Financial Management Report: Sweet Menu and Blue Island Analysis

VerifiedAdded on 2020/01/28

|14

|4960

|44

Report

AI Summary

This report delves into the financial management of Sweet Menu and Blue Island restaurants. It begins by identifying and evaluating various sources of finance, including long-term options like retained earnings, loans, share capital, and venture capital, as well as short-term sources such as trade credit and hire purchase. The implications of each source are analyzed, considering legal, financial, and ownership aspects. The report then evaluates the most appropriate financial resources for Sweet Menu, recommending a combination of share issuance, bank loans, and trade credit. It assesses the costs associated with each financing method and highlights the importance of financial planning. The report also examines the significance of financial statements for Blue Island, analyzing costs, financial planning, stakeholder information, and the impact of financial sources. It explores budgeting, unit costs, pricing decisions, and investment appraisal techniques. Finally, it provides a comprehensive overview of financial statements and conducts a ratio analysis to evaluate the financial performance of both restaurants.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Available sources of finances.....................................................................................................3

1.2 Implication of the sources..........................................................................................................4

1.3 Evaluation of most appropriate sources.....................................................................................4

TASK 2.................................................................................................................................................5

2.1 Analysing cost............................................................................................................................5

2.2 Importance of financial planning...............................................................................................5

2.3 Assessing information of stakeholders......................................................................................6

2.4 Impact of the sources of finance................................................................................................6

TASK 3.................................................................................................................................................7

3.1 Analysing budget and proposing recommendations..................................................................7

3.2 Unit cost and pricing decision...................................................................................................7

3.3 Assessment through investment appraisal technique.................................................................8

TASK 4...............................................................................................................................................10

4.1 Financial statements.................................................................................................................10

4.2 Comparison between financial formats...................................................................................10

4.3 Ratio Analysis..........................................................................................................................10

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Available sources of finances.....................................................................................................3

1.2 Implication of the sources..........................................................................................................4

1.3 Evaluation of most appropriate sources.....................................................................................4

TASK 2.................................................................................................................................................5

2.1 Analysing cost............................................................................................................................5

2.2 Importance of financial planning...............................................................................................5

2.3 Assessing information of stakeholders......................................................................................6

2.4 Impact of the sources of finance................................................................................................6

TASK 3.................................................................................................................................................7

3.1 Analysing budget and proposing recommendations..................................................................7

3.2 Unit cost and pricing decision...................................................................................................7

3.3 Assessment through investment appraisal technique.................................................................8

TASK 4...............................................................................................................................................10

4.1 Financial statements.................................................................................................................10

4.2 Comparison between financial formats...................................................................................10

4.3 Ratio Analysis..........................................................................................................................10

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

INTRODUCTION

Management of financial resources refers to effectively allocating monetary fund in a

business. The financial manager is responsible to manage the resource in a way so that it can be

utilised to their maximum capacity. Managing finance is a crucial aspect for the financial manager.

Due to the fact that finance is the main element help to operate business activity. For managing the

finance, the manager makes different strategies so as to effectively achieve his/her objectives.

Another aspect of financial management is decision making ability of a financial manager. The

organisation must make accurate decision regarding management of financial resources of the

company.

The report discusses the financial management of Sweet Menu restaurant and Blue Island

restaurant. The main objective of the research is to identify appropriate financial resources for

Sweet Menu restaurant. It is vital for the restaurant owner to select a financial source to raise the

capital. As the organization wants to raise €300,000 and €500,000 for its branches in Central

London and Croydon various options are evaluated in order to choose correct source to raise

finance. On the other hand, the research also highlights the importance of financial statement for the

Blue Island restaurant. The owner of the restaurant wants to evaluate the effectiveness of a financial

statement. This report conducts a study to properly analyte various statements and their significance

to an organization.

TASK 1

1.1 Available sources of finances

Available sources of funds refer to the current accessible funds for a business. Source of

finance are bifurcated into two types i.e. long term finances and short term sources of finance. Long

term sources provide financial assistance that can be used for more than one year whereas short

term is supposed to be used within a year. Sweet menu restaurant wants to expand its business on

two locations, thus the first step must be to identify appropriate source of finance. They are as

followed.

Long term source are-

Retained Earnings- The business can use the earning that has been retained by it. Each

year the business can store a portion of its earnings from the profit or may distribute it to the

shareholders or the debenture holders. These earnings can be saved by reducing the dividend

given to the shareholders.

Long term loan- A loan is an amount which is taken on credit basis from the financial

institution or a bank. The business which is applying for a loan has to agree to deposit a

security in order to acquire loan as well as the company is entitled to pay for an interest

Management of financial resources refers to effectively allocating monetary fund in a

business. The financial manager is responsible to manage the resource in a way so that it can be

utilised to their maximum capacity. Managing finance is a crucial aspect for the financial manager.

Due to the fact that finance is the main element help to operate business activity. For managing the

finance, the manager makes different strategies so as to effectively achieve his/her objectives.

Another aspect of financial management is decision making ability of a financial manager. The

organisation must make accurate decision regarding management of financial resources of the

company.

The report discusses the financial management of Sweet Menu restaurant and Blue Island

restaurant. The main objective of the research is to identify appropriate financial resources for

Sweet Menu restaurant. It is vital for the restaurant owner to select a financial source to raise the

capital. As the organization wants to raise €300,000 and €500,000 for its branches in Central

London and Croydon various options are evaluated in order to choose correct source to raise

finance. On the other hand, the research also highlights the importance of financial statement for the

Blue Island restaurant. The owner of the restaurant wants to evaluate the effectiveness of a financial

statement. This report conducts a study to properly analyte various statements and their significance

to an organization.

TASK 1

1.1 Available sources of finances

Available sources of funds refer to the current accessible funds for a business. Source of

finance are bifurcated into two types i.e. long term finances and short term sources of finance. Long

term sources provide financial assistance that can be used for more than one year whereas short

term is supposed to be used within a year. Sweet menu restaurant wants to expand its business on

two locations, thus the first step must be to identify appropriate source of finance. They are as

followed.

Long term source are-

Retained Earnings- The business can use the earning that has been retained by it. Each

year the business can store a portion of its earnings from the profit or may distribute it to the

shareholders or the debenture holders. These earnings can be saved by reducing the dividend

given to the shareholders.

Long term loan- A loan is an amount which is taken on credit basis from the financial

institution or a bank. The business which is applying for a loan has to agree to deposit a

security in order to acquire loan as well as the company is entitled to pay for an interest

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount in each instalment.

