Corporate Accounting: Analyzing Flight Centre and Webjet Financials

VerifiedAdded on 2020/10/22

|18

|4388

|122

Report

AI Summary

This report offers a comparative analysis of the financial statements of Flight Centre Travel Limited and Webjet Limited, both prominent companies in the travel and tourism industry. The analysis encompasses a range of financial aspects, including the examination of owners' equity, debt and equity positions, and cash flow statements. It also delves into the components of other comprehensive income statements and the reasons for their exclusion from profit and loss accounts. Furthermore, the report explores corporate income tax accounting, including effective tax rate calculations, deferred tax assets and liabilities, and the reconciliation of book and cash tax amounts. The comparative study provides insights into the financial health, investment strategies, and operational efficiency of both companies, highlighting their expansion phases, saturation stages, and risk profiles, along with a detailed interpretation of their financial performance over a three-year period.

CORPORATE

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report is presenting comparison of Financial Statements of two companies, Flight

Centre Travel Limited and Webjet Limited. These both companies are involved in travel and

tourism business. This report presents different items of Balance sheets, comparison of

borrowings with owner’s funds, benefits and uses of cash flow statements, comparison of cash

tax with book tax amount.

This report is presenting comparison of Financial Statements of two companies, Flight

Centre Travel Limited and Webjet Limited. These both companies are involved in travel and

tourism business. This report presents different items of Balance sheets, comparison of

borrowings with owner’s funds, benefits and uses of cash flow statements, comparison of cash

tax with book tax amount.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Owners’ Equity................................................................................................................................1

(i)The Items of Equity listed in Financial Statements and understanding of both companies-:. 1

The statement of changes in equity of both companies are given below-:.............................2

(ii) Comparative Analysis of Debt and Equity Position........................................................2

Cash Flow Statement.......................................................................................................................3

(iii)List of items of Cash Flow Statements.............................................................................3

(iv)Comparative analysis of three activities of Cash Flow Statements for past three years-: 4

(v)Comparative Analysis of Cash Flow Statements of both companies................................5

OTHER COMPREHENSIVE INCOME STATEMENTS..............................................................6

(vi)Items that are needed to report In Comprehensive Income Statements............................6

(vii)Stating reasons for items of Comprehensive Income statements are not recorded in P&L 6

(viii)Comparative Analysis of Other Comprehensive Income Statements............................7

(ix)Evaluation with Inclusion of Items of Comprehensive Income Statements.....................7

Accounting for Corporate Income Tax............................................................................................8

(x)The Tax expenses that are shown in both of companies for current year-:.......................8

(xi)Calculation of Effective tax rate for both companies.......................................................8

(xii)Stating Reasons why Deferred tax Assets and Liabilities occurs....................................8

(xiii)There was increase in Deferred Tax Assets reported from last years for both of

companies-:.............................................................................................................................9

(xiv)Calculation of Cash tax amount by using book tax amount with help of Deferred Tax

Liability and Deferred Tax Assets given in Balance sheets of both companies..................10

(xv)Calculation of cash tax rate of both companies that are calculated after adjustment of

DTA are-:..............................................................................................................................11

(xvi)Reasons stating difference in Tax rate and Book Rate.................................................11

INTRODUCTION...........................................................................................................................1

Owners’ Equity................................................................................................................................1

(i)The Items of Equity listed in Financial Statements and understanding of both companies-:. 1

The statement of changes in equity of both companies are given below-:.............................2

(ii) Comparative Analysis of Debt and Equity Position........................................................2

Cash Flow Statement.......................................................................................................................3

(iii)List of items of Cash Flow Statements.............................................................................3

(iv)Comparative analysis of three activities of Cash Flow Statements for past three years-: 4

(v)Comparative Analysis of Cash Flow Statements of both companies................................5

OTHER COMPREHENSIVE INCOME STATEMENTS..............................................................6

(vi)Items that are needed to report In Comprehensive Income Statements............................6

(vii)Stating reasons for items of Comprehensive Income statements are not recorded in P&L 6

(viii)Comparative Analysis of Other Comprehensive Income Statements............................7

(ix)Evaluation with Inclusion of Items of Comprehensive Income Statements.....................7

Accounting for Corporate Income Tax............................................................................................8

(x)The Tax expenses that are shown in both of companies for current year-:.......................8

(xi)Calculation of Effective tax rate for both companies.......................................................8

(xii)Stating Reasons why Deferred tax Assets and Liabilities occurs....................................8

(xiii)There was increase in Deferred Tax Assets reported from last years for both of

companies-:.............................................................................................................................9

(xiv)Calculation of Cash tax amount by using book tax amount with help of Deferred Tax

Liability and Deferred Tax Assets given in Balance sheets of both companies..................10

(xv)Calculation of cash tax rate of both companies that are calculated after adjustment of

DTA are-:..............................................................................................................................11

(xvi)Reasons stating difference in Tax rate and Book Rate.................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

REFERENCES..............................................................................................................................13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Corporate accounting is that branch which deals with preparation of financial statements

which includes Profit and loss account, Balance Sheets, Cash Flow Statements, Statements of

Change in Equity (Schaltegger, 2017). The two companies which had been taken for

comparative analysis are operators of travel and tourism business, they are Flight Centre Travel

Group Limited and Web Jet Limited.

Webjet limited is an online travel agency that has operations in Australia and New

Zealand. It has been listed in Australia Securities Exchange from 18/12/1997 having a market

capital of $1999 million. The shares that are quoted in stock exchange are 101.1 million.

Flight Centre Travel Group Limited is a listed company in Australia Securities Exchange

has been doing principal business of leisure and corporate travels. They are having a market

capital of $5717 million and had been listed in exchange from 01/12/1995. The no. shares that

are quoted is stock exchange are 120.1 million.]

This reports consist of comparative study of companies which are stated above according

to their financial statements which will include Ratio analysis, comparison of book tax with cash

tax and many more.

Owners’ Equity

(i)The Items of Equity listed in Financial Statements and understanding of both companies-:

1. Capital- The capital is invested by owners of company to earn profits. They are economic

resource that are measured in terms of Money (Cao, 2015).

