Financial Analysis: Budget Variances, Performance, Recommendations

VerifiedAdded on 2023/06/12

|14

|2245

|410

Report

AI Summary

This report provides a comprehensive analysis of Houzit's financial performance, focusing on budget analysis and variance reporting. It examines sales budgets, profit budgets, and debtor analysis, identifying issues such as high anticipated costs, unclear discount records, and inadequate debtor balance reconciliation. The report includes a variance report comparing budgeted and actual performance, revealing unfavorable sales results and gross margins. It also assesses Houzit's performance within the retail industry, highlighting the impact of credit policies on debtor balances and liquidity. Recommendations are provided to improve cost management and financial management practices, including the implementation of an ERP system and enhanced internal controls. The report also addresses tax compliance and relevant regulations under the Corporation Act 2001.

Running head: MANAGE FINANCES

Manage Finances

Name of the Student:

Name of the University:

Author’s Note

Manage Finances

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGE FINANCES

Table of Contents

Assessment Task 1...........................................................................................................................2

Part 1............................................................................................................................................2

Budget Analysis...........................................................................................................................5

Part 2............................................................................................................................................7

Assessment 2...................................................................................................................................9

Variance Report...........................................................................................................................9

Debtor Analysis.........................................................................................................................10

Issues which Can be Identified..................................................................................................10

Analysis of variances in Different Budgets...............................................................................10

Performance Analysis................................................................................................................11

Recommendation...........................................................................................................................12

Reference.......................................................................................................................................13

MANAGE FINANCES

Table of Contents

Assessment Task 1...........................................................................................................................2

Part 1............................................................................................................................................2

Budget Analysis...........................................................................................................................5

Part 2............................................................................................................................................7

Assessment 2...................................................................................................................................9

Variance Report...........................................................................................................................9

Debtor Analysis.........................................................................................................................10

Issues which Can be Identified..................................................................................................10

Analysis of variances in Different Budgets...............................................................................10

Performance Analysis................................................................................................................11

Recommendation...........................................................................................................................12

Reference.......................................................................................................................................13

2

MANAGE FINANCES

Assessment Task 1

Part 1

MANAGE FINANCES

Assessment Task 1

Part 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGE FINANCES

MANAGE FINANCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGE FINANCES

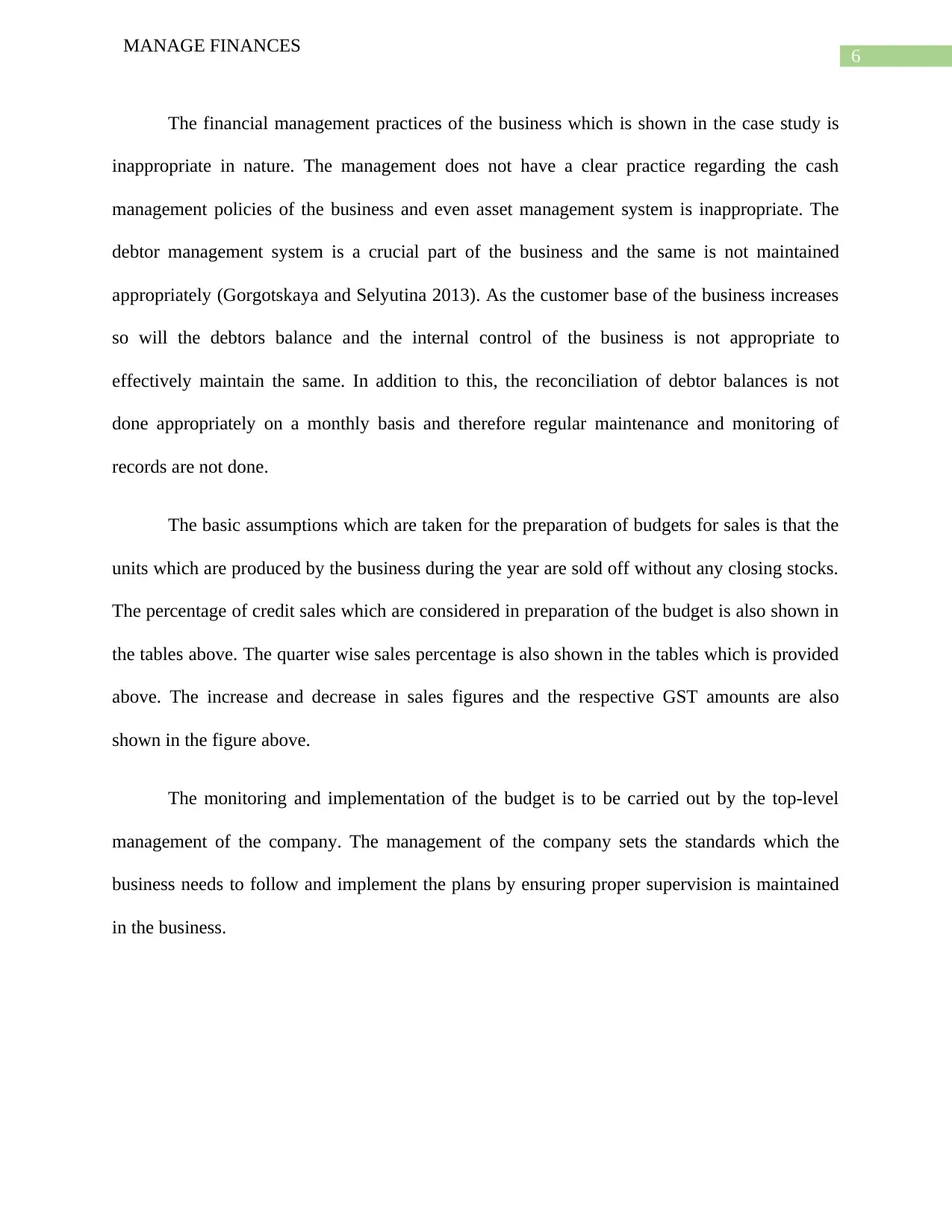

Particulars 2010/11 Growth % /Amount 2011/12

Revenue:

