Management Accounting Report: Analysis of Zylla Company Finances

VerifiedAdded on 2020/11/23

|13

|3799

|195

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within the context of Zylla Company. It begins by defining management accounting and its essential requirements, differentiating it from financial accounting and exploring various management accounting systems such as cost accounting, inventory management, job costing, price optimization, and variable costing. The report then delves into different methods applied for management accounting reporting, including budgets, cost reports, performance reports, and accounts receivable aging reports. A key section focuses on calculating costs using marginal and absorption costing techniques, providing detailed income statements for Zylla Company. Furthermore, the report examines various planning tools and budgetary control systems, including master and capital budgets. Finally, it compares how organizations adapt management accounting systems to respond to financial problems, offering insights into Zylla Company's financial strategies. The report concludes with a summary of findings and recommendations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1: Understanding of management accounting systems........................................................1

P1 Management accounting and essential requirements of various types of management

accounting system..................................................................................................................1

P2 Different methods applied for management accounting reporting....................................2

TASK 2............................................................................................................................................3

P3 Calculating cost is appropriate tools and techniques in making income statements.........3

TASK 3............................................................................................................................................6

P4. Various kinds of planning tools and budgetary control system.......................................6

TASK 4............................................................................................................................................8

P5 Comparing organisation adapting management accounting systems to respond to financial

problems.................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1: Understanding of management accounting systems........................................................1

P1 Management accounting and essential requirements of various types of management

accounting system..................................................................................................................1

P2 Different methods applied for management accounting reporting....................................2

TASK 2............................................................................................................................................3

P3 Calculating cost is appropriate tools and techniques in making income statements.........3

TASK 3............................................................................................................................................6

P4. Various kinds of planning tools and budgetary control system.......................................6

TASK 4............................................................................................................................................8

P5 Comparing organisation adapting management accounting systems to respond to financial

problems.................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

The main objective of this report is to determine management accounting fundamentals

that are applied to the business environment as well as the corporations that are operated in that

environment. The report will also identify how management accounting uses financial data or

information in planning decision, monitoring and managing finance in Zylla Company or

business. The report will determine advantages and disadvantages of different types of planning

tools used in controlling budget. Furthermore, the report will also compare Zylla Company is

adapting management accounting systems to respond various financial issues or problems in an

organisation.

TASK 1: Understanding of management accounting systems.

P1 Management accounting and essential requirements of various types of management

accounting system

Management accounting refers to the procedure of identifying, measuring, interpreting,

communicating financial data or information in the achievement of the business goals and

objectives. It is also referred to us a cost accounting, the major difference between management

accounting and financial accounting is that information of management accounting helps

managers in a company to make effective decisions, on the other hand financial accounting is

aimed at providing data or information to the external parties of a company or organization. The

process of preparing management reports or accounts provides accurate and timely financial as

well as statistical information required by managers in establishing day to day decisions. It

consists reports that are developed in order to meet the needs of the management. Management

accounting systems differs in their applications, each and every system is designed for providing

different managerial information on the basis of management needs which helps in making

decisions. There are various kinds of managing accounting systems which are applied in an

organisation. However, all types of accounting systems help in achieving a common objective

and assist in analysing, identifying and communicating financial data in an organisation. The

different types of accounting systems are described as below -

Cost accounting system – The cost accounting system is a framework applied by an

organisation to analyse the cost of its products to analyse profit, cost control and

inventory valuation. Cost accounting is known as the most essential concept in

1

The main objective of this report is to determine management accounting fundamentals

that are applied to the business environment as well as the corporations that are operated in that

environment. The report will also identify how management accounting uses financial data or

information in planning decision, monitoring and managing finance in Zylla Company or

business. The report will determine advantages and disadvantages of different types of planning

tools used in controlling budget. Furthermore, the report will also compare Zylla Company is

adapting management accounting systems to respond various financial issues or problems in an

organisation.

TASK 1: Understanding of management accounting systems.

P1 Management accounting and essential requirements of various types of management

accounting system

Management accounting refers to the procedure of identifying, measuring, interpreting,

communicating financial data or information in the achievement of the business goals and

objectives. It is also referred to us a cost accounting, the major difference between management

accounting and financial accounting is that information of management accounting helps

managers in a company to make effective decisions, on the other hand financial accounting is

aimed at providing data or information to the external parties of a company or organization. The

process of preparing management reports or accounts provides accurate and timely financial as

well as statistical information required by managers in establishing day to day decisions. It

consists reports that are developed in order to meet the needs of the management. Management

accounting systems differs in their applications, each and every system is designed for providing

different managerial information on the basis of management needs which helps in making

decisions. There are various kinds of managing accounting systems which are applied in an

organisation. However, all types of accounting systems help in achieving a common objective

and assist in analysing, identifying and communicating financial data in an organisation. The

different types of accounting systems are described as below -

Cost accounting system – The cost accounting system is a framework applied by an

organisation to analyse the cost of its products to analyse profit, cost control and

inventory valuation. Cost accounting is known as the most essential concept in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management accounting as it provides the analytical tools like marginal costing,

budgetary-control, operating costing, standard costing and inventory control.