2. Reserves- These are provisions which are made for specific purpose for an unknown

expenditure that may arise in the future.

1. General Reserves-: They are accumulated profits which are yet to distributed to

shareholders.

2. Capital Reserves-: They are usually used in Long Term project. These reserves

also belong to shareholders but are not distributed to them.

3. Share Premium Reserves-: It is created when there is difference between face

value and issue value of shares.

3. Surplus- These are credit balances of P&L account in financial accounting. The surplus is

made after providing bonus, general reserves etc.

1

Corporate accounting is that branch which deals with preparation of financial statements

which includes Profit and loss account, Balance Sheets, Cash Flow Statements, Statements of

Change in Equity (Schaltegger, 2017). The two companies which had been taken for

comparative analysis are operators of travel and tourism business, they are Flight Centre Travel

Group Limited and Web Jet Limited.

Webjet limited is an online travel agency that has operations in Australia and New

Zealand. It has been listed in Australia Securities Exchange from 18/12/1997 having a market

capital of $1999 million. The shares that are quoted in stock exchange are 101.1 million.

Flight Centre Travel Group Limited is a listed company in Australia Securities Exchange

has been doing principal business of leisure and corporate travels. They are having a market

capital of $5717 million and had been listed in exchange from 01/12/1995. The no. shares that

are quoted is stock exchange are 120.1 million.]

This reports consist of comparative study of companies which are stated above according

to their financial statements which will include Ratio analysis, comparison of book tax with cash

tax and many more.

Owners’ Equity

(i)The Items of Equity listed in Financial Statements and understanding of both companies-:

1. Capital- The capital is invested by owners of company to earn profits. They are economic

resource that are measured in terms of Money (Cao, 2015).

2. Reserves- These are provisions which are made for specific purpose for an unknown

expenditure that may arise in the future.

1. General Reserves-: They are accumulated profits which are yet to distributed to

shareholders.

2. Capital Reserves-: They are usually used in Long Term project. These reserves

also belong to shareholders but are not distributed to them.

3. Share Premium Reserves-: It is created when there is difference between face

value and issue value of shares.

3. Surplus- These are credit balances of P&L account in financial accounting. The surplus is

made after providing bonus, general reserves etc.

1

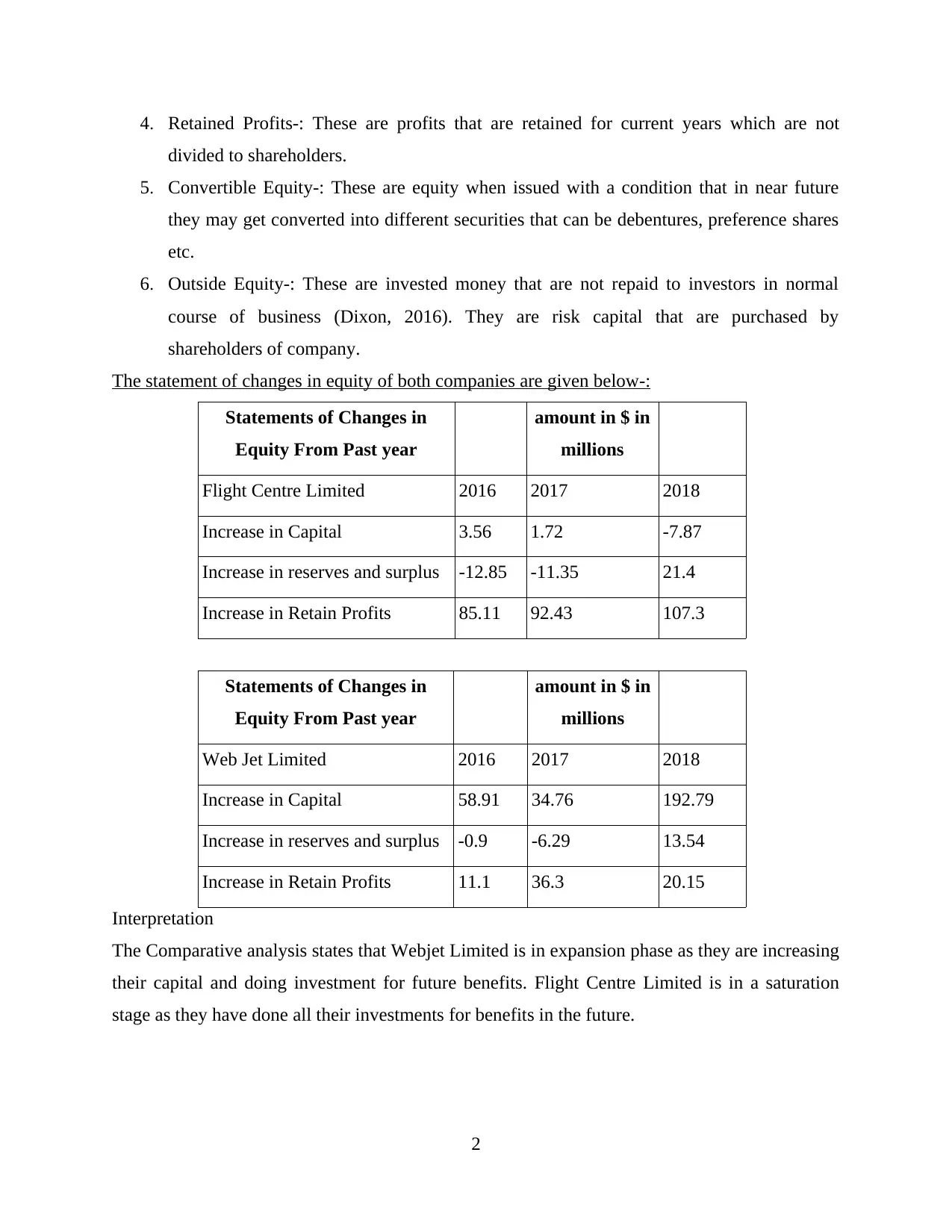

4. Retained Profits-: These are profits that are retained for current years which are not

divided to shareholders.

