Comparative Financial Analysis: Zoopla Plc and Rightmove Plc Report

VerifiedAdded on 2020/06/05

|14

|2723

|36

Report

AI Summary

This report presents a comprehensive financial analysis comparing the performance of Zoopla Plc and Rightmove Plc. It utilizes ratio analysis to evaluate profitability, liquidity, asset utilization, gearing, and stock market performance. The analysis examines key financial metrics such as revenue growth, operating margins, and earnings per share, providing insights into each company's financial health and market position. The report highlights key findings, such as Zoopla's revenue growth and Rightmove's strong operating margins, and offers recommendations for improvement. The analysis covers data from FY2015 and FY2016, providing a detailed overview of the companies' financial performance during this period. The study concludes with a summary of findings, emphasizing the importance of cost management and efficient asset utilization for both companies. The report also includes supporting figures and tables, along with references to relevant literature.

Financial analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

FINANCIAL ANALYSIS...............................................................................................................1

Profitability analysis....................................................................................................................1

Liquidity performance..................................................................................................................4

Assets utilization ratio..................................................................................................................5

Gearing ratio................................................................................................................................6

Stock market performance analysis.............................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................12

Table of Figures

Figure 1 Profitability performance of Zoopla Plc and Rightmove Plc...........................................1

Figure 2 Segmental revenue of Zoopla in FY 2016.......................................................................3

Figure 3 Current ratio of Zoopla Plc..............................................................................................4

Figure 4 Assets utilization ratio of Zoopla Plc and Rightmove Plc................................................5

Figure 5 Capital structure of Zoopla Plc and Rightmove Plc.........................................................6

Figure 6 Earnings per share and Dividend per Share of Zoopla Plc and Right move Plc...............7

Figure 7 Share price comparison of Zoopla Plc and Rightmove Plc..............................................8

INTRODUCTION...........................................................................................................................1

FINANCIAL ANALYSIS...............................................................................................................1

Profitability analysis....................................................................................................................1

Liquidity performance..................................................................................................................4

Assets utilization ratio..................................................................................................................5

Gearing ratio................................................................................................................................6

Stock market performance analysis.............................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................12

Table of Figures

Figure 1 Profitability performance of Zoopla Plc and Rightmove Plc...........................................1

Figure 2 Segmental revenue of Zoopla in FY 2016.......................................................................3

Figure 3 Current ratio of Zoopla Plc..............................................................................................4

Figure 4 Assets utilization ratio of Zoopla Plc and Rightmove Plc................................................5

Figure 5 Capital structure of Zoopla Plc and Rightmove Plc.........................................................6

Figure 6 Earnings per share and Dividend per Share of Zoopla Plc and Right move Plc...............7

Figure 7 Share price comparison of Zoopla Plc and Rightmove Plc..............................................8

INTRODUCTION

In today’s competitive world, every organization keep continuous track over their

business financing activities to determine their performance and suitability. Companies just not

only need to examine their own performance but also need to examine competitor’s behavior,

strategies, actions and performance. UK Real Estate industry is a major contributor to the

economy as it contributes £94 billion and employs 1 million people in the sector (About Real

Estate, 2016). Zoopla Plc is a public limited company that provides information about property

prices, area, value estimates and other required information on it search engine. Its performance

will be compare with Rightmove Plc, which is UK’s biggest online property website and real

estate portal. Both the companies are listed on LSE and a constituent of FTSE 250 Index. The

research will analyze and compare the financial results of the companies using ratio analysis

technique.

FINANCIAL ANALYSIS

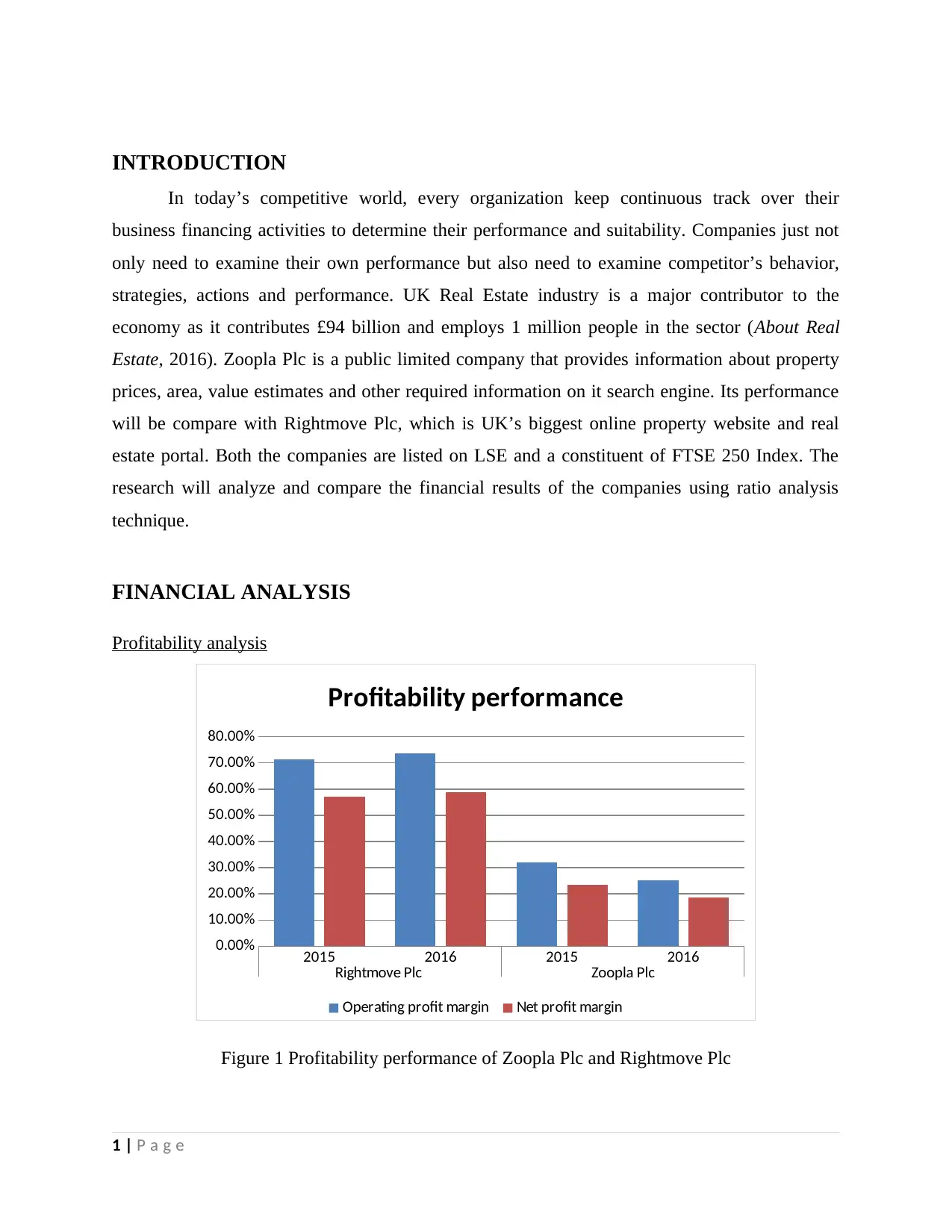

Profitability analysis

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Profitability performance

Operating profit margin Net profit margin

Figure 1 Profitability performance of Zoopla Plc and Rightmove Plc

1 | P a g e

In today’s competitive world, every organization keep continuous track over their

business financing activities to determine their performance and suitability. Companies just not

only need to examine their own performance but also need to examine competitor’s behavior,

strategies, actions and performance. UK Real Estate industry is a major contributor to the

economy as it contributes £94 billion and employs 1 million people in the sector (About Real

Estate, 2016). Zoopla Plc is a public limited company that provides information about property

prices, area, value estimates and other required information on it search engine. Its performance

will be compare with Rightmove Plc, which is UK’s biggest online property website and real

estate portal. Both the companies are listed on LSE and a constituent of FTSE 250 Index. The

research will analyze and compare the financial results of the companies using ratio analysis

technique.

