Analyzing Financial and Non-Financial Performance: Next Plc & H&M

VerifiedAdded on 2020/01/28

|13

|2965

|155

Report

AI Summary

This report presents a comprehensive financial analysis of Next Plc and H&M, evaluating their performance using profitability and efficiency ratios. It compares their financial strengths and weaknesses, offering recommendations for improvement. The report also delves into investment appraisal techniques, including payback period, net present value (NPV), and average rate of return (ARR), to aid in making sound investment decisions. The analysis covers the cash inflows of different projects, calculates the payback period, and determines the NPV and ARR to assess the viability of investment options. Furthermore, the report acknowledges the limitations of financial ratios and investment appraisal techniques, providing a balanced perspective on their application in financial analysis and decision-making.

Accounting and Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...............................................................................................................................3

Question 1.............................................................................................................................................3

1. Analyzing financial and non-financial performance of Next Plc and H&M...............................3

2. Using charts to compare the performance of two companies .....................................................5

3. Recommending the ways through which Next plc and H&M can improve its financial

performance ....................................................................................................................................7

4. Stating the limitations of financial ratios.....................................................................................7

Question 2.............................................................................................................................................8

1. Using investment appraisal techniques for making the best investment decisions.....................8

Cash inflow of project 2...................................................................................................................8

2. Stating the limitations of investment appraisal techniques........................................................10

CONCLUSION..................................................................................................................................10

References..........................................................................................................................................12

2

INTRODUCTION ...............................................................................................................................3

Question 1.............................................................................................................................................3

1. Analyzing financial and non-financial performance of Next Plc and H&M...............................3

2. Using charts to compare the performance of two companies .....................................................5

3. Recommending the ways through which Next plc and H&M can improve its financial

performance ....................................................................................................................................7

4. Stating the limitations of financial ratios.....................................................................................7

Question 2.............................................................................................................................................8

1. Using investment appraisal techniques for making the best investment decisions.....................8

Cash inflow of project 2...................................................................................................................8

2. Stating the limitations of investment appraisal techniques........................................................10

CONCLUSION..................................................................................................................................10

References..........................................................................................................................................12

2

INTRODUCTION

Accounting is the main part of finance which provides deeper insight to the manager about

the monetary transaction which are made by them during the accounting year. By making thorough

analysis of such aspects finance manager can make strategic decisions (Gitman, 2013). Further,

investment appraisal techniques are also the most effectual tool which helps manager in making

suitable investment decision which aid in the growth and profitability of it. This report is based on

the different case scenarios. The present report will shed light on the financial health and

performance of H&M and Next plc. It will also describe the extent to which capital budgeting tool

helps Hilltop Ltd. In making best investment decisions.

QUESTION 1

1. Analyzing financial and non-financial performance of Next Plc and H&M

Financial ratios: It refers to those which helps in evaluating the financial health, position and

performance of the enterprise are as follows:

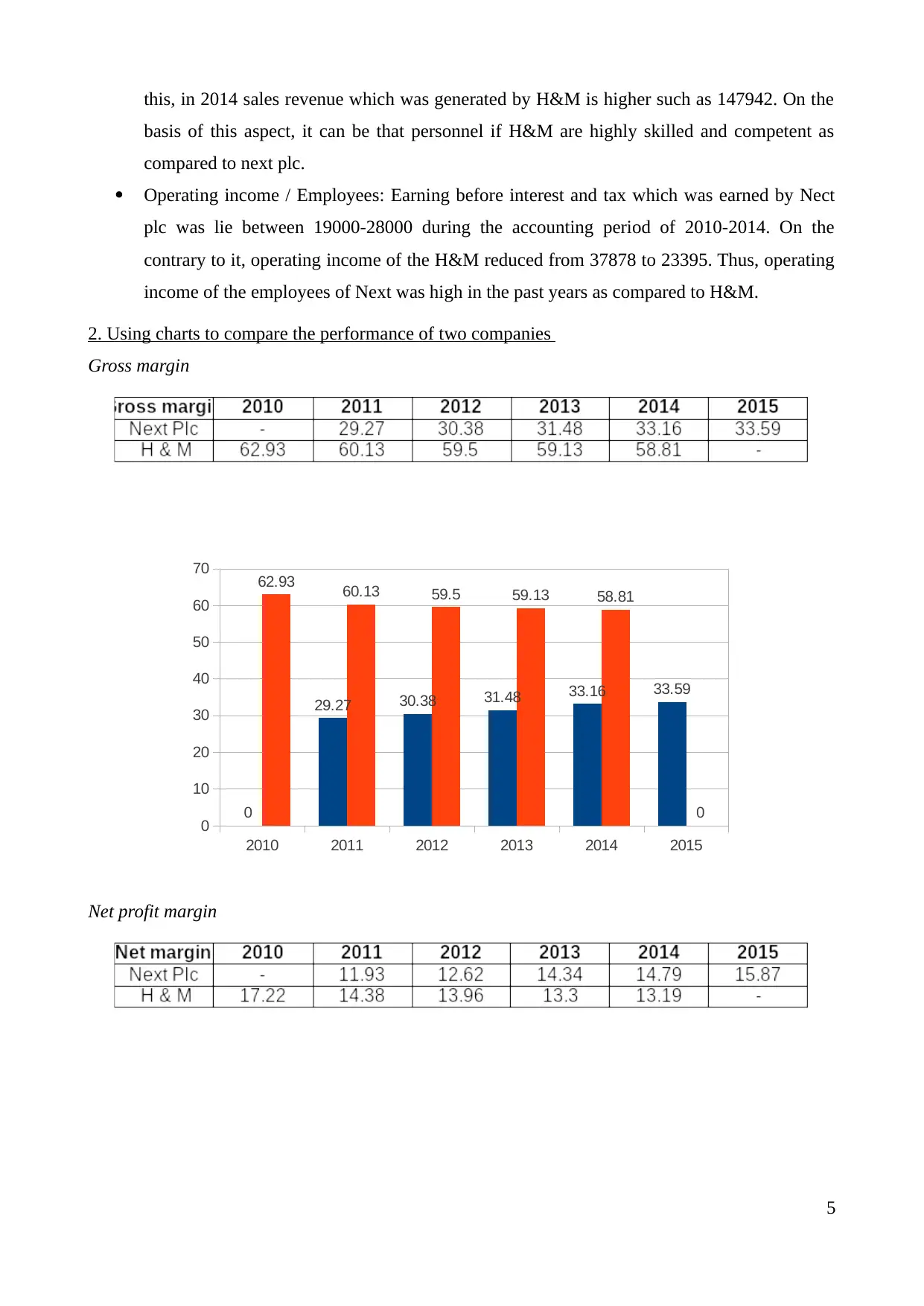

Profitability ratios Gross profit margin: In 2011 and 2012, gross profitability of Next plc was 29.27% &

30.38%. Whereas in 2015, GP ratio of the firm was 33.59% which shows that gross margin

of the business unit is get inclined. In comparison to Next plc, gross profitability of H&M

had reduced from 2010 to 2014 in terms of 62.93% to 58.81%. Thus , it can be said that

H&M failed to generate high amount of sales over the expenses in 2015 as compared to

Next plc. Net profit margin: This measure provides deeper insight about the profit which is generated

by them during the year after paying the tax amount. Net profit margin of Next Plc was

increased from 11.93% to 15.87%. This, profit margin of the firm increased in last five

years. Whereas, net profit margin of H&M showed declining trend in the performance. In

2010 NP ratio of H&M was 17.22% and it reached on 13.19%. Low sales may be cause of

declining trend in the net profitability of the business unit.

COGS /Revenue: It represents the revenue which is generated by the firm by incurring the

indirect expenses. During the financial year 2011, this ratio of Nest plc was 69.62%,

whereas COGS/revenue percentage of H&M is 39.87%. This ratio of H&M was increased

from 37.047% to 41.19%. On the contrary to it, in 2015 COGS /Revenue of Next plc was

66.41%. By referring this aspect it can be said that sales revenue of Nect plc had decreased

over the past years.

3

Accounting is the main part of finance which provides deeper insight to the manager about

the monetary transaction which are made by them during the accounting year. By making thorough

analysis of such aspects finance manager can make strategic decisions (Gitman, 2013). Further,

investment appraisal techniques are also the most effectual tool which helps manager in making

suitable investment decision which aid in the growth and profitability of it. This report is based on

the different case scenarios. The present report will shed light on the financial health and

performance of H&M and Next plc. It will also describe the extent to which capital budgeting tool

helps Hilltop Ltd. In making best investment decisions.

QUESTION 1

1. Analyzing financial and non-financial performance of Next Plc and H&M

Financial ratios: It refers to those which helps in evaluating the financial health, position and

performance of the enterprise are as follows:

Profitability ratios Gross profit margin: In 2011 and 2012, gross profitability of Next plc was 29.27% &

30.38%. Whereas in 2015, GP ratio of the firm was 33.59% which shows that gross margin

of the business unit is get inclined. In comparison to Next plc, gross profitability of H&M

had reduced from 2010 to 2014 in terms of 62.93% to 58.81%. Thus , it can be said that

H&M failed to generate high amount of sales over the expenses in 2015 as compared to

Next plc. Net profit margin: This measure provides deeper insight about the profit which is generated

by them during the year after paying the tax amount. Net profit margin of Next Plc was

increased from 11.93% to 15.87%. This, profit margin of the firm increased in last five

years. Whereas, net profit margin of H&M showed declining trend in the performance. In

2010 NP ratio of H&M was 17.22% and it reached on 13.19%. Low sales may be cause of

declining trend in the net profitability of the business unit.

COGS /Revenue: It represents the revenue which is generated by the firm by incurring the

indirect expenses. During the financial year 2011, this ratio of Nest plc was 69.62%,

whereas COGS/revenue percentage of H&M is 39.87%. This ratio of H&M was increased

from 37.047% to 41.19%. On the contrary to it, in 2015 COGS /Revenue of Next plc was

66.41%. By referring this aspect it can be said that sales revenue of Nect plc had decreased

over the past years.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency ratio Asset turnover: By taking into account the performance of Next plc it can be said that it

failed to generate enough amount of sales from assets. In 2015 asset turnover ratio of Nect

plc was 1.81:1 which shows decreasing trend in the performance of firm. As compared o

this, asset tu rover ratio of H&M had increased from 1.91:1 to 2.14:1. This aspect clearly

shows that H&M had made effective use of their assets in against to Next plc.

Receivable turnover: Next plc had received payment more earlier in period of 2015 in

comparison to the before years. Receivable turnover of Next plc reduced from 6.14:1 to

5.45. Receivable turnover of H&M was more high such as 11.02 in 2014 as compared to

Nect plc. High turnover closely influence the day to day operations of the firm.

