Financial Accounting Report: Regulations and Client Account Analysis

VerifiedAdded on 2020/11/12

|37

|5577

|390

Report

AI Summary

This financial accounting report begins with an introduction to financial accounting, emphasizing its role in building strong capital structures and managing financial operations. It then delves into accounting regulations, principles, and frameworks, including GAAP, IFRS, and IASB. The report presents several client case studies, each involving the preparation of various financial statements such as journal entries, ledger accounts, trial balances, balance sheets, and bank reconciliation statements. It covers topics like income statements, financial position statements, and the purpose of depreciation. The report also addresses concepts like material disclosure, consistency, and the preparation of control accounts and suspense accounts. The report concludes with a discussion on different types of accounts used for framing reconciliation and methods of accounting. The report aims to provide a comprehensive understanding of financial accounting practices and their applications in real-world scenarios, offering valuable insights into financial analysis and reporting.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Ascertaining the regulations relevant with accounting as discussed in report..................1

1 Financial accounting............................................................................................................2

2.Regulations relevant with financial accounting..................................................................2

3. Rule and regulations of accounting....................................................................................4

4. Concepts of material disclosure and consistency...............................................................5

b. Accounting measurements for portfolio clients.................................................................6

CLIENT 1........................................................................................................................................6

1. Preparing the book of prime entries for Alexandra Study..................................................6

2. Computing double entry recording with the help of ledger accounts................................9

3. Completion of each accounts with a contrast of drawing trial balance for 31st January 2018

..............................................................................................................................................17

M1 Ascertainment of several transactions compiled in Trial balance.................................18

D1 Records of all transactions in Trial balance....................................................................18

CLIENT 2......................................................................................................................................18

A. Drafting income statement for Peter Piper 31st December 2017....................................18

B. Preparing financial position statements for Peter Piper as on 31st December 2017.......19

CLIENT 3......................................................................................................................................20

A. Preparation of income statement for Raintree Ltd...........................................................20

B. Preparing balance sheet for Raintree Ltd as on 31st December 2017.............................21

C. Discussion over accounting concepts such as prudency and consistency.......................25

D. Purpose of formulating depreciation in accounting statements as well as calculating it with

various methods....................................................................................................................26

M2 Evaluating the P&L account, cash flow statement as well as balance sheet of firm.....26

D2 Construction of final accounts based on accurate information.......................................26

CLIENT 4......................................................................................................................................27

A. Ascertaining purpose and reasons behind preparing Bank Reconciliation Statement for

Kendal Ltd............................................................................................................................27

INTRODUCTION...........................................................................................................................1

A. Ascertaining the regulations relevant with accounting as discussed in report..................1

1 Financial accounting............................................................................................................2

2.Regulations relevant with financial accounting..................................................................2

3. Rule and regulations of accounting....................................................................................4

4. Concepts of material disclosure and consistency...............................................................5

b. Accounting measurements for portfolio clients.................................................................6

CLIENT 1........................................................................................................................................6

1. Preparing the book of prime entries for Alexandra Study..................................................6

2. Computing double entry recording with the help of ledger accounts................................9

3. Completion of each accounts with a contrast of drawing trial balance for 31st January 2018

..............................................................................................................................................17

M1 Ascertainment of several transactions compiled in Trial balance.................................18

D1 Records of all transactions in Trial balance....................................................................18

CLIENT 2......................................................................................................................................18

A. Drafting income statement for Peter Piper 31st December 2017....................................18

B. Preparing financial position statements for Peter Piper as on 31st December 2017.......19

CLIENT 3......................................................................................................................................20

A. Preparation of income statement for Raintree Ltd...........................................................20

B. Preparing balance sheet for Raintree Ltd as on 31st December 2017.............................21

C. Discussion over accounting concepts such as prudency and consistency.......................25

D. Purpose of formulating depreciation in accounting statements as well as calculating it with

various methods....................................................................................................................26

M2 Evaluating the P&L account, cash flow statement as well as balance sheet of firm.....26

D2 Construction of final accounts based on accurate information.......................................26

CLIENT 4......................................................................................................................................27

A. Ascertaining purpose and reasons behind preparing Bank Reconciliation Statement for

Kendal Ltd............................................................................................................................27

B. Explaining and listing various areas which causes verification of records in bank statement

..............................................................................................................................................27

C. Referencing the cash book with preparation of various accounts...................................27

M3 Not sufficient funds and process of preparing deposits in transit..................................28

D3 Drafting accurate BRS....................................................................................................28

