Corporate Accounting Report: Financial Analysis of Rio Tinto (2016)

VerifiedAdded on 2020/06/04

|12

|2893

|33

Report

AI Summary

This report provides a comprehensive analysis of Rio Tinto's financial performance based on its 2016 annual report. It delves into various aspects of corporate accounting, including the roles of independent directors, their qualifications, and experiences. The report examines the company's profitability, dividend payments, equity growth, and future growth opportunities, while also addressing current business challenges and contributions to social and environmental sustainability. Furthermore, it explores the types of leases used by Rio Tinto, their treatment in the annual report, and the advantages and disadvantages of leasing. The report also covers key aspects of consolidation financial statements and the impact of income tax. Overall, the analysis offers valuable insights into Rio Tinto's financial health and strategic decisions.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

PART 1............................................................................................................................................1

1. Independent directors of the company...............................................................................1

2. Number of directors of each gender...................................................................................2

3. Qualification of three directors...........................................................................................2

4. Experience of these three directors.....................................................................................2

5. Were they on other boards .................................................................................................3

PART 2 (REPORT).........................................................................................................................3

1. Profitability level of the company and stability of level in past years...............................3

2. Regarding dividend payment and growth of Equity in recent year....................................3

3. Opportunity for the future growth .....................................................................................4

4. Challenges in the current business activities......................................................................4

5. Contribution to social and environmental sustainability....................................................4

QUESTION 2...................................................................................................................................5

PART 1............................................................................................................................................5

1. A) Types of lease Rio Tinto used for its offices or properties...........................................5

B) Lease used for equipment or other assets..........................................................................5

2. Requirement of particular type of each case......................................................................5

3. Treatment of leases in company's Annual report 2016......................................................5

4. Advantages and disadvantage of lease...............................................................................5

PART 2............................................................................................................................................6

1. Identify types of lease.........................................................................................................6

2. Critical analysis of leasing..................................................................................................6

QUESTION 3...................................................................................................................................6

A. Key aspects of consolidation financial statements............................................................6

B. Impact of income tax on consolidate statements...............................................................7

C. To convert unrealised profits into realised profits.............................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

PART 1............................................................................................................................................1

1. Independent directors of the company...............................................................................1

2. Number of directors of each gender...................................................................................2

3. Qualification of three directors...........................................................................................2

4. Experience of these three directors.....................................................................................2

5. Were they on other boards .................................................................................................3

PART 2 (REPORT).........................................................................................................................3

1. Profitability level of the company and stability of level in past years...............................3

2. Regarding dividend payment and growth of Equity in recent year....................................3

3. Opportunity for the future growth .....................................................................................4

4. Challenges in the current business activities......................................................................4

5. Contribution to social and environmental sustainability....................................................4

QUESTION 2...................................................................................................................................5

PART 1............................................................................................................................................5

1. A) Types of lease Rio Tinto used for its offices or properties...........................................5

B) Lease used for equipment or other assets..........................................................................5

2. Requirement of particular type of each case......................................................................5

3. Treatment of leases in company's Annual report 2016......................................................5

4. Advantages and disadvantage of lease...............................................................................5

PART 2............................................................................................................................................6

1. Identify types of lease.........................................................................................................6

2. Critical analysis of leasing..................................................................................................6

QUESTION 3...................................................................................................................................6

A. Key aspects of consolidation financial statements............................................................6

B. Impact of income tax on consolidate statements...............................................................7

C. To convert unrealised profits into realised profits.............................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is a branch of accounting which deals with articular areas of

finance that examine the financial decision of business firm. It consists of various aspects of

accounting such as investment or capital budgeting and financing decision as well as daily

operations of company (Bhasin, 2015). Under this accounting system measurement, recording

and analysis of financial data is related with the limited company. The project report consists of

various financial questions of RIO TINTO company which is an Australian firm. On the basis of

company's annual report for financial year 2016, the analysis is been done here in the report.

Further, the overall project evaluation is done in order to get useful information about company’s

performance.