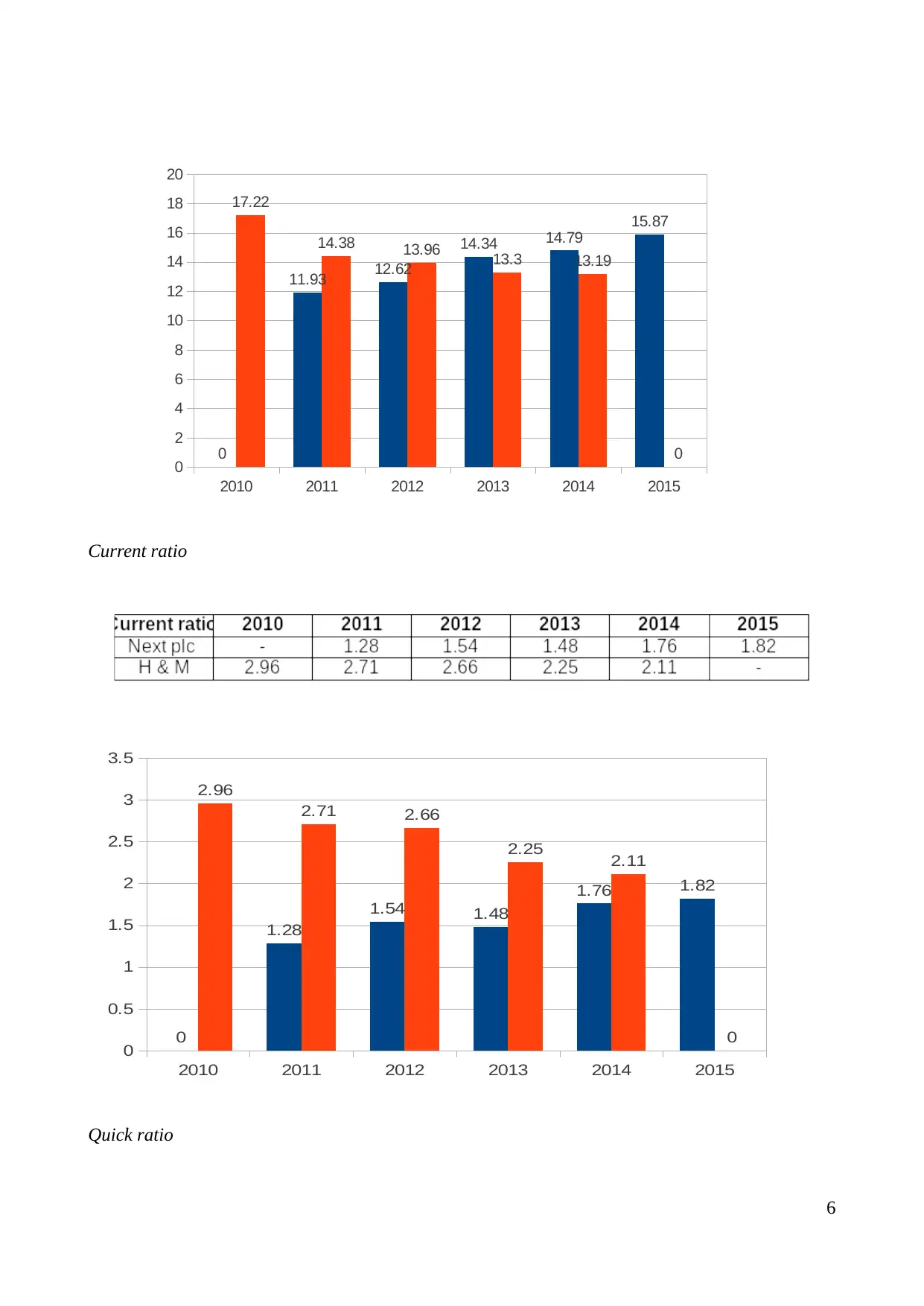

Financial strengths Current ratio: Ratio analysis represents that financial capability of Next plc is continuously

increasing in terms of 1.28 to 1.82. Further, current ratio of H&M was 2.11 in the

accounting year 2014. Thus, both the company has ability to fulfil their financial obligations

within the suitable time frame.

Quick ratio: Next plc and H&M both had maintained high level of current which can be

easily convertible into cash. Thus, Next plc and H&M can build good image in the mind of

stakeholders by meeting the short term obligations on time.

