Financial Reporting: Analysis of Rita Plc's Financial Statements

VerifiedAdded on 2020/07/23

|13

|2757

|48

Report

AI Summary

This report provides an overview of financial reporting, discussing its purposes, objectives, and the preparation of financial statements such as the Profit and Loss (P&L), Balance Sheet (B/S), and Statement of Changes in Equity for Rita Plc. It also explores the advantages of International Financial Reporting Standards (IFRS) and factors influencing IFRS compliance. Furthermore, the report analyzes the financial performance of GlaxoSmithKline (GSK) using financial ratios, comparing IAS and IFRS, and examining the impact of financial reporting on various stakeholders, including employees, managers, customers, shareholders, and the government. The report emphasizes the importance of financial reporting in assessing a company's financial position and making informed decisions.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Procedure of preparing financial statements with the help of different transactions of an

organisation and present to these in front of different stakeholders is known as financial

reporting. The present report shows about different stakeholders of an enterprise who uses

financial statements for taking profitable decisions. Apart from this, purposes as well as

objectives of the financial reporting are addressed in the current assignment. The study reflects

on procedure of preparing P&L, B/S as well as statement of changes in equity for the firm Rita

Plc for the year ended 31st December 2016 using trial balance. Further, advantages of the

International Financial Reporting Standard (IFRS) are described in present project. At the end of

project, those elements are introduced which create impact on compliance with IFRS.

1.

Financial reporting is supportive for the company in order to present publish final

accounts of it in front of various stakeholders. It is highly supportive for the management in

order to assess financial position and stakeholders as well. Further, its primary and important

purposes are stated as follows:

Key objectove of it is to give highly proper data regarding to various financials to the

owner of the firm. On the basis of this, he or she easily able to know that it performs up

to which extent in the industry (Costello, 2011). Therefore, fruitful decisions which are

required to take in the workplace can be easily made.

In order to keep all the financial statements of an entity legal, the financial reporting is an

important tool.

For reducing issues like scandals, malpractices etc. in the final accounts also it is used by

the businesses.

At the time of framing the financial reports in proper direction, various complexities and

issues incurred which are resolved with the help of financial reporting.

With reference to shareholders, the financial reporting provides an outline of profitability,

liquidity and cash position of business to them. Further, profitable decisions for making

investment in the business are taken by shareholders in an appropriate way (Nobes,

2014).

1

Procedure of preparing financial statements with the help of different transactions of an

organisation and present to these in front of different stakeholders is known as financial

reporting. The present report shows about different stakeholders of an enterprise who uses

financial statements for taking profitable decisions. Apart from this, purposes as well as

objectives of the financial reporting are addressed in the current assignment. The study reflects

on procedure of preparing P&L, B/S as well as statement of changes in equity for the firm Rita

Plc for the year ended 31st December 2016 using trial balance. Further, advantages of the

International Financial Reporting Standard (IFRS) are described in present project. At the end of

project, those elements are introduced which create impact on compliance with IFRS.

1.

Financial reporting is supportive for the company in order to present publish final

accounts of it in front of various stakeholders. It is highly supportive for the management in

order to assess financial position and stakeholders as well. Further, its primary and important

purposes are stated as follows:

Key objectove of it is to give highly proper data regarding to various financials to the

owner of the firm. On the basis of this, he or she easily able to know that it performs up

to which extent in the industry (Costello, 2011). Therefore, fruitful decisions which are

required to take in the workplace can be easily made.

In order to keep all the financial statements of an entity legal, the financial reporting is an

important tool.

For reducing issues like scandals, malpractices etc. in the final accounts also it is used by

the businesses.

At the time of framing the financial reports in proper direction, various complexities and

issues incurred which are resolved with the help of financial reporting.

With reference to shareholders, the financial reporting provides an outline of profitability,

liquidity and cash position of business to them. Further, profitable decisions for making

investment in the business are taken by shareholders in an appropriate way (Nobes,

2014).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.

