Management Accounting Report: Financial Analysis of Creams Limited

VerifiedAdded on 2023/01/11

|18

|4466

|44

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices applied to Creams Limited, a medium-sized food and beverage company. It begins with an introduction to management accounting, differentiating it from financial accounting, and explores various systems like price optimization, cost accounting, and inventory management. The report then delves into the methods used for managing accounting reporting, including budgeting, accounts receivable, inventory, performance, and department reports. It highlights the benefits of adopting a management accounting system and the impact of integrating management reports with the accounting system. The core of the report focuses on revenue statements using managerial accounting techniques, such as marginal and absorption costing, along with a detailed analysis of financial data. Furthermore, it examines the benefits and drawbacks of managerial planning tools, emphasizing their importance in budgeting and forecasting. The report concludes by studying how managerial accounting tools can be applied to solve financial problems, offering insights into how these tools can lead organizations to sustainable success and evaluating how planning tools help overcome financial challenges. The report uses examples and calculations to demonstrate how the concepts are applied.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................3

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Understanding of Management accounting system................................................................4

P2 Methods used for managing accounting reporting.................................................................6

M1 Benefits of adopting management accounting system..........................................................7

D1 Impact of integration of management report and accounting system..................................8

TASK 2............................................................................................................................................8

P3 Revenue statement applying managerial accounting techniques...........................................8

D2 Analysis of data by financial report.....................................................................................12

TASK 3..........................................................................................................................................12

P4 understanding of benefit and drawbacks of managerial planning tools...............................12

M3 Importance of planning tools for budgeting and forecasting process.................................14

TASK 4..........................................................................................................................................15

P5 detail study of how managerial accounting tool apply to solve financial problem..............15

M4 Interpretation of how, in responding to financial problems, management accounting can

lead organizations to sustainable success..................................................................................16

D3 Evaluation of how planning tools for accounting to overcome financial problems to lead

organizations to success.............................................................................................................16

CONCLUSION..............................................................................................................................17

REFRENCES.................................................................................................................................18

Contents...........................................................................................................................................3

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Understanding of Management accounting system................................................................4

P2 Methods used for managing accounting reporting.................................................................6

M1 Benefits of adopting management accounting system..........................................................7

D1 Impact of integration of management report and accounting system..................................8

TASK 2............................................................................................................................................8

P3 Revenue statement applying managerial accounting techniques...........................................8

D2 Analysis of data by financial report.....................................................................................12

TASK 3..........................................................................................................................................12

P4 understanding of benefit and drawbacks of managerial planning tools...............................12

M3 Importance of planning tools for budgeting and forecasting process.................................14

TASK 4..........................................................................................................................................15

P5 detail study of how managerial accounting tool apply to solve financial problem..............15

M4 Interpretation of how, in responding to financial problems, management accounting can

lead organizations to sustainable success..................................................................................16

D3 Evaluation of how planning tools for accounting to overcome financial problems to lead

organizations to success.............................................................................................................16

CONCLUSION..............................................................................................................................17

REFRENCES.................................................................................................................................18

INTRODUCTION

Management accounting the word is a combination of 2 different elements of business,

management is a process of influencing workforce to done their work in order to achieve goal of

organization on the other hand accounting is a process of presenting accounting data in effective

way, thus management accounting refers as a systematic framework which provides accounting

information in an effective which help in formulating polices, planning, and controlling

operational activities of organization (Cescon, Costantini and Grassetti, 2019). This report is

prepared for solving issues of Creams Limited, it is medium size organization which provides

foods and beverage items to their customers. In this report uses of cost, price job accounting

system for formulating of policies, various report use for performance evolution has been

describe. This report also included technique which helps in reorganization of profits and tools

used for identification of reason of financial problems and ways through which organization can

overcome this problem has been defined clearly.

TASK 1

P1 Understanding of Management accounting system.

Management accounting is a framework which helps in representing accounting data in

order to formulate strategic plans for attaining future goals of business organization (Agustia,

Sawarjuwono and Dianawati, 2019).

Financial Accounting: It is a branch of accounting which is related with recording,

summarizing and communicating only financial transactions (Weygandt, Kimmel and Kieso,

2019).

Difference between management accounting and financial accounting

Management Accounting Financial Accounting

It provides information for internal parties It provides information for external parties

It is futuristic In this accounting historical data a use for

interpretation

It measure financial and operation

performance

It measure only financial information.

Management accounting the word is a combination of 2 different elements of business,

management is a process of influencing workforce to done their work in order to achieve goal of

organization on the other hand accounting is a process of presenting accounting data in effective

way, thus management accounting refers as a systematic framework which provides accounting

information in an effective which help in formulating polices, planning, and controlling

operational activities of organization (Cescon, Costantini and Grassetti, 2019). This report is

prepared for solving issues of Creams Limited, it is medium size organization which provides

foods and beverage items to their customers. In this report uses of cost, price job accounting

system for formulating of policies, various report use for performance evolution has been

describe. This report also included technique which helps in reorganization of profits and tools

used for identification of reason of financial problems and ways through which organization can

overcome this problem has been defined clearly.

TASK 1

P1 Understanding of Management accounting system.