FINANCIAL ANALYSIS

Profitability analysis

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Profitability performance

Operating profit margin Net profit margin

Figure 1 Profitability performance of Zoopla Plc and Rightmove Plc

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

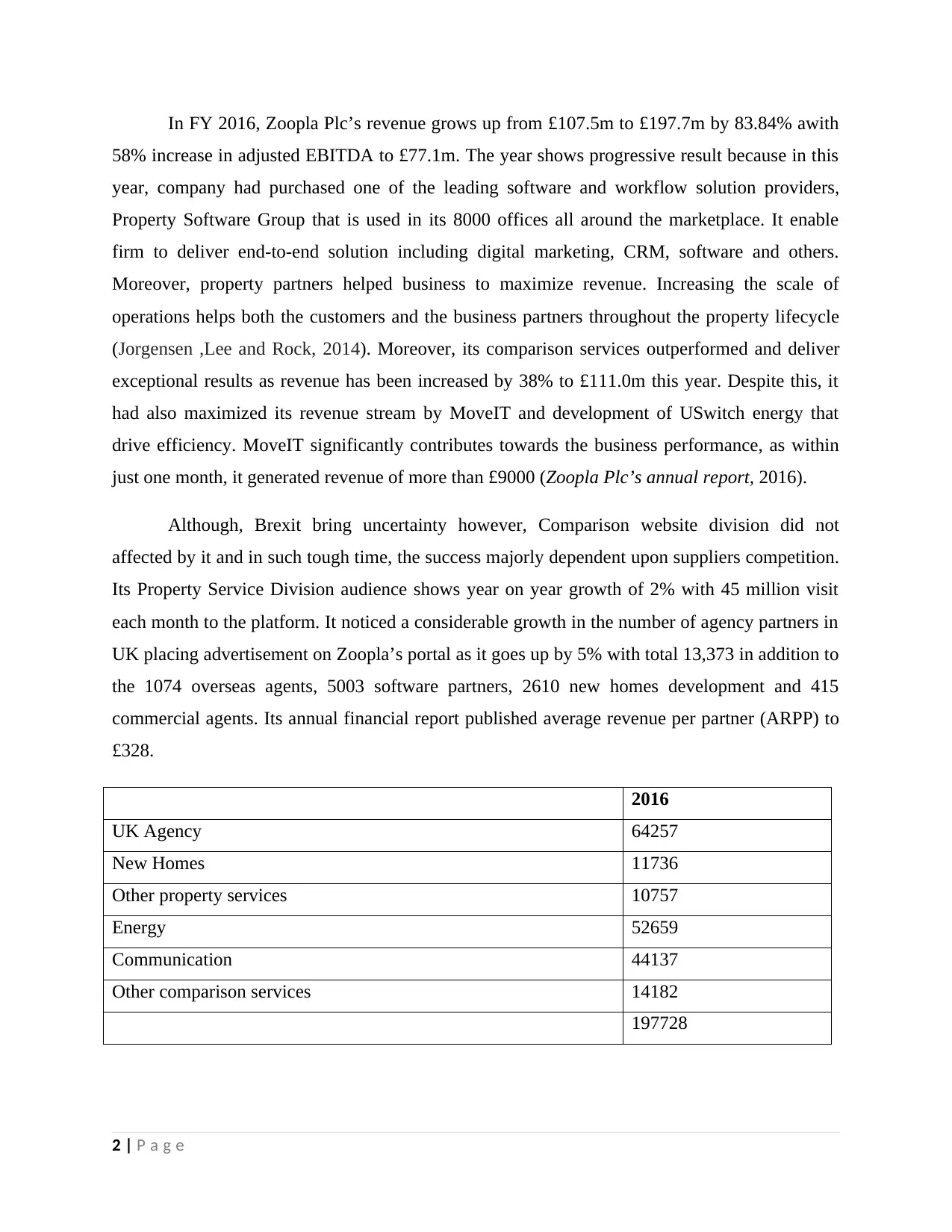

In FY 2016, Zoopla Plc’s revenue grows up from £107.5m to £197.7m by 83.84% awith

58% increase in adjusted EBITDA to £77.1m. The year shows progressive result because in this

year, company had purchased one of the leading software and workflow solution providers,

Property Software Group that is used in its 8000 offices all around the marketplace. It enable

firm to deliver end-to-end solution including digital marketing, CRM, software and others.

Moreover, property partners helped business to maximize revenue. Increasing the scale of

operations helps both the customers and the business partners throughout the property lifecycle

(Jorgensen ,Lee and Rock, 2014). Moreover, its comparison services outperformed and deliver

exceptional results as revenue has been increased by 38% to £111.0m this year. Despite this, it

had also maximized its revenue stream by MoveIT and development of USwitch energy that

drive efficiency. MoveIT significantly contributes towards the business performance, as within

just one month, it generated revenue of more than £9000 (Zoopla Plc’s annual report, 2016).

Although, Brexit bring uncertainty however, Comparison website division did not

affected by it and in such tough time, the success majorly dependent upon suppliers competition.

Its Property Service Division audience shows year on year growth of 2% with 45 million visit

each month to the platform. It noticed a considerable growth in the number of agency partners in

UK placing advertisement on Zoopla’s portal as it goes up by 5% with total 13,373 in addition to

the 1074 overseas agents, 5003 software partners, 2610 new homes development and 415

commercial agents. Its annual financial report published average revenue per partner (ARPP) to

£328.

2016

UK Agency 64257

New Homes 11736

Other property services 10757

Energy 52659

Communication 44137

Other comparison services 14182

197728

2 | P a g e

58% increase in adjusted EBITDA to £77.1m. The year shows progressive result because in this

year, company had purchased one of the leading software and workflow solution providers,

Property Software Group that is used in its 8000 offices all around the marketplace. It enable

firm to deliver end-to-end solution including digital marketing, CRM, software and others.