The conceptual and regulatory framework of financial reporting is highly used by the

businesses due to helping in order to prepare effectual final reports. With the help of such

framework the management can easily examine its position in the industry in context to the

financials. Moreover, these are needed for making all the financial statements and publish them

in legal manner. In order to reflect actual performance of the company in front of all the people

who are directly or indirectly associated with it, the financial reporting is required for

management. It has some basic principles which are used by firms at the time of preparing and

reporting various financials, listed below:

Revenue

Expense

Matching

Cost

Consistency

Objectivity

Continuity

Going concern

Unit-of-measure assumption

Separate entity assumption

The qualitative characteristics are highly supportive for the firm in order to make various

reports regarding to financials reliable. The reason is that, it states clear and proper outline of the

overall business which are actually incurred with the firm. Under the quantitative, some

assumptions and estimations are made like budgets etc. which sometimes create

misunderstanding among stakeholders (Li, 2010). Hence, it can be said that qualitative kind of

information create reliable data of the firm in front of various stakeholders.

2

The conceptual and regulatory framework of financial reporting is highly used by the

businesses due to helping in order to prepare effectual final reports. With the help of such

framework the management can easily examine its position in the industry in context to the

financials. Moreover, these are needed for making all the financial statements and publish them

in legal manner. In order to reflect actual performance of the company in front of all the people

who are directly or indirectly associated with it, the financial reporting is required for

management. It has some basic principles which are used by firms at the time of preparing and

reporting various financials, listed below:

Revenue

Expense

Matching

Cost

Consistency

Objectivity

Continuity

Going concern

Unit-of-measure assumption

Separate entity assumption

The qualitative characteristics are highly supportive for the firm in order to make various

reports regarding to financials reliable. The reason is that, it states clear and proper outline of the

overall business which are actually incurred with the firm. Under the quantitative, some

assumptions and estimations are made like budgets etc. which sometimes create

misunderstanding among stakeholders (Li, 2010). Hence, it can be said that qualitative kind of

information create reliable data of the firm in front of various stakeholders.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.

Financials of an enterprise are mostly used by the stakeholders whether they are internal

or external. The reason is that, it helps to make an effective as well as fruitful decisions towards

the businesses and gain proper and high level of returns. Further, ways through which different

stakeholders are beneficial from various financial information of the firm are stated below:

Employees: These are one of the major stakeholders for the firm due to converting the

raw materials into finished goods and deliver these up to the customers. These are mainly

concern towards the firm that it will provide a satisfactory salary along with some

allowances and bonuses. Further, under the financial data, if level of profitability is of the

high level then they will analyse that company will give better salary and other

allowances in expected manner (Epstein and Jermakowicz, 2010).

Managers: Managers of each department use the financial information in order to

determine level of profitability and liquidity. From this, they found that, business is up to

which extent able to provide salary and other bonuses or allowances in proper way. Apart

from this, if any financial plan or strategies are required to frame and employ then also

such information used.

Customers: These are always concerned for higher quality of products at lower costs.

From the financial statements, if they found that firm generates higher profit then will

expect very lower cost of goods and services. Further, they expect some additional

discounts and schemes as well.

Shareholders: Financial information used by shareholders in order to know firm's

capability in order to provide dividend or additional discounts on the shares purchased

(Barth and Landsman, 2010). Further, by considering financial statements these kinds of

stakeholders make investment decisions.

Government: This is also a major external stakeholder of the company which looks

towards the financial reports for assessing tax payable capability of an organisation.

When enterprise generates higher profit then it will impose more tax rate along with insist

for making huge contribution in the social welfare activities.

3

Financials of an enterprise are mostly used by the stakeholders whether they are internal

or external. The reason is that, it helps to make an effective as well as fruitful decisions towards

the businesses and gain proper and high level of returns. Further, ways through which different

stakeholders are beneficial from various financial information of the firm are stated below:

Employees: These are one of the major stakeholders for the firm due to converting the

raw materials into finished goods and deliver these up to the customers. These are mainly

concern towards the firm that it will provide a satisfactory salary along with some

allowances and bonuses. Further, under the financial data, if level of profitability is of the

high level then they will analyse that company will give better salary and other

allowances in expected manner (Epstein and Jermakowicz, 2010).

Managers: Managers of each department use the financial information in order to

determine level of profitability and liquidity. From this, they found that, business is up to

which extent able to provide salary and other bonuses or allowances in proper way. Apart

from this, if any financial plan or strategies are required to frame and employ then also

such information used.

Customers: These are always concerned for higher quality of products at lower costs.

From the financial statements, if they found that firm generates higher profit then will

expect very lower cost of goods and services. Further, they expect some additional

discounts and schemes as well.

Shareholders: Financial information used by shareholders in order to know firm's

capability in order to provide dividend or additional discounts on the shares purchased

(Barth and Landsman, 2010). Further, by considering financial statements these kinds of

stakeholders make investment decisions.

