Financial Management Report: Analysis of Dividend and Investment

VerifiedAdded on 2020/12/09

|15

|3985

|175

Report

AI Summary

This financial management report delves into key aspects of financial decision-making, specifically focusing on dividend policy and investment appraisal techniques. It begins by calculating the fair market value of Planet shares using the dividend growth model, considering both the initial and adjusted required rates of return. The report then critically evaluates the dividend growth model, highlighting its strengths and limitations, such as its sensitivity to input changes and its inability to account for non-dividend factors. Furthermore, the report analyzes investment appraisal techniques, including net present value (NPV), internal rate of return (IRR), and payback period, to assess the economic feasibility of a project. The report also examines the advantages and disadvantages of different investment appraisal methods. The analysis includes computations of cash flows, discount rates, and interpretations of the results to facilitate informed financial decisions.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 2........................................................................................................................................1

a. Calculation of the fair market value of planet shares..............................................................1

b. Computation of the new fair value for planet shares..............................................................2

c. Outlining the problems faced while using the dividend growth model in terms of valuing

the shares. ...................................................................................................................................2

Question 3........................................................................................................................................4

2. Evaluating the advantages and disadvantages of different investment appraisal technique...9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

Question 2........................................................................................................................................1

a. Calculation of the fair market value of planet shares..............................................................1

b. Computation of the new fair value for planet shares..............................................................2

c. Outlining the problems faced while using the dividend growth model in terms of valuing

the shares. ...................................................................................................................................2

Question 3........................................................................................................................................4

2. Evaluating the advantages and disadvantages of different investment appraisal technique...9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

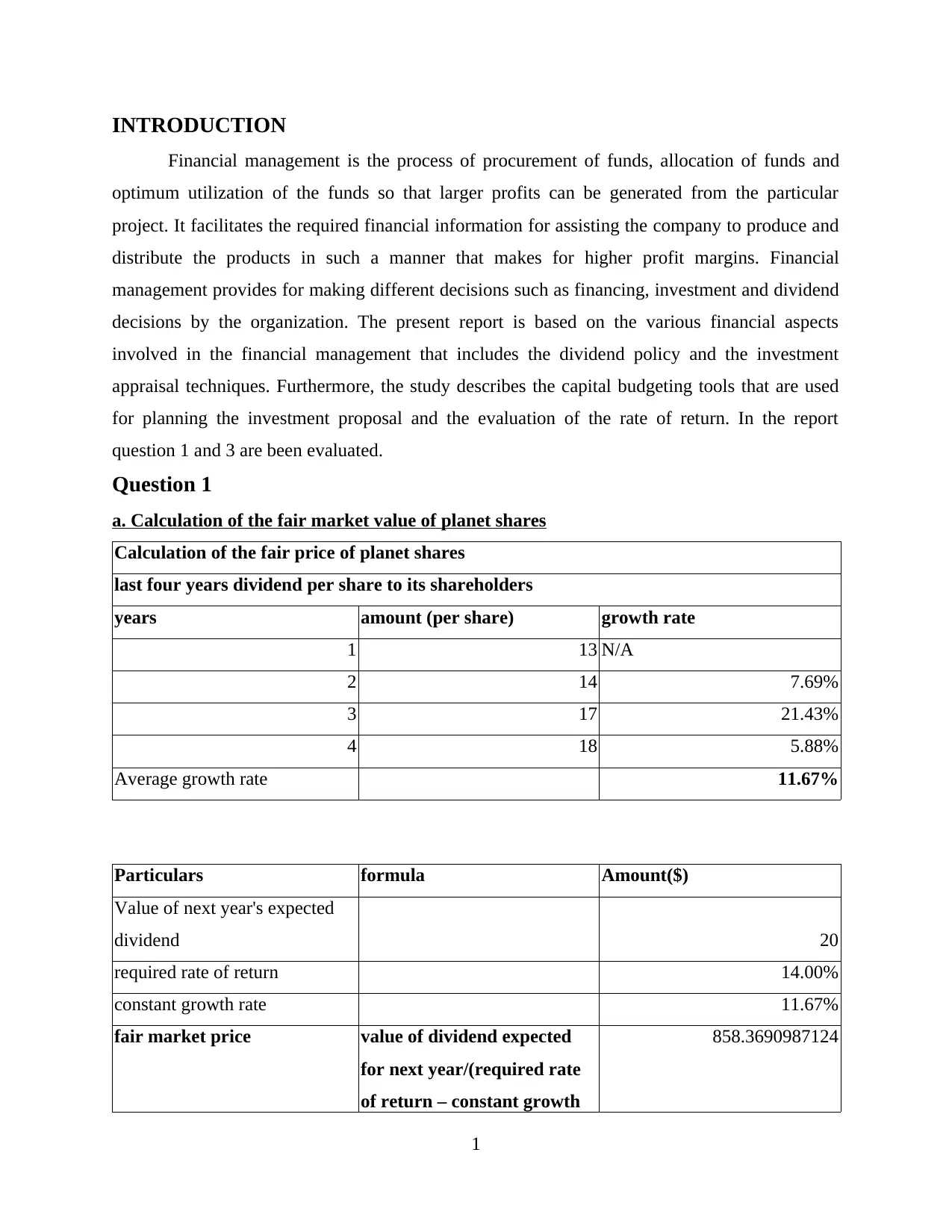

INTRODUCTION

Financial management is the process of procurement of funds, allocation of funds and

optimum utilization of the funds so that larger profits can be generated from the particular

project. It facilitates the required financial information for assisting the company to produce and

distribute the products in such a manner that makes for higher profit margins. Financial

management provides for making different decisions such as financing, investment and dividend

decisions by the organization. The present report is based on the various financial aspects

involved in the financial management that includes the dividend policy and the investment

appraisal techniques. Furthermore, the study describes the capital budgeting tools that are used

for planning the investment proposal and the evaluation of the rate of return. In the report

question 1 and 3 are been evaluated.

Question 1

a. Calculation of the fair market value of planet shares

Calculation of the fair price of planet shares

last four years dividend per share to its shareholders

years amount (per share) growth rate

1 13 N/A

2 14 7.69%

3 17 21.43%

4 18 5.88%

Average growth rate 11.67%

Particulars formula Amount($)

Value of next year's expected

dividend 20

required rate of return 14.00%

constant growth rate 11.67%

fair market price value of dividend expected

for next year/(required rate

of return – constant growth

858.3690987124

1

Financial management is the process of procurement of funds, allocation of funds and

optimum utilization of the funds so that larger profits can be generated from the particular

project. It facilitates the required financial information for assisting the company to produce and

distribute the products in such a manner that makes for higher profit margins. Financial

management provides for making different decisions such as financing, investment and dividend

decisions by the organization. The present report is based on the various financial aspects

involved in the financial management that includes the dividend policy and the investment

appraisal techniques. Furthermore, the study describes the capital budgeting tools that are used

for planning the investment proposal and the evaluation of the rate of return. In the report

question 1 and 3 are been evaluated.