Moreover, property partners helped business to maximize revenue. Increasing the scale of

operations helps both the customers and the business partners throughout the property lifecycle

(Jorgensen ,Lee and Rock, 2014). Moreover, its comparison services outperformed and deliver

exceptional results as revenue has been increased by 38% to £111.0m this year. Despite this, it

had also maximized its revenue stream by MoveIT and development of USwitch energy that

drive efficiency. MoveIT significantly contributes towards the business performance, as within

just one month, it generated revenue of more than £9000 (Zoopla Plc’s annual report, 2016).

Although, Brexit bring uncertainty however, Comparison website division did not

affected by it and in such tough time, the success majorly dependent upon suppliers competition.

Its Property Service Division audience shows year on year growth of 2% with 45 million visit

each month to the platform. It noticed a considerable growth in the number of agency partners in

UK placing advertisement on Zoopla’s portal as it goes up by 5% with total 13,373 in addition to

the 1074 overseas agents, 5003 software partners, 2610 new homes development and 415

commercial agents. Its annual financial report published average revenue per partner (ARPP) to

£328.

2016

UK Agency 64257

New Homes 11736

Other property services 10757

Energy 52659

Communication 44137

Other comparison services 14182

197728

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

32%

6%

5%27%

22% 7%

Segmental revenue of Zoopla for FY

2016

UK Agency

New Homes

Other property services

Energy

Communication

Other comparison services

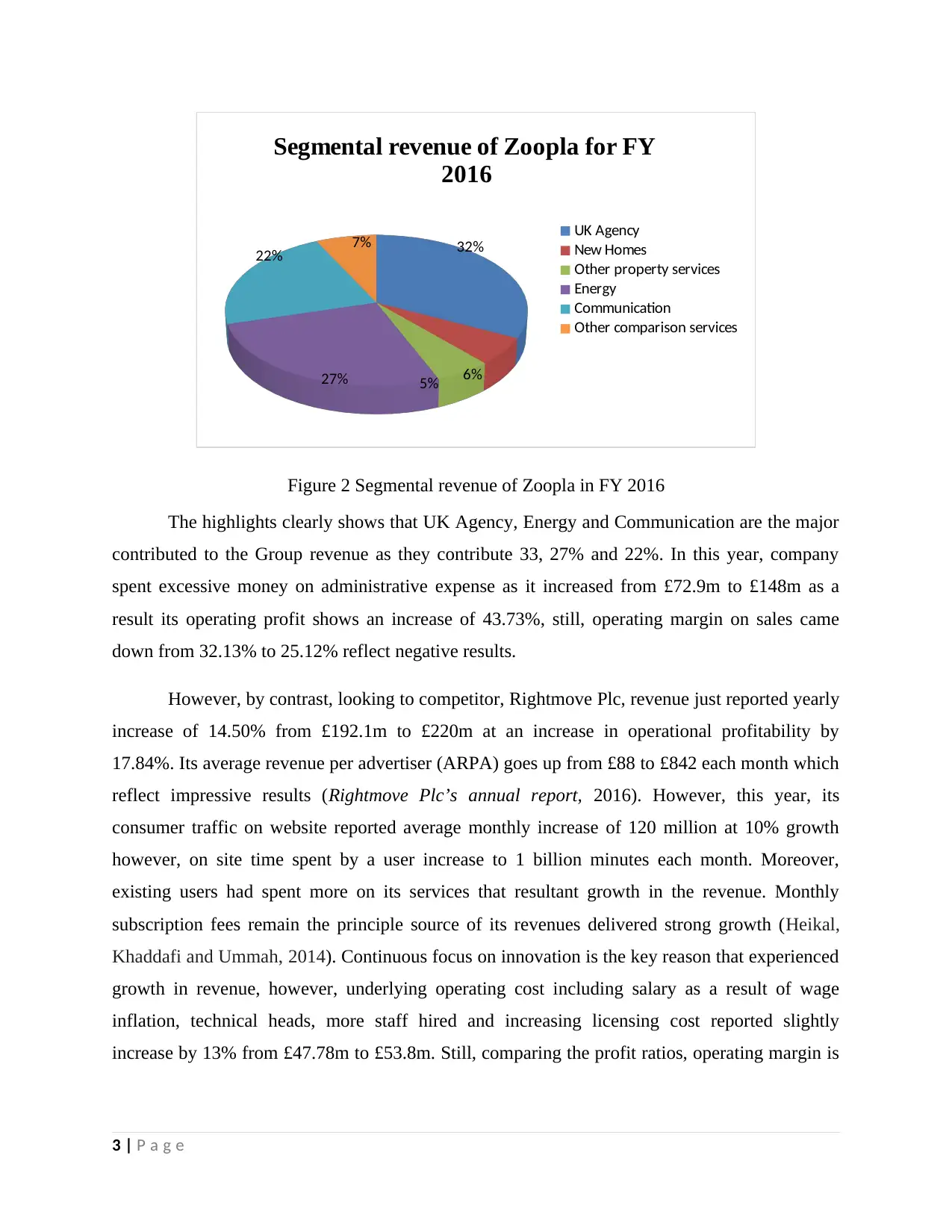

Figure 2 Segmental revenue of Zoopla in FY 2016

The highlights clearly shows that UK Agency, Energy and Communication are the major

contributed to the Group revenue as they contribute 33, 27% and 22%. In this year, company

spent excessive money on administrative expense as it increased from £72.9m to £148m as a

result its operating profit shows an increase of 43.73%, still, operating margin on sales came

down from 32.13% to 25.12% reflect negative results.

However, by contrast, looking to competitor, Rightmove Plc, revenue just reported yearly

increase of 14.50% from £192.1m to £220m at an increase in operational profitability by

17.84%. Its average revenue per advertiser (ARPA) goes up from £88 to £842 each month which

reflect impressive results (Rightmove Plc’s annual report, 2016). However, this year, its

consumer traffic on website reported average monthly increase of 120 million at 10% growth

however, on site time spent by a user increase to 1 billion minutes each month. Moreover,

existing users had spent more on its services that resultant growth in the revenue. Monthly

subscription fees remain the principle source of its revenues delivered strong growth (Heikal,

Khaddafi and Ummah, 2014). Continuous focus on innovation is the key reason that experienced

growth in revenue, however, underlying operating cost including salary as a result of wage

inflation, technical heads, more staff hired and increasing licensing cost reported slightly

increase by 13% from £47.78m to £53.8m. Still, comparing the profit ratios, operating margin is

3 | P a g e

6%

5%27%

22% 7%

Segmental revenue of Zoopla for FY

2016

UK Agency

New Homes

Other property services

Energy

Communication

Other comparison services

Figure 2 Segmental revenue of Zoopla in FY 2016

The highlights clearly shows that UK Agency, Energy and Communication are the major

contributed to the Group revenue as they contribute 33, 27% and 22%. In this year, company

spent excessive money on administrative expense as it increased from £72.9m to £148m as a

result its operating profit shows an increase of 43.73%, still, operating margin on sales came

down from 32.13% to 25.12% reflect negative results.