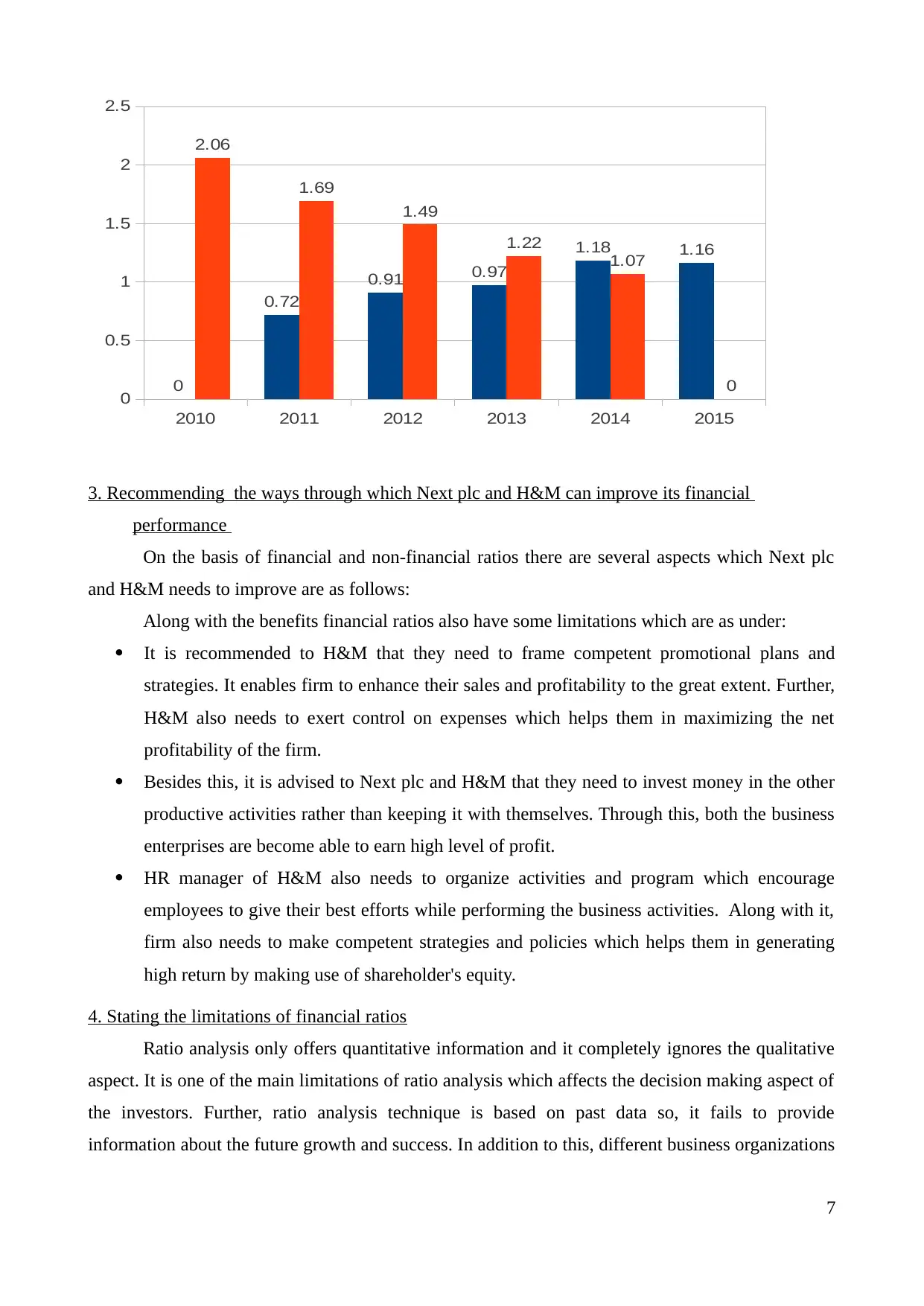

Debt-equity ratio: By doing ratio analysis it has been assessed that Next plc had met most of

its financial needs from debt instruments rather than equity. Debt-equity ratio of Next plc

inclined from 2.57 to 2.661 which is not good for the company.

Pay out ratio: Next plc had paid less dividend to the shareholders from their earnings in

comparison to H&M. In 2014, pay out ratio of Nect plc was 35.04% which is highly lower

as compared to H&M who paid 80.78% earnings to the shareholders in the form of

dividend.

Management effectiveness

Return on equity: Financial ratios clearly shows that Next plc had made optimum use of

equity in relation to the generation of sales (Liao and et.al., 2012). Return which was earned

by H&M is more less as compared to Next plc.

Non-financial ratios: Theses ratios are those which include employee productivity and profitability,

turnover, absenteeism rate etc. to measure the effectiveness of business organization (Chen and

Gavious, 2016).

Revenue / Employees: This ratio states that human resources of Next plc had generated high

sales revenue by performing their activities more effectively and efficiently. In contrast to

4

failed to generate enough amount of sales from assets. In 2015 asset turnover ratio of Nect

plc was 1.81:1 which shows decreasing trend in the performance of firm. As compared o

this, asset tu rover ratio of H&M had increased from 1.91:1 to 2.14:1. This aspect clearly

shows that H&M had made effective use of their assets in against to Next plc.

Receivable turnover: Next plc had received payment more earlier in period of 2015 in

comparison to the before years. Receivable turnover of Next plc reduced from 6.14:1 to

5.45. Receivable turnover of H&M was more high such as 11.02 in 2014 as compared to

Nect plc. High turnover closely influence the day to day operations of the firm.

Financial strengths Current ratio: Ratio analysis represents that financial capability of Next plc is continuously

increasing in terms of 1.28 to 1.82. Further, current ratio of H&M was 2.11 in the

accounting year 2014. Thus, both the company has ability to fulfil their financial obligations

within the suitable time frame.

Quick ratio: Next plc and H&M both had maintained high level of current which can be

easily convertible into cash. Thus, Next plc and H&M can build good image in the mind of

stakeholders by meeting the short term obligations on time.

Debt-equity ratio: By doing ratio analysis it has been assessed that Next plc had met most of

its financial needs from debt instruments rather than equity. Debt-equity ratio of Next plc

inclined from 2.57 to 2.661 which is not good for the company.

Pay out ratio: Next plc had paid less dividend to the shareholders from their earnings in

comparison to H&M. In 2014, pay out ratio of Nect plc was 35.04% which is highly lower

as compared to H&M who paid 80.78% earnings to the shareholders in the form of

dividend.

Management effectiveness

Return on equity: Financial ratios clearly shows that Next plc had made optimum use of

equity in relation to the generation of sales (Liao and et.al., 2012). Return which was earned

by H&M is more less as compared to Next plc.

Non-financial ratios: Theses ratios are those which include employee productivity and profitability,

turnover, absenteeism rate etc. to measure the effectiveness of business organization (Chen and

Gavious, 2016).

Revenue / Employees: This ratio states that human resources of Next plc had generated high

sales revenue by performing their activities more effectively and efficiently. In contrast to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this, in 2014 sales revenue which was generated by H&M is higher such as 147942. On the

basis of this aspect, it can be that personnel if H&M are highly skilled and competent as

compared to next plc.

Operating income / Employees: Earning before interest and tax which was earned by Nect

plc was lie between 19000-28000 during the accounting period of 2010-2014. On the

contrary to it, operating income of the H&M reduced from 37878 to 23395. Thus, operating

income of the employees of Next was high in the past years as compared to H&M.

2. Using charts to compare the performance of two companies

Gross margin

Net profit margin

5

2010 2011 2012 2013 2014 2015

0

10

20

30

40

50

60

70

0

29.27 30.38 31.48 33.16 33.59

62.93 60.13 59.5 59.13 58.81

0

basis of this aspect, it can be that personnel if H&M are highly skilled and competent as

compared to next plc.

Operating income / Employees: Earning before interest and tax which was earned by Nect

plc was lie between 19000-28000 during the accounting period of 2010-2014. On the

contrary to it, operating income of the H&M reduced from 37878 to 23395. Thus, operating

income of the employees of Next was high in the past years as compared to H&M.

