University Management Accounting: Financial Analysis and Budget Report

VerifiedAdded on 2021/05/31

|17

|2886

|111

Report

AI Summary

This report presents a comprehensive financial analysis of a company, encompassing profitability, liquidity, and asset utilization. It begins with an introduction outlining the report's objectives, the purpose of financial analysis, and the report's structure. The analysis includes the calculation and evaluation of various financial ratios, such as profitability (gross profit, net profit), liquidity (current, quick, and debt-equity ratios), inventory turnover, and accounts receivable. The report evaluates the business's profitability, financial stability, and asset utilization, providing detailed figures and comparisons. Recommendations are offered to improve sales, reduce debt, and optimize asset allocation. The report concludes with a summary of key findings, limitations of financial analysis, and a list of references. The report also includes a budget and addresses variances in projected sales and cost of goods.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of Student:

Name of University:

Author’s Note:

Management Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Requirement One- Financial Analysis Report.................................................................................3

1. Introduction..................................................................................................................................3

a. Objective of the report.............................................................................................................3

b. Purpose of financial analysis...................................................................................................3

c. Description on the structure of report......................................................................................3

2. Financial Analysis.......................................................................................................................3

a. Calculation of the financial ratios............................................................................................4

i. Profitability Ratios................................................................................................................4

ii. Liquidity Ratios...................................................................................................................4

iii. Inventory Turnover ratios...................................................................................................4

iv. Accounts receivable ratio...................................................................................................5

b. Analysis and evaluation of the business’ profitability.............................................................6

c. Analysis and evaluation of business’ financial stability..........................................................7

d. Analysis and evaluation on the business’ asset utilisation......................................................8

Recommendations............................................................................................................................8

Conclusion.......................................................................................................................................8

a. Summarization of key points from the previous sections........................................................8

b. Limitations of financial analysis..............................................................................................9

References......................................................................................................................................10

Requirement Two – Budget...........................................................................................................11

Requirement Three- Financial Analysis Report............................................................................11

Part a and Part b.........................................................................................................................11

Table of Contents

Requirement One- Financial Analysis Report.................................................................................3

1. Introduction..................................................................................................................................3

a. Objective of the report.............................................................................................................3

b. Purpose of financial analysis...................................................................................................3

c. Description on the structure of report......................................................................................3

2. Financial Analysis.......................................................................................................................3

a. Calculation of the financial ratios............................................................................................4

i. Profitability Ratios................................................................................................................4

ii. Liquidity Ratios...................................................................................................................4

iii. Inventory Turnover ratios...................................................................................................4

iv. Accounts receivable ratio...................................................................................................5

b. Analysis and evaluation of the business’ profitability.............................................................6

c. Analysis and evaluation of business’ financial stability..........................................................7

d. Analysis and evaluation on the business’ asset utilisation......................................................8

Recommendations............................................................................................................................8

Conclusion.......................................................................................................................................8

a. Summarization of key points from the previous sections........................................................8

b. Limitations of financial analysis..............................................................................................9

References......................................................................................................................................10

Requirement Two – Budget...........................................................................................................11

Requirement Three- Financial Analysis Report............................................................................11

Part a and Part b.........................................................................................................................11

2MANAGEMENT ACCOUNTING

Part c..........................................................................................................................................11

Requirement Four – CVP..............................................................................................................11

Part a..........................................................................................................................................11

Part b..........................................................................................................................................12

Part c and Part d.........................................................................................................................13

List of Appendix- Budget..............................................................................................................14

Part c..........................................................................................................................................11

Requirement Four – CVP..............................................................................................................11

Part a..........................................................................................................................................11

Part b..........................................................................................................................................12

Part c and Part d.........................................................................................................................13

List of Appendix- Budget..............................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Requirement One- Financial Analysis Report

1. Introduction

a. Objective of the report

The reports intend to conduct a financial analysis calculating the various types of the

financial ratios such as gross profit., net profit and return on equity. Some of the liquid ratio

analysis has been performed with the evaluating of the current ratio, quick ratio and the

conduction of the equity ratio. The next aspect of the ratio analysis has conducted the ratio

analysis of the accounts receivable. This section of the report has bee seen to be followed by the

various types of the others discourse of the report which has been seen to be related to the

evaluation of the business profitability. The next important aspect of the report has been further

seen to be based on the conduction of the various aspects of the financial stability along with the

evaluating the business asset utilization.

b. Purpose of financial analysis

The main purpose of the financial analysis will be able to state on the facility of the

liquidity, efficiency and profitability of the company.

c. Description on the structure of report

The structure of the report has been divided into four main categories including several

types of the subsections in the study. The first discussion of the study has been seen to focus on

the main form of the evaluation of the financial ratios. The second subsection of the first part of

the report has been seen to be related to the conduction of the profitability analysis of the

company, evaluation of the nosiness financial stability and analysis of the business asset

utilization. The third section of the report has stated on recommendation which has been abet to

state on the relevant nature of the scope of the future financial improvements.