However, by contrast, looking to competitor, Rightmove Plc, revenue just reported yearly

increase of 14.50% from £192.1m to £220m at an increase in operational profitability by

17.84%. Its average revenue per advertiser (ARPA) goes up from £88 to £842 each month which

reflect impressive results (Rightmove Plc’s annual report, 2016). However, this year, its

consumer traffic on website reported average monthly increase of 120 million at 10% growth

however, on site time spent by a user increase to 1 billion minutes each month. Moreover,

existing users had spent more on its services that resultant growth in the revenue. Monthly

subscription fees remain the principle source of its revenues delivered strong growth (Heikal,

Khaddafi and Ummah, 2014). Continuous focus on innovation is the key reason that experienced

growth in revenue, however, underlying operating cost including salary as a result of wage

inflation, technical heads, more staff hired and increasing licensing cost reported slightly

increase by 13% from £47.78m to £53.8m. Still, comparing the profit ratios, operating margin is

3 | P a g e

too high from Zoopla Plc as in FY 2015, it was 71.40% goes up to 73.48% in FY 2016. The

financial results illustrates that it is performing great comparatively than Zoopla Plc.

In 2016, Net profit ratio of Zoopla Plc dropped from 23.60% to 18.55% indicates that its

performance is declining. On the contrary, Rightmove Plc continued focus of the firm on the cost

control reported growth from 56.98% to 58.88% shows increased profitability. However,

Zoopla’s policy is to pay 35%-45% of after-tax return to shareholders, and in 2016, its post-tax

profit increased to £36.7m by 44.50% (Al Nimer, Warrad and Al Mari, 2015). Despite revenue,

admin cost and others, changing regulation also affects its return due to increased compliance

cost. Due to more debt, Zoopla’s financing expense increased from £1.2m to £3.6m while

income tax liability grows up from £8.2m to £9.5m resultant poor net margin. However,

Rightmove reported a little increase in financing cost from £183,000 to £209,000 and income tax

increased from £27.6m to £32m coupled with high growth in profitability.

Liquidity performance

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.92 0.91

0.67

0.59

Current ratio (CR)

Current ratio

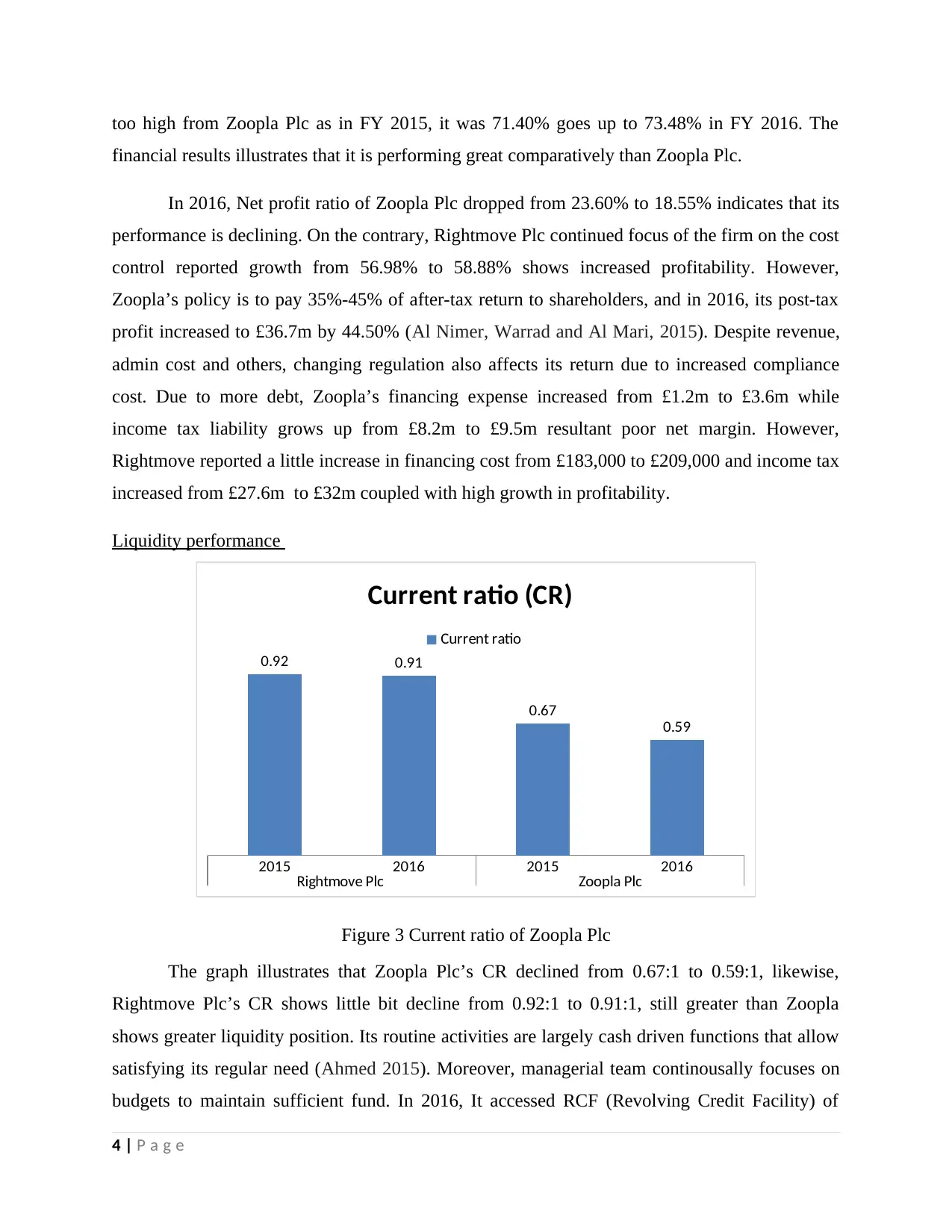

Figure 3 Current ratio of Zoopla Plc

The graph illustrates that Zoopla Plc’s CR declined from 0.67:1 to 0.59:1, likewise,

Rightmove Plc’s CR shows little bit decline from 0.92:1 to 0.91:1, still greater than Zoopla

shows greater liquidity position. Its routine activities are largely cash driven functions that allow

satisfying its regular need (Ahmed 2015). Moreover, managerial team continousally focuses on

budgets to maintain sufficient fund. In 2016, It accessed RCF (Revolving Credit Facility) of

4 | P a g e

financial results illustrates that it is performing great comparatively than Zoopla Plc.

In 2016, Net profit ratio of Zoopla Plc dropped from 23.60% to 18.55% indicates that its

performance is declining. On the contrary, Rightmove Plc continued focus of the firm on the cost

control reported growth from 56.98% to 58.88% shows increased profitability. However,

Zoopla’s policy is to pay 35%-45% of after-tax return to shareholders, and in 2016, its post-tax

profit increased to £36.7m by 44.50% (Al Nimer, Warrad and Al Mari, 2015). Despite revenue,

admin cost and others, changing regulation also affects its return due to increased compliance

cost. Due to more debt, Zoopla’s financing expense increased from £1.2m to £3.6m while

income tax liability grows up from £8.2m to £9.5m resultant poor net margin. However,

Rightmove reported a little increase in financing cost from £183,000 to £209,000 and income tax

increased from £27.6m to £32m coupled with high growth in profitability.