Sales 15,714,108 25.97% 19,795,297

Cost of Goods Sold 8,799,900 11,283,319

Gross Profit 6,914,208 8,511,978

Gross Profit Margin 44% -1% 43%

Expenses:

Accounting Fees 9,000 1,000 10,000

Interest Expense 90,508 -6,000 84,508

Bank Charges 1,600 0 1,600

Depreciation 170,000 0 170,000

Insurance 12,875 4% 13,390

Store Supplies 3,605 4% 3,749

Advertising 280,000 70,000 350,000

Cleaning 15,656 4% 16,282

Repairs & Maintenance 61,800 4% 64,272

Rent 2,538,950 4% 2,640,508

Telephone 14,420 4% 14,997

Electricity Expense 25,750 4% 26,780

Luxury Car Tax 7,491

Fringe Benefit Tax 28,000 -2,000 26,000

Superannuation 171,495 187,020

Wages & Salaries 1,905,500 172,500 2,078,000

Payroll Tax 90,511 98,705

Worker's Compensation 38,110 41,560

Total Expenses 5,457,780 5,834,863

Net Profit (Before Tax) 1,456,428 2,677,116

Income Tax 436,928 803,135

Net Profit 1,019,500 1,873,981

Net Profit Margin 6.49% 9.47%

MANAGE FINANCES

Particulars 2010/11 Growth % /Amount 2011/12

Revenue:

Sales 15,714,108 25.97% 19,795,297

Cost of Goods Sold 8,799,900 11,283,319

Gross Profit 6,914,208 8,511,978

Gross Profit Margin 44% -1% 43%

Expenses:

Accounting Fees 9,000 1,000 10,000

Interest Expense 90,508 -6,000 84,508

Bank Charges 1,600 0 1,600

Depreciation 170,000 0 170,000

Insurance 12,875 4% 13,390

Store Supplies 3,605 4% 3,749

Advertising 280,000 70,000 350,000

Cleaning 15,656 4% 16,282

Repairs & Maintenance 61,800 4% 64,272

Rent 2,538,950 4% 2,640,508

Telephone 14,420 4% 14,997

Electricity Expense 25,750 4% 26,780

Luxury Car Tax 7,491

Fringe Benefit Tax 28,000 -2,000 26,000

Superannuation 171,495 187,020

Wages & Salaries 1,905,500 172,500 2,078,000

Payroll Tax 90,511 98,705

Worker's Compensation 38,110 41,560

Total Expenses 5,457,780 5,834,863

Net Profit (Before Tax) 1,456,428 2,677,116

Income Tax 436,928 803,135

Net Profit 1,019,500 1,873,981

Net Profit Margin 6.49% 9.47%

5

MANAGE FINANCES

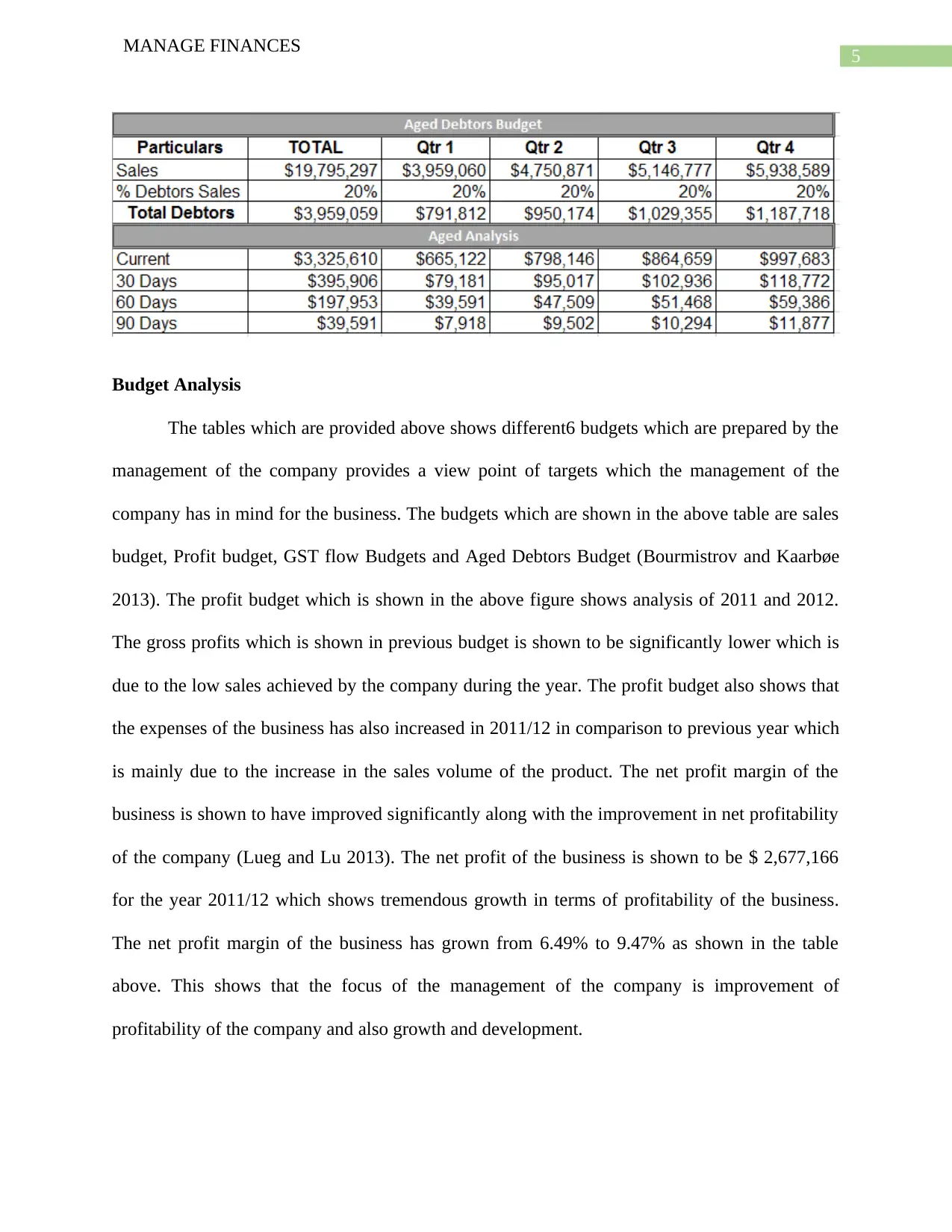

Budget Analysis

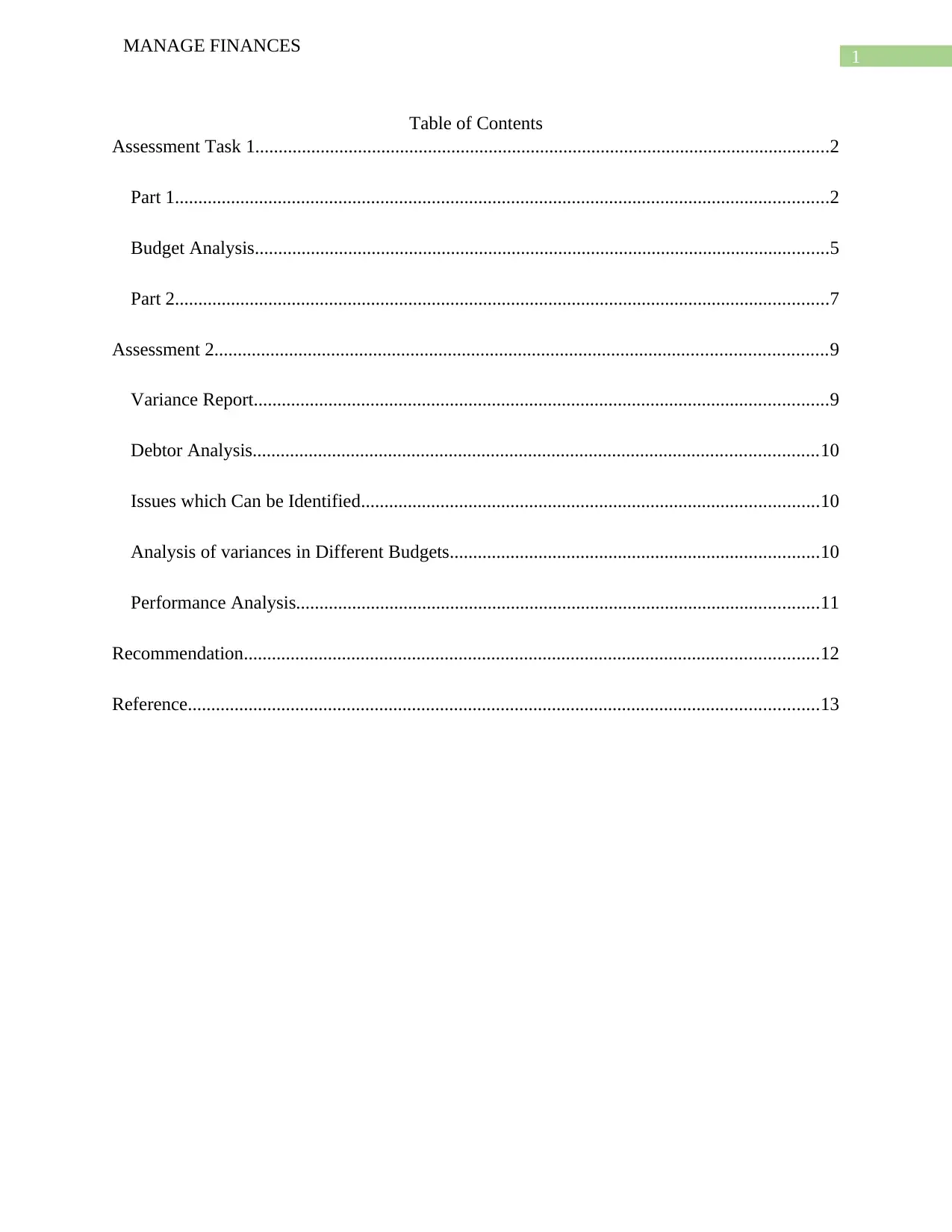

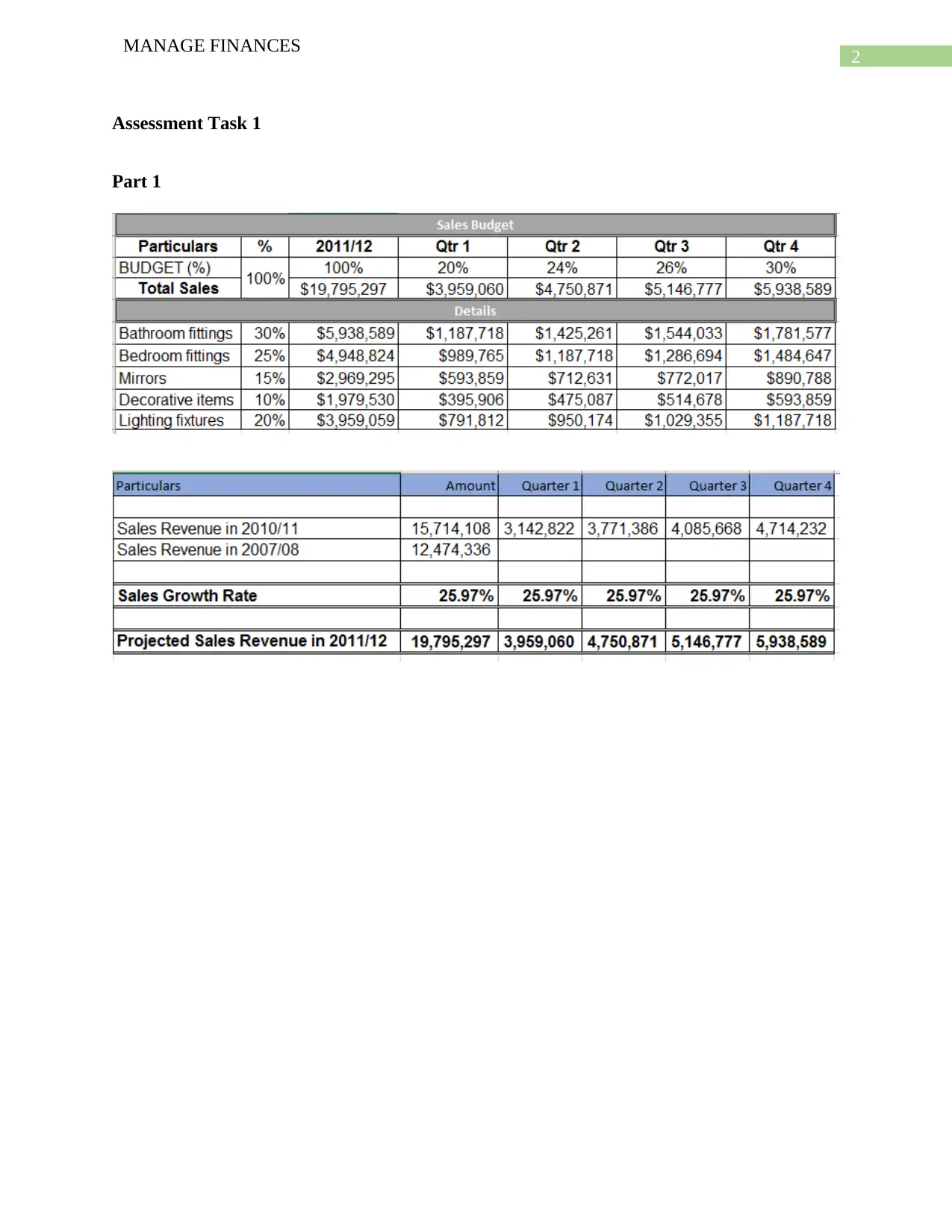

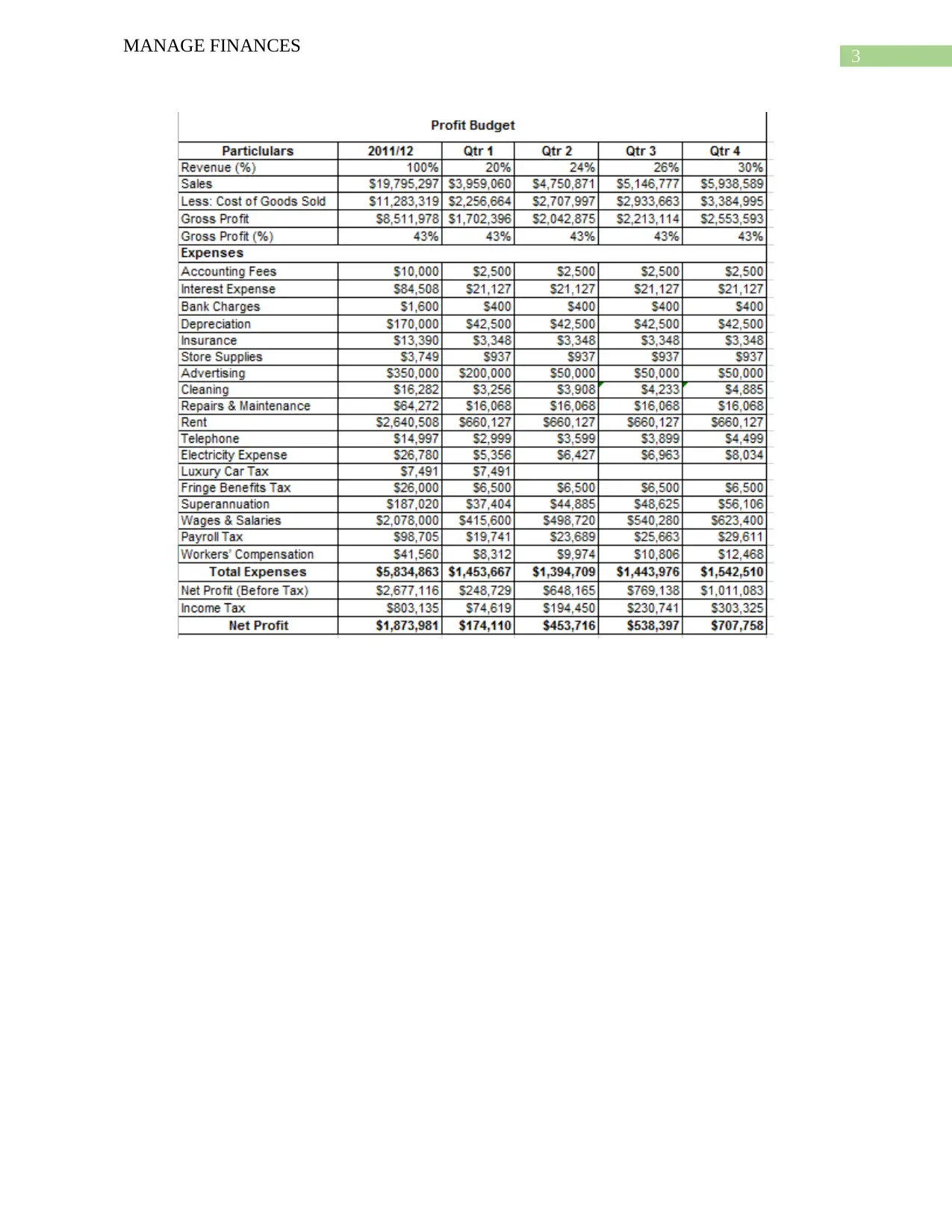

The tables which are provided above shows different6 budgets which are prepared by the

management of the company provides a view point of targets which the management of the

company has in mind for the business. The budgets which are shown in the above table are sales

budget, Profit budget, GST flow Budgets and Aged Debtors Budget (Bourmistrov and Kaarbøe

2013). The profit budget which is shown in the above figure shows analysis of 2011 and 2012.

The gross profits which is shown in previous budget is shown to be significantly lower which is

due to the low sales achieved by the company during the year. The profit budget also shows that

the expenses of the business has also increased in 2011/12 in comparison to previous year which

is mainly due to the increase in the sales volume of the product. The net profit margin of the

business is shown to have improved significantly along with the improvement in net profitability

of the company (Lueg and Lu 2013). The net profit of the business is shown to be $ 2,677,166

for the year 2011/12 which shows tremendous growth in terms of profitability of the business.

