Management Accounting Report: Ever Joy Enterprises Financial Analysis

VerifiedAdded on 2020/12/10

|17

|4757

|225

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within Ever Joy Enterprises. It begins by defining management accounting and contrasting it with financial accounting, emphasizing its role in internal decision-making. The report then delves into various management accounting systems, including cost accounting, inventory management, and job costing, detailing their functionalities and importance. Different management accounting reporting methods, such as budget reports, cost managerial reports, and job cost reports, are explained, highlighting their significance in providing timely and relevant financial information to management. The report further explores the calculation of income statements using absorption and marginal costing techniques, offering insights into their respective methodologies and implications. Additionally, the report discusses the advantages and disadvantages of planning tools for budgetary control and examines how organizations adapt management accounting systems to address financial challenges. The report concludes by emphasizing the importance of a sound accounting system for effective business operations and financial decision-making within the company.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Explaining management accounting and different type of management accounting system.....3

a. Presenting difference between Management Accounting and Financial Accounting.............3

b. Cost accounting system:..........................................................................................................4

c. Inventory Management System:..............................................................................................5

d. Job costing system:.................................................................................................................5

e. Explaining different methods used for management accounting reporting............................6

f...................................................................................................................................................7

TASK 2............................................................................................................................................7

Calculating the income statement using absorption and marginal costing techniques of

accounting method......................................................................................................................7

TASK 3............................................................................................................................................8

a. Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control........................................................................................................................8

b. Comparing how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Explaining management accounting and different type of management accounting system.....3

a. Presenting difference between Management Accounting and Financial Accounting.............3

b. Cost accounting system:..........................................................................................................4

c. Inventory Management System:..............................................................................................5

d. Job costing system:.................................................................................................................5

e. Explaining different methods used for management accounting reporting............................6

f...................................................................................................................................................7

TASK 2............................................................................................................................................7

Calculating the income statement using absorption and marginal costing techniques of

accounting method......................................................................................................................7

TASK 3............................................................................................................................................8

a. Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control........................................................................................................................8

b. Comparing how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is important concept for an organisation. It help the

management of the organisation to make important decisions with the relevant information

provided by the different departments. In a competitive corporate world, having effective

management accounting system is crucial to be remain competitive in the market. The

management accounting system and reporting helps in efficient running of financial and other

business activities in organisation.

The present report is based on Ever Joy Enterprises, which will help it to understand the

importance of having an effective management accounting system in organisation. The present

report will discuss the importance of management accounting system and different types of

accounting system. Further, the report will demonstrate different type managerial accounting

reporting and its importance in company. The report than include a calculation of net income

with different accounting techniques. Furthermore, the report will ,depict about the advantage

and disadvantage of planning tools for budgetary control. At last, the report will discuss how

management accounting system can help the company to resolve its financial problem.

TASK 1

Explaining management accounting and different type of management accounting system

a. Presenting difference between Management Accounting and Financial Accounting.

It is the process of preparing and providing the information regarding financial and

statistical to the higher authority of management so that they make the strategies and decisions

regarding the long term as well as the short term managerial decisions (Kaplan and Atkinson,

2015). It helps the management of the company to perform their basic functions like planning,

organising, managing and controlling of the overall business activities so as to achieve their

overall business objectives.

The difference between management accounting and financial accounting are:

Management accounting Financial accounting

It is an accounting system that are prepared to

provide the information to the manager to

It is the accounting system that are focuses on

preparing the financial statement of the

Management accounting is important concept for an organisation. It help the

management of the organisation to make important decisions with the relevant information

provided by the different departments. In a competitive corporate world, having effective

management accounting system is crucial to be remain competitive in the market. The

management accounting system and reporting helps in efficient running of financial and other

business activities in organisation.

The present report is based on Ever Joy Enterprises, which will help it to understand the

importance of having an effective management accounting system in organisation. The present

report will discuss the importance of management accounting system and different types of

accounting system. Further, the report will demonstrate different type managerial accounting

reporting and its importance in company. The report than include a calculation of net income

with different accounting techniques. Furthermore, the report will ,depict about the advantage

and disadvantage of planning tools for budgetary control. At last, the report will discuss how

management accounting system can help the company to resolve its financial problem.

