Financial Accounting Report: Client Portfolio and Financial Analysis

VerifiedAdded on 2020/06/06

|27

|2041

|76

Report

AI Summary

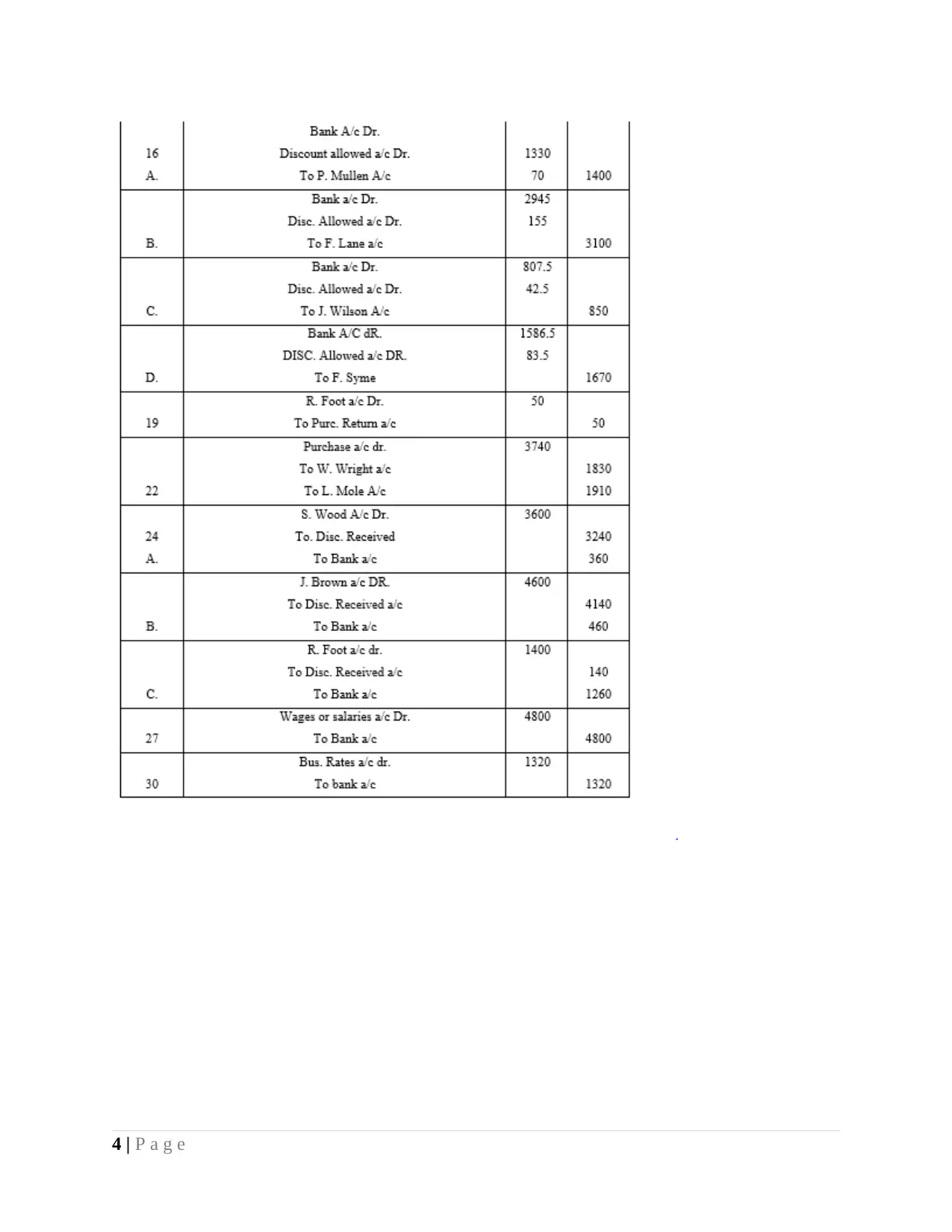

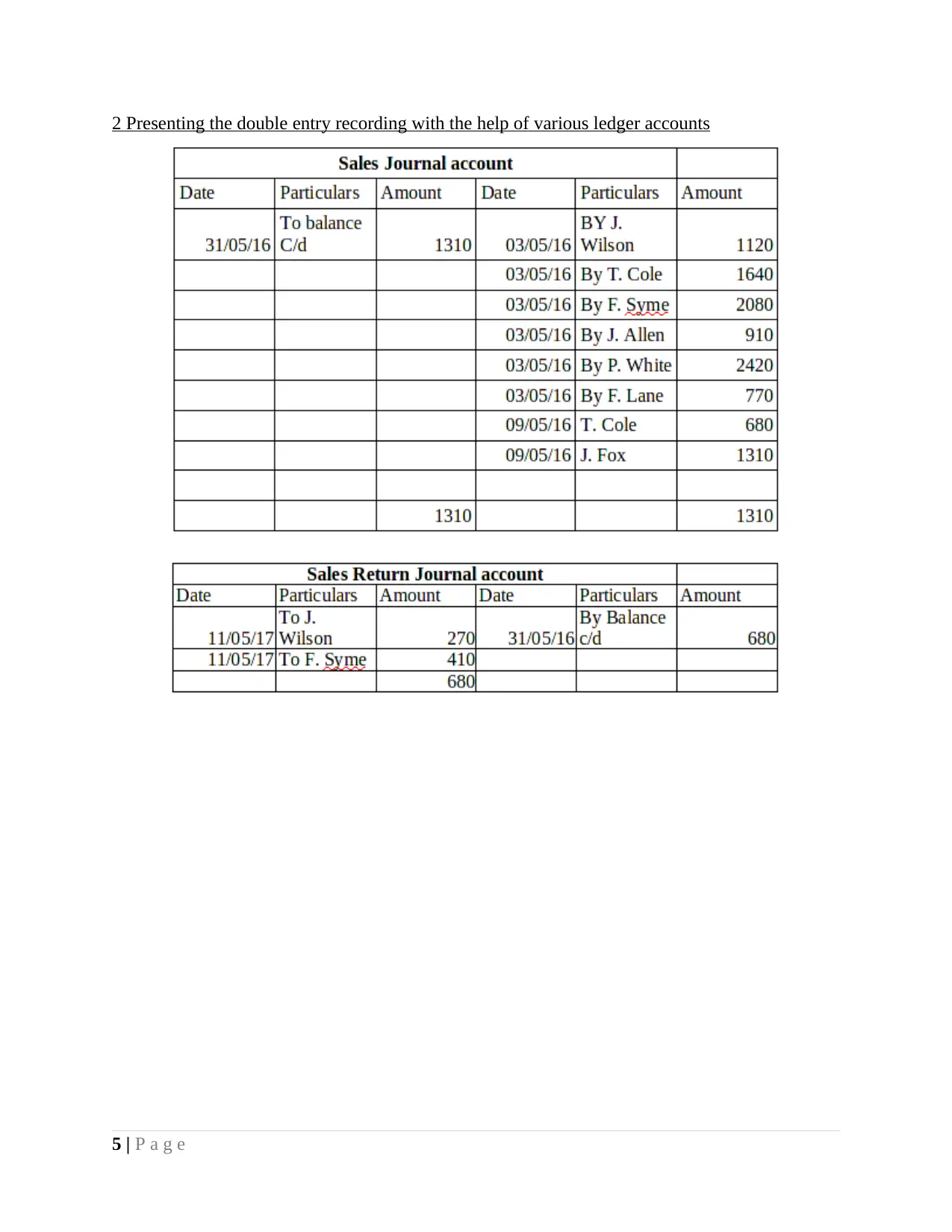

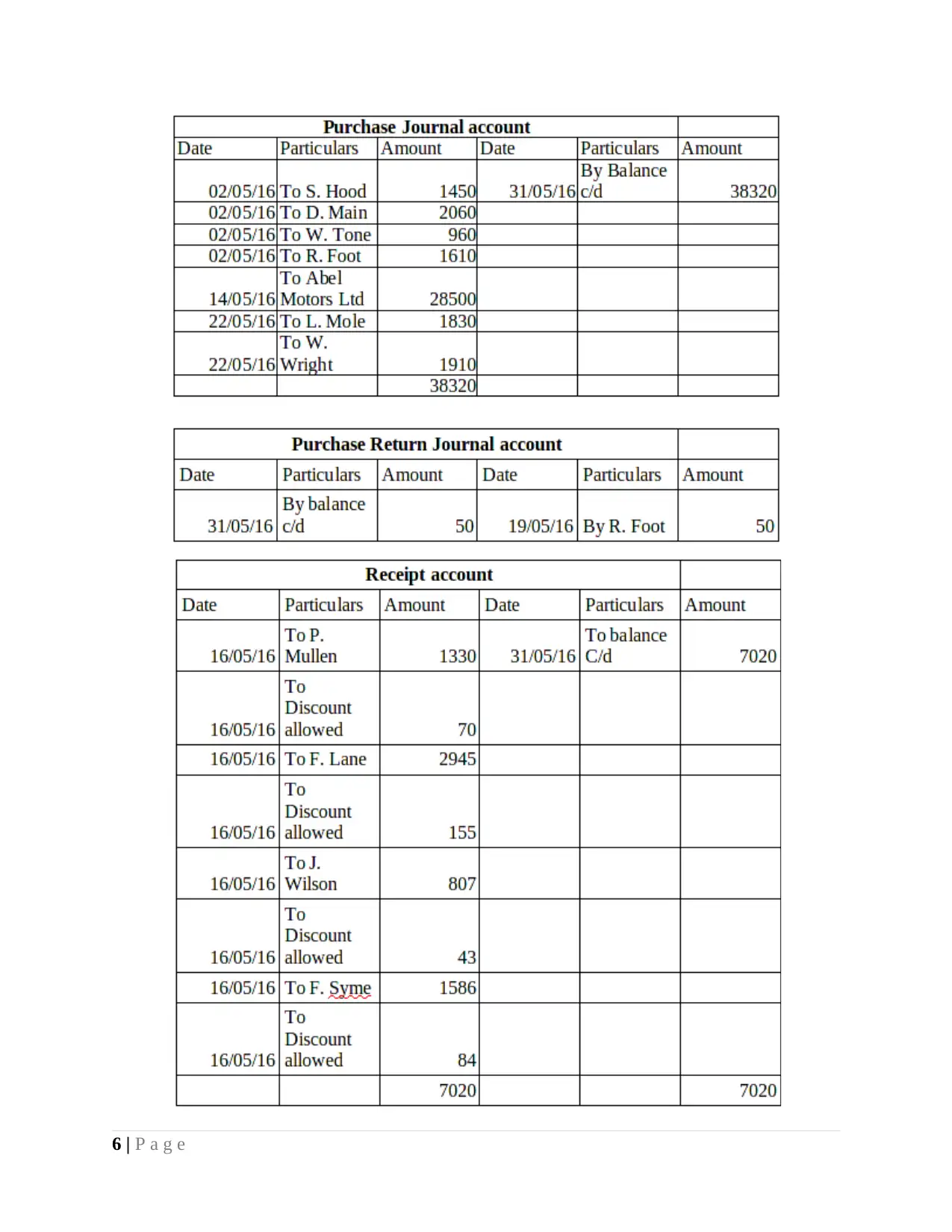

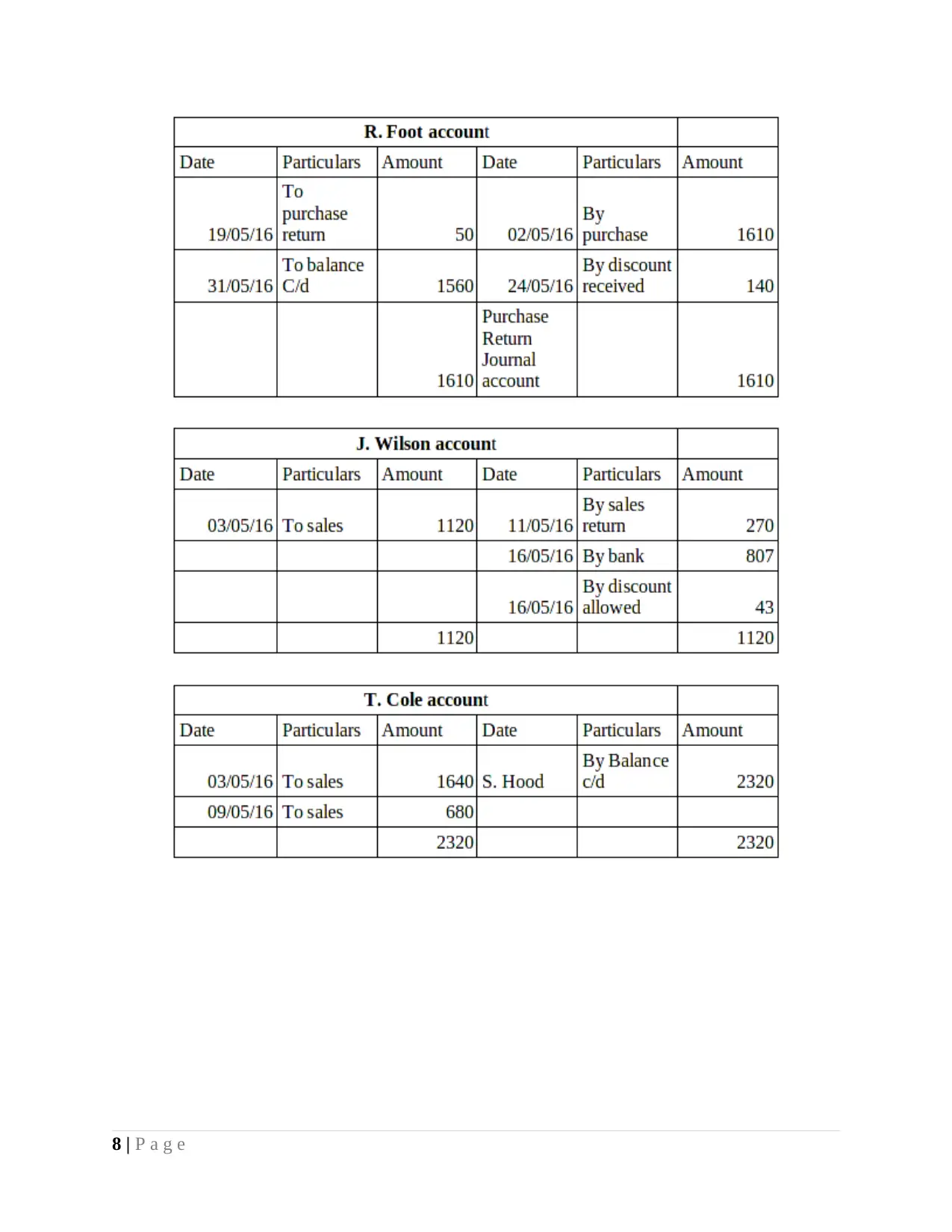

