Financial Reporting: IAS, IFRS, and Financial Statement Analysis

VerifiedAdded on 2020/10/05

|18

|4021

|212

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, encompassing its context, purpose, and the conceptual and regulatory framework that governs it. The report explores the qualitative characteristics of financial information, emphasizing relevance, reliability, comparability, and understandability. It identifies the main stakeholders of an organization, including internal and external users, and details the benefits of financial information to each group. The value of financial reporting in meeting organizational objectives and fostering growth is examined, along with an overview of the main financial statements as per IAS 1, including the statement of profit and loss, balance sheet, statement of equity, and cash flow statements. A comparative analysis of Marks & Spencer's financial statements over two years is presented, along with a discussion of the differences between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), and the benefits of IFRS adoption. The report concludes by addressing the varying degrees of compliance with IFRS by organizations globally.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

1. Context and purpose of financial reporting..............................................................................3

2. The conceptual and regulatory framework of financial reporting and its qualitative

characteristics...............................................................................................................................4

3. The main stakeholders of an organization and benefits of financial information to them ......6

4. Value of financial reporting for meeting organizational objectives and growth ...................7

5. Main financial statements as per IAS 1....................................................................................8

6. Two years financial statements of marks and Spencer..........................................................11

7. Difference between international accounting standard (IAS) and International Financial

reporting standards (IFRS).........................................................................................................13

8. Benefits of IFRS.....................................................................................................................14

9. Identifying the varying degree of compliance with IFRS by organization across the world

....................................................................................................................................................15

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

1. Context and purpose of financial reporting..............................................................................3

2. The conceptual and regulatory framework of financial reporting and its qualitative

characteristics...............................................................................................................................4

3. The main stakeholders of an organization and benefits of financial information to them ......6

4. Value of financial reporting for meeting organizational objectives and growth ...................7

5. Main financial statements as per IAS 1....................................................................................8

6. Two years financial statements of marks and Spencer..........................................................11

7. Difference between international accounting standard (IAS) and International Financial

reporting standards (IFRS).........................................................................................................13

8. Benefits of IFRS.....................................................................................................................14

9. Identifying the varying degree of compliance with IFRS by organization across the world

....................................................................................................................................................15

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Financial reporting is a process through which financial information is presented in the

statements. It helps in providing information to stakeholders about the performance and position

of firm. Financial reporting includes profit and loss statement, balance sheet and cash flow

statement. This assignment will include context and purpose of financial reporting. Furthermore,

it will examine the conceptual and regulatory framework of financial reporting and its qualitative

characteristics that makes the financial information more reliable. Also, it will provide main

stakeholders of organization and benefit to them by financial information. Moreover, it will

provide importance of financial reporting. Also, it will contain information about the financial

statement of the organization to identify its performance. This assignment will consist

difference between international accounting standard and international financial reporting

standards.

MAIN BODY

1. Context and purpose of financial reporting.

Financial reporting includes disclosure of financial information to management to

provide them information about the performance of organization to make effective decision to

improve the performance of firm. Financial reporting is used for the serving two purposes. first,

it helps management in effective decision making which helps the organization in performing

effectively and efficiently in the industry to increase its profitability (Chen and et.al., 2016). It

provides information to management about the strength and weakness of company to make

strategies and planning to reduce the weaknesses to improve performance of firm. Second,

financial reporting provides information to the stakeholders of company about the financial

health and activities of the firm.

This information provides assistance to stakeholders to make their decision about the

investment to be done in the organization. Also helps the stakeholder to compare the firm

performance with that of other to identify its growth in the industry (Nobes, 2014). It provides

assistance to management by providing them relevant and useful information. Financial reporting

includes profit and loss accounting, balance sheet and cash flows statements.