The net profit margin of the business has grown from 6.49% to 9.47% as shown in the table

above. This shows that the focus of the management of the company is improvement of

profitability of the company and also growth and development.

MANAGE FINANCES

Budget Analysis

The tables which are provided above shows different6 budgets which are prepared by the

management of the company provides a view point of targets which the management of the

company has in mind for the business. The budgets which are shown in the above table are sales

budget, Profit budget, GST flow Budgets and Aged Debtors Budget (Bourmistrov and Kaarbøe

2013). The profit budget which is shown in the above figure shows analysis of 2011 and 2012.

The gross profits which is shown in previous budget is shown to be significantly lower which is

due to the low sales achieved by the company during the year. The profit budget also shows that

the expenses of the business has also increased in 2011/12 in comparison to previous year which

is mainly due to the increase in the sales volume of the product. The net profit margin of the

business is shown to have improved significantly along with the improvement in net profitability

of the company (Lueg and Lu 2013). The net profit of the business is shown to be $ 2,677,166

for the year 2011/12 which shows tremendous growth in terms of profitability of the business.

The net profit margin of the business has grown from 6.49% to 9.47% as shown in the table

above. This shows that the focus of the management of the company is improvement of

profitability of the company and also growth and development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGE FINANCES

The financial management practices of the business which is shown in the case study is

inappropriate in nature. The management does not have a clear practice regarding the cash

management policies of the business and even asset management system is inappropriate. The

debtor management system is a crucial part of the business and the same is not maintained

appropriately (Gorgotskaya and Selyutina 2013). As the customer base of the business increases