Government: This is also a major external stakeholder of the company which looks

towards the financial reports for assessing tax payable capability of an organisation.

When enterprise generates higher profit then it will impose more tax rate along with insist

for making huge contribution in the social welfare activities.

3

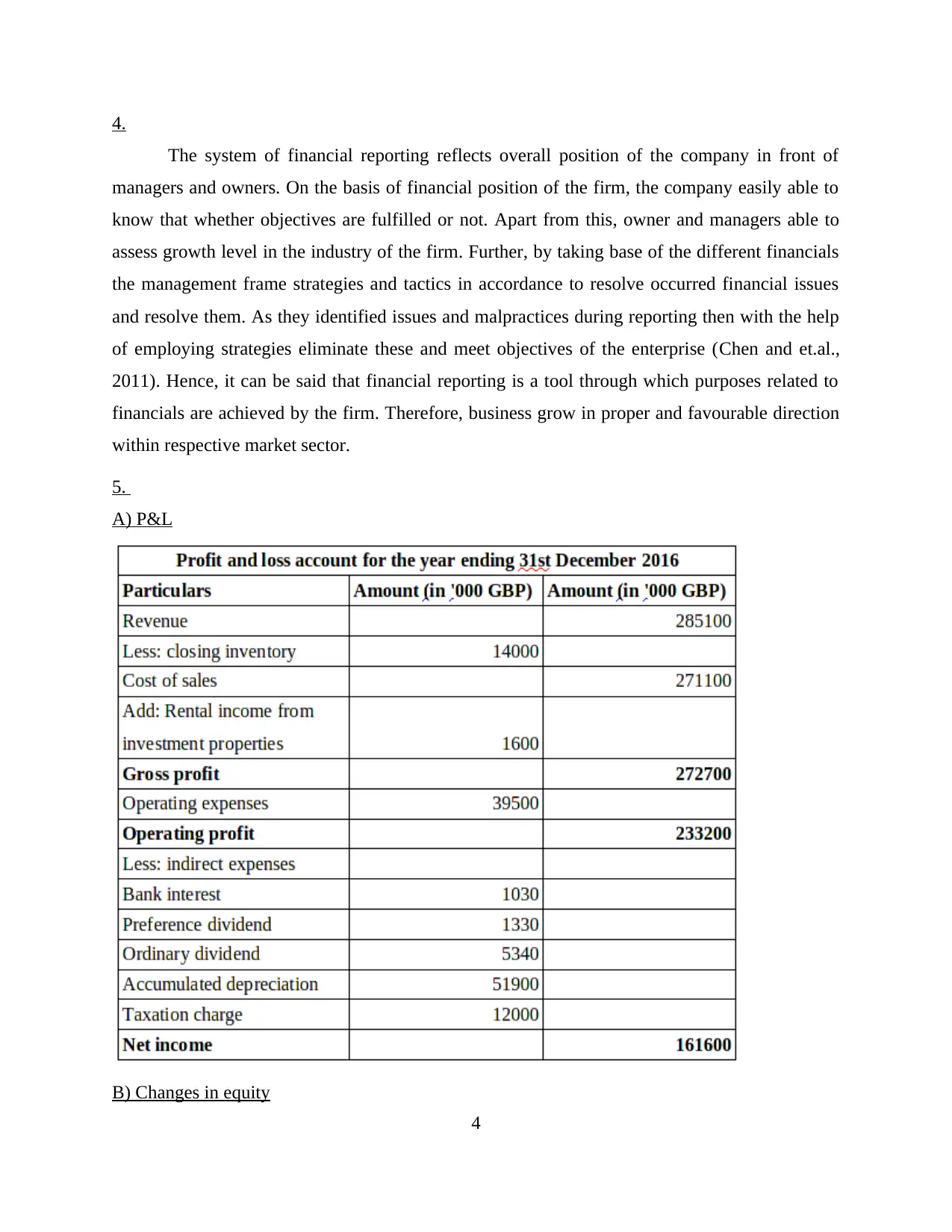

4.

The system of financial reporting reflects overall position of the company in front of

managers and owners. On the basis of financial position of the firm, the company easily able to

know that whether objectives are fulfilled or not. Apart from this, owner and managers able to

assess growth level in the industry of the firm. Further, by taking base of the different financials

the management frame strategies and tactics in accordance to resolve occurred financial issues

and resolve them. As they identified issues and malpractices during reporting then with the help

of employing strategies eliminate these and meet objectives of the enterprise (Chen and et.al.,

2011). Hence, it can be said that financial reporting is a tool through which purposes related to

financials are achieved by the firm. Therefore, business grow in proper and favourable direction

within respective market sector.

