Comprehensive Financial Report: Ratio Analysis and Investment Review

VerifiedAdded on 2023/06/04

|18

|3937

|410

Report

AI Summary

This report provides a comprehensive financial analysis, beginning with the computation of financial ratios for Liverton Co. for the years 2018 and 2019, including gross profit margin, asset usage ratio, current ratio, acid test ratio, inventory holding period, and debt to equity ratio, followed by an assessment of the importance of financial statements. It includes the preparation of opening statements and a monthly cash budget for six months, along with observations on additional expenditures. The report also determines the break-even point (BEP) in units and sales revenue for both 2019 and 2020, computes the margin of safety, and analyzes the impact of a new business strategy. Finally, it computes investment appraisal techniques such as the payback period, net present value, and average rate of return for different projects, determining the most suitable method for capital investment appraisal. Desklib offers a range of solved assignments and study tools for students.

Introduction to Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Computation of financial ratios of Liverton Co. for the year ended 2018 and 2019...................1

Importance of financial statements .............................................................................................3

Question 2........................................................................................................................................3

a) preparation of an opening statements at the start of July ........................................................3

b) monthly budget of cash for 6 months .....................................................................................3

c) observation of extra additional expenditure ............................................................................4

Question 3........................................................................................................................................4

a) Findings of break even point (BEP)........................................................................................4

b) computation of margin of safety in year 2019 and 2020 ........................................................6

c) Determination of new strategy which evolved to impact on company that has been formed

by Jessica ....................................................................................................................................6

Question 4 .......................................................................................................................................7

a) Computation of payback period, net present value and average rate of return ......................7

Determination of best suitable method for appraisal technique ..................................................9

Capital investment appraisal techniques ..................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Computation of financial ratios of Liverton Co. for the year ended 2018 and 2019...................1

Importance of financial statements .............................................................................................3

Question 2........................................................................................................................................3

a) preparation of an opening statements at the start of July ........................................................3

b) monthly budget of cash for 6 months .....................................................................................3

c) observation of extra additional expenditure ............................................................................4

Question 3........................................................................................................................................4

a) Findings of break even point (BEP)........................................................................................4

b) computation of margin of safety in year 2019 and 2020 ........................................................6

c) Determination of new strategy which evolved to impact on company that has been formed

by Jessica ....................................................................................................................................6

Question 4 .......................................................................................................................................7

a) Computation of payback period, net present value and average rate of return ......................7

Determination of best suitable method for appraisal technique ..................................................9

Capital investment appraisal techniques ..................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES .............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Businessmen need various types of funds to expand their operation and to be sustain in

market for long run. An enterprise should operate in specific industry with a huge amount of

capital for long term growth. It covers almost all aspect of a particular business in term of

financial opportunities and its overall operating expenses like capital asset purchase, meeting

demand supply problems, fluctuation in cash and to put money in return giving assets like

machinery and equipment at the opening of business. In the below report, it includes calculation

of Financial ratios and explanation of financial statements (Baber, 2019) . Further, preparation of

financial position and cash flow budget. The break even point which tells about the situation of

no profit or no loss calculated in both the term of units and sales revenue. Additionally, there is

computation for margin of safety in terms of units and amount. In the end, calculation of

investment appraisal techniques like payback period, accounting rate of return and net present

value.

Question 1

Computation of financial ratios of Liverton Co. for the year ended 2018 and 2019

Gross profit margin ratio for the year 2019 = ( revenue – cost of goods sold ) / sales *

100

= ( 3495 – 2182 ) / 3495 * 100

= 37.57 %

Conclusion : This ratio finalized into profitability ratio where operation of the company are

remarkably decline from 50.26 % in 2018 to 37.57 % in 2019. due to huge increase in operating

expenses during the year 2019.

Assets usage ratio for the year 2019 = total revenue / total asset average

= 3495 / ( 3812 + 2503 / 2 )

= 1.10 times

Conclusion : This ratio indicates the portion of proprietors fund or shareholder's fund invested in

fixed assets and current assets constitute to total assets. It is also an indicator of the efficiency of

management regarding the formulation of financial planning.

Current ratio = current assets / current liabilities

1

Businessmen need various types of funds to expand their operation and to be sustain in

market for long run. An enterprise should operate in specific industry with a huge amount of

capital for long term growth. It covers almost all aspect of a particular business in term of

financial opportunities and its overall operating expenses like capital asset purchase, meeting

demand supply problems, fluctuation in cash and to put money in return giving assets like

machinery and equipment at the opening of business. In the below report, it includes calculation

of Financial ratios and explanation of financial statements (Baber, 2019) . Further, preparation of

financial position and cash flow budget. The break even point which tells about the situation of

no profit or no loss calculated in both the term of units and sales revenue. Additionally, there is

computation for margin of safety in terms of units and amount. In the end, calculation of

investment appraisal techniques like payback period, accounting rate of return and net present

value.

Question 1

Computation of financial ratios of Liverton Co. for the year ended 2018 and 2019

Gross profit margin ratio for the year 2019 = ( revenue – cost of goods sold ) / sales *

100

= ( 3495 – 2182 ) / 3495 * 100

= 37.57 %

Conclusion : This ratio finalized into profitability ratio where operation of the company are

remarkably decline from 50.26 % in 2018 to 37.57 % in 2019. due to huge increase in operating

expenses during the year 2019.

Assets usage ratio for the year 2019 = total revenue / total asset average

= 3495 / ( 3812 + 2503 / 2 )

= 1.10 times

Conclusion : This ratio indicates the portion of proprietors fund or shareholder's fund invested in

fixed assets and current assets constitute to total assets. It is also an indicator of the efficiency of

management regarding the formulation of financial planning.