Inventory management – Inventory management refers to the technique of overseeing

and controlling the use, ordering and storage of elements which are applied by an

organisation in the production of the goods it offers. There are many functions of

inventory management such as developing purchase order, receiving, adjusting,

reallocating and disposing inventory. This management accounting system assist an

organisation to improve company workflow and enhance inventory accuracy (Fullerton,

Kennedy and Widener, 2017).

Job costing system – The job costing system refers to the system of allocating

production costs to the individual batches or item of goods. The job costing system needs

accumulating three types of direct information such as labour overhead and direct

material.

Price optimisation system – It refers to the application of statistical analysis to the

organisation or business in order to determine consumer reaction on different price for

their products and services.

Utilisation of data – Management accounting information provides data impelled look

at how to develop an effective organisation. The accounting data or information helps in

calculating day to day expenses such as operating cost, hence collecting, measuring and

analysing this data is essential.

Variable costing – As per the Generally accepted accounting principles, every single

cost of manufacturing products should be mentioned and recorded in the books of

account in an organisation. It assists in identifying the variable cost of production or

operation which is very essential to be determined n order to maintain an effective flow

of finance or money ion a company (Renz and Herman, 2017).

P2 Different methods applied for management accounting reporting

Management accounting is very much essential in order to have a look into concept that

there are many operations which organization need to precede as per the budget and actual

expenditure which business is having. Management accounting focuses on internal data and

information received through financial accounting. Management accounting is applied for

planning, controlling and making decisions. Managerial accountants depends upon financial

2

budgetary-control, operating costing, standard costing and inventory control.

Inventory management – Inventory management refers to the technique of overseeing

and controlling the use, ordering and storage of elements which are applied by an

organisation in the production of the goods it offers. There are many functions of

inventory management such as developing purchase order, receiving, adjusting,

reallocating and disposing inventory. This management accounting system assist an

organisation to improve company workflow and enhance inventory accuracy (Fullerton,

Kennedy and Widener, 2017).

Job costing system – The job costing system refers to the system of allocating

production costs to the individual batches or item of goods. The job costing system needs

accumulating three types of direct information such as labour overhead and direct

material.

Price optimisation system – It refers to the application of statistical analysis to the

organisation or business in order to determine consumer reaction on different price for

their products and services.

Utilisation of data – Management accounting information provides data impelled look

at how to develop an effective organisation. The accounting data or information helps in

calculating day to day expenses such as operating cost, hence collecting, measuring and

analysing this data is essential.

Variable costing – As per the Generally accepted accounting principles, every single

cost of manufacturing products should be mentioned and recorded in the books of

account in an organisation. It assists in identifying the variable cost of production or

operation which is very essential to be determined n order to maintain an effective flow

of finance or money ion a company (Renz and Herman, 2017).

P2 Different methods applied for management accounting reporting

Management accounting is very much essential in order to have a look into concept that

there are many operations which organization need to precede as per the budget and actual

expenditure which business is having. Management accounting focuses on internal data and

information received through financial accounting. Management accounting is applied for

planning, controlling and making decisions. Managerial accountants depends upon financial

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements consisting income statement, balance sheet and cash flow statement. The various

methods applied for reporting management accounting can be described as below -

1. Budgets – One of the major component of management accounting is preparing budgets,

Budgets are created by applying budgets of previous year and adjusting them to forecast

future. The budgets of an organisation includes all the revenues sources and expenses,

the company tries to achieve its goals and objectives staying within the budgeted amount.

2. Cost reports – Management accounting analyse or calculate the cost of products

produced. It is done by adding all the costs, raw product overhead, labour and extra cost

in consideration. The sum is then divided into amounts of products manufactured. All the

information or data is compacted in the cost report. This report allows managers to

identify and view the cost value of goods with respect to their selling price. It also helps

managers to plan and control profit margin.

3. Performance report – Management accountants apply budgets to compare expenses and

actual revenues to the budgeted amounts. The differences identified are analysed and

evaluated when shaping or designing new budgets and all data concerned to amounts is

listed within the performance report. These reports are computed every year, but some

organisations developed them monthly or quarterly. This report helps managers to plan

for the upcoming demand s in cost increment and production (Schaltegger and Burritt,

2016).

4. Accounts receivable ageing report – There are huge number of debtors of an

organization like the customers or clients who are yet to pay money to a company or

business. It can be delay in payment or any other issue which becomes a barrier I

payment of a product, services or an order. All these types of dents are recorded in this

type of report so that the organisation can identify the money or revenue yet to be

received.

TASK 2

P3 Calculating cost is appropriate tools and techniques in making income statements.