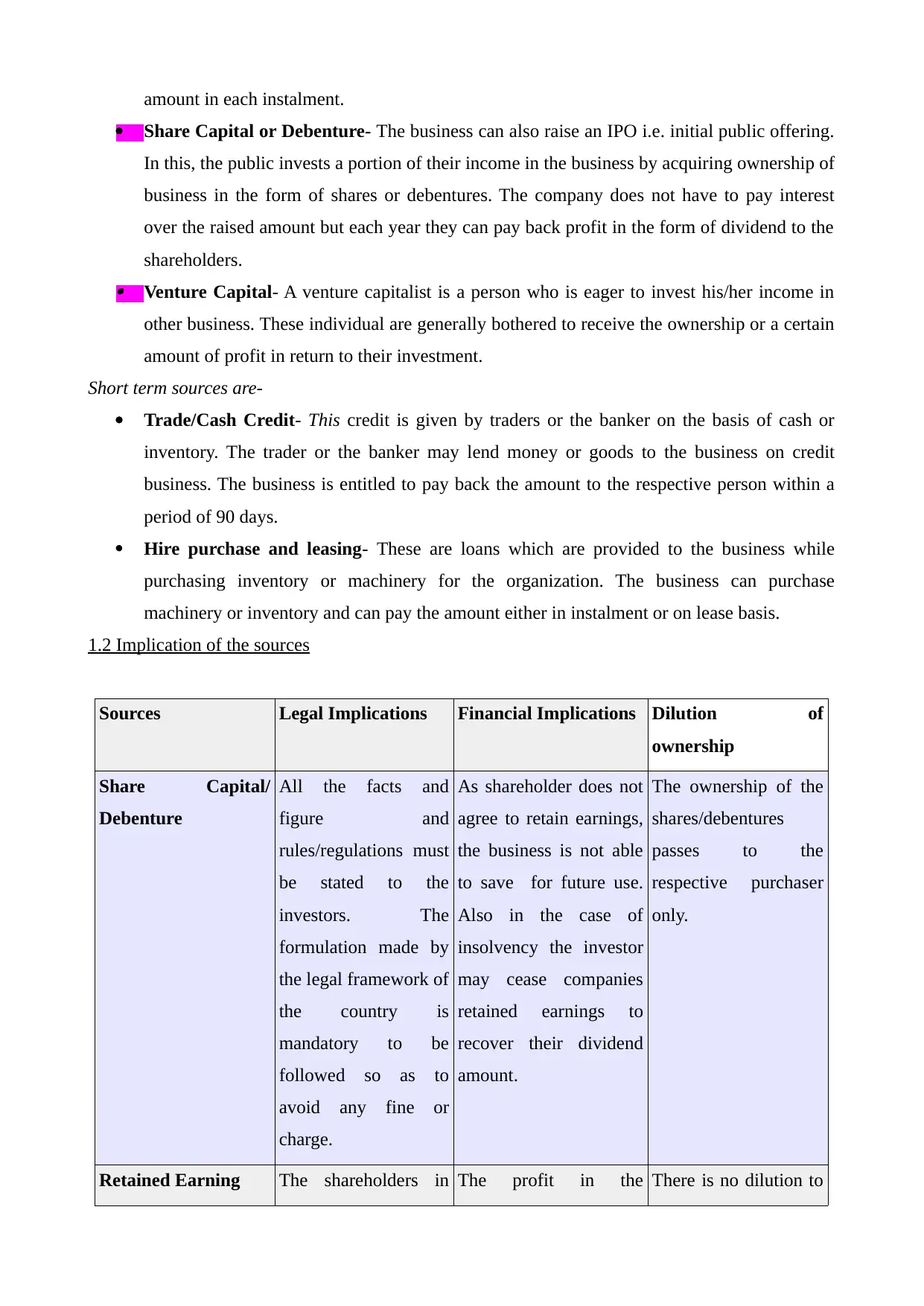

Share Capital or Debenture- The business can also raise an IPO i.e. initial public offering.

In this, the public invests a portion of their income in the business by acquiring ownership of

business in the form of shares or debentures. The company does not have to pay interest

over the raised amount but each year they can pay back profit in the form of dividend to the

shareholders. Venture Capital- A venture capitalist is a person who is eager to invest his/her income in

other business. These individual are generally bothered to receive the ownership or a certain

amount of profit in return to their investment.

Short term sources are-

Trade/Cash Credit- This credit is given by traders or the banker on the basis of cash or

inventory. The trader or the banker may lend money or goods to the business on credit

business. The business is entitled to pay back the amount to the respective person within a

period of 90 days.

Hire purchase and leasing- These are loans which are provided to the business while

purchasing inventory or machinery for the organization. The business can purchase

machinery or inventory and can pay the amount either in instalment or on lease basis.

1.2 Implication of the sources

Sources Legal Implications Financial Implications Dilution of

ownership

Share Capital/

Debenture

All the facts and

figure and

rules/regulations must

be stated to the

investors. The

formulation made by

the legal framework of

the country is

mandatory to be

followed so as to

avoid any fine or

charge.

As shareholder does not

agree to retain earnings,

the business is not able

to save for future use.

Also in the case of

insolvency the investor

may cease companies

retained earnings to

recover their dividend

amount.

The ownership of the

shares/debentures

passes to the

respective purchaser

only.

Retained Earning The shareholders in The profit in the There is no dilution to

Share Capital or Debenture- The business can also raise an IPO i.e. initial public offering.

In this, the public invests a portion of their income in the business by acquiring ownership of

business in the form of shares or debentures. The company does not have to pay interest

over the raised amount but each year they can pay back profit in the form of dividend to the

shareholders. Venture Capital- A venture capitalist is a person who is eager to invest his/her income in

other business. These individual are generally bothered to receive the ownership or a certain

amount of profit in return to their investment.

Short term sources are-

Trade/Cash Credit- This credit is given by traders or the banker on the basis of cash or

inventory. The trader or the banker may lend money or goods to the business on credit

business. The business is entitled to pay back the amount to the respective person within a

period of 90 days.

Hire purchase and leasing- These are loans which are provided to the business while

purchasing inventory or machinery for the organization. The business can purchase

machinery or inventory and can pay the amount either in instalment or on lease basis.

1.2 Implication of the sources

Sources Legal Implications Financial Implications Dilution of

ownership

Share Capital/

Debenture

All the facts and

figure and

rules/regulations must

be stated to the

investors. The

formulation made by

the legal framework of

the country is

mandatory to be

followed so as to

avoid any fine or

charge.

As shareholder does not

agree to retain earnings,

the business is not able

to save for future use.

Also in the case of

insolvency the investor

may cease companies

retained earnings to

recover their dividend

amount.

The ownership of the

shares/debentures

passes to the

respective purchaser

only.

Retained Earning The shareholders in The profit in the There is no dilution to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

many instances do not

agree to retain

business earning as

this way they do not

get dividends. Thus

they legally bound

the business.

financial statement

reduces if the business

does not retain its

earning. This is not

considered as an ideal

situation for the

business.

ownership as retained

earnings are part of

compan’s own

earnings unless paid to

the shareholders.

Loan All the major

formalities must be

clearly read and

understood by the

business before

agreeing to the terms

of the banker. Loan

has to be paid on time

so as to not let the

banker cease the

property of the

business to recover

their amount.

Bank or the financial

institution will cease

company’s property to

claim their amount

loaned to the business.

The loan amount can

be used but it has to be

paid back with interest

to the banker. Thus,

the ownership of the

money still stays with

the banker or the loan

giver.

