Cost and Revenues Report - Financial Analysis & Reporting - Semester 1

VerifiedAdded on 2020/10/22

|19

|3512

|437

Report

AI Summary

This report comprehensively examines cost and revenue management within an organization. It begins by outlining the importance of internal reporting, the relationship between various costing systems (job and process), and the roles of responsibility centers (cost, profit, and investment centers). The report then delves into cost classification, differentiating between fixed and variable costs, departmental and customer costs, and comparing marginal and absorption costing methods. Task 2 focuses on recording and analyzing cost information related to materials, labor, and expenses, including the stages of inventory and valuation techniques (FIFO, LIFO, weighted average). Task 3 addresses overhead costs, covering absorption rates, adjustments for over/under recovered overhead, and methods of allocation and apportionment. Task 4 compares actual and budgeted costs, analyzing variances for management reports. Finally, Task 5 explores cost estimation, the impact of changing activity levels on unit costs, and factors influencing short-term and long-term decision-making. The report concludes with a discussion on the key takeaways and implications of the analysis.

Cost and Revenues

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

I.1 Purpose of internal reporting and providing accurate information to management...............4

1.2 Relationship between various costing system........................................................................4

1.3 responsibility centers, cost centers, profit centers and investment centers within an

organization..................................................................................................................................4

1.4 Characteristics of different types of cost classification.........................................................5

1.5 Difference between marginal and absorption costing............................................................6

TASK 2............................................................................................................................................6

2.1 Record cost information for material, labor and expenses in accordance with the

Organization’s costing procedures...............................................................................................6

2.2 Analysis of cost information..................................................................................................6

2.3 Various stages of inventory...................................................................................................7

2.4 Valuation of inventory...........................................................................................................7

2.5 Behavior of various costs.....................................................................................................10

2.6 Record cost system..............................................................................................................10

TASK 3..........................................................................................................................................11

3.1 Overhead cost of production and service cost centre...........................................................11

3.2 Calculation of different types of absorption rate.................................................................11

3.3Adjustments of over or under recovered overhead ..............................................................12

3.4 Methods of absorption, allocation and apportionment........................................................13

3.5 Resolve queries related to overhead cost data ....................................................................13

TASK 4. ........................................................................................................................................14

4.1 compare actual and budget cost...........................................................................................14

4.2 Variance for the management report....................................................................................14

4.3 Information of budget holders ............................................................................................14

4.4 Management report:............................................................................................................14

TASK 5..........................................................................................................................................15

5.1 Estimates of cost and future income for decision making...................................................15

5.2 Effect on changing activity levels on unit cost....................................................................15

2

INTRODUCTION...........................................................................................................................4

I.1 Purpose of internal reporting and providing accurate information to management...............4

1.2 Relationship between various costing system........................................................................4

1.3 responsibility centers, cost centers, profit centers and investment centers within an

organization..................................................................................................................................4

1.4 Characteristics of different types of cost classification.........................................................5

1.5 Difference between marginal and absorption costing............................................................6

TASK 2............................................................................................................................................6

2.1 Record cost information for material, labor and expenses in accordance with the

Organization’s costing procedures...............................................................................................6

2.2 Analysis of cost information..................................................................................................6

2.3 Various stages of inventory...................................................................................................7

2.4 Valuation of inventory...........................................................................................................7

2.5 Behavior of various costs.....................................................................................................10

2.6 Record cost system..............................................................................................................10

TASK 3..........................................................................................................................................11

3.1 Overhead cost of production and service cost centre...........................................................11

3.2 Calculation of different types of absorption rate.................................................................11

3.3Adjustments of over or under recovered overhead ..............................................................12

3.4 Methods of absorption, allocation and apportionment........................................................13

3.5 Resolve queries related to overhead cost data ....................................................................13

TASK 4. ........................................................................................................................................14

4.1 compare actual and budget cost...........................................................................................14

4.2 Variance for the management report....................................................................................14

4.3 Information of budget holders ............................................................................................14

4.4 Management report:............................................................................................................14

TASK 5..........................................................................................................................................15

5.1 Estimates of cost and future income for decision making...................................................15

5.2 Effect on changing activity levels on unit cost....................................................................15

2

5.3 How to calculate effect of changing activity levels on unit cost .......................................15

5.4 Factors affecting short term and long term decision making ..............................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

3

5.4 Factors affecting short term and long term decision making ..............................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Cost and revenues are the concept of cost and accounts and it is essential for the company

to minimize the cost and maximize the revenues, so that it can earn maximum amount of profit.