2. Financial Analysis

Requirement One- Financial Analysis Report

1. Introduction

a. Objective of the report

The reports intend to conduct a financial analysis calculating the various types of the

financial ratios such as gross profit., net profit and return on equity. Some of the liquid ratio

analysis has been performed with the evaluating of the current ratio, quick ratio and the

conduction of the equity ratio. The next aspect of the ratio analysis has conducted the ratio

analysis of the accounts receivable. This section of the report has bee seen to be followed by the

various types of the others discourse of the report which has been seen to be related to the

evaluation of the business profitability. The next important aspect of the report has been further

seen to be based on the conduction of the various aspects of the financial stability along with the

evaluating the business asset utilization.

b. Purpose of financial analysis

The main purpose of the financial analysis will be able to state on the facility of the

liquidity, efficiency and profitability of the company.

c. Description on the structure of report

The structure of the report has been divided into four main categories including several

types of the subsections in the study. The first discussion of the study has been seen to focus on

the main form of the evaluation of the financial ratios. The second subsection of the first part of

the report has been seen to be related to the conduction of the profitability analysis of the

company, evaluation of the nosiness financial stability and analysis of the business asset

utilization. The third section of the report has stated on recommendation which has been abet to

state on the relevant nature of the scope of the future financial improvements.

2. Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

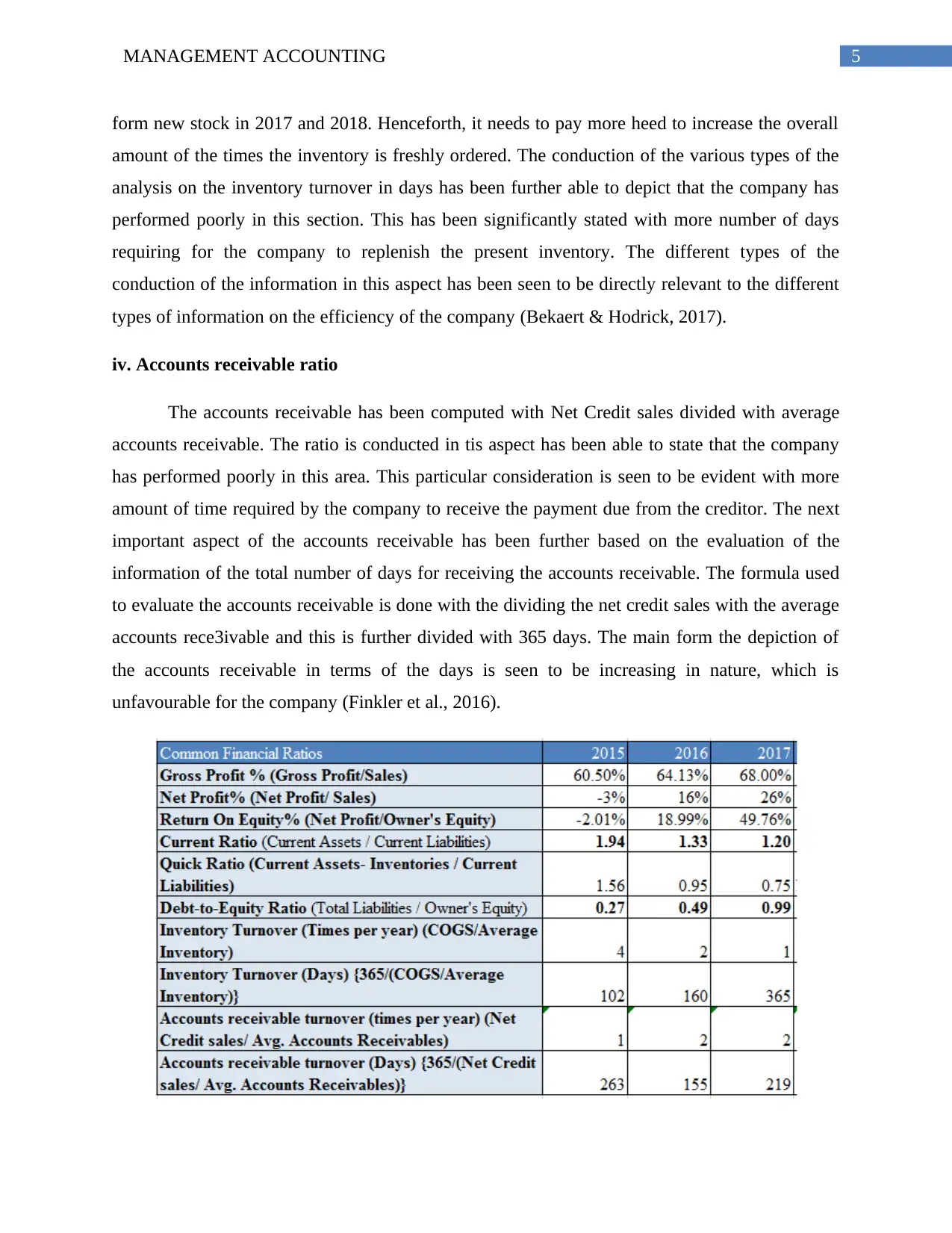

a. Calculation of the financial ratios

i. Profitability Ratios

The gross profit ratio has been calculated by dividing the gross profit by sales. Based on

the evaluation of the gross profit ratio it has been see that the company has able to significantly

increasing the total amount of the gross profit ratio from 2015 to 2018. Net profit ratio is

calculated by dividing net profit by the owner’s equity. The several types of the depictions as per

the net profit ratio has been able to state that the company has been able to make the significant

nature of the improvement in this section. This seen to be evident with 16% improvement from

2016 to 26% in 2017 (Titman, Keown & Martin, 2017).

ii. Liquidity Ratios

The current ratio is calculated by dividing the current assets with current liabilities. The

various types of the depiction on the current ratio has been able to state that the company has

performed poorly in this section. This is observed with decreasing amount of the liquid cash to

support the short-term liabilities. The quick ratio is calculated with subtracting the inventories

from the current assets. The evaluation of the quick ratio for the company has not been able to

perform well in this regard. The total quick ratio is seen to be decreasing over the years. This has