Financial reporting is a process through which financial information is presented in the

statements. It helps in providing information to stakeholders about the performance and position

of firm. Financial reporting includes profit and loss statement, balance sheet and cash flow

statement. This assignment will include context and purpose of financial reporting. Furthermore,

it will examine the conceptual and regulatory framework of financial reporting and its qualitative

characteristics that makes the financial information more reliable. Also, it will provide main

stakeholders of organization and benefit to them by financial information. Moreover, it will

provide importance of financial reporting. Also, it will contain information about the financial

statement of the organization to identify its performance. This assignment will consist

difference between international accounting standard and international financial reporting

standards.

MAIN BODY

1. Context and purpose of financial reporting.

Financial reporting includes disclosure of financial information to management to

provide them information about the performance of organization to make effective decision to

improve the performance of firm. Financial reporting is used for the serving two purposes. first,

it helps management in effective decision making which helps the organization in performing

effectively and efficiently in the industry to increase its profitability (Chen and et.al., 2016). It

provides information to management about the strength and weakness of company to make

strategies and planning to reduce the weaknesses to improve performance of firm. Second,

financial reporting provides information to the stakeholders of company about the financial

health and activities of the firm.

This information provides assistance to stakeholders to make their decision about the

investment to be done in the organization. Also helps the stakeholder to compare the firm

performance with that of other to identify its growth in the industry (Nobes, 2014). It provides

assistance to management by providing them relevant and useful information. Financial reporting

includes profit and loss accounting, balance sheet and cash flows statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit and loss accounts are prepared to provide information about the net profit and loss

for the company. This statement provides the information about performance of the organization

by operating its various activities (financial reporting, 2016). Balance sheet is prepared in which

assets and liabilities of the firm are provided on the basis of which the position of the

organization is determined at a particular point of time. Cash flow statement under the financial

reporting provide information about cash inflow and outflow for the period on the basis of which

cash requirement of the company are determined to maintain the cash requirement for

performing various future activities of the company.

Financial reporting support in preparing budget for the future activities to perform the various

activities according to budget to get the profitability derived according to budget. Financial

reporting is used for various purposes which include decision making, information to

stakeholders, to identify the profitability and performance, determining the cash requirement etc.

2. The conceptual and regulatory framework of financial reporting and its qualitative

characteristics

The conceptual framework of financial reporting is based on objective of general purpose

of financial reporting and it also provides various qualitative characteristics on the basis of which

financial reporting are prepared. It set out the definition of assets , liabilities , equity, incomes

and expenses. The conceptual framework include the criteria for including assets and liabilities

and various measurement bases for them. It provides the concepts and guidance for presentation

and disclosure and also provide concepts relating to capital and capital maintenance.

Financial reporting are governed according to the standards set by international

accounting standard board. According to the set standards the main objective 0fn financial

reporting is to provide financial information to the stakeholders to make their decisions about

company growth. Financial reports are prepared according to the set standards to provide useful

and relevant information to various stakeholders of the organization. This information helps

them in determining the performance and position of the firm in the market. Regulatory

framework for financial reporting is different for different organization such as sole proprietor,

partnership and company.

for the company. This statement provides the information about performance of the organization

by operating its various activities (financial reporting, 2016). Balance sheet is prepared in which

assets and liabilities of the firm are provided on the basis of which the position of the

organization is determined at a particular point of time. Cash flow statement under the financial

reporting provide information about cash inflow and outflow for the period on the basis of which

cash requirement of the company are determined to maintain the cash requirement for

performing various future activities of the company.

Financial reporting support in preparing budget for the future activities to perform the various

activities according to budget to get the profitability derived according to budget. Financial

reporting is used for various purposes which include decision making, information to

stakeholders, to identify the profitability and performance, determining the cash requirement etc.

2. The conceptual and regulatory framework of financial reporting and its qualitative

characteristics

The conceptual framework of financial reporting is based on objective of general purpose

of financial reporting and it also provides various qualitative characteristics on the basis of which

financial reporting are prepared. It set out the definition of assets , liabilities , equity, incomes

and expenses. The conceptual framework include the criteria for including assets and liabilities

and various measurement bases for them. It provides the concepts and guidance for presentation

and disclosure and also provide concepts relating to capital and capital maintenance.