TASK 1

Explaining management accounting and different type of management accounting system

a. Presenting difference between Management Accounting and Financial Accounting.

It is the process of preparing and providing the information regarding financial and

statistical to the higher authority of management so that they make the strategies and decisions

regarding the long term as well as the short term managerial decisions (Kaplan and Atkinson,

2015). It helps the management of the company to perform their basic functions like planning,

organising, managing and controlling of the overall business activities so as to achieve their

overall business objectives.

The difference between management accounting and financial accounting are:

Management accounting Financial accounting

It is an accounting system that are prepared to

provide the information to the manager to

It is the accounting system that are focuses on

preparing the financial statement of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

make policies, plans and strategies for the

efficient business operations.

organisation for the internal as well as the

external users to provide information of the

company's financial performance.

Management accounting provides monetary as

well as the non-monetary information of the

company also.

Financial accounting provides monetary

information of the company only.

Management accounting's main objectives is to

assist the management in providing the

information which helps in decision making

process of company.

Financial accounting main objective is to

provide information about the company's

financial performance to the outside users like

shareholder, investors, auditor, government etc

(Hilton and Platt, 2013).

Management accounting can be prepared at

any time when required and as per the need of

management.

Financial accounting re prepared at the end of

each accounting year.

Management accounting system is essential for the Ever Joy enterprises, so that the

management can make the effective decisions and policies to increase the company' future

performance. The management can take the company's financial information to develop the

report for making decisions. The management accounting system helps the company to make

more effective decisions from the information and reports. Management accounting system

focuses on the costs that are associated with the production of goods and services in an

organisation. There are different types of management accounting system that can be used by

Ever Joy enterprises. They are:

b. Cost accounting system:

It the method of evaluating a company's cost in producing a single product by evaluating

its overhead costs and fixed cost (Ward, 2012). The company analyse the cost to know the

profitability analysis, inventory valuation and controlling of the cost incurred. Its important for a

company to know the profitability of the product, which can be ascertained when the actual price

of the product will be estimated. Cost accounting system are of two main types they are:

efficient business operations.

organisation for the internal as well as the

external users to provide information of the

company's financial performance.

Management accounting provides monetary as

well as the non-monetary information of the

company also.

Financial accounting provides monetary

information of the company only.

Management accounting's main objectives is to

assist the management in providing the

information which helps in decision making

process of company.

Financial accounting main objective is to

provide information about the company's

financial performance to the outside users like

shareholder, investors, auditor, government etc

(Hilton and Platt, 2013).

Management accounting can be prepared at

any time when required and as per the need of

management.

Financial accounting re prepared at the end of

each accounting year.

Management accounting system is essential for the Ever Joy enterprises, so that the

management can make the effective decisions and policies to increase the company' future

performance. The management can take the company's financial information to develop the

report for making decisions. The management accounting system helps the company to make

more effective decisions from the information and reports. Management accounting system

focuses on the costs that are associated with the production of goods and services in an

organisation. There are different types of management accounting system that can be used by

Ever Joy enterprises. They are:

b. Cost accounting system:

It the method of evaluating a company's cost in producing a single product by evaluating

its overhead costs and fixed cost (Ward, 2012). The company analyse the cost to know the

profitability analysis, inventory valuation and controlling of the cost incurred. Its important for a

company to know the profitability of the product, which can be ascertained when the actual price

of the product will be estimated. Cost accounting system are of two main types they are:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard costing: it is the techniques of the accounting which are used to identify the

differences between the actual cost of the good produced and the cost that should be

incurred in the production.

Direct cost: it is the price that are assigned to the production of the certain goods or

services. there are certain cost that are difficult to assign in the production that are

depreciation or the administrative expenses which are included in the indirect expenses.

Direct cost is useful for the management at the time of decision making regarding the

cost controlling.

Actual costing: it is the cost that are incurred in the production process of a product.

Actual cost includes direct labour, direct material, and other direct charges.