been seen to be evident with the total amount of the quick ratio decreasing from the 1.56 in 2015

to 0.95 in 2016 to 0.75 in 2017.

The Depiction of the debt equity ratio for the company has been seen to be conducted by

dividing the total liabilities and owner’s equity. The overall evaluation of the has been seen with

increasing nature of debt to support the operating activities of the company. This is particularly

seen to be a negative aspect for the company (Renz, D. O., & Herman, 2016).

iii. Inventory Turnover ratios

The inventory turnover has been computed by dividing the “cost of goods sold” by

average inventory. The average inventory is the sum of the previous year’s inventory and present

year’s inventory, the amount is then divided by 2. Based on the conduction of the inventory

turnover ratio it has been seen that the company is not able to effective sell its existing inventory.

The main from of the depictions has been able to state that the company has seldom ordered

a. Calculation of the financial ratios

i. Profitability Ratios

The gross profit ratio has been calculated by dividing the gross profit by sales. Based on

the evaluation of the gross profit ratio it has been see that the company has able to significantly

increasing the total amount of the gross profit ratio from 2015 to 2018. Net profit ratio is

calculated by dividing net profit by the owner’s equity. The several types of the depictions as per

the net profit ratio has been able to state that the company has been able to make the significant

nature of the improvement in this section. This seen to be evident with 16% improvement from

2016 to 26% in 2017 (Titman, Keown & Martin, 2017).

ii. Liquidity Ratios

The current ratio is calculated by dividing the current assets with current liabilities. The

various types of the depiction on the current ratio has been able to state that the company has

performed poorly in this section. This is observed with decreasing amount of the liquid cash to

support the short-term liabilities. The quick ratio is calculated with subtracting the inventories

from the current assets. The evaluation of the quick ratio for the company has not been able to

perform well in this regard. The total quick ratio is seen to be decreasing over the years. This has

been seen to be evident with the total amount of the quick ratio decreasing from the 1.56 in 2015

to 0.95 in 2016 to 0.75 in 2017.

The Depiction of the debt equity ratio for the company has been seen to be conducted by

dividing the total liabilities and owner’s equity. The overall evaluation of the has been seen with

increasing nature of debt to support the operating activities of the company. This is particularly

seen to be a negative aspect for the company (Renz, D. O., & Herman, 2016).

iii. Inventory Turnover ratios

The inventory turnover has been computed by dividing the “cost of goods sold” by

average inventory. The average inventory is the sum of the previous year’s inventory and present

year’s inventory, the amount is then divided by 2. Based on the conduction of the inventory

turnover ratio it has been seen that the company is not able to effective sell its existing inventory.