This report covers various topics related to cost and revenue such as purpose of internal reporting

and role of costing system, stages of inventory management and methods and relation between

costing systems. Apart from this it also discuss various types of cost which are involved in

manufacturing of product.

TASK 1.

1.1 Purpose of internal reporting and providing accurate information to management

Internal reporting is very important for the management as it shows the data about how

much work has been done by the employees in a day. The reporting is helpful in the deciding and

delegating task for future accordingly (Internal reporting, 2018). The main purpose of internal

reporting is to provide valuable report to the top management so that they can take the right

decision in order to make strategic decisions. The accurate information assists management to

take better and relevant decision in favor of company. As accurate information is source for

management to make better and cost effective decision in the organization.

1.2 Relationship between various costing system

Cost is an element which is incurred by the company in order to produce a goods or

service. There are various costing system which are used by an organization in order to

manufacturing of goods and services. As job costing system is the system which is used by every

organization to ascertain the cost of each job. As there are different cost like material, labor and

overhead, so a job is assigned to each cost to know the amount of individual job’s cost. The

process costing is another system in which material, labor and overheads are combined together.

So as there is a relationship between these costing system that both costing system have same

cost component.

1.3 Responsibility centres, cost centers, profit centres and investment centres within an

organization

Responsibility Centre:

4

Cost and revenues are the concept of cost and accounts and it is essential for the company

to minimize the cost and maximize the revenues, so that it can earn maximum amount of profit.

This report covers various topics related to cost and revenue such as purpose of internal reporting

and role of costing system, stages of inventory management and methods and relation between

costing systems. Apart from this it also discuss various types of cost which are involved in

manufacturing of product.

TASK 1.

1.1 Purpose of internal reporting and providing accurate information to management

Internal reporting is very important for the management as it shows the data about how

much work has been done by the employees in a day. The reporting is helpful in the deciding and

delegating task for future accordingly (Internal reporting, 2018). The main purpose of internal

reporting is to provide valuable report to the top management so that they can take the right

decision in order to make strategic decisions. The accurate information assists management to

take better and relevant decision in favor of company. As accurate information is source for

management to make better and cost effective decision in the organization.

1.2 Relationship between various costing system

Cost is an element which is incurred by the company in order to produce a goods or

service. There are various costing system which are used by an organization in order to

manufacturing of goods and services. As job costing system is the system which is used by every

organization to ascertain the cost of each job. As there are different cost like material, labor and

overhead, so a job is assigned to each cost to know the amount of individual job’s cost. The

process costing is another system in which material, labor and overheads are combined together.

So as there is a relationship between these costing system that both costing system have same

cost component.

1.3 Responsibility centres, cost centers, profit centres and investment centres within an

organization

Responsibility Centre:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Responsibility centre is basically a division in an organization. The large organization

divided its business into smaller groups for smooth functioning of businesses. The manager of

organization is liable for the managing the sub units of organization.

Cost Centre

The cost is incurred for managing the operation of organization. The managers have duty

to incur and control the cost.

Profit Centre

Profit centre is also managed by the managers so they are responsible for revenue

generation and expense incurred in the sub unit of organization.

Investment Centre

The sub unit also require some amount of investment so the manager of organization

decide how much amount of capital investment will be required by sub unit of organizations.

1.4 Characteristics of different types of cost classification.

The cost classification includes the segregation of a group of expenses. It is helpful for

management to bring attention to certain costs that are important than others. The different types

of cost classification are as follows:

Fixed and Variable Cost:

The costs are segregated in fixed and variable cost. Then variable cost deducted from

sales to get contribution margin. (Awudu and Zhang, 2013).

Departmental Cost:

As expense are assigned to the different departments and then this information is used on

trend line to determine ability of department manager to control assigned cost (DRURY, 2013).

Customer Cost:

Expenses are classified by individual customer like cost of warranties, returns and

customer service. This information is useful to ascertain individual customer profitability.

5

divided its business into smaller groups for smooth functioning of businesses. The manager of

organization is liable for the managing the sub units of organization.

Cost Centre

The cost is incurred for managing the operation of organization. The managers have duty

to incur and control the cost.