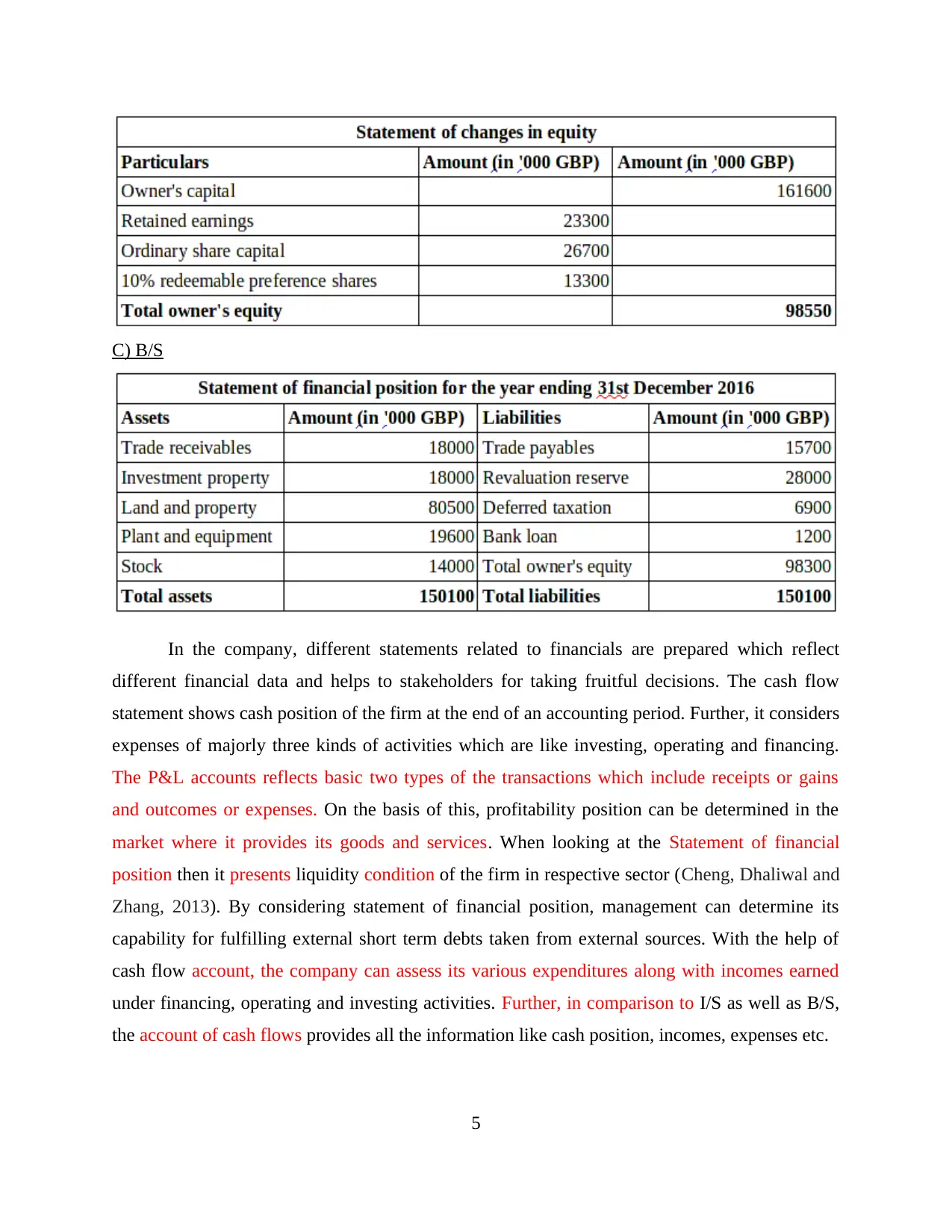

5.

A) P&L

B) Changes in equity

4

The system of financial reporting reflects overall position of the company in front of

managers and owners. On the basis of financial position of the firm, the company easily able to

know that whether objectives are fulfilled or not. Apart from this, owner and managers able to

assess growth level in the industry of the firm. Further, by taking base of the different financials

the management frame strategies and tactics in accordance to resolve occurred financial issues

and resolve them. As they identified issues and malpractices during reporting then with the help

of employing strategies eliminate these and meet objectives of the enterprise (Chen and et.al.,

2011). Hence, it can be said that financial reporting is a tool through which purposes related to

financials are achieved by the firm. Therefore, business grow in proper and favourable direction

within respective market sector.