so will the debtors balance and the internal control of the business is not appropriate to

effectively maintain the same. In addition to this, the reconciliation of debtor balances is not

done appropriately on a monthly basis and therefore regular maintenance and monitoring of

records are not done.

The basic assumptions which are taken for the preparation of budgets for sales is that the

units which are produced by the business during the year are sold off without any closing stocks.

The percentage of credit sales which are considered in preparation of the budget is also shown in

the tables above. The quarter wise sales percentage is also shown in the tables which is provided

above. The increase and decrease in sales figures and the respective GST amounts are also

shown in the figure above.

The monitoring and implementation of the budget is to be carried out by the top-level

management of the company. The management of the company sets the standards which the

business needs to follow and implement the plans by ensuring proper supervision is maintained

in the business.

MANAGE FINANCES

The financial management practices of the business which is shown in the case study is

inappropriate in nature. The management does not have a clear practice regarding the cash

management policies of the business and even asset management system is inappropriate. The

debtor management system is a crucial part of the business and the same is not maintained

appropriately (Gorgotskaya and Selyutina 2013). As the customer base of the business increases

so will the debtors balance and the internal control of the business is not appropriate to

effectively maintain the same. In addition to this, the reconciliation of debtor balances is not

done appropriately on a monthly basis and therefore regular maintenance and monitoring of

records are not done.

The basic assumptions which are taken for the preparation of budgets for sales is that the

units which are produced by the business during the year are sold off without any closing stocks.