Normal cost: it is the estimated or predetermined cost of producing a good.

c. Inventory Management System:

This system helps in tracking goods in its entire process production the process of the

supply chain in company (Otley and Emmanuel, 2013). It cover the flow of goods from the

production to retail, warehousing to shipping and all other movements of the goods involved

between the final delivery of the product to the customer. This management helps in evaluating

the total cost of inventories so as to generate high profit return to the company. There are various

cost that are holds with the inventories, the inventory management system helps in evaluating the

need of the inventories so as to explicit the cost of the product. There are three methods of

inventory valuation:

FIFO: in this method it is assumed that the goods that are manufactured first will be sold first and

newer inventory will remain unsold.

LIFO: in this method the old product or inventory manufactured will be out for sale first. it will

be used when company assumes that the price of inventory will rise in future.

Average cost method: it helps in calculating the cost of ending inventory and the coast of good

sold will be calculated on the weighted average cost per unit of inventory.

d. Job costing system:

in this system the cost is assigned to every product which helps in evaluating the manager

the actual expenses in manufacturing of that product. It the assigning of the manufacturing costs

differences between the actual cost of the good produced and the cost that should be

incurred in the production.

Direct cost: it is the price that are assigned to the production of the certain goods or

services. there are certain cost that are difficult to assign in the production that are

depreciation or the administrative expenses which are included in the indirect expenses.

Direct cost is useful for the management at the time of decision making regarding the

cost controlling.

Actual costing: it is the cost that are incurred in the production process of a product.

Actual cost includes direct labour, direct material, and other direct charges.

Normal cost: it is the estimated or predetermined cost of producing a good.

c. Inventory Management System:

This system helps in tracking goods in its entire process production the process of the

supply chain in company (Otley and Emmanuel, 2013). It cover the flow of goods from the

production to retail, warehousing to shipping and all other movements of the goods involved

between the final delivery of the product to the customer. This management helps in evaluating

the total cost of inventories so as to generate high profit return to the company. There are various

cost that are holds with the inventories, the inventory management system helps in evaluating the

need of the inventories so as to explicit the cost of the product. There are three methods of

inventory valuation:

FIFO: in this method it is assumed that the goods that are manufactured first will be sold first and

newer inventory will remain unsold.

LIFO: in this method the old product or inventory manufactured will be out for sale first. it will

be used when company assumes that the price of inventory will rise in future.

Average cost method: it helps in calculating the cost of ending inventory and the coast of good

sold will be calculated on the weighted average cost per unit of inventory.

d. Job costing system:

in this system the cost is assigned to every product which helps in evaluating the manager

the actual expenses in manufacturing of that product. It the assigning of the manufacturing costs

to an individual product systematically in overhead expenses, direct labour, material so as to

estimating the actual value of the product (Wild, 2017). This system is very essential to control

the use of raw materials, labour hours by assigning each cost for different customer.

Batch costing is specific form of order costing. A finished products requires different

components for assemble and may be manufactures in economical batch lot. In Batch costing

items are manufactured for cost.

e. Explaining different methods used for management accounting reporting.

Management accounting report are the tools which helps in understanding the financial

performance of the company to the higher authority of management. The management reports

includes all the statistical and financial data that are to be required to the management of Ever

Joy enterprises to formulate the decisions and strategies for the future performance of the

company (Hilton and Platt, 2013). Managerial reports are continuously generated throughout the

accounting period. It is important for the managers to provide relevant data and information on

correct time so that the management can take the efficient decisions regarding the operations of

the organisation. There are different types of management accounting reports which are

essentials to the Ever Joy enterprise's management :

Budget report:

It is the most fundamental report off managerial reporting. It is very essential report that

help in measuring company's actual performance with the budgeted performance (Fullerton,

Kennedy and Widener, 2013). It helps in analysing the performance of different department and

in controlling cost of the expenses. The budged is usually based on the expenses incurred from

the prior years budget. All sources of earning and expenses are being estimated and on the basis

of that the cost are being allocated to each department of the organisation. It is the main objective

off the company to run its operations by limiting in the budgeted amount.

Cost managerial accounting reports:

This reports help in calculating' the actual expenses incurred in manufacturing of the

product this report includes the expenses of raw material, direct labour (DRUR, 2013). Overhead

cost and other expenses. The cost managerial reports involves all the information which help the

management in estimating the total cost of production. It assist the management in evaluating

estimating the actual value of the product (Wild, 2017). This system is very essential to control

the use of raw materials, labour hours by assigning each cost for different customer.