Financial reporting are governed according to the standards set by international

accounting standard board. According to the set standards the main objective 0fn financial

reporting is to provide financial information to the stakeholders to make their decisions about

company growth. Financial reports are prepared according to the set standards to provide useful

and relevant information to various stakeholders of the organization. This information helps

them in determining the performance and position of the firm in the market. Regulatory

framework for financial reporting is different for different organization such as sole proprietor,

partnership and company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The financial reports are governed according to various rules and guidelines to form the

authentic information about the various activities of the organization. It is governed according to

IFRS and IASB. These are the boards which are formed for handling matters relating to reporting

of financial information. IFRS is international financial reporting standard boards which have set

the various standards for preparing the financial reporting. IASB is the board which has lead

down some rules which firm have to follow while preparing financial reports.

The qualitative characteristics of financial reporting

These are the attributes that makes the financial information provided in the financial

statements useful for the users. It denotes the quality of information provided and ensures that

the information is reliable and authentic. The following are the various quantitative

characteristics of financial reporting:

Relevance: it implies that the information contained in the financial statements are useful

to users as it helps them in making decisions. The information included must provide

helps the users in evaluating the past, present and futures activities of the firm.

Reliability: the information must be reliable and free from material error (Patelli and

Pedrini, 2015). Thus the information presented in the statements must be faithful and

present the authentic information about the transactions.

Comparability: the information provided in the financial reports must be comparable

with the other financial information of other accounting periods to determine the

performance of firm over the years.

Understandability: the information must be readily understandable to the users of

financial statements. It means that the information must be clearly presented to five

better understanding of the various activities of the firm.

authentic information about the various activities of the organization. It is governed according to

IFRS and IASB. These are the boards which are formed for handling matters relating to reporting

of financial information. IFRS is international financial reporting standard boards which have set

the various standards for preparing the financial reporting. IASB is the board which has lead

down some rules which firm have to follow while preparing financial reports.

The qualitative characteristics of financial reporting

These are the attributes that makes the financial information provided in the financial

statements useful for the users. It denotes the quality of information provided and ensures that

the information is reliable and authentic. The following are the various quantitative

characteristics of financial reporting:

Relevance: it implies that the information contained in the financial statements are useful

to users as it helps them in making decisions. The information included must provide

helps the users in evaluating the past, present and futures activities of the firm.

Reliability: the information must be reliable and free from material error (Patelli and

Pedrini, 2015). Thus the information presented in the statements must be faithful and

present the authentic information about the transactions.

Comparability: the information provided in the financial reports must be comparable

with the other financial information of other accounting periods to determine the

performance of firm over the years.

Understandability: the information must be readily understandable to the users of

financial statements. It means that the information must be clearly presented to five

better understanding of the various activities of the firm.

3. The main stakeholders of an organization and benefits of financial information to them

`There are various stakeholders of the organization which use the financial information to

determine various information about the company to make decision. There are internal and

external users of financial information.

`Internal stakeholders: It consist of users of financial information which are working in the

organization it consists of management, employees etc.

Management: the management of firm require the financial information for making

decisions to improve the performance and profitability of the firm on the basis of

information contained in the financial statements (Hunton, Libby and Mazza, 2015).

Management is provided with the financial information to make various operational and

financing decisions.

Employees: They are provided the financial information to determine the financial

performance of the firm in which they are working to identify their career goals.

Financial statements are provided to them to increase their employee involvement and

provide them understanding of the business.

External stakeholders: there are users of financial statements which are outside the

organization but have their interest in knowing the financial performance and position of firm. It

consists of the following:

Customers: they are provided by the financial statements to attract them towards the

organization to purchase their goods and services (Users of the Financial Statements,

2017). Financial statements help the customers in identifying the organization ability to

provide products and services according to their demands.

Investors: they are provided with the financial statements to provide them information

about the financial health of the firm to invest their money in business to get higher

returns.