The main from of the depictions has been able to state that the company has seldom ordered

5MANAGEMENT ACCOUNTING

form new stock in 2017 and 2018. Henceforth, it needs to pay more heed to increase the overall

amount of the times the inventory is freshly ordered. The conduction of the various types of the

analysis on the inventory turnover in days has been further able to depict that the company has

performed poorly in this section. This has been significantly stated with more number of days

requiring for the company to replenish the present inventory. The different types of the

conduction of the information in this aspect has been seen to be directly relevant to the different

types of information on the efficiency of the company (Bekaert & Hodrick, 2017).

iv. Accounts receivable ratio

The accounts receivable has been computed with Net Credit sales divided with average

accounts receivable. The ratio is conducted in tis aspect has been able to state that the company

has performed poorly in this area. This particular consideration is seen to be evident with more

amount of time required by the company to receive the payment due from the creditor. The next

important aspect of the accounts receivable has been further based on the evaluation of the

information of the total number of days for receiving the accounts receivable. The formula used

to evaluate the accounts receivable is done with the dividing the net credit sales with the average

accounts rece3ivable and this is further divided with 365 days. The main form the depiction of

the accounts receivable in terms of the days is seen to be increasing in nature, which is

unfavourable for the company (Finkler et al., 2016).

form new stock in 2017 and 2018. Henceforth, it needs to pay more heed to increase the overall

amount of the times the inventory is freshly ordered. The conduction of the various types of the

analysis on the inventory turnover in days has been further able to depict that the company has

performed poorly in this section. This has been significantly stated with more number of days

requiring for the company to replenish the present inventory. The different types of the

conduction of the information in this aspect has been seen to be directly relevant to the different

types of information on the efficiency of the company (Bekaert & Hodrick, 2017).

iv. Accounts receivable ratio

The accounts receivable has been computed with Net Credit sales divided with average

accounts receivable. The ratio is conducted in tis aspect has been able to state that the company

has performed poorly in this area. This particular consideration is seen to be evident with more

amount of time required by the company to receive the payment due from the creditor. The next

important aspect of the accounts receivable has been further based on the evaluation of the

information of the total number of days for receiving the accounts receivable. The formula used

to evaluate the accounts receivable is done with the dividing the net credit sales with the average

accounts rece3ivable and this is further divided with 365 days. The main form the depiction of

the accounts receivable in terms of the days is seen to be increasing in nature, which is

unfavourable for the company (Finkler et al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

Figure: Calculation of all the financial ratios

(Source: As stated by the author)