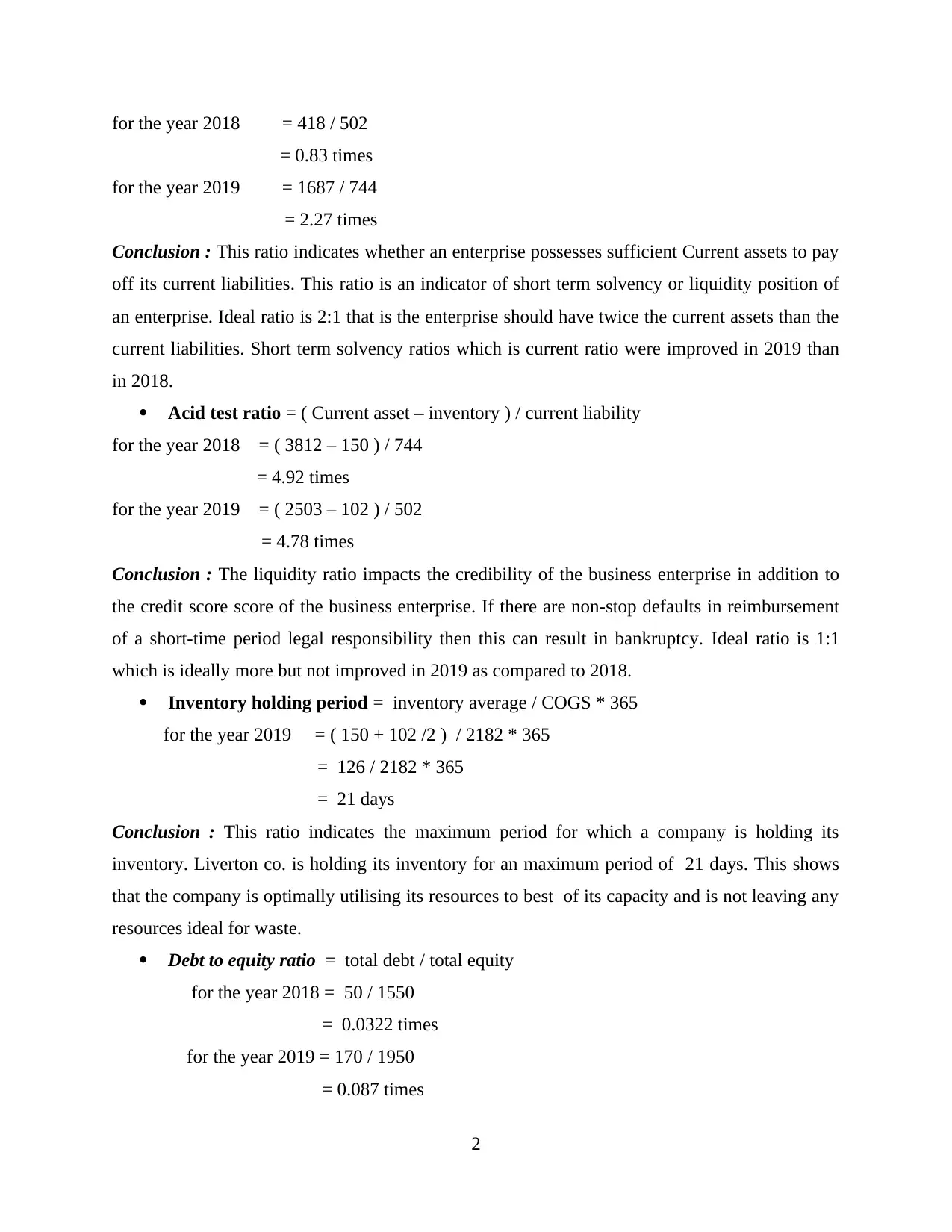

Current ratio = current assets / current liabilities

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for the year 2018 = 418 / 502

= 0.83 times

for the year 2019 = 1687 / 744

= 2.27 times

Conclusion : This ratio indicates whether an enterprise possesses sufficient Current assets to pay

off its current liabilities. This ratio is an indicator of short term solvency or liquidity position of

an enterprise. Ideal ratio is 2:1 that is the enterprise should have twice the current assets than the

current liabilities. Short term solvency ratios which is current ratio were improved in 2019 than

in 2018.

Acid test ratio = ( Current asset – inventory ) / current liability

for the year 2018 = ( 3812 – 150 ) / 744

= 4.92 times

for the year 2019 = ( 2503 – 102 ) / 502

= 4.78 times

Conclusion : The liquidity ratio impacts the credibility of the business enterprise in addition to

the credit score score of the business enterprise. If there are non-stop defaults in reimbursement

of a short-time period legal responsibility then this can result in bankruptcy. Ideal ratio is 1:1

which is ideally more but not improved in 2019 as compared to 2018.

Inventory holding period = inventory average / COGS * 365

for the year 2019 = ( 150 + 102 /2 ) / 2182 * 365

= 126 / 2182 * 365

= 21 days

Conclusion : This ratio indicates the maximum period for which a company is holding its

inventory. Liverton co. is holding its inventory for an maximum period of 21 days. This shows

that the company is optimally utilising its resources to best of its capacity and is not leaving any

resources ideal for waste.

Debt to equity ratio = total debt / total equity

for the year 2018 = 50 / 1550

= 0.0322 times

for the year 2019 = 170 / 1950

= 0.087 times

2

= 0.83 times

for the year 2019 = 1687 / 744

= 2.27 times

Conclusion : This ratio indicates whether an enterprise possesses sufficient Current assets to pay

off its current liabilities. This ratio is an indicator of short term solvency or liquidity position of

an enterprise. Ideal ratio is 2:1 that is the enterprise should have twice the current assets than the

current liabilities. Short term solvency ratios which is current ratio were improved in 2019 than

in 2018.

Acid test ratio = ( Current asset – inventory ) / current liability

for the year 2018 = ( 3812 – 150 ) / 744

= 4.92 times

for the year 2019 = ( 2503 – 102 ) / 502

= 4.78 times

Conclusion : The liquidity ratio impacts the credibility of the business enterprise in addition to

the credit score score of the business enterprise. If there are non-stop defaults in reimbursement

of a short-time period legal responsibility then this can result in bankruptcy. Ideal ratio is 1:1

which is ideally more but not improved in 2019 as compared to 2018.

Inventory holding period = inventory average / COGS * 365

for the year 2019 = ( 150 + 102 /2 ) / 2182 * 365

= 126 / 2182 * 365

= 21 days

Conclusion : This ratio indicates the maximum period for which a company is holding its

inventory. Liverton co. is holding its inventory for an maximum period of 21 days. This shows

that the company is optimally utilising its resources to best of its capacity and is not leaving any

resources ideal for waste.