2. Using charts to compare the performance of two companies

Gross margin

Net profit margin

5

2010 2011 2012 2013 2014 2015

0

10

20

30

40

50

60

70

0

29.27 30.38 31.48 33.16 33.59

62.93 60.13 59.5 59.13 58.81

0

Current ratio

Quick ratio

6

2010 2011 2012 2013 2014 2015

0

2

4

6

8

10

12

14

16

18

20

0

11.93 12.62

14.34 14.79

15.87

17.22

14.38 13.96 13.3 13.19

0

2010 2011 2012 2013 2014 2015

0

0.5

1

1.5

2

2.5

3

3.5

0

1.28

1.54 1.48

1.76 1.82

2.96

2.71 2.66

2.25 2.11

0

Quick ratio

6

2010 2011 2012 2013 2014 2015

0

2

4

6

8

10

12

14

16

18

20

0

11.93 12.62

14.34 14.79

15.87

17.22

14.38 13.96 13.3 13.19

0

2010 2011 2012 2013 2014 2015

0

0.5

1

1.5

2

2.5

3

3.5

0

1.28

1.54 1.48

1.76 1.82

2.96

2.71 2.66

2.25 2.11

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Recommending the ways through which Next plc and H&M can improve its financial

performance

On the basis of financial and non-financial ratios there are several aspects which Next plc

and H&M needs to improve are as follows:

Along with the benefits financial ratios also have some limitations which are as under:

It is recommended to H&M that they need to frame competent promotional plans and

strategies. It enables firm to enhance their sales and profitability to the great extent. Further,

H&M also needs to exert control on expenses which helps them in maximizing the net

profitability of the firm.

Besides this, it is advised to Next plc and H&M that they need to invest money in the other

productive activities rather than keeping it with themselves. Through this, both the business

enterprises are become able to earn high level of profit.

HR manager of H&M also needs to organize activities and program which encourage

employees to give their best efforts while performing the business activities. Along with it,

firm also needs to make competent strategies and policies which helps them in generating

high return by making use of shareholder's equity.

4. Stating the limitations of financial ratios

Ratio analysis only offers quantitative information and it completely ignores the qualitative

aspect. It is one of the main limitations of ratio analysis which affects the decision making aspect of

the investors. Further, ratio analysis technique is based on past data so, it fails to provide

information about the future growth and success. In addition to this, different business organizations

7

2010 2011 2012 2013 2014 2015

0

0.5

1

1.5

2

2.5

0

0.72

0.91 0.97

1.18 1.16

2.06

1.69

1.49

1.22

1.07

0

performance

On the basis of financial and non-financial ratios there are several aspects which Next plc

and H&M needs to improve are as follows:

Along with the benefits financial ratios also have some limitations which are as under:

It is recommended to H&M that they need to frame competent promotional plans and

strategies. It enables firm to enhance their sales and profitability to the great extent. Further,

H&M also needs to exert control on expenses which helps them in maximizing the net

profitability of the firm.

Besides this, it is advised to Next plc and H&M that they need to invest money in the other

productive activities rather than keeping it with themselves. Through this, both the business

enterprises are become able to earn high level of profit.

HR manager of H&M also needs to organize activities and program which encourage

employees to give their best efforts while performing the business activities. Along with it,

firm also needs to make competent strategies and policies which helps them in generating

high return by making use of shareholder's equity.

4. Stating the limitations of financial ratios

Ratio analysis only offers quantitative information and it completely ignores the qualitative

aspect. It is one of the main limitations of ratio analysis which affects the decision making aspect of

the investors. Further, ratio analysis technique is based on past data so, it fails to provide

information about the future growth and success. In addition to this, different business organizations

7

2010 2011 2012 2013 2014 2015

0

0.5

1

1.5

2

2.5

0

0.72

0.91 0.97

1.18 1.16

2.06

1.69

1.49

1.22

1.07

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

follow varied accounting rules and principles while framing the financial statements for firm

(Kumbirai and Webb, 2013). In this, it is highly difficult for the business unit to make comparison

of the financial performance of one firm with another. Varied environmental condition and market

structure also have high level of influence on the financial performance of firm. Further, economic

condition such as inflation or deflation is also affects the financials of the business enterprise

(Limitations of ratio analysis, 2013). Moreover, economic conditions are not remains same in each

year. Strategies which are employed by the manager also differs from business to business (Karande

and Chakraborty, 2012). Thus, all these aspects negatively hampers the significance of ration

analysis to some extent.

QUESTION 2

1. Using investment appraisal techniques for making the best investment decisions

Capital budgeting or investment appraisal tools include payback period, net present value

and average rate of return method which helps manager in assessing the profitability of project

(Dellavigna and Pollet, 2013). These tools and techniques assist investment manager of Hilltop Ltd.

in the selection of project which offers high return to them.

