University Financial Analysis Report: Red Ltd vs Blue Ltd (PSB 2.4)

VerifiedAdded on 2023/06/10

|13

|751

|370

Report

AI Summary

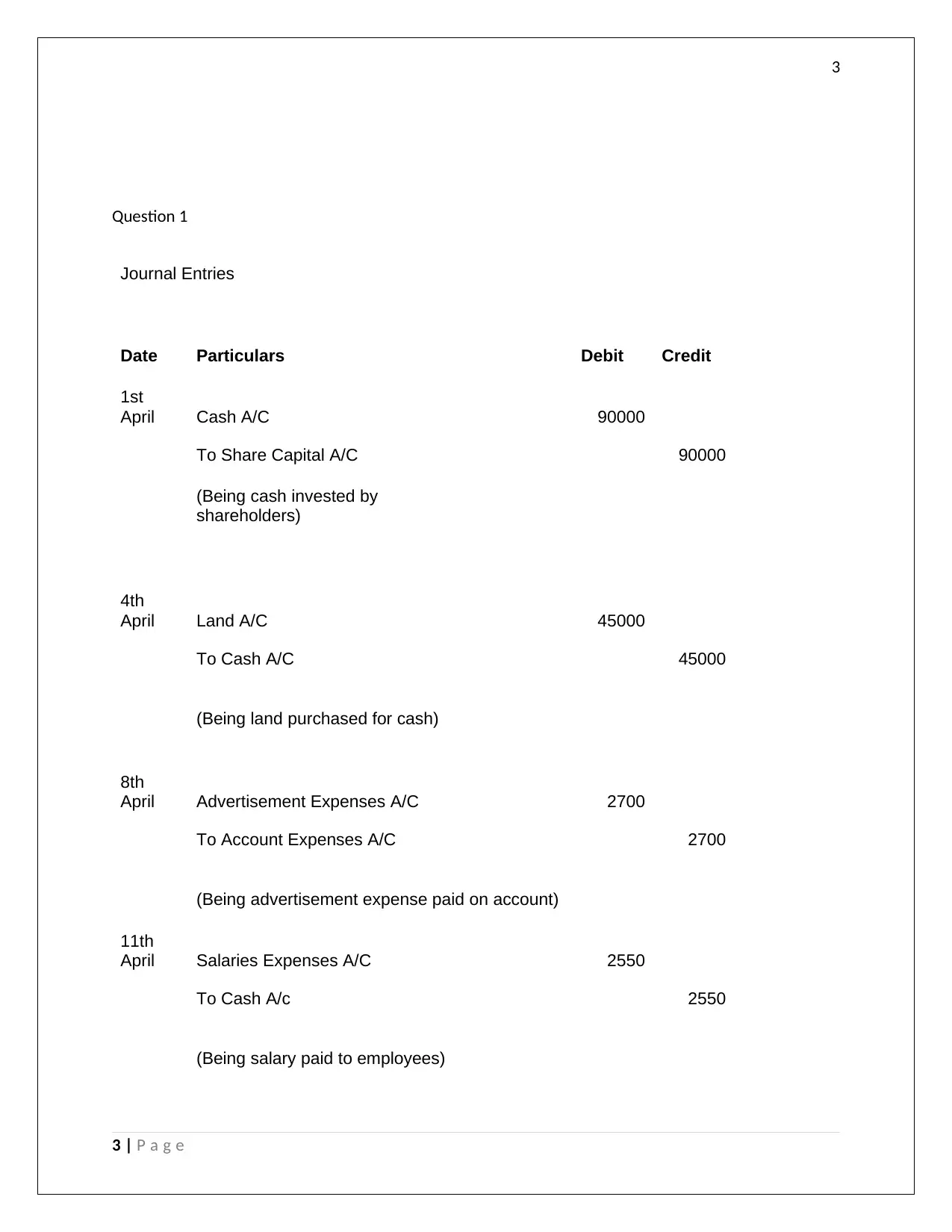

