Financial Analysis Report: Fine Furnishings Performance Review

VerifiedAdded on 2023/04/21

|8

|1809

|429

Report

AI Summary

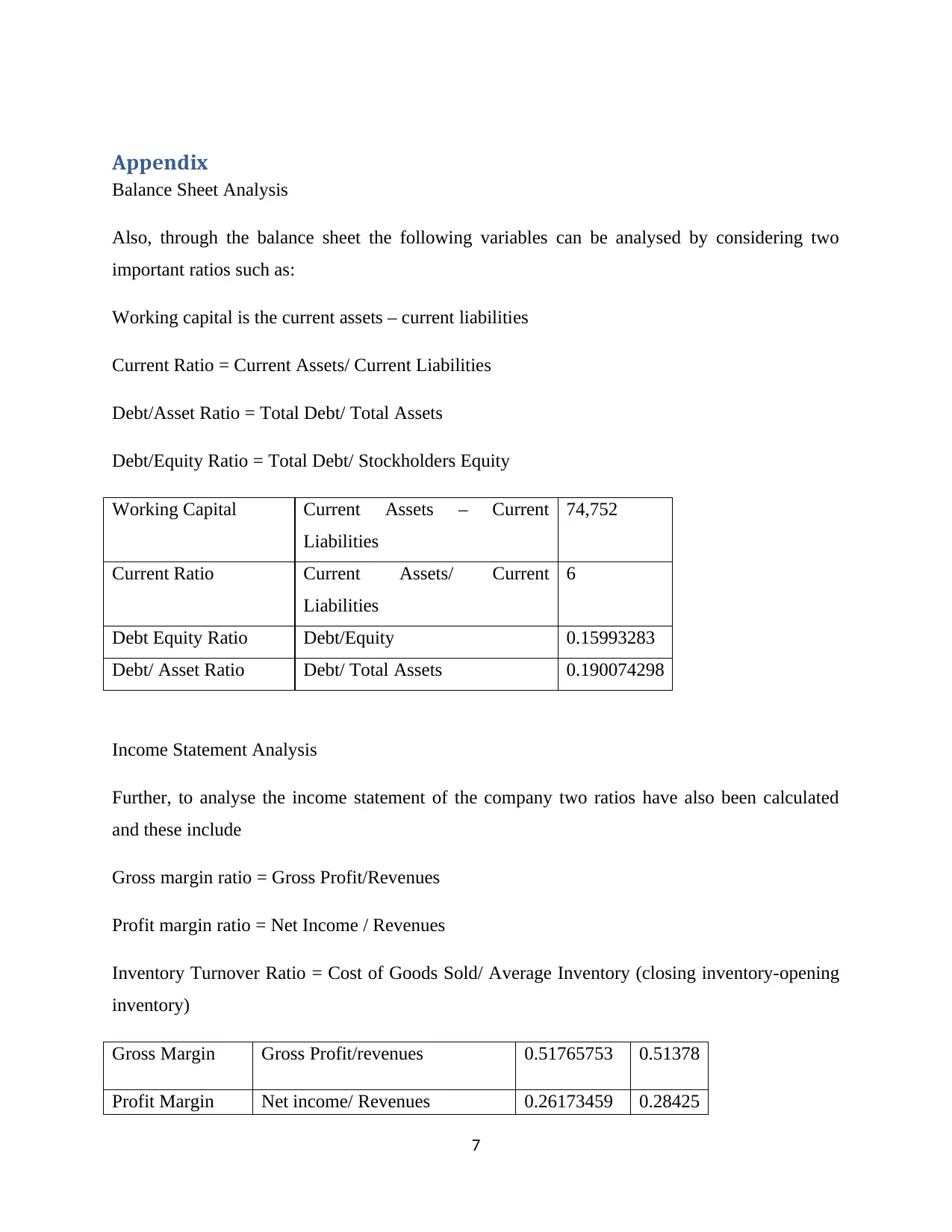

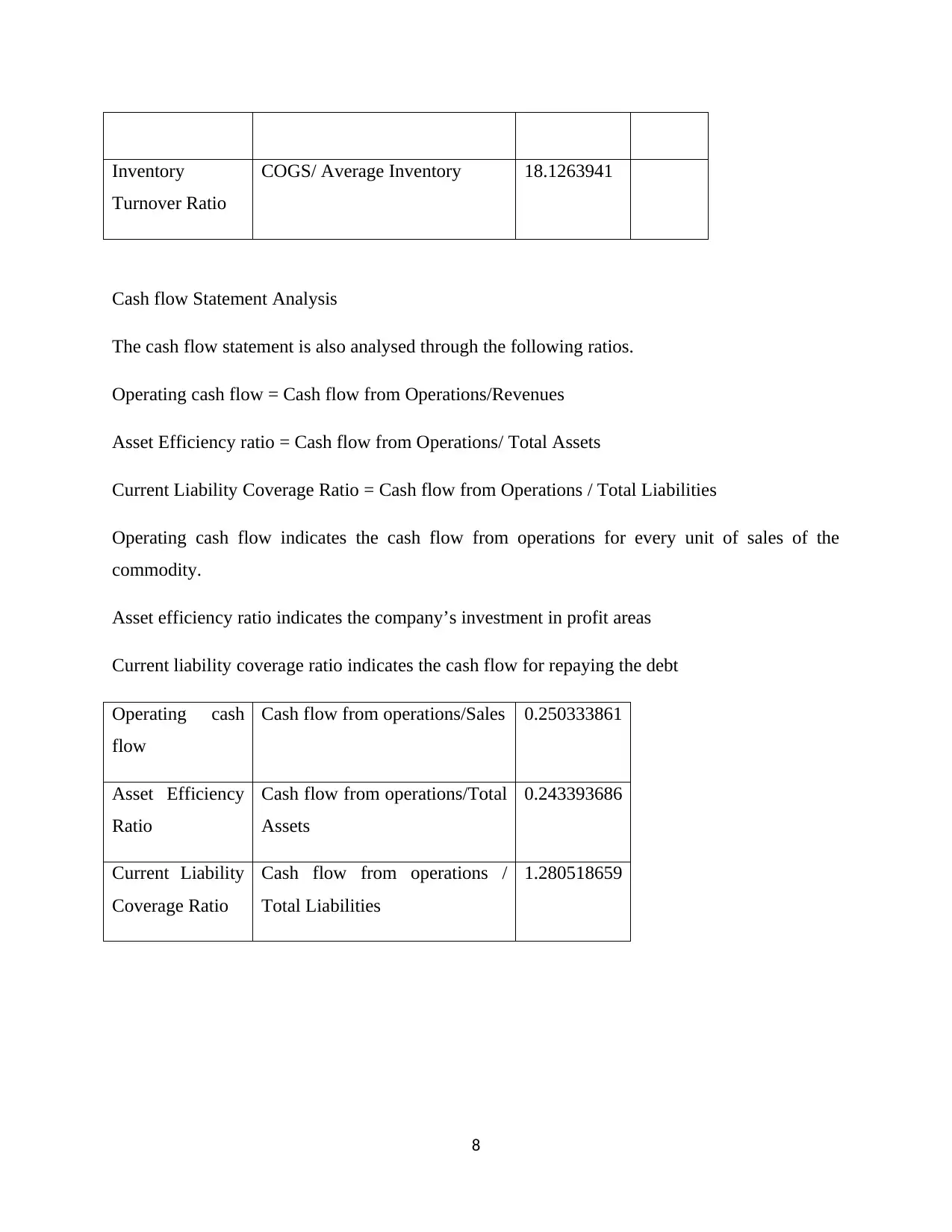

This report presents a financial analysis of Fine Furnishings, evaluating its performance based on balance sheet, income statement, and cash flow statement data. The analysis includes assessment of working capital, debt ratios, inventory turnover, and profitability metrics. The report highlights a decrease in revenues, reduction in inventory, and increased expenses, leading to a decline in gross profit. Despite a good current ratio and liquidity position, the report suggests that the company should invest in innovative products, increase advertising, and explore new markets to improve its financial standing and competitive position. The analysis also provides key ratios such as gross margin, profit margin, and asset efficiency ratio, which are used to assess the financial health of the company. The report concludes with recommendations for management to enhance revenues and improve the company's market position.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.