Venture Capital The right or

ownership given to the

capitalist must be

limited to a certain

extent. So as to avoid

any issue regarding

legal rights of the

company for the

future.

The company is entitled

to pay for the venture

capitalist his/her share

of ownership despite

facing losses or deficits.

The venture capital

receives a share in the

business in exchange

of his/her investment.

Trade/ Cash credit All the paper work

regarding interest and

time period must be

understood very

properly. Legal action

The banker or the debtor

may charge extra in case

of late payment this will

increase the cost for the

business.

The ownership of the

money stays with the

banker as the money

or credit given must be

paid back.

agree to retain

business earning as

this way they do not

get dividends. Thus

they legally bound

the business.

financial statement

reduces if the business

does not retain its

earning. This is not

considered as an ideal

situation for the

business.

ownership as retained

earnings are part of

compan’s own

earnings unless paid to

the shareholders.

Loan All the major

formalities must be

clearly read and

understood by the

business before

agreeing to the terms

of the banker. Loan

has to be paid on time

so as to not let the

banker cease the

property of the

business to recover

their amount.

Bank or the financial

institution will cease

company’s property to

claim their amount

loaned to the business.

The loan amount can

be used but it has to be

paid back with interest

to the banker. Thus,

the ownership of the

money still stays with

the banker or the loan

giver.

Venture Capital The right or

ownership given to the

capitalist must be

limited to a certain

extent. So as to avoid

any issue regarding

legal rights of the

company for the

future.

The company is entitled

to pay for the venture

capitalist his/her share

of ownership despite

facing losses or deficits.

The venture capital

receives a share in the

business in exchange

of his/her investment.

Trade/ Cash credit All the paper work

regarding interest and

time period must be

understood very

properly. Legal action

The banker or the debtor

may charge extra in case

of late payment this will

increase the cost for the

business.

The ownership of the

money stays with the

banker as the money

or credit given must be

paid back.

can be taken if the

credit is not returned

on time.

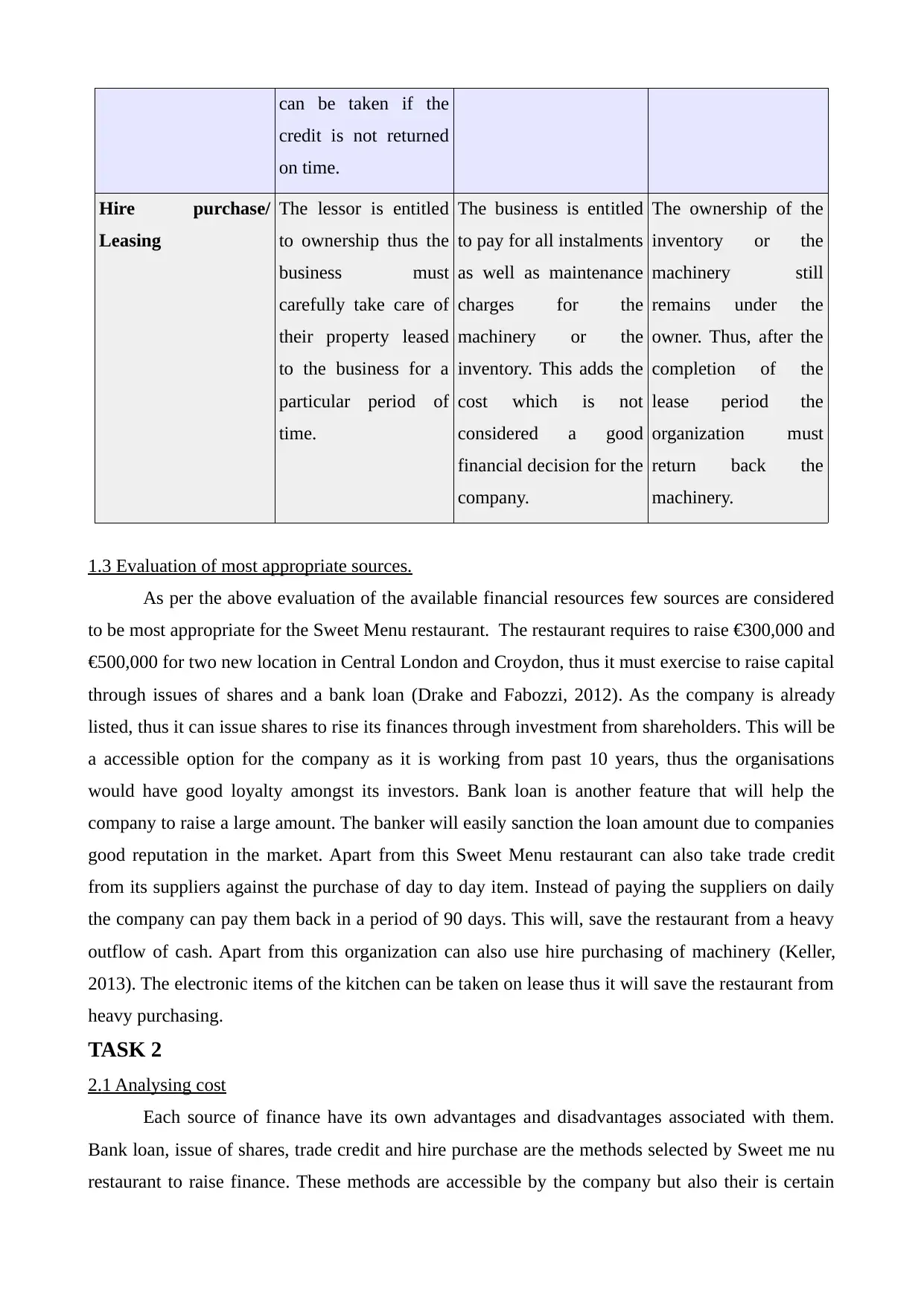

Hire purchase/

Leasing

The lessor is entitled

to ownership thus the

business must

carefully take care of

their property leased

to the business for a

particular period of

time.

The business is entitled

to pay for all instalments

as well as maintenance

charges for the

machinery or the

inventory. This adds the

cost which is not

considered a good

financial decision for the

company.

The ownership of the

inventory or the

machinery still

remains under the

owner. Thus, after the

completion of the

lease period the

organization must

return back the

machinery.

1.3 Evaluation of most appropriate sources.

As per the above evaluation of the available financial resources few sources are considered

to be most appropriate for the Sweet Menu restaurant. The restaurant requires to raise €300,000 and

€500,000 for two new location in Central London and Croydon, thus it must exercise to raise capital

through issues of shares and a bank loan (Drake and Fabozzi, 2012). As the company is already

listed, thus it can issue shares to rise its finances through investment from shareholders. This will be

a accessible option for the company as it is working from past 10 years, thus the organisations

would have good loyalty amongst its investors. Bank loan is another feature that will help the

company to raise a large amount. The banker will easily sanction the loan amount due to companies

good reputation in the market. Apart from this Sweet Menu restaurant can also take trade credit

from its suppliers against the purchase of day to day item. Instead of paying the suppliers on daily

the company can pay them back in a period of 90 days. This will, save the restaurant from a heavy

outflow of cash. Apart from this organization can also use hire purchasing of machinery (Keller,

2013). The electronic items of the kitchen can be taken on lease thus it will save the restaurant from

heavy purchasing.