CLIENT 5......................................................................................................................................29

A. Balancing and preparing books of accounts for Henderson as on January 2018............29

B. Explaining terms of preparing Control accounts.............................................................29

CLIENT 6......................................................................................................................................29

A. Explaining terms and features of preparing suspense accounts......................................29

B. Preparation of Trial balance on contrast with balance of control account.......................30

C. Preparation of Journal entries with contrast of trial balance failure................................30

D. Analysing the differences between Suspense account and Clearing account.................31

M4 Types of accounts for framing reconciliation................................................................31

D4 Providing appropriate methods of accounting................................................................31

CONCLUSION .............................................................................................................................31

REFERENCES..............................................................................................................................33

..............................................................................................................................................27

C. Referencing the cash book with preparation of various accounts...................................27

M3 Not sufficient funds and process of preparing deposits in transit..................................28

D3 Drafting accurate BRS....................................................................................................28

CLIENT 5......................................................................................................................................29

A. Balancing and preparing books of accounts for Henderson as on January 2018............29

B. Explaining terms of preparing Control accounts.............................................................29

CLIENT 6......................................................................................................................................29

A. Explaining terms and features of preparing suspense accounts......................................29

B. Preparation of Trial balance on contrast with balance of control account.......................30

C. Preparation of Journal entries with contrast of trial balance failure................................30

D. Analysing the differences between Suspense account and Clearing account.................31

M4 Types of accounts for framing reconciliation................................................................31

D4 Providing appropriate methods of accounting................................................................31

CONCLUSION .............................................................................................................................31

REFERENCES..............................................................................................................................33

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the technique which will be assistive and helpful to the firm in

terms of building the strong capital structure as well as suggesting suitable way to manage

financial operations in firm. In the present report there will be discussion based on various

accounting principles and regulatory framework of financial institutions which are facilitating

appropriate accounting methods. There will be preparation of various financial accounts which

will be prepared to resolve financial issues of all clients which are here for operative decision. It

comprises with several accounts such as journal entries, ledger accounts, trial balance accounts,

balance sheet, bank reconciliation statement and suspense accounts. Therefore, such preparation

of these accounts will have positive influences as per analysing financial issues and management

of operations.

A. Ascertaining the regulations relevant with accounting as discussed in report

1

Financial accounting is the technique which will be assistive and helpful to the firm in

terms of building the strong capital structure as well as suggesting suitable way to manage

financial operations in firm. In the present report there will be discussion based on various

accounting principles and regulatory framework of financial institutions which are facilitating

appropriate accounting methods. There will be preparation of various financial accounts which

will be prepared to resolve financial issues of all clients which are here for operative decision. It

comprises with several accounts such as journal entries, ledger accounts, trial balance accounts,

balance sheet, bank reconciliation statement and suspense accounts. Therefore, such preparation

of these accounts will have positive influences as per analysing financial issues and management

of operations.

A. Ascertaining the regulations relevant with accounting as discussed in report

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From: Junior Accountant

To: Line manager

Subject: Accounting regulations, rules and principles for better financial control in business

Sir,

On contrary with analysing the operational activities of entity. Therefore, in relation

with operating accounts in premises will need a proper framework and adequate techniques in

preparing them. Discussion will be based on various accounting principles as well as

operational tools which will help in improving business efficiencies. Ascertaining appropriate

rules and regulations will be assistive in building suitable financial environment. It highlights

the methods of preparing financial statements which brings the suitable information among the

users of such accounts (Singleton-Green, 2016).

The managerial professionals as well as accounting personnel will have an appropriate

knowledge relevant with expenditures and revenues in due period. It benefits the external users

such as shareholders which seek for the appropriate disclosure of the accounts and financial

statements. They are mainly attracted towards profitability of firm as well as capital structure in

terms of making capital payments. There is a need to have an appropriate disclosure for

Achieving suitable market value for better operational practices of accounts. This will be an

assistive tool which brings control over operations.

1 Financial accounting

These are the accounts which keep records of all transactions that will be helpful and

assistive to unit in terms of making suitable strategies for operational activities as well as

suggests techniques to reduce costs implied in such activities. Administration of all financial

transactions will be collected, analysed and summarised into final accounts. It enables

accounting personnel to have the most appropriate information relevant with accounting control

and management of operations (Pawlowski, Nalbantis and Coates, 2018).

Usefulness of these accounts is that it brings information relevant with financial

operations as well as uplifts business efficiency in due course. Require information by users

such as consumers, competitors, investors as well as legal authorities which in turn analyse

operational activities of firm and make necessary operational practices in due period.