Profit Centre

Profit centre is also managed by the managers so they are responsible for revenue

generation and expense incurred in the sub unit of organization.

Investment Centre

The sub unit also require some amount of investment so the manager of organization

decide how much amount of capital investment will be required by sub unit of organizations.

1.4 Characteristics of different types of cost classification.

The cost classification includes the segregation of a group of expenses. It is helpful for

management to bring attention to certain costs that are important than others. The different types

of cost classification are as follows:

Fixed and Variable Cost:

The costs are segregated in fixed and variable cost. Then variable cost deducted from

sales to get contribution margin. (Awudu and Zhang, 2013).

Departmental Cost:

As expense are assigned to the different departments and then this information is used on

trend line to determine ability of department manager to control assigned cost (DRURY, 2013).

Customer Cost:

Expenses are classified by individual customer like cost of warranties, returns and

customer service. This information is useful to ascertain individual customer profitability.

5

1.5 Difference between marginal and absorption costing

In Marginal costing variable costs are charged to cost units and fixed expenditures

imputable to the relevant period is written off.

Absorption Costing refers to all production cost which are absorbed by the units produced.

The difference is discussed as below:

Cost Application:

As only variable cost is applied to inventory under marginal cost while under absorption

costing the fixed overheads are also applied.

Profitability:

The profitability of each individual sell will be appear higher in marginal costing while in

absorption costing it will be appear lower (Färe and Grosskopf, 2012).

Measurement:

The measurement of profits under marginal costing use the contribution margin while

under absorption costing the gross margin is used which includes overhead.

TASK 2

2.1 Record cost information for material, labor and expenses in accordance with the

Organization’s costing procedures

Labor Expenses Material

$ 50000 55000 $150000

Direct labour cost: It is directly involves in production of goods and it is assignable to particular

product, cost centre etc.

Direct expenses: These are those expenditures which incurred and varies directly with change in

the volume of a cost object.

Direct material cost: It is the cost of raw material and components which are used to develop a

product.

6

In Marginal costing variable costs are charged to cost units and fixed expenditures

imputable to the relevant period is written off.

Absorption Costing refers to all production cost which are absorbed by the units produced.

The difference is discussed as below:

Cost Application:

As only variable cost is applied to inventory under marginal cost while under absorption

costing the fixed overheads are also applied.

Profitability:

The profitability of each individual sell will be appear higher in marginal costing while in

absorption costing it will be appear lower (Färe and Grosskopf, 2012).

Measurement:

The measurement of profits under marginal costing use the contribution margin while

under absorption costing the gross margin is used which includes overhead.

TASK 2

2.1 Record cost information for material, labor and expenses in accordance with the

Organization’s costing procedures

Labor Expenses Material

$ 50000 55000 $150000

Direct labour cost: It is directly involves in production of goods and it is assignable to particular

product, cost centre etc.

Direct expenses: These are those expenditures which incurred and varies directly with change in

the volume of a cost object.

Direct material cost: It is the cost of raw material and components which are used to develop a

product.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Analysis of cost information

The organizations have bought raw material at cost of $150000 which shows that

company is planning to produce in bulk to lower their cost of production. The labor cost which

will be incurred by company is too expensive which shows that company needs to control their

labor cost to increase their profits. As company has incurred some overheads also which

amounting 55000. So company needs to control its overhead also so they can increase their sales

and revenues as well.

2.3 Various stages of inventory

There are various stages for converting raw material inventory into finished goods. These

are as follows:

Raw Material:

This is the first stage of converting raw material inventory into finished goods. Every

finished goods is processed from raw material like to make furniture the wood will be raw

material.

Work in Progress:

This is the process after raw material processing but before completion of finished goods.

At this tage various kind of costs are incurred like labour and manufacturing cost and other costs.

Finished Goods:

This is last stage of production process where raw material input come as finished good

output.