Marginal costing-

Marginal costing technique would not be including any kind of fixed overheads or cost

as it should be including only variable cost (Cooper, Ezzamel and Qu, 2017). Marginal costing is

3

methods applied for reporting management accounting can be described as below -

1. Budgets – One of the major component of management accounting is preparing budgets,

Budgets are created by applying budgets of previous year and adjusting them to forecast

future. The budgets of an organisation includes all the revenues sources and expenses,

the company tries to achieve its goals and objectives staying within the budgeted amount.

2. Cost reports – Management accounting analyse or calculate the cost of products

produced. It is done by adding all the costs, raw product overhead, labour and extra cost

in consideration. The sum is then divided into amounts of products manufactured. All the

information or data is compacted in the cost report. This report allows managers to

identify and view the cost value of goods with respect to their selling price. It also helps

managers to plan and control profit margin.

3. Performance report – Management accountants apply budgets to compare expenses and

actual revenues to the budgeted amounts. The differences identified are analysed and

evaluated when shaping or designing new budgets and all data concerned to amounts is

listed within the performance report. These reports are computed every year, but some

organisations developed them monthly or quarterly. This report helps managers to plan

for the upcoming demand s in cost increment and production (Schaltegger and Burritt,

2016).

4. Accounts receivable ageing report – There are huge number of debtors of an

organization like the customers or clients who are yet to pay money to a company or

business. It can be delay in payment or any other issue which becomes a barrier I

payment of a product, services or an order. All these types of dents are recorded in this

type of report so that the organisation can identify the money or revenue yet to be

received.

TASK 2

P3 Calculating cost is appropriate tools and techniques in making income statements.

Marginal costing-

Marginal costing technique would not be including any kind of fixed overheads or cost

as it should be including only variable cost (Cooper, Ezzamel and Qu, 2017). Marginal costing is

3

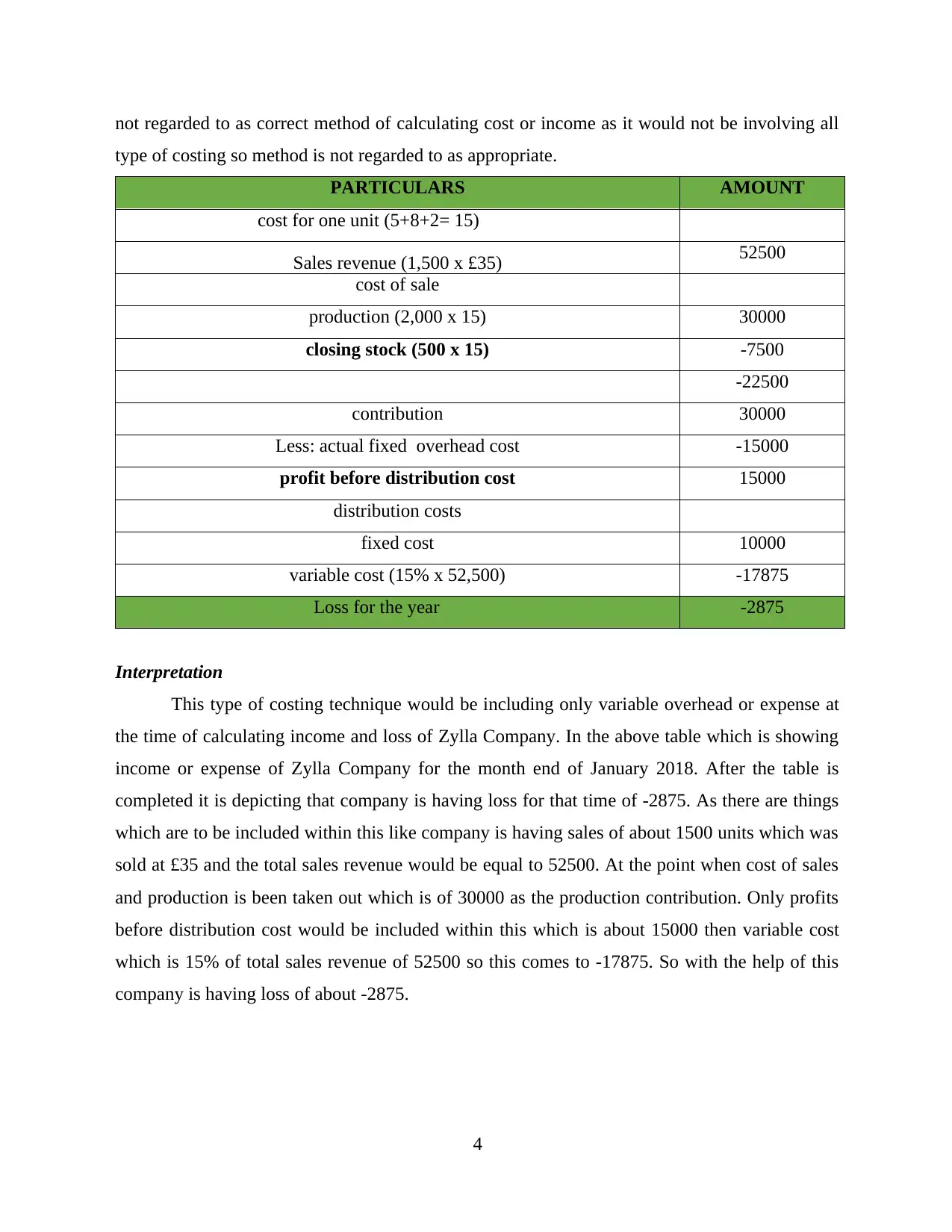

not regarded to as correct method of calculating cost or income as it would not be involving all

type of costing so method is not regarded to as appropriate.

