly reports and this helps in getting cost transparency.

D1 Management accounting system and reporting.

Management Accounting System collect the financial data from operation department of the

organization or company's such as the sales cost, row marital and cost resources, cost then

converting that data into information and analysis this report. It helps in making the decision

making, planning of goals and objective other efficiency. Reporting is done for or analysing

the current conditions company. It is done for analysing the the creditors and investors and

for maintaining them for financing more creditor and investor in market. Basically they both

help the company for economic level and manages the finical conditions.

TASK 3

P4. Advantages and disadvantage of Planning Tools used for Budgetary Control.

Every organisation wants to get the work done in the minimum investment while getting

maximum results and for this the managers of company have the tool of budgetary control.

9

Enhances profitability: Engagement accounting exercises budgetary control and capital

budgeting which enables it to reduce the cost and increase the profitability.

Makes company more efficient: Management accounting is used as it evaluate company actual

performance with set performance and finds out the variance. There are specific budgetary

tools available to reduce or remove those variances hence making it more efficient.

Decision making simplified: Managerial decision making regarding financial statements is

simplified as management accounting provides weekly and monthly reports which enables

the managers in understanding about the available finance and the extra cost (Christ, and

Burritt,2013).

Enables control over fluctuation: Management accounting provides extra control over any future

fluctuation in market or financial resources. As it has provision of emergency funds and also

it studies fund flow in detail.

Enhances Cost transparency: Company is able to analyse the total cost and expenditure in all the

weekly and monthly reports and this helps in getting cost transparency.

D1 Management accounting system and reporting.

Management Accounting System collect the financial data from operation department of the

organization or company's such as the sales cost, row marital and cost resources, cost then

converting that data into information and analysis this report. It helps in making the decision

making, planning of goals and objective other efficiency. Reporting is done for or analysing

the current conditions company. It is done for analysing the the creditors and investors and

for maintaining them for financing more creditor and investor in market. Basically they both

help the company for economic level and manages the finical conditions.

TASK 3

P4. Advantages and disadvantage of Planning Tools used for Budgetary Control.

Every organisation wants to get the work done in the minimum investment while getting

maximum results and for this the managers of company have the tool of budgetary control.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgetary Control is a process of setting financial and performance goals with budgets, compare

the actual results and push performance to even higher standard. The whole process is to be

done by the manager, as its him who has to find the most efficient way to getting things done.

Budgetary control is one of the best tool to reduce cost to the optimum levels. Basically

managers prepares different types of budgets under budgetary control. Usually there are few

purpose which are served by the budgets-

In setting standard for all process

Co-ordination of resources

Provides basis for evaluation of different units.

Provides clarity about all available resources

Mostly, organisations use 3 types of budgets- Financial budgets, Operating budgets and Non-

Monetary budgets. Financial Budgets provide overview about the possible sources of income and

where the money will be spent. It embraces the impact of all financial decisions of the firm,

Some sources of cash include- Sales revenue, the sale of assets, issuance of stocks and debtors

payment of loans with interest. On the other hand cash is used to pay debts, dividends, loans,

expenses. Financial budget include Cash budget and balance sheet budget (Shah, Malik, and

Malik, , 2011).

Operating budgets are associated with the estimation of income and expenses based on

forecasted sales revenue during given period of time. It have sub budgets, such as- the sales and

revenue budget, the expense budget, the project budget. Non-monetary budgets are expressed in

non-financial sales or revenue and expenses. If the profits are too low then steps are needed to be

taken by either cutting expenses or increasing sales budget. There are certain advantages and

disadvantages of different types of tools of Budgetary Control-

Advantages:

Well defined planning: Budgets are based on well defined plans which enable different

departments about what is to be done. They have their own budgets and they have to

make sure to keep the ratio of income and expenditure maintained.

Increased effectiveness and efficiency: Budgeting is the most efficient and effective

way to reducing over expenditure and helps in maintaining the cost at optimum level.