Question 1

a. Calculation of the fair market value of planet shares

Calculation of the fair price of planet shares

last four years dividend per share to its shareholders

years amount (per share) growth rate

1 13 N/A

2 14 7.69%

3 17 21.43%

4 18 5.88%

Average growth rate 11.67%

Particulars formula Amount($)

Value of next year's expected

dividend 20

required rate of return 14.00%

constant growth rate 11.67%

fair market price value of dividend expected

for next year/(required rate

of return – constant growth

858.3690987124

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

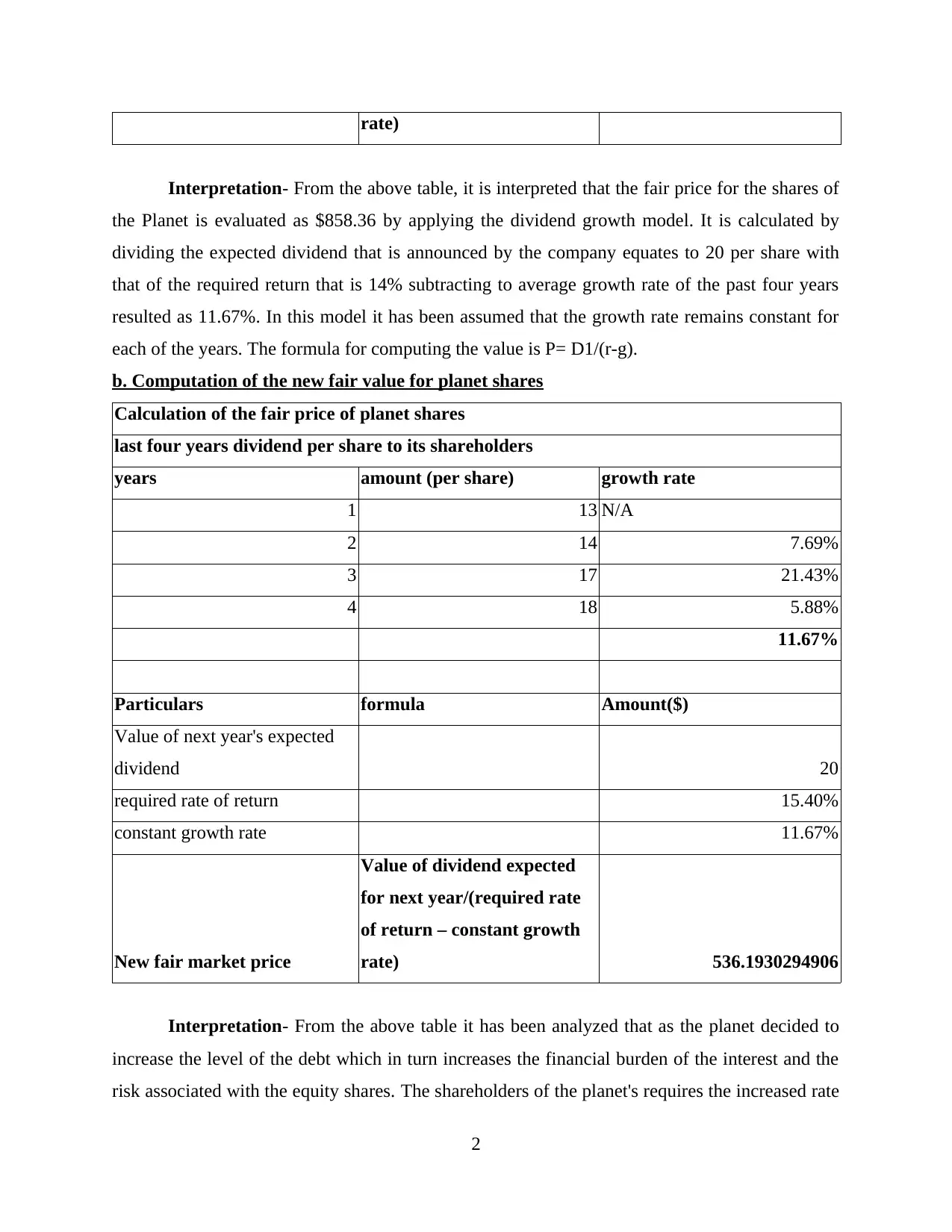

rate)

Interpretation- From the above table, it is interpreted that the fair price for the shares of

the Planet is evaluated as $858.36 by applying the dividend growth model. It is calculated by

dividing the expected dividend that is announced by the company equates to 20 per share with

that of the required return that is 14% subtracting to average growth rate of the past four years

resulted as 11.67%. In this model it has been assumed that the growth rate remains constant for

each of the years. The formula for computing the value is P= D1/(r-g).

b. Computation of the new fair value for planet shares

Calculation of the fair price of planet shares

last four years dividend per share to its shareholders

years amount (per share) growth rate

1 13 N/A

2 14 7.69%

3 17 21.43%

4 18 5.88%

11.67%

Particulars formula Amount($)

Value of next year's expected

dividend 20

required rate of return 15.40%

constant growth rate 11.67%

New fair market price

Value of dividend expected

for next year/(required rate

of return – constant growth

rate) 536.1930294906

Interpretation- From the above table it has been analyzed that as the planet decided to

increase the level of the debt which in turn increases the financial burden of the interest and the

risk associated with the equity shares. The shareholders of the planet's requires the increased rate

2

Interpretation- From the above table, it is interpreted that the fair price for the shares of

the Planet is evaluated as $858.36 by applying the dividend growth model. It is calculated by

dividing the expected dividend that is announced by the company equates to 20 per share with

that of the required return that is 14% subtracting to average growth rate of the past four years

resulted as 11.67%. In this model it has been assumed that the growth rate remains constant for

each of the years. The formula for computing the value is P= D1/(r-g).

b. Computation of the new fair value for planet shares

Calculation of the fair price of planet shares

last four years dividend per share to its shareholders

years amount (per share) growth rate

1 13 N/A

2 14 7.69%

3 17 21.43%

4 18 5.88%

11.67%

Particulars formula Amount($)

Value of next year's expected

dividend 20

required rate of return 15.40%

constant growth rate 11.67%

New fair market price

Value of dividend expected

for next year/(required rate

of return – constant growth

rate) 536.1930294906

Interpretation- From the above table it has been analyzed that as the planet decided to

increase the level of the debt which in turn increases the financial burden of the interest and the

risk associated with the equity shares. The shareholders of the planet's requires the increased rate

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of return of 15.4%. Due to the increase in the required rate of return the new fair value of the

shares has been ascertained as $536.19.

c. Outlining the problems faced while using the dividend growth model in terms of valuing the

shares.

Dividend growth model is the model that computes the fair value of the stock with the

assumption that the growth rate of the dividend is stable for perpetual years. This model

determines if the stock is undervalued and overvalued with the anticipation that the expected

dividends of the enterprise grows with a same rate which is deducted from the rate of return that

is required (Karadag, 2015). At the time of valuation of the shares many problems are faced

under the dividend growth model such as precision is needed as the model is very much sensitive

to the changes in the inputs. For example- if the little changes are made in the constant growth

rate then there occurs a huge change in the evaluated terminal value which in turn changes the

value of stock. Thus, for developing the accuracy in the model, inputs need to be forecasted

accurately. The problem incurred is that forecasting of the accurate inputs are not possible with

the great degree of the precision by the investors (Bowman, 2016). The growth patterns in the

dividend growth model is non-linear as the constant growth rate is assumed. It is non-linear

because of the existence of the business cycles. During the boom times, corporate experience a

situation of surge in the earnings and pays out the generous dividends and during the lean or

depression times the company pays out very low amount of dividend. Thus, it creates difficulty

for the firm to smoothen out its dividend payments. By this, best approximations cannot be made

at the time of valuing the shares through dividend growth model (Engel and et.al., 2018).

Problem relating to the forecasting is also present in the dividend growth model as it needs

enormous amount of the speculation in forecasting the future dividends and is based on the

assumption that the future cash dividends can only provide a reliable estimate of the intrinsic

value of the corporation.

The dividend growth model is not said to be useful for resolving the problem of the high

growing value of the stocks. For instance- if the growth rate of the dividend exceeds the rate of

return expected, the value cannot be computed as the resultant denominator will be in negative

value and the value of the stock can never be negative so this is the major problem. Dividend

growth model is also known as Gordon Growth Model (Nhleko and Musingwini, 2016). One of

the most important issue which dividend growth model face during making valuation of shares of

3

shares has been ascertained as $536.19.

c. Outlining the problems faced while using the dividend growth model in terms of valuing the

shares.