PARTICULARS AMOUNT

cost for one unit (5+8+2= 15)

Sales revenue (1,500 x £35) 52500

cost of sale

production (2,000 x 15) 30000

closing stock (500 x 15) -7500

-22500

contribution 30000

Less: actual fixed overhead cost -15000

profit before distribution cost 15000

distribution costs

fixed cost 10000

variable cost (15% x 52,500) -17875

Loss for the year -2875

Interpretation

This type of costing technique would be including only variable overhead or expense at

the time of calculating income and loss of Zylla Company. In the above table which is showing

income or expense of Zylla Company for the month end of January 2018. After the table is

completed it is depicting that company is having loss for that time of -2875. As there are things

which are to be included within this like company is having sales of about 1500 units which was

sold at £35 and the total sales revenue would be equal to 52500. At the point when cost of sales

and production is been taken out which is of 30000 as the production contribution. Only profits

before distribution cost would be included within this which is about 15000 then variable cost

which is 15% of total sales revenue of 52500 so this comes to -17875. So with the help of this

company is having loss of about -2875.

4

type of costing so method is not regarded to as appropriate.

PARTICULARS AMOUNT

cost for one unit (5+8+2= 15)

Sales revenue (1,500 x £35) 52500

cost of sale

production (2,000 x 15) 30000

closing stock (500 x 15) -7500

-22500

contribution 30000

Less: actual fixed overhead cost -15000

profit before distribution cost 15000

distribution costs

fixed cost 10000

variable cost (15% x 52,500) -17875

Loss for the year -2875

Interpretation

This type of costing technique would be including only variable overhead or expense at

the time of calculating income and loss of Zylla Company. In the above table which is showing

income or expense of Zylla Company for the month end of January 2018. After the table is

completed it is depicting that company is having loss for that time of -2875. As there are things

which are to be included within this like company is having sales of about 1500 units which was

sold at £35 and the total sales revenue would be equal to 52500. At the point when cost of sales

and production is been taken out which is of 30000 as the production contribution. Only profits

before distribution cost would be included within this which is about 15000 then variable cost

which is 15% of total sales revenue of 52500 so this comes to -17875. So with the help of this

company is having loss of about -2875.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