Management accounting is a framework which helps in representing accounting data in

order to formulate strategic plans for attaining future goals of business organization (Agustia,

Sawarjuwono and Dianawati, 2019).

Financial Accounting: It is a branch of accounting which is related with recording,

summarizing and communicating only financial transactions (Weygandt, Kimmel and Kieso,

2019).

Difference between management accounting and financial accounting

Management Accounting Financial Accounting

It provides information for internal parties It provides information for external parties

It is futuristic In this accounting historical data a use for

interpretation

It measure financial and operation

performance

It measure only financial information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For formulation of various strategies manager needs to use some specific system of this

branch of accounting, these are described below:

Price Optimising System: This system is used to define various types of pricing

strategies an organization can use for selling their products. Manager will take

decision regarding their product prices on the basis of their organizations needs and

the cost incurred during the whole process of converting raw material into final

product. Organization can use price retraction, price skimming, and cost of pricing,

discounting strategies of price they decide it on the basis of scanning their

competitor industries, external factors and future objective of organization. It also

depends on the product life cycle as well as industrial life cycle of the organization.

The main requirement of this system is to ascertain behavioural change among

consumers due to performing the act of price change. This help to attract new

potential consumers.

Cost Accounting system: It is a framework which provides various types of

technique though which organization can easily evaluate cost incurring during their

production process by the uses of this system manager can evaluate activities which

incurred high rate of expenses (Hasyim and Jabid, 2019). Job costing, process

costing, marginal and standard costing are part of this system. Business

organization applies system of cost on their basis of their size, external as well as

internal factors of the organization. Process costing is used for mostly

manufacturing units, marginal and standard costing can be adopted by any type of

organization theses technique help in determining of profits as well as risk factor of

the enterprises. The main requirement of this system is to ascertain costing

associated with production of each unit so further actions can be taken to minimise

expenses and costings.

Inventory Management System: Inventory is most essential part of every

organization success of an enterprise depends on how effectively their manager use

and maintain stock in effective way (Swafford and Costello, RTC Ind Inc, 2019).

For this purpose, inventory management system has to been developed through

which organization can plan, manage and control stock. By the uses of EOQ, LIFO,

FIFO, method managers calculate maximum, minimum, and dangers level of

branch of accounting, these are described below:

Price Optimising System: This system is used to define various types of pricing

strategies an organization can use for selling their products. Manager will take

decision regarding their product prices on the basis of their organizations needs and

the cost incurred during the whole process of converting raw material into final

product. Organization can use price retraction, price skimming, and cost of pricing,

discounting strategies of price they decide it on the basis of scanning their

competitor industries, external factors and future objective of organization. It also

depends on the product life cycle as well as industrial life cycle of the organization.

The main requirement of this system is to ascertain behavioural change among

consumers due to performing the act of price change. This help to attract new

potential consumers.

Cost Accounting system: It is a framework which provides various types of

technique though which organization can easily evaluate cost incurring during their

production process by the uses of this system manager can evaluate activities which

incurred high rate of expenses (Hasyim and Jabid, 2019). Job costing, process

costing, marginal and standard costing are part of this system. Business

organization applies system of cost on their basis of their size, external as well as

internal factors of the organization. Process costing is used for mostly

manufacturing units, marginal and standard costing can be adopted by any type of

organization theses technique help in determining of profits as well as risk factor of

the enterprises. The main requirement of this system is to ascertain costing

associated with production of each unit so further actions can be taken to minimise

expenses and costings.

Inventory Management System: Inventory is most essential part of every

organization success of an enterprise depends on how effectively their manager use

and maintain stock in effective way (Swafford and Costello, RTC Ind Inc, 2019).

For this purpose, inventory management system has to been developed through

which organization can plan, manage and control stock. By the uses of EOQ, LIFO,

FIFO, method managers calculate maximum, minimum, and dangers level of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventories these methods use for proper managing of stock item of organization.

With the implementation of ABC, JIT analysis technique managers can maintain

records of all the elements of stock, it will help in controlling cost and wastage of

inventories within the workplace. This system has main requirement related to

effective management of inventory so able to complete the actions properly on

time.

P2 Methods used for managing accounting reporting

Managerial accounting reports are prepared by manager in order to collect essential

information data for formulating future polices will help in decision making process (Carini,

Giacomini and Teodori, 2019). Following are the reports manager of Creams limited will be

used:

Budgeting report: This report defines the overall summery of various types of

budget made by managers it includes, production, purchase, manufacturing and

master budget for the organization, it includes main essential elements of all the

budgets, for example this report provide brief summary of total revenue,

expenditure, cost of manufacturing products, total items of purchasing of raw

material, selling units etc. With the use of this report manager can analysis their

organization performance and it will help in risk management also

Account receivable report: This report is very necessary for organization in order

to maintain their position and increase cash inflow, manager of Cream limited will

use account receivable report for take record regarding their receivable account,

this report is used for formulating and managing debtor policy of the organization

(Ajanaku and Ekundayo, 2019). It will provide information related to number of

default debtor, available in present time period, amount of cash has so been taken

from debtor’s reason of delay in payment by potential debtors and also number of

non-performing assets within the organization. By using all the relevant

information manager of Creams limited may prepared rigid polices for their

account receivable they can sue case or charge penalties for late payment of their

selling product. This report also used to identify main target market customer

which is faithful to the organization.