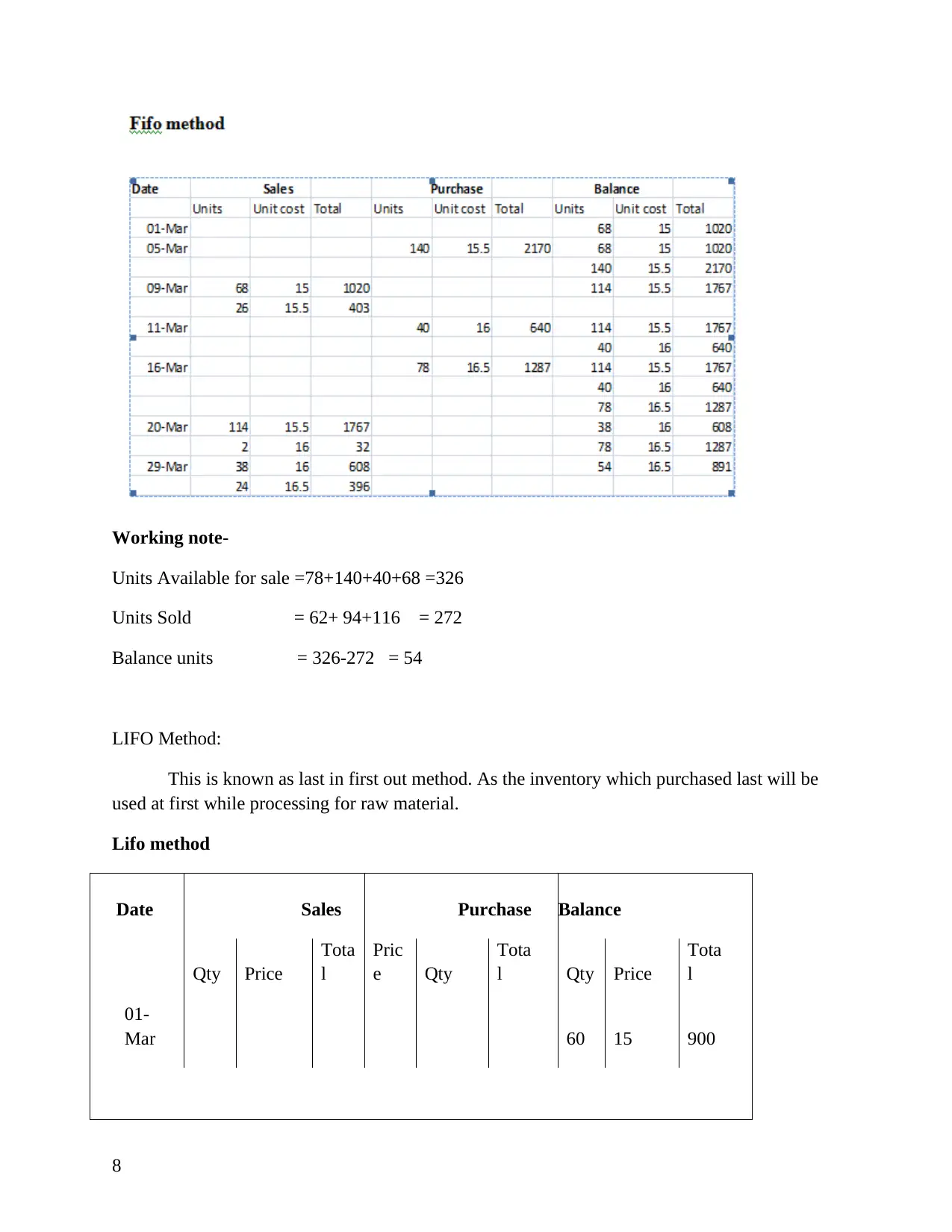

2.4 Valuation of inventory

The valuation of inventory is being done by various methods like FIFO method, LIFO

method and weighted average method.

FIFO Method

7

The organizations have bought raw material at cost of $150000 which shows that

company is planning to produce in bulk to lower their cost of production. The labor cost which

will be incurred by company is too expensive which shows that company needs to control their

labor cost to increase their profits. As company has incurred some overheads also which

amounting 55000. So company needs to control its overhead also so they can increase their sales

and revenues as well.

2.3 Various stages of inventory

There are various stages for converting raw material inventory into finished goods. These

are as follows:

Raw Material:

This is the first stage of converting raw material inventory into finished goods. Every

finished goods is processed from raw material like to make furniture the wood will be raw

material.

Work in Progress:

This is the process after raw material processing but before completion of finished goods.

At this tage various kind of costs are incurred like labour and manufacturing cost and other costs.

Finished Goods:

This is last stage of production process where raw material input come as finished good

output.