QUESTION 1

PART 1

1. Independent directors of the company

In Rio Tinto plc have a common board of directors. They all are responsible for the

growth and development of the company and, through the independent supervision of

management, is responsible to shareholders for the execution of the business operations. The

total number of independent directors are 12. Those are:

Megan Clark AC

Robert Brown

David Constable

Ann Godbehere

Anne Lauvergeon

Hon. Paul Tellier

Sam Laidlaw

Michael L Estrange AO

Simon Thompson

John Varley

Simon Henry

Richard Goodmanson

1

Corporate accounting is a branch of accounting which deals with articular areas of

finance that examine the financial decision of business firm. It consists of various aspects of

accounting such as investment or capital budgeting and financing decision as well as daily

operations of company (Bhasin, 2015). Under this accounting system measurement, recording

and analysis of financial data is related with the limited company. The project report consists of

various financial questions of RIO TINTO company which is an Australian firm. On the basis of

company's annual report for financial year 2016, the analysis is been done here in the report.

Further, the overall project evaluation is done in order to get useful information about company’s

performance.

QUESTION 1

PART 1

1. Independent directors of the company

In Rio Tinto plc have a common board of directors. They all are responsible for the

growth and development of the company and, through the independent supervision of

management, is responsible to shareholders for the execution of the business operations. The

total number of independent directors are 12. Those are:

Megan Clark AC

Robert Brown

David Constable

Ann Godbehere

Anne Lauvergeon

Hon. Paul Tellier

Sam Laidlaw

Michael L Estrange AO

Simon Thompson

John Varley

Simon Henry

Richard Goodmanson

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

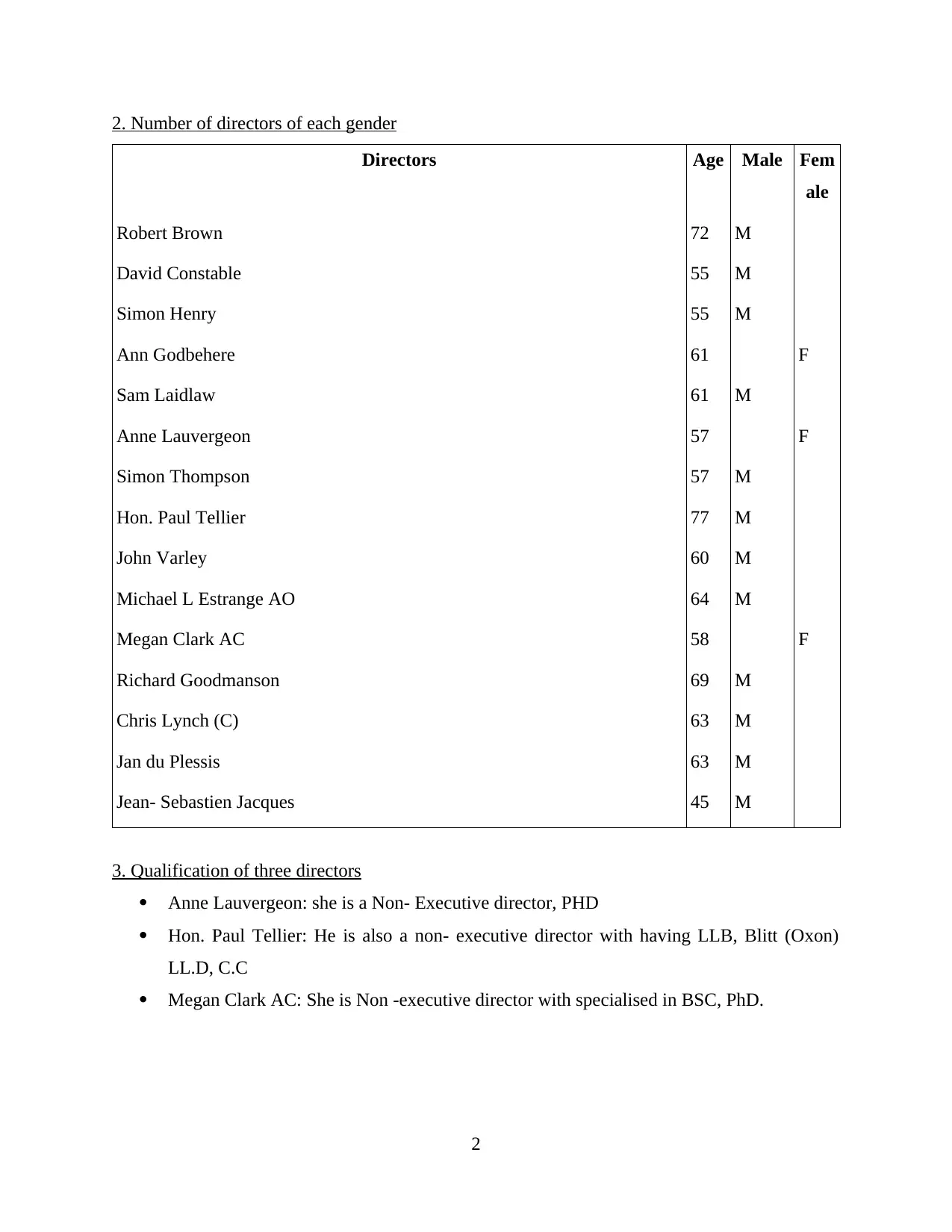

2. Number of directors of each gender

Directors Age Male Fem

ale

Robert Brown 72 M

David Constable 55 M

Simon Henry 55 M

Ann Godbehere 61 F

Sam Laidlaw 61 M

Anne Lauvergeon 57 F

Simon Thompson 57 M

Hon. Paul Tellier 77 M

John Varley 60 M

Michael L Estrange AO 64 M

Megan Clark AC 58 F

Richard Goodmanson 69 M

Chris Lynch (C) 63 M

Jan du Plessis 63 M

Jean- Sebastien Jacques 45 M

3. Qualification of three directors

Anne Lauvergeon: she is a Non- Executive director, PHD

Hon. Paul Tellier: He is also a non- executive director with having LLB, Blitt (Oxon)

LL.D, C.C

Megan Clark AC: She is Non -executive director with specialised in BSC, PhD.

2

Directors Age Male Fem

ale

Robert Brown 72 M

David Constable 55 M

Simon Henry 55 M

Ann Godbehere 61 F

Sam Laidlaw 61 M

Anne Lauvergeon 57 F

Simon Thompson 57 M

Hon. Paul Tellier 77 M

John Varley 60 M

Michael L Estrange AO 64 M

Megan Clark AC 58 F

Richard Goodmanson 69 M

Chris Lynch (C) 63 M

Jan du Plessis 63 M

Jean- Sebastien Jacques 45 M

3. Qualification of three directors

Anne Lauvergeon: she is a Non- Executive director, PHD

Hon. Paul Tellier: He is also a non- executive director with having LLB, Blitt (Oxon)

LL.D, C.C

Megan Clark AC: She is Non -executive director with specialised in BSC, PhD.

2

4. Experience of these three directors

Anne Lauvergeon: She is a French citizen, has a strong board strategic and general

management experience in various sectors (Zadek, Evans and Pruzan, 2013). Like energy,

communication and financial services. In year 1983, she started her professional career in steel

industry and in 1990, she become advisor for economic international affairs at French

presidency.

Hon. Paul Tellier: He has a great experience in corporate sector and the civil services.

Megan Clark AC: She had an extensive career in both private and public sector,

combining all its expertise in metals and mining business with high level of experience in

science, research and technology.

5. Were they on other boards

Anne Lauvergeon: Yes, she belongs to other boards also. For nomination committees

and sustainability committee and part of Independent board of director.

Hon. Paul Tellier: He is also be the part of other board. Such as Audit, remuneration,

Nomination and Independent.

Megan Clark AC: She also work for sustainability committee, nomination, remuneration

as well as independent committees under this company.

PART 2 (REPORT)

1. Profitability level of the company and stability of level in past years

Profitability level of \ company is much more appropriate level as in 2016, total net profit

generated by the company is 6,343 US$m. after meeting out all those expenses which are used

during production process Rio Tinto is able to incurred a sufficient amount of profit during the

year (Brown, Beekes and Verhoeven 2011, p.96-172). If we, compare it with last few years, it

has been seen that in last year it was in -726US$m. If going back, the results are favourable as in

2013 company has generated a profit of 3505m and in 2014 it was 9552m. The overall results are

fluctuating in past year. The profitability position of the company are favourable in current year

as compare to past.