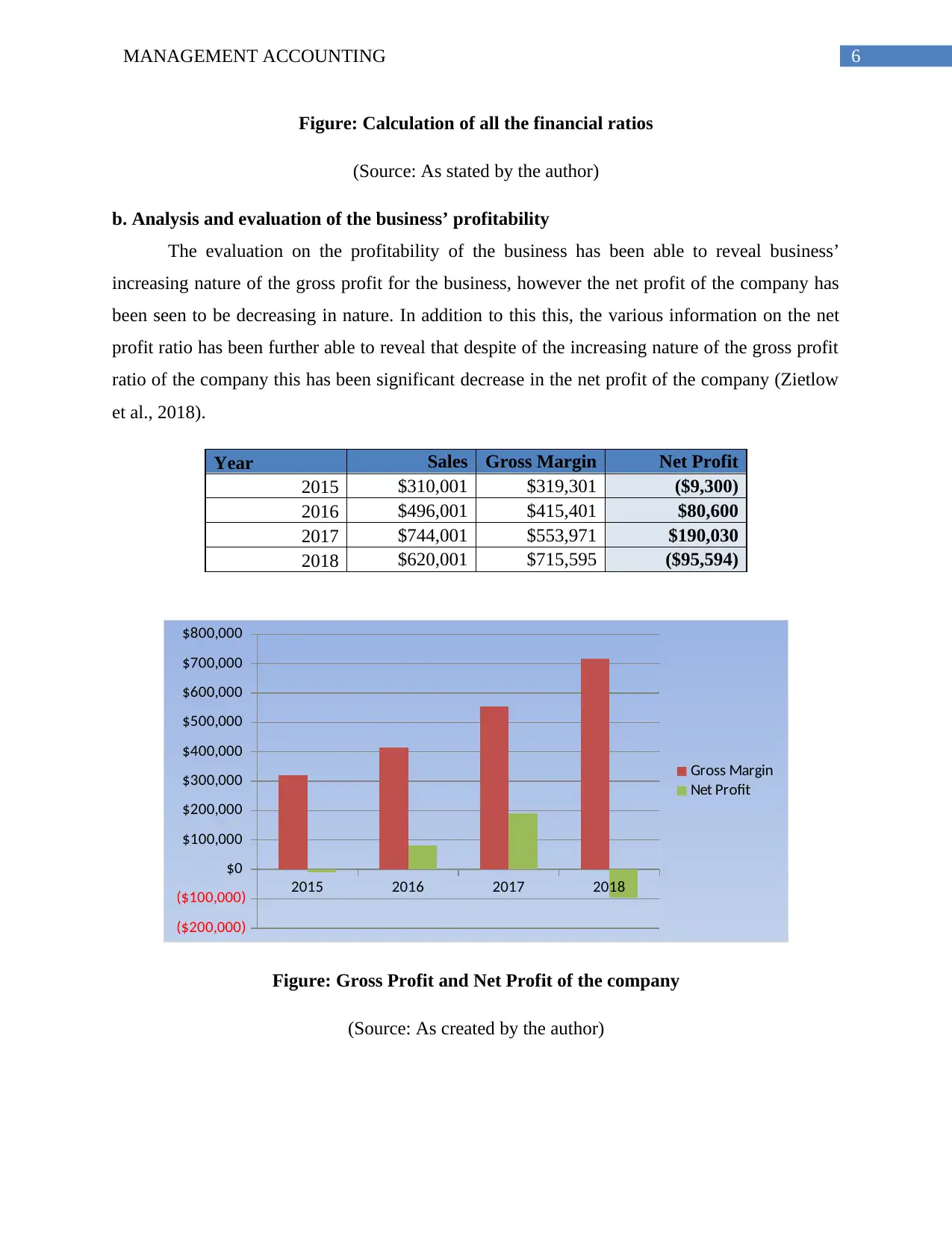

b. Analysis and evaluation of the business’ profitability

The evaluation on the profitability of the business has been able to reveal business’

increasing nature of the gross profit for the business, however the net profit of the company has

been seen to be decreasing in nature. In addition to this this, the various information on the net

profit ratio has been further able to reveal that despite of the increasing nature of the gross profit

ratio of the company this has been significant decrease in the net profit of the company (Zietlow

et al., 2018).

Year Sales Gross Margin Net Profit

2015 $310,001 $319,301 ($9,300)

2016 $496,001 $415,401 $80,600

2017 $744,001 $553,971 $190,030

2018 $620,001 $715,595 ($95,594)

2015 2016 2017 2018

($200,000)

($100,000)

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

Gross Margin

Net Profit

Figure: Gross Profit and Net Profit of the company

(Source: As created by the author)

Figure: Calculation of all the financial ratios

(Source: As stated by the author)

b. Analysis and evaluation of the business’ profitability

The evaluation on the profitability of the business has been able to reveal business’

increasing nature of the gross profit for the business, however the net profit of the company has

been seen to be decreasing in nature. In addition to this this, the various information on the net

profit ratio has been further able to reveal that despite of the increasing nature of the gross profit

ratio of the company this has been significant decrease in the net profit of the company (Zietlow

et al., 2018).

Year Sales Gross Margin Net Profit

2015 $310,001 $319,301 ($9,300)

2016 $496,001 $415,401 $80,600

2017 $744,001 $553,971 $190,030

2018 $620,001 $715,595 ($95,594)

2015 2016 2017 2018

($200,000)

($100,000)

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

Gross Margin

Net Profit

Figure: Gross Profit and Net Profit of the company

(Source: As created by the author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

The different types of the depictions on the pre-tax margin and PBT has been seen with a

positive increasing from 2015 to 2017, however it decreased in 2018.

Sales

Profit Before

tax

Pretax Net

Margin

2015 310,001 -9,300 -3%

2016 496,001 80,600 16%

2017 744,001 190,030 26%

2018 620,001 -136,563 -22%

2015 2016 2017 2018

-200,000

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

-30%

-20%

-10%

0%

10%

20%

30%

Profit Before tax

Pretax Net Margin

Figure: PBT and pre-tax net margin the company

(Source: As created by the author)

c. Analysis and evaluation of business’ financial stability

The various types of the depiction on the finical ratio has been performed with the

conduction of the debt equity ratio. The main findings in this aspect has shown that the company

is not stable in with an increasing nature of the debt equity ratio (Barr, 2018).

The different types of the depictions on the pre-tax margin and PBT has been seen with a

positive increasing from 2015 to 2017, however it decreased in 2018.

Sales

Profit Before

tax

Pretax Net

Margin

2015 310,001 -9,300 -3%

2016 496,001 80,600 16%

2017 744,001 190,030 26%

2018 620,001 -136,563 -22%

2015 2016 2017 2018

-200,000

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

-30%

-20%

-10%

0%

10%

20%

30%

Profit Before tax

Pretax Net Margin

Figure: PBT and pre-tax net margin the company

(Source: As created by the author)

c. Analysis and evaluation of business’ financial stability

The various types of the depiction on the finical ratio has been performed with the

conduction of the debt equity ratio. The main findings in this aspect has shown that the company

is not stable in with an increasing nature of the debt equity ratio (Barr, 2018).