5. Convertible Equity-: These are equity when issued with a condition that in near future

they may get converted into different securities that can be debentures, preference shares

etc.

6. Outside Equity-: These are invested money that are not repaid to investors in normal

course of business (Dixon, 2016). They are risk capital that are purchased by

shareholders of company.

The statement of changes in equity of both companies are given below-:

Statements of Changes in

Equity From Past year

amount in $ in

millions

Flight Centre Limited 2016 2017 2018

Increase in Capital 3.56 1.72 -7.87

Increase in reserves and surplus -12.85 -11.35 21.4

Increase in Retain Profits 85.11 92.43 107.3

Statements of Changes in

Equity From Past year

amount in $ in

millions

Web Jet Limited 2016 2017 2018

Increase in Capital 58.91 34.76 192.79

Increase in reserves and surplus -0.9 -6.29 13.54

Increase in Retain Profits 11.1 36.3 20.15

Interpretation

The Comparative analysis states that Webjet Limited is in expansion phase as they are increasing

their capital and doing investment for future benefits. Flight Centre Limited is in a saturation

stage as they have done all their investments for benefits in the future.

2

divided to shareholders.

5. Convertible Equity-: These are equity when issued with a condition that in near future

they may get converted into different securities that can be debentures, preference shares

etc.

6. Outside Equity-: These are invested money that are not repaid to investors in normal

course of business (Dixon, 2016). They are risk capital that are purchased by

shareholders of company.

The statement of changes in equity of both companies are given below-:

Statements of Changes in

Equity From Past year

amount in $ in

millions

Flight Centre Limited 2016 2017 2018

Increase in Capital 3.56 1.72 -7.87

Increase in reserves and surplus -12.85 -11.35 21.4

Increase in Retain Profits 85.11 92.43 107.3

Statements of Changes in

Equity From Past year

amount in $ in

millions

Web Jet Limited 2016 2017 2018

Increase in Capital 58.91 34.76 192.79

Increase in reserves and surplus -0.9 -6.29 13.54

Increase in Retain Profits 11.1 36.3 20.15

Interpretation

The Comparative analysis states that Webjet Limited is in expansion phase as they are increasing

their capital and doing investment for future benefits. Flight Centre Limited is in a saturation

stage as they have done all their investments for benefits in the future.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

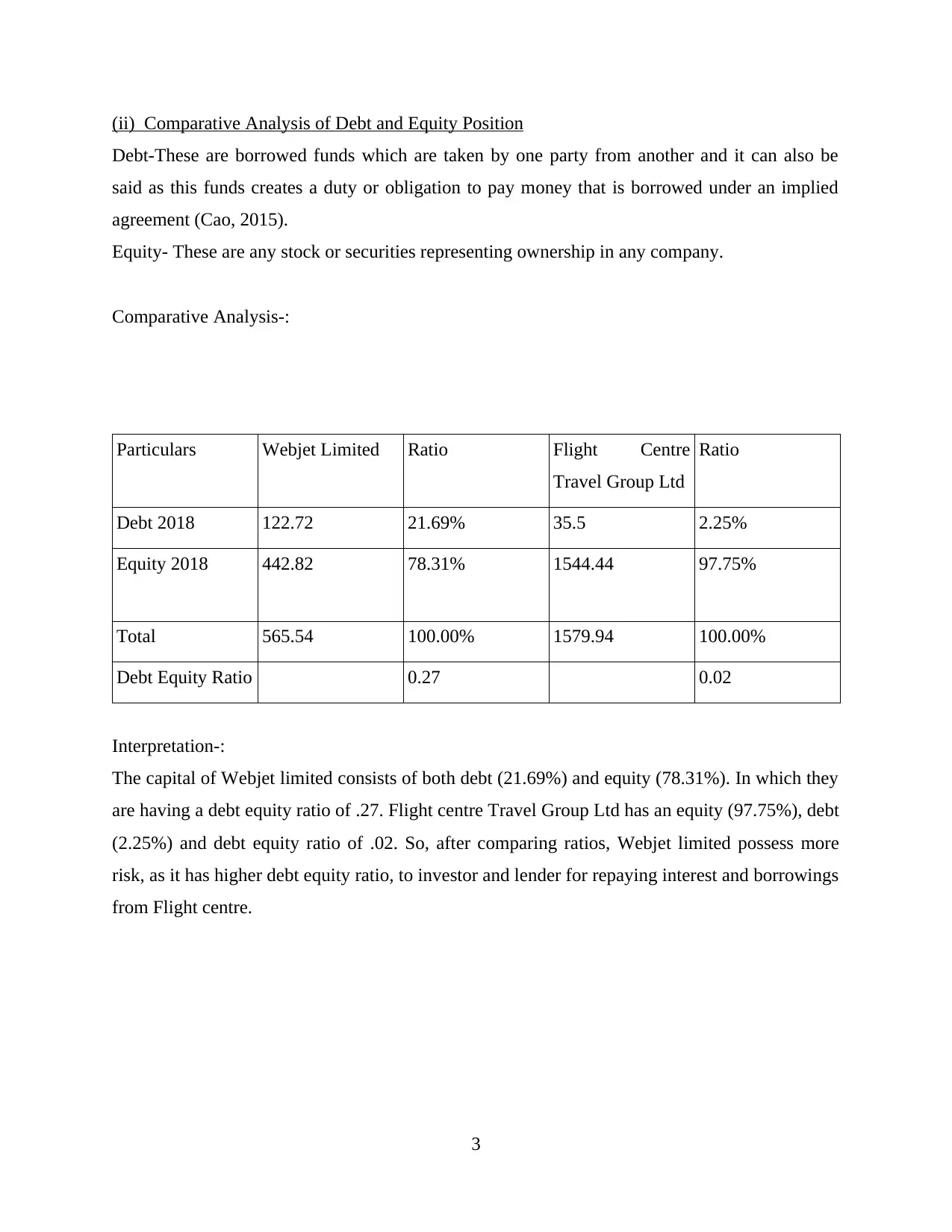

(ii) Comparative Analysis of Debt and Equity Position

Debt-These are borrowed funds which are taken by one party from another and it can also be

said as this funds creates a duty or obligation to pay money that is borrowed under an implied

agreement (Cao, 2015).