With the implementation of ABC, JIT analysis technique managers can maintain

records of all the elements of stock, it will help in controlling cost and wastage of

inventories within the workplace. This system has main requirement related to

effective management of inventory so able to complete the actions properly on

time.

P2 Methods used for managing accounting reporting

Managerial accounting reports are prepared by manager in order to collect essential

information data for formulating future polices will help in decision making process (Carini,

Giacomini and Teodori, 2019). Following are the reports manager of Creams limited will be

used:

Budgeting report: This report defines the overall summery of various types of

budget made by managers it includes, production, purchase, manufacturing and

master budget for the organization, it includes main essential elements of all the

budgets, for example this report provide brief summary of total revenue,

expenditure, cost of manufacturing products, total items of purchasing of raw

material, selling units etc. With the use of this report manager can analysis their

organization performance and it will help in risk management also

Account receivable report: This report is very necessary for organization in order

to maintain their position and increase cash inflow, manager of Cream limited will

use account receivable report for take record regarding their receivable account,

this report is used for formulating and managing debtor policy of the organization

(Ajanaku and Ekundayo, 2019). It will provide information related to number of

default debtor, available in present time period, amount of cash has so been taken

from debtor’s reason of delay in payment by potential debtors and also number of

non-performing assets within the organization. By using all the relevant

information manager of Creams limited may prepared rigid polices for their

account receivable they can sue case or charge penalties for late payment of their

selling product. This report also used to identify main target market customer

which is faithful to the organization.

Inventory report: This report is formulated on the basis of data collected from

various inventory management techniques it is used ABC, JIT and records of

inventory document for formation of inventory report. Manager of Creams limited

must be used this report for providing a report which define detail summery of

stock calculation, verification process of inventory cycle and methods use of

measuring of stock value and managing stock has been describe briefly it will help

in analysing performance of company and build effective policy of inventory

regarding future.

Performance report: This report is used for evaluation of performance and help

identification of each employee performance on the basis of their work.

Performance report is parodied summery related to the work performance of

departments as well as their well employees (Douriez, Messmerand Raffin, 2019).

It will help in taken decision regarding bonus or promotion or provide prestigious

benefits to their skilled employees. It will help in enhancing motivation of

workforce also this report is useful for decision making regarding divide

distribution. Manager of Creams limited will use this technique for analysing

performance and taken decision regarding distribution of profits.

Department report: This report has been formulated to record all the essential

information regarding each department of organization. M manager of Creams

limited formulated this reports it will help them to identify performance of each

department, and also it is beneficial for supervision of all activities of department.

This report helps them to analysis whatever all department work with coordination

or not breaching any ethics and law of constitution.

M1 Benefits of adopting management accounting system

Management accounting system includes cost, price job, inventory account system which

will uses for providing relevant information as well as they are helpful in control cost, managing

all activities and provide guideline for future activities (Calza, Goedhuys and Trifković, 2019).

Manager of Cream limited use all these method and tools of management accounting for gain

profits.

various inventory management techniques it is used ABC, JIT and records of

inventory document for formation of inventory report. Manager of Creams limited

must be used this report for providing a report which define detail summery of

stock calculation, verification process of inventory cycle and methods use of

measuring of stock value and managing stock has been describe briefly it will help

in analysing performance of company and build effective policy of inventory

regarding future.

Performance report: This report is used for evaluation of performance and help

identification of each employee performance on the basis of their work.

Performance report is parodied summery related to the work performance of

departments as well as their well employees (Douriez, Messmerand Raffin, 2019).

It will help in taken decision regarding bonus or promotion or provide prestigious

benefits to their skilled employees. It will help in enhancing motivation of

workforce also this report is useful for decision making regarding divide

distribution. Manager of Creams limited will use this technique for analysing

performance and taken decision regarding distribution of profits.

Department report: This report has been formulated to record all the essential

information regarding each department of organization. M manager of Creams

limited formulated this reports it will help them to identify performance of each

department, and also it is beneficial for supervision of all activities of department.

This report helps them to analysis whatever all department work with coordination

or not breaching any ethics and law of constitution.

M1 Benefits of adopting management accounting system

Management accounting system includes cost, price job, inventory account system which

will uses for providing relevant information as well as they are helpful in control cost, managing

all activities and provide guideline for future activities (Calza, Goedhuys and Trifković, 2019).

Manager of Cream limited use all these method and tools of management accounting for gain

profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1 Impact of integration of management report and accounting system

This is very essential for the manager of Creams limited to integrate report ad system of

manager accountant only then they can formulate policies and work in an effective manner by

using information of accounting system reports are prepared which provides direction to

formulate strategies this interaction of management reporting and management accounting

system are essential for achieve goal of the organization (Aureli, Del Baldo and Lombardi,

2019).