2.Regulations relevant with financial accounting

2

To: Line manager

Subject: Accounting regulations, rules and principles for better financial control in business

Sir,

On contrary with analysing the operational activities of entity. Therefore, in relation

with operating accounts in premises will need a proper framework and adequate techniques in

preparing them. Discussion will be based on various accounting principles as well as

operational tools which will help in improving business efficiencies. Ascertaining appropriate

rules and regulations will be assistive in building suitable financial environment. It highlights

the methods of preparing financial statements which brings the suitable information among the

users of such accounts (Singleton-Green, 2016).

The managerial professionals as well as accounting personnel will have an appropriate

knowledge relevant with expenditures and revenues in due period. It benefits the external users

such as shareholders which seek for the appropriate disclosure of the accounts and financial

statements. They are mainly attracted towards profitability of firm as well as capital structure in

terms of making capital payments. There is a need to have an appropriate disclosure for

Achieving suitable market value for better operational practices of accounts. This will be an

assistive tool which brings control over operations.

1 Financial accounting

These are the accounts which keep records of all transactions that will be helpful and

assistive to unit in terms of making suitable strategies for operational activities as well as

suggests techniques to reduce costs implied in such activities. Administration of all financial

transactions will be collected, analysed and summarised into final accounts. It enables

accounting personnel to have the most appropriate information relevant with accounting control

and management of operations (Pawlowski, Nalbantis and Coates, 2018).

Usefulness of these accounts is that it brings information relevant with financial

operations as well as uplifts business efficiency in due course. Require information by users

such as consumers, competitors, investors as well as legal authorities which in turn analyse

operational activities of firm and make necessary operational practices in due period.

2.Regulations relevant with financial accounting

2

It comprises with various legal regulations which in turn approaches towards

preparation of financial accounts for better operational management. Demonstrating the

requirement of preparing the financial accounts in relation with communicating the information

among external users (Samreen, 2018). Therefore, influences of various legal authorities will

have effective control over operational practices as well as management of activities.

Main motive of implicating regulations in financial operation is that the accounting

professionals are bound to prepare statements which will be prepared with considering all legal

and authentic frameworks (Regulations in Financial Accounting, 2017). It consists all details

such as recording of transactions as well as reporting the same among users. It communicates

the financial health of a business among note only domestic but also gathers international

investors for capital funding. Moreover, there are some regulatory authorities which enforces a

business in preparation of fruitful financials disclosures such as:

Generally Accepted Accounting Principles (GAAP): This organisation developed the

principles and rules of recoding accounting transactions for the specific period. Preparation of

all rules and principles will be effective and adequate as per managing operational activities of a

firm. Concepts and principles used here are the best for funnelling accounting professionals in

terms of better financial control in organisation as well as management of operational activities

(Kouki, 2018). It ascertains proper recording of all transactions in various accounts with their

appropriate methods of recoding transactions.

International Financial Reporting Standards (IFRS): These are the standards which

consists of all information that will be useful to firm in terms of preparation of statements and

accounts that will be useful and appropriate in terms of communicating financial health of entity

among external users (Bloomfield and et.al, 2017). It enables the professionals in making

appropriate decision as well as developing plans and policies as per guiding the accounting

professionals or auditors to control operational activities in business. These are international

standards which comprises with all information and techniques to prepare financial statements

for business.

International Accounting Standard Board (IASB): In accordance with operational

activities and the operational framework of IASB are based providing the accounting standard

among all the organisation. Th motive is for upgrading the accounting and book-keeping in the

3

preparation of financial accounts for better operational management. Demonstrating the

requirement of preparing the financial accounts in relation with communicating the information

among external users (Samreen, 2018). Therefore, influences of various legal authorities will

have effective control over operational practices as well as management of activities.

Main motive of implicating regulations in financial operation is that the accounting

professionals are bound to prepare statements which will be prepared with considering all legal

and authentic frameworks (Regulations in Financial Accounting, 2017). It consists all details

such as recording of transactions as well as reporting the same among users. It communicates

the financial health of a business among note only domestic but also gathers international

investors for capital funding. Moreover, there are some regulatory authorities which enforces a

business in preparation of fruitful financials disclosures such as:

Generally Accepted Accounting Principles (GAAP): This organisation developed the

principles and rules of recoding accounting transactions for the specific period. Preparation of

all rules and principles will be effective and adequate as per managing operational activities of a

firm. Concepts and principles used here are the best for funnelling accounting professionals in

terms of better financial control in organisation as well as management of operational activities

(Kouki, 2018). It ascertains proper recording of all transactions in various accounts with their

appropriate methods of recoding transactions.