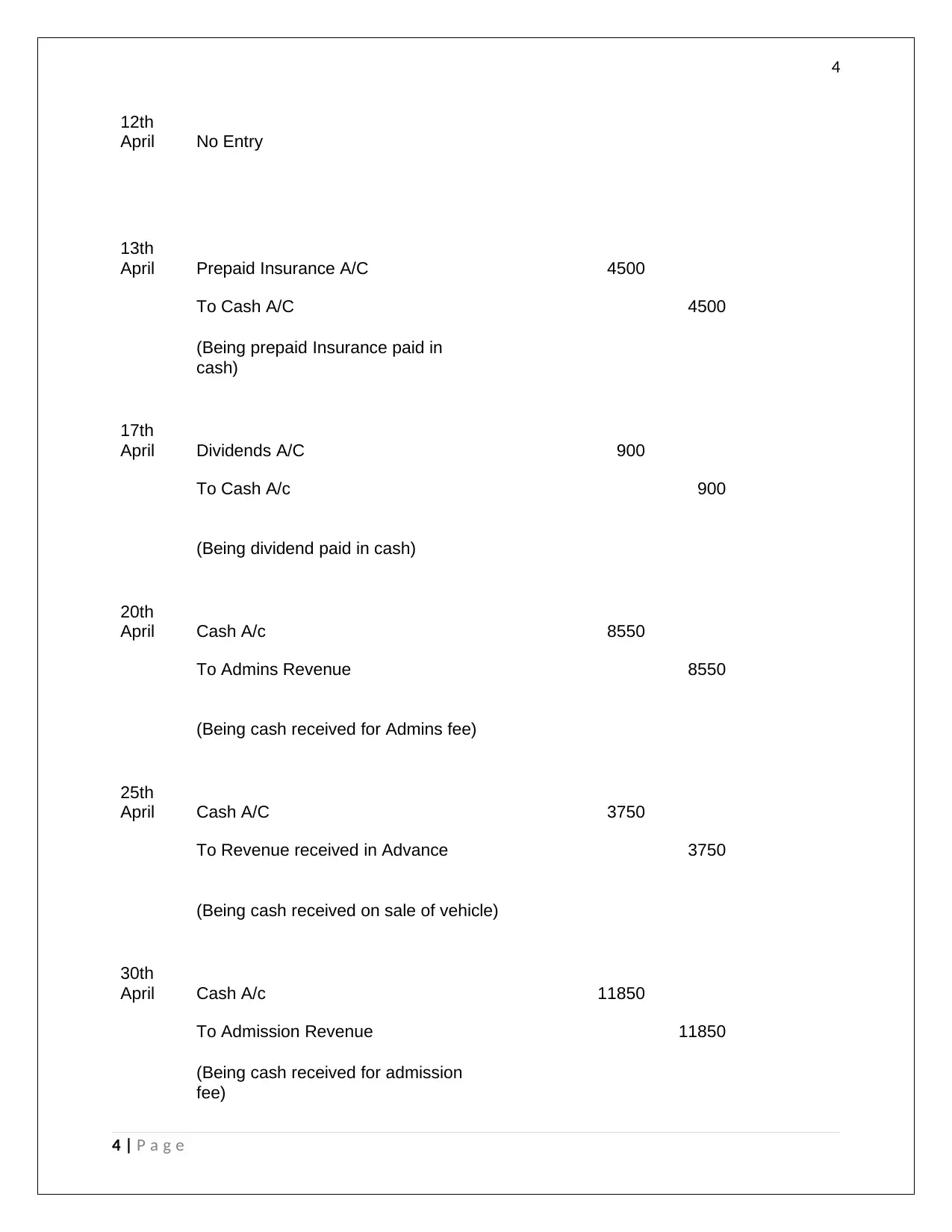

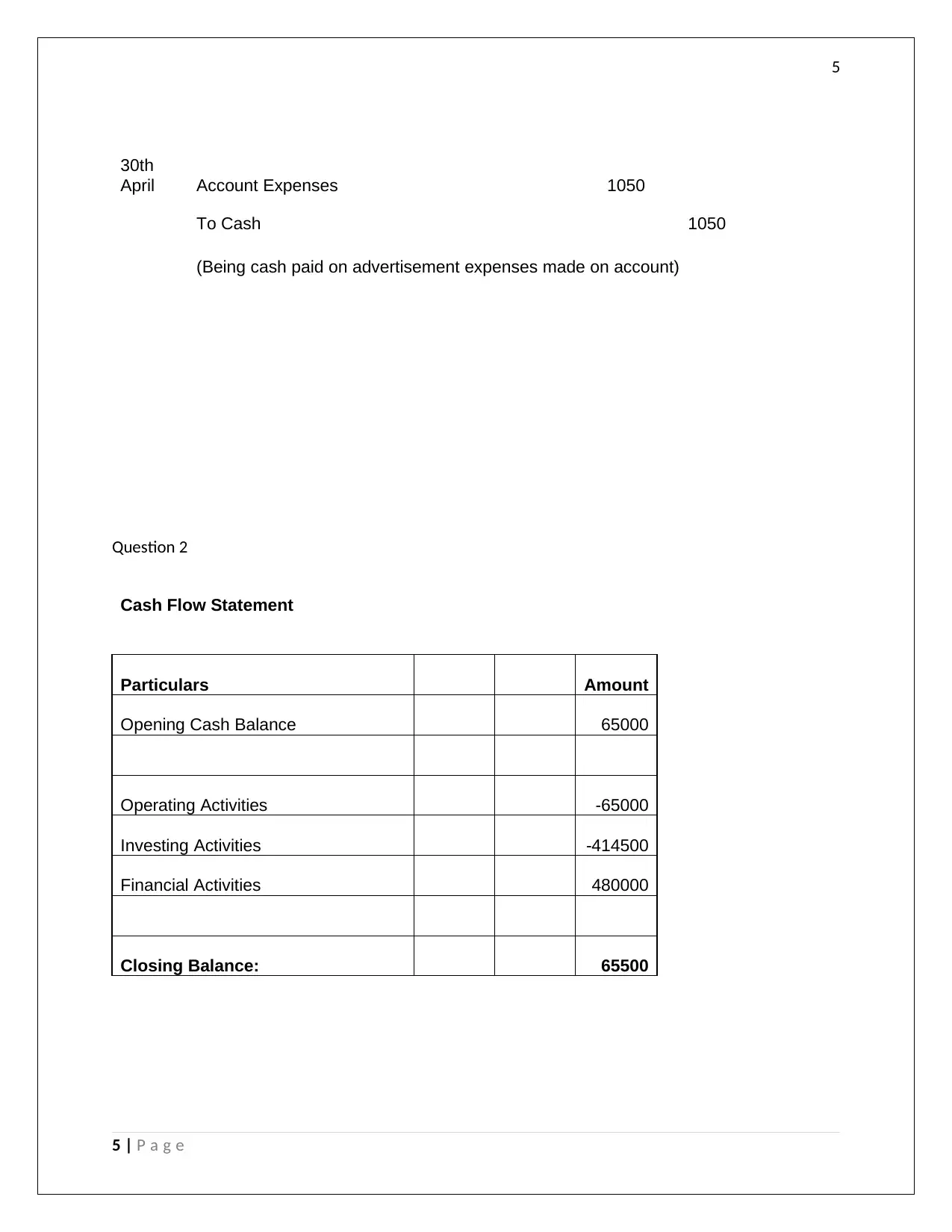

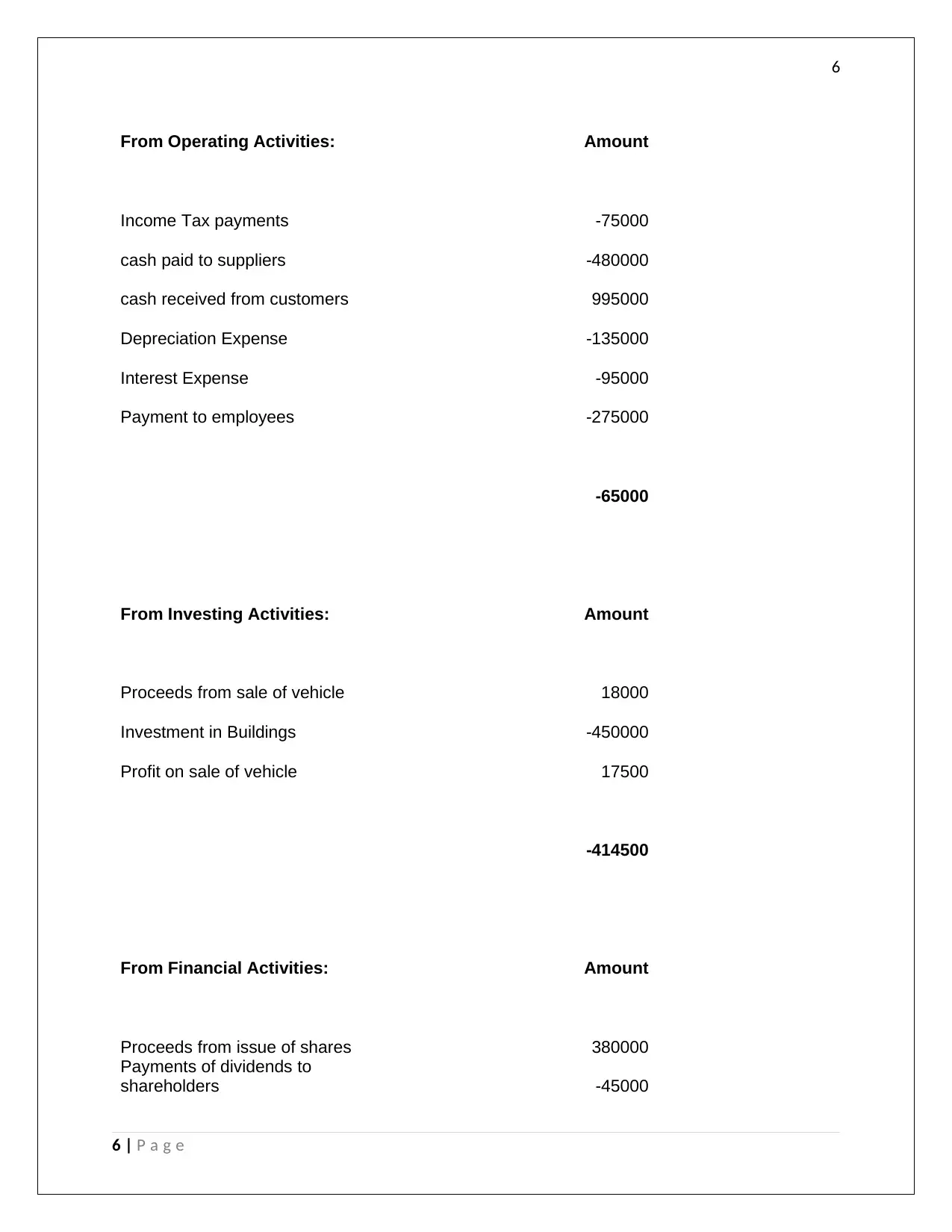

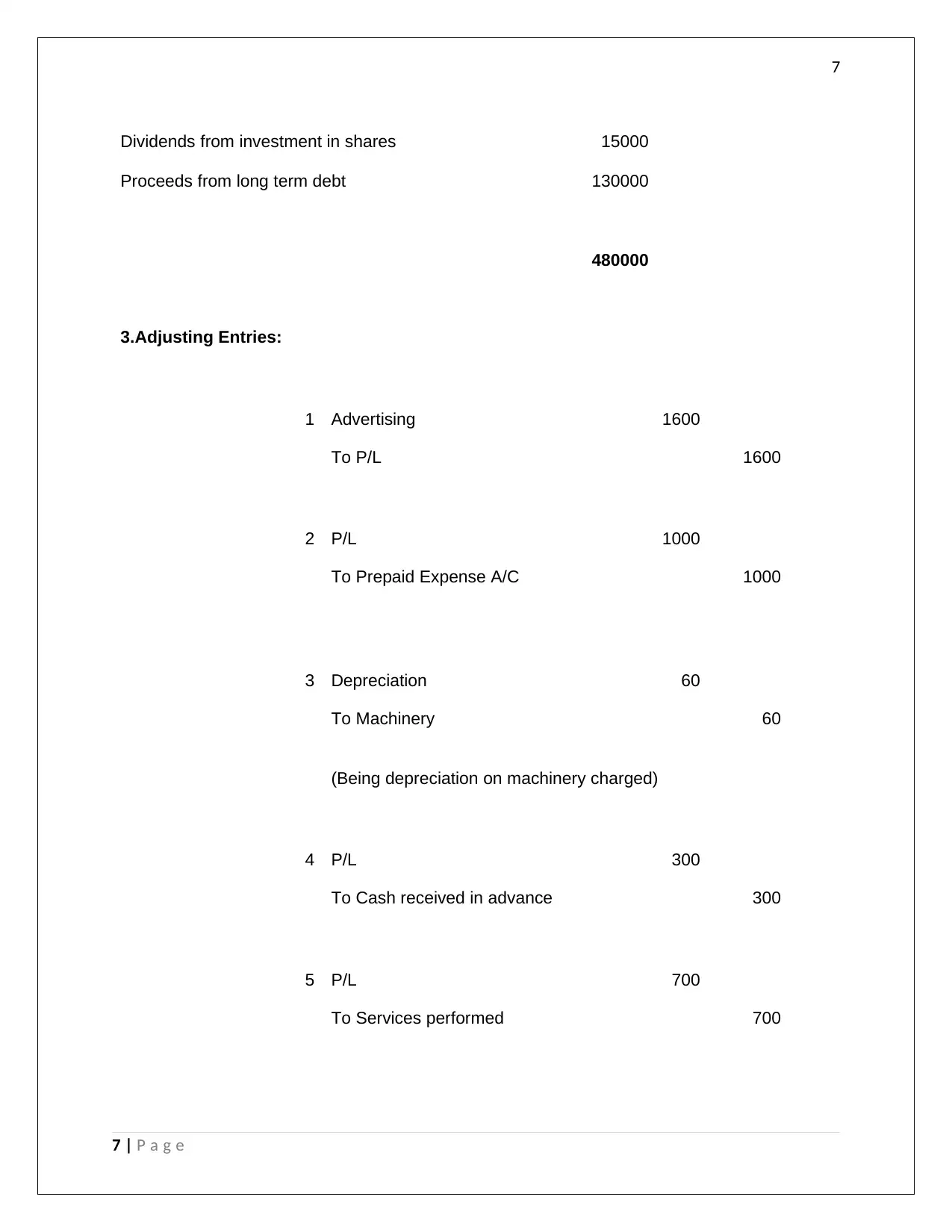