TASK 2

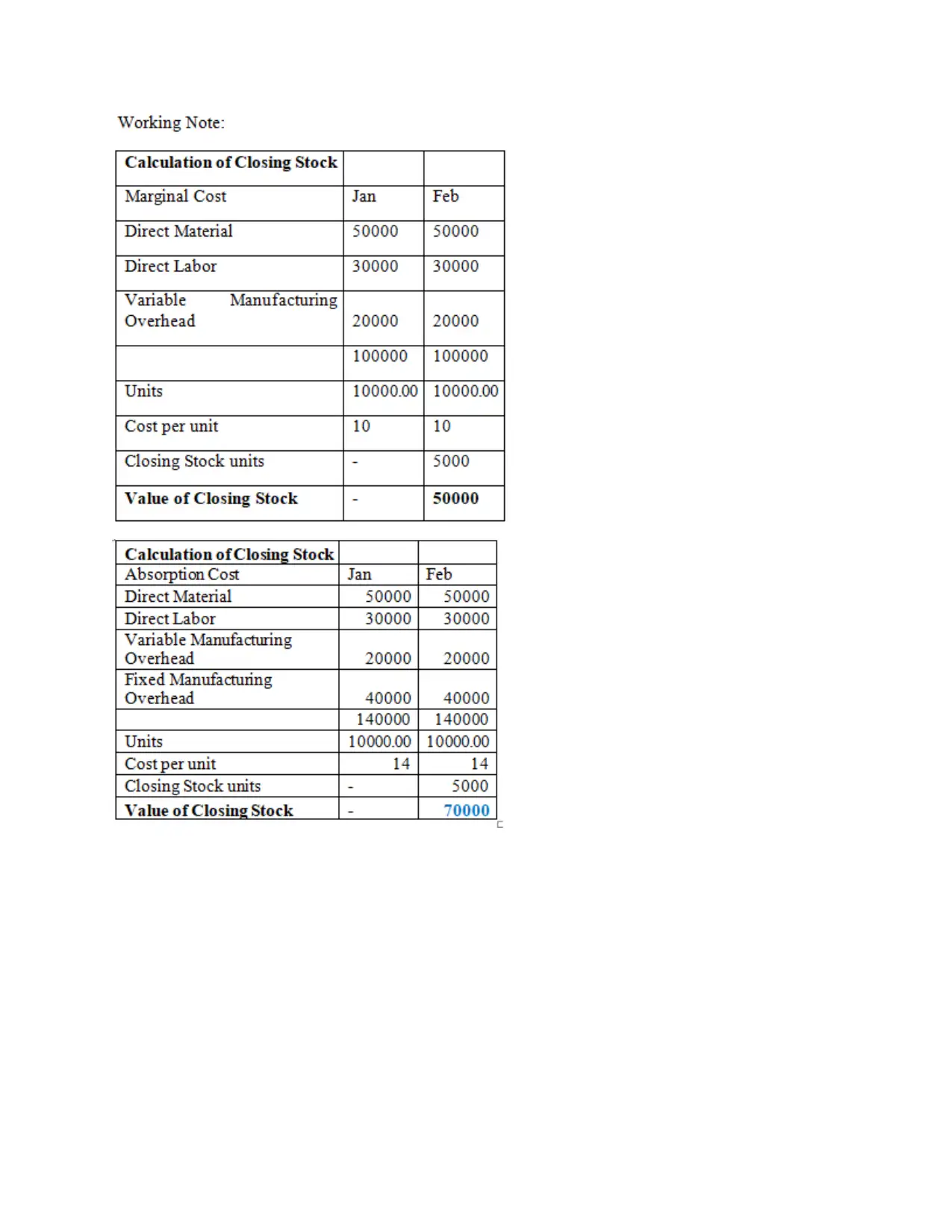

P3 Revenue statement applying managerial accounting techniques

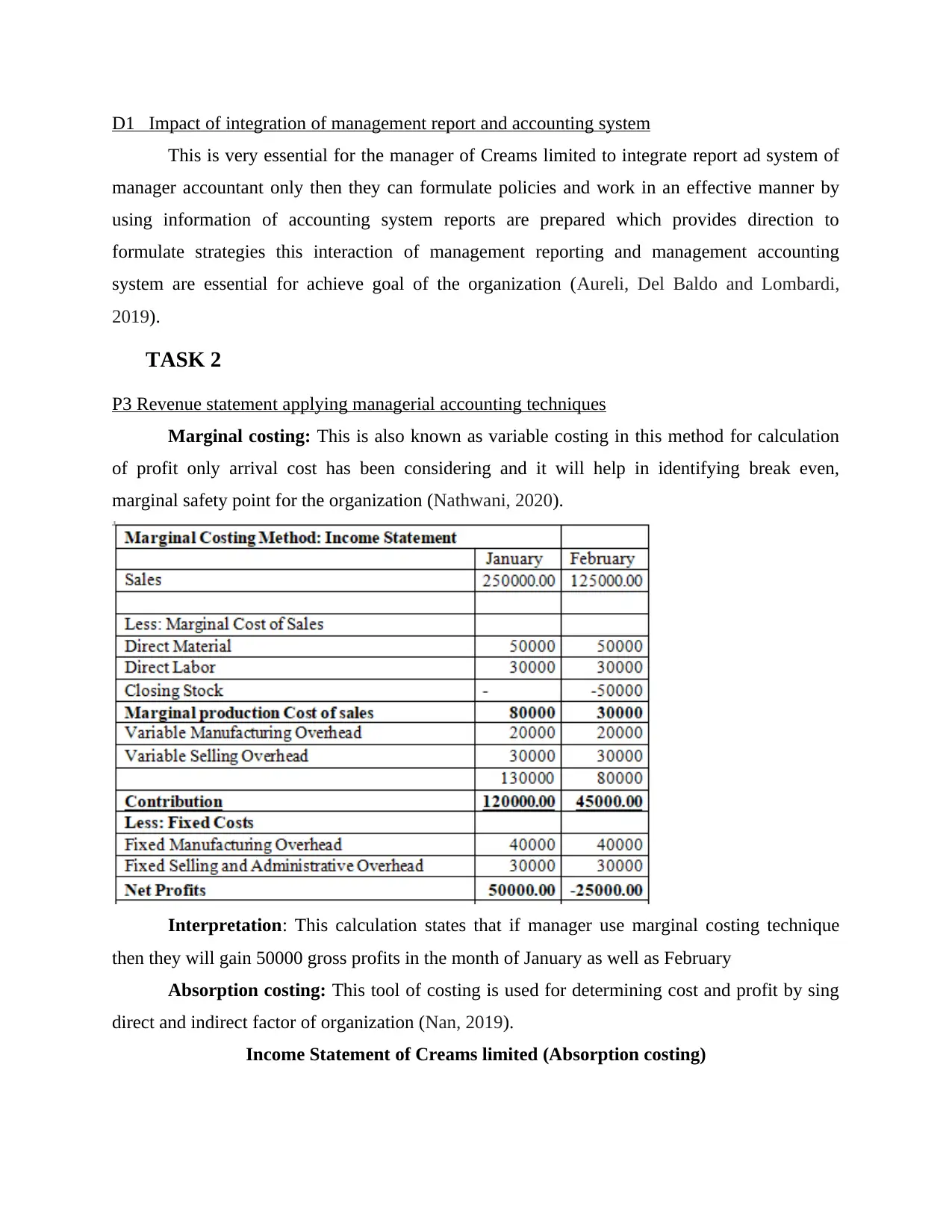

Marginal costing: This is also known as variable costing in this method for calculation

of profit only arrival cost has been considering and it will help in identifying break even,

marginal safety point for the organization (Nathwani, 2020).

Interpretation: This calculation states that if manager use marginal costing technique

then they will gain 50000 gross profits in the month of January as well as February