Liquidity performance

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.92 0.91

0.67

0.59

Current ratio (CR)

Current ratio

Figure 3 Current ratio of Zoopla Plc

The graph illustrates that Zoopla Plc’s CR declined from 0.67:1 to 0.59:1, likewise,

Rightmove Plc’s CR shows little bit decline from 0.92:1 to 0.91:1, still greater than Zoopla

shows greater liquidity position. Its routine activities are largely cash driven functions that allow

satisfying its regular need (Ahmed 2015). Moreover, managerial team continousally focuses on

budgets to maintain sufficient fund. In 2016, It accessed RCF (Revolving Credit Facility) of

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

£200m however, Rightmove had an agreement with HSBC for £10,000 RCF (Rightmove Plc’s

annual report, 2016). Being subscription fees as a major source of revenue; Rightmove Plc is

able to receive regular cash allow business to meet out their financial liabilities. Throughout the

period, Group became able to satisfy its cash on demand in order to meet out operational

requirements excluding unpredictable circumstances like natural disasters. Comparing to the

benchmark of 1:1, it can be said that Rightmove’s CR is closer to it, shows strong liquidity.

Assets utilization ratio

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Assets utilization ratio

Assets turnover ratio Debtors recievable ratio

Figure 4 Assets utilization ratio of Zoopla Plc and Rightmove Plc

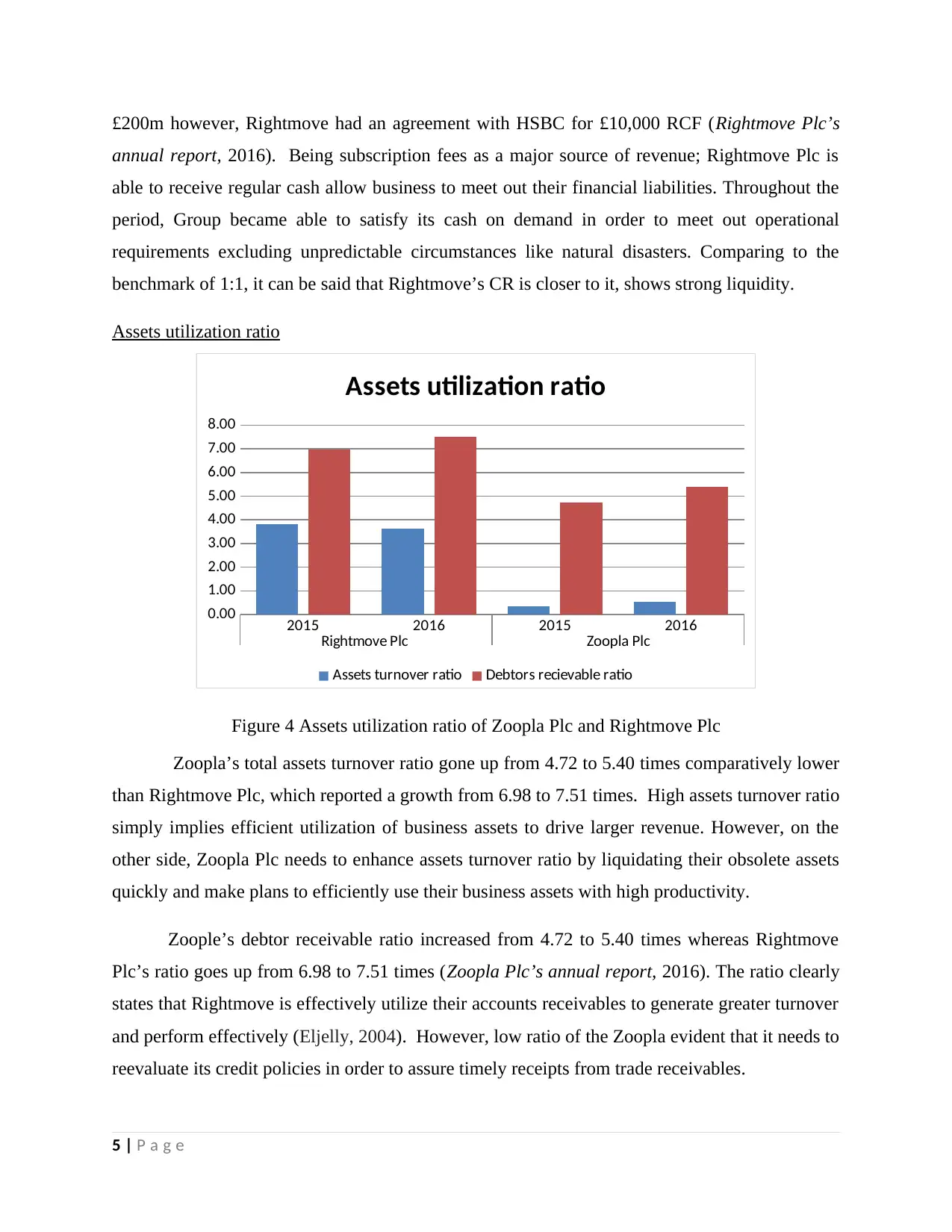

Zoopla’s total assets turnover ratio gone up from 4.72 to 5.40 times comparatively lower

than Rightmove Plc, which reported a growth from 6.98 to 7.51 times. High assets turnover ratio

simply implies efficient utilization of business assets to drive larger revenue. However, on the

other side, Zoopla Plc needs to enhance assets turnover ratio by liquidating their obsolete assets

quickly and make plans to efficiently use their business assets with high productivity.

Zoople’s debtor receivable ratio increased from 4.72 to 5.40 times whereas Rightmove

Plc’s ratio goes up from 6.98 to 7.51 times (Zoopla Plc’s annual report, 2016). The ratio clearly

states that Rightmove is effectively utilize their accounts receivables to generate greater turnover

and perform effectively (Eljelly, 2004). However, low ratio of the Zoopla evident that it needs to

reevaluate its credit policies in order to assure timely receipts from trade receivables.

5 | P a g e

annual report, 2016). Being subscription fees as a major source of revenue; Rightmove Plc is

able to receive regular cash allow business to meet out their financial liabilities. Throughout the

period, Group became able to satisfy its cash on demand in order to meet out operational

requirements excluding unpredictable circumstances like natural disasters. Comparing to the

benchmark of 1:1, it can be said that Rightmove’s CR is closer to it, shows strong liquidity.

Assets utilization ratio

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Assets utilization ratio

Assets turnover ratio Debtors recievable ratio

Figure 4 Assets utilization ratio of Zoopla Plc and Rightmove Plc

Zoopla’s total assets turnover ratio gone up from 4.72 to 5.40 times comparatively lower

than Rightmove Plc, which reported a growth from 6.98 to 7.51 times. High assets turnover ratio

simply implies efficient utilization of business assets to drive larger revenue. However, on the

other side, Zoopla Plc needs to enhance assets turnover ratio by liquidating their obsolete assets

quickly and make plans to efficiently use their business assets with high productivity.