Batch costing is specific form of order costing. A finished products requires different

components for assemble and may be manufactures in economical batch lot. In Batch costing

items are manufactured for cost.

e. Explaining different methods used for management accounting reporting.

Management accounting report are the tools which helps in understanding the financial

performance of the company to the higher authority of management. The management reports

includes all the statistical and financial data that are to be required to the management of Ever

Joy enterprises to formulate the decisions and strategies for the future performance of the

company (Hilton and Platt, 2013). Managerial reports are continuously generated throughout the

accounting period. It is important for the managers to provide relevant data and information on

correct time so that the management can take the efficient decisions regarding the operations of

the organisation. There are different types of management accounting reports which are

essentials to the Ever Joy enterprise's management :

Budget report:

It is the most fundamental report off managerial reporting. It is very essential report that

help in measuring company's actual performance with the budgeted performance (Fullerton,

Kennedy and Widener, 2013). It helps in analysing the performance of different department and

in controlling cost of the expenses. The budged is usually based on the expenses incurred from

the prior years budget. All sources of earning and expenses are being estimated and on the basis

of that the cost are being allocated to each department of the organisation. It is the main objective

off the company to run its operations by limiting in the budgeted amount.

Cost managerial accounting reports:

This reports help in calculating' the actual expenses incurred in manufacturing of the

product this report includes the expenses of raw material, direct labour (DRUR, 2013). Overhead

cost and other expenses. The cost managerial reports involves all the information which help the

management in estimating the total cost of production. It assist the management in evaluating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production cost of a product and the selling cost of the product. Profit margin are than estimated

in these report which helps the management in making decisions regarding the manufacturing

activities and controlling costs.

Account receivable ageing report:

This report are essential when business are relies on providing credit facilities to its

customer or distributors (Callahan, Stetz and Brooks, 2011). These reports are very vital for the

company as it helps in ascertaining the balances of the clients and distributors. These report also

helps the accountant to know the defaulter and finding issues regarding the collection process of

the company. The report helps in making policies for tightening credit facility that can help the

management in sufficient cash flow in company.

Job cost reports:

These report shows the expenses regarding the manufacturing of a product or a assigned

job. These report usually made to check the estimated revenue to evaluate the profitability of the

job. It helps the management to know the higher earning area of the organisation, so that the

management can focus and provide extra efforts to profitable area (Hoitash and Hoitash, 2017).

It assist the management in proper allocation of cost, from the area which are not are not so

profitable for the organisation.

f. The need for the sound accounting system and the importance for the department producing

timely.

Maintaining the sound accounting accounting system is important for the success of Ever

Joy Enterprises. it is an important system to control and ensure the proper management and

business operation of the company. The need of sound management system can be understand

from the importance if effective naad efficient operations, reliable reporting and compliance with

applicable laws and regulation. The importance of department in producing reports timely are:

Management can take the decisions regarding the future growth and policies timely.

Providing accurate information will help in making budgets for all the departments as per

their performance, so that the department can do their operations effectively.

In order to prevent any fraud in the company. The accounting report will help to evaluate

and prevent any fraud in the organisation.

in these report which helps the management in making decisions regarding the manufacturing

activities and controlling costs.

Account receivable ageing report:

This report are essential when business are relies on providing credit facilities to its

customer or distributors (Callahan, Stetz and Brooks, 2011). These reports are very vital for the

company as it helps in ascertaining the balances of the clients and distributors. These report also

helps the accountant to know the defaulter and finding issues regarding the collection process of

the company. The report helps in making policies for tightening credit facility that can help the

management in sufficient cash flow in company.

Job cost reports:

These report shows the expenses regarding the manufacturing of a product or a assigned

job. These report usually made to check the estimated revenue to evaluate the profitability of the

job. It helps the management to know the higher earning area of the organisation, so that the

management can focus and provide extra efforts to profitable area (Hoitash and Hoitash, 2017).

It assist the management in proper allocation of cost, from the area which are not are not so

profitable for the organisation.

f. The need for the sound accounting system and the importance for the department producing

timely.