8MANAGEMENT ACCOUNTING

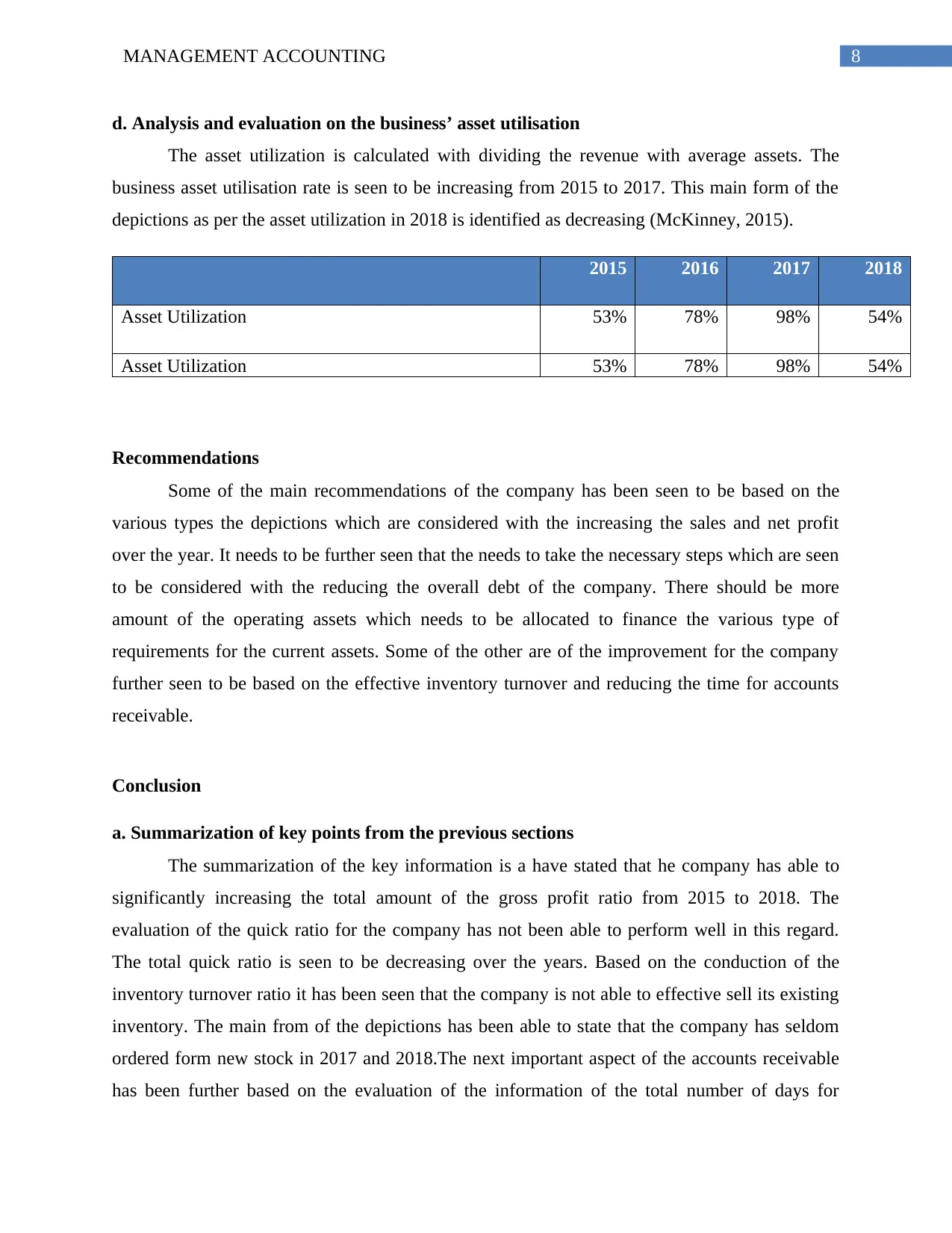

d. Analysis and evaluation on the business’ asset utilisation

The asset utilization is calculated with dividing the revenue with average assets. The

business asset utilisation rate is seen to be increasing from 2015 to 2017. This main form of the

depictions as per the asset utilization in 2018 is identified as decreasing (McKinney, 2015).

2015 2016 2017 2018

Asset Utilization 53% 78% 98% 54%

Asset Utilization 53% 78% 98% 54%

Recommendations

Some of the main recommendations of the company has been seen to be based on the

various types the depictions which are considered with the increasing the sales and net profit

over the year. It needs to be further seen that the needs to take the necessary steps which are seen

to be considered with the reducing the overall debt of the company. There should be more

amount of the operating assets which needs to be allocated to finance the various type of

requirements for the current assets. Some of the other are of the improvement for the company

further seen to be based on the effective inventory turnover and reducing the time for accounts

receivable.