Equity- These are any stock or securities representing ownership in any company.

Comparative Analysis-:

Particulars Webjet Limited Ratio Flight Centre

Travel Group Ltd

Ratio

Debt 2018 122.72 21.69% 35.5 2.25%

Equity 2018 442.82 78.31% 1544.44 97.75%

Total 565.54 100.00% 1579.94 100.00%

Debt Equity Ratio 0.27 0.02

Interpretation-:

The capital of Webjet limited consists of both debt (21.69%) and equity (78.31%). In which they

are having a debt equity ratio of .27. Flight centre Travel Group Ltd has an equity (97.75%), debt

(2.25%) and debt equity ratio of .02. So, after comparing ratios, Webjet limited possess more

risk, as it has higher debt equity ratio, to investor and lender for repaying interest and borrowings

from Flight centre.

3

Debt-These are borrowed funds which are taken by one party from another and it can also be

said as this funds creates a duty or obligation to pay money that is borrowed under an implied

agreement (Cao, 2015).

Equity- These are any stock or securities representing ownership in any company.

Comparative Analysis-:

Particulars Webjet Limited Ratio Flight Centre

Travel Group Ltd

Ratio

Debt 2018 122.72 21.69% 35.5 2.25%

Equity 2018 442.82 78.31% 1544.44 97.75%

Total 565.54 100.00% 1579.94 100.00%

Debt Equity Ratio 0.27 0.02

Interpretation-:

The capital of Webjet limited consists of both debt (21.69%) and equity (78.31%). In which they

are having a debt equity ratio of .27. Flight centre Travel Group Ltd has an equity (97.75%), debt

(2.25%) and debt equity ratio of .02. So, after comparing ratios, Webjet limited possess more

risk, as it has higher debt equity ratio, to investor and lender for repaying interest and borrowings

from Flight centre.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

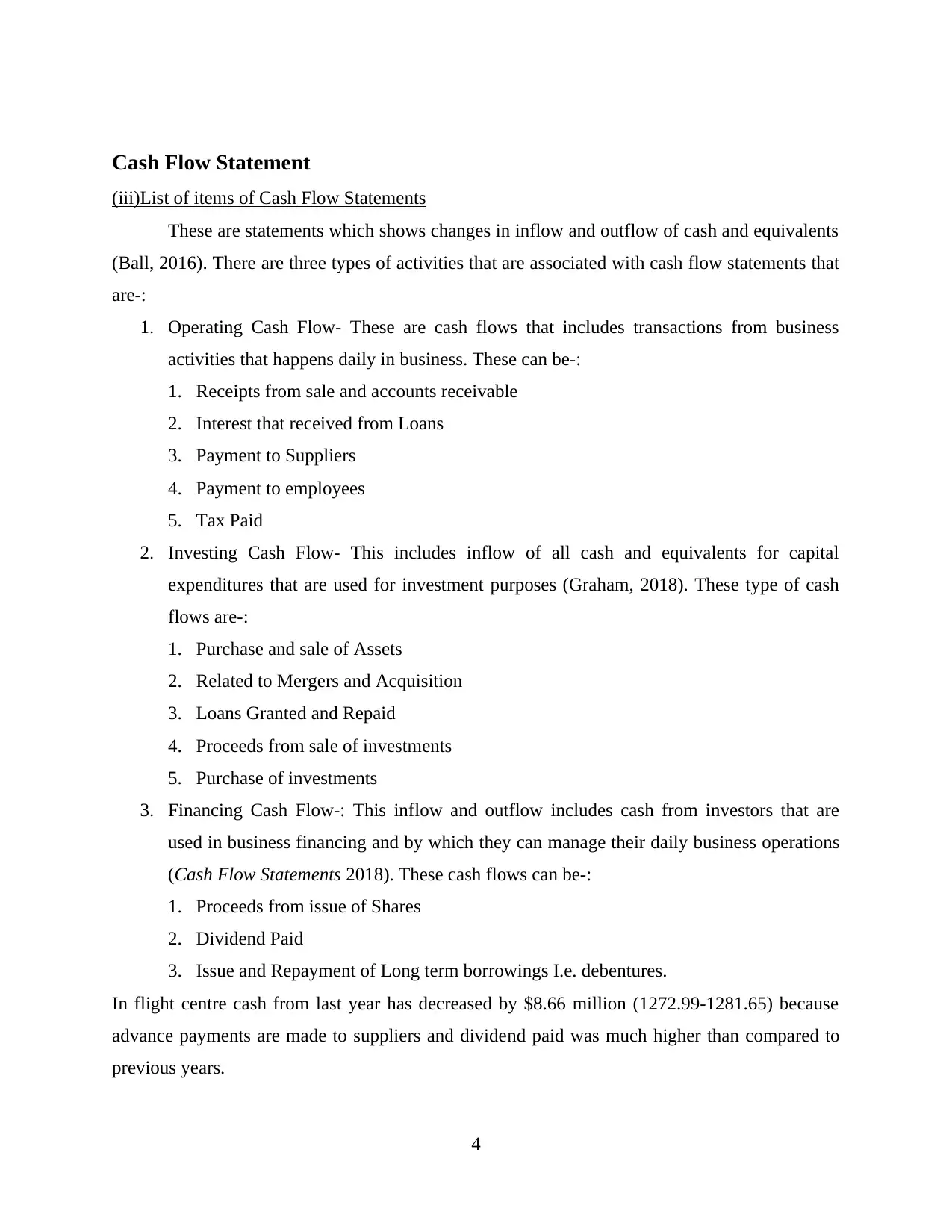

Cash Flow Statement

(iii)List of items of Cash Flow Statements

These are statements which shows changes in inflow and outflow of cash and equivalents

(Ball, 2016). There are three types of activities that are associated with cash flow statements that

are-:

1. Operating Cash Flow- These are cash flows that includes transactions from business

activities that happens daily in business. These can be-:

1. Receipts from sale and accounts receivable

2. Interest that received from Loans

3. Payment to Suppliers

4. Payment to employees

5. Tax Paid

2. Investing Cash Flow- This includes inflow of all cash and equivalents for capital

expenditures that are used for investment purposes (Graham, 2018). These type of cash

flows are-:

1. Purchase and sale of Assets

2. Related to Mergers and Acquisition

3. Loans Granted and Repaid

4. Proceeds from sale of investments

5. Purchase of investments

3. Financing Cash Flow-: This inflow and outflow includes cash from investors that are

used in business financing and by which they can manage their daily business operations

(Cash Flow Statements 2018). These cash flows can be-:

1. Proceeds from issue of Shares

2. Dividend Paid

3. Issue and Repayment of Long term borrowings I.e. debentures.

In flight centre cash from last year has decreased by $8.66 million (1272.99-1281.65) because

advance payments are made to suppliers and dividend paid was much higher than compared to

previous years.

4

(iii)List of items of Cash Flow Statements

These are statements which shows changes in inflow and outflow of cash and equivalents

(Ball, 2016). There are three types of activities that are associated with cash flow statements that

are-:

1. Operating Cash Flow- These are cash flows that includes transactions from business

activities that happens daily in business. These can be-:

1. Receipts from sale and accounts receivable

2. Interest that received from Loans

3. Payment to Suppliers

4. Payment to employees

5. Tax Paid

2. Investing Cash Flow- This includes inflow of all cash and equivalents for capital

expenditures that are used for investment purposes (Graham, 2018). These type of cash

flows are-:

1. Purchase and sale of Assets

2. Related to Mergers and Acquisition

3. Loans Granted and Repaid

4. Proceeds from sale of investments

5. Purchase of investments

3. Financing Cash Flow-: This inflow and outflow includes cash from investors that are

used in business financing and by which they can manage their daily business operations

(Cash Flow Statements 2018). These cash flows can be-:

1. Proceeds from issue of Shares

2. Dividend Paid

3. Issue and Repayment of Long term borrowings I.e. debentures.

In flight centre cash from last year has decreased by $8.66 million (1272.99-1281.65) because

advance payments are made to suppliers and dividend paid was much higher than compared to

previous years.

4

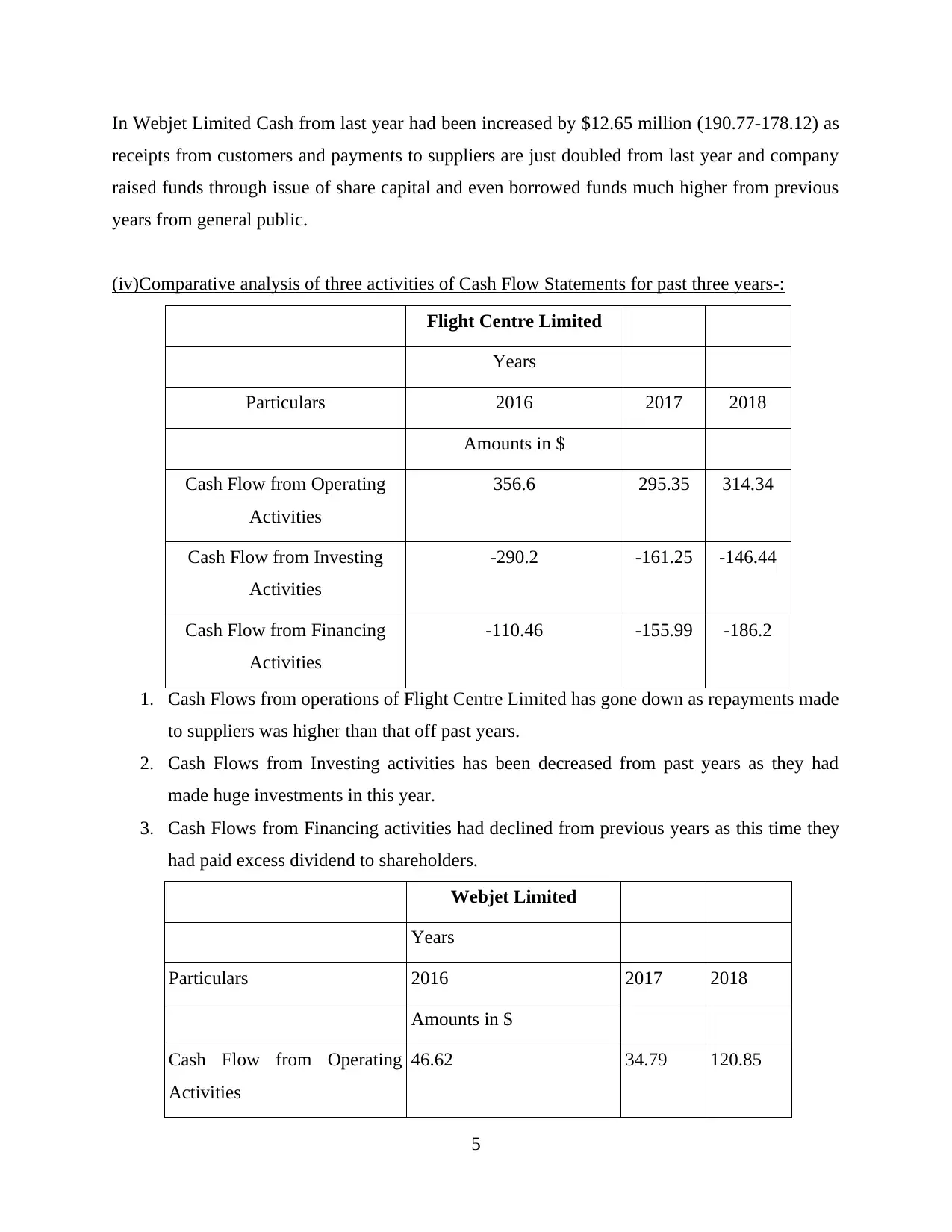

In Webjet Limited Cash from last year had been increased by $12.65 million (190.77-178.12) as

receipts from customers and payments to suppliers are just doubled from last year and company

raised funds through issue of share capital and even borrowed funds much higher from previous

years from general public.