Dividend growth model is the model that computes the fair value of the stock with the

assumption that the growth rate of the dividend is stable for perpetual years. This model

determines if the stock is undervalued and overvalued with the anticipation that the expected

dividends of the enterprise grows with a same rate which is deducted from the rate of return that

is required (Karadag, 2015). At the time of valuation of the shares many problems are faced

under the dividend growth model such as precision is needed as the model is very much sensitive

to the changes in the inputs. For example- if the little changes are made in the constant growth

rate then there occurs a huge change in the evaluated terminal value which in turn changes the

value of stock. Thus, for developing the accuracy in the model, inputs need to be forecasted

accurately. The problem incurred is that forecasting of the accurate inputs are not possible with

the great degree of the precision by the investors (Bowman, 2016). The growth patterns in the

dividend growth model is non-linear as the constant growth rate is assumed. It is non-linear

because of the existence of the business cycles. During the boom times, corporate experience a

situation of surge in the earnings and pays out the generous dividends and during the lean or

depression times the company pays out very low amount of dividend. Thus, it creates difficulty

for the firm to smoothen out its dividend payments. By this, best approximations cannot be made

at the time of valuing the shares through dividend growth model (Engel and et.al., 2018).

Problem relating to the forecasting is also present in the dividend growth model as it needs

enormous amount of the speculation in forecasting the future dividends and is based on the

assumption that the future cash dividends can only provide a reliable estimate of the intrinsic

value of the corporation.

The dividend growth model is not said to be useful for resolving the problem of the high

growing value of the stocks. For instance- if the growth rate of the dividend exceeds the rate of

return expected, the value cannot be computed as the resultant denominator will be in negative

value and the value of the stock can never be negative so this is the major problem. Dividend

growth model is also known as Gordon Growth Model (Nhleko and Musingwini, 2016). One of

the most important issue which dividend growth model face during making valuation of shares of

3

the company is by not taking into consideration all the non dividend factors related to the

company. This model doesn't take into consideration factors which are not directly linked with

the dividend policy of the company and which is influencing the dividend distribution policy of

the company (Duncan and et.al., 2017). Non dividend factors of the company includes Brand

loyalty, retention and satisfaction of customer, ownership related to the acquisition of any

intangible assets, all this factors leads to increase in the market value of the company and its

shares or stocks. But this growth model doesn't consider it while valuing shares of company and

hence correct valuation of company's share is not possible or not done.

Also, the Dividend growth model relies mostly on one assumption which states that the

growth rate of the company is stable, constant and also know (Ozuomba, Anichebe and Okoye,

2016). The stock price of the company is directly related to the rate of dividend growth chosen

with assumption that the growth rate cannot exceed the cost of equity of the company, which is

not always reliable and true (Mugoša and Popović, 2015). Another issue of this dividend growth

model is that if the growth rate is higher than the required rate of return, the model can have

negative value. Also, when the growth rate and required rate of return have same value then the

value of share will be infinite which is not possible.

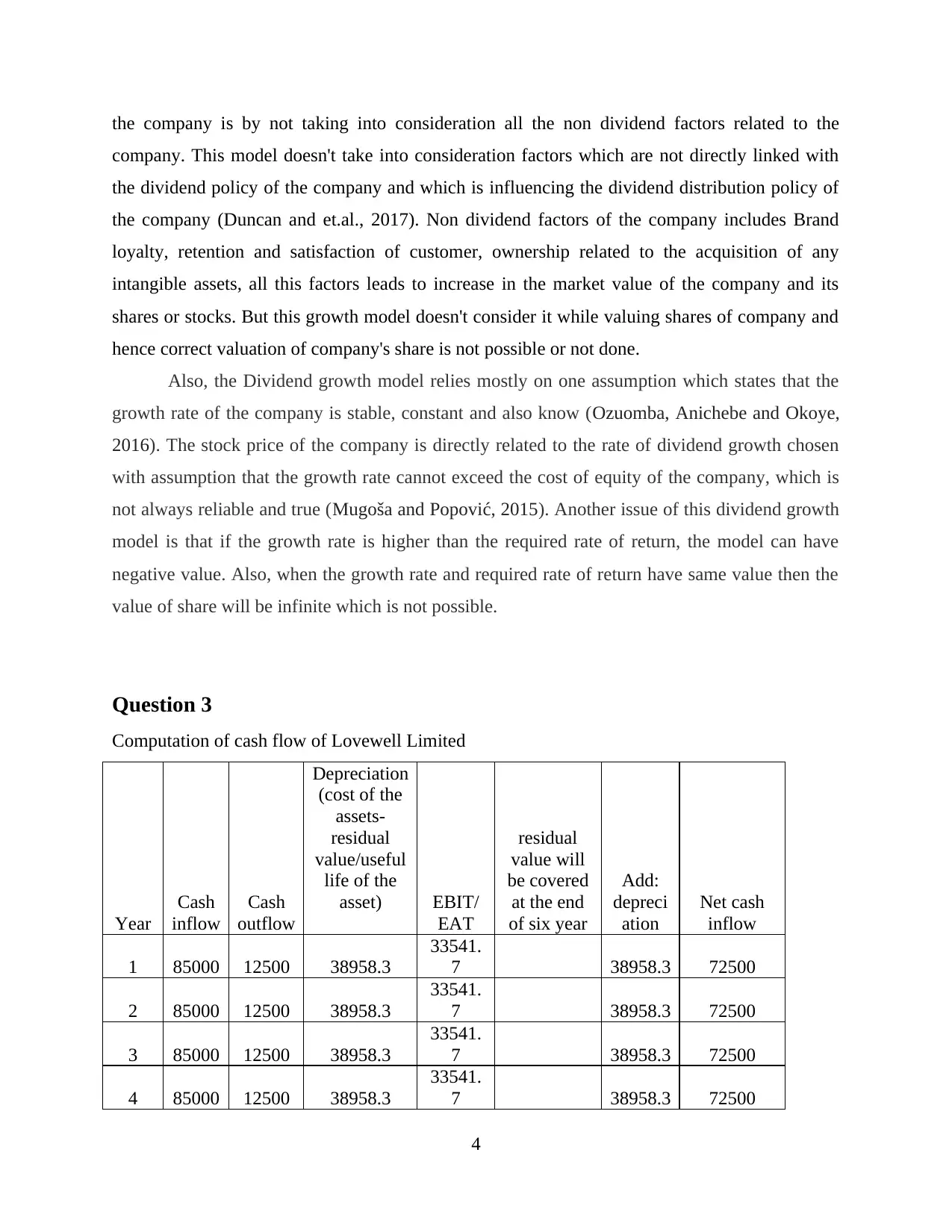

Question 3

Computation of cash flow of Lovewell Limited

Year

Cash

inflow

Cash

outflow

Depreciation

(cost of the

assets-

residual

value/useful

life of the

asset) EBIT/

EAT

residual

value will

be covered

at the end

of six year

Add:

depreci

ation

Net cash

inflow

1 85000 12500 38958.3

33541.

7 38958.3 72500

2 85000 12500 38958.3

33541.

7 38958.3 72500

3 85000 12500 38958.3

33541.

7 38958.3 72500

4 85000 12500 38958.3

33541.

7 38958.3 72500

4

company. This model doesn't take into consideration factors which are not directly linked with

the dividend policy of the company and which is influencing the dividend distribution policy of

the company (Duncan and et.al., 2017). Non dividend factors of the company includes Brand

loyalty, retention and satisfaction of customer, ownership related to the acquisition of any

intangible assets, all this factors leads to increase in the market value of the company and its

shares or stocks. But this growth model doesn't consider it while valuing shares of company and

hence correct valuation of company's share is not possible or not done.

Also, the Dividend growth model relies mostly on one assumption which states that the

growth rate of the company is stable, constant and also know (Ozuomba, Anichebe and Okoye,

2016). The stock price of the company is directly related to the rate of dividend growth chosen

with assumption that the growth rate cannot exceed the cost of equity of the company, which is

not always reliable and true (Mugoša and Popović, 2015). Another issue of this dividend growth

model is that if the growth rate is higher than the required rate of return, the model can have

negative value. Also, when the growth rate and required rate of return have same value then the

value of share will be infinite which is not possible.