Maintaining the sound accounting accounting system is important for the success of Ever

Joy Enterprises. it is an important system to control and ensure the proper management and

business operation of the company. The need of sound management system can be understand

from the importance if effective naad efficient operations, reliable reporting and compliance with

applicable laws and regulation. The importance of department in producing reports timely are:

Management can take the decisions regarding the future growth and policies timely.

Providing accurate information will help in making budgets for all the departments as per

their performance, so that the department can do their operations effectively.

In order to prevent any fraud in the company. The accounting report will help to evaluate

and prevent any fraud in the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Calculating the income statement using absorption and marginal costing techniques of

accounting method.

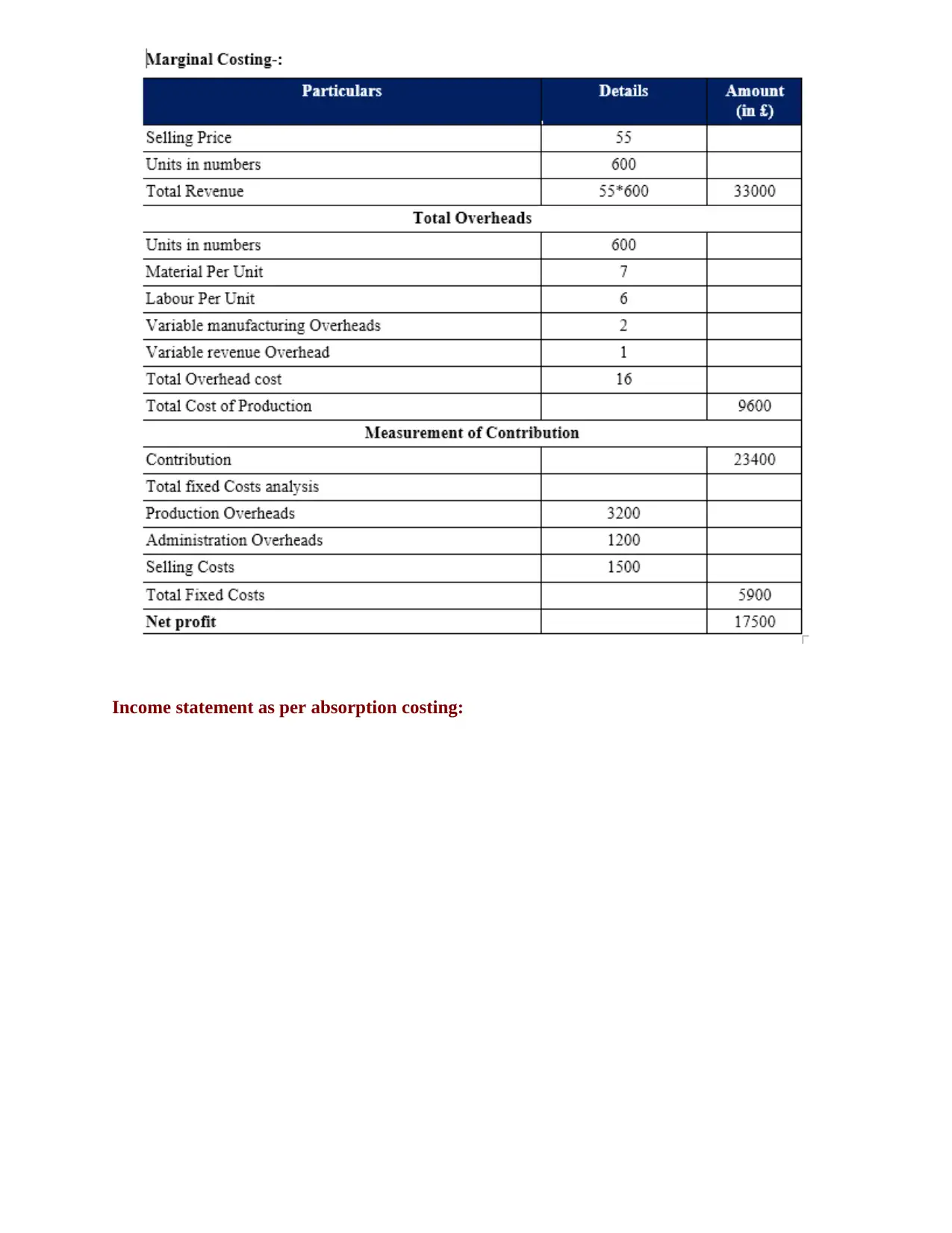

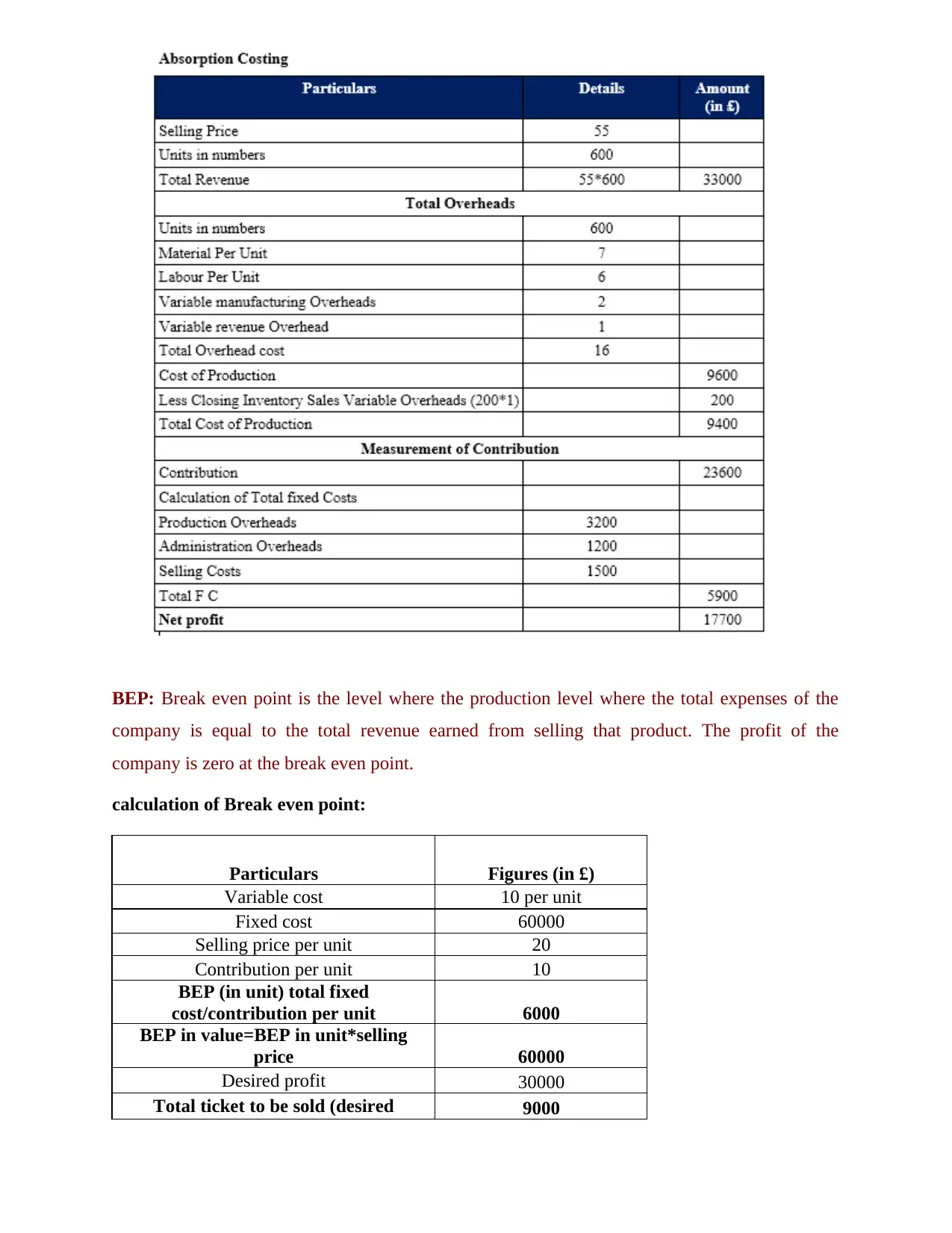

Absorption Costing:

It is a techniques of accounting method of evaluating the cost of inventory. Absorption

costing is full costing method as it considered both fixed and variable cost in calculating the

manufacturing cost of the product (Liu, Zhang and Wu, 2011). It takes into account all the

manufacturing costs in the unit produces. This cost will include the direct material, direct labour,

and both variable and fixed manufacturing expenses. It is considered as most suitable as the other

method as it considered all the possible manufacturing costs.