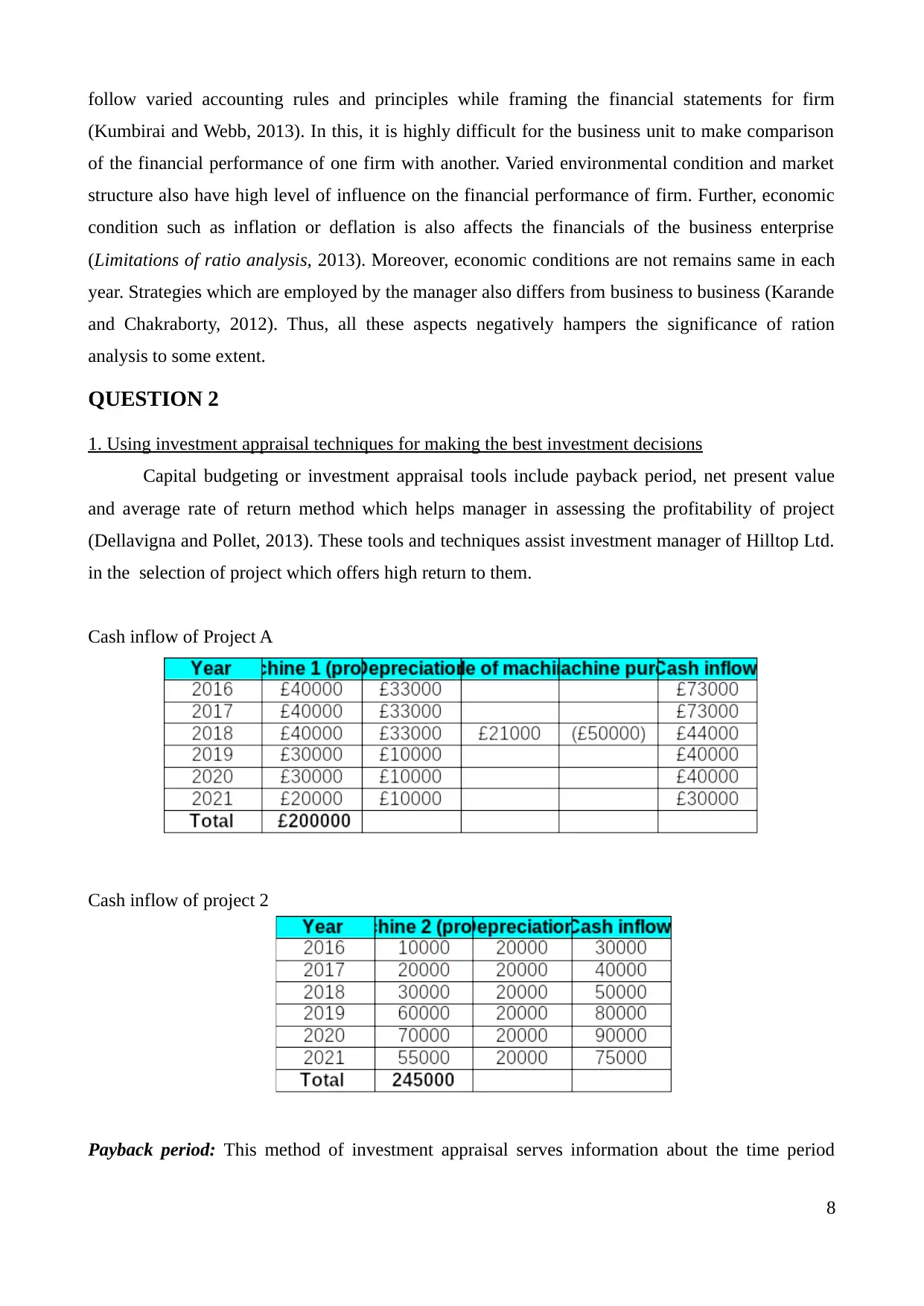

Cash inflow of Project A

Cash inflow of project 2

Payback period: This method of investment appraisal serves information about the time period

8

(Kumbirai and Webb, 2013). In this, it is highly difficult for the business unit to make comparison

of the financial performance of one firm with another. Varied environmental condition and market

structure also have high level of influence on the financial performance of firm. Further, economic

condition such as inflation or deflation is also affects the financials of the business enterprise

(Limitations of ratio analysis, 2013). Moreover, economic conditions are not remains same in each

year. Strategies which are employed by the manager also differs from business to business (Karande

and Chakraborty, 2012). Thus, all these aspects negatively hampers the significance of ration

analysis to some extent.

QUESTION 2

1. Using investment appraisal techniques for making the best investment decisions

Capital budgeting or investment appraisal tools include payback period, net present value

and average rate of return method which helps manager in assessing the profitability of project

(Dellavigna and Pollet, 2013). These tools and techniques assist investment manager of Hilltop Ltd.

in the selection of project which offers high return to them.

Cash inflow of Project A

Cash inflow of project 2

Payback period: This method of investment appraisal serves information about the time period

8

within which business organization can recover its initial investment.