TASK 2

2.1 Analysing cost

Each source of finance have its own advantages and disadvantages associated with them.

Bank loan, issue of shares, trade credit and hire purchase are the methods selected by Sweet me nu

restaurant to raise finance. These methods are accessible by the company but also their is certain

credit is not returned

on time.

Hire purchase/

Leasing

The lessor is entitled

to ownership thus the

business must

carefully take care of

their property leased

to the business for a

particular period of

time.

The business is entitled

to pay for all instalments

as well as maintenance

charges for the

machinery or the

inventory. This adds the

cost which is not

considered a good

financial decision for the

company.

The ownership of the

inventory or the

machinery still

remains under the

owner. Thus, after the

completion of the

lease period the

organization must

return back the

machinery.

1.3 Evaluation of most appropriate sources.

As per the above evaluation of the available financial resources few sources are considered

to be most appropriate for the Sweet Menu restaurant. The restaurant requires to raise €300,000 and

€500,000 for two new location in Central London and Croydon, thus it must exercise to raise capital

through issues of shares and a bank loan (Drake and Fabozzi, 2012). As the company is already

listed, thus it can issue shares to rise its finances through investment from shareholders. This will be

a accessible option for the company as it is working from past 10 years, thus the organisations

would have good loyalty amongst its investors. Bank loan is another feature that will help the

company to raise a large amount. The banker will easily sanction the loan amount due to companies

good reputation in the market. Apart from this Sweet Menu restaurant can also take trade credit

from its suppliers against the purchase of day to day item. Instead of paying the suppliers on daily

the company can pay them back in a period of 90 days. This will, save the restaurant from a heavy

outflow of cash. Apart from this organization can also use hire purchasing of machinery (Keller,

2013). The electronic items of the kitchen can be taken on lease thus it will save the restaurant from

heavy purchasing.

TASK 2

2.1 Analysing cost

Each source of finance have its own advantages and disadvantages associated with them.

Bank loan, issue of shares, trade credit and hire purchase are the methods selected by Sweet me nu

restaurant to raise finance. These methods are accessible by the company but also their is certain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

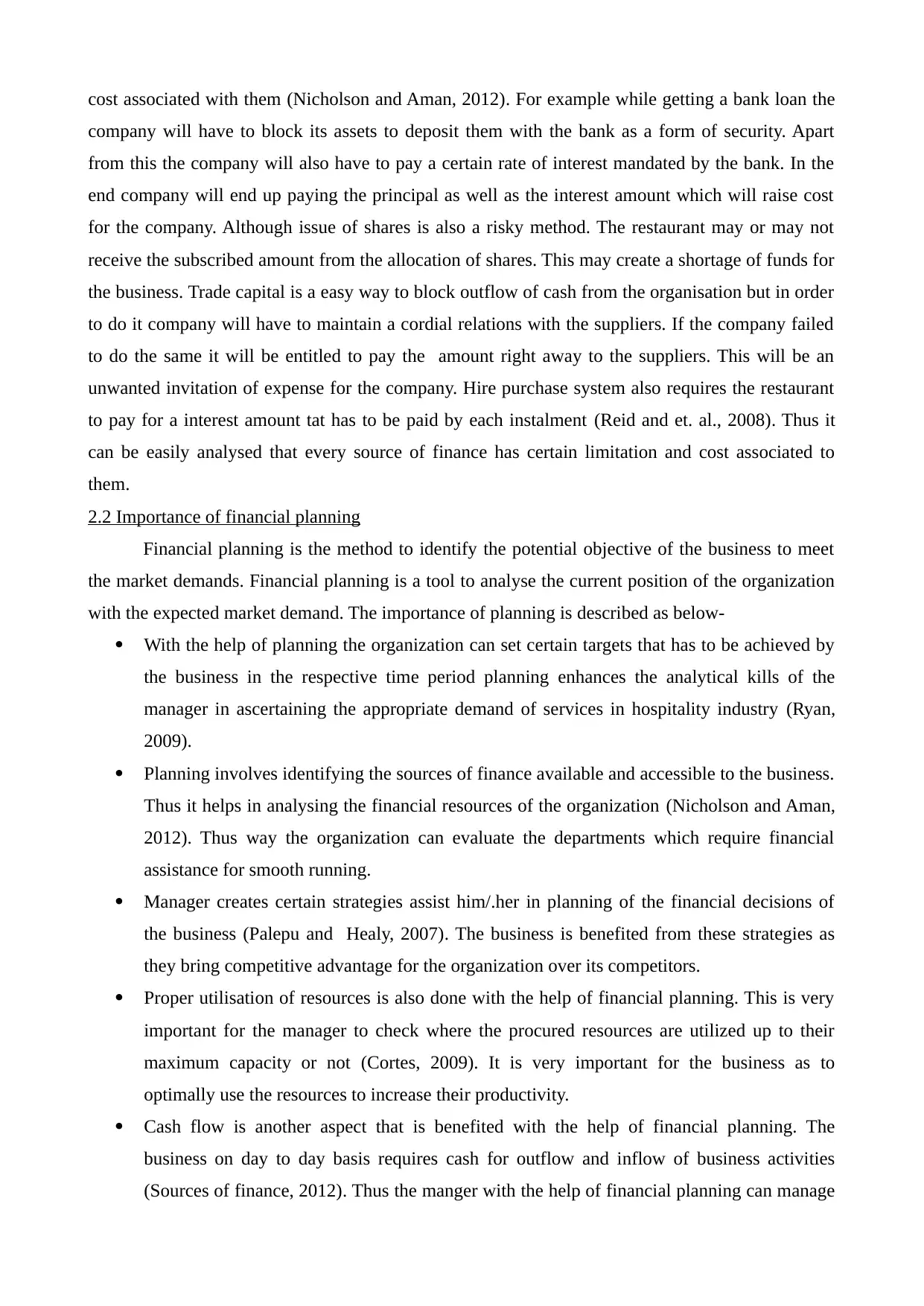

cost associated with them (Nicholson and Aman, 2012). For example while getting a bank loan the

company will have to block its assets to deposit them with the bank as a form of security. Apart

from this the company will also have to pay a certain rate of interest mandated by the bank. In the

end company will end up paying the principal as well as the interest amount which will raise cost

for the company. Although issue of shares is also a risky method. The restaurant may or may not

receive the subscribed amount from the allocation of shares. This may create a shortage of funds for

the business. Trade capital is a easy way to block outflow of cash from the organisation but in order

to do it company will have to maintain a cordial relations with the suppliers. If the company failed

to do the same it will be entitled to pay the amount right away to the suppliers. This will be an

unwanted invitation of expense for the company. Hire purchase system also requires the restaurant

to pay for a interest amount tat has to be paid by each instalment (Reid and et. al., 2008). Thus it

can be easily analysed that every source of finance has certain limitation and cost associated to

them.