2.4 Valuation of inventory

The valuation of inventory is being done by various methods like FIFO method, LIFO

method and weighted average method.

FIFO Method

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working note-

Units Available for sale =78+140+40+68 =326

Units Sold = 62+ 94+116 = 272

Balance units = 326-272 = 54

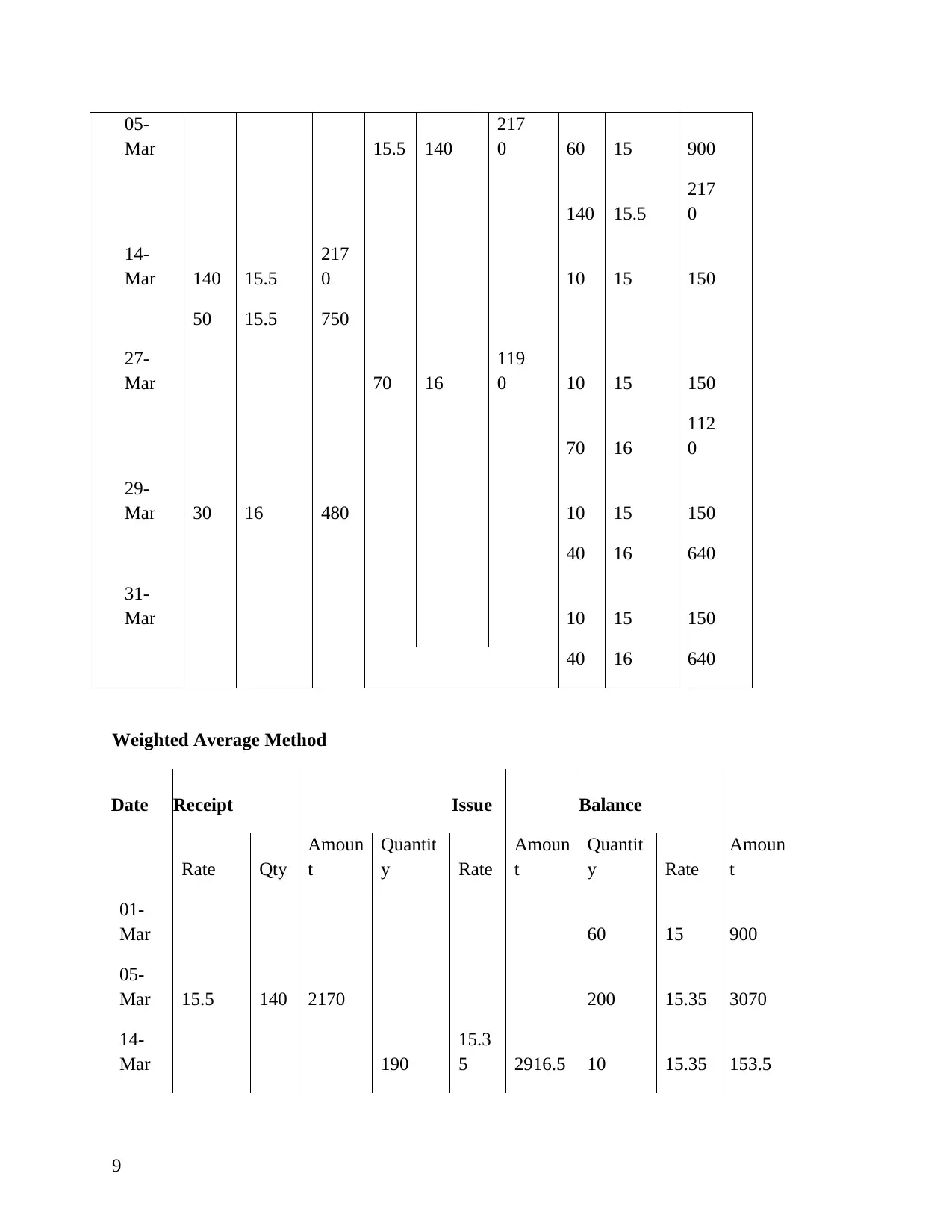

LIFO Method:

This is known as last in first out method. As the inventory which purchased last will be

used at first while processing for raw material.