Computation of pay back period

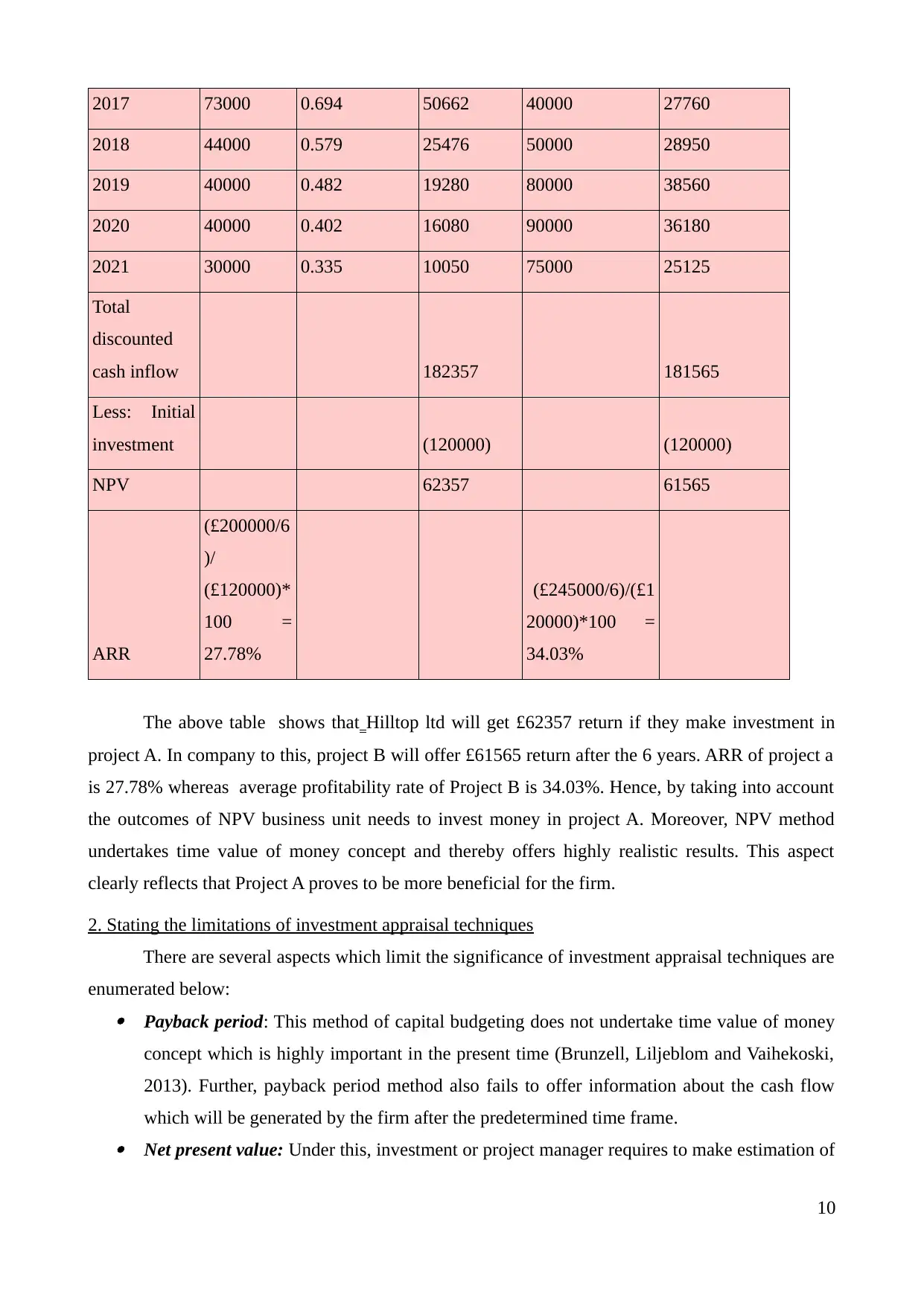

Year Project A Project B

Cash inflow in

£)

Cumulative cash

inflow ( in £)

Cash inflow£) Cumulative cash

inflow (in £)

2016 73000 73000 30000 30000

2017 73000 146000 40000 70000

2018 44000 190000 50000 120000

2019 40000 230000 80000 200000

2020 40000 270000 90000 290000

2021 30000 300000 75000 365000

Machine A: 1+ (47000 / 73000) = 1.64 years

Machine B: 3 year in which cumulative cash inflow is equal to the initial investment

On the basis of above mentioned calculation it has been analyzing that Hilltop Ltd. has to

wait for 1 year and 6 months to recover the initial amount which is invested by the organization in

machine 1. On the contrary to it, for machine B business unit will take 3 years to get back the

investment which is primarily invested by the firm. Thus, Hilltop ltd needs to make investment in

project A over the project B.

Net present value (NPV) and Average rate of return (ARR): Net present value method entail

the return which business unit will earn after the predetermined time period (Dellavigna and Pollet,

2013). Whereas, ARR method helps in identifying the average return which business unit will get

during the time frame.

Computation of NPV

Year Project A Project B

Cash

inflow (In

£)

Discounting

factor @20%

Discouted

cash inflow

(In £)

Cash inflow (In

£)

Discouted cash

inflow (In £)

2016 73000 0.833 60809 30000 24990

9

Computation of pay back period

Year Project A Project B

Cash inflow in

£)

Cumulative cash

inflow ( in £)

Cash inflow£) Cumulative cash

inflow (in £)

2016 73000 73000 30000 30000

2017 73000 146000 40000 70000

2018 44000 190000 50000 120000

2019 40000 230000 80000 200000

2020 40000 270000 90000 290000

2021 30000 300000 75000 365000

Machine A: 1+ (47000 / 73000) = 1.64 years

Machine B: 3 year in which cumulative cash inflow is equal to the initial investment

On the basis of above mentioned calculation it has been analyzing that Hilltop Ltd. has to

wait for 1 year and 6 months to recover the initial amount which is invested by the organization in

machine 1. On the contrary to it, for machine B business unit will take 3 years to get back the

investment which is primarily invested by the firm. Thus, Hilltop ltd needs to make investment in

project A over the project B.

Net present value (NPV) and Average rate of return (ARR): Net present value method entail

the return which business unit will earn after the predetermined time period (Dellavigna and Pollet,

2013). Whereas, ARR method helps in identifying the average return which business unit will get

during the time frame.

Computation of NPV

Year Project A Project B

Cash

inflow (In

£)

Discounting

factor @20%

Discouted

cash inflow

(In £)

Cash inflow (In

£)

Discouted cash

inflow (In £)

2016 73000 0.833 60809 30000 24990

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 73000 0.694 50662 40000 27760

2018 44000 0.579 25476 50000 28950

2019 40000 0.482 19280 80000 38560

2020 40000 0.402 16080 90000 36180

2021 30000 0.335 10050 75000 25125

Total

discounted

cash inflow 182357 181565

Less: Initial

investment (120000) (120000)

NPV 62357 61565

ARR

(£200000/6

)/

(£120000)*

100 =

27.78%

(£245000/6)/(£1

20000)*100 =

34.03%

The above table shows that Hilltop ltd will get £62357 return if they make investment in

project A. In company to this, project B will offer £61565 return after the 6 years. ARR of project a

is 27.78% whereas average profitability rate of Project B is 34.03%. Hence, by taking into account

the outcomes of NPV business unit needs to invest money in project A. Moreover, NPV method

undertakes time value of money concept and thereby offers highly realistic results. This aspect

clearly reflects that Project A proves to be more beneficial for the firm.