International Financial Reporting Standards (IFRS): These are the standards which

consists of all information that will be useful to firm in terms of preparation of statements and

accounts that will be useful and appropriate in terms of communicating financial health of entity

among external users (Bloomfield and et.al, 2017). It enables the professionals in making

appropriate decision as well as developing plans and policies as per guiding the accounting

professionals or auditors to control operational activities in business. These are international

standards which comprises with all information and techniques to prepare financial statements

for business.

International Accounting Standard Board (IASB): In accordance with operational

activities and the operational framework of IASB are based providing the accounting standard

among all the organisation. Th motive is for upgrading the accounting and book-keeping in the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operational predicates with proper considerations of all the relevant information (Busco and

Quattrone, 2018). There are rules and principle relevant with each statement and transaction to

be recorded in the authentic manner. It brings the uniformity in financial disclosure as well as

helps in making proper records of all transactions.

Financial Reporting Council (FRC): This is UK's personal financial reporting council

which insists that perpetration of financial statements as well as operational regulations

(Financial Reporting Council, 2018). Accessibility of this organisation is in UK and Ireland.

Therefore, it approaches that the financial disclosure in both translocations needed to be

authenticate and appropriate.

Financial Accounting Standard Board (FASB): The purpose of implicating this board

is for monitoring and managing the operational activities which will be effective and helpful as

per managing business operations (Constable and Kuasirikun, 2018). It improves the already

existed accounting standards which were being formulated by GAAP.

3. Rule and regulations of accounting

To manage transactions in various books and accounts which have an appropriate

records of all transactions. Regulations and rules incorporated with recording transactions in

various accounts will have effective control over operations of firm (Damodaran, 2016). These

are the principles which are generally offered by GAAP which insists that the all the

transactions are needed to be recorded properly in the books and have satisfactory analysis over

it. Moreover, there will be record of all transactions in accordance with accounting principles

such as:

Going concern principle: These principles comprised with the rule that the firm is

operating the current period or they have initiate business will have long-term operations.

Therefore, it will be treated as the continuously operating entity in world. Thus, the firm will

being never liquidate it will continue to have trade practices in environment.

Separate legal entity: This principle comprised with the statements and rule that a firm

will be treat as a separate individual other that its owners. Therefore, itself has the operational

activities. Revenue, expenditures apart from the personal capital and costs incurred by its

owners (Robson, Young and Power, 2017). Therefore, this principle authorities does not have

4

Quattrone, 2018). There are rules and principle relevant with each statement and transaction to

be recorded in the authentic manner. It brings the uniformity in financial disclosure as well as

helps in making proper records of all transactions.

Financial Reporting Council (FRC): This is UK's personal financial reporting council

which insists that perpetration of financial statements as well as operational regulations

(Financial Reporting Council, 2018). Accessibility of this organisation is in UK and Ireland.

Therefore, it approaches that the financial disclosure in both translocations needed to be

authenticate and appropriate.

Financial Accounting Standard Board (FASB): The purpose of implicating this board

is for monitoring and managing the operational activities which will be effective and helpful as

per managing business operations (Constable and Kuasirikun, 2018). It improves the already

existed accounting standards which were being formulated by GAAP.

3. Rule and regulations of accounting

To manage transactions in various books and accounts which have an appropriate

records of all transactions. Regulations and rules incorporated with recording transactions in

various accounts will have effective control over operations of firm (Damodaran, 2016). These

are the principles which are generally offered by GAAP which insists that the all the

transactions are needed to be recorded properly in the books and have satisfactory analysis over

it. Moreover, there will be record of all transactions in accordance with accounting principles

such as:

Going concern principle: These principles comprised with the rule that the firm is

operating the current period or they have initiate business will have long-term operations.

Therefore, it will be treated as the continuously operating entity in world. Thus, the firm will

being never liquidate it will continue to have trade practices in environment.

Separate legal entity: This principle comprised with the statements and rule that a firm

will be treat as a separate individual other that its owners. Therefore, itself has the operational

activities. Revenue, expenditures apart from the personal capital and costs incurred by its

owners (Robson, Young and Power, 2017). Therefore, this principle authorities does not have

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

any rights to use the revenue generated by firm in their personal use as they have to make

payment to the dividend holders and settlement of all accounts in right time.