Debt to equity ratio = total debt / total equity

for the year 2018 = 50 / 1550

= 0.0322 times

for the year 2019 = 170 / 1950

= 0.087 times

2

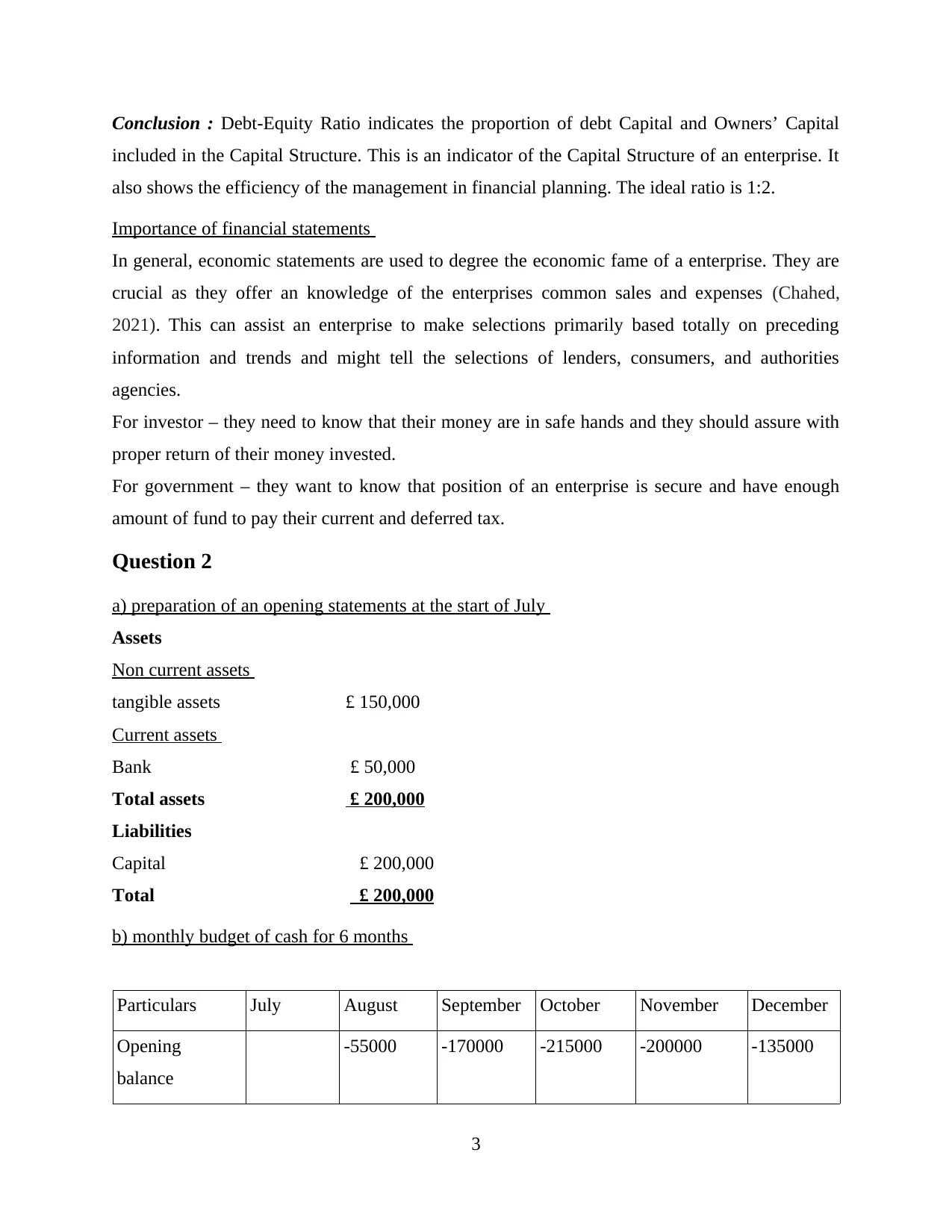

Conclusion : Debt-Equity Ratio indicates the proportion of debt Capital and Owners’ Capital

included in the Capital Structure. This is an indicator of the Capital Structure of an enterprise. It

also shows the efficiency of the management in financial planning. The ideal ratio is 1:2.

Importance of financial statements

In general, economic statements are used to degree the economic fame of a enterprise. They are

crucial as they offer an knowledge of the enterprises common sales and expenses (Chahed,

2021). This can assist an enterprise to make selections primarily based totally on preceding

information and trends and might tell the selections of lenders, consumers, and authorities

agencies.

For investor – they need to know that their money are in safe hands and they should assure with

proper return of their money invested.

For government – they want to know that position of an enterprise is secure and have enough

amount of fund to pay their current and deferred tax.