10

the actual results and push performance to even higher standard. The whole process is to be

done by the manager, as its him who has to find the most efficient way to getting things done.

Budgetary control is one of the best tool to reduce cost to the optimum levels. Basically

managers prepares different types of budgets under budgetary control. Usually there are few

purpose which are served by the budgets-

In setting standard for all process

Co-ordination of resources

Provides basis for evaluation of different units.

Provides clarity about all available resources

Mostly, organisations use 3 types of budgets- Financial budgets, Operating budgets and Non-

Monetary budgets. Financial Budgets provide overview about the possible sources of income and

where the money will be spent. It embraces the impact of all financial decisions of the firm,

Some sources of cash include- Sales revenue, the sale of assets, issuance of stocks and debtors

payment of loans with interest. On the other hand cash is used to pay debts, dividends, loans,

expenses. Financial budget include Cash budget and balance sheet budget (Shah, Malik, and

Malik, , 2011).

Operating budgets are associated with the estimation of income and expenses based on

forecasted sales revenue during given period of time. It have sub budgets, such as- the sales and

revenue budget, the expense budget, the project budget. Non-monetary budgets are expressed in

non-financial sales or revenue and expenses. If the profits are too low then steps are needed to be

taken by either cutting expenses or increasing sales budget. There are certain advantages and

disadvantages of different types of tools of Budgetary Control-

Advantages:

Well defined planning: Budgets are based on well defined plans which enable different

departments about what is to be done. They have their own budgets and they have to

make sure to keep the ratio of income and expenditure maintained.

Increased effectiveness and efficiency: Budgeting is the most efficient and effective

way to reducing over expenditure and helps in maintaining the cost at optimum level.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strengthen the over all control system: Budgeting is the best way to make sure that the

organisation keeps its proper control over income and expenditure ratio. It also reduces

the variance between the actual and standard performance.

Enhances co-ordination: Budgets make sure that all the department co-ordinate while

they are free for their own expenses and income. But if the need arise proper sharing of

resources is done.

Attempts to delegate more authority: Budgeting provides encouragement to delegation

of authority. It also set the limit on the use of delegated authority usage.

Dis-advantages

Based on estimation: estimations are prediction which are not fixed. If in any case

estimation are wrong then company will suffer big losses.

Time and resource consuming: Budgetary control is a best tool but it consumes a lot of

time and also consumes resources, as experts are hired. which turns into its disadvantage

Budgets Revision: With the change in scenario Budgets are revised which leads to more

resource consumptions and increases administration cost.

Constraint for managerial initiative: managers try to keep the cost as low as possible to

achieve the budgetary figures and when this happens they are not able to exercise their

managerial innovations (Contrafatto, . and Burns,2013).

Develops Conflicts: Every line manager wants more resource for his department in while

M3. Preparation and forecasting of budget.

It is essential for a company is that they make their budget in an effective way. It required

pre planning and there are various factors involved which can be influenced such budget. As a

manager of the firm they required to study all these factors carefully which can help to evaluate

budget in an effective manner. It is systematic process where the income and expenditure

calculated. In the next stage they frame the target which are related with the income and

expenditure. The cited business unit is required that to forecast all factors and elements so that

they can make their budget and attain its desired goals and objectives (van 2011).

11

organisation keeps its proper control over income and expenditure ratio. It also reduces

the variance between the actual and standard performance.

Enhances co-ordination: Budgets make sure that all the department co-ordinate while

they are free for their own expenses and income. But if the need arise proper sharing of

resources is done.

Attempts to delegate more authority: Budgeting provides encouragement to delegation

of authority. It also set the limit on the use of delegated authority usage.

Dis-advantages

Based on estimation: estimations are prediction which are not fixed. If in any case

estimation are wrong then company will suffer big losses.

Time and resource consuming: Budgetary control is a best tool but it consumes a lot of

time and also consumes resources, as experts are hired. which turns into its disadvantage

Budgets Revision: With the change in scenario Budgets are revised which leads to more

resource consumptions and increases administration cost.