Monetary unit: This concept insists rules that all disclosure of financial statements and

the amount listed in the final accounts needed to be converted into US dollars. Therefore, it will

be profitable and helpful as per communicating financial details of firm among international

user of such accounts (Beatty and Liao, 2014). Therefore, there will e rise in the capital revenue

of a business. This technique will have positive impacts among the investors in terms with

analysing financial health various businesses as per a uniform disclosure of accounts.

Time period: This rule insists that disclosure as well as financial audit of the business

will be based on periodical presentations (Accounting Principles, 2018). Moreover, it bounds

the accounting professionals and auditors of unit in terms of making periodical disclosure in

considerations with a financial year of a firm.

Cost Principles: Accounting is records of all financial transactions on which it can be

said that there will be use of various spendings such as cash or other cash equivalents.

Moreover, it can be said that all transactions are needed to be recorded in proper amounts over

such transactions.

Full Disclosure: This principle comprised with the preparation of financial statements

based on full disclosure of accountants. Therefore, it comprised with framework of accounting

disclosure is that all accounts are needed to be prepared properly and have records in all the

accounts (Bushman, 2014). Therefore, in relation with same it can be said that companies are

bound to make disclosure of accounts such as income statement, balance sheet, statement of

change in equity and cash flow statement.

4. Concepts of material disclosure and consistency

Material Disclosure: It considered that the all the materialistic informations are to be

added by the professional in the financial disclosure as well as preparation of accounts. Thus,

the unrealistic and immaterialist things are not needed to be added in the financial disclosure of

firm (Materiality Concept in Accounting, 2018). It is essential that business have implication of

all financial details and disclosure of accounts.

Consistency: Similarly, with the going concern concept of business it can be said that

5

payment to the dividend holders and settlement of all accounts in right time.

Monetary unit: This concept insists rules that all disclosure of financial statements and

the amount listed in the final accounts needed to be converted into US dollars. Therefore, it will

be profitable and helpful as per communicating financial details of firm among international

user of such accounts (Beatty and Liao, 2014). Therefore, there will e rise in the capital revenue

of a business. This technique will have positive impacts among the investors in terms with

analysing financial health various businesses as per a uniform disclosure of accounts.

Time period: This rule insists that disclosure as well as financial audit of the business

will be based on periodical presentations (Accounting Principles, 2018). Moreover, it bounds

the accounting professionals and auditors of unit in terms of making periodical disclosure in

considerations with a financial year of a firm.

Cost Principles: Accounting is records of all financial transactions on which it can be

said that there will be use of various spendings such as cash or other cash equivalents.

Moreover, it can be said that all transactions are needed to be recorded in proper amounts over

such transactions.

Full Disclosure: This principle comprised with the preparation of financial statements

based on full disclosure of accountants. Therefore, it comprised with framework of accounting

disclosure is that all accounts are needed to be prepared properly and have records in all the

accounts (Bushman, 2014). Therefore, in relation with same it can be said that companies are

bound to make disclosure of accounts such as income statement, balance sheet, statement of

change in equity and cash flow statement.

4. Concepts of material disclosure and consistency

Material Disclosure: It considered that the all the materialistic informations are to be

added by the professional in the financial disclosure as well as preparation of accounts. Thus,

the unrealistic and immaterialist things are not needed to be added in the financial disclosure of

firm (Materiality Concept in Accounting, 2018). It is essential that business have implication of

all financial details and disclosure of accounts.

Consistency: Similarly, with the going concern concept of business it can be said that

5

the firm is needed to have fruitful discoloured of accounts in consistent manner. Thus, it can be

said that there is needed to have records of transactions of regular basis and monthly at the time

of activity took place. It created\s the proper recoding of all transaction held in a period and

does not have any burden over professionals. In relation with auditing of accounts there will be

investigation over all accounts in periodical basis such as daily, weekly, monthly, quarterly and

yearly.

