Accounting for Managers Project Report: Financial Performance Analysis

VerifiedAdded on 2023/06/07

|7

|967

|264

Report

AI Summary

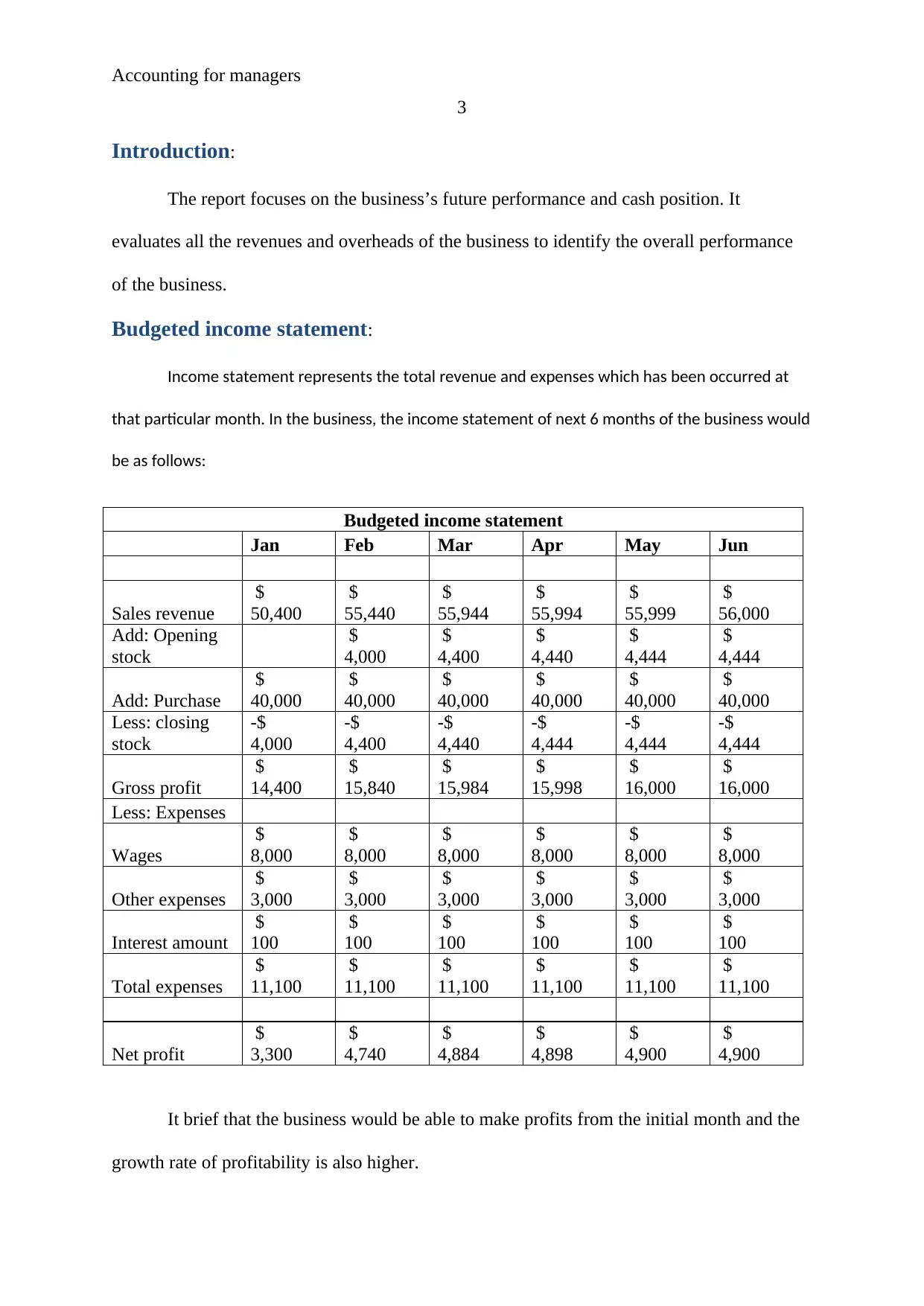

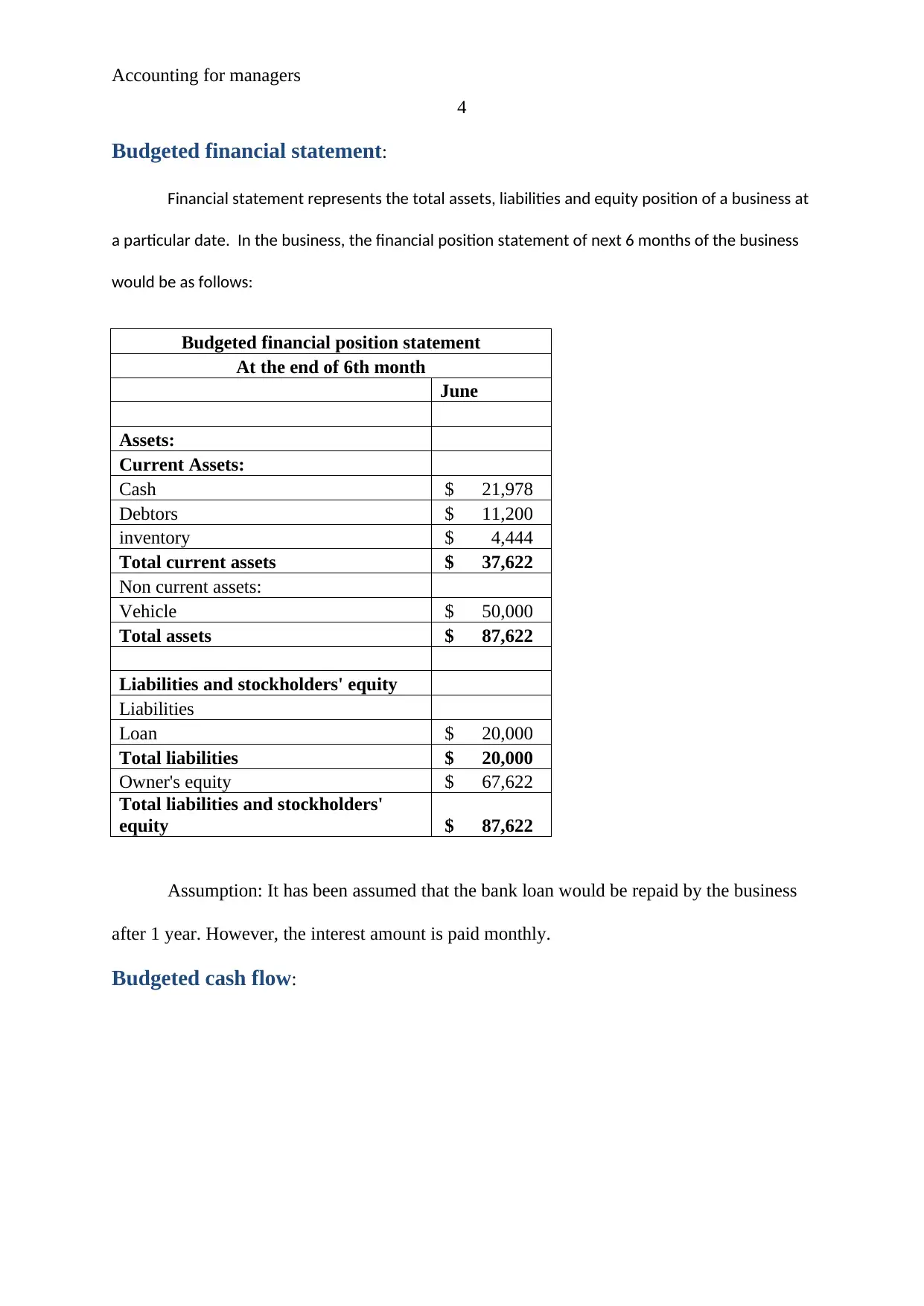

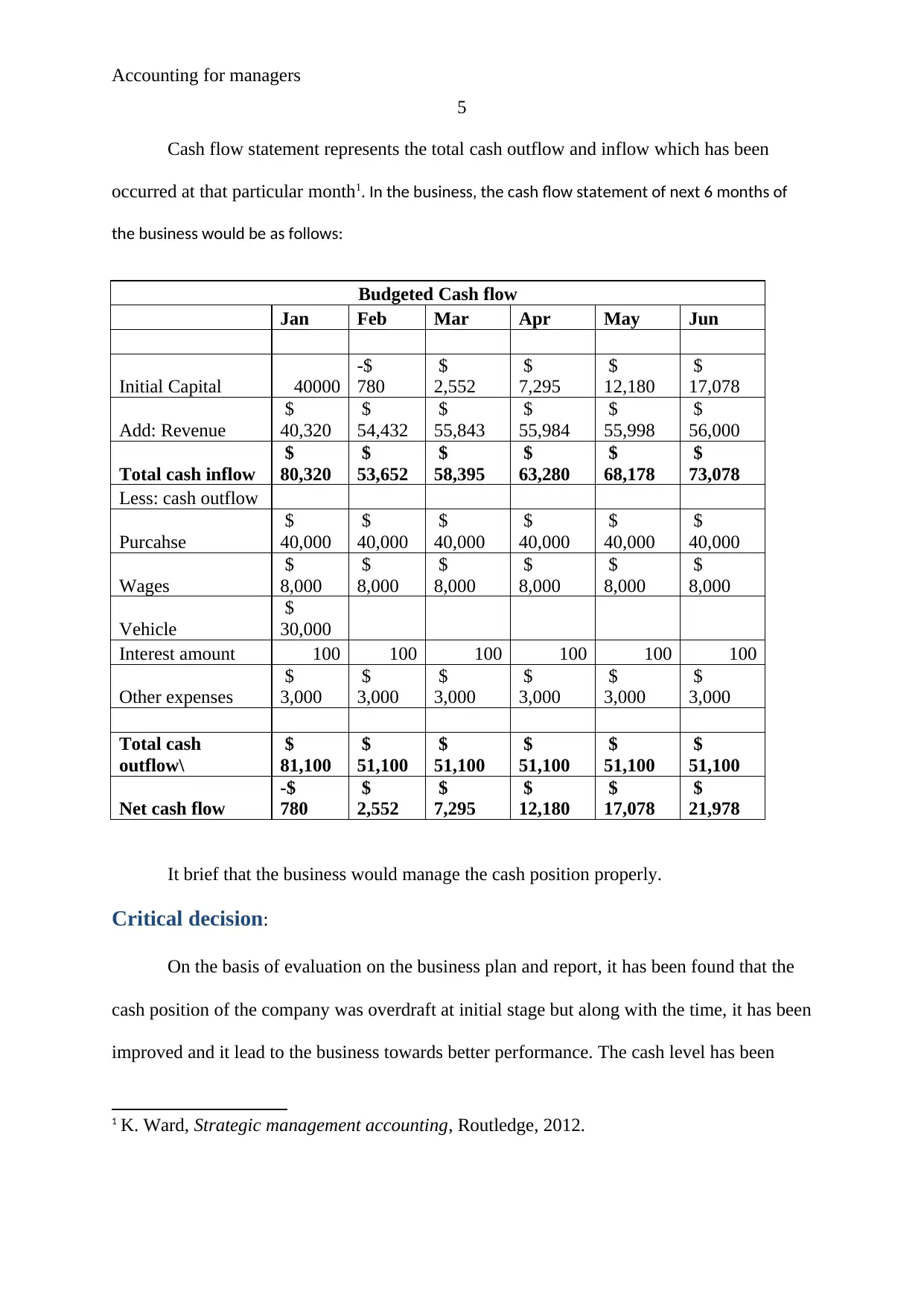

This project report for Accounting for Managers analyzes a business's future financial performance and cash position. It includes a budgeted income statement projecting revenues and expenses over six months, demonstrating profitability and growth. A budgeted financial position statement outlines the assets, liabilities, and equity at the end of the period. Furthermore, a budgeted cash flow statement details cash inflows and outflows, highlighting the company's ability to manage its cash effectively. The report identifies a critical decision regarding cash flow management, specifically the timing of payments to creditors and receipts from debtors, and recommends adjusting payment terms to improve the company's cash position and working capital requirements. References to relevant accounting literature are also included.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.