5.

A) P&L

B) Changes in equity

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

C) B/S

In the company, different statements related to financials are prepared which reflect

different financial data and helps to stakeholders for taking fruitful decisions. The cash flow

statement shows cash position of the firm at the end of an accounting period. Further, it considers

expenses of majorly three kinds of activities which are like investing, operating and financing.

The P&L accounts reflects basic two types of the transactions which include receipts or gains

and outcomes or expenses. On the basis of this, profitability position can be determined in the

market where it provides its goods and services. When looking at the Statement of financial

position then it presents liquidity condition of the firm in respective sector (Cheng, Dhaliwal and

Zhang, 2013). By considering statement of financial position, management can determine its

capability for fulfilling external short term debts taken from external sources. With the help of

cash flow account, the company can assess its various expenditures along with incomes earned

under financing, operating and investing activities. Further, in comparison to I/S as well as B/S,

the account of cash flows provides all the information like cash position, incomes, expenses etc.

5

In the company, different statements related to financials are prepared which reflect

different financial data and helps to stakeholders for taking fruitful decisions. The cash flow

statement shows cash position of the firm at the end of an accounting period. Further, it considers

expenses of majorly three kinds of activities which are like investing, operating and financing.

The P&L accounts reflects basic two types of the transactions which include receipts or gains

and outcomes or expenses. On the basis of this, profitability position can be determined in the

market where it provides its goods and services. When looking at the Statement of financial

position then it presents liquidity condition of the firm in respective sector (Cheng, Dhaliwal and

Zhang, 2013). By considering statement of financial position, management can determine its

capability for fulfilling external short term debts taken from external sources. With the help of

cash flow account, the company can assess its various expenditures along with incomes earned

under financing, operating and investing activities. Further, in comparison to I/S as well as B/S,

the account of cash flows provides all the information like cash position, incomes, expenses etc.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