Gross profit Margin: Gross profit / Net sales

: 6343 / 33781 *100= 18.77%

3

Anne Lauvergeon: She is a French citizen, has a strong board strategic and general

management experience in various sectors (Zadek, Evans and Pruzan, 2013). Like energy,

communication and financial services. In year 1983, she started her professional career in steel

industry and in 1990, she become advisor for economic international affairs at French

presidency.

Hon. Paul Tellier: He has a great experience in corporate sector and the civil services.

Megan Clark AC: She had an extensive career in both private and public sector,

combining all its expertise in metals and mining business with high level of experience in

science, research and technology.

5. Were they on other boards

Anne Lauvergeon: Yes, she belongs to other boards also. For nomination committees

and sustainability committee and part of Independent board of director.

Hon. Paul Tellier: He is also be the part of other board. Such as Audit, remuneration,

Nomination and Independent.

Megan Clark AC: She also work for sustainability committee, nomination, remuneration

as well as independent committees under this company.

PART 2 (REPORT)

1. Profitability level of the company and stability of level in past years

Profitability level of \ company is much more appropriate level as in 2016, total net profit

generated by the company is 6,343 US$m. after meeting out all those expenses which are used

during production process Rio Tinto is able to incurred a sufficient amount of profit during the

year (Brown, Beekes and Verhoeven 2011, p.96-172). If we, compare it with last few years, it

has been seen that in last year it was in -726US$m. If going back, the results are favourable as in

2013 company has generated a profit of 3505m and in 2014 it was 9552m. The overall results are

fluctuating in past year. The profitability position of the company are favourable in current year

as compare to past.

Gross profit Margin: Gross profit / Net sales

: 6343 / 33781 *100= 18.77%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Regarding dividend payment and growth of Equity in recent year

In the initial stages which was started in 2007, the company is paying a healthy amount

as divided to its shareholders. In coming next year it was increases at a sufficient price in 2014 -

15 it become constant at 215.00c. Now, in current year it fall drastically with 170.00c. So the

fall in dividend rate in last few year are:

In 2016: 170, 2015: 215.00

Dividend changes: 215-170 /215 *100= -20 %. A fall of 20% in current year in dividend are

recorded.

While, equity portion of company in the recent year is 13%. In comparison to last few

year they are fluctuating with specific percentage. In 2015 it is 11% which is low as compare to

current year. In 2015, it is the most effective percentage recorded in equity portion for the

company (Bodie, 2013). Because it is very low as from the last so many years of working.

3. Opportunity for the future growth

After making a proper analysis of the annual report of Rio Tinto. It has been found that

company is very much healthy position to expand their business in different parts of the country.

It if financial strong and have the potential to implement new unit into various level. For the

investors it has made a great growth opportunity to invest under there project. Employment

opportunity are also been created by the company to explore new skills and knowledge. So that

more effective results can be generated in coming time. The current mining sectors are growing

at a positive rate and the company have the chance to make expansion. So that maximum

productivity and profitability can be achieved by in next year.

4. Challenges in the current business activities

As it has been observed that current stage in the mining sectors had a tremendous

opportunity for innovation. This is time for the mining sectors to embrace technology and

business model innovation. They are developing a great transformation in building competitive

advantages over other competitors. There are so many other companies which are associated in

same business will be the huge challenge for Rio Tinto to compete against them. Such as BHP

Billiton is one of the company which is dealing in same business and one of the top most

company in Australia (Du and DU 2010, p.017). To make their product more effective is going

to be the huge challenge for Rio Tinto in coming time.

4

In the initial stages which was started in 2007, the company is paying a healthy amount

as divided to its shareholders. In coming next year it was increases at a sufficient price in 2014 -

15 it become constant at 215.00c. Now, in current year it fall drastically with 170.00c. So the

fall in dividend rate in last few year are:

In 2016: 170, 2015: 215.00

Dividend changes: 215-170 /215 *100= -20 %. A fall of 20% in current year in dividend are

recorded.