Question 3

Computation of cash flow of Lovewell Limited

Year

Cash

inflow

Cash

outflow

Depreciation

(cost of the

assets-

residual

value/useful

life of the

asset) EBIT/

EAT

residual

value will

be covered

at the end

of six year

Add:

depreci

ation

Net cash

inflow

1 85000 12500 38958.3

33541.

7 38958.3 72500

2 85000 12500 38958.3

33541.

7 38958.3 72500

3 85000 12500 38958.3

33541.

7 38958.3 72500

4 85000 12500 38958.3

33541.

7 38958.3 72500

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 85000 12500 38958.3

33541.

7 38958.3 72500

6 85000 12500 38958.3

33541.

7 41250 38958.3 113750

Interpretation- From the table the calculation relating to the cash flow is made where

the cash outflows are deducted from the cash inflows after making adjustments regarding the

depreciation. Earning after tax is evaluated as the deducting the depreciation from the cash

outflows then the cash outflows are subtracted from cash inflows. After this the depreciation

amount is added to the earnings for ascertaining the net cash inflows equates to $72500 for 5

years and in the end of the sixth year due to the addition of the residual value the amount resulted

as $113750.

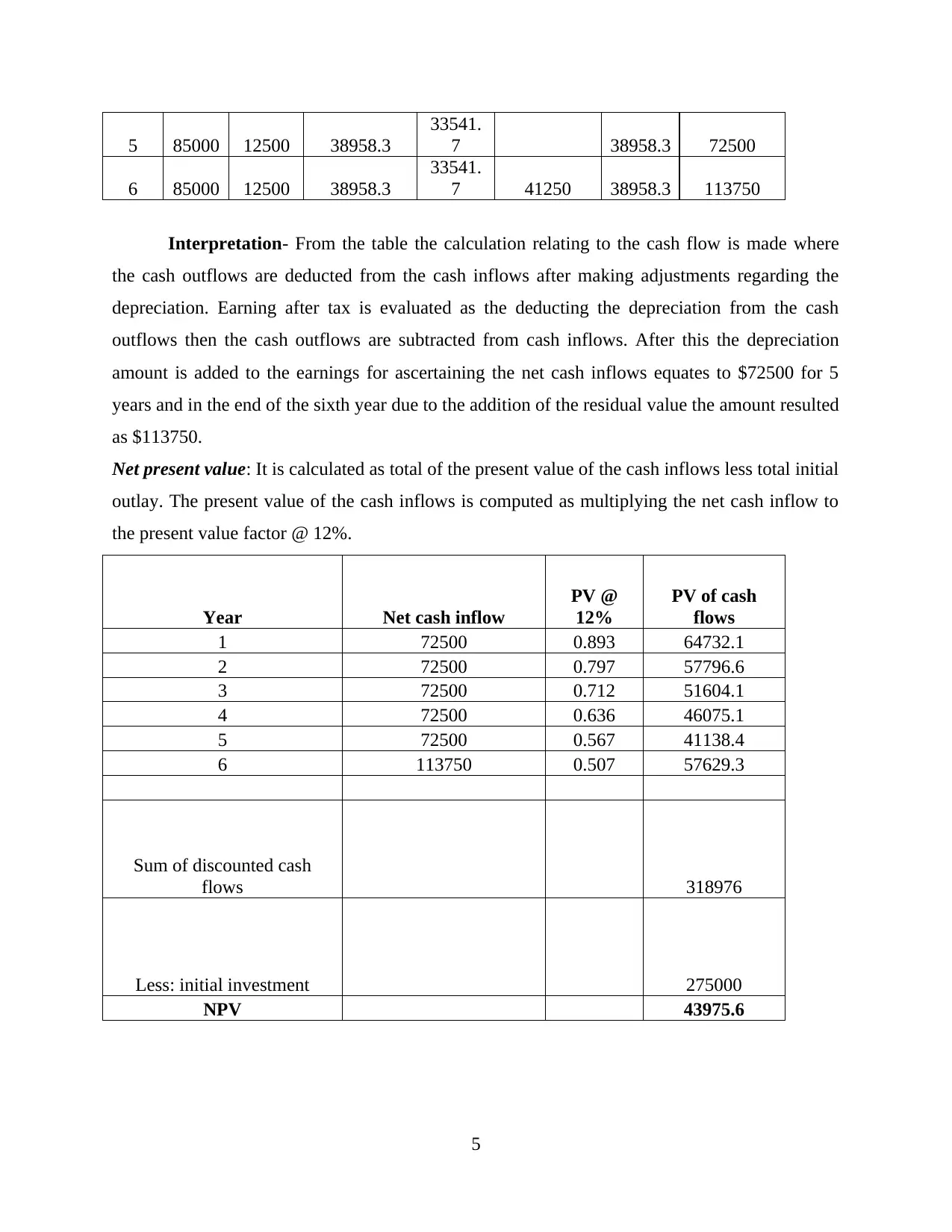

Net present value: It is calculated as total of the present value of the cash inflows less total initial

outlay. The present value of the cash inflows is computed as multiplying the net cash inflow to

the present value factor @ 12%.

Year Net cash inflow

PV @

12%

PV of cash

flows

1 72500 0.893 64732.1

2 72500 0.797 57796.6

3 72500 0.712 51604.1

4 72500 0.636 46075.1

5 72500 0.567 41138.4

6 113750 0.507 57629.3

Sum of discounted cash

flows 318976

Less: initial investment 275000

NPV 43975.6

5

33541.

7 38958.3 72500

6 85000 12500 38958.3

33541.

7 41250 38958.3 113750

Interpretation- From the table the calculation relating to the cash flow is made where

the cash outflows are deducted from the cash inflows after making adjustments regarding the

depreciation. Earning after tax is evaluated as the deducting the depreciation from the cash

outflows then the cash outflows are subtracted from cash inflows. After this the depreciation

amount is added to the earnings for ascertaining the net cash inflows equates to $72500 for 5

years and in the end of the sixth year due to the addition of the residual value the amount resulted

as $113750.

Net present value: It is calculated as total of the present value of the cash inflows less total initial

outlay. The present value of the cash inflows is computed as multiplying the net cash inflow to

the present value factor @ 12%.

Year Net cash inflow

PV @

12%

PV of cash

flows

1 72500 0.893 64732.1

2 72500 0.797 57796.6

3 72500 0.712 51604.1

4 72500 0.636 46075.1

5 72500 0.567 41138.4

6 113750 0.507 57629.3

Sum of discounted cash

flows 318976

Less: initial investment 275000

NPV 43975.6

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- The above table reflects the positive net present value which indicates that the

project will generate greater profits. Thus, the economic feasibility of the project of the Lovewell

is stating a positive return.