Conclusion

a. Summarization of key points from the previous sections

The summarization of the key information is a have stated that he company has able to

significantly increasing the total amount of the gross profit ratio from 2015 to 2018. The

evaluation of the quick ratio for the company has not been able to perform well in this regard.

The total quick ratio is seen to be decreasing over the years. Based on the conduction of the

inventory turnover ratio it has been seen that the company is not able to effective sell its existing

inventory. The main from of the depictions has been able to state that the company has seldom

ordered form new stock in 2017 and 2018.The next important aspect of the accounts receivable

has been further based on the evaluation of the information of the total number of days for

d. Analysis and evaluation on the business’ asset utilisation

The asset utilization is calculated with dividing the revenue with average assets. The

business asset utilisation rate is seen to be increasing from 2015 to 2017. This main form of the

depictions as per the asset utilization in 2018 is identified as decreasing (McKinney, 2015).

2015 2016 2017 2018

Asset Utilization 53% 78% 98% 54%

Asset Utilization 53% 78% 98% 54%

Recommendations

Some of the main recommendations of the company has been seen to be based on the

various types the depictions which are considered with the increasing the sales and net profit

over the year. It needs to be further seen that the needs to take the necessary steps which are seen

to be considered with the reducing the overall debt of the company. There should be more

amount of the operating assets which needs to be allocated to finance the various type of

requirements for the current assets. Some of the other are of the improvement for the company

further seen to be based on the effective inventory turnover and reducing the time for accounts

receivable.

Conclusion

a. Summarization of key points from the previous sections

The summarization of the key information is a have stated that he company has able to

significantly increasing the total amount of the gross profit ratio from 2015 to 2018. The

evaluation of the quick ratio for the company has not been able to perform well in this regard.

The total quick ratio is seen to be decreasing over the years. Based on the conduction of the

inventory turnover ratio it has been seen that the company is not able to effective sell its existing

inventory. The main from of the depictions has been able to state that the company has seldom

ordered form new stock in 2017 and 2018.The next important aspect of the accounts receivable

has been further based on the evaluation of the information of the total number of days for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

receiving the accounts receivable. The various information on the net profit ratio has been further

able to reveal that despite of the increasing nature of the gross profit ratio of the company this

has been significant decrease in the net profit of the company.

b. Limitations of financial analysis

The ratio analysis limitations are seen with the non-consideration of the stock market

performance.

receiving the accounts receivable. The various information on the net profit ratio has been further

able to reveal that despite of the increasing nature of the gross profit ratio of the company this

has been significant decrease in the net profit of the company.

b. Limitations of financial analysis

The ratio analysis limitations are seen with the non-consideration of the stock market

performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

References

Barr, M. J. (2018). Budgets and financial management in higher education. John Wiley & Sons.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge University

Press.

Finkler, S. A., Smith, D. L., Calabrese, T. D., & Purtell, R. M. (2016). Financial management

for public, health, and not-for-profit organizations. CQ Press.

McKinney, J. B. (2015). Effective financial management in public and nonprofit agencies. ABC-

CLIO.

Renz, D. O., & Herman, R. D. (Eds.). (2016). The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Zietlow, J., Hankin, J. A., Seidner, A., & O'Brien, T. (2018). Financial management for

nonprofit organizations: Policies and practices. John Wiley & Sons.

References

Barr, M. J. (2018). Budgets and financial management in higher education. John Wiley & Sons.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge University

Press.

Finkler, S. A., Smith, D. L., Calabrese, T. D., & Purtell, R. M. (2016). Financial management

for public, health, and not-for-profit organizations. CQ Press.

McKinney, J. B. (2015). Effective financial management in public and nonprofit agencies. ABC-

CLIO.

Renz, D. O., & Herman, R. D. (Eds.). (2016). The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Zietlow, J., Hankin, J. A., Seidner, A., & O'Brien, T. (2018). Financial management for

nonprofit organizations: Policies and practices. John Wiley & Sons.