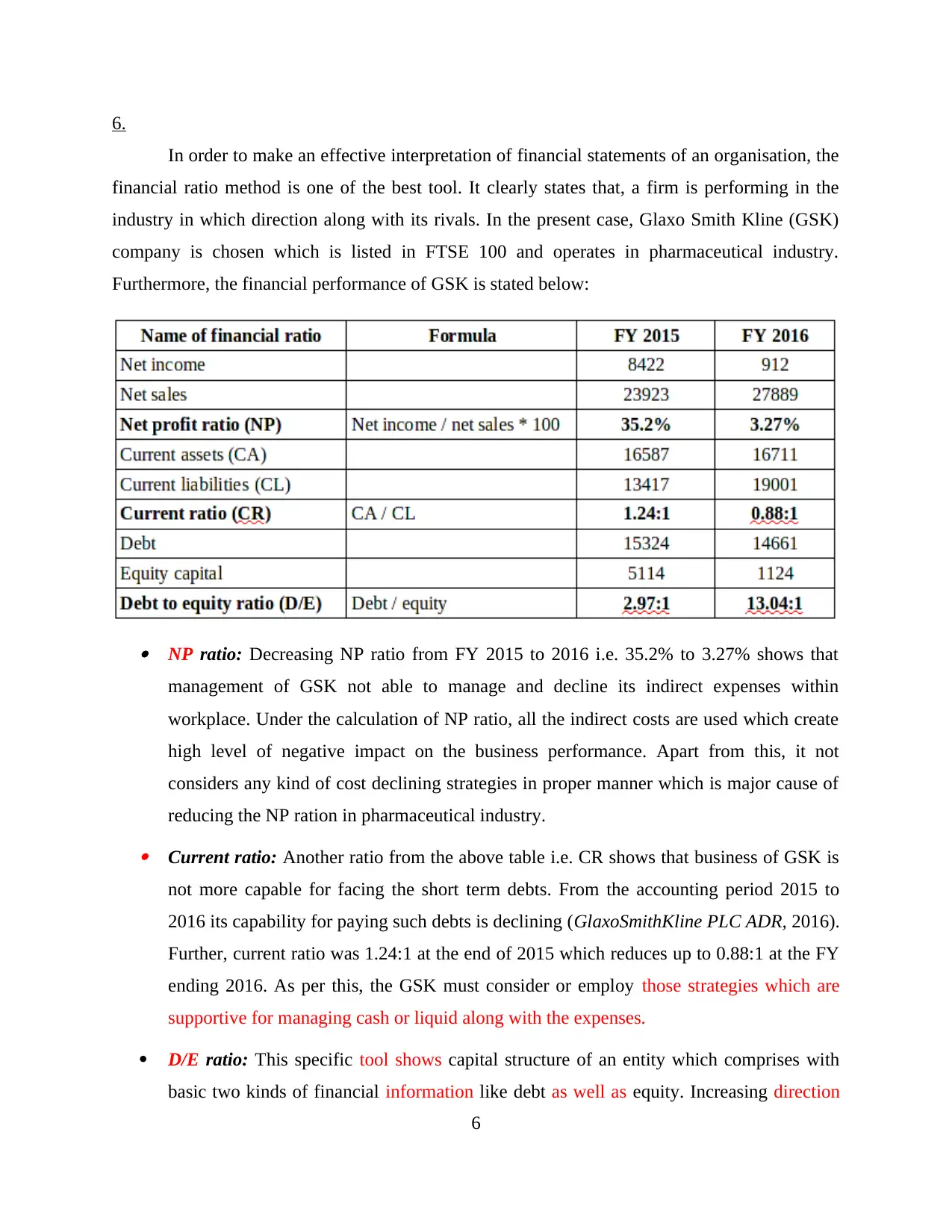

6.

In order to make an effective interpretation of financial statements of an organisation, the

financial ratio method is one of the best tool. It clearly states that, a firm is performing in the

industry in which direction along with its rivals. In the present case, Glaxo Smith Kline (GSK)

company is chosen which is listed in FTSE 100 and operates in pharmaceutical industry.

Furthermore, the financial performance of GSK is stated below:

NP ratio: Decreasing NP ratio from FY 2015 to 2016 i.e. 35.2% to 3.27% shows that

management of GSK not able to manage and decline its indirect expenses within

workplace. Under the calculation of NP ratio, all the indirect costs are used which create

high level of negative impact on the business performance. Apart from this, it not

considers any kind of cost declining strategies in proper manner which is major cause of

reducing the NP ration in pharmaceutical industry. Current ratio: Another ratio from the above table i.e. CR shows that business of GSK is

not more capable for facing the short term debts. From the accounting period 2015 to

2016 its capability for paying such debts is declining (GlaxoSmithKline PLC ADR, 2016).

Further, current ratio was 1.24:1 at the end of 2015 which reduces up to 0.88:1 at the FY

ending 2016. As per this, the GSK must consider or employ those strategies which are

supportive for managing cash or liquid along with the expenses.

D/E ratio: This specific tool shows capital structure of an entity which comprises with

basic two kinds of financial information like debt as well as equity. Increasing direction

6

In order to make an effective interpretation of financial statements of an organisation, the

financial ratio method is one of the best tool. It clearly states that, a firm is performing in the

industry in which direction along with its rivals. In the present case, Glaxo Smith Kline (GSK)

company is chosen which is listed in FTSE 100 and operates in pharmaceutical industry.

Furthermore, the financial performance of GSK is stated below:

NP ratio: Decreasing NP ratio from FY 2015 to 2016 i.e. 35.2% to 3.27% shows that

management of GSK not able to manage and decline its indirect expenses within

workplace. Under the calculation of NP ratio, all the indirect costs are used which create

high level of negative impact on the business performance. Apart from this, it not

considers any kind of cost declining strategies in proper manner which is major cause of

reducing the NP ration in pharmaceutical industry. Current ratio: Another ratio from the above table i.e. CR shows that business of GSK is

not more capable for facing the short term debts. From the accounting period 2015 to

2016 its capability for paying such debts is declining (GlaxoSmithKline PLC ADR, 2016).

Further, current ratio was 1.24:1 at the end of 2015 which reduces up to 0.88:1 at the FY

ending 2016. As per this, the GSK must consider or employ those strategies which are

supportive for managing cash or liquid along with the expenses.

D/E ratio: This specific tool shows capital structure of an entity which comprises with

basic two kinds of financial information like debt as well as equity. Increasing direction

6

of D/E ratio i.e. from 2.97:1 to 13.04:1 shows that, it has more debt or loan amount as

compared to equity capital. In comparison to standard D/E i.e. 0.5:1, business

performance of GSK is poor up to the larger level.