While, equity portion of company in the recent year is 13%. In comparison to last few

year they are fluctuating with specific percentage. In 2015 it is 11% which is low as compare to

current year. In 2015, it is the most effective percentage recorded in equity portion for the

company (Bodie, 2013). Because it is very low as from the last so many years of working.

3. Opportunity for the future growth

After making a proper analysis of the annual report of Rio Tinto. It has been found that

company is very much healthy position to expand their business in different parts of the country.

It if financial strong and have the potential to implement new unit into various level. For the

investors it has made a great growth opportunity to invest under there project. Employment

opportunity are also been created by the company to explore new skills and knowledge. So that

more effective results can be generated in coming time. The current mining sectors are growing

at a positive rate and the company have the chance to make expansion. So that maximum

productivity and profitability can be achieved by in next year.

4. Challenges in the current business activities

As it has been observed that current stage in the mining sectors had a tremendous

opportunity for innovation. This is time for the mining sectors to embrace technology and

business model innovation. They are developing a great transformation in building competitive

advantages over other competitors. There are so many other companies which are associated in

same business will be the huge challenge for Rio Tinto to compete against them. Such as BHP

Billiton is one of the company which is dealing in same business and one of the top most

company in Australia (Du and DU 2010, p.017). To make their product more effective is going

to be the huge challenge for Rio Tinto in coming time.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Contribution to social and environmental sustainability

Producing minerals and metals is more important for the sustaining and growing social

well-being. It is necessary for the human progress. Company's activities can affect the people,

communities and the environment as well. Rio Tinto is contributing to sustainable development

underpins company's ongoing commercial outcomes. It make more benefits to shareholders,

partners, customers and employees (Lee, 2014). The concern sustainability committee ensure

that approach is consistent with Rio Tinto's vision and values, that materiality risks are managed

effectively. Or other activities must be contribution to sustainable development. Some of the

programs which are organised by the company are:

Rolling out the CRM programme across more than 60 operational sites, resulting in 1.3 m

risk verification.

25.9 per cent reduction in our greenhouse gas emissions intensity from 2008; 7

percentage improvement from last year.

QUESTION 2

PART 1

1. A) Types of lease Rio Tinto used for its offices or properties

Financial lease is been used by Rio Tinto in case of offices or properties. Because they

are based on company long term investments which are covered in more than one year time.

B) Lease used for equipment or other assets

Operating lease is been used by the company in order to meet out its expenses which are

incurred by company during one year of time.

2. Requirement of particular type of each case

As it has been observed that in case of office and properties leasing can be taken for very

long time. So that their operations can be performed. While, if operating lease is considered as

short term lease which is taken for less than one year time. The residual risk is not applicable in

finance lease as compare to operating lease it is beard by leasing company if a maintenance

contract is taken.

5

Producing minerals and metals is more important for the sustaining and growing social

well-being. It is necessary for the human progress. Company's activities can affect the people,

communities and the environment as well. Rio Tinto is contributing to sustainable development

underpins company's ongoing commercial outcomes. It make more benefits to shareholders,

partners, customers and employees (Lee, 2014). The concern sustainability committee ensure

that approach is consistent with Rio Tinto's vision and values, that materiality risks are managed

effectively. Or other activities must be contribution to sustainable development. Some of the

programs which are organised by the company are:

Rolling out the CRM programme across more than 60 operational sites, resulting in 1.3 m

risk verification.

25.9 per cent reduction in our greenhouse gas emissions intensity from 2008; 7

percentage improvement from last year.

QUESTION 2

PART 1

1. A) Types of lease Rio Tinto used for its offices or properties

Financial lease is been used by Rio Tinto in case of offices or properties. Because they

are based on company long term investments which are covered in more than one year time.

B) Lease used for equipment or other assets

Operating lease is been used by the company in order to meet out its expenses which are

incurred by company during one year of time.

2. Requirement of particular type of each case

As it has been observed that in case of office and properties leasing can be taken for very

long time. So that their operations can be performed. While, if operating lease is considered as

short term lease which is taken for less than one year time. The residual risk is not applicable in

finance lease as compare to operating lease it is beard by leasing company if a maintenance

contract is taken.