Question 2

a) preparation of an opening statements at the start of July

Assets

Non current assets

tangible assets £ 150,000

Current assets

Bank £ 50,000

Total assets £ 200,000

Liabilities

Capital £ 200,000

Total £ 200,000

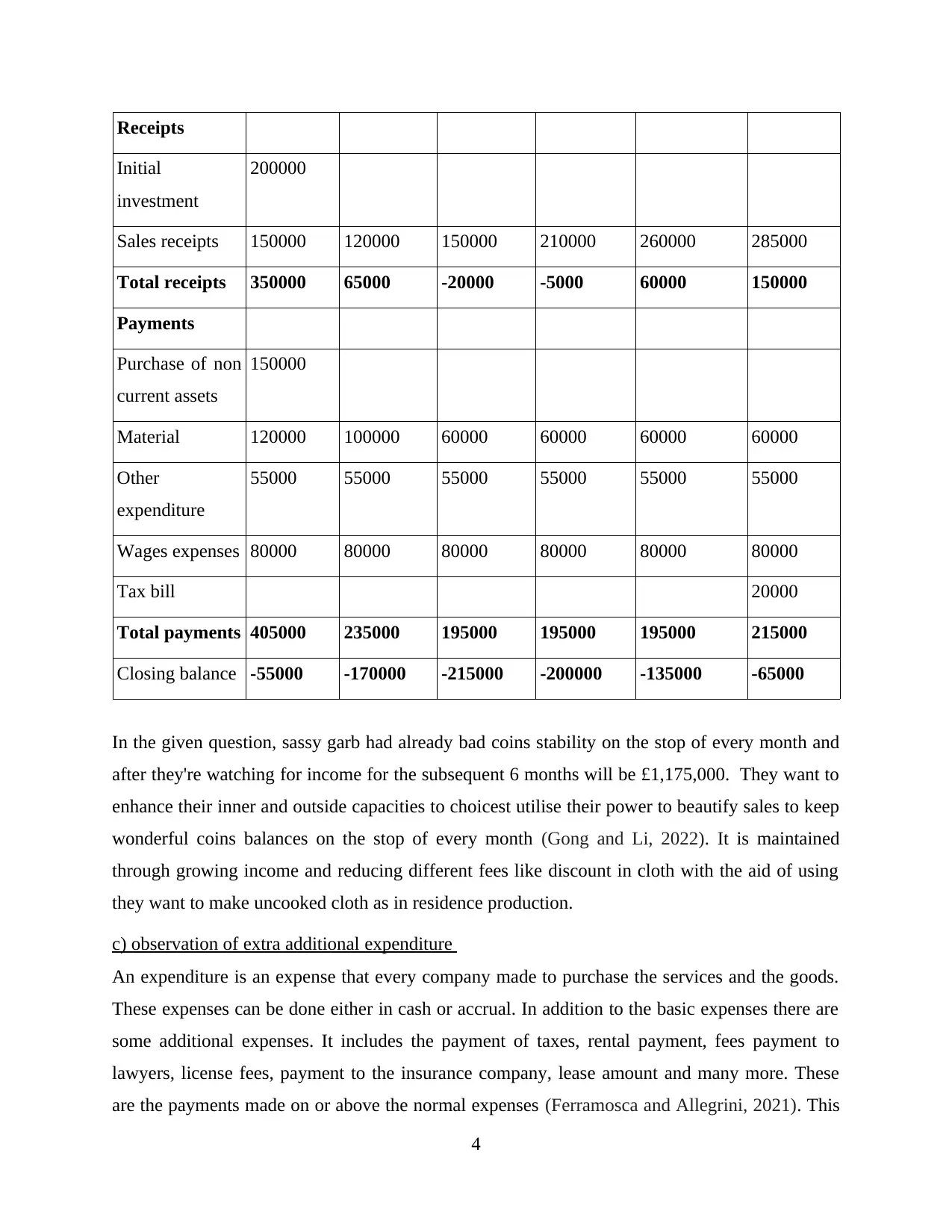

b) monthly budget of cash for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

3

included in the Capital Structure. This is an indicator of the Capital Structure of an enterprise. It

also shows the efficiency of the management in financial planning. The ideal ratio is 1:2.

Importance of financial statements

In general, economic statements are used to degree the economic fame of a enterprise. They are

crucial as they offer an knowledge of the enterprises common sales and expenses (Chahed,

2021). This can assist an enterprise to make selections primarily based totally on preceding

information and trends and might tell the selections of lenders, consumers, and authorities

agencies.

For investor – they need to know that their money are in safe hands and they should assure with

proper return of their money invested.

For government – they want to know that position of an enterprise is secure and have enough

amount of fund to pay their current and deferred tax.

Question 2

a) preparation of an opening statements at the start of July

Assets

Non current assets

tangible assets £ 150,000

Current assets

Bank £ 50,000

Total assets £ 200,000

Liabilities

Capital £ 200,000

Total £ 200,000

b) monthly budget of cash for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of non

current assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

In the given question, sassy garb had already bad coins stability on the stop of every month and

after they're watching for income for the subsequent 6 months will be £1,175,000. They want to

enhance their inner and outside capacities to choicest utilise their power to beautify sales to keep

wonderful coins balances on the stop of every month (Gong and Li, 2022). It is maintained

through growing income and reducing different fees like discount in cloth with the aid of using

they want to make uncooked cloth as in residence production.

c) observation of extra additional expenditure

An expenditure is an expense that every company made to purchase the services and the goods.

These expenses can be done either in cash or accrual. In addition to the basic expenses there are

some additional expenses. It includes the payment of taxes, rental payment, fees payment to

lawyers, license fees, payment to the insurance company, lease amount and many more. These

are the payments made on or above the normal expenses (Ferramosca and Allegrini, 2021). This

4

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of non

current assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

In the given question, sassy garb had already bad coins stability on the stop of every month and

after they're watching for income for the subsequent 6 months will be £1,175,000. They want to

enhance their inner and outside capacities to choicest utilise their power to beautify sales to keep

wonderful coins balances on the stop of every month (Gong and Li, 2022). It is maintained

through growing income and reducing different fees like discount in cloth with the aid of using

they want to make uncooked cloth as in residence production.

c) observation of extra additional expenditure

An expenditure is an expense that every company made to purchase the services and the goods.

These expenses can be done either in cash or accrual. In addition to the basic expenses there are

some additional expenses. It includes the payment of taxes, rental payment, fees payment to

lawyers, license fees, payment to the insurance company, lease amount and many more. These

are the payments made on or above the normal expenses (Ferramosca and Allegrini, 2021). This

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maintains the continuity in the continuity of the business. If any company fails to make payments

then it may results in the failure of the business operations.