Lifo method

Date Sales Purchase Balance

Qty Price

Tota

l

Pric

e Qty

Tota

l Qty Price

Tota

l

01-

Mar 60 15 900

8

Units Available for sale =78+140+40+68 =326

Units Sold = 62+ 94+116 = 272

Balance units = 326-272 = 54

LIFO Method:

This is known as last in first out method. As the inventory which purchased last will be

used at first while processing for raw material.

Lifo method

Date Sales Purchase Balance

Qty Price

Tota

l

Pric

e Qty

Tota

l Qty Price

Tota

l

01-

Mar 60 15 900

8

05-

Mar 15.5 140

217

0 60 15 900

140 15.5

217

0

14-

Mar 140 15.5

217

0 10 15 150

50 15.5 750

27-

Mar 70 16

119

0 10 15 150

70 16

112

0

29-

Mar 30 16 480 10 15 150

40 16 640

31-

Mar 10 15 150

40 16 640

Weighted Average Method

Date Receipt Issue Balance

Rate Qty

Amoun

t

Quantit

y Rate

Amoun

t

Quantit

y Rate

Amoun

t

01-

Mar 60 15 900

05-

Mar 15.5 140 2170 200 15.35 3070

14-

Mar 190

15.3

5 2916.5 10 15.35 153.5

9

Mar 15.5 140

217

0 60 15 900

140 15.5

217

0

14-

Mar 140 15.5

217

0 10 15 150

50 15.5 750

27-

Mar 70 16

119

0 10 15 150

70 16

112

0

29-

Mar 30 16 480 10 15 150

40 16 640

31-

Mar 10 15 150

40 16 640

Weighted Average Method

Date Receipt Issue Balance

Rate Qty

Amoun

t

Quantit

y Rate

Amoun

t

Quantit

y Rate

Amoun

t

01-

Mar 60 15 900

05-

Mar 15.5 140 2170 200 15.35 3070

14-

Mar 190

15.3

5 2916.5 10 15.35 153.5

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

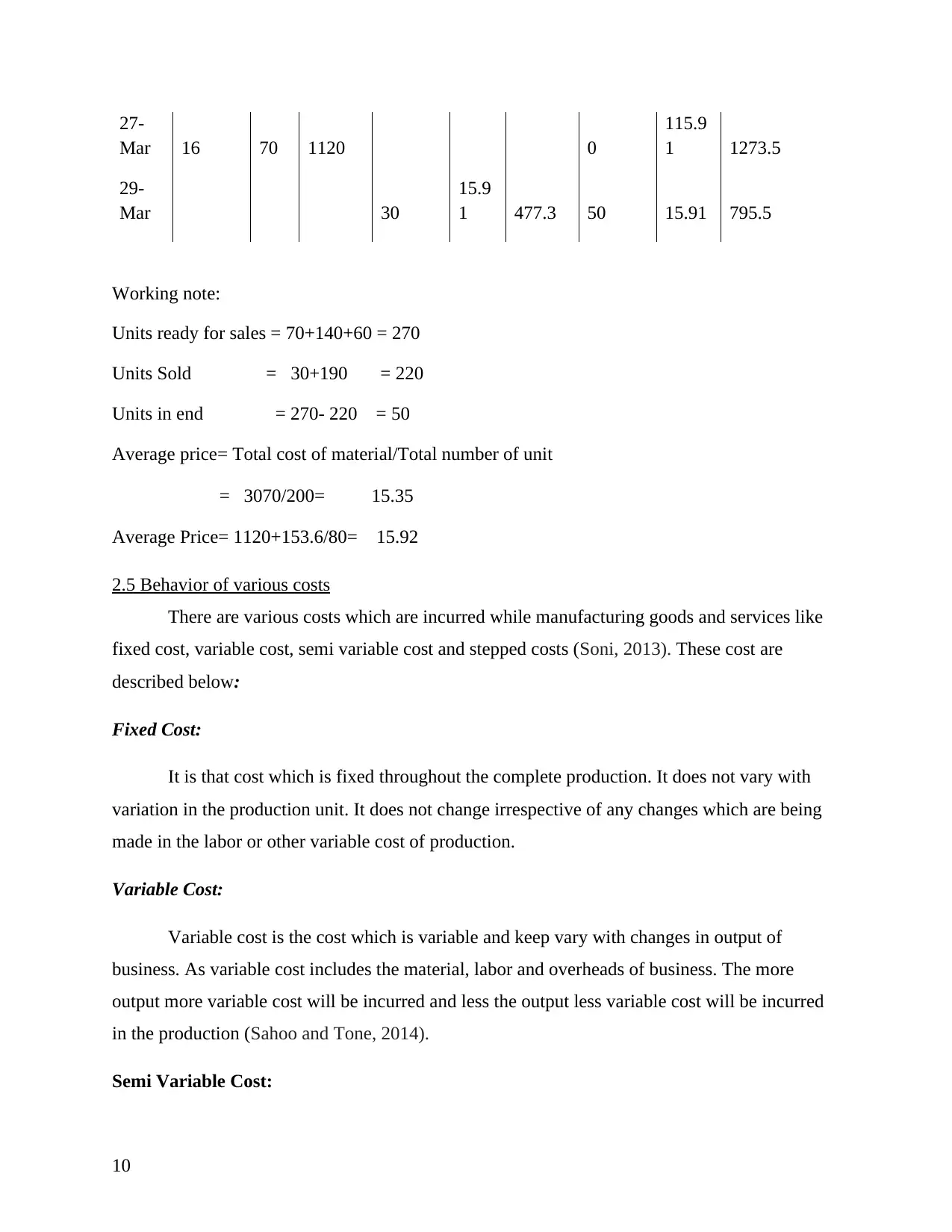

27-

Mar 16 70 1120 0

115.9

1 1273.5

29-

Mar 30

15.9

1 477.3 50 15.91 795.5

Working note:

Units ready for sales = 70+140+60 = 270

Units Sold = 30+190 = 220

Units in end = 270- 220 = 50

Average price= Total cost of material/Total number of unit

= 3070/200= 15.35

Average Price= 1120+153.6/80= 15.92

2.5 Behavior of various costs

There are various costs which are incurred while manufacturing goods and services like

fixed cost, variable cost, semi variable cost and stepped costs (Soni, 2013). These cost are

described below:

Fixed Cost:

It is that cost which is fixed throughout the complete production. It does not vary with

variation in the production unit. It does not change irrespective of any changes which are being

made in the labor or other variable cost of production.

Variable Cost:

Variable cost is the cost which is variable and keep vary with changes in output of

business. As variable cost includes the material, labor and overheads of business. The more