Zoople’s debtor receivable ratio increased from 4.72 to 5.40 times whereas Rightmove

Plc’s ratio goes up from 6.98 to 7.51 times (Zoopla Plc’s annual report, 2016). The ratio clearly

states that Rightmove is effectively utilize their accounts receivables to generate greater turnover

and perform effectively (Eljelly, 2004). However, low ratio of the Zoopla evident that it needs to

reevaluate its credit policies in order to assure timely receipts from trade receivables.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gearing ratio

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0

50000

100000

150000

200000

250000

300000

350000

Capital structure

Debt and equity (In GBP000)

Figure 5 Capital structure of Zoopla Plc and Rightmove Plc

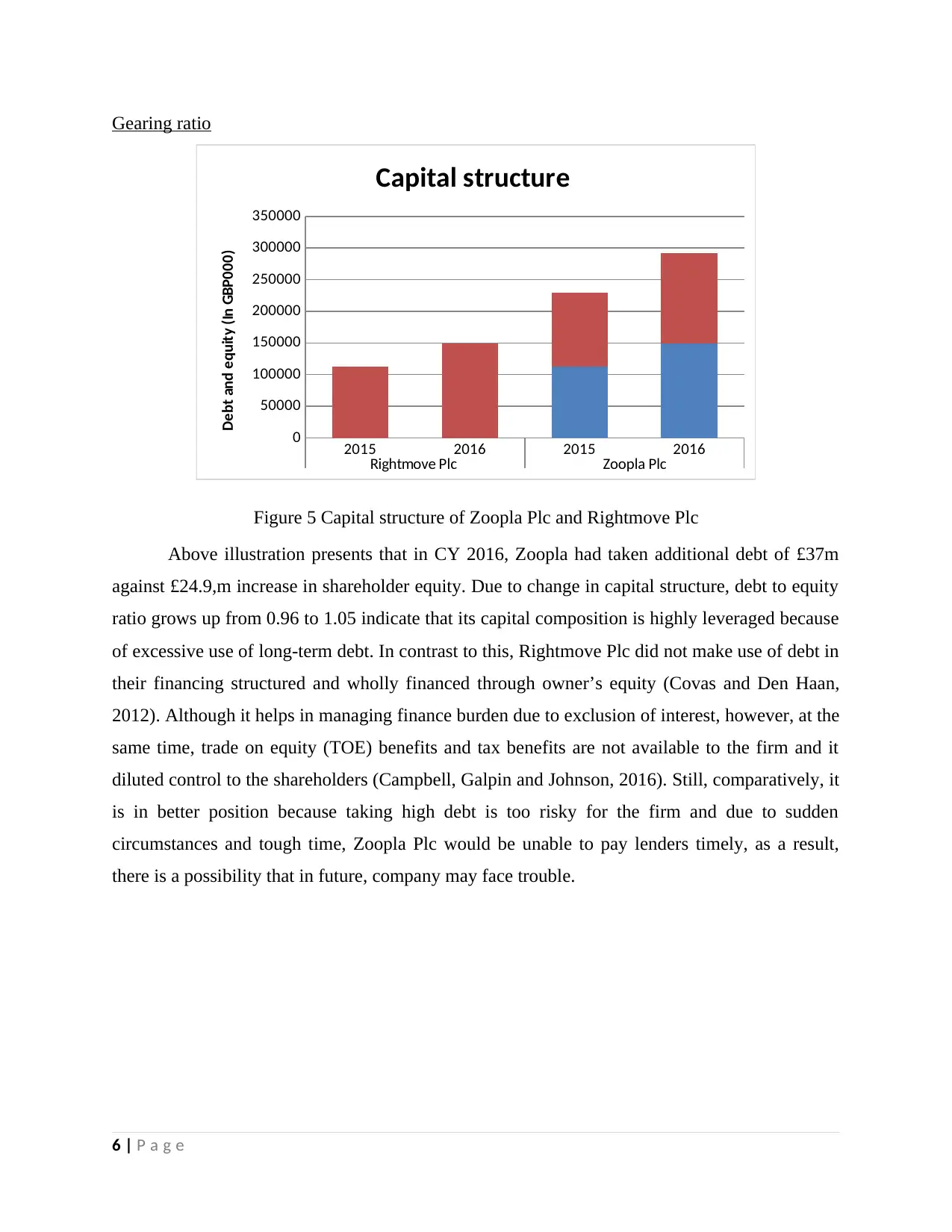

Above illustration presents that in CY 2016, Zoopla had taken additional debt of £37m

against £24.9,m increase in shareholder equity. Due to change in capital structure, debt to equity

ratio grows up from 0.96 to 1.05 indicate that its capital composition is highly leveraged because

of excessive use of long-term debt. In contrast to this, Rightmove Plc did not make use of debt in

their financing structured and wholly financed through owner’s equity (Covas and Den Haan,

2012). Although it helps in managing finance burden due to exclusion of interest, however, at the

same time, trade on equity (TOE) benefits and tax benefits are not available to the firm and it

diluted control to the shareholders (Campbell, Galpin and Johnson, 2016). Still, comparatively, it

is in better position because taking high debt is too risky for the firm and due to sudden

circumstances and tough time, Zoopla Plc would be unable to pay lenders timely, as a result,

there is a possibility that in future, company may face trouble.

6 | P a g e

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0

50000

100000

150000

200000

250000

300000

350000

Capital structure

Debt and equity (In GBP000)

Figure 5 Capital structure of Zoopla Plc and Rightmove Plc

Above illustration presents that in CY 2016, Zoopla had taken additional debt of £37m

against £24.9,m increase in shareholder equity. Due to change in capital structure, debt to equity

ratio grows up from 0.96 to 1.05 indicate that its capital composition is highly leveraged because

of excessive use of long-term debt. In contrast to this, Rightmove Plc did not make use of debt in

their financing structured and wholly financed through owner’s equity (Covas and Den Haan,

2012). Although it helps in managing finance burden due to exclusion of interest, however, at the

same time, trade on equity (TOE) benefits and tax benefits are not available to the firm and it

diluted control to the shareholders (Campbell, Galpin and Johnson, 2016). Still, comparatively, it

is in better position because taking high debt is too risky for the firm and due to sudden

circumstances and tough time, Zoopla Plc would be unable to pay lenders timely, as a result,

there is a possibility that in future, company may face trouble.