Lenders or suppliers: they are the users of financial statements which lend money and

supply goods and services to organization. They require financial statements to get the

assurance about their money to be paid back which they have lent to the firm.

`There are various stakeholders of the organization which use the financial information to

determine various information about the company to make decision. There are internal and

external users of financial information.

`Internal stakeholders: It consist of users of financial information which are working in the

organization it consists of management, employees etc.

Management: the management of firm require the financial information for making

decisions to improve the performance and profitability of the firm on the basis of

information contained in the financial statements (Hunton, Libby and Mazza, 2015).

Management is provided with the financial information to make various operational and

financing decisions.

Employees: They are provided the financial information to determine the financial

performance of the firm in which they are working to identify their career goals.

Financial statements are provided to them to increase their employee involvement and

provide them understanding of the business.

External stakeholders: there are users of financial statements which are outside the

organization but have their interest in knowing the financial performance and position of firm. It

consists of the following:

Customers: they are provided by the financial statements to attract them towards the

organization to purchase their goods and services (Users of the Financial Statements,

2017). Financial statements help the customers in identifying the organization ability to

provide products and services according to their demands.

Investors: they are provided with the financial statements to provide them information

about the financial health of the firm to invest their money in business to get higher

returns.

Lenders or suppliers: they are the users of financial statements which lend money and

supply goods and services to organization. They require financial statements to get the

assurance about their money to be paid back which they have lent to the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Government: financial statements are provided to the governments to identify if the firm

is performing its activities according the rules and regulations or not. Governments use

the financial information to determine if the company has paid the tax amount properly or

not.

Benefits to stakeholders of financial information

It helps the users of financial information to determine the profitability of the firm.

It supports the management in making decision or the organization to improve its

performance.

It helps investors in identifying the firm ability to generate higher returns for them.

It helps the suppliers and lenders in identifying the ability of the firm to pay its various

obligations.

4. Value of financial reporting for meeting organizational objectives and growth

Financial reporting is important for determining the profitability and position of the firm.

Financial reporting is valuable for achieving the objectives of organization as it helps the firm in

identifying its financial conditions on the basis of which firm is able to take decision. Financial

reporting assists the organization in improving their liquidity position to achieve their objectives

and targeted goals to attract more customers towards the firm (Leuz and Wysocki, 2016).

Financial reporting helps in increasing the brand image of the firm which assist in increasing the

investors for the company. Financial reporting assist in formulating strategies to improve the

operational activities of firm. It helps the firm in achieving their targeted goals by making

effective decisions for increasing the profitability of firm.

It assists in identifying the future cash requirement of the firm to perform various

activities accordingly to maintain the cash to pay the obligation of the organization. Financial

reporting helps the firm in identifying its performance to compare the results with its

competitors. Financial reporting is important to identify the various transactions taken place in

the firm to determine the growth of the firm and compare its performance with the past.

Financial statements prepared by the organization helps in providing direction to the organization

to improve the functioning to achieve the targeted goals of company effectively and efficiently

is performing its activities according the rules and regulations or not. Governments use

the financial information to determine if the company has paid the tax amount properly or

not.

Benefits to stakeholders of financial information

It helps the users of financial information to determine the profitability of the firm.

It supports the management in making decision or the organization to improve its

performance.

It helps investors in identifying the firm ability to generate higher returns for them.

It helps the suppliers and lenders in identifying the ability of the firm to pay its various

obligations.

4. Value of financial reporting for meeting organizational objectives and growth

Financial reporting is important for determining the profitability and position of the firm.

Financial reporting is valuable for achieving the objectives of organization as it helps the firm in

identifying its financial conditions on the basis of which firm is able to take decision. Financial

reporting assists the organization in improving their liquidity position to achieve their objectives

and targeted goals to attract more customers towards the firm (Leuz and Wysocki, 2016).