output more variable cost will be incurred and less the output less variable cost will be incurred

in the production (Sahoo and Tone, 2014).

Semi Variable Cost:

10

Mar 16 70 1120 0

115.9

1 1273.5

29-

Mar 30

15.9

1 477.3 50 15.91 795.5

Working note:

Units ready for sales = 70+140+60 = 270

Units Sold = 30+190 = 220

Units in end = 270- 220 = 50

Average price= Total cost of material/Total number of unit

= 3070/200= 15.35

Average Price= 1120+153.6/80= 15.92

2.5 Behavior of various costs

There are various costs which are incurred while manufacturing goods and services like

fixed cost, variable cost, semi variable cost and stepped costs (Soni, 2013). These cost are

described below:

Fixed Cost:

It is that cost which is fixed throughout the complete production. It does not vary with

variation in the production unit. It does not change irrespective of any changes which are being

made in the labor or other variable cost of production.

Variable Cost:

Variable cost is the cost which is variable and keep vary with changes in output of

business. As variable cost includes the material, labor and overheads of business. The more

output more variable cost will be incurred and less the output less variable cost will be incurred

in the production (Sahoo and Tone, 2014).

Semi Variable Cost:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is known as fixed cost also. As it includes both fixed and variable cost. Under this

cost keep fixed at certain level of production after this it becomes the variable. Like wages is

being fixed at 48 hours in a week and beyond this employee will get extra benefits.

Stepped Cost:

It is the part of total cost of an activity at various levels. It keeps constant at particular

level of production. After that it gets start increasing or decreasing.

2.6 Record cost system

There are different costing systems which are recorded. These are as follows:

Job System:

Job cost system is a system which is used by the manufacturers to give a unique job to

each cost. As there are different cost is incurred like fixed and variable etc. So an unique job is

given to each job to ascertain which job has incurred more expenditure (Sufian and Kamarudin,

2015).

Batch:

It is a type of specific order costing. It is similar to job costing. Each batch is a separately

identifiable cost unit which is given a batch number in the same way that each job is given a

number.