Question 3

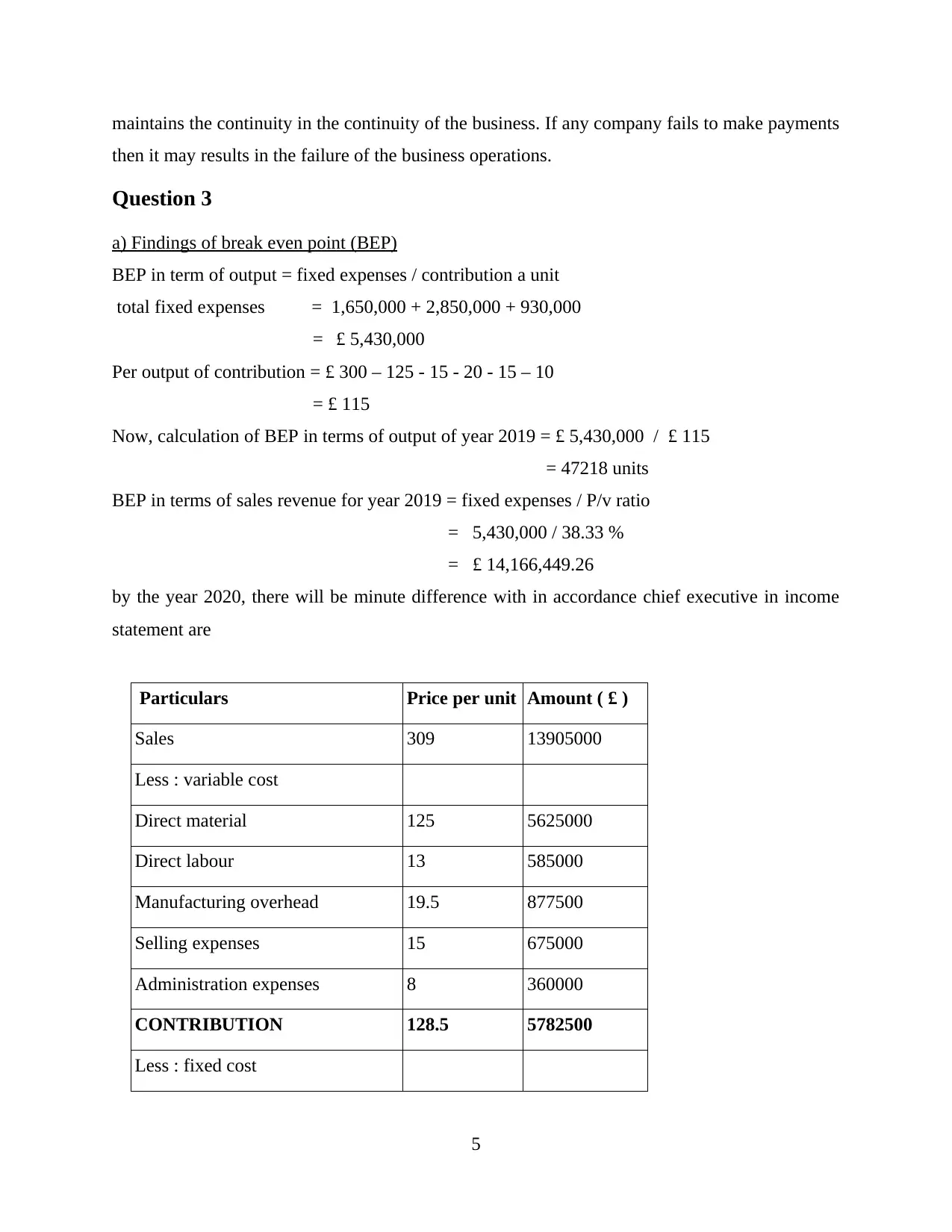

a) Findings of break even point (BEP)

BEP in term of output = fixed expenses / contribution a unit

total fixed expenses = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

Per output of contribution = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

Now, calculation of BEP in terms of output of year 2019 = £ 5,430,000 / £ 115

= 47218 units

BEP in terms of sales revenue for year 2019 = fixed expenses / P/v ratio

= 5,430,000 / 38.33 %

= £ 14,166,449.26

by the year 2020, there will be minute difference with in accordance chief executive in income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

5

then it may results in the failure of the business operations.

Question 3

a) Findings of break even point (BEP)

BEP in term of output = fixed expenses / contribution a unit

total fixed expenses = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

Per output of contribution = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

Now, calculation of BEP in terms of output of year 2019 = £ 5,430,000 / £ 115

= 47218 units

BEP in terms of sales revenue for year 2019 = fixed expenses / P/v ratio

= 5,430,000 / 38.33 %

= £ 14,166,449.26

by the year 2020, there will be minute difference with in accordance chief executive in income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