Financial reporting helps in increasing the brand image of the firm which assist in increasing the

investors for the company. Financial reporting assist in formulating strategies to improve the

operational activities of firm. It helps the firm in achieving their targeted goals by making

effective decisions for increasing the profitability of firm.

It assists in identifying the future cash requirement of the firm to perform various

activities accordingly to maintain the cash to pay the obligation of the organization. Financial

reporting helps the firm in identifying its performance to compare the results with its

competitors. Financial reporting is important to identify the various transactions taken place in

the firm to determine the growth of the firm and compare its performance with the past.

Financial statements prepared by the organization helps in providing direction to the organization

to improve the functioning to achieve the targeted goals of company effectively and efficiently

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Francis and et.al.,2015). It assists in identifying the value of its assets in the market to have

strong financial position to grow their business.

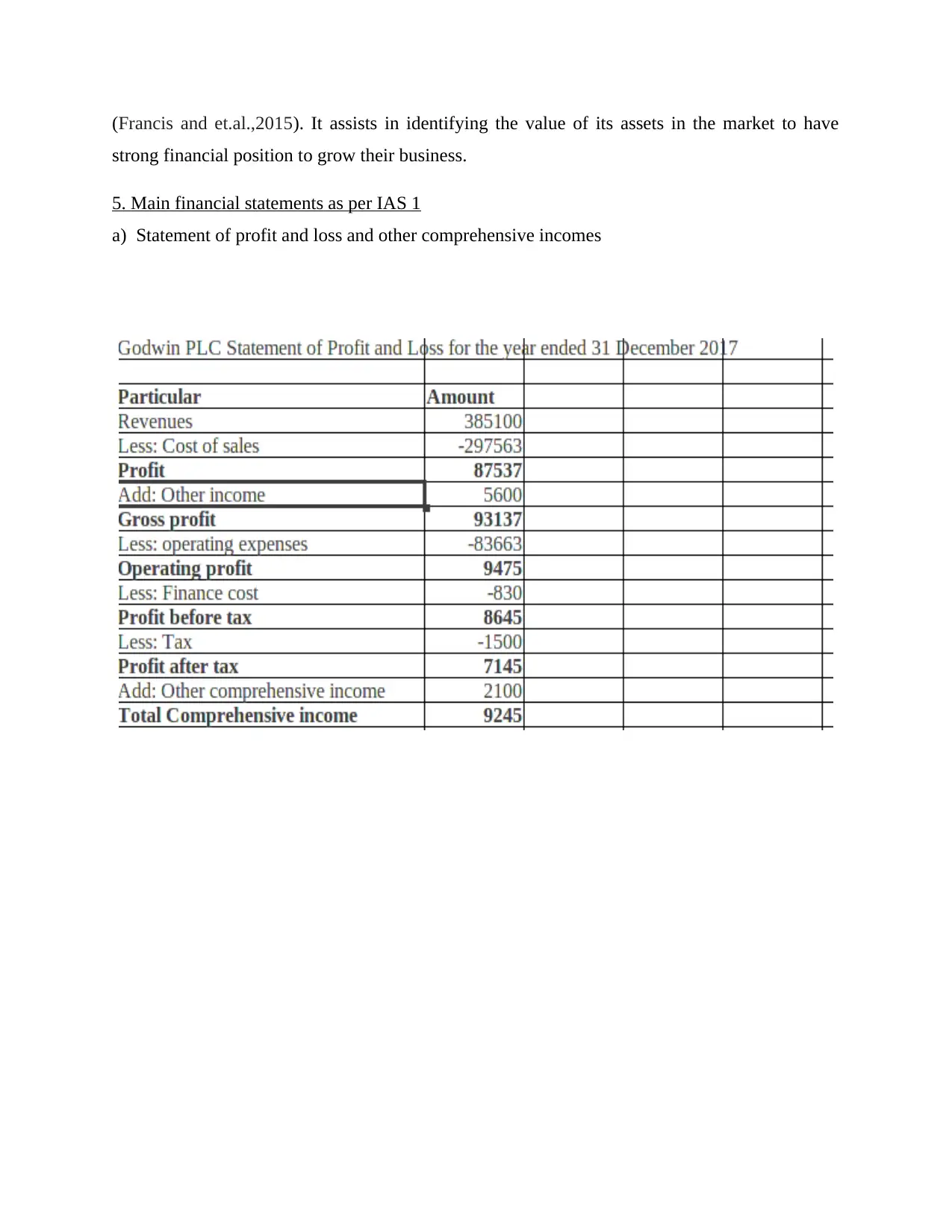

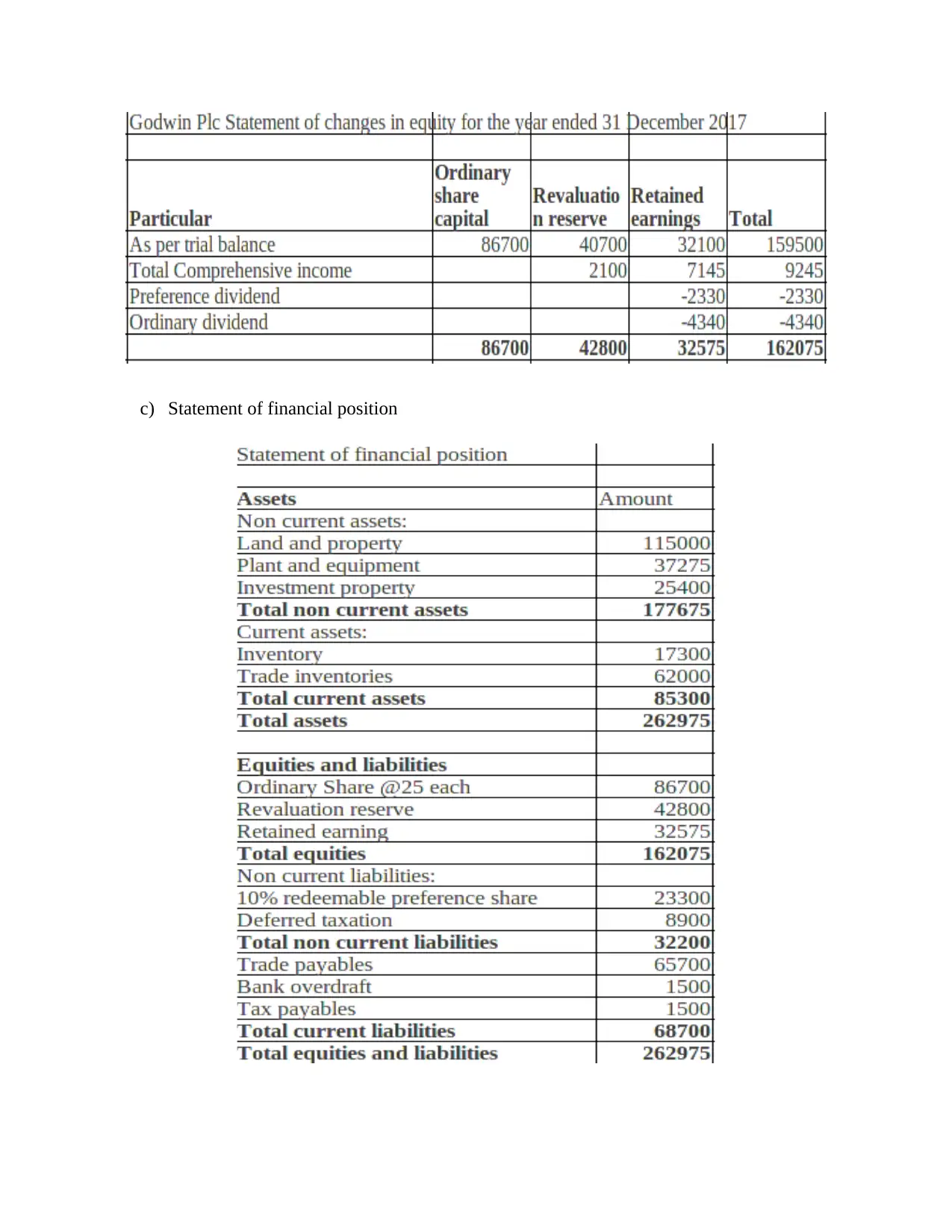

5. Main financial statements as per IAS 1

a) Statement of profit and loss and other comprehensive incomes

strong financial position to grow their business.