2.2 Importance of financial planning

Financial planning is the method to identify the potential objective of the business to meet

the market demands. Financial planning is a tool to analyse the current position of the organization

with the expected market demand. The importance of planning is described as below-

With the help of planning the organization can set certain targets that has to be achieved by

the business in the respective time period planning enhances the analytical kills of the

manager in ascertaining the appropriate demand of services in hospitality industry (Ryan,

2009).

Planning involves identifying the sources of finance available and accessible to the business.

Thus it helps in analysing the financial resources of the organization (Nicholson and Aman,

2012). Thus way the organization can evaluate the departments which require financial

assistance for smooth running.

Manager creates certain strategies assist him/.her in planning of the financial decisions of

the business (Palepu and Healy, 2007). The business is benefited from these strategies as

they bring competitive advantage for the organization over its competitors.

Proper utilisation of resources is also done with the help of financial planning. This is very

important for the manager to check where the procured resources are utilized up to their

maximum capacity or not (Cortes, 2009). It is very important for the business as to

optimally use the resources to increase their productivity.

Cash flow is another aspect that is benefited with the help of financial planning. The

business on day to day basis requires cash for outflow and inflow of business activities

(Sources of finance, 2012). Thus the manger with the help of financial planning can manage

company will have to block its assets to deposit them with the bank as a form of security. Apart

from this the company will also have to pay a certain rate of interest mandated by the bank. In the

end company will end up paying the principal as well as the interest amount which will raise cost

for the company. Although issue of shares is also a risky method. The restaurant may or may not

receive the subscribed amount from the allocation of shares. This may create a shortage of funds for

the business. Trade capital is a easy way to block outflow of cash from the organisation but in order

to do it company will have to maintain a cordial relations with the suppliers. If the company failed

to do the same it will be entitled to pay the amount right away to the suppliers. This will be an

unwanted invitation of expense for the company. Hire purchase system also requires the restaurant

to pay for a interest amount tat has to be paid by each instalment (Reid and et. al., 2008). Thus it

can be easily analysed that every source of finance has certain limitation and cost associated to

them.

2.2 Importance of financial planning

Financial planning is the method to identify the potential objective of the business to meet

the market demands. Financial planning is a tool to analyse the current position of the organization

with the expected market demand. The importance of planning is described as below-

With the help of planning the organization can set certain targets that has to be achieved by

the business in the respective time period planning enhances the analytical kills of the

manager in ascertaining the appropriate demand of services in hospitality industry (Ryan,

2009).

Planning involves identifying the sources of finance available and accessible to the business.

Thus it helps in analysing the financial resources of the organization (Nicholson and Aman,

2012). Thus way the organization can evaluate the departments which require financial

assistance for smooth running.

Manager creates certain strategies assist him/.her in planning of the financial decisions of

the business (Palepu and Healy, 2007). The business is benefited from these strategies as

they bring competitive advantage for the organization over its competitors.

Proper utilisation of resources is also done with the help of financial planning. This is very

important for the manager to check where the procured resources are utilized up to their

maximum capacity or not (Cortes, 2009). It is very important for the business as to

optimally use the resources to increase their productivity.

Cash flow is another aspect that is benefited with the help of financial planning. The

business on day to day basis requires cash for outflow and inflow of business activities

(Sources of finance, 2012). Thus the manger with the help of financial planning can manage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

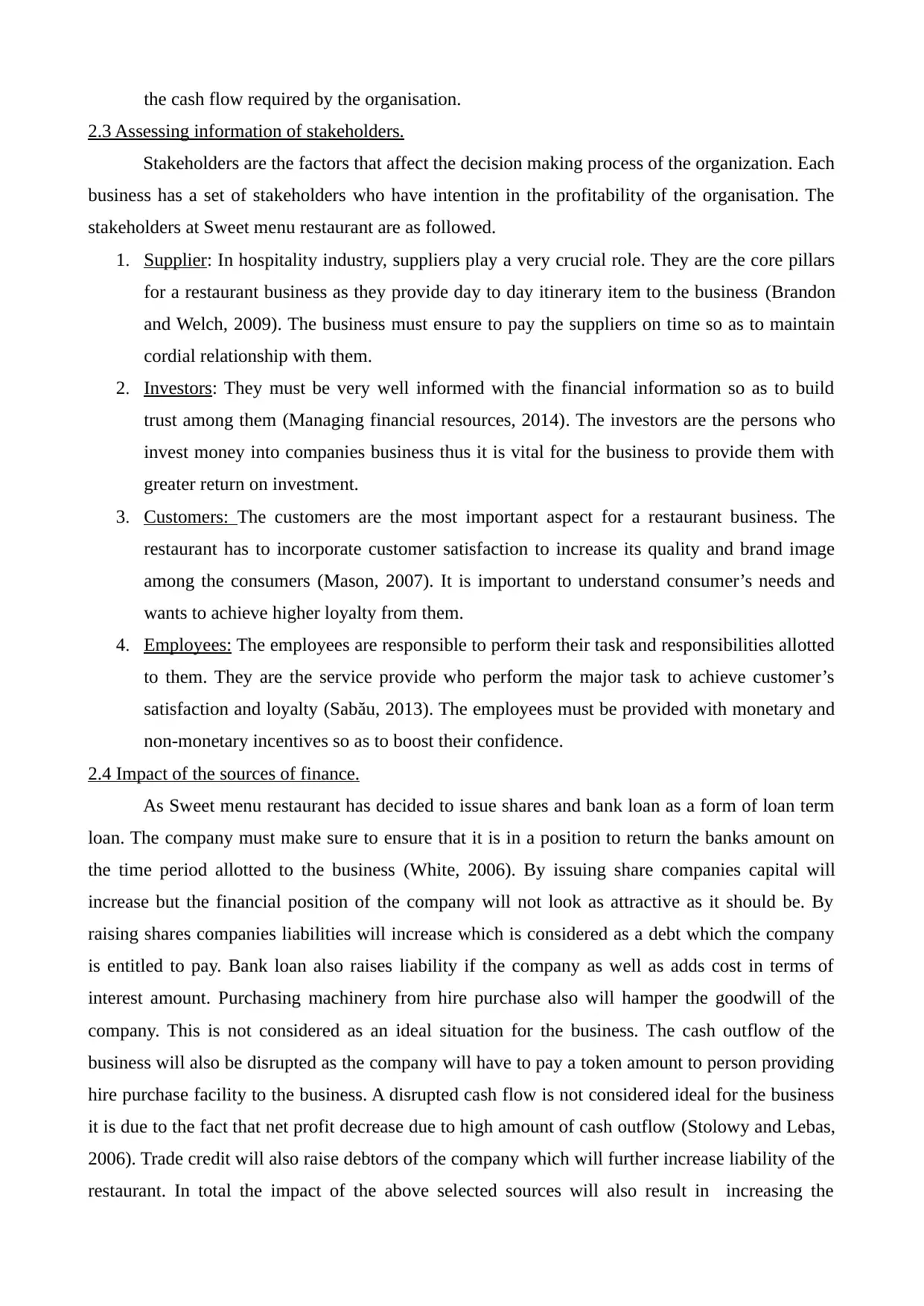

the cash flow required by the organisation.