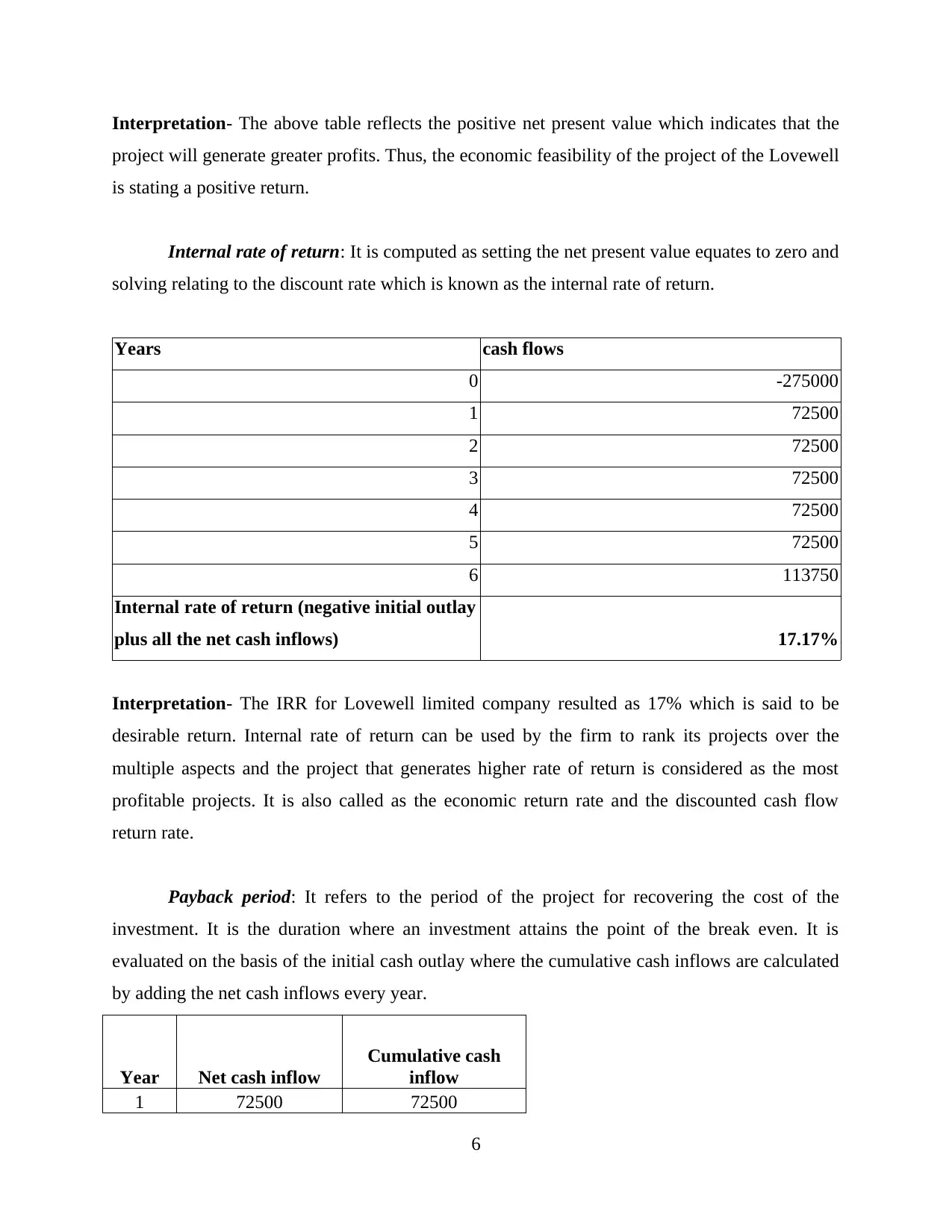

Internal rate of return: It is computed as setting the net present value equates to zero and

solving relating to the discount rate which is known as the internal rate of return.

Years cash flows

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

Internal rate of return (negative initial outlay

plus all the net cash inflows) 17.17%

Interpretation- The IRR for Lovewell limited company resulted as 17% which is said to be

desirable return. Internal rate of return can be used by the firm to rank its projects over the

multiple aspects and the project that generates higher rate of return is considered as the most

profitable projects. It is also called as the economic return rate and the discounted cash flow

return rate.

Payback period: It refers to the period of the project for recovering the cost of the

investment. It is the duration where an investment attains the point of the break even. It is

evaluated on the basis of the initial cash outlay where the cumulative cash inflows are calculated

by adding the net cash inflows every year.

Year Net cash inflow

Cumulative cash

inflow

1 72500 72500

6

project will generate greater profits. Thus, the economic feasibility of the project of the Lovewell

is stating a positive return.

Internal rate of return: It is computed as setting the net present value equates to zero and

solving relating to the discount rate which is known as the internal rate of return.

Years cash flows

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

Internal rate of return (negative initial outlay

plus all the net cash inflows) 17.17%

Interpretation- The IRR for Lovewell limited company resulted as 17% which is said to be

desirable return. Internal rate of return can be used by the firm to rank its projects over the

multiple aspects and the project that generates higher rate of return is considered as the most

profitable projects. It is also called as the economic return rate and the discounted cash flow

return rate.

Payback period: It refers to the period of the project for recovering the cost of the

investment. It is the duration where an investment attains the point of the break even. It is

evaluated on the basis of the initial cash outlay where the cumulative cash inflows are calculated

by adding the net cash inflows every year.

Year Net cash inflow

Cumulative cash

inflow

1 72500 72500

6

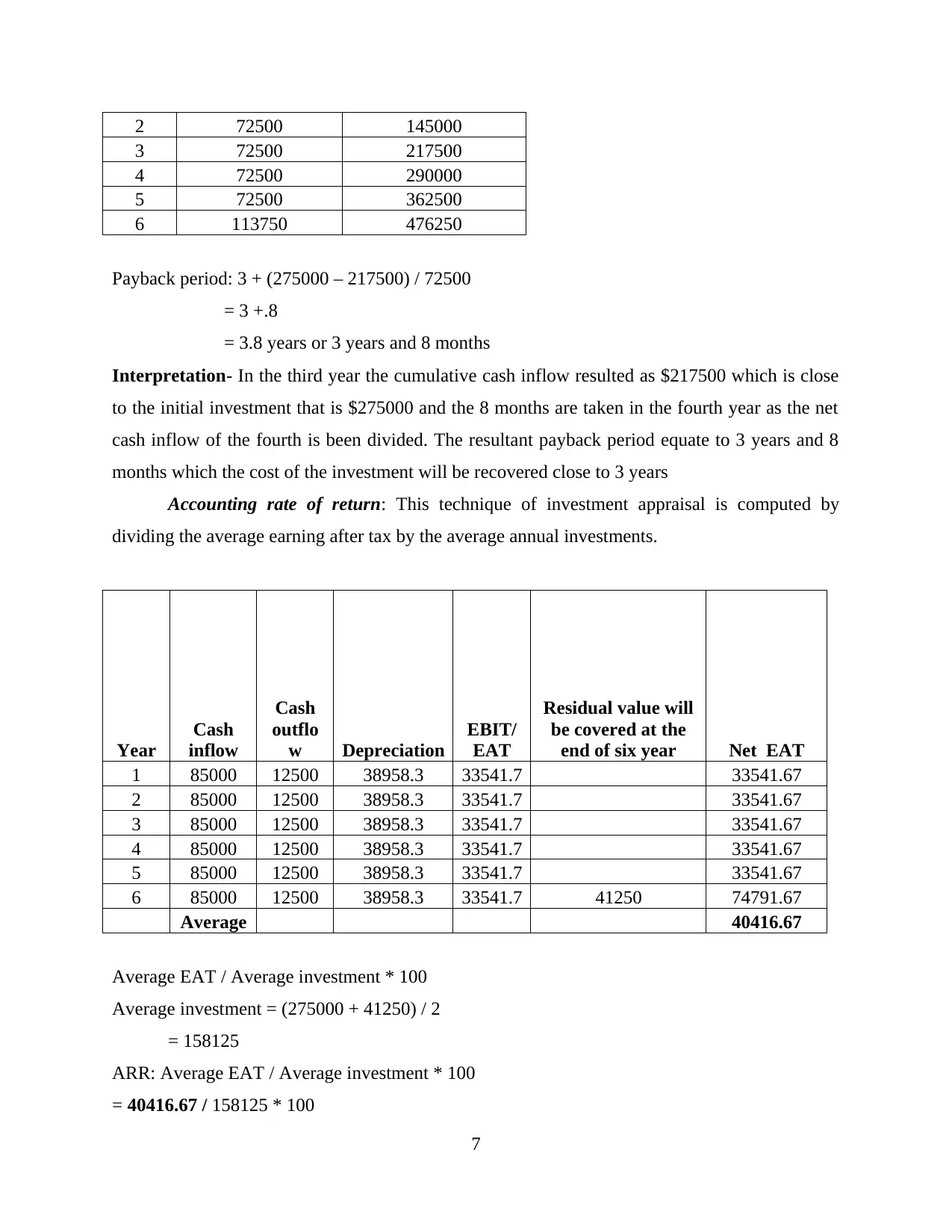

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 113750 476250

Payback period: 3 + (275000 – 217500) / 72500

= 3 +.8

= 3.8 years or 3 years and 8 months

Interpretation- In the third year the cumulative cash inflow resulted as $217500 which is close

to the initial investment that is $275000 and the 8 months are taken in the fourth year as the net

cash inflow of the fourth is been divided. The resultant payback period equate to 3 years and 8

months which the cost of the investment will be recovered close to 3 years

Accounting rate of return: This technique of investment appraisal is computed by

dividing the average earning after tax by the average annual investments.