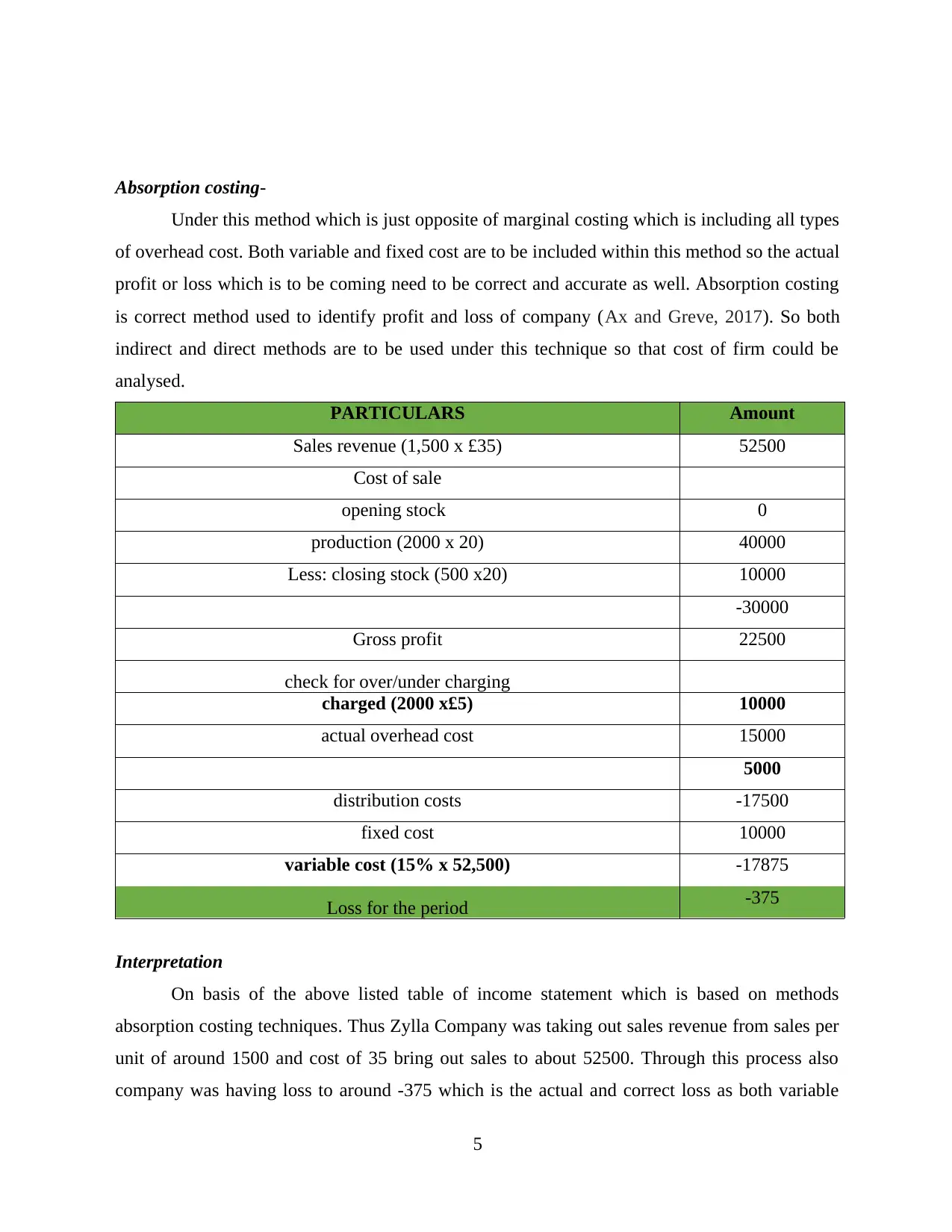

Absorption costing-

Under this method which is just opposite of marginal costing which is including all types

of overhead cost. Both variable and fixed cost are to be included within this method so the actual

profit or loss which is to be coming need to be correct and accurate as well. Absorption costing

is correct method used to identify profit and loss of company (Ax and Greve, 2017). So both

indirect and direct methods are to be used under this technique so that cost of firm could be

analysed.

PARTICULARS Amount

Sales revenue (1,500 x £35) 52500

Cost of sale

opening stock 0

production (2000 x 20) 40000

Less: closing stock (500 x20) 10000

-30000

Gross profit 22500

check for over/under charging

charged (2000 x£5) 10000

actual overhead cost 15000

5000

distribution costs -17500

fixed cost 10000

variable cost (15% x 52,500) -17875

Loss for the period -375

Interpretation

On basis of the above listed table of income statement which is based on methods

absorption costing techniques. Thus Zylla Company was taking out sales revenue from sales per

unit of around 1500 and cost of 35 bring out sales to about 52500. Through this process also

company was having loss to around -375 which is the actual and correct loss as both variable

5

Under this method which is just opposite of marginal costing which is including all types

of overhead cost. Both variable and fixed cost are to be included within this method so the actual

profit or loss which is to be coming need to be correct and accurate as well. Absorption costing

is correct method used to identify profit and loss of company (Ax and Greve, 2017). So both

indirect and direct methods are to be used under this technique so that cost of firm could be

analysed.

PARTICULARS Amount

Sales revenue (1,500 x £35) 52500

Cost of sale

opening stock 0

production (2000 x 20) 40000

Less: closing stock (500 x20) 10000

-30000

Gross profit 22500

check for over/under charging

charged (2000 x£5) 10000

actual overhead cost 15000

5000

distribution costs -17500

fixed cost 10000

variable cost (15% x 52,500) -17875

Loss for the period -375

Interpretation

On basis of the above listed table of income statement which is based on methods

absorption costing techniques. Thus Zylla Company was taking out sales revenue from sales per

unit of around 1500 and cost of 35 bring out sales to about 52500. Through this process also

company was having loss to around -375 which is the actual and correct loss as both variable

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and fixed cost to be included within this method. Thus it is regarded to company should be using

this absorption technique only which would be helping them to come with appropriate results

and company could be enhancing their operational activities. Zylla Company in order to

maintain maximum amount of profits need to include this absorption costing techniques so that

results would be generated.

All the management accounting techniques would be including firm to analyse the

financial profitability and maximising profits which company is earning (MITCHELL and

NØRREKLIT, 2017). On the bases of both marginal and absorption costing techniques income

was calculated which is showing or depicting profit or loss of company.

TASK 3

P4. Various kinds of planning tools and budgetary control system

Budgets is that proposal plan for company which is enabling firm to use all sources of

funds for that specified period of time so that they would be able to make assumptions of price

and profits of firm. This is very much important for company to implement use of correct

budgetary system so that they are to determine what profits they could made. All budgets would

be as per long or short run goal or objective of firm which is according to financial position and

cash flow statements as well. There are mainly two types of budget one is master and another

one is capital both of them are been prepared by company on bases of specified period of time.

Master budget-

This is the long term budget which is been prepared over certain time period and it would

be including all types of budget prepared by different departments like production or marketing

(Nielsen and Kristensen, 2017). All overheads and expenses are to be included like direct labour,

material and expense as well this would be involved under production department of firm. So all

budgets which are prepared by each of the departments would be called off and included to as

one master budget.