b. Accounting measurements for portfolio clients

CLIENT 1

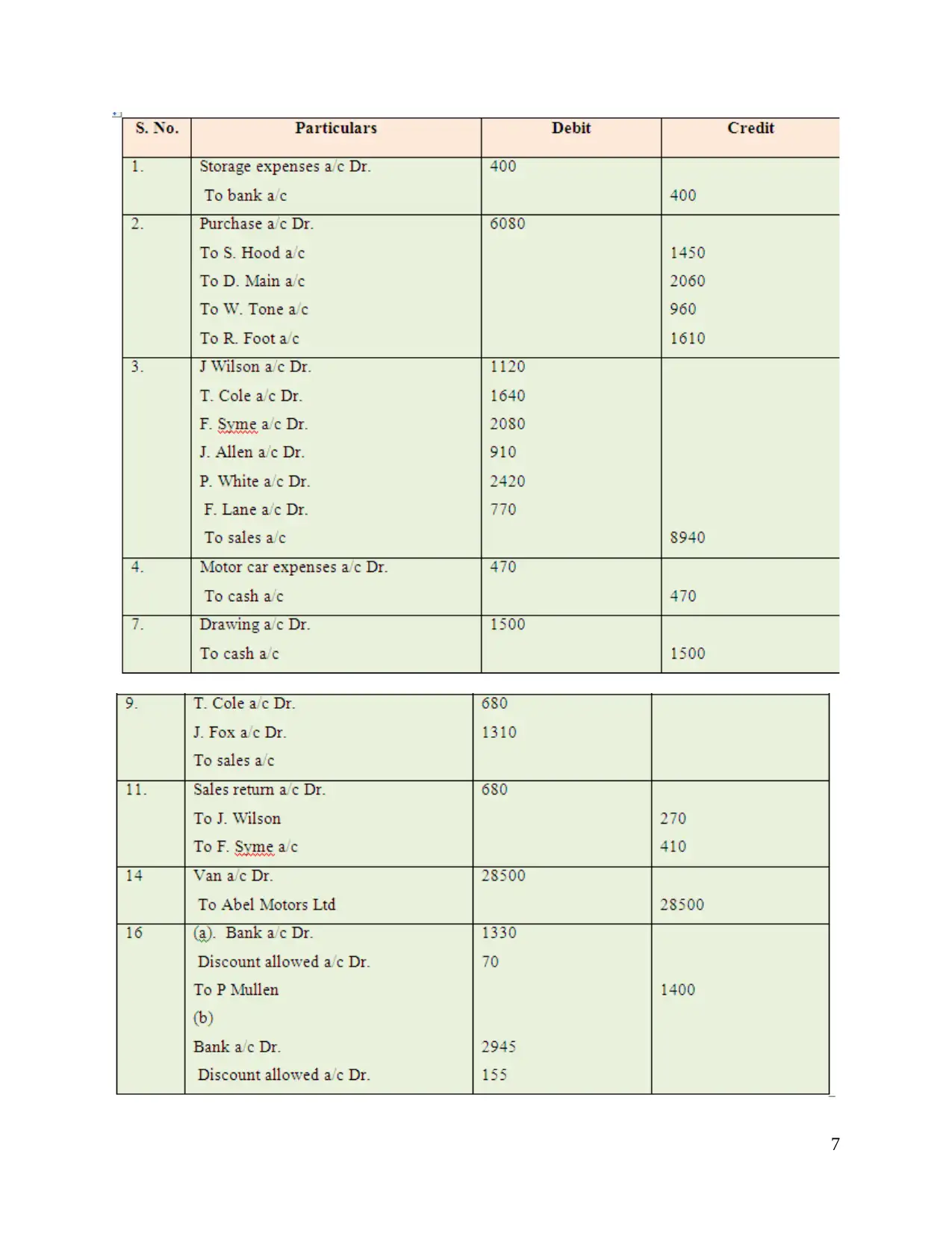

1. Preparing the book of prime entries for Alexandra Study

There will be use of several accounting records and transactions which are needed to be

add in an initial account. Therefore, there will be preparation of all the transactional entries in

different books. All inflows and outflows in an accounting period will have fruitful records of

transactions (Macve, 2015). It consists of all entries such as Adjusting retirers, Compound

entries, Reversing entries etc. Thus, such records will be helpful to the professionals in terms of

developing suitable operational records which are later adjusted in various other accounts.

6

said that there is needed to have records of transactions of regular basis and monthly at the time

of activity took place. It created\s the proper recoding of all transaction held in a period and

does not have any burden over professionals. In relation with auditing of accounts there will be

investigation over all accounts in periodical basis such as daily, weekly, monthly, quarterly and

yearly.

b. Accounting measurements for portfolio clients

CLIENT 1

1. Preparing the book of prime entries for Alexandra Study

There will be use of several accounting records and transactions which are needed to be

add in an initial account. Therefore, there will be preparation of all the transactional entries in

different books. All inflows and outflows in an accounting period will have fruitful records of

transactions (Macve, 2015). It consists of all entries such as Adjusting retirers, Compound

entries, Reversing entries etc. Thus, such records will be helpful to the professionals in terms of

developing suitable operational records which are later adjusted in various other accounts.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