5

3. Treatment of leases in company's Annual report 2016

The financial lease are recorded into balance sheet of the company. While operating lease

are shown outside of balance sheets.

4. Advantages and disadvantage of lease

Lease agreements is a term which means a contract between two parties in which owner

of asset grant permission to another contractor to use it in place of something as a security.

Hence in this type of agreements owner is act as a lessor and user is seen as a lessee. Therefore,

lease contracts has been classified into two categories which are having few benefits and

drawbacks are stated as follows:-

Finance lease: - According to this segment risk has been transferred lessee where it puts

lessee in a similar circumstances (Belal and Cooper 2011, p.654-667). One of a major benefit of

this category is that it allows user to use an asset whereas, drawback is that in this user don't have

any authority to make any alterations or improvements in asset.

Operating lease: - Other than finance is consider as a operating lease in which risk is not

transferred by lessor to lessee which is beneficial for user but creates barrier for owner (Finance

Lease, 2017).

Lease standard AASB 117 was amended and enforced by international accounting

standard board whose main motive is to prescribe for lessors and user of asset an effective

financial policies and disclosure for applying linking with leases.

PART 2

1. Identify types of lease

The lease arrangement said to be an operating lease. As because, a lessee uses the assets

for a term period of less than a life which is mentioned under the situation. Generally, less than

75% of its total life.

6

The financial lease are recorded into balance sheet of the company. While operating lease

are shown outside of balance sheets.

4. Advantages and disadvantage of lease

Lease agreements is a term which means a contract between two parties in which owner

of asset grant permission to another contractor to use it in place of something as a security.

Hence in this type of agreements owner is act as a lessor and user is seen as a lessee. Therefore,

lease contracts has been classified into two categories which are having few benefits and

drawbacks are stated as follows:-

Finance lease: - According to this segment risk has been transferred lessee where it puts

lessee in a similar circumstances (Belal and Cooper 2011, p.654-667). One of a major benefit of

this category is that it allows user to use an asset whereas, drawback is that in this user don't have

any authority to make any alterations or improvements in asset.

Operating lease: - Other than finance is consider as a operating lease in which risk is not

transferred by lessor to lessee which is beneficial for user but creates barrier for owner (Finance

Lease, 2017).

Lease standard AASB 117 was amended and enforced by international accounting

standard board whose main motive is to prescribe for lessors and user of asset an effective

financial policies and disclosure for applying linking with leases.

PART 2

1. Identify types of lease

The lease arrangement said to be an operating lease. As because, a lessee uses the assets

for a term period of less than a life which is mentioned under the situation. Generally, less than

75% of its total life.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Critical analysis of leasing

According to AASB 117, if a sale and leaseback transactions are results in finance lease,

any excess amount of sales proceeds over the carrying cost shall not be recognised as income by

a seller-lessee. While if sale is made on operating lease and it was cleared that transaction is

made at fair value, any profit and loss is recognised immediately. Under the situation of Triton

Ltd it was clear that sale was made at fair value that fulfil the criteria of operating leasing.

QUESTION 3

A. Key aspects of consolidation financial statements

Consolidated financial statement: These are those financial statements of a group in

which the equity, liabilities, assets and cash flow of the parent company and its units are given as

those of individual economic entity. There are some important key points in relation to these

statements:

It consists of a parent business entity to represent consolidated financial statements.

The principle of authority and control are determine as the major base for the

consolidation under the company. It is done in order to make it more effective and

accurate.

It set a benchmark that how to apply the principle of control to know that an investor

should be able to control an investee and also must merge the investee (Burritt,

Schaltegger and Zvezdov 2011, p.80-98).

The requirement of accounting record in order to make consolidation to financial

statements.

Identify an investment authority and set exception to consolidate a particular units of a

single investment entity.

B. Impact of income tax on consolidate statements

Consolidation is based on the concept of control and changes on ownership value while

control is maintained as accounting of transaction among owners and entity. Accounting for tax

is governed by AASB 112 income Tax. Deferred tax are lifted when a short-lived difference

arise because the tax base for an assets or liabilities are decreased from the carrying costs. Some

of the consolidation adjustments get over in changing the carrying amounts of assets and

liabilities. This results a temporary difference and it does not have any changes over the tax.