Capital budgets-

This type of budget would be related to only flow of capital both inflow and outflow

which is prepared in keeping into account all expenditure and income in respect to investments

made by firm.

6

this absorption technique only which would be helping them to come with appropriate results

and company could be enhancing their operational activities. Zylla Company in order to

maintain maximum amount of profits need to include this absorption costing techniques so that

results would be generated.

All the management accounting techniques would be including firm to analyse the

financial profitability and maximising profits which company is earning (MITCHELL and

NØRREKLIT, 2017). On the bases of both marginal and absorption costing techniques income

was calculated which is showing or depicting profit or loss of company.

TASK 3

P4. Various kinds of planning tools and budgetary control system

Budgets is that proposal plan for company which is enabling firm to use all sources of

funds for that specified period of time so that they would be able to make assumptions of price

and profits of firm. This is very much important for company to implement use of correct

budgetary system so that they are to determine what profits they could made. All budgets would

be as per long or short run goal or objective of firm which is according to financial position and

cash flow statements as well. There are mainly two types of budget one is master and another

one is capital both of them are been prepared by company on bases of specified period of time.

Master budget-

This is the long term budget which is been prepared over certain time period and it would

be including all types of budget prepared by different departments like production or marketing

(Nielsen and Kristensen, 2017). All overheads and expenses are to be included like direct labour,

material and expense as well this would be involved under production department of firm. So all

budgets which are prepared by each of the departments would be called off and included to as

one master budget.

Capital budgets-

This type of budget would be related to only flow of capital both inflow and outflow

which is prepared in keeping into account all expenditure and income in respect to investments

made by firm.

6

There are many techniques which are to be included within capital budgeting like that of

accounting rate of return and payback period method. Both of them are having their own

advantages and disadvantages which is included like that of:

Payback period-

If company is making any kind of investment in any project of certain amount then in

how much time the investment would be coming back for company (Tyagi, 2017). The time

which is taken by company the amount of cash inflow from the total amount which is invested

should be equal to cash outflow which is expressed in one year. Under this type of budgeting

control method how much time it would be taken to pay back the cost of project. All the project

which is not to be included within this payback period would not be included by company as

that would be exceeding the expected period.

Advantages of payback period method

The method is very easy to calculate and person could be easily understanding this

method.

The method is not incorporating any type of accounting profits as only focus is on flow

of cash over that period.

This technique would also be used as eliminating stage of projects which is not to be

used or applied as well.

In case of short terms project of firm both the important factor of business and financial

risk would be incorporated or used in this type of method (Lachmann, Trapp and Trapp,

2017).

At the time of those projects which are giving or generating huge amount of additional

cash is also good as this would be having capital rationing in this situation.

Disadvantage of payback period

The time which is taken in this type of method is clearly been ignored as only amount

which is invested should be coming back to company with tracking any time of that.

After the end of the project all cash flow and total amount returned would be ignored.

If two projects are having same payback period then it becomes impossible for company

to compare them both.

Accounting rate of return

7

accounting rate of return and payback period method. Both of them are having their own

advantages and disadvantages which is included like that of:

Payback period-

If company is making any kind of investment in any project of certain amount then in

how much time the investment would be coming back for company (Tyagi, 2017). The time

which is taken by company the amount of cash inflow from the total amount which is invested

should be equal to cash outflow which is expressed in one year. Under this type of budgeting

control method how much time it would be taken to pay back the cost of project. All the project

which is not to be included within this payback period would not be included by company as

that would be exceeding the expected period.

Advantages of payback period method

The method is very easy to calculate and person could be easily understanding this

method.

The method is not incorporating any type of accounting profits as only focus is on flow

of cash over that period.

This technique would also be used as eliminating stage of projects which is not to be

used or applied as well.

In case of short terms project of firm both the important factor of business and financial

risk would be incorporated or used in this type of method (Lachmann, Trapp and Trapp,

2017).

At the time of those projects which are giving or generating huge amount of additional

cash is also good as this would be having capital rationing in this situation.

Disadvantage of payback period

The time which is taken in this type of method is clearly been ignored as only amount

which is invested should be coming back to company with tracking any time of that.

After the end of the project all cash flow and total amount returned would be ignored.

If two projects are having same payback period then it becomes impossible for company

to compare them both.