Constraint for managerial initiative: managers try to keep the cost as low as possible to

achieve the budgetary figures and when this happens they are not able to exercise their

managerial innovations (Contrafatto, . and Burns,2013).

Develops Conflicts: Every line manager wants more resource for his department in while

M3. Preparation and forecasting of budget.

It is essential for a company is that they make their budget in an effective way. It required

pre planning and there are various factors involved which can be influenced such budget. As a

manager of the firm they required to study all these factors carefully which can help to evaluate

budget in an effective manner. It is systematic process where the income and expenditure

calculated. In the next stage they frame the target which are related with the income and

expenditure. The cited business unit is required that to forecast all factors and elements so that

they can make their budget and attain its desired goals and objectives (van 2011).

11

Task 4

P5. Adaption of Management Accounting System during financial problem.

A management accounting system is basically the process in which all the financial data from the

business operations which includes changes in raw material cost, or shifts in inventory, etc. is

being collected and then converted to analyse reports and helps the managers to take productive

decisions. After collection of the required information it is being checked by managers who will

understand the given matter and the accounts and will then send all of it to the organisation. All

the data send to the organisation will help the management in improving their performance

(Albelda,2011.). To select management accounting system is always considered as an intelligent

business decision as it integrates with the financial accounting system of a company. This system

is generally used to prepare budgets and also in planning various functions by the managers.

Budgets for the various periods are made and then the budgets of the past are compared with the

current period budgets and are analysed and through this a comparison of information which

shows data related to sales revenue and all other expenses will required to be done. In

management accounting data is accurate, is also arranged in a sequential order and the most

important always ensures timely information. Due to all these features of management

accounting system a business has an advantage of cutting excessive costs, streamlining

operations procedure and also helps in building capital for future business expansion. It should

be flexible and fast so that data can be easily accessible to the authority and also any change in

companies external or internal factors can be made while practising it. Various financial

problems are faced by an organisation but very few of them know that these problems can be

solved by adapting their business design, policies and strategies. They all usually fail in adapting

the management accounting systems. To solve these problems every company has its own ways

and tools.

UNICORN GROCERY BEANIES WHOLEFOODS

Variance analysis is a tool in which difference

in planned budget and actual budget is

analysed and investigated. This and such other

In order to get good results beanies holding is

using various tools of management accounting.

Various products are being manufactured by

12

P5. Adaption of Management Accounting System during financial problem.

A management accounting system is basically the process in which all the financial data from the

business operations which includes changes in raw material cost, or shifts in inventory, etc. is

being collected and then converted to analyse reports and helps the managers to take productive

decisions. After collection of the required information it is being checked by managers who will

understand the given matter and the accounts and will then send all of it to the organisation. All

the data send to the organisation will help the management in improving their performance

(Albelda,2011.). To select management accounting system is always considered as an intelligent

business decision as it integrates with the financial accounting system of a company. This system

is generally used to prepare budgets and also in planning various functions by the managers.

Budgets for the various periods are made and then the budgets of the past are compared with the

current period budgets and are analysed and through this a comparison of information which

shows data related to sales revenue and all other expenses will required to be done. In

management accounting data is accurate, is also arranged in a sequential order and the most

important always ensures timely information. Due to all these features of management

accounting system a business has an advantage of cutting excessive costs, streamlining

operations procedure and also helps in building capital for future business expansion. It should

be flexible and fast so that data can be easily accessible to the authority and also any change in

companies external or internal factors can be made while practising it. Various financial

problems are faced by an organisation but very few of them know that these problems can be

solved by adapting their business design, policies and strategies. They all usually fail in adapting

the management accounting systems. To solve these problems every company has its own ways

and tools.

UNICORN GROCERY BEANIES WHOLEFOODS

Variance analysis is a tool in which difference

in planned budget and actual budget is

analysed and investigated. This and such other

In order to get good results beanies holding is

using various tools of management accounting.

Various products are being manufactured by

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.