When considering to the overall ratios then it can be interpreted that, financial

performance of GSK within pharmaceutical industry is poor at the FY ending 2016 in

comparison to fiscal period 2015.

7.

IAS stands for the International Accounting Standards while IFRS reflects to the

International Financial Reporting Standards in context to the financials.

Those rules and standards which are published between the FY 1973 to 2001 are included

under IAS whereas standards published later to 2001 are part of IFRS which are presently

considered by majority of the firms.

Issuing and regulatory body of IAS is IASC while IFRS issues or published in the

accounting term by IASB. Further, IFRS is updated or advanced version of IAS (Horton,

Serafeim and Serafeim, 2013).

Those principles, rules as well as standards involved in IAS are not a portion of IFRS.

Therefore, both the terms have different principles and rules in their nature.

Besides these all, IAS has total 41 standards while IFRS consists with only 9 standards.

8.

International Financial Reporting Standard (IFRS) is a concept which helps to the

multinational companies in order to frame different financial statements in proper direction.

When a firm adopts this particular aspect then become advantageous in different ways which are

stated below:

Global comparability: When an organisation wants to compare its financial

performance or any other aspect in relation to financials then IFRS is helpful tool. The

reason is that, financial statements framed under this, are at the proper and international

level. On the other side, if it not prepares final accounts by considering IFRS then cannot

make comparison with those firms who have presence at international level (Shete,

2014).

7

compared to equity capital. In comparison to standard D/E i.e. 0.5:1, business

performance of GSK is poor up to the larger level.

When considering to the overall ratios then it can be interpreted that, financial

performance of GSK within pharmaceutical industry is poor at the FY ending 2016 in

comparison to fiscal period 2015.

7.

IAS stands for the International Accounting Standards while IFRS reflects to the

International Financial Reporting Standards in context to the financials.

Those rules and standards which are published between the FY 1973 to 2001 are included

under IAS whereas standards published later to 2001 are part of IFRS which are presently

considered by majority of the firms.

Issuing and regulatory body of IAS is IASC while IFRS issues or published in the

accounting term by IASB. Further, IFRS is updated or advanced version of IAS (Horton,

Serafeim and Serafeim, 2013).

Those principles, rules as well as standards involved in IAS are not a portion of IFRS.

Therefore, both the terms have different principles and rules in their nature.

Besides these all, IAS has total 41 standards while IFRS consists with only 9 standards.

8.

International Financial Reporting Standard (IFRS) is a concept which helps to the

multinational companies in order to frame different financial statements in proper direction.

When a firm adopts this particular aspect then become advantageous in different ways which are

stated below:

Global comparability: When an organisation wants to compare its financial

performance or any other aspect in relation to financials then IFRS is helpful tool. The

reason is that, financial statements framed under this, are at the proper and international

level. On the other side, if it not prepares final accounts by considering IFRS then cannot

make comparison with those firms who have presence at international level (Shete,

2014).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reduce recognition timeliness: In order to recognise any kind of financial statement and

publish as well by following all the laws, huge time was considered by the firms. As the

accountants consider various principles and standards of IFRS for preparing final

accounts of the firm then time-frame for acknowledgement is declined up to the greater

level.

Better access to foreign capital markets: IFRS helps to frame the final accounts of a

firm at international level which leads to create high level of access to enter in the capital

markets of another countries. Furthermore, it creates better level of understanding for the

investors who invest sum of money in the company. Apart from this, when the

management wants to make chances for generating adequate level of accession in foreign

capital market IFRS is supportive (6 Advantages and Disadvantages of Adopting IFRS,

2015).

Understandability: Besides these, in order to make proper understanding about the

financial statements of a company for several stakeholders the IFRS is helpful. Along

with this, stakeholders of the firm easily able to make an effective and fruitful decisions

towards the business.

Enhance transparency of financial reporting: The IFRS is supportive in order to boost

up transparency as well as accuracy of the financial reporting system. Moreover, in order

to use process of the auditing the IFRS is an effectual along with profitable tool where

malpractice is easily detected.

9.

When the company is going to consider the principles, theories and standards of IFRS

within workplace then necessary to follow regulations and compliances of it. Due to lack of

using various compliances associated with IFRS the firm cannot frame final accounts in proper

direction. Those factors which create impact on compliance with IFRS are stated below:

Company size is one of the major factor which affect to the compliance involved with

IFRS in the firm. The reason is that, there is very high level of disclosure compliance are

there incurred with IFRS. Apart from this, size of the company is involved in the business

in positive direction (Christensen, Hail and Leuz, 2013).