Year

Cash

inflow

Cash

outflo

w Depreciation

EBIT/

EAT

Residual value will

be covered at the

end of six year Net EAT

1 85000 12500 38958.3 33541.7 33541.67

2 85000 12500 38958.3 33541.7 33541.67

3 85000 12500 38958.3 33541.7 33541.67

4 85000 12500 38958.3 33541.7 33541.67

5 85000 12500 38958.3 33541.7 33541.67

6 85000 12500 38958.3 33541.7 41250 74791.67

Average 40416.67

Average EAT / Average investment * 100

Average investment = (275000 + 41250) / 2

= 158125

ARR: Average EAT / Average investment * 100

= 40416.67 / 158125 * 100

7

3 72500 217500

4 72500 290000

5 72500 362500

6 113750 476250

Payback period: 3 + (275000 – 217500) / 72500

= 3 +.8

= 3.8 years or 3 years and 8 months

Interpretation- In the third year the cumulative cash inflow resulted as $217500 which is close

to the initial investment that is $275000 and the 8 months are taken in the fourth year as the net

cash inflow of the fourth is been divided. The resultant payback period equate to 3 years and 8

months which the cost of the investment will be recovered close to 3 years

Accounting rate of return: This technique of investment appraisal is computed by

dividing the average earning after tax by the average annual investments.

Year

Cash

inflow

Cash

outflo

w Depreciation

EBIT/

EAT

Residual value will

be covered at the

end of six year Net EAT

1 85000 12500 38958.3 33541.7 33541.67

2 85000 12500 38958.3 33541.7 33541.67

3 85000 12500 38958.3 33541.7 33541.67

4 85000 12500 38958.3 33541.7 33541.67

5 85000 12500 38958.3 33541.7 33541.67

6 85000 12500 38958.3 33541.7 41250 74791.67

Average 40416.67

Average EAT / Average investment * 100

Average investment = (275000 + 41250) / 2

= 158125

ARR: Average EAT / Average investment * 100

= 40416.67 / 158125 * 100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

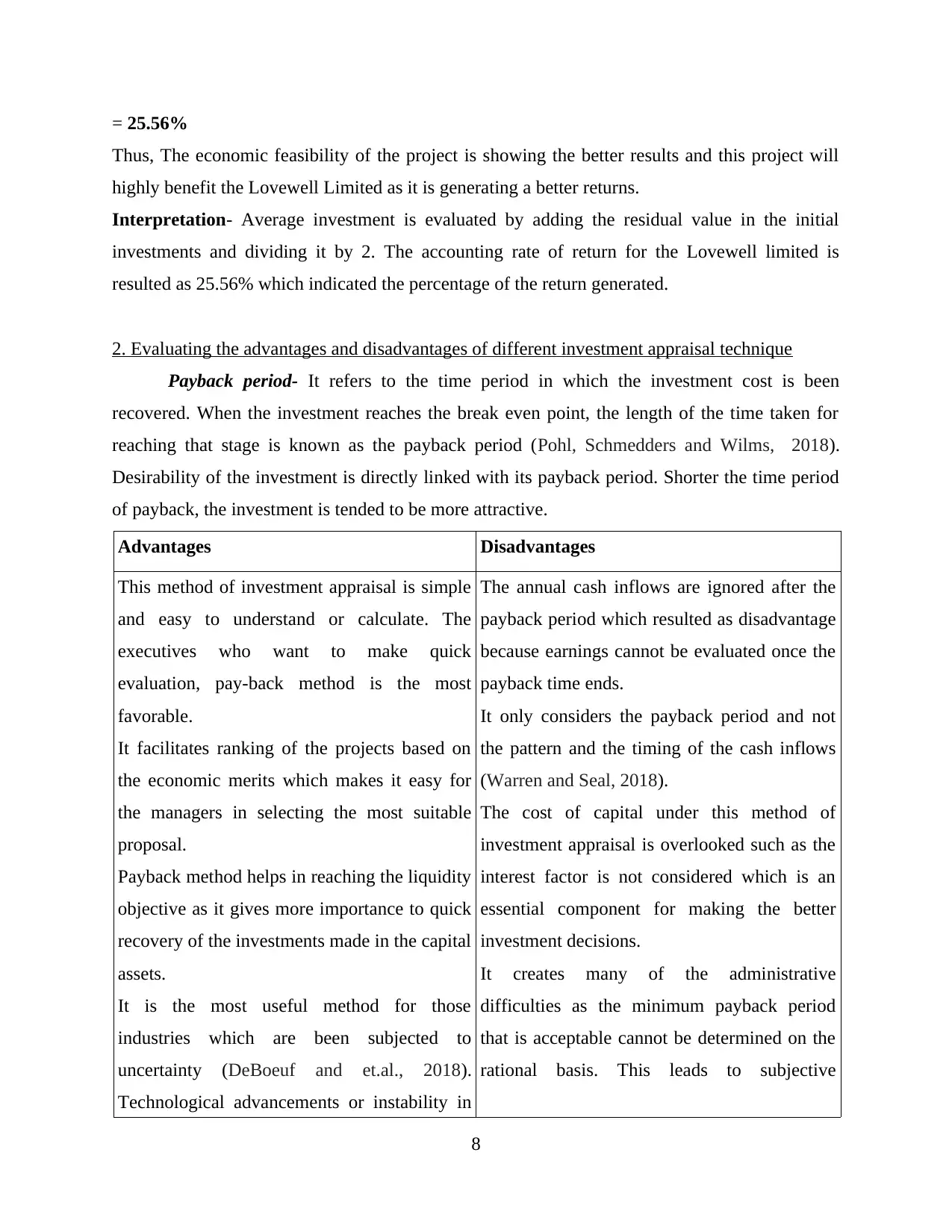

= 25.56%

Thus, The economic feasibility of the project is showing the better results and this project will

highly benefit the Lovewell Limited as it is generating a better returns.

Interpretation- Average investment is evaluated by adding the residual value in the initial

investments and dividing it by 2. The accounting rate of return for the Lovewell limited is

resulted as 25.56% which indicated the percentage of the return generated.

2. Evaluating the advantages and disadvantages of different investment appraisal technique

Payback period- It refers to the time period in which the investment cost is been

recovered. When the investment reaches the break even point, the length of the time taken for

reaching that stage is known as the payback period (Pohl, Schmedders and Wilms, 2018).

Desirability of the investment is directly linked with its payback period. Shorter the time period

of payback, the investment is tended to be more attractive.

Advantages Disadvantages

This method of investment appraisal is simple

and easy to understand or calculate. The

executives who want to make quick

evaluation, pay-back method is the most

favorable.

It facilitates ranking of the projects based on

the economic merits which makes it easy for

the managers in selecting the most suitable

proposal.

Payback method helps in reaching the liquidity

objective as it gives more importance to quick

recovery of the investments made in the capital

assets.

It is the most useful method for those

industries which are been subjected to

uncertainty (DeBoeuf and et.al., 2018).