The percentage of credit sales which are considered in preparation of the budget is also shown in

the tables above. The quarter wise sales percentage is also shown in the tables which is provided

above. The increase and decrease in sales figures and the respective GST amounts are also

shown in the figure above.

The monitoring and implementation of the budget is to be carried out by the top-level

management of the company. The management of the company sets the standards which the

business needs to follow and implement the plans by ensuring proper supervision is maintained

in the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGE FINANCES

Part 2

The different taxes which are applicable on the business of Houzit are GST provision,

income tax provision and different types of taxes which are applicable to the business of Houzit.

The relevant taxes which are in force are applicable on the business.

The management of Houzit needs to focus on the rules and regulations which are set in

Corporation Act 2001. The management of the company needs to comply with section 111AA

and division 2 and division 3 in order to ensure that all relevant regulations are followed by the

company.

The management of Houzit is planning to bring about growth in the business and also

increase the sales revenue of the business. The management also needs to focus on the recording

and monitoring of the revenues and expenses of the business. The management can implement

ERP system or Sage Accounting software in order to maintain and improve the reporting

structure of the business (Wyslocka, and Jelonek 2015). The adoption of ERP system would be

most appropriate as the same will provide the option to the management to record, maintain and

analyze the financial information to the company.

The matching principle states that the expenses of the business should match the revenue

which is generated by the business during the year. The management needs to consider the

estimated revenue which the business plans to achieve and on the basis of the revenue the costs

of the business (Borowczyk-Martins, Jolivet and Postel-Vinay 2013). Account groups are

different accounts which are considered while preparing the mater records. The account groups

are integral when a business is preparing a budget of the company. The timeline of a budget

MANAGE FINANCES

Part 2

The different taxes which are applicable on the business of Houzit are GST provision,

income tax provision and different types of taxes which are applicable to the business of Houzit.

The relevant taxes which are in force are applicable on the business.

The management of Houzit needs to focus on the rules and regulations which are set in

Corporation Act 2001. The management of the company needs to comply with section 111AA

and division 2 and division 3 in order to ensure that all relevant regulations are followed by the

company.

The management of Houzit is planning to bring about growth in the business and also

increase the sales revenue of the business. The management also needs to focus on the recording

and monitoring of the revenues and expenses of the business. The management can implement

ERP system or Sage Accounting software in order to maintain and improve the reporting

structure of the business (Wyslocka, and Jelonek 2015). The adoption of ERP system would be

most appropriate as the same will provide the option to the management to record, maintain and

analyze the financial information to the company.

The matching principle states that the expenses of the business should match the revenue

which is generated by the business during the year. The management needs to consider the

estimated revenue which the business plans to achieve and on the basis of the revenue the costs

of the business (Borowczyk-Martins, Jolivet and Postel-Vinay 2013). Account groups are

different accounts which are considered while preparing the mater records. The account groups

are integral when a business is preparing a budget of the company. The timeline of a budget

8

MANAGE FINANCES

refers to the minimum time which the management will be requiring to achieve the goals of the

business which can be short term in nature.

The principle of probity is to ensure the policies of honesty, decency and moral principles

are followed while preparing and implementing budgeting practices. This is to be done in order

to ensure that the budget is showing true and fair view and accurate information reflecting the

current capability of the business.

The critical dates which are to be considered are the quarterly target dates on which the

performance of the business is to be monitored and also the timeline in which the project is to be

completed.

The management needs to identify more costs which are associated with day to day

operations of the business. The management also needs to identify the source of different costs

which can be direct nature or indirect nature.

In order to bring about appropriate improvements in the process and procedures the

internal control system of the business needs to be improved. The introduction of new

accounting information system will bring about significant improvement in the reporting

framework of the business.

MANAGE FINANCES

refers to the minimum time which the management will be requiring to achieve the goals of the

business which can be short term in nature.

The principle of probity is to ensure the policies of honesty, decency and moral principles

are followed while preparing and implementing budgeting practices. This is to be done in order

to ensure that the budget is showing true and fair view and accurate information reflecting the

current capability of the business.

The critical dates which are to be considered are the quarterly target dates on which the

performance of the business is to be monitored and also the timeline in which the project is to be

completed.

The management needs to identify more costs which are associated with day to day

operations of the business. The management also needs to identify the source of different costs

which can be direct nature or indirect nature.

In order to bring about appropriate improvements in the process and procedures the

internal control system of the business needs to be improved. The introduction of new

accounting information system will bring about significant improvement in the reporting