8

publish as well by following all the laws, huge time was considered by the firms. As the

accountants consider various principles and standards of IFRS for preparing final

accounts of the firm then time-frame for acknowledgement is declined up to the greater

level.

Better access to foreign capital markets: IFRS helps to frame the final accounts of a

firm at international level which leads to create high level of access to enter in the capital

markets of another countries. Furthermore, it creates better level of understanding for the

investors who invest sum of money in the company. Apart from this, when the

management wants to make chances for generating adequate level of accession in foreign

capital market IFRS is supportive (6 Advantages and Disadvantages of Adopting IFRS,

2015).

Understandability: Besides these, in order to make proper understanding about the

financial statements of a company for several stakeholders the IFRS is helpful. Along

with this, stakeholders of the firm easily able to make an effective and fruitful decisions

towards the business.

Enhance transparency of financial reporting: The IFRS is supportive in order to boost

up transparency as well as accuracy of the financial reporting system. Moreover, in order

to use process of the auditing the IFRS is an effectual along with profitable tool where

malpractice is easily detected.

9.

When the company is going to consider the principles, theories and standards of IFRS

within workplace then necessary to follow regulations and compliances of it. Due to lack of

using various compliances associated with IFRS the firm cannot frame final accounts in proper

direction. Those factors which create impact on compliance with IFRS are stated below:

Company size is one of the major factor which affect to the compliance involved with

IFRS in the firm. The reason is that, there is very high level of disclosure compliance are

there incurred with IFRS. Apart from this, size of the company is involved in the business

in positive direction (Christensen, Hail and Leuz, 2013).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Leverage is another aspect which is involved within an entity in a positive manner and

highly affect to compliance with the International Financial Reporting Standard. Higher

the value of leverage is when incurred in the workplace then it is clear indication of few

and little equity capital availability.

Liquidity is identified in the firm for assessing financial position in the industry which

should be of the higher proportion in the company. The basic reason behind this is that,

due to lack of adequate availability of this tool the firm unable to apply all the required

compliance with IFRS while framing final accounts. Moreover, there is positive relation

among these both the factors i.e. compliance with IFRS and liquidity.

Apart from the above aspects, age of company, ownership structure, profitability

condition, national or international presence etc. factors are also having high level of

impact on this mentioned aspect (Brochet, Jagolinzer and Riedl, 2013).

CONCLUSION

From the above report it can be summarised that, financial reporting is a supportive tool

in order to make profitable decisions for business as well as stakeholders properly. There are

various people like customers, managers, owner, shareholders, government, employees etc. Use

financial statements in different manners. It can be assessed from the financial performance that,

Glaxo Smith Kline performs negative or poor in the pharmaceutical industry at the end of 2016

in comparison to 2015. Apart from these all, the IFRS differs from IAS and has wide benefits for

the company when it uses IFRS in the firm. Besides these, there are some elements like company

size and age, structure of ownership, leverage, liquidity, probability etc. create impact on

compliance with IFRS.

9

highly affect to compliance with the International Financial Reporting Standard. Higher

the value of leverage is when incurred in the workplace then it is clear indication of few

and little equity capital availability.

Liquidity is identified in the firm for assessing financial position in the industry which

should be of the higher proportion in the company. The basic reason behind this is that,

due to lack of adequate availability of this tool the firm unable to apply all the required

compliance with IFRS while framing final accounts. Moreover, there is positive relation

among these both the factors i.e. compliance with IFRS and liquidity.

Apart from the above aspects, age of company, ownership structure, profitability

condition, national or international presence etc. factors are also having high level of

impact on this mentioned aspect (Brochet, Jagolinzer and Riedl, 2013).

CONCLUSION

From the above report it can be summarised that, financial reporting is a supportive tool

in order to make profitable decisions for business as well as stakeholders properly. There are

various people like customers, managers, owner, shareholders, government, employees etc. Use

financial statements in different manners. It can be assessed from the financial performance that,

Glaxo Smith Kline performs negative or poor in the pharmaceutical industry at the end of 2016

in comparison to 2015. Apart from these all, the IFRS differs from IAS and has wide benefits for

the company when it uses IFRS in the firm. Besides these, there are some elements like company

size and age, structure of ownership, leverage, liquidity, probability etc. create impact on

compliance with IFRS.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.