Technological advancements or instability in

The annual cash inflows are ignored after the

payback period which resulted as disadvantage

because earnings cannot be evaluated once the

payback time ends.

It only considers the payback period and not

the pattern and the timing of the cash inflows

(Warren and Seal, 2018).

The cost of capital under this method of

investment appraisal is overlooked such as the

interest factor is not considered which is an

essential component for making the better

investment decisions.

It creates many of the administrative

difficulties as the minimum payback period

that is acceptable cannot be determined on the

rational basis. This leads to subjective

8

Thus, The economic feasibility of the project is showing the better results and this project will

highly benefit the Lovewell Limited as it is generating a better returns.

Interpretation- Average investment is evaluated by adding the residual value in the initial

investments and dividing it by 2. The accounting rate of return for the Lovewell limited is

resulted as 25.56% which indicated the percentage of the return generated.

2. Evaluating the advantages and disadvantages of different investment appraisal technique

Payback period- It refers to the time period in which the investment cost is been

recovered. When the investment reaches the break even point, the length of the time taken for

reaching that stage is known as the payback period (Pohl, Schmedders and Wilms, 2018).

Desirability of the investment is directly linked with its payback period. Shorter the time period

of payback, the investment is tended to be more attractive.

Advantages Disadvantages

This method of investment appraisal is simple

and easy to understand or calculate. The

executives who want to make quick

evaluation, pay-back method is the most

favorable.

It facilitates ranking of the projects based on

the economic merits which makes it easy for

the managers in selecting the most suitable

proposal.

Payback method helps in reaching the liquidity

objective as it gives more importance to quick

recovery of the investments made in the capital

assets.

It is the most useful method for those

industries which are been subjected to

uncertainty (DeBoeuf and et.al., 2018).

Technological advancements or instability in

The annual cash inflows are ignored after the

payback period which resulted as disadvantage

because earnings cannot be evaluated once the

payback time ends.

It only considers the payback period and not

the pattern and the timing of the cash inflows

(Warren and Seal, 2018).

The cost of capital under this method of

investment appraisal is overlooked such as the

interest factor is not considered which is an

essential component for making the better

investment decisions.

It creates many of the administrative

difficulties as the minimum payback period

that is acceptable cannot be determined on the

rational basis. This leads to subjective

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the industries due to the future uncertain event

do not permit for the anticipation of the yearly

cash inflows after a limited time period.

Payback method reduces the chances of loss

caused due to obsolescence.

decisions of the management.

Slight changes in the cost of the operation

might affect the inflow of cash. By this it is

depicted that payback method is rigid and

delicate in nature.

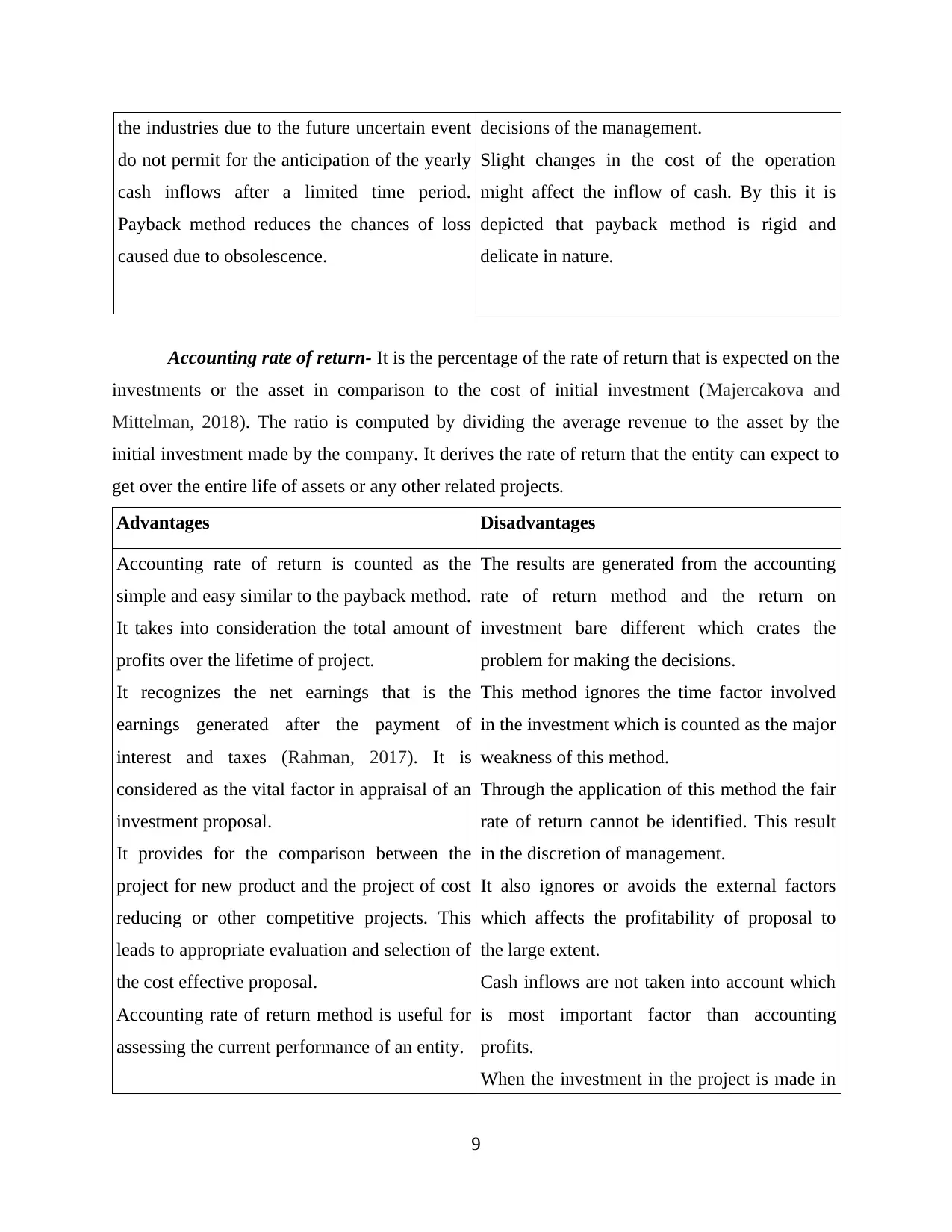

Accounting rate of return- It is the percentage of the rate of return that is expected on the

investments or the asset in comparison to the cost of initial investment (Majercakova and

Mittelman, 2018). The ratio is computed by dividing the average revenue to the asset by the

initial investment made by the company. It derives the rate of return that the entity can expect to

get over the entire life of assets or any other related projects.

Advantages Disadvantages

Accounting rate of return is counted as the

simple and easy similar to the payback method.

It takes into consideration the total amount of

profits over the lifetime of project.

It recognizes the net earnings that is the

earnings generated after the payment of

interest and taxes (Rahman, 2017). It is

considered as the vital factor in appraisal of an

investment proposal.

It provides for the comparison between the

project for new product and the project of cost

reducing or other competitive projects. This

leads to appropriate evaluation and selection of

the cost effective proposal.

Accounting rate of return method is useful for

assessing the current performance of an entity.

The results are generated from the accounting

rate of return method and the return on

investment bare different which crates the

problem for making the decisions.

This method ignores the time factor involved

in the investment which is counted as the major

weakness of this method.

Through the application of this method the fair

rate of return cannot be identified. This result

in the discretion of management.

It also ignores or avoids the external factors

which affects the profitability of proposal to

the large extent.

Cash inflows are not taken into account which

is most important factor than accounting

profits.

When the investment in the project is made in

9

do not permit for the anticipation of the yearly

cash inflows after a limited time period.

Payback method reduces the chances of loss

caused due to obsolescence.

decisions of the management.

Slight changes in the cost of the operation

might affect the inflow of cash. By this it is

depicted that payback method is rigid and

delicate in nature.