(iv)Comparative analysis of three activities of Cash Flow Statements for past three years-:

Flight Centre Limited

Years

Particulars 2016 2017 2018

Amounts in $

Cash Flow from Operating

Activities

356.6 295.35 314.34

Cash Flow from Investing

Activities

-290.2 -161.25 -146.44

Cash Flow from Financing

Activities

-110.46 -155.99 -186.2

1. Cash Flows from operations of Flight Centre Limited has gone down as repayments made

to suppliers was higher than that off past years.

2. Cash Flows from Investing activities has been decreased from past years as they had

made huge investments in this year.

3. Cash Flows from Financing activities had declined from previous years as this time they

had paid excess dividend to shareholders.

Webjet Limited

Years

Particulars 2016 2017 2018

Amounts in $

Cash Flow from Operating

Activities

46.62 34.79 120.85

5

receipts from customers and payments to suppliers are just doubled from last year and company

raised funds through issue of share capital and even borrowed funds much higher from previous

years from general public.

(iv)Comparative analysis of three activities of Cash Flow Statements for past three years-:

Flight Centre Limited

Years

Particulars 2016 2017 2018

Amounts in $

Cash Flow from Operating

Activities

356.6 295.35 314.34

Cash Flow from Investing

Activities

-290.2 -161.25 -146.44

Cash Flow from Financing

Activities

-110.46 -155.99 -186.2

1. Cash Flows from operations of Flight Centre Limited has gone down as repayments made

to suppliers was higher than that off past years.

2. Cash Flows from Investing activities has been decreased from past years as they had

made huge investments in this year.

3. Cash Flows from Financing activities had declined from previous years as this time they

had paid excess dividend to shareholders.

Webjet Limited

Years

Particulars 2016 2017 2018

Amounts in $

Cash Flow from Operating

Activities

46.62 34.79 120.85

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

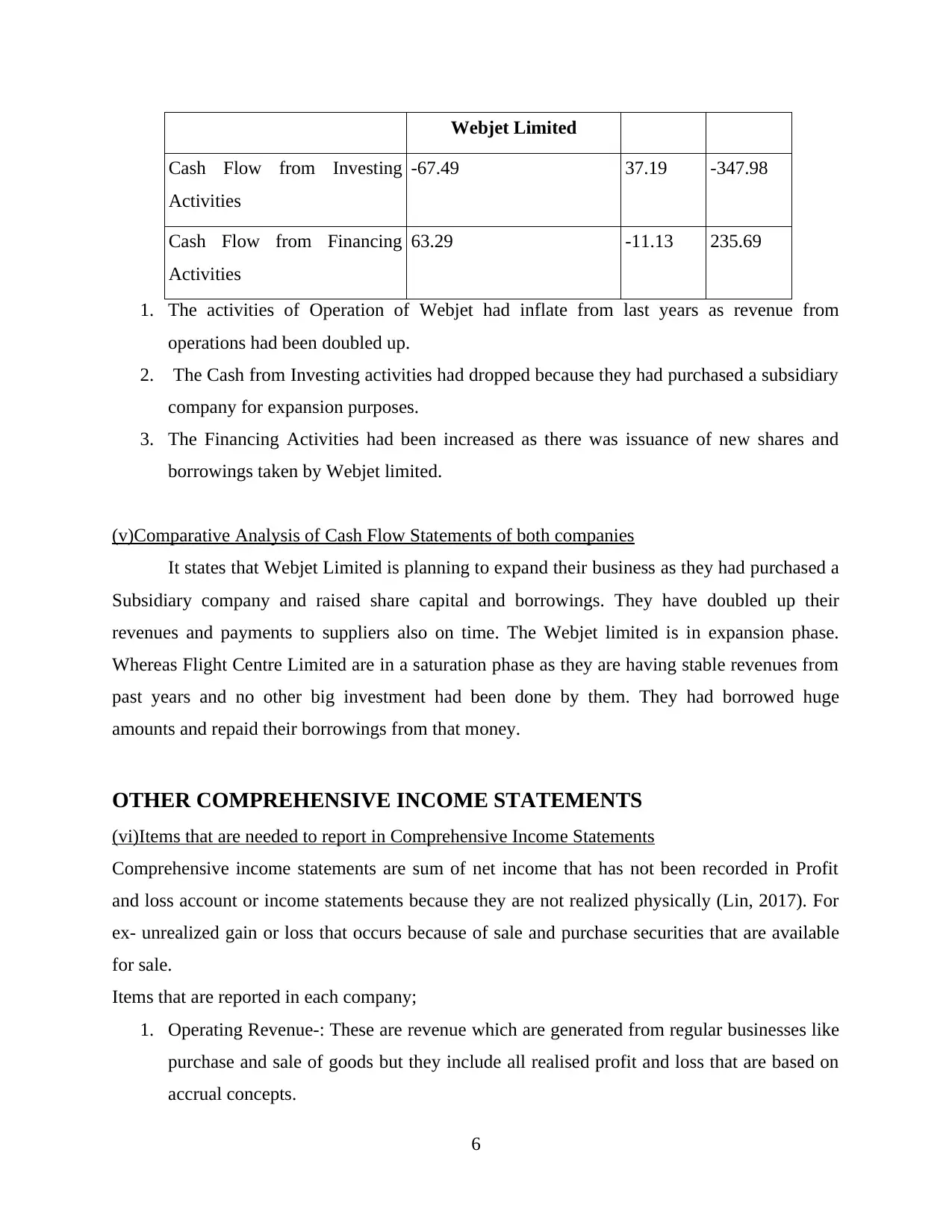

Webjet Limited

Cash Flow from Investing

Activities

-67.49 37.19 -347.98

Cash Flow from Financing

Activities

63.29 -11.13 235.69

1. The activities of Operation of Webjet had inflate from last years as revenue from

operations had been doubled up.