Marginal costing:

It is the techniques of costing method where only variable cost are taken into

consideration while calculating the manufacturing cost of the inventory. Under the marginal

costing, the fixed cost are considered to be constant for the accounting year (Ilak and et.al.,

2018). It is based on the behaviour of cost that changes with the level of output. It is not

considered as an appropriate method as it does not take fixed cost into calculating net profit.

Income statement as per marginal cost:

Calculating the income statement using absorption and marginal costing techniques of

accounting method.

Absorption Costing:

It is a techniques of accounting method of evaluating the cost of inventory. Absorption

costing is full costing method as it considered both fixed and variable cost in calculating the

manufacturing cost of the product (Liu, Zhang and Wu, 2011). It takes into account all the

manufacturing costs in the unit produces. This cost will include the direct material, direct labour,

and both variable and fixed manufacturing expenses. It is considered as most suitable as the other

method as it considered all the possible manufacturing costs.

Marginal costing:

It is the techniques of costing method where only variable cost are taken into

consideration while calculating the manufacturing cost of the inventory. Under the marginal

costing, the fixed cost are considered to be constant for the accounting year (Ilak and et.al.,

2018). It is based on the behaviour of cost that changes with the level of output. It is not

considered as an appropriate method as it does not take fixed cost into calculating net profit.

Income statement as per marginal cost:

Income statement as per absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEP: Break even point is the level where the production level where the total expenses of the

company is equal to the total revenue earned from selling that product. The profit of the

company is zero at the break even point.

calculation of Break even point:

Particulars Figures (in £)

Variable cost 10 per unit

Fixed cost 60000

Selling price per unit 20

Contribution per unit 10

BEP (in unit) total fixed

cost/contribution per unit 6000

BEP in value=BEP in unit*selling

price 60000

Desired profit 30000

Total ticket to be sold (desired 9000

company is equal to the total revenue earned from selling that product. The profit of the

company is zero at the break even point.

calculation of Break even point:

Particulars Figures (in £)

Variable cost 10 per unit

Fixed cost 60000

Selling price per unit 20

Contribution per unit 10

BEP (in unit) total fixed

cost/contribution per unit 6000

BEP in value=BEP in unit*selling

price 60000

Desired profit 30000

Total ticket to be sold (desired 9000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit/contribution+bep)

Profit if 8000 ticket are sold 20000

Interpretation

As per analysing the calculation above, it can be said that the break even point of ticket

in units is 6000. however, the break even profit is 60000 pounds. In order to get desired profit of

30000, the ticket that need to be sold is 9000. if the company wanted to sell 8000 tickets, the

total profit earned will be estimated is 2000.

TASK 3

a. Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgeting is a process of estimating revenue and expenditure over a specified future

period of time. At company it is an important tool used by the management of company to

evaluate their income and expenses for the future period, such budgets are prepared by

evaluating the prior budgets (Dunk, 2011). Budgeting is the process of preparing a budget. It is

process of planning future activities of the business and establishing the goals that should be

achieved in the coming year. Budgeting helps in making financial goal for the company and

helps in achieving those goals by creating a proper plan.

Budgetary control is the process through which the actual performance of the company is

being compared to the budgeted plan in order to find any variances if any. This variances will

help the management in to take corrective measures to improve the performance. Budgetary

control act as a tool for controlling the finance of the company. Ever Joy Enterprises should

established budgetary control as a tool to control its financial problems.

Budgetary control ids a continuous process that helps in planning and coordination. There

are various planning tools that helps in controlling the budgets of the company (Silva and

Jayamaha, 2012). Planning tools are the techniques which compares the actual results with the

planned one, and helps in controlling the variances to achieve maximum profitability for the

firm. The planning tools for budgetary controlling are:

Cash budgets:

Profit if 8000 ticket are sold 20000

Interpretation

As per analysing the calculation above, it can be said that the break even point of ticket

in units is 6000. however, the break even profit is 60000 pounds. In order to get desired profit of

30000, the ticket that need to be sold is 9000. if the company wanted to sell 8000 tickets, the

total profit earned will be estimated is 2000.