Accounting rate of return- It is the percentage of the rate of return that is expected on the

investments or the asset in comparison to the cost of initial investment (Majercakova and

Mittelman, 2018). The ratio is computed by dividing the average revenue to the asset by the

initial investment made by the company. It derives the rate of return that the entity can expect to

get over the entire life of assets or any other related projects.

Advantages Disadvantages

Accounting rate of return is counted as the

simple and easy similar to the payback method.

It takes into consideration the total amount of

profits over the lifetime of project.

It recognizes the net earnings that is the

earnings generated after the payment of

interest and taxes (Rahman, 2017). It is

considered as the vital factor in appraisal of an

investment proposal.

It provides for the comparison between the

project for new product and the project of cost

reducing or other competitive projects. This

leads to appropriate evaluation and selection of

the cost effective proposal.

Accounting rate of return method is useful for

assessing the current performance of an entity.

The results are generated from the accounting

rate of return method and the return on

investment bare different which crates the

problem for making the decisions.

This method ignores the time factor involved

in the investment which is counted as the major

weakness of this method.

Through the application of this method the fair

rate of return cannot be identified. This result

in the discretion of management.

It also ignores or avoids the external factors

which affects the profitability of proposal to

the large extent.

Cash inflows are not taken into account which

is most important factor than accounting

profits.

When the investment in the project is made in

9

parts, then this method cannot be applied.

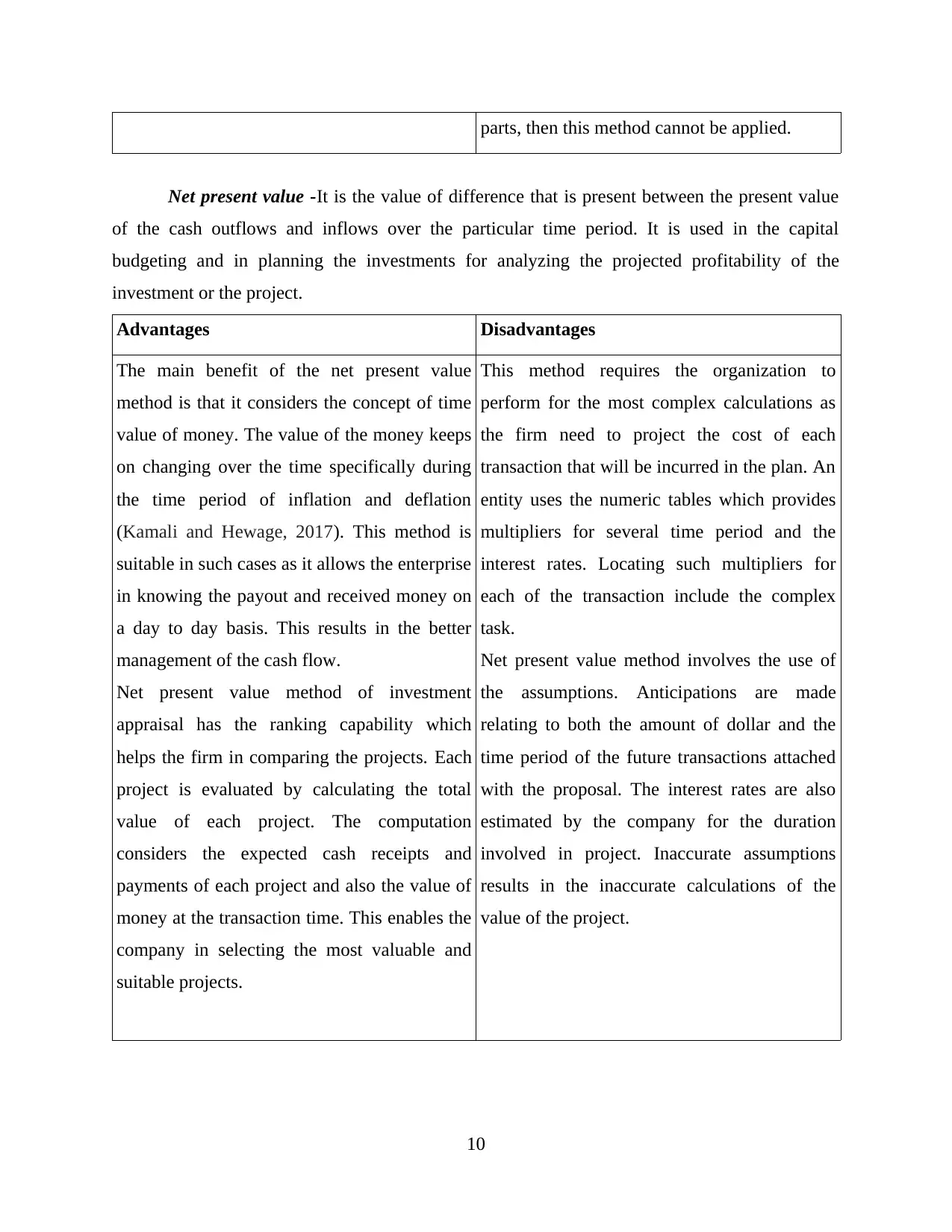

Net present value -It is the value of difference that is present between the present value

of the cash outflows and inflows over the particular time period. It is used in the capital

budgeting and in planning the investments for analyzing the projected profitability of the

investment or the project.

Advantages Disadvantages

The main benefit of the net present value

method is that it considers the concept of time

value of money. The value of the money keeps

on changing over the time specifically during

the time period of inflation and deflation

(Kamali and Hewage, 2017). This method is

suitable in such cases as it allows the enterprise

in knowing the payout and received money on

a day to day basis. This results in the better

management of the cash flow.

Net present value method of investment

appraisal has the ranking capability which

helps the firm in comparing the projects. Each

project is evaluated by calculating the total

value of each project. The computation

considers the expected cash receipts and

payments of each project and also the value of

money at the transaction time. This enables the

company in selecting the most valuable and

suitable projects.

This method requires the organization to

perform for the most complex calculations as

the firm need to project the cost of each

transaction that will be incurred in the plan. An

entity uses the numeric tables which provides

multipliers for several time period and the

interest rates. Locating such multipliers for

each of the transaction include the complex

task.

Net present value method involves the use of

the assumptions. Anticipations are made

relating to both the amount of dollar and the

time period of the future transactions attached

with the proposal. The interest rates are also

estimated by the company for the duration

involved in project. Inaccurate assumptions

results in the inaccurate calculations of the

value of the project.

10

Net present value -It is the value of difference that is present between the present value

of the cash outflows and inflows over the particular time period. It is used in the capital

budgeting and in planning the investments for analyzing the projected profitability of the

investment or the project.

Advantages Disadvantages

The main benefit of the net present value

method is that it considers the concept of time

value of money. The value of the money keeps

on changing over the time specifically during

the time period of inflation and deflation

(Kamali and Hewage, 2017). This method is

suitable in such cases as it allows the enterprise

in knowing the payout and received money on

a day to day basis. This results in the better

management of the cash flow.

Net present value method of investment

appraisal has the ranking capability which

helps the firm in comparing the projects. Each

project is evaluated by calculating the total

value of each project. The computation

considers the expected cash receipts and

payments of each project and also the value of

money at the transaction time. This enables the

company in selecting the most valuable and

suitable projects.

This method requires the organization to

perform for the most complex calculations as

the firm need to project the cost of each

transaction that will be incurred in the plan. An

entity uses the numeric tables which provides

multipliers for several time period and the

interest rates. Locating such multipliers for

each of the transaction include the complex

task.

Net present value method involves the use of

the assumptions. Anticipations are made

relating to both the amount of dollar and the

time period of the future transactions attached

with the proposal. The interest rates are also

estimated by the company for the duration

involved in project. Inaccurate assumptions

results in the inaccurate calculations of the

value of the project.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.