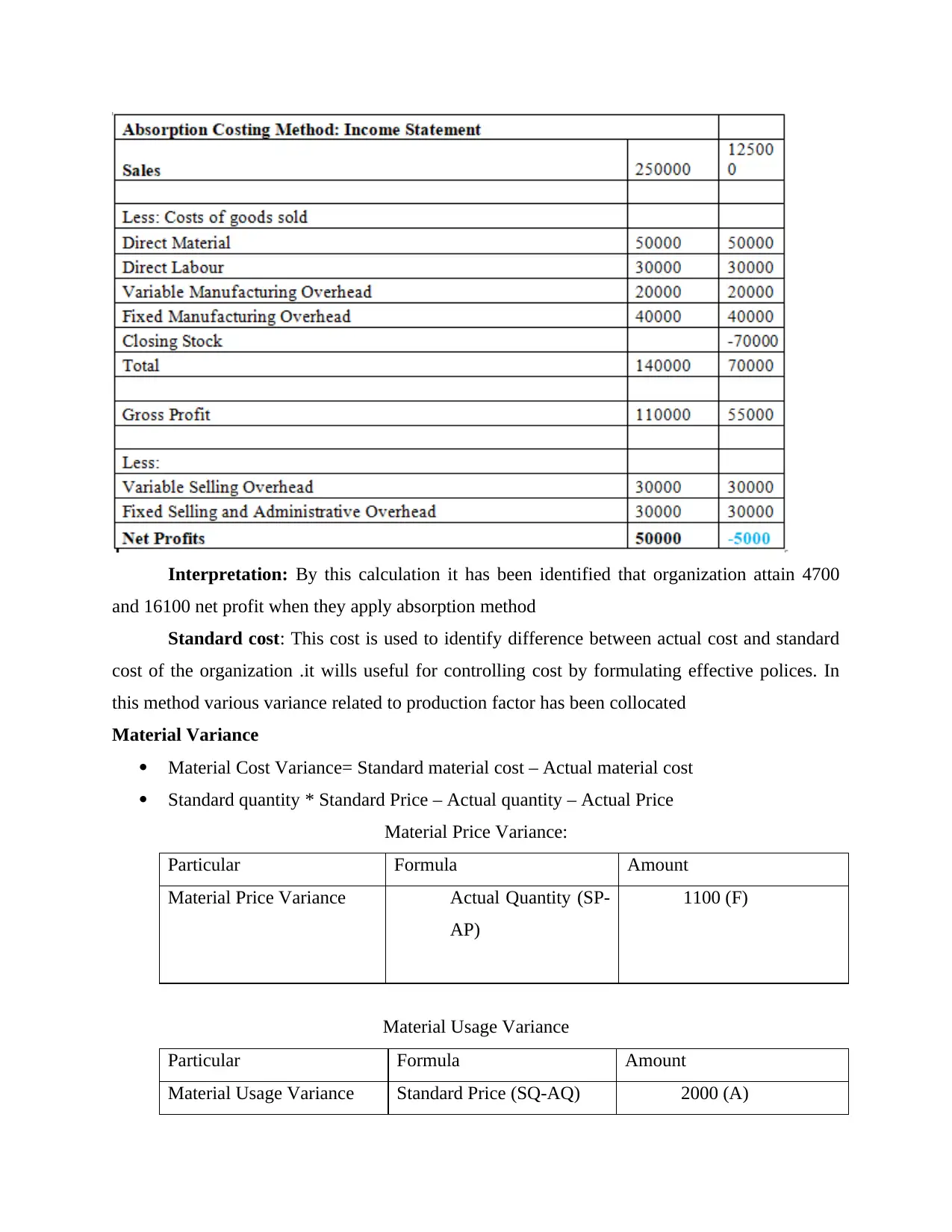

Absorption costing: This tool of costing is used for determining cost and profit by sing

direct and indirect factor of organization (Nan, 2019).

Income Statement of Creams limited (Absorption costing)

This is very essential for the manager of Creams limited to integrate report ad system of

manager accountant only then they can formulate policies and work in an effective manner by

using information of accounting system reports are prepared which provides direction to

formulate strategies this interaction of management reporting and management accounting

system are essential for achieve goal of the organization (Aureli, Del Baldo and Lombardi,

2019).

TASK 2

P3 Revenue statement applying managerial accounting techniques

Marginal costing: This is also known as variable costing in this method for calculation

of profit only arrival cost has been considering and it will help in identifying break even,

marginal safety point for the organization (Nathwani, 2020).

Interpretation: This calculation states that if manager use marginal costing technique

then they will gain 50000 gross profits in the month of January as well as February

Absorption costing: This tool of costing is used for determining cost and profit by sing

direct and indirect factor of organization (Nan, 2019).

Income Statement of Creams limited (Absorption costing)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: By this calculation it has been identified that organization attain 4700

and 16100 net profit when they apply absorption method

Standard cost: This cost is used to identify difference between actual cost and standard

cost of the organization .it wills useful for controlling cost by formulating effective polices. In

this method various variance related to production factor has been collocated

Material Variance

Material Cost Variance= Standard material cost – Actual material cost

Standard quantity * Standard Price – Actual quantity – Actual Price

Material Price Variance:

Particular Formula Amount

Material Price Variance Actual Quantity (SP-

AP)

1100 (F)

Material Usage Variance

Particular Formula Amount

Material Usage Variance Standard Price (SQ-AQ) 2000 (A)

and 16100 net profit when they apply absorption method

Standard cost: This cost is used to identify difference between actual cost and standard

cost of the organization .it wills useful for controlling cost by formulating effective polices. In

this method various variance related to production factor has been collocated

Material Variance

Material Cost Variance= Standard material cost – Actual material cost

Standard quantity * Standard Price – Actual quantity – Actual Price

Material Price Variance:

Particular Formula Amount

Material Price Variance Actual Quantity (SP-

AP)

1100 (F)

Material Usage Variance

Particular Formula Amount

Material Usage Variance Standard Price (SQ-AQ) 2000 (A)