2.3 Assessing information of stakeholders.

Stakeholders are the factors that affect the decision making process of the organization. Each

business has a set of stakeholders who have intention in the profitability of the organisation. The

stakeholders at Sweet menu restaurant are as followed.

1. Supplier: In hospitality industry, suppliers play a very crucial role. They are the core pillars

for a restaurant business as they provide day to day itinerary item to the business (Brandon

and Welch, 2009). The business must ensure to pay the suppliers on time so as to maintain

cordial relationship with them.

2. Investors: They must be very well informed with the financial information so as to build

trust among them (Managing financial resources, 2014). The investors are the persons who

invest money into companies business thus it is vital for the business to provide them with

greater return on investment.

3. Customers: The customers are the most important aspect for a restaurant business. The

restaurant has to incorporate customer satisfaction to increase its quality and brand image

among the consumers (Mason, 2007). It is important to understand consumer’s needs and

wants to achieve higher loyalty from them.

4. Employees: The employees are responsible to perform their task and responsibilities allotted

to them. They are the service provide who perform the major task to achieve customer’s

satisfaction and loyalty (Sabău, 2013). The employees must be provided with monetary and

non-monetary incentives so as to boost their confidence.

2.4 Impact of the sources of finance.

As Sweet menu restaurant has decided to issue shares and bank loan as a form of loan term

loan. The company must make sure to ensure that it is in a position to return the banks amount on

the time period allotted to the business (White, 2006). By issuing share companies capital will

increase but the financial position of the company will not look as attractive as it should be. By

raising shares companies liabilities will increase which is considered as a debt which the company

is entitled to pay. Bank loan also raises liability if the company as well as adds cost in terms of

interest amount. Purchasing machinery from hire purchase also will hamper the goodwill of the

company. This is not considered as an ideal situation for the business. The cash outflow of the

business will also be disrupted as the company will have to pay a token amount to person providing

hire purchase facility to the business. A disrupted cash flow is not considered ideal for the business

it is due to the fact that net profit decrease due to high amount of cash outflow (Stolowy and Lebas,

2006). Trade credit will also raise debtors of the company which will further increase liability of the

restaurant. In total the impact of the above selected sources will also result in increasing the

2.3 Assessing information of stakeholders.

Stakeholders are the factors that affect the decision making process of the organization. Each

business has a set of stakeholders who have intention in the profitability of the organisation. The

stakeholders at Sweet menu restaurant are as followed.

1. Supplier: In hospitality industry, suppliers play a very crucial role. They are the core pillars

for a restaurant business as they provide day to day itinerary item to the business (Brandon

and Welch, 2009). The business must ensure to pay the suppliers on time so as to maintain

cordial relationship with them.

2. Investors: They must be very well informed with the financial information so as to build

trust among them (Managing financial resources, 2014). The investors are the persons who

invest money into companies business thus it is vital for the business to provide them with

greater return on investment.

3. Customers: The customers are the most important aspect for a restaurant business. The

restaurant has to incorporate customer satisfaction to increase its quality and brand image

among the consumers (Mason, 2007). It is important to understand consumer’s needs and

wants to achieve higher loyalty from them.

4. Employees: The employees are responsible to perform their task and responsibilities allotted

to them. They are the service provide who perform the major task to achieve customer’s

satisfaction and loyalty (Sabău, 2013). The employees must be provided with monetary and

non-monetary incentives so as to boost their confidence.

2.4 Impact of the sources of finance.

As Sweet menu restaurant has decided to issue shares and bank loan as a form of loan term

loan. The company must make sure to ensure that it is in a position to return the banks amount on

the time period allotted to the business (White, 2006). By issuing share companies capital will

increase but the financial position of the company will not look as attractive as it should be. By

raising shares companies liabilities will increase which is considered as a debt which the company

is entitled to pay. Bank loan also raises liability if the company as well as adds cost in terms of

interest amount. Purchasing machinery from hire purchase also will hamper the goodwill of the

company. This is not considered as an ideal situation for the business. The cash outflow of the

business will also be disrupted as the company will have to pay a token amount to person providing

hire purchase facility to the business. A disrupted cash flow is not considered ideal for the business

it is due to the fact that net profit decrease due to high amount of cash outflow (Stolowy and Lebas,

2006). Trade credit will also raise debtors of the company which will further increase liability of the

restaurant. In total the impact of the above selected sources will also result in increasing the

liability of the business.

TASK 3

3.1 Analysing budget and proposing recommendations

Budget analysis enables thee manger in creating a budget for the goals and objectives

of the business. The process of the budget analysis includes formulating, estimating and report

making of the proposed budget of the company (Sources of finance, 2012). In the case study it

present financial statement of the Blue Island restaurant were presented. From these statements it

was identified that the restaurant is expensing more and earning less. It is also reducing company’s

profitability. Although cash and credit sales of the company are good but the expenses re very high

in comparison. The balance between earning and expenses is clearly not maintained which is

depicting a poor financial condition. Restaurant is not able to make god revenue due to the same

issue. In the month of November and December specifically the sales are low in comparison with

the high number of expenses. There is a negative net balance which shows that company must

make improvements in the present situation. The restaurant must make strategies and reduce

resources that are increasing cost of the company’s services (Mason, 2007). The management must

try to reduce prices of the services so as to attract higher number of customers . Apart from this un-

necessary expense must also be analysed and removed immediately.

3.2 Unit cost and pricing decision

Cost per Items Cost (£)

Non vegetarian Item 3

Vegetarian elements 1.5

Cost of making 3.5

Overhead Expenses 2

Total Cost 10

Mark Up (40%) 4

Value Added Tax (VAT) 2

Total Selling Price 16

Formula for Food Cost Percentage=

Total Costs of Ingredients/ Selling Price * 100

TASK 3

3.1 Analysing budget and proposing recommendations

Budget analysis enables thee manger in creating a budget for the goals and objectives

of the business. The process of the budget analysis includes formulating, estimating and report

making of the proposed budget of the company (Sources of finance, 2012). In the case study it

present financial statement of the Blue Island restaurant were presented. From these statements it

was identified that the restaurant is expensing more and earning less. It is also reducing company’s

profitability. Although cash and credit sales of the company are good but the expenses re very high

in comparison. The balance between earning and expenses is clearly not maintained which is

depicting a poor financial condition. Restaurant is not able to make god revenue due to the same

issue. In the month of November and December specifically the sales are low in comparison with

the high number of expenses. There is a negative net balance which shows that company must

make improvements in the present situation. The restaurant must make strategies and reduce

resources that are increasing cost of the company’s services (Mason, 2007). The management must

try to reduce prices of the services so as to attract higher number of customers . Apart from this un-

necessary expense must also be analysed and removed immediately.