TASK 3

a. Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgeting is a process of estimating revenue and expenditure over a specified future

period of time. At company it is an important tool used by the management of company to

evaluate their income and expenses for the future period, such budgets are prepared by

evaluating the prior budgets (Dunk, 2011). Budgeting is the process of preparing a budget. It is

process of planning future activities of the business and establishing the goals that should be

achieved in the coming year. Budgeting helps in making financial goal for the company and

helps in achieving those goals by creating a proper plan.

Budgetary control is the process through which the actual performance of the company is

being compared to the budgeted plan in order to find any variances if any. This variances will

help the management in to take corrective measures to improve the performance. Budgetary

control act as a tool for controlling the finance of the company. Ever Joy Enterprises should

established budgetary control as a tool to control its financial problems.

Budgetary control ids a continuous process that helps in planning and coordination. There

are various planning tools that helps in controlling the budgets of the company (Silva and

Jayamaha, 2012). Planning tools are the techniques which compares the actual results with the

planned one, and helps in controlling the variances to achieve maximum profitability for the

firm. The planning tools for budgetary controlling are:

Cash budgets:

It is process through which company forecast its cash receipts and payment through

which the actual cash is measured in a specific time period. It is a process of evaluating the

company's cash position. It includes the inflow and outflow of cash that involves the revenue

collected, expenses paid, and other loans receipts and payments (Hofstede, 2012). Management

uses the cash budget too manage the cash flows of the company and to be sure that there is

enough cash flow in the company to fulfilled any requirement.

Advantage of cash budgets:

It helps in avoiding the debt situation for company. It ensure that company have the

sufficient case to pay its bill.

It helps in better coordination of the employees and all the activities in organisation

(Otley and Emmanuel, 2013). Cash budget helps in showing the availability of excess cash, which makes it possible to

plan any profitable investment plan (What is Budgetary control? ,2018).

Disadvantages of Cash Budget:

The success of cash budgets relies on the activities performed by employees.

It is prepared in the future estimation of receipts and payments, any uncertainty can be

happen that leads to failure of the budget.

There is no or little flexibility in the cash budget, once the budget is prepared it is very

difficult to make any changes as the budget will be presented to the management of

company.

Zero based budgeting:

It is method of budgeting in which a new budget is prepared without considering the prior

years budget. Thus, the new budget will be based on zero basis, it will consider the performance

of the activity in organisation. On the basis of performance the budget will be prepared and

allocation of cost will be done accordingly (O'connor, 2017). In zero based budgeting method,

company has to review each activity in order to control the spendings of activity that are not

accordingly to estimated budgets. In such case, prior performance of that activity is of no use. Th

budget has to prepared.

which the actual cash is measured in a specific time period. It is a process of evaluating the

company's cash position. It includes the inflow and outflow of cash that involves the revenue

collected, expenses paid, and other loans receipts and payments (Hofstede, 2012). Management

uses the cash budget too manage the cash flows of the company and to be sure that there is

enough cash flow in the company to fulfilled any requirement.

Advantage of cash budgets:

It helps in avoiding the debt situation for company. It ensure that company have the

sufficient case to pay its bill.

It helps in better coordination of the employees and all the activities in organisation

(Otley and Emmanuel, 2013). Cash budget helps in showing the availability of excess cash, which makes it possible to

plan any profitable investment plan (What is Budgetary control? ,2018).

Disadvantages of Cash Budget:

The success of cash budgets relies on the activities performed by employees.

It is prepared in the future estimation of receipts and payments, any uncertainty can be

happen that leads to failure of the budget.

There is no or little flexibility in the cash budget, once the budget is prepared it is very

difficult to make any changes as the budget will be presented to the management of

company.

Zero based budgeting:

It is method of budgeting in which a new budget is prepared without considering the prior

years budget. Thus, the new budget will be based on zero basis, it will consider the performance

of the activity in organisation. On the basis of performance the budget will be prepared and

allocation of cost will be done accordingly (O'connor, 2017). In zero based budgeting method,

company has to review each activity in order to control the spendings of activity that are not

accordingly to estimated budgets. In such case, prior performance of that activity is of no use. Th

budget has to prepared.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.