6 | P a g e

Stock market performance analysis

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

EPS and DPS Results

EPS and DPS (In Pence)

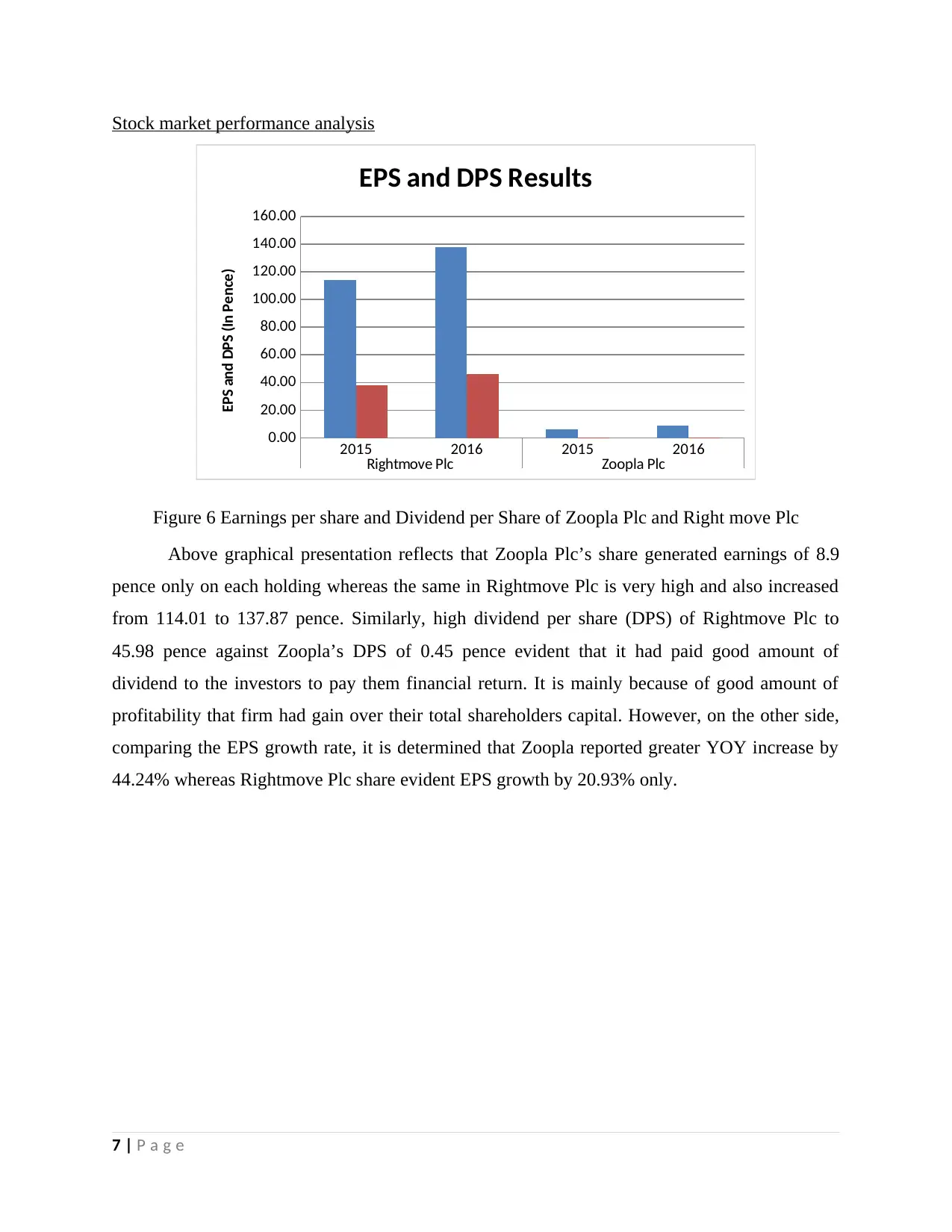

Figure 6 Earnings per share and Dividend per Share of Zoopla Plc and Right move Plc

Above graphical presentation reflects that Zoopla Plc’s share generated earnings of 8.9

pence only on each holding whereas the same in Rightmove Plc is very high and also increased

from 114.01 to 137.87 pence. Similarly, high dividend per share (DPS) of Rightmove Plc to

45.98 pence against Zoopla’s DPS of 0.45 pence evident that it had paid good amount of

dividend to the investors to pay them financial return. It is mainly because of good amount of

profitability that firm had gain over their total shareholders capital. However, on the other side,

comparing the EPS growth rate, it is determined that Zoopla reported greater YOY increase by

44.24% whereas Rightmove Plc share evident EPS growth by 20.93% only.

7 | P a g e

2015 2016 2015 2016

Rightmove Plc Zoopla Plc

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

EPS and DPS Results

EPS and DPS (In Pence)

Figure 6 Earnings per share and Dividend per Share of Zoopla Plc and Right move Plc

Above graphical presentation reflects that Zoopla Plc’s share generated earnings of 8.9

pence only on each holding whereas the same in Rightmove Plc is very high and also increased

from 114.01 to 137.87 pence. Similarly, high dividend per share (DPS) of Rightmove Plc to

45.98 pence against Zoopla’s DPS of 0.45 pence evident that it had paid good amount of

dividend to the investors to pay them financial return. It is mainly because of good amount of

profitability that firm had gain over their total shareholders capital. However, on the other side,

comparing the EPS growth rate, it is determined that Zoopla reported greater YOY increase by

44.24% whereas Rightmove Plc share evident EPS growth by 20.93% only.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

