Financial Analysis: Smart Safety Break-Even and Production Variance

VerifiedAdded on 2020/03/23

|4

|445

|49

Report

AI Summary

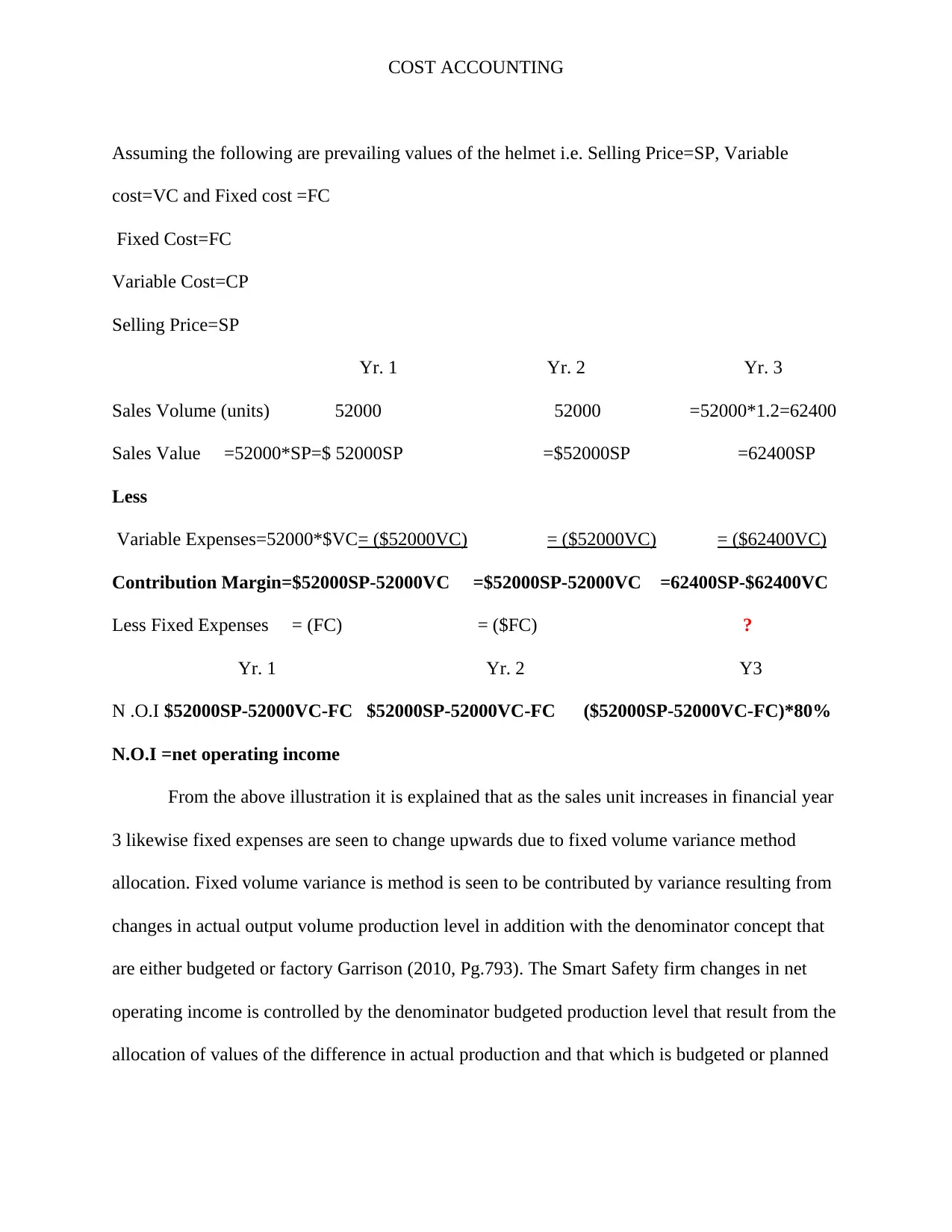

This report provides a financial analysis of Smart Safety, focusing on break-even points and production volume variance. It examines the impact of fixed and variable costs on the company's net operating income. The analysis highlights how changes in production volume affect the allocation of fixed overhead costs, influencing the break-even point. The report references relevant literature to support its findings, including the works of Garrison et al. (2010) and Roth (2008). The conclusion emphasizes the significance of the budgeted production level method in allocating fixed overheads and its effect on net income, even when sales and other factors remain constant. The report suggests that the increase in actual production from 52,000 to 62,400 units resulted in a favorable volume variance, but this also impacted the net operating income due to changes in the fixed cost allocation. The report is a great resource for students who need help with similar assignments.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.