2. Stating the limitations of investment appraisal techniques

There are several aspects which limit the significance of investment appraisal techniques are

enumerated below: Payback period: This method of capital budgeting does not undertake time value of money

concept which is highly important in the present time (Brunzell, Liljeblom and Vaihekoski,

2013). Further, payback period method also fails to offer information about the cash flow

which will be generated by the firm after the predetermined time frame. Net present value: Under this, investment or project manager requires to make estimation of

10

2018 44000 0.579 25476 50000 28950

2019 40000 0.482 19280 80000 38560

2020 40000 0.402 16080 90000 36180

2021 30000 0.335 10050 75000 25125

Total

discounted

cash inflow 182357 181565

Less: Initial

investment (120000) (120000)

NPV 62357 61565

ARR

(£200000/6

)/

(£120000)*

100 =

27.78%

(£245000/6)/(£1

20000)*100 =

34.03%

The above table shows that Hilltop ltd will get £62357 return if they make investment in

project A. In company to this, project B will offer £61565 return after the 6 years. ARR of project a

is 27.78% whereas average profitability rate of Project B is 34.03%. Hence, by taking into account

the outcomes of NPV business unit needs to invest money in project A. Moreover, NPV method

undertakes time value of money concept and thereby offers highly realistic results. This aspect

clearly reflects that Project A proves to be more beneficial for the firm.

2. Stating the limitations of investment appraisal techniques

There are several aspects which limit the significance of investment appraisal techniques are

enumerated below: Payback period: This method of capital budgeting does not undertake time value of money

concept which is highly important in the present time (Brunzell, Liljeblom and Vaihekoski,

2013). Further, payback period method also fails to offer information about the cash flow

which will be generated by the firm after the predetermined time frame. Net present value: Under this, investment or project manager requires to make estimation of

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the cost of capital (Mbabazize and Daniel, 2014). If manager fails to opt suitable discounting

factor then this method does not offer suitable framework for the purpose of decision

making.

Averages rate of return: This tool of investment appraisal also avoids time value of money

concept (Wood and et.al., 2013). Furthermore, ARR method does not offer suitable

framework when its is used to compare the two mutually exclusive projects.

CONCLUSION

From the above report, it can be concluded that profitability and liquidity position of Next

plc is improved as compared to past. Whereas, financial health and performance of H&M had

decreased in comparison to before years which is not good sign for the firm. Thus, business unit

needs to undertake effectual measure which provides assistance to them in improving the financial

aspects. Furthermore, it can be inferred that Hilltop ltd needs to select project A which will help

them in attaining success in the strategic business arena.

11

factor then this method does not offer suitable framework for the purpose of decision

making.

Averages rate of return: This tool of investment appraisal also avoids time value of money

concept (Wood and et.al., 2013). Furthermore, ARR method does not offer suitable

framework when its is used to compare the two mutually exclusive projects.

CONCLUSION

From the above report, it can be concluded that profitability and liquidity position of Next

plc is improved as compared to past. Whereas, financial health and performance of H&M had

decreased in comparison to before years which is not good sign for the firm. Thus, business unit

needs to undertake effectual measure which provides assistance to them in improving the financial

aspects. Furthermore, it can be inferred that Hilltop ltd needs to select project A which will help

them in attaining success in the strategic business arena.

11

REFERENCES

Books and Journals

Brunzell, T., Liljeblom, E. and Vaihekoski, M., 2013. Determinants of capital budgeting methods

and hurdle rates in Nordic firms. Accounting & Finance. 53(1). pp.85-110.

Chen, E. and Gavious, I., 2016. Unrealized earnings, dividends and reporting aggressiveness: an

examination of firms’ behavior in the era of fair value accounting. Accounting & Finance.

56(1). pp.217-250.

Dellavigna, S. and Pollet, J.M., 2013. Capital budgeting versus market timing: An evaluation using

demographics. The Journal of Finance. 68(1). pp.237-270.

Gitman, L.J., 2013. Principles of Managerial Finance: Global Edition. Pearson Higher Ed.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37. pp.317-

324.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1). pp.30-53.

Liao, G.J. and et.al., 2012. Noninvasive prenatal diagnosis of fetal trisomy 21 by allelic ratio

analysis using targeted massively parallel sequencing of maternal plasma DNA. PLoS One.

7(5). pp.e38154.

Mbabazize, P.M. and Daniel, T., 2014. Capital Budgeting Practices In Developing Countries: A

Case Of Rwanda. Research journali’s Journal of Finance. 2(3). pp.34, 38.

Wood, D.P. and et.al., 2013. Applications and limitations of wrap-around ratio to vehicle speed

estimation in pedestrian collision analysis. International Journal of Crashworthiness. 18(3).

pp.288-305.

Online

Limitations of ratio analysis, 2013. [Online]. Available through:

<http://accountingexplained.com/financial/ratios/advantages-limitations>. [Accessed on 25th

April 2016].

12

Books and Journals

Brunzell, T., Liljeblom, E. and Vaihekoski, M., 2013. Determinants of capital budgeting methods

and hurdle rates in Nordic firms. Accounting & Finance. 53(1). pp.85-110.

Chen, E. and Gavious, I., 2016. Unrealized earnings, dividends and reporting aggressiveness: an

examination of firms’ behavior in the era of fair value accounting. Accounting & Finance.

56(1). pp.217-250.

Dellavigna, S. and Pollet, J.M., 2013. Capital budgeting versus market timing: An evaluation using

demographics. The Journal of Finance. 68(1). pp.237-270.

Gitman, L.J., 2013. Principles of Managerial Finance: Global Edition. Pearson Higher Ed.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37. pp.317-

324.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1). pp.30-53.

Liao, G.J. and et.al., 2012. Noninvasive prenatal diagnosis of fetal trisomy 21 by allelic ratio

analysis using targeted massively parallel sequencing of maternal plasma DNA. PLoS One.

7(5). pp.e38154.

Mbabazize, P.M. and Daniel, T., 2014. Capital Budgeting Practices In Developing Countries: A

Case Of Rwanda. Research journali’s Journal of Finance. 2(3). pp.34, 38.

Wood, D.P. and et.al., 2013. Applications and limitations of wrap-around ratio to vehicle speed

estimation in pedestrian collision analysis. International Journal of Crashworthiness. 18(3).

pp.288-305.

Online

Limitations of ratio analysis, 2013. [Online]. Available through:

<http://accountingexplained.com/financial/ratios/advantages-limitations>. [Accessed on 25th

April 2016].

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.