5. Main financial statements as per IAS 1

a) Statement of profit and loss and other comprehensive incomes

b) Statement of equity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c) Statement of financial position

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d) Cash flow statements provide information relating to cash inflow and outflow which helps 9n

determining the minimum cash requirement of the organization (Chen and et.al., 2016). Cash

flow statements include various activities such as operating activities, financing activity and

investing activity. There are various information which is not includes in the profit and loss

statements and balance sheet and are included in the cash flow statements. This information

include payment to suppliers for goods and services, buying merchandise receipts of sale of fixed

assets , payments related to mergers and acquisitions, payments of dividends, net borrowing etc.

cash flow shows changes in balance sheet and income affect cash and cash equivalent. Profit

and loss statements only include the activities of relating to expenses and incomes whereas cash

flow statement includes all the activities which causes inflow and outflow of cash. Balance sheet

statement include liabilities and assets which are important for identifying the position of

organization which are not included in cash flow statement as various activities which result into

flow of cash are included in the cash flow statement.

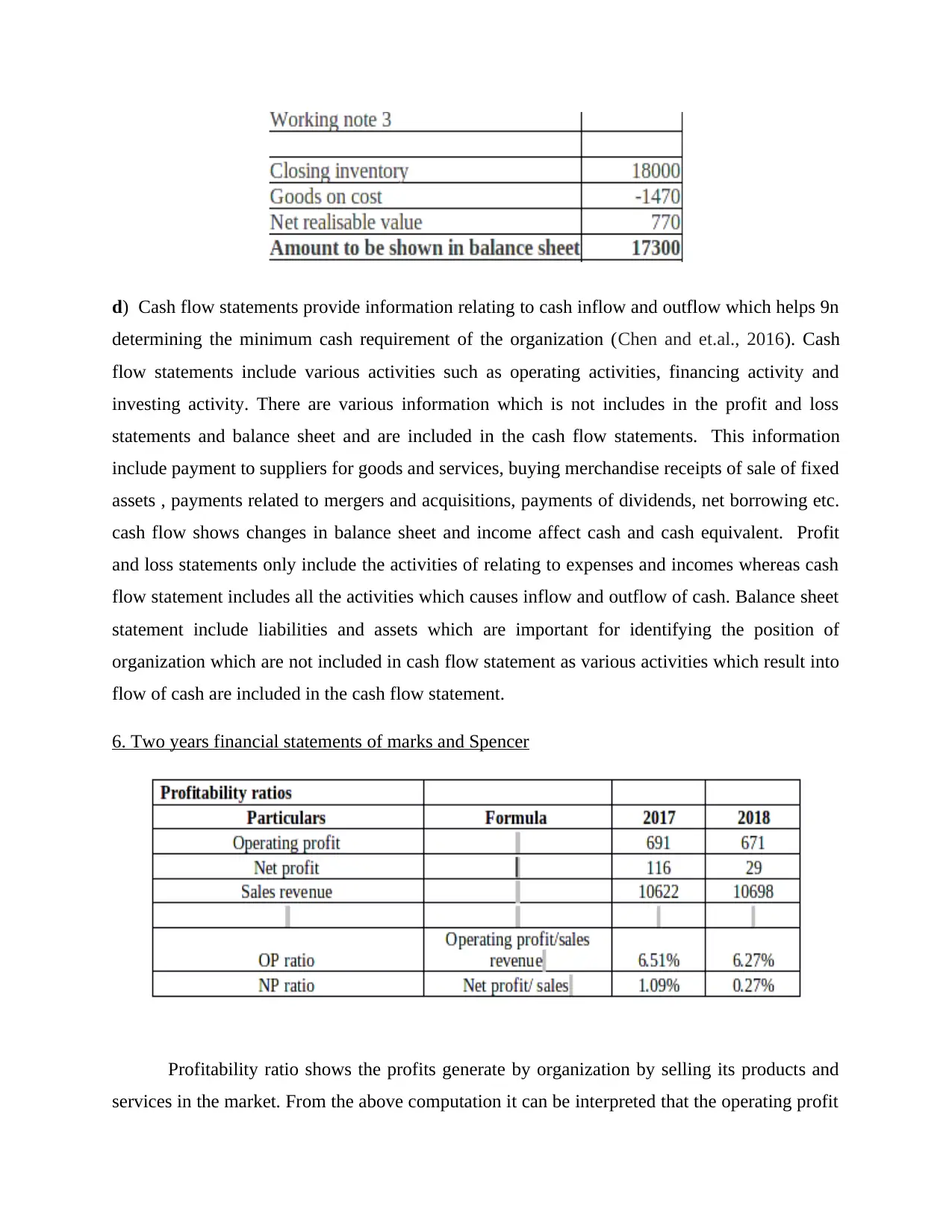

6. Two years financial statements of marks and Spencer

Profitability ratio shows the profits generate by organization by selling its products and

services in the market. From the above computation it can be interpreted that the operating profit

determining the minimum cash requirement of the organization (Chen and et.al., 2016). Cash

flow statements include various activities such as operating activities, financing activity and

investing activity. There are various information which is not includes in the profit and loss

statements and balance sheet and are included in the cash flow statements. This information

include payment to suppliers for goods and services, buying merchandise receipts of sale of fixed

assets , payments related to mergers and acquisitions, payments of dividends, net borrowing etc.

cash flow shows changes in balance sheet and income affect cash and cash equivalent. Profit