framework of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGE FINANCES

Assessment 2

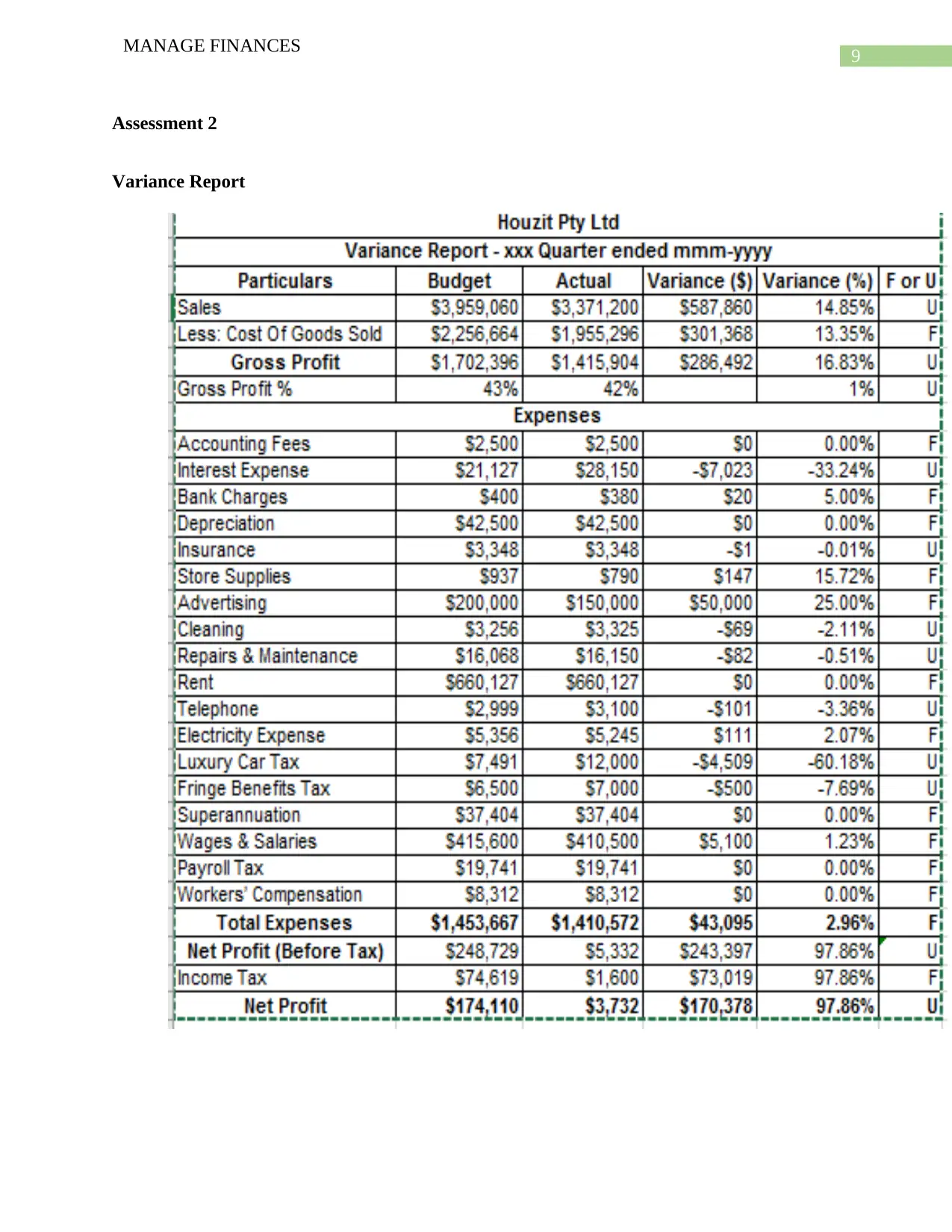

Variance Report

MANAGE FINANCES

Assessment 2

Variance Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGE FINANCES

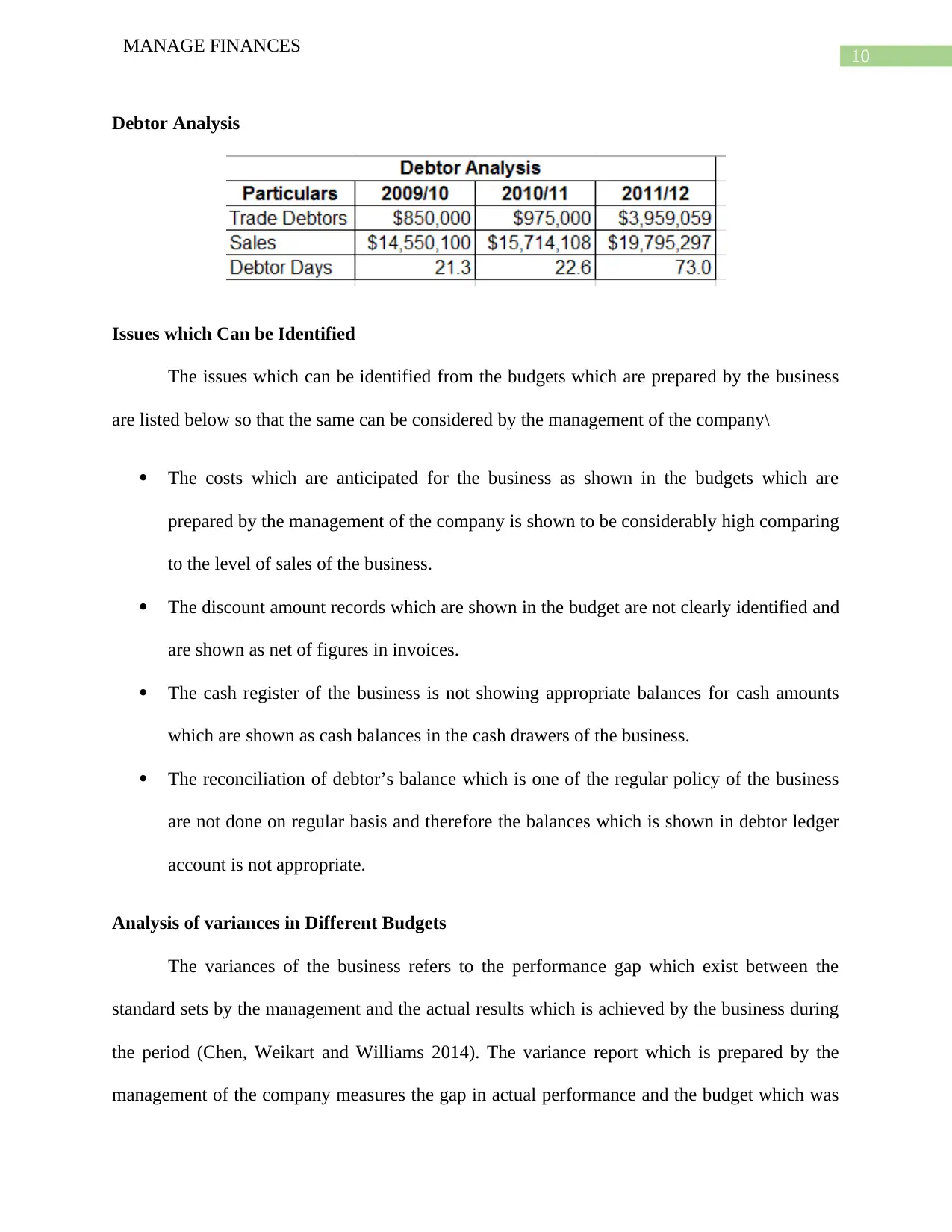

Debtor Analysis

Issues which Can be Identified

The issues which can be identified from the budgets which are prepared by the business

are listed below so that the same can be considered by the management of the company\

The costs which are anticipated for the business as shown in the budgets which are

prepared by the management of the company is shown to be considerably high comparing

to the level of sales of the business.

The discount amount records which are shown in the budget are not clearly identified and

are shown as net of figures in invoices.

The cash register of the business is not showing appropriate balances for cash amounts

which are shown as cash balances in the cash drawers of the business.

The reconciliation of debtor’s balance which is one of the regular policy of the business

are not done on regular basis and therefore the balances which is shown in debtor ledger

account is not appropriate.

Analysis of variances in Different Budgets

The variances of the business refers to the performance gap which exist between the

standard sets by the management and the actual results which is achieved by the business during

the period (Chen, Weikart and Williams 2014). The variance report which is prepared by the

management of the company measures the gap in actual performance and the budget which was

MANAGE FINANCES

Debtor Analysis

Issues which Can be Identified

The issues which can be identified from the budgets which are prepared by the business

are listed below so that the same can be considered by the management of the company\

The costs which are anticipated for the business as shown in the budgets which are

prepared by the management of the company is shown to be considerably high comparing

to the level of sales of the business.

The discount amount records which are shown in the budget are not clearly identified and

are shown as net of figures in invoices.

The cash register of the business is not showing appropriate balances for cash amounts

which are shown as cash balances in the cash drawers of the business.

The reconciliation of debtor’s balance which is one of the regular policy of the business

are not done on regular basis and therefore the balances which is shown in debtor ledger

account is not appropriate.

Analysis of variances in Different Budgets

The variances of the business refers to the performance gap which exist between the

standard sets by the management and the actual results which is achieved by the business during

the period (Chen, Weikart and Williams 2014). The variance report which is prepared by the

management of the company measures the gap in actual performance and the budget which was

11

MANAGE FINANCES

set by the business in pursuance of the goals of the business. The variance report shows that the

sales result for the current year is much lower than the figure which was anticipated by the

management and therefore the balance is shown to be unfavorable in nature (Jansen and Zarges