Unit:

This cost is incurred by the company to produce a one unit of a particular product. This

includes the all fixed costs and all variable costs which involved in production.

Process costing:

The process costing is a method for assigning cost to units of production in companies to

manufacture large quantities of homogeneous products. It is used to ascertain the cost of product

at each stage (Xu and Li, 2013).

Service:

11

cost keep fixed at certain level of production after this it becomes the variable. Like wages is

being fixed at 48 hours in a week and beyond this employee will get extra benefits.

Stepped Cost:

It is the part of total cost of an activity at various levels. It keeps constant at particular

level of production. After that it gets start increasing or decreasing.

2.6 Record cost system

There are different costing systems which are recorded. These are as follows:

Job System:

Job cost system is a system which is used by the manufacturers to give a unique job to

each cost. As there are different cost is incurred like fixed and variable etc. So an unique job is

given to each job to ascertain which job has incurred more expenditure (Sufian and Kamarudin,

2015).

Batch:

It is a type of specific order costing. It is similar to job costing. Each batch is a separately

identifiable cost unit which is given a batch number in the same way that each job is given a

number.

Unit:

This cost is incurred by the company to produce a one unit of a particular product. This

includes the all fixed costs and all variable costs which involved in production.

Process costing:

The process costing is a method for assigning cost to units of production in companies to

manufacture large quantities of homogeneous products. It is used to ascertain the cost of product

at each stage (Xu and Li, 2013).

Service:

11

It is a type of costing which is useful in business which provides and produce services

instead of goods

TASK 3

3.1 Overhead cost of production and service cost centre

For a manufacture it is important to know about various types of costs occurred in the

process of production of goods and services. It is discussed as follows:

Step down cost: In this method other operating departments of organization assign its cost with

service department. For example, Rank can be given to different of company on the basis of cost

allocation (Sako, 2012).

Direct cost: It is directly associated with the value of product. For example, Commission paid by

the organization to its suppliers.

3.2 Calculation of different types of absorption rate

Basis of cost Absorption rate of overhead Absorption based overhead

Raw material Factory OH/ Cost of material

150000/110000*100= 136.6%

OH absorption rate*material

cost of job

136.6*240 % =327

Direct labour Factory OH/ Labour cost*100

150000/90000*100 = 166.67%

Labour cost* absorption rate of

OH

200*166.7 % = 333

Prime cost Factory OH/ Prime cost

150000/200000*100 = 75%

Prime cost of job* absorption

rate

240+200*75% = 330

Units of

Production

Factory OH/ Units of output*100

150000/500*100 = 30

Units of output* absorption

rate

10*30 = 300

Direct labour basis Factort OH/ Labour rate*100

150000/30000*100 =5

Labours hours* Absorption

rate of OH

63*5 = 315

Machine hour

basis

Factory OH/machine hours*100

150000/25000*100 =6

Machine hours for job* OH

absorption rate

44*6 = 264

12

instead of goods

TASK 3

3.1 Overhead cost of production and service cost centre

For a manufacture it is important to know about various types of costs occurred in the

process of production of goods and services. It is discussed as follows:

Step down cost: In this method other operating departments of organization assign its cost with

service department. For example, Rank can be given to different of company on the basis of cost

allocation (Sako, 2012).

Direct cost: It is directly associated with the value of product. For example, Commission paid by

the organization to its suppliers.

3.2 Calculation of different types of absorption rate

Basis of cost Absorption rate of overhead Absorption based overhead

Raw material Factory OH/ Cost of material

150000/110000*100= 136.6%

OH absorption rate*material

cost of job

136.6*240 % =327

Direct labour Factory OH/ Labour cost*100

150000/90000*100 = 166.67%

Labour cost* absorption rate of

OH

200*166.7 % = 333

Prime cost Factory OH/ Prime cost

150000/200000*100 = 75%

Prime cost of job* absorption

rate

240+200*75% = 330

Units of

Production

Factory OH/ Units of output*100

150000/500*100 = 30

Units of output* absorption

rate

10*30 = 300

Direct labour basis Factort OH/ Labour rate*100

150000/30000*100 =5

Labours hours* Absorption

rate of OH

63*5 = 315

Machine hour

basis

Factory OH/machine hours*100

150000/25000*100 =6

Machine hours for job* OH

absorption rate

44*6 = 264

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.