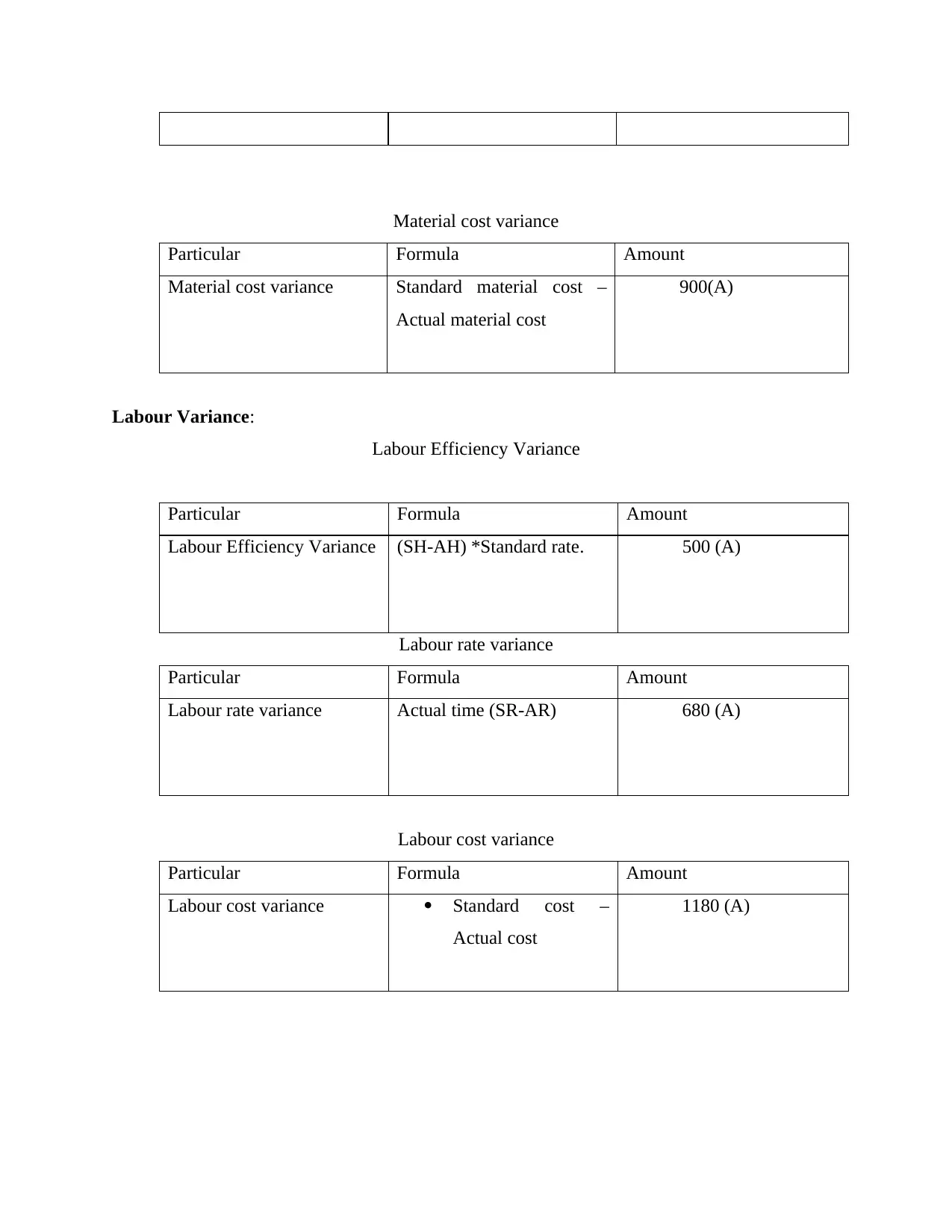

Material cost variance

Particular Formula Amount

Material cost variance Standard material cost –

Actual material cost

900(A)

Labour Variance:

Labour Efficiency Variance

Particular Formula Amount

Labour Efficiency Variance (SH-AH) *Standard rate. 500 (A)

Labour rate variance

Particular Formula Amount

Labour rate variance Actual time (SR-AR) 680 (A)

Labour cost variance

Particular Formula Amount

Labour cost variance Standard cost –

Actual cost

1180 (A)

Particular Formula Amount

Material cost variance Standard material cost –

Actual material cost

900(A)

Labour Variance:

Labour Efficiency Variance

Particular Formula Amount

Labour Efficiency Variance (SH-AH) *Standard rate. 500 (A)

Labour rate variance

Particular Formula Amount

Labour rate variance Actual time (SR-AR) 680 (A)