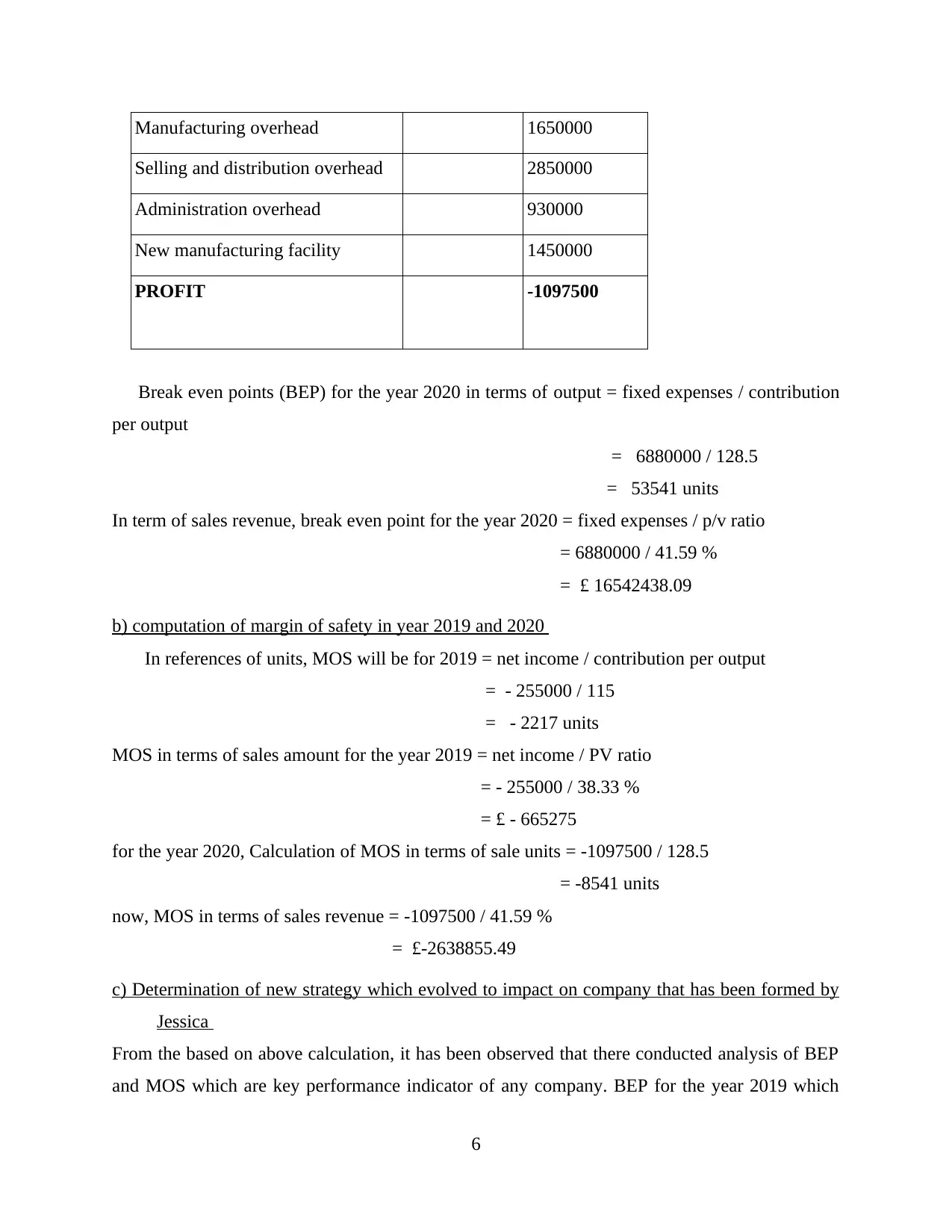

5

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even points (BEP) for the year 2020 in terms of output = fixed expenses / contribution

per output

= 6880000 / 128.5

= 53541 units

In term of sales revenue, break even point for the year 2020 = fixed expenses / p/v ratio

= 6880000 / 41.59 %

= £ 16542438.09

b) computation of margin of safety in year 2019 and 2020

In references of units, MOS will be for 2019 = net income / contribution per output

= - 255000 / 115

= - 2217 units

MOS in terms of sales amount for the year 2019 = net income / PV ratio

= - 255000 / 38.33 %

= £ - 665275

for the year 2020, Calculation of MOS in terms of sale units = -1097500 / 128.5

= -8541 units

now, MOS in terms of sales revenue = -1097500 / 41.59 %

= £-2638855.49

c) Determination of new strategy which evolved to impact on company that has been formed by

Jessica

From the based on above calculation, it has been observed that there conducted analysis of BEP

and MOS which are key performance indicator of any company. BEP for the year 2019 which

6

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even points (BEP) for the year 2020 in terms of output = fixed expenses / contribution

per output

= 6880000 / 128.5

= 53541 units

In term of sales revenue, break even point for the year 2020 = fixed expenses / p/v ratio

= 6880000 / 41.59 %

= £ 16542438.09

b) computation of margin of safety in year 2019 and 2020

In references of units, MOS will be for 2019 = net income / contribution per output

= - 255000 / 115

= - 2217 units

MOS in terms of sales amount for the year 2019 = net income / PV ratio

= - 255000 / 38.33 %

= £ - 665275

for the year 2020, Calculation of MOS in terms of sale units = -1097500 / 128.5

= -8541 units

now, MOS in terms of sales revenue = -1097500 / 41.59 %

= £-2638855.49

c) Determination of new strategy which evolved to impact on company that has been formed by

Jessica

From the based on above calculation, it has been observed that there conducted analysis of BEP

and MOS which are key performance indicator of any company. BEP for the year 2019 which

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

was before Jessica's strategy comes out to be 47218 units while Jessica's strategy for 2020

resultant to be 53541 units. From this, it means that new strategy need more units to reach the

level of no profit no loss situation. Company would like to prefer for old strategy in this case.

Now, when it comes to margin of safety for the year 2019 in terms of sales units was – 2217

units which signifies to they need to produce more units to comes margin level. While, for the

year 2020 was – 8541 units, when compare to 2019 it would require more units to reach on to the

level of margin. They want to beautify their income and want to enhance their boom through

income merchandising and different selling tools(Mooney and Dugan, 2019). For accomplishing

more growth prospectus, they nearly spent already 1,450,000 as a fixed expenses which is quite

raised due to ground of happening loss.