3.2 Unit cost and pricing decision

Cost per Items Cost (£)

Non vegetarian Item 3

Vegetarian elements 1.5

Cost of making 3.5

Overhead Expenses 2

Total Cost 10

Mark Up (40%) 4

Value Added Tax (VAT) 2

Total Selling Price 16

Formula for Food Cost Percentage=

Total Costs of Ingredients/ Selling Price * 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Percentage of Food Cost = 10/16*100

Total Percentage = 62.50%

The unit cost analysis is done to identify the profit made by the company after the

calculation of the cost its products and services (Management accounting, 2014). After levying 20

% VAT and service tax charges the restaurant is estimated to make 40% profit from the cost

analysis. The selling price of each menu is £16 and the food cost percentage is 62.50%. This depicts

that the company will be able to generate a reasonable amount of profit from the sale of its services.

The restaurant must plan for the rice of its items so as to increase the profit margin. Already the

restaurant is making 40% profit from the cost analysis (Palepu and Healy, 2007). It can increase the

profit by reasonable pricing the products and lowering the cost of its services.

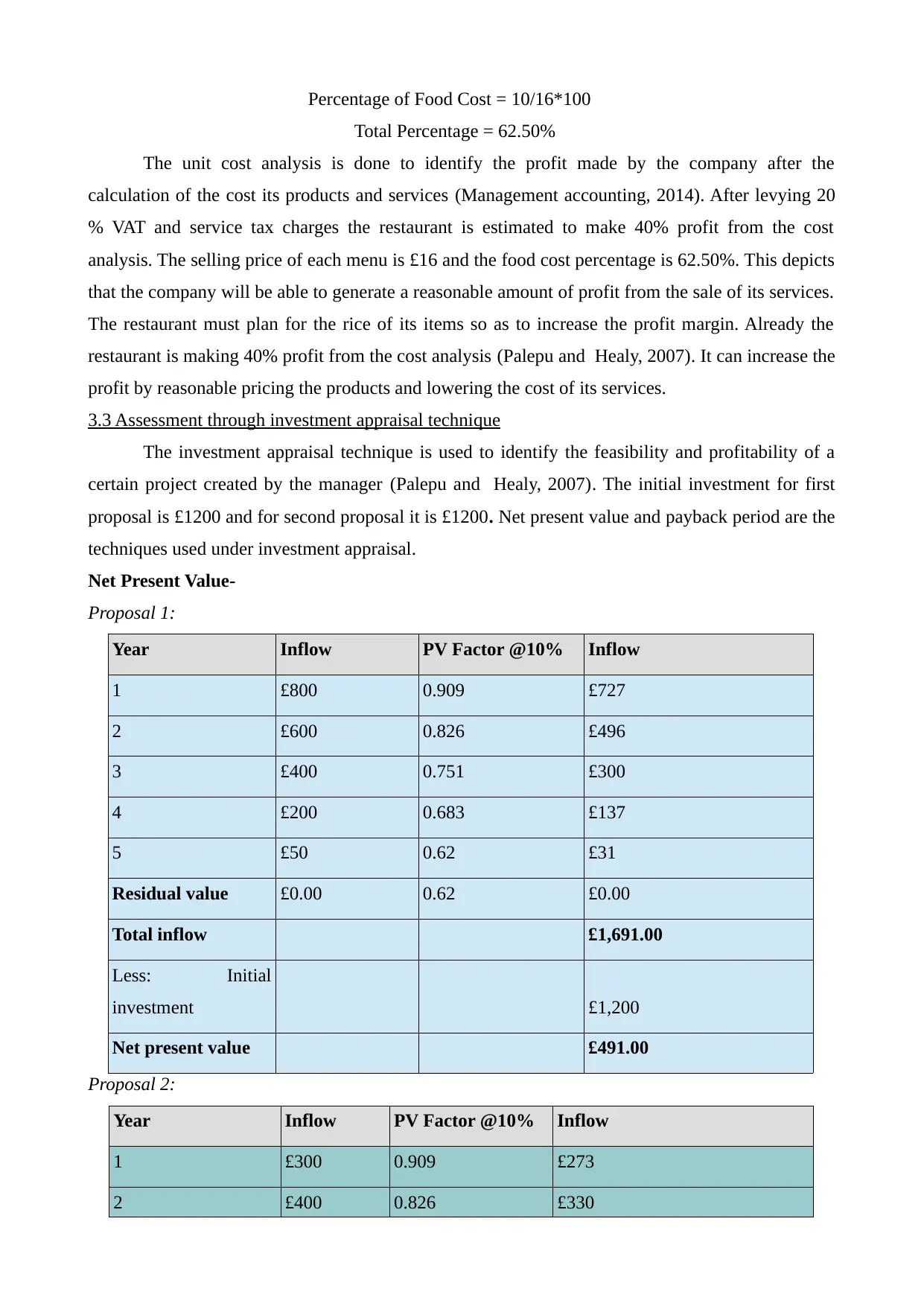

3.3 Assessment through investment appraisal technique

The investment appraisal technique is used to identify the feasibility and profitability of a

certain project created by the manager (Palepu and Healy, 2007). The initial investment for first

proposal is £1200 and for second proposal it is £1200. Net present value and payback period are the

techniques used under investment appraisal.

Net Present Value-

Proposal 1:

Year Inflow PV Factor @10% Inflow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow PV Factor @10% Inflow

1 £300 0.909 £273

2 £400 0.826 £330

Total Percentage = 62.50%

The unit cost analysis is done to identify the profit made by the company after the

calculation of the cost its products and services (Management accounting, 2014). After levying 20

% VAT and service tax charges the restaurant is estimated to make 40% profit from the cost

analysis. The selling price of each menu is £16 and the food cost percentage is 62.50%. This depicts

that the company will be able to generate a reasonable amount of profit from the sale of its services.

The restaurant must plan for the rice of its items so as to increase the profit margin. Already the

restaurant is making 40% profit from the cost analysis (Palepu and Healy, 2007). It can increase the

profit by reasonable pricing the products and lowering the cost of its services.

3.3 Assessment through investment appraisal technique

The investment appraisal technique is used to identify the feasibility and profitability of a

certain project created by the manager (Palepu and Healy, 2007). The initial investment for first

proposal is £1200 and for second proposal it is £1200. Net present value and payback period are the

techniques used under investment appraisal.