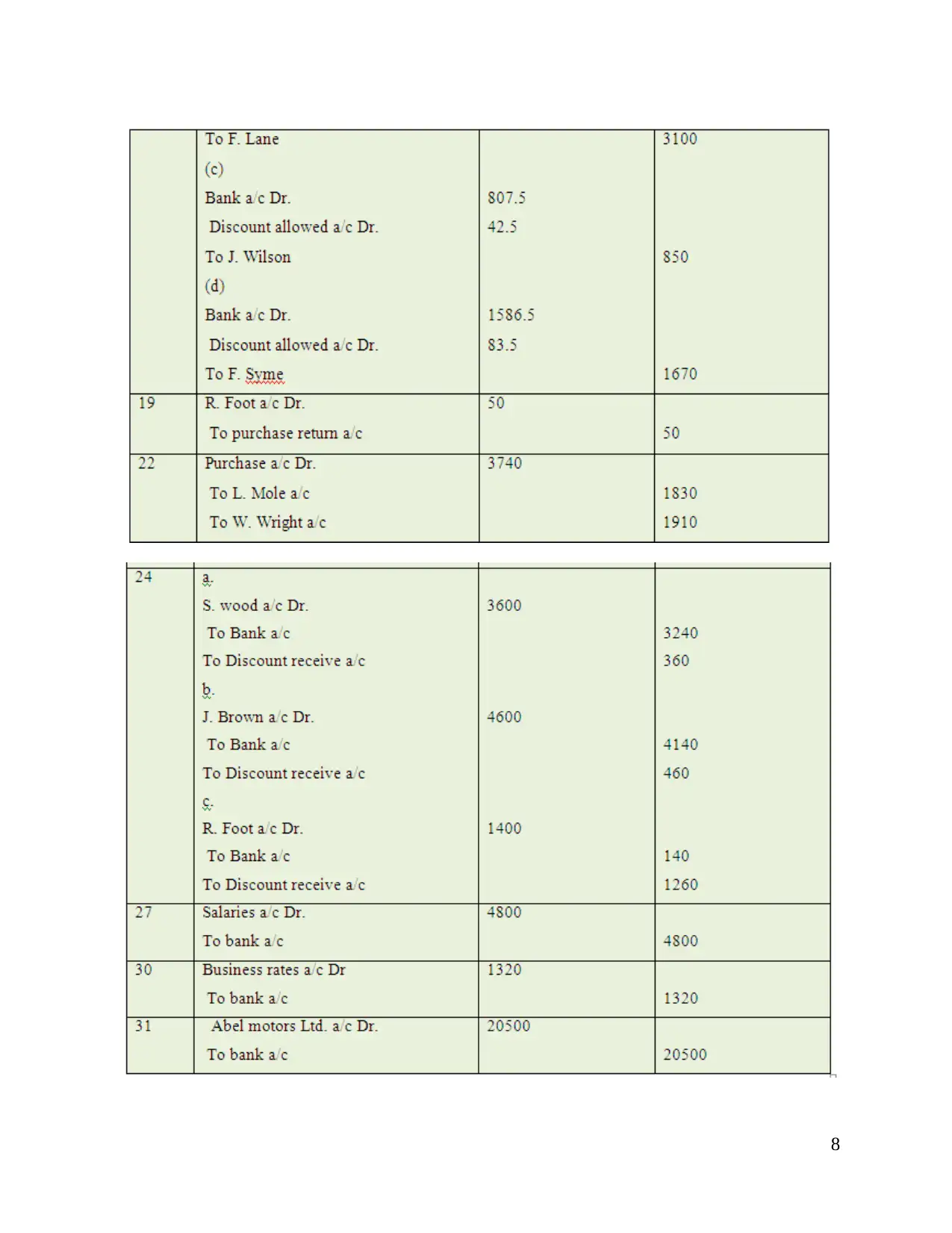

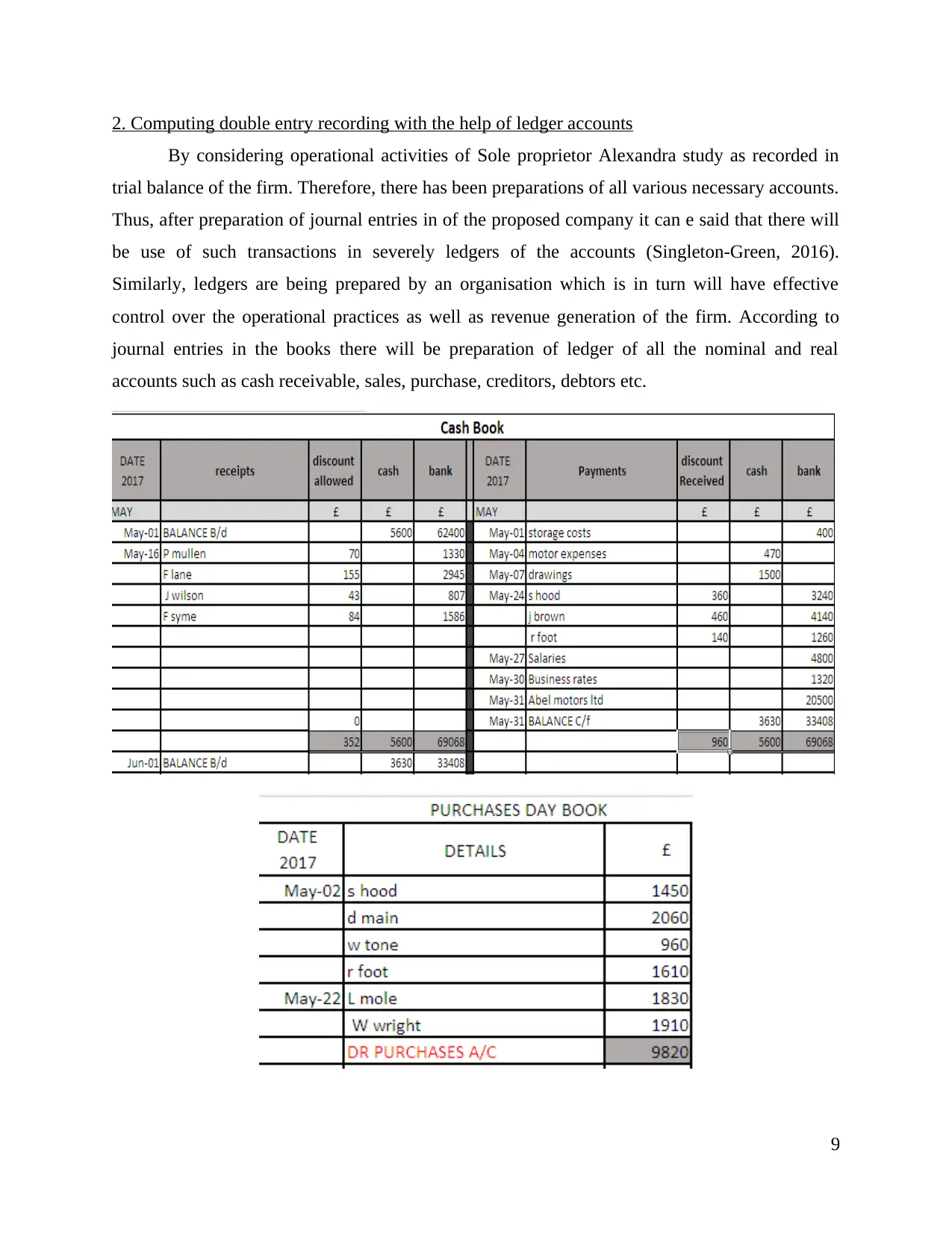

2. Computing double entry recording with the help of ledger accounts

By considering operational activities of Sole proprietor Alexandra study as recorded in

trial balance of the firm. Therefore, there has been preparations of all various necessary accounts.

Thus, after preparation of journal entries in of the proposed company it can e said that there will

be use of such transactions in severely ledgers of the accounts (Singleton-Green, 2016).

Similarly, ledgers are being prepared by an organisation which is in turn will have effective

control over the operational practices as well as revenue generation of the firm. According to

journal entries in the books there will be preparation of ledger of all the nominal and real

accounts such as cash receivable, sales, purchase, creditors, debtors etc.

9

By considering operational activities of Sole proprietor Alexandra study as recorded in

trial balance of the firm. Therefore, there has been preparations of all various necessary accounts.

Thus, after preparation of journal entries in of the proposed company it can e said that there will

be use of such transactions in severely ledgers of the accounts (Singleton-Green, 2016).

Similarly, ledgers are being prepared by an organisation which is in turn will have effective

control over the operational practices as well as revenue generation of the firm. According to

journal entries in the books there will be preparation of ledger of all the nominal and real

accounts such as cash receivable, sales, purchase, creditors, debtors etc.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.