Accounting rate of return

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

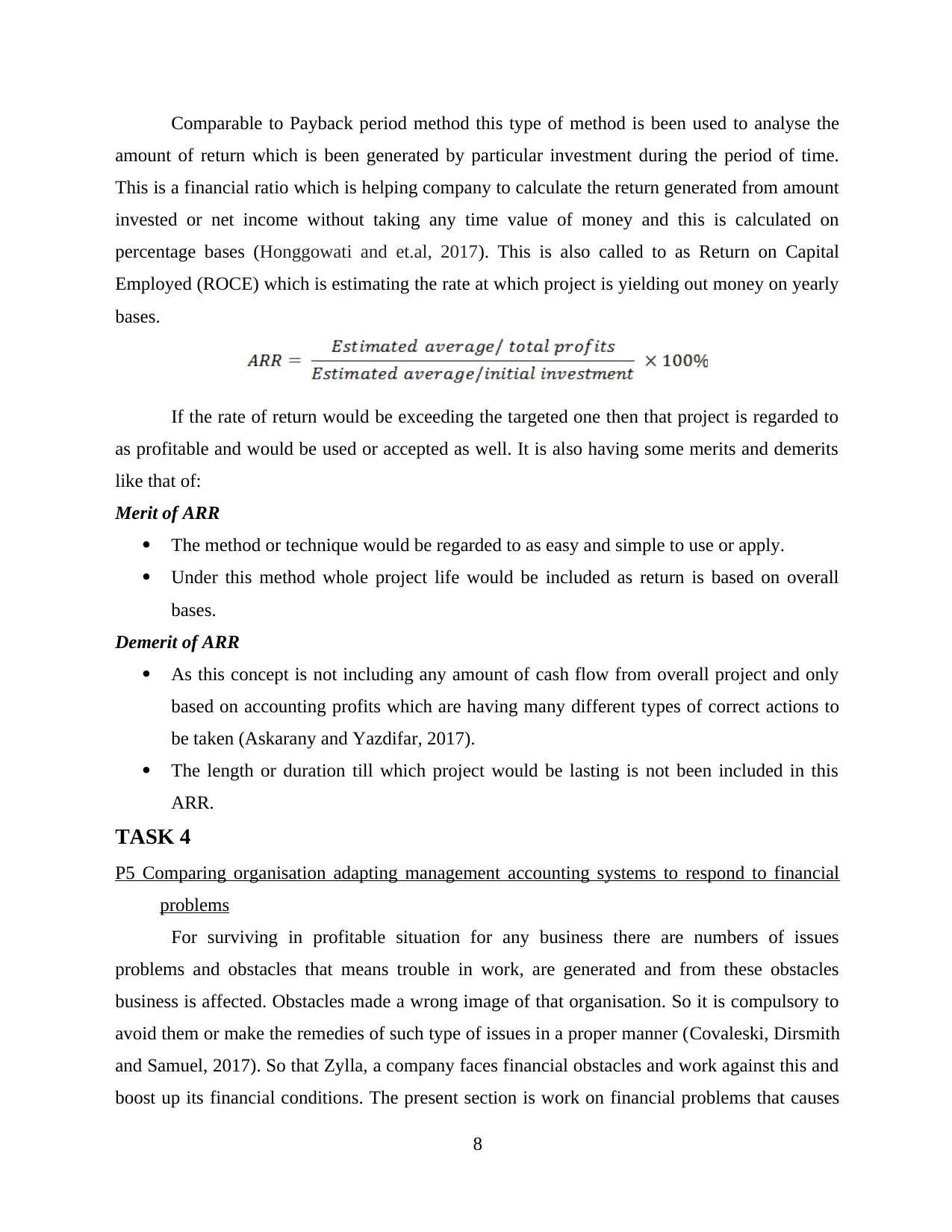

Comparable to Payback period method this type of method is been used to analyse the

amount of return which is been generated by particular investment during the period of time.

This is a financial ratio which is helping company to calculate the return generated from amount

invested or net income without taking any time value of money and this is calculated on

percentage bases (Honggowati and et.al, 2017). This is also called to as Return on Capital

Employed (ROCE) which is estimating the rate at which project is yielding out money on yearly

bases.

If the rate of return would be exceeding the targeted one then that project is regarded to

as profitable and would be used or accepted as well. It is also having some merits and demerits

like that of:

Merit of ARR

The method or technique would be regarded to as easy and simple to use or apply.

Under this method whole project life would be included as return is based on overall

bases.

Demerit of ARR

As this concept is not including any amount of cash flow from overall project and only

based on accounting profits which are having many different types of correct actions to

be taken (Askarany and Yazdifar, 2017).

The length or duration till which project would be lasting is not been included in this

ARR.

TASK 4

P5 Comparing organisation adapting management accounting systems to respond to financial

problems

For surviving in profitable situation for any business there are numbers of issues

problems and obstacles that means trouble in work, are generated and from these obstacles

business is affected. Obstacles made a wrong image of that organisation. So it is compulsory to

avoid them or make the remedies of such type of issues in a proper manner (Covaleski, Dirsmith

and Samuel, 2017). So that Zylla, a company faces financial obstacles and work against this and

boost up its financial conditions. The present section is work on financial problems that causes

8

amount of return which is been generated by particular investment during the period of time.

This is a financial ratio which is helping company to calculate the return generated from amount

invested or net income without taking any time value of money and this is calculated on

percentage bases (Honggowati and et.al, 2017). This is also called to as Return on Capital

Employed (ROCE) which is estimating the rate at which project is yielding out money on yearly

bases.

If the rate of return would be exceeding the targeted one then that project is regarded to

as profitable and would be used or accepted as well. It is also having some merits and demerits

like that of:

Merit of ARR

The method or technique would be regarded to as easy and simple to use or apply.