11MANAGEMENT ACCOUNTING

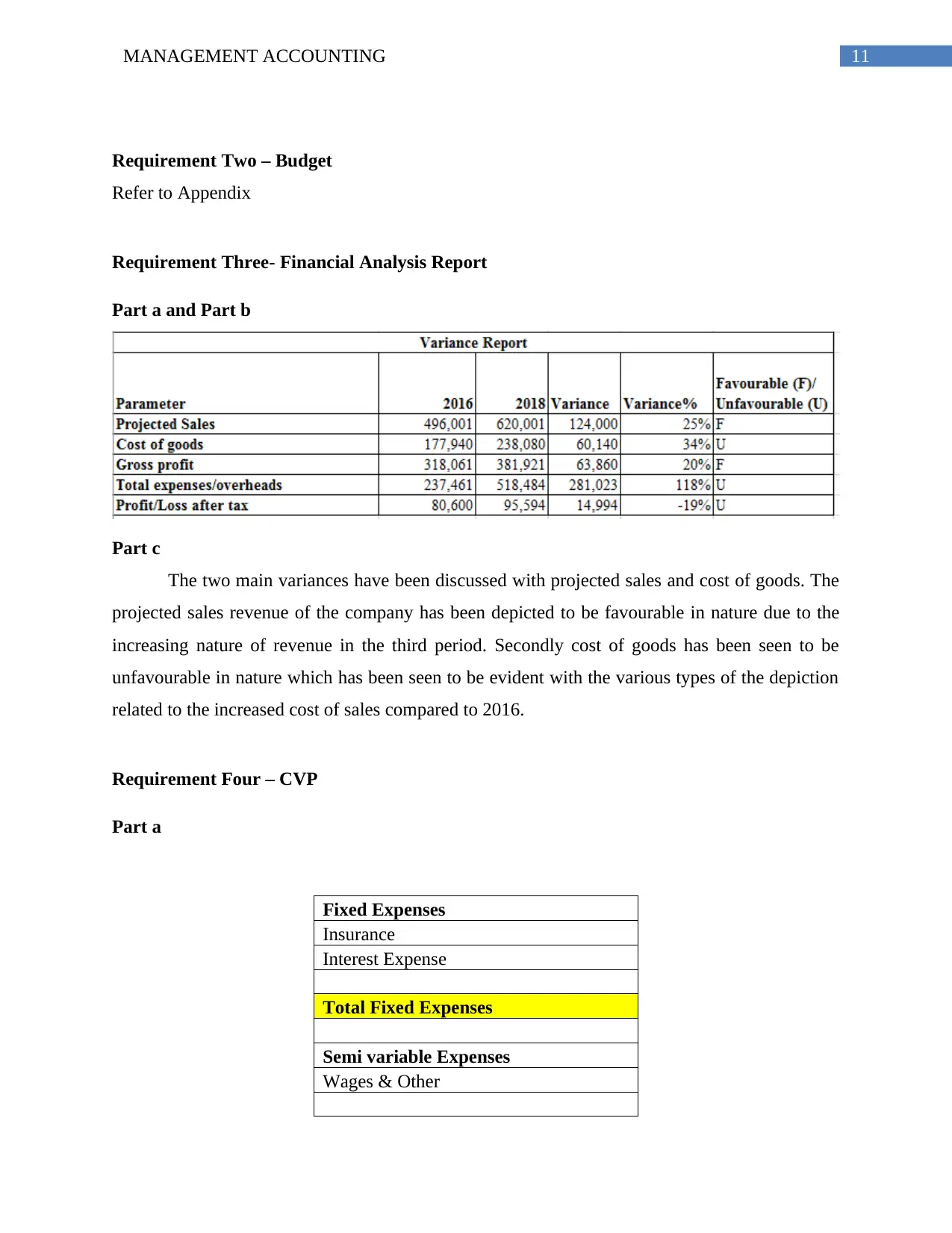

Requirement Two – Budget

Refer to Appendix

Requirement Three- Financial Analysis Report

Part a and Part b

Part c

The two main variances have been discussed with projected sales and cost of goods. The

projected sales revenue of the company has been depicted to be favourable in nature due to the

increasing nature of revenue in the third period. Secondly cost of goods has been seen to be

unfavourable in nature which has been seen to be evident with the various types of the depiction

related to the increased cost of sales compared to 2016.

Requirement Four – CVP

Part a

Fixed Expenses

Insurance

Interest Expense

Total Fixed Expenses

Semi variable Expenses

Wages & Other

Requirement Two – Budget

Refer to Appendix

Requirement Three- Financial Analysis Report

Part a and Part b

Part c

The two main variances have been discussed with projected sales and cost of goods. The

projected sales revenue of the company has been depicted to be favourable in nature due to the

increasing nature of revenue in the third period. Secondly cost of goods has been seen to be

unfavourable in nature which has been seen to be evident with the various types of the depiction

related to the increased cost of sales compared to 2016.

Requirement Four – CVP

Part a

Fixed Expenses

Insurance

Interest Expense

Total Fixed Expenses

Semi variable Expenses

Wages & Other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.