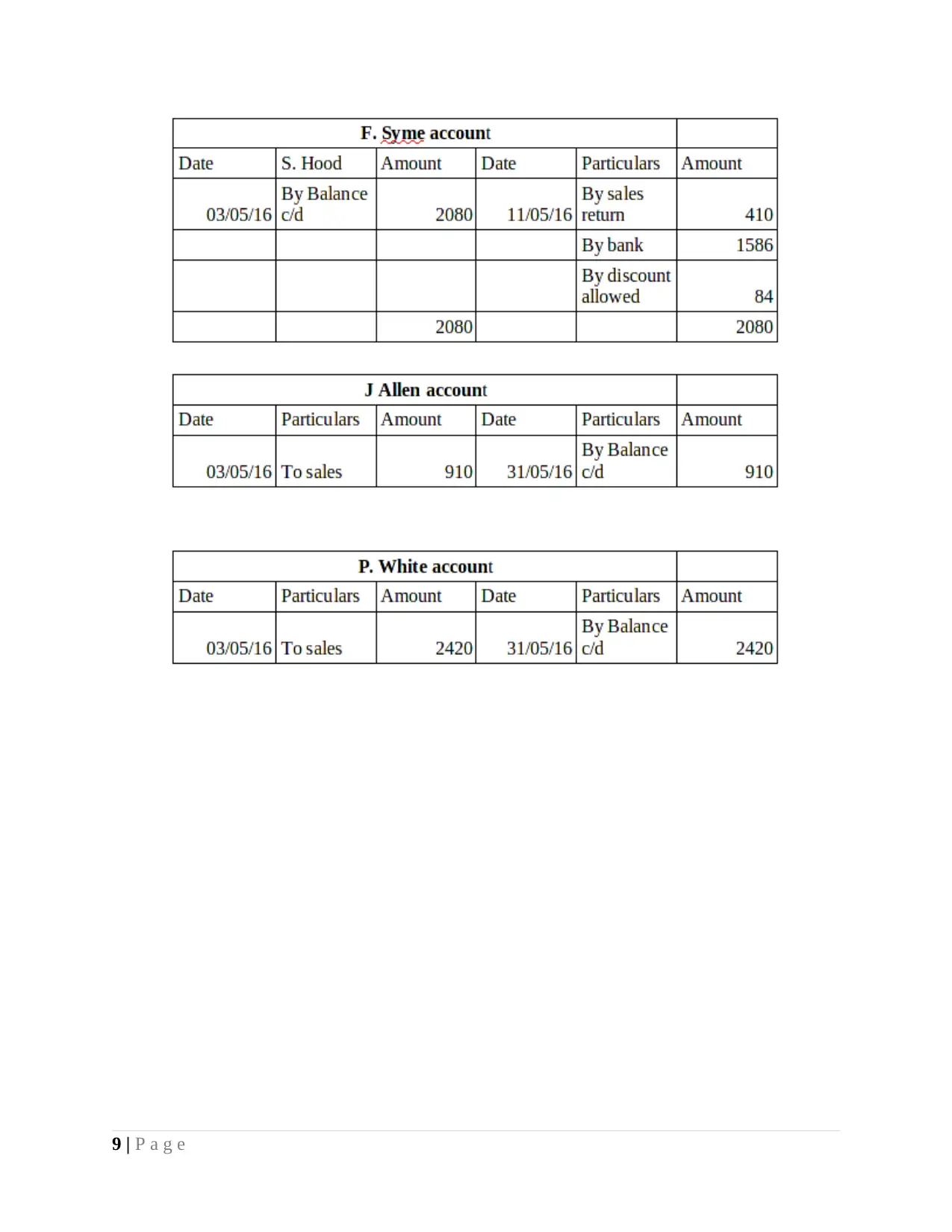

This comprehensive financial accounting report provides an in-depth analysis of various accounting principles and practices. It begins with an introduction outlining the importance of accounting for firms and the structure of the report, which includes sections for line managers and different clients. The report delves into financial accounting rules and principles, including GAAP and IFRS, cost principles, and time period assumptions. It then presents a portfolio catering to various clients, analyzing journal entries, double-entry recordings, and the arithmetical accuracy of the double-entry system. The report includes income statements and balance sheets for different clients, along with explanations of accounting concepts like prudence and consistency. Furthermore, it explores depreciation methods, bank reconciliation statements, control accounts, suspense accounts, and clearing accounts, providing a detailed comparison of these accounting tools. The conclusion emphasizes the significance of accurate accounting practices and the importance of careful consideration when preparing suspense and clearing accounts. The report also includes a detailed reference list of books and journals used in the analysis.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.