Labour cost variance

Particular Formula Amount

Labour cost variance Standard cost –

Actual cost

1180 (A)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

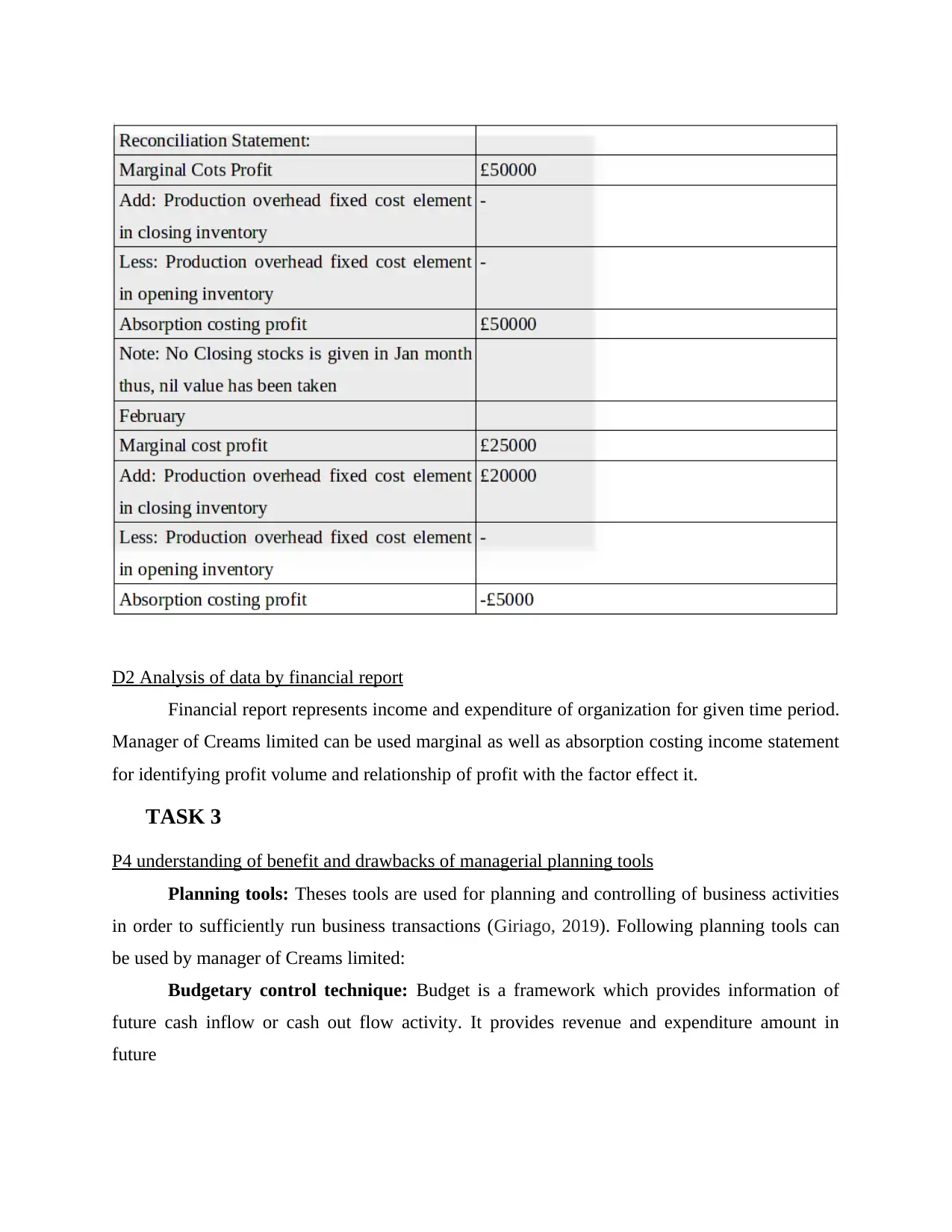

D2 Analysis of data by financial report

Financial report represents income and expenditure of organization for given time period.

Manager of Creams limited can be used marginal as well as absorption costing income statement

for identifying profit volume and relationship of profit with the factor effect it.

TASK 3

P4 understanding of benefit and drawbacks of managerial planning tools

Planning tools: Theses tools are used for planning and controlling of business activities

in order to sufficiently run business transactions (Giriago, 2019). Following planning tools can

be used by manager of Creams limited:

Budgetary control technique: Budget is a framework which provides information of

future cash inflow or cash out flow activity. It provides revenue and expenditure amount in

future

Financial report represents income and expenditure of organization for given time period.

Manager of Creams limited can be used marginal as well as absorption costing income statement

for identifying profit volume and relationship of profit with the factor effect it.

TASK 3

P4 understanding of benefit and drawbacks of managerial planning tools

Planning tools: Theses tools are used for planning and controlling of business activities

in order to sufficiently run business transactions (Giriago, 2019). Following planning tools can

be used by manager of Creams limited:

Budgetary control technique: Budget is a framework which provides information of

future cash inflow or cash out flow activity. It provides revenue and expenditure amount in

future

Zero Base Budgets: Theses budgets are prepared on the basis of deep research of

external and internal factors affecting the organization, it collects data from initial level thus it is

called zero bade budget, which is starting from scratch level (Ibrahim, 2019). Following are the

advantage and disadvantage of adopting this method for preparation of budget:

Advantages

Zero based budget help in provide relevant and accurate information regarding future.

Manager of Creams limited use it budgetary control because help to get reliable

information.

This method is helpful in utilization of resources through which possible to build reliable

accounts

Disadvantage

Having deep research take time as it started from zero level.

It requires to hire skilled and experience researcher for formulating budget.

Rolling Budget: This type of budget in formulated for short time period, less than one

year it. Rolling budget is techniques of budgeting in which budgets are prepared on continuous

basis when period of a budget competes then another budget is formulated on the basis of data

collected from previous budget to remove errors of previous budget.

Advantages

Rolling budget help in enhancing efficiency of organization as aid in getting of regular

amount of information.

Manager of Creams limited it will improve productivity of the organization and aid in in

performance of regular functioning.

Disadvantage

Employees get frustrated due to changes of policies and more flexibility in work force.

It is time consuming process.

Activity Base Budget: This type of budgeting technique includes making budget on the

basis of allocation of cost of each activity of the organization (Pagare, 2020).

Advantages

external and internal factors affecting the organization, it collects data from initial level thus it is

called zero bade budget, which is starting from scratch level (Ibrahim, 2019). Following are the

advantage and disadvantage of adopting this method for preparation of budget:

Advantages

Zero based budget help in provide relevant and accurate information regarding future.

Manager of Creams limited use it budgetary control because help to get reliable

information.

This method is helpful in utilization of resources through which possible to build reliable

accounts

Disadvantage

Having deep research take time as it started from zero level.

It requires to hire skilled and experience researcher for formulating budget.

Rolling Budget: This type of budget in formulated for short time period, less than one

year it. Rolling budget is techniques of budgeting in which budgets are prepared on continuous

basis when period of a budget competes then another budget is formulated on the basis of data

collected from previous budget to remove errors of previous budget.

Advantages

Rolling budget help in enhancing efficiency of organization as aid in getting of regular

amount of information.

Manager of Creams limited it will improve productivity of the organization and aid in in

performance of regular functioning.

Disadvantage

Employees get frustrated due to changes of policies and more flexibility in work force.

It is time consuming process.

Activity Base Budget: This type of budgeting technique includes making budget on the

basis of allocation of cost of each activity of the organization (Pagare, 2020).

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.