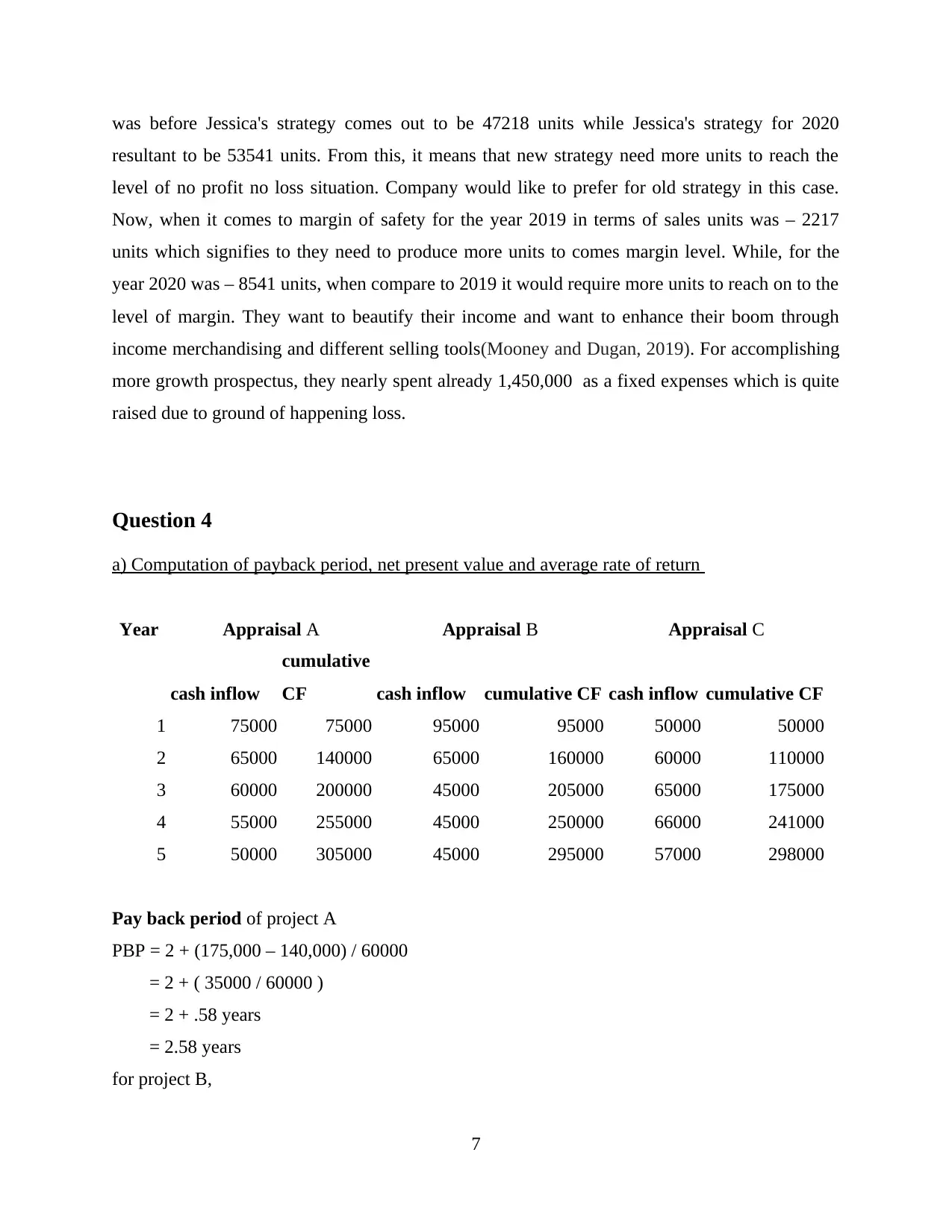

Question 4

a) Computation of payback period, net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF cash inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

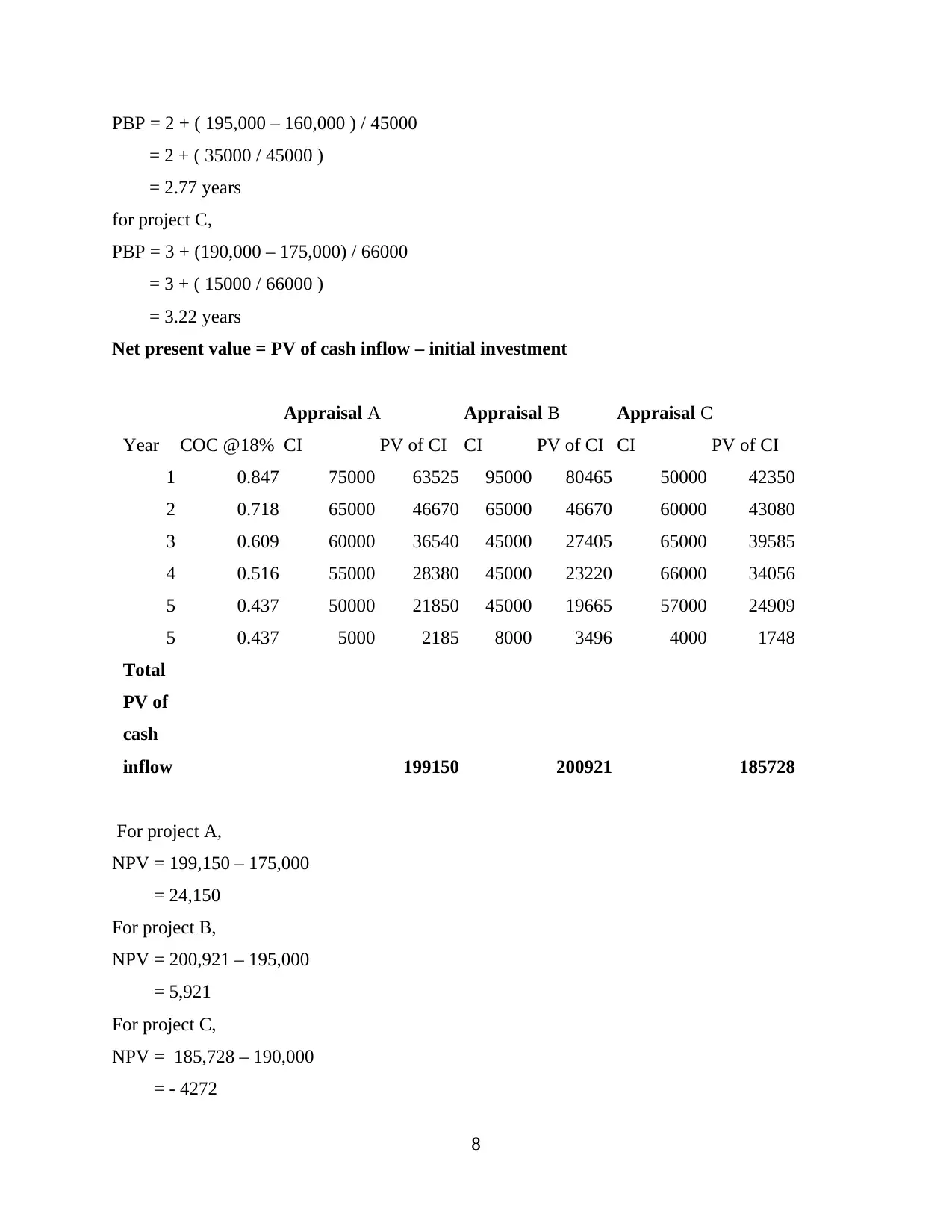

Pay back period of project A

PBP = 2 + (175,000 – 140,000) / 60000

= 2 + ( 35000 / 60000 )

= 2 + .58 years

= 2.58 years

for project B,

7

resultant to be 53541 units. From this, it means that new strategy need more units to reach the

level of no profit no loss situation. Company would like to prefer for old strategy in this case.

Now, when it comes to margin of safety for the year 2019 in terms of sales units was – 2217

units which signifies to they need to produce more units to comes margin level. While, for the

year 2020 was – 8541 units, when compare to 2019 it would require more units to reach on to the

level of margin. They want to beautify their income and want to enhance their boom through

income merchandising and different selling tools(Mooney and Dugan, 2019). For accomplishing

more growth prospectus, they nearly spent already 1,450,000 as a fixed expenses which is quite

raised due to ground of happening loss.