Net Present Value-

Proposal 1:

Year Inflow PV Factor @10% Inflow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

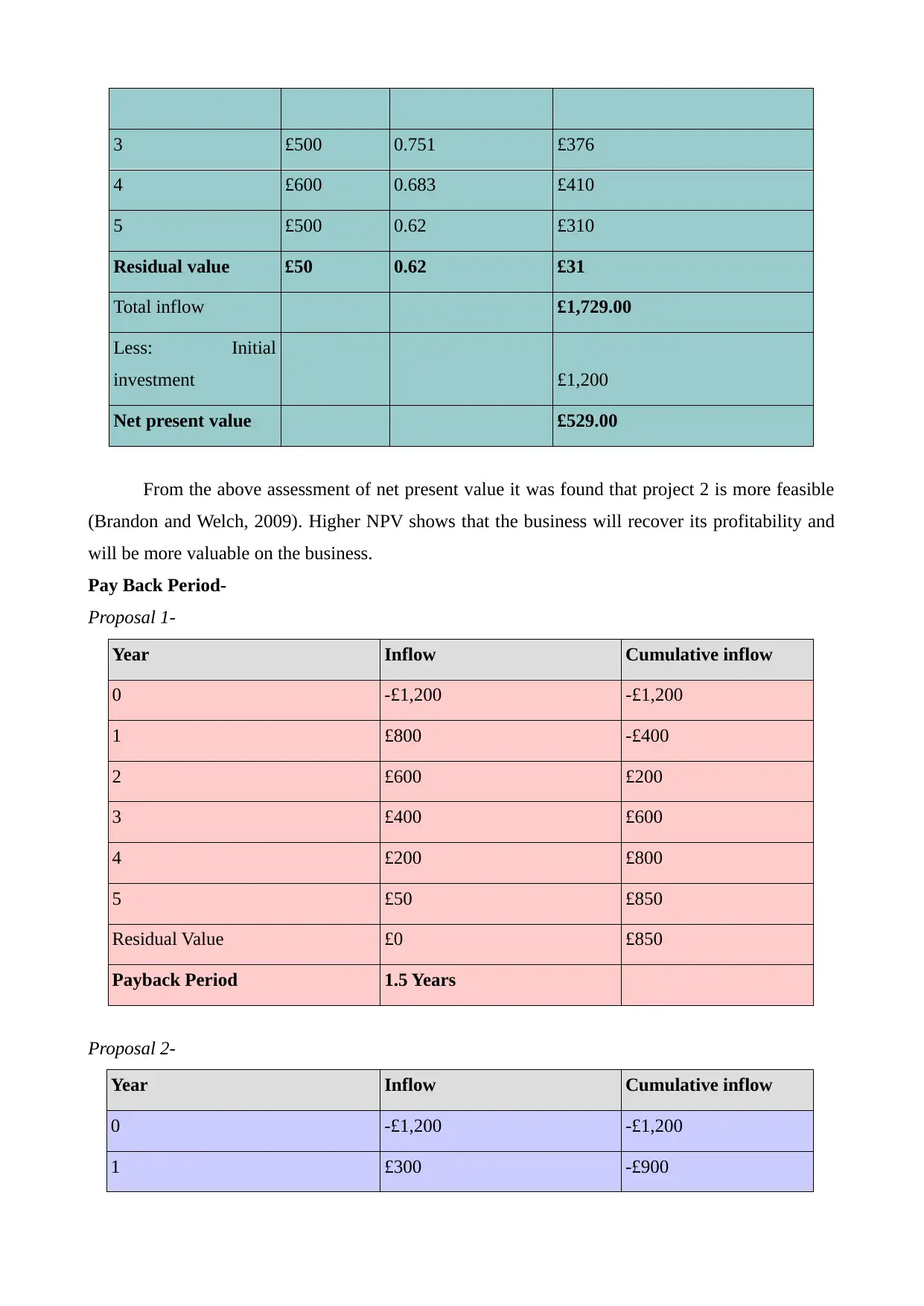

Proposal 2:

Year Inflow PV Factor @10% Inflow

1 £300 0.909 £273

2 £400 0.826 £330

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

From the above assessment of net present value it was found that project 2 is more feasible

(Brandon and Welch, 2009). Higher NPV shows that the business will recover its profitability and

will be more valuable on the business.

Pay Back Period-

Proposal 1-

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2-

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

From the above assessment of net present value it was found that project 2 is more feasible

(Brandon and Welch, 2009). Higher NPV shows that the business will recover its profitability and

will be more valuable on the business.

Pay Back Period-

Proposal 1-

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2-

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

It is very clear from the above that proposal 1 yields and early return on the investment

(Brandon and Welch, 2009). Thus it is feasible for the business to choose this proposal to achieve a

higher return on the investment in 1.5 year’s only.

TASK 4

4.1 Financial statements

Financial statements are used to record all the financial transactions of the business. The

Blue Island restaurant presents information about business financial position in the following

statements.

Balance Sheet- The restaurant prepares balance sheet to identify its financial position. The

assets and liabilities are calculated to calculate the profit and revenue earned by the

company (White, 2006). The balance sheet also depicts the balance which is created

between assets and liability so as to maintain the financial position for the business.

Cash Flow statement- All the information about the inflow and outflow of cash is

represented in the cash flow statement (Management accounting, 2014). Cash received or

earned and cash paid in any expense or investment activity is noted in this statement. This is

helpful for the business in identify the position of cash in the business.

Income statement- The profit and loss earned by the business is mentioned in the income

statement (Drake and Fabozzi, 2012). The income statement basically depicts the income

earned by the business and is useful in identifying the net profit of the business.

4.2 Comparison between financial formats

Businesses are divided on the basis of their ownership. They are sole proprietor, limited

company and partnership firm. Each business maintains different financial formats, they are as

followed. Sole Proprietor- A sole proprietor is a business owner who individually operates and mange

business. In sole proprietorship the owner is not entitled to maintain all the financial

statements (Palepu and Healy, 2007). Only in final assessment of tax the proprietor is

required to maintain the record of earnings.

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

It is very clear from the above that proposal 1 yields and early return on the investment

(Brandon and Welch, 2009). Thus it is feasible for the business to choose this proposal to achieve a

higher return on the investment in 1.5 year’s only.

TASK 4

4.1 Financial statements

Financial statements are used to record all the financial transactions of the business. The

Blue Island restaurant presents information about business financial position in the following

statements.

Balance Sheet- The restaurant prepares balance sheet to identify its financial position. The

assets and liabilities are calculated to calculate the profit and revenue earned by the

company (White, 2006). The balance sheet also depicts the balance which is created

between assets and liability so as to maintain the financial position for the business.

Cash Flow statement- All the information about the inflow and outflow of cash is

represented in the cash flow statement (Management accounting, 2014). Cash received or

earned and cash paid in any expense or investment activity is noted in this statement. This is

helpful for the business in identify the position of cash in the business.

Income statement- The profit and loss earned by the business is mentioned in the income

statement (Drake and Fabozzi, 2012). The income statement basically depicts the income

earned by the business and is useful in identifying the net profit of the business.

4.2 Comparison between financial formats

Businesses are divided on the basis of their ownership. They are sole proprietor, limited

company and partnership firm. Each business maintains different financial formats, they are as

followed. Sole Proprietor- A sole proprietor is a business owner who individually operates and mange

business. In sole proprietorship the owner is not entitled to maintain all the financial

statements (Palepu and Healy, 2007). Only in final assessment of tax the proprietor is

required to maintain the record of earnings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.