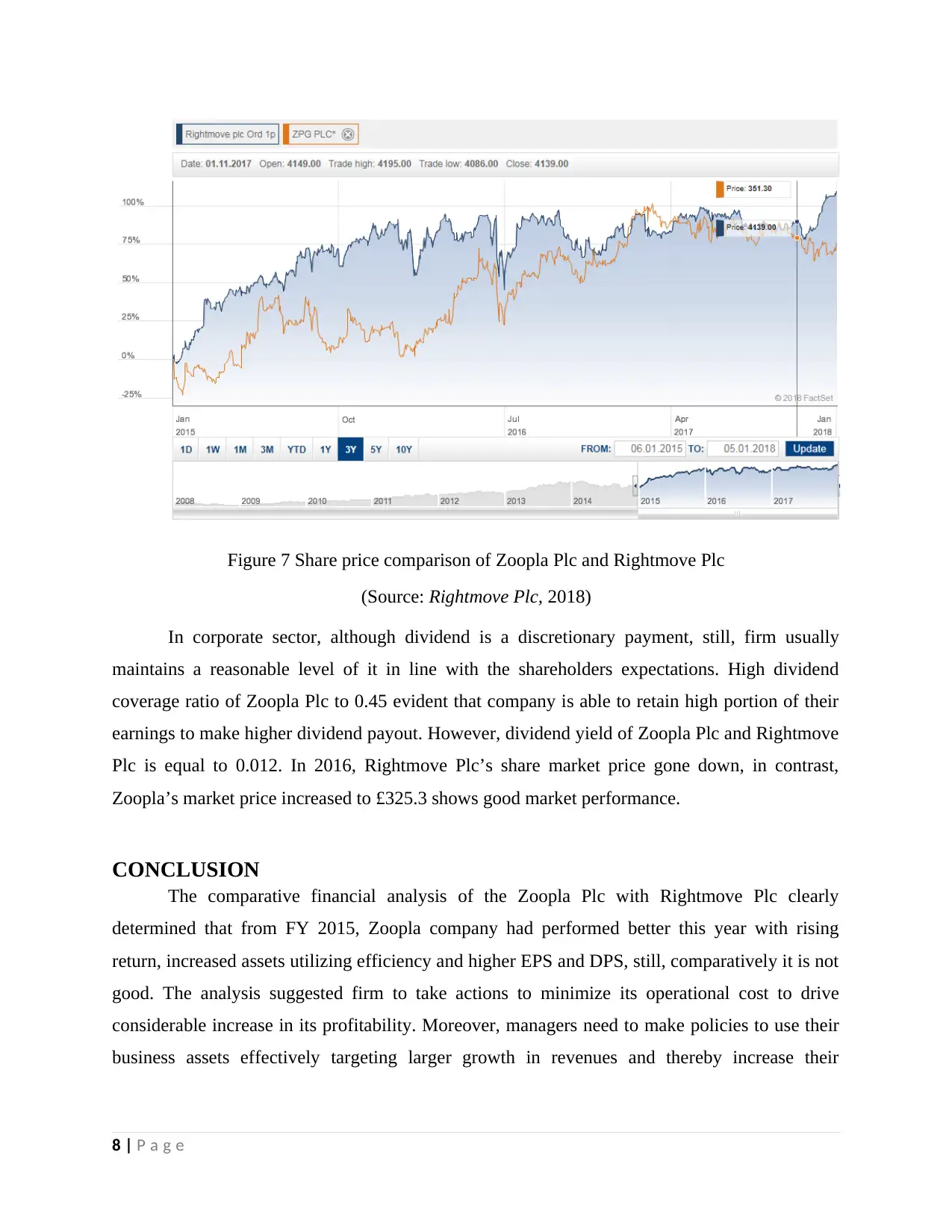

Figure 7 Share price comparison of Zoopla Plc and Rightmove Plc

(Source: Rightmove Plc, 2018)

In corporate sector, although dividend is a discretionary payment, still, firm usually

maintains a reasonable level of it in line with the shareholders expectations. High dividend

coverage ratio of Zoopla Plc to 0.45 evident that company is able to retain high portion of their

earnings to make higher dividend payout. However, dividend yield of Zoopla Plc and Rightmove

Plc is equal to 0.012. In 2016, Rightmove Plc’s share market price gone down, in contrast,

Zoopla’s market price increased to £325.3 shows good market performance.

CONCLUSION

The comparative financial analysis of the Zoopla Plc with Rightmove Plc clearly

determined that from FY 2015, Zoopla company had performed better this year with rising

return, increased assets utilizing efficiency and higher EPS and DPS, still, comparatively it is not

good. The analysis suggested firm to take actions to minimize its operational cost to drive

considerable increase in its profitability. Moreover, managers need to make policies to use their

business assets effectively targeting larger growth in revenues and thereby increase their

8 | P a g e

(Source: Rightmove Plc, 2018)

In corporate sector, although dividend is a discretionary payment, still, firm usually

maintains a reasonable level of it in line with the shareholders expectations. High dividend

coverage ratio of Zoopla Plc to 0.45 evident that company is able to retain high portion of their

earnings to make higher dividend payout. However, dividend yield of Zoopla Plc and Rightmove

Plc is equal to 0.012. In 2016, Rightmove Plc’s share market price gone down, in contrast,

Zoopla’s market price increased to £325.3 shows good market performance.

CONCLUSION

The comparative financial analysis of the Zoopla Plc with Rightmove Plc clearly

determined that from FY 2015, Zoopla company had performed better this year with rising

return, increased assets utilizing efficiency and higher EPS and DPS, still, comparatively it is not

good. The analysis suggested firm to take actions to minimize its operational cost to drive

considerable increase in its profitability. Moreover, managers need to make policies to use their

business assets effectively targeting larger growth in revenues and thereby increase their

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial results. However, on the other side, to reduce excessive burden, it is consider better to

suggest firm to minimize excessively debt and improve solvency position.

9 | P a g e

suggest firm to minimize excessively debt and improve solvency position.

9 | P a g e

REFERENCES

Books and Journals

Ahmed, I.E., 2015. Liquidity, Profitability and the Dividends Payout Policy. World Review of

Business Research. 5(2). pp.73-85.

Al Nimer, M., Warrad, L. and Al Mari, R., 2015. The Impact of liquidity on Jordanian banks

profitability through return on assets. European Journal of Business and Management.

7(7). pp.229-232.

Campbell, T.C., Galpin, N. and Johnson, S.A., 2016. Optimal inside debt compensation and the

value of equity and debt. Journal of Financial Economics. 119(2). pp.336-352.

Covas, F. and Den Haan, W.J., 2012. The role of debt and equity finance over the business cycle. The

Economic Journal. 122(565). pp.1262-1286.

Eljelly, A.M., 2004. Liquidity‐profitability tradeoff: An empirical investigation in an emerging

market. International journal of commerce and management. 14(2). pp.48-61.

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current

ratio (CR), against corporate profit growth in automotive in Indonesia stock

exchange. International Journal of Academic Research in Business and Social Sciences.

4(12). p.101.

Jorgensen, B.N., Lee, Y.G. and Rock, S., 2014. The shapes of scaled earnings histograms are not

due to scaling and sample selection: Evidence from distributions of reported earnings per

share. Contemporary Accounting Research. 31(2). pp.498-521.

Online

About Real Estate. 2016. [Online]. Available through: http://www.bpf.org.uk/about-real-estate

Rightmove Plc. 2018. [Online]. Available through: < http://www.hl.co.uk/shares/shares-search-

results/r/rightmove-plc-ord-1p/share-charts>.

10 | P a g e

Books and Journals

Ahmed, I.E., 2015. Liquidity, Profitability and the Dividends Payout Policy. World Review of

Business Research. 5(2). pp.73-85.

Al Nimer, M., Warrad, L. and Al Mari, R., 2015. The Impact of liquidity on Jordanian banks

profitability through return on assets. European Journal of Business and Management.

7(7). pp.229-232.

Campbell, T.C., Galpin, N. and Johnson, S.A., 2016. Optimal inside debt compensation and the

value of equity and debt. Journal of Financial Economics. 119(2). pp.336-352.

Covas, F. and Den Haan, W.J., 2012. The role of debt and equity finance over the business cycle. The

Economic Journal. 122(565). pp.1262-1286.

Eljelly, A.M., 2004. Liquidity‐profitability tradeoff: An empirical investigation in an emerging

market. International journal of commerce and management. 14(2). pp.48-61.

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current

ratio (CR), against corporate profit growth in automotive in Indonesia stock

exchange. International Journal of Academic Research in Business and Social Sciences.

4(12). p.101.

Jorgensen, B.N., Lee, Y.G. and Rock, S., 2014. The shapes of scaled earnings histograms are not

due to scaling and sample selection: Evidence from distributions of reported earnings per

share. Contemporary Accounting Research. 31(2). pp.498-521.

Online

About Real Estate. 2016. [Online]. Available through: http://www.bpf.org.uk/about-real-estate

Rightmove Plc. 2018. [Online]. Available through: < http://www.hl.co.uk/shares/shares-search-

results/r/rightmove-plc-ord-1p/share-charts>.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.