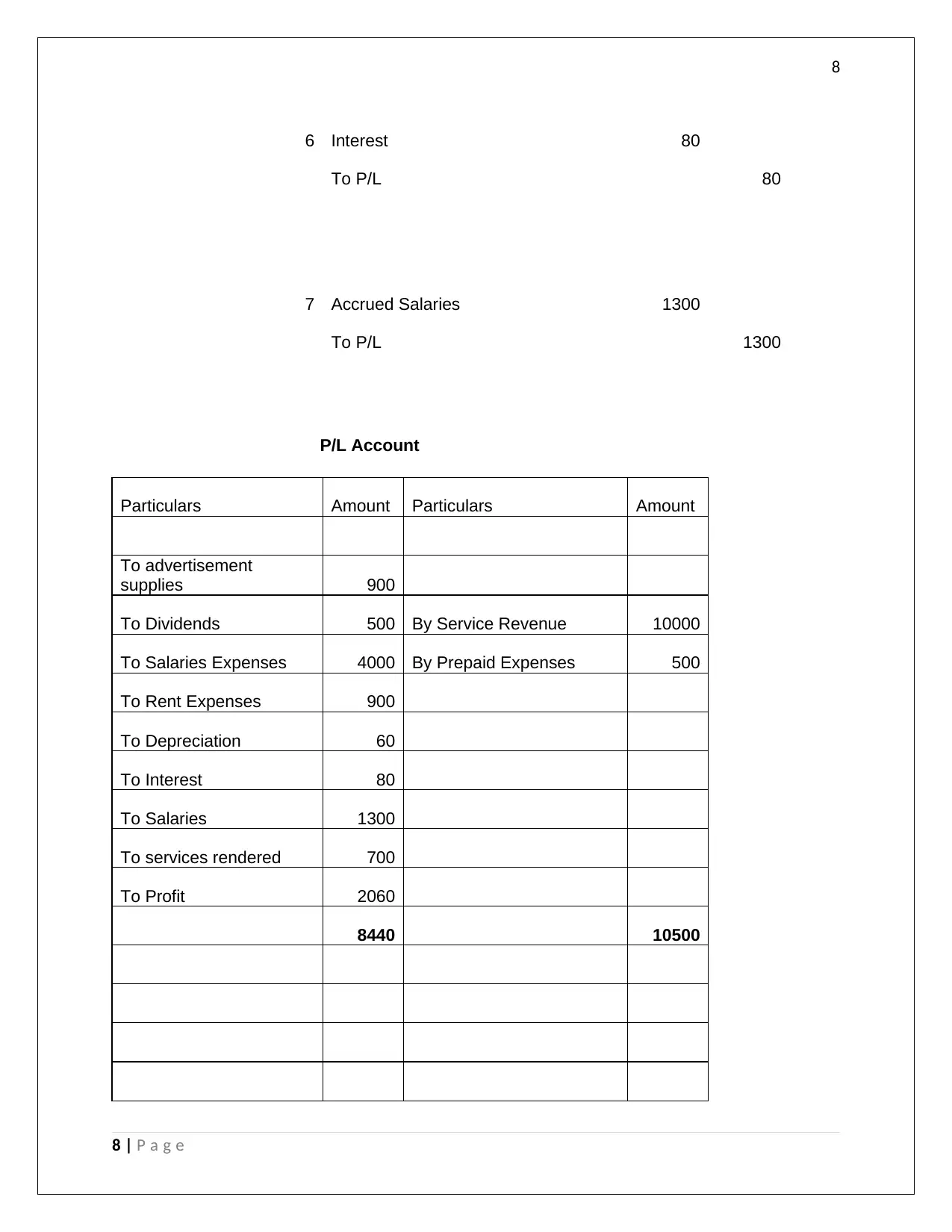

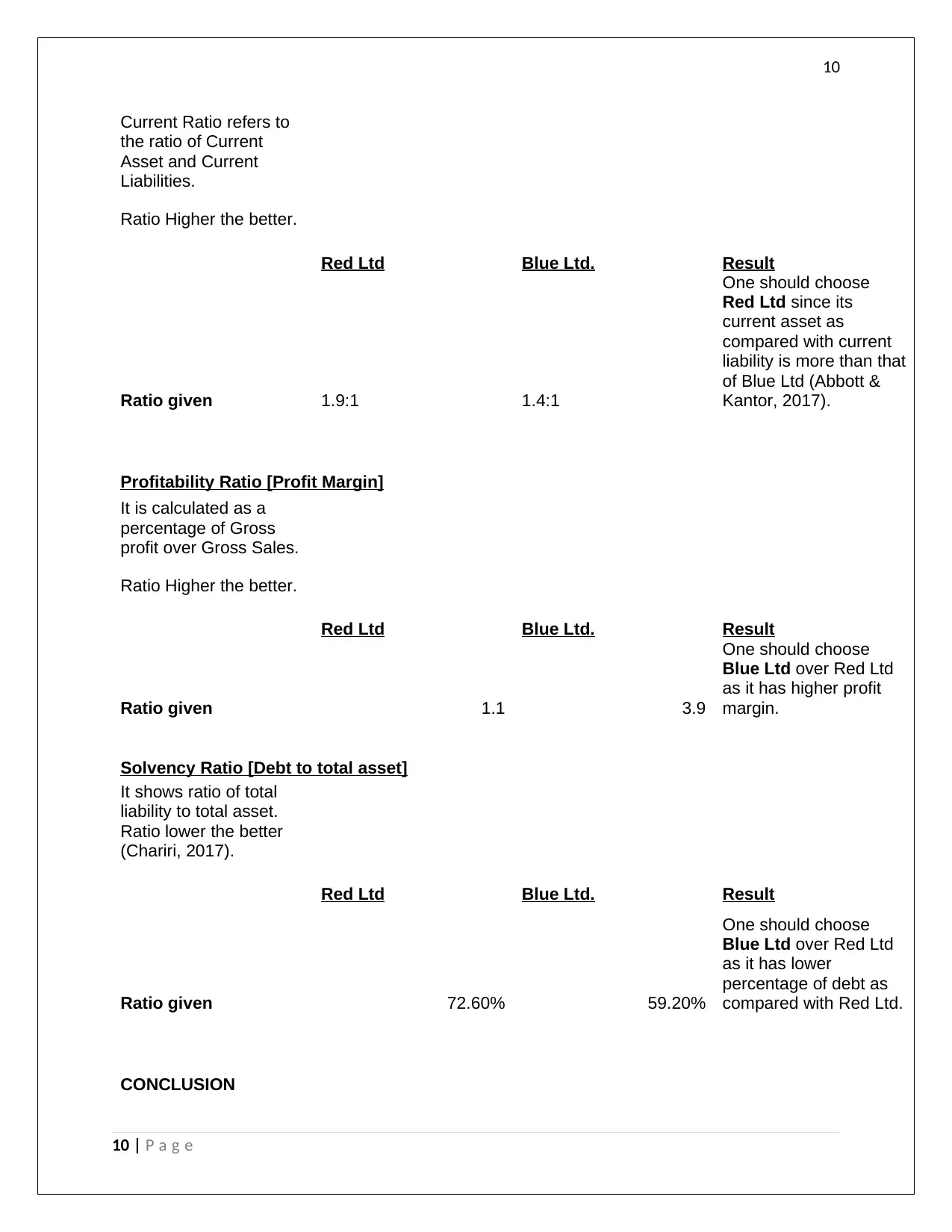

This report presents a financial analysis of Red Ltd and Blue Ltd, focusing on key financial ratios to assess their performance and investment potential. The analysis includes journal entries, a cash flow statement, and adjusting entries to provide a comprehensive overview of each company's financial position. The report compares the two companies based on liquidity, profitability, and solvency ratios, including current ratio, profit margin, and debt-to-total-assets ratio. The findings suggest that Blue Ltd is a better investment option based on the analyzed ratios. The report concludes with a recommendation for investors, supported by the ratio comparisons and analysis. References to relevant accounting literature are also included.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.