Question 4

a) Computation of payback period, net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF cash inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of project A

PBP = 2 + (175,000 – 140,000) / 60000

= 2 + ( 35000 / 60000 )

= 2 + .58 years

= 2.58 years

for project B,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PBP = 2 + ( 195,000 – 160,000 ) / 45000

= 2 + ( 35000 / 45000 )

= 2.77 years

for project C,

PBP = 3 + (190,000 – 175,000) / 66000

= 3 + ( 15000 / 66000 )

= 3.22 years

Net present value = PV of cash inflow – initial investment

Appraisal A Appraisal B Appraisal C

Year COC @18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

For project A,

NPV = 199,150 – 175,000

= 24,150

For project B,

NPV = 200,921 – 195,000

= 5,921

For project C,

NPV = 185,728 – 190,000

= - 4272

8

= 2 + ( 35000 / 45000 )

= 2.77 years

for project C,

PBP = 3 + (190,000 – 175,000) / 66000

= 3 + ( 15000 / 66000 )

= 3.22 years

Net present value = PV of cash inflow – initial investment

Appraisal A Appraisal B Appraisal C

Year COC @18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

For project A,

NPV = 199,150 – 175,000

= 24,150

For project B,

NPV = 200,921 – 195,000

= 5,921

For project C,

NPV = 185,728 – 190,000

= - 4272

8

It can be concluded that by using NPV techniques project A or project B can be selected but for

choosing only one project it would be project A as it has higher NPV of 24,150.

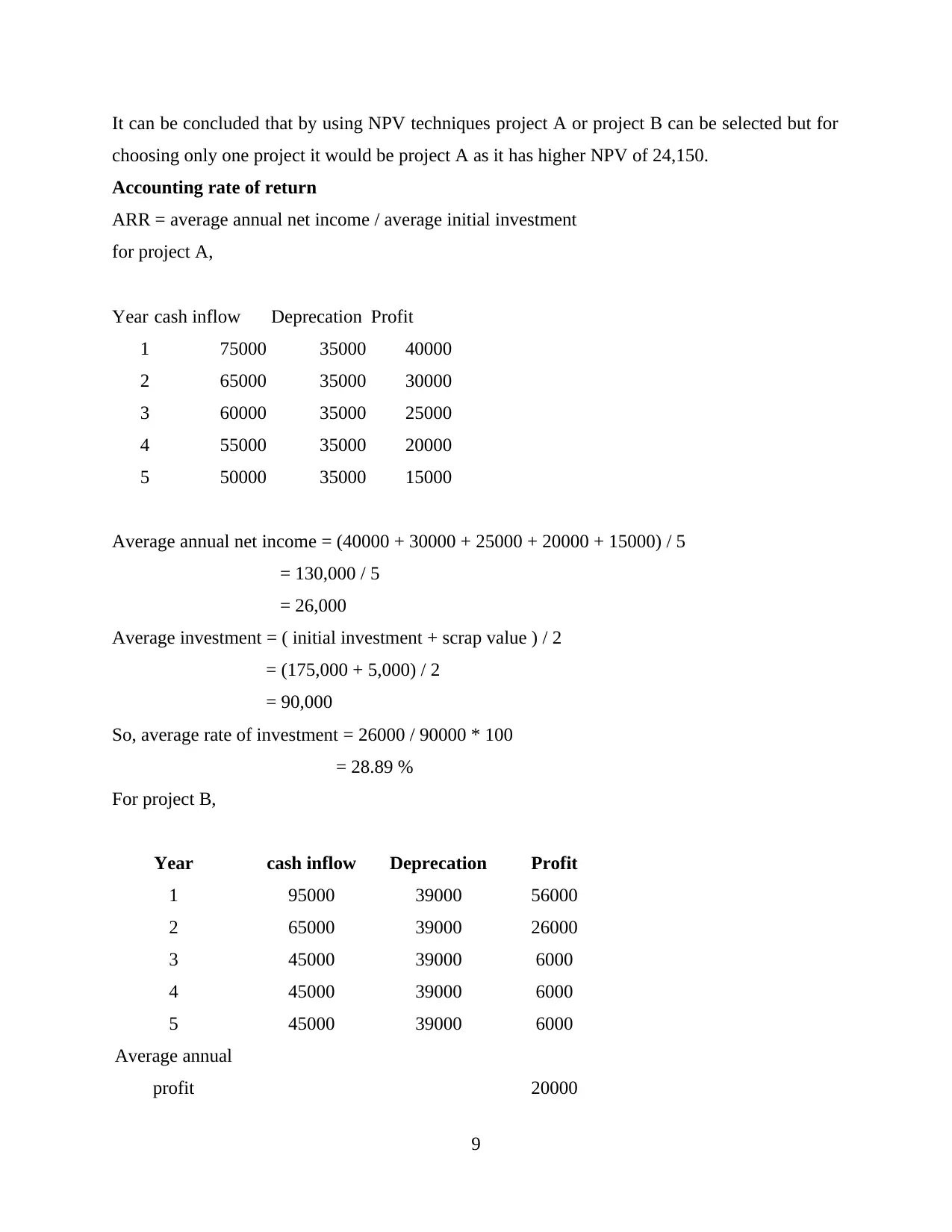

Accounting rate of return

ARR = average annual net income / average initial investment

for project A,

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual net income = (40000 + 30000 + 25000 + 20000 + 15000) / 5

= 130,000 / 5

= 26,000

Average investment = ( initial investment + scrap value ) / 2

= (175,000 + 5,000) / 2

= 90,000

So, average rate of investment = 26000 / 90000 * 100

= 28.89 %

For project B,

Year cash inflow Deprecation Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average annual

profit 20000

9

choosing only one project it would be project A as it has higher NPV of 24,150.

Accounting rate of return

ARR = average annual net income / average initial investment

for project A,

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual net income = (40000 + 30000 + 25000 + 20000 + 15000) / 5

= 130,000 / 5

= 26,000

Average investment = ( initial investment + scrap value ) / 2

= (175,000 + 5,000) / 2

= 90,000

So, average rate of investment = 26000 / 90000 * 100

= 28.89 %

For project B,

Year cash inflow Deprecation Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average annual

profit 20000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.