Under this method whole project life would be included as return is based on overall

bases.

Demerit of ARR

As this concept is not including any amount of cash flow from overall project and only

based on accounting profits which are having many different types of correct actions to

be taken (Askarany and Yazdifar, 2017).

The length or duration till which project would be lasting is not been included in this

ARR.

TASK 4

P5 Comparing organisation adapting management accounting systems to respond to financial

problems

For surviving in profitable situation for any business there are numbers of issues

problems and obstacles that means trouble in work, are generated and from these obstacles

business is affected. Obstacles made a wrong image of that organisation. So it is compulsory to

avoid them or make the remedies of such type of issues in a proper manner (Covaleski, Dirsmith

and Samuel, 2017). So that Zylla, a company faces financial obstacles and work against this and

boost up its financial conditions. The present section is work on financial problems that causes

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reduce profit and revenue, declining return on investment, increasing cost and expenses. Further

management of Zylla is determining various systems of management accounting in order to

make better the workplace with reducing these types of issues.

In addition, these all systems or methods are determined under-

Financial Governance– for solving all the financial related problems, some part of corporate

governance are help within the work place of Zylla is called Financial Governance. It applies for

showing that how to use financial resources by employees of organisation. Possible solutions

made by utilising various effective techniques only when if outcome are not desired. From use

of this method problems related to can be easily solve out and performance of Zylla is to be

improve.

Balance Scorecard– in the industry it is one of the best technique for assessing business

performance. Next, it consists of basically four functions these are financial, customer, learning

and growth as well as growth. By utilising the first most effective technique, Zylla calculate

various financial aspects and on the basis of that it finds that how's going performance well or

not (Nguyen, 2018). If any problem occurred then it must be clear by BSC technique.

Variance Analysis– a different approach of management accounting is to determine variance

analysis. In this technique budgeted and real data both are compared with each other. In Zylla

capable to achieve forecasted information then it can say that business is performed in well

condition in their industry. On other side if objectives are not get then proper action will be used

for improve the results and reached the better position in their respective sector

CONCLUSION

Arranged the base of directly above report, it can be decided that here has been

assessment of numerous costing and budgeting methods. Various reporting methods and the

performance appraisals existed and appraised which in turn show to be obliging for Zylla

Company executives to make all the pertinent evidence which are upsetting working enactment

of commercial. More, there have been calculations which are relevant with the marginal and an

absorption costing system which in turn characterises that absorption costing will be helpful for

managers as it carries the maximum suitable consequences. Afterward the procedure the

preparation tools then they will simply be employment in resolving the monetary difficulties to

withstand in the marketplace in addition for the accomplishment of Zylla Company. The

application will formerly be controlled by the advanced authority to see that around is no

9

management of Zylla is determining various systems of management accounting in order to

make better the workplace with reducing these types of issues.

In addition, these all systems or methods are determined under-

Financial Governance– for solving all the financial related problems, some part of corporate

governance are help within the work place of Zylla is called Financial Governance. It applies for

showing that how to use financial resources by employees of organisation. Possible solutions

made by utilising various effective techniques only when if outcome are not desired. From use

of this method problems related to can be easily solve out and performance of Zylla is to be

improve.

Balance Scorecard– in the industry it is one of the best technique for assessing business

performance. Next, it consists of basically four functions these are financial, customer, learning

and growth as well as growth. By utilising the first most effective technique, Zylla calculate

various financial aspects and on the basis of that it finds that how's going performance well or

not (Nguyen, 2018). If any problem occurred then it must be clear by BSC technique.

Variance Analysis– a different approach of management accounting is to determine variance

analysis. In this technique budgeted and real data both are compared with each other. In Zylla

capable to achieve forecasted information then it can say that business is performed in well

condition in their industry. On other side if objectives are not get then proper action will be used

for improve the results and reached the better position in their respective sector

CONCLUSION

Arranged the base of directly above report, it can be decided that here has been

assessment of numerous costing and budgeting methods. Various reporting methods and the

performance appraisals existed and appraised which in turn show to be obliging for Zylla

Company executives to make all the pertinent evidence which are upsetting working enactment

of commercial. More, there have been calculations which are relevant with the marginal and an

absorption costing system which in turn characterises that absorption costing will be helpful for

managers as it carries the maximum suitable consequences. Afterward the procedure the

preparation tools then they will simply be employment in resolving the monetary difficulties to

withstand in the marketplace in addition for the accomplishment of Zylla Company. The

application will formerly be controlled by the advanced authority to see that around is no

9

consumption of the capitals of the firm. If the firm is intelligent to resolve the problem of all the

fiscal matter. The maintainable accomplishment of business is also very significant. If the firm

essential to revenue out the income of year then they will commercial performance in Zylla

Company.

10

fiscal matter. The maintainable accomplishment of business is also very significant. If the firm

essential to revenue out the income of year then they will commercial performance in Zylla

Company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.