2. The Cash from Investing activities had dropped because they had purchased a subsidiary

company for expansion purposes.

3. The Financing Activities had been increased as there was issuance of new shares and

borrowings taken by Webjet limited.

(v)Comparative Analysis of Cash Flow Statements of both companies

It states that Webjet Limited is planning to expand their business as they had purchased a

Subsidiary company and raised share capital and borrowings. They have doubled up their

revenues and payments to suppliers also on time. The Webjet limited is in expansion phase.

Whereas Flight Centre Limited are in a saturation phase as they are having stable revenues from

past years and no other big investment had been done by them. They had borrowed huge

amounts and repaid their borrowings from that money.

OTHER COMPREHENSIVE INCOME STATEMENTS

(vi)Items that are needed to report in Comprehensive Income Statements

Comprehensive income statements are sum of net income that has not been recorded in Profit

and loss account or income statements because they are not realized physically (Lin, 2017). For

ex- unrealized gain or loss that occurs because of sale and purchase securities that are available

for sale.

Items that are reported in each company;

1. Operating Revenue-: These are revenue which are generated from regular businesses like

purchase and sale of goods but they include all realised profit and loss that are based on

accrual concepts.

6

Cash Flow from Investing

Activities

-67.49 37.19 -347.98

Cash Flow from Financing

Activities

63.29 -11.13 235.69

1. The activities of Operation of Webjet had inflate from last years as revenue from

operations had been doubled up.

2. The Cash from Investing activities had dropped because they had purchased a subsidiary

company for expansion purposes.

3. The Financing Activities had been increased as there was issuance of new shares and

borrowings taken by Webjet limited.

(v)Comparative Analysis of Cash Flow Statements of both companies

It states that Webjet Limited is planning to expand their business as they had purchased a

Subsidiary company and raised share capital and borrowings. They have doubled up their

revenues and payments to suppliers also on time. The Webjet limited is in expansion phase.

Whereas Flight Centre Limited are in a saturation phase as they are having stable revenues from

past years and no other big investment had been done by them. They had borrowed huge

amounts and repaid their borrowings from that money.

OTHER COMPREHENSIVE INCOME STATEMENTS

(vi)Items that are needed to report in Comprehensive Income Statements

Comprehensive income statements are sum of net income that has not been recorded in Profit

and loss account or income statements because they are not realized physically (Lin, 2017). For

ex- unrealized gain or loss that occurs because of sale and purchase securities that are available

for sale.

Items that are reported in each company;

1. Operating Revenue-: These are revenue which are generated from regular businesses like

purchase and sale of goods but they include all realised profit and loss that are based on

accrual concepts.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Unrealized gains and losses are attained because of Hedging of financial instruments

3. Adjustments of Foreign Currency

4. Profit or loss of Post-retirement benefits plans

5. Unrealized Gain/Loss of investments that are available for sale.

(vii)Stating reasons for items of Comprehensive Income statements are not recorded in P&L

These statements are not reported in income statements because financial accounting uses

accrual basis method that means effect of transactions are recorded when they occur (Graham,

2018). The items which are included in comprehensive income statements are excluded from

profit and loss accounts, as income statements are prepared on Accrual Basis Concept. There

may be differences if done on cash basis. It includes those revenues, incomes, losses that are

excluded from net income from income statements. In this statement revenues expenses losses

are recorded even when they are not realized. This accrual concept states that revenues should be

recorded when they have earned but not when received in cash and same with expenses, they are

entered into books of accounts when occurred not when they are paid.

(viii)Comparative Analysis of Other Comprehensive Income Statements

Other Comprehensive Income statements is used for measuring owners interest. This is

statements where income and expenses are recorded that are by-passed in income statement as

they have not been realized according to accrual concept (Dixon, 2016). The items that are not

included in income statement are recorded here-:

1. Losses and profits from derivatives

2. Unrealized profit and loss from debt security

3. Gain and losses from pension and retirement plan

4. Foreign currency transactions

5. Unrealized gain and losses from securities that are available for sale

Comparison of Other Comprehensive Statements

Particulars Webjet Limited Flight Centre Travel Limited

Profit of Current Period 41474 264213

Comprehensive Incomes 13139 15804

7

3. Adjustments of Foreign Currency

4. Profit or loss of Post-retirement benefits plans

5. Unrealized Gain/Loss of investments that are available for sale.

(vii)Stating reasons for items of Comprehensive Income statements are not recorded in P&L

These statements are not reported in income statements because financial accounting uses

accrual basis method that means effect of transactions are recorded when they occur (Graham,

2018). The items which are included in comprehensive income statements are excluded from

profit and loss accounts, as income statements are prepared on Accrual Basis Concept. There

may be differences if done on cash basis. It includes those revenues, incomes, losses that are

excluded from net income from income statements. In this statement revenues expenses losses

are recorded even when they are not realized. This accrual concept states that revenues should be

recorded when they have earned but not when received in cash and same with expenses, they are

entered into books of accounts when occurred not when they are paid.

(viii)Comparative Analysis of Other Comprehensive Income Statements

Other Comprehensive Income statements is used for measuring owners interest. This is

statements where income and expenses are recorded that are by-passed in income statement as

they have not been realized according to accrual concept (Dixon, 2016). The items that are not

included in income statement are recorded here-:

1. Losses and profits from derivatives

2. Unrealized profit and loss from debt security

3. Gain and losses from pension and retirement plan

4. Foreign currency transactions

5. Unrealized gain and losses from securities that are available for sale

Comparison of Other Comprehensive Statements

Particulars Webjet Limited Flight Centre Travel Limited

Profit of Current Period 41474 264213

Comprehensive Incomes 13139 15804

7

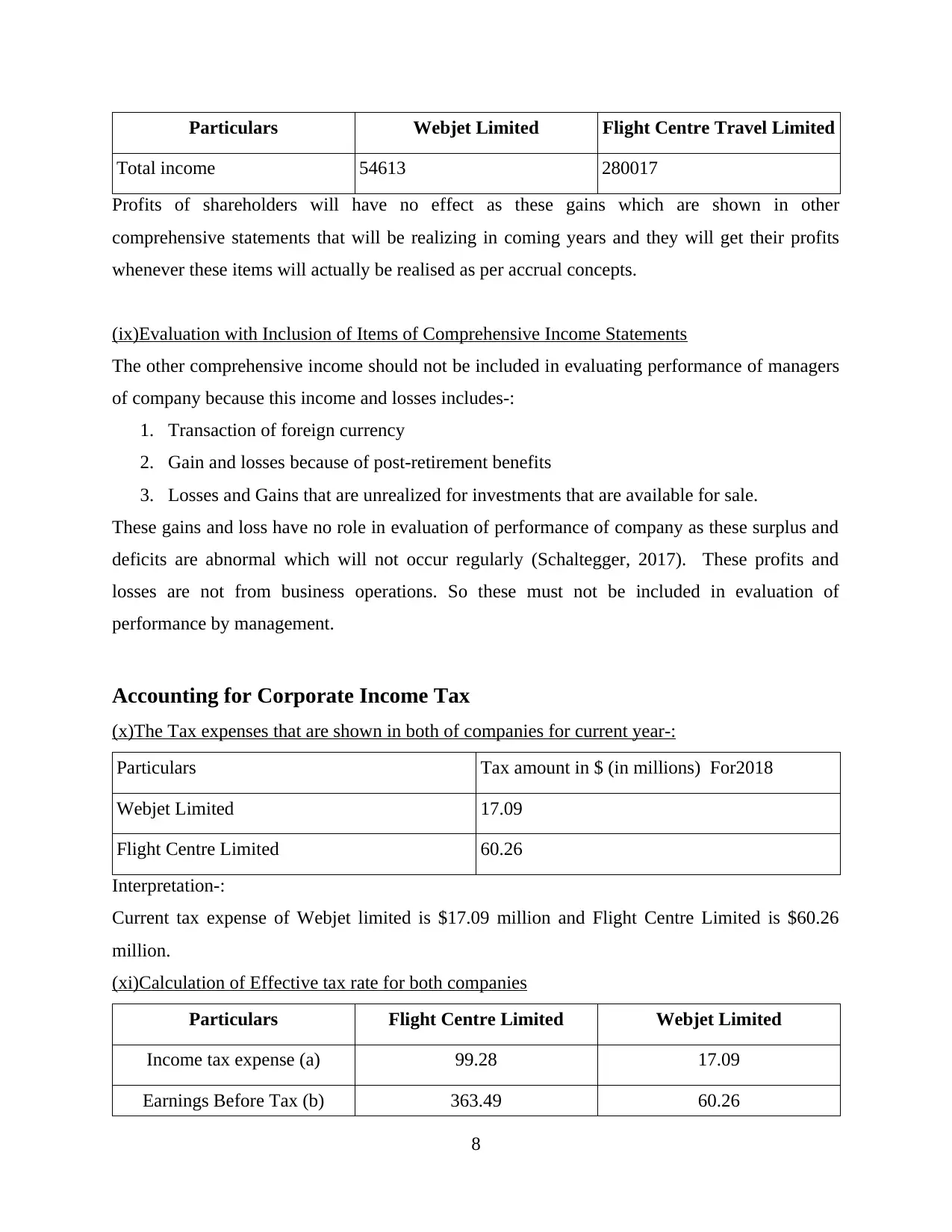

Particulars Webjet Limited Flight Centre Travel Limited

Total income 54613 280017

Profits of shareholders will have no effect as these gains which are shown in other

comprehensive statements that will be realizing in coming years and they will get their profits

whenever these items will actually be realised as per accrual concepts.

(ix)Evaluation with Inclusion of Items of Comprehensive Income Statements

The other comprehensive income should not be included in evaluating performance of managers

of company because this income and losses includes-:

1. Transaction of foreign currency

2. Gain and losses because of post-retirement benefits

3. Losses and Gains that are unrealized for investments that are available for sale.

These gains and loss have no role in evaluation of performance of company as these surplus and

deficits are abnormal which will not occur regularly (Schaltegger, 2017). These profits and

losses are not from business operations. So these must not be included in evaluation of

performance by management.

Accounting for Corporate Income Tax

(x)The Tax expenses that are shown in both of companies for current year-:

Particulars Tax amount in $ (in millions) For2018

Webjet Limited 17.09

Flight Centre Limited 60.26

Interpretation-:

Current tax expense of Webjet limited is $17.09 million and Flight Centre Limited is $60.26

million.

(xi)Calculation of Effective tax rate for both companies

Particulars Flight Centre Limited Webjet Limited

Income tax expense (a) 99.28 17.09

Earnings Before Tax (b) 363.49 60.26

8

Total income 54613 280017

Profits of shareholders will have no effect as these gains which are shown in other

comprehensive statements that will be realizing in coming years and they will get their profits

whenever these items will actually be realised as per accrual concepts.

(ix)Evaluation with Inclusion of Items of Comprehensive Income Statements

The other comprehensive income should not be included in evaluating performance of managers

of company because this income and losses includes-:

1. Transaction of foreign currency

2. Gain and losses because of post-retirement benefits

3. Losses and Gains that are unrealized for investments that are available for sale.

These gains and loss have no role in evaluation of performance of company as these surplus and

deficits are abnormal which will not occur regularly (Schaltegger, 2017). These profits and

losses are not from business operations. So these must not be included in evaluation of

performance by management.

Accounting for Corporate Income Tax

(x)The Tax expenses that are shown in both of companies for current year-:

Particulars Tax amount in $ (in millions) For2018

Webjet Limited 17.09

Flight Centre Limited 60.26

Interpretation-:

Current tax expense of Webjet limited is $17.09 million and Flight Centre Limited is $60.26

million.

(xi)Calculation of Effective tax rate for both companies

Particulars Flight Centre Limited Webjet Limited

Income tax expense (a) 99.28 17.09

Earnings Before Tax (b) 363.49 60.26

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.