and loss statements only include the activities of relating to expenses and incomes whereas cash

flow statement includes all the activities which causes inflow and outflow of cash. Balance sheet

statement include liabilities and assets which are important for identifying the position of

organization which are not included in cash flow statement as various activities which result into

flow of cash are included in the cash flow statement.

6. Two years financial statements of marks and Spencer

Profitability ratio shows the profits generate by organization by selling its products and

services in the market. From the above computation it can be interpreted that the operating profit

ratio is 6.51 % which reduced to 6.27 % that shows profitability of marks and Spencer is

reduced. Furthermore, it can be interpreted that net profit of marks and Spencer were 1.09 % in

2017 which reduced to 0.27 % in 2018 that shows the profit for the period is reduced.

Liquidity ratio shows the ability of organization to pay its obligation. Current ratio as

computed above is 0.73 in 2017 which increased to 0.29 in 2018. It shows that the firm does not

have enough current assets to pay its obligations. Furthermore, it can be interpreted that quick

ratio as calculated is 0.41 in 2017 which reduced to 0.29 in 2018 it shows that firm is not capable

of paying its obligations.

Efficiency ratio measure the ability of organization to use its assets to generate income.

From the above computation it can be interpreted that stock turnover ratio is increased to 8.64 in

reduced. Furthermore, it can be interpreted that net profit of marks and Spencer were 1.09 % in

2017 which reduced to 0.27 % in 2018 that shows the profit for the period is reduced.

Liquidity ratio shows the ability of organization to pay its obligation. Current ratio as

computed above is 0.73 in 2017 which increased to 0.29 in 2018. It shows that the firm does not

have enough current assets to pay its obligations. Furthermore, it can be interpreted that quick

ratio as calculated is 0.41 in 2017 which reduced to 0.29 in 2018 it shows that firm is not capable

of paying its obligations.

Efficiency ratio measure the ability of organization to use its assets to generate income.

From the above computation it can be interpreted that stock turnover ratio is increased to 8.64 in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.