2014). The gross margin and net margin of the business is also shown to be unfavorable in nature

which is mainly due to the lower figure of sales which is achieved by the business in the current

year and also due to the high costs which are incurred by the business during the period.

Performance Analysis

As per the performance of the business in terms of the industry is the business is doing

well. The retail industry is on the verge of further developments as there is high growth and

profitability for businesses. In addition to this, the level of competition is also very high in such

an industry which can also be one of the reason for the high costs as the costs of the resources are

also high (Yu, Ramanathan and Nath 2014). The sales which is achieved by the business is

reasonable but improvements can be made in the same.

As per the debtor’s policy of the business, the management of the company is increasing

the credit period which is allowed to such debtors. The overall debtors of the business have

improved significantly over the years which is mainly due to credit sales undertaken by the

business. The debtor analysis which is shown above, the credit sales of the business has

increased exponentially in 2011/12 which is due to the increase in credit policy. However, it is to

be noted that the increase in credit period will also block the funds of the business for a longer

period and thereby affecting the liquidity of the business.

MANAGE FINANCES

set by the business in pursuance of the goals of the business. The variance report shows that the

sales result for the current year is much lower than the figure which was anticipated by the

management and therefore the balance is shown to be unfavorable in nature (Jansen and Zarges

2014). The gross margin and net margin of the business is also shown to be unfavorable in nature

which is mainly due to the lower figure of sales which is achieved by the business in the current

year and also due to the high costs which are incurred by the business during the period.

Performance Analysis

As per the performance of the business in terms of the industry is the business is doing

well. The retail industry is on the verge of further developments as there is high growth and

profitability for businesses. In addition to this, the level of competition is also very high in such

an industry which can also be one of the reason for the high costs as the costs of the resources are

also high (Yu, Ramanathan and Nath 2014). The sales which is achieved by the business is

reasonable but improvements can be made in the same.

As per the debtor’s policy of the business, the management of the company is increasing

the credit period which is allowed to such debtors. The overall debtors of the business have

improved significantly over the years which is mainly due to credit sales undertaken by the

business. The debtor analysis which is shown above, the credit sales of the business has

increased exponentially in 2011/12 which is due to the increase in credit policy. However, it is to

be noted that the increase in credit period will also block the funds of the business for a longer

period and thereby affecting the liquidity of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.