7

According to AASB 117, if a sale and leaseback transactions are results in finance lease,

any excess amount of sales proceeds over the carrying cost shall not be recognised as income by

a seller-lessee. While if sale is made on operating lease and it was cleared that transaction is

made at fair value, any profit and loss is recognised immediately. Under the situation of Triton

Ltd it was clear that sale was made at fair value that fulfil the criteria of operating leasing.

QUESTION 3

A. Key aspects of consolidation financial statements

Consolidated financial statement: These are those financial statements of a group in

which the equity, liabilities, assets and cash flow of the parent company and its units are given as

those of individual economic entity. There are some important key points in relation to these

statements:

It consists of a parent business entity to represent consolidated financial statements.

The principle of authority and control are determine as the major base for the

consolidation under the company. It is done in order to make it more effective and

accurate.

It set a benchmark that how to apply the principle of control to know that an investor

should be able to control an investee and also must merge the investee (Burritt,

Schaltegger and Zvezdov 2011, p.80-98).

The requirement of accounting record in order to make consolidation to financial

statements.

Identify an investment authority and set exception to consolidate a particular units of a

single investment entity.

B. Impact of income tax on consolidate statements

Consolidation is based on the concept of control and changes on ownership value while

control is maintained as accounting of transaction among owners and entity. Accounting for tax

is governed by AASB 112 income Tax. Deferred tax are lifted when a short-lived difference

arise because the tax base for an assets or liabilities are decreased from the carrying costs. Some

of the consolidation adjustments get over in changing the carrying amounts of assets and

liabilities. This results a temporary difference and it does not have any changes over the tax.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Those cost which are different from that recorded by the acquirer of the decrease assets within an

intergroup transaction.

C. To convert unrealised profits into realised profits

By the way of acquisition, company can make their unrealised profits into realised

profits. Reverse merge is an example of this. Under this, unrealised profits are made into the

realised.

CONCLUSION

From the above project report, it has been articulated that corporate accounting is an

important aspect of Rio Tinto because their financial statements are recorded and analysed on

that basis. Various questions are being solved that are based on the annual report of 2016.

Overall, it has been found that project targets company's performance and growth in the coming

future.

8

intergroup transaction.

C. To convert unrealised profits into realised profits

By the way of acquisition, company can make their unrealised profits into realised

profits. Reverse merge is an example of this. Under this, unrealised profits are made into the

realised.

CONCLUSION

From the above project report, it has been articulated that corporate accounting is an

important aspect of Rio Tinto because their financial statements are recorded and analysed on

that basis. Various questions are being solved that are based on the annual report of 2016.

Overall, it has been found that project targets company's performance and growth in the coming

future.

8

REFERENCES

Books and Journals

Belal, A.R. and Cooper, S., 2011. The absence of corporate social responsibility reporting in

Bangladesh. Critical Perspectives on Accounting. 22(7). pp.654-667.

Bhasin, M.L., 2015. Corporate accounting fraud: A case study of Satyam Computers Limited.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brown, P., Beekes, W. and Verhoeven, P., 2011. Corporate governance, accounting and finance:

A review. Accounting & finance. 51(1). pp.96-172.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting:

explaining practice in leading German companies. Australian Accounting Review. 21(1).

pp.80-98.

DU, X.Q. and DU, Y.J., 2010. Charitable Donation, Accounting Performance and Market

Performance: Empirical Evidences from Wenchuan Earthquake [J]. Contemporary

Finance & Economics. 2. p.017.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging practice

in social and ethical accounting and auditing. Routledge.

Online

Finance Lease. 2017.[Online]. Available Through:

<https://www.contracthireandleasing.com/guides/finance-lease/>. [Accessed on 14th

September 2017].

9

Books and Journals

Belal, A.R. and Cooper, S., 2011. The absence of corporate social responsibility reporting in

Bangladesh. Critical Perspectives on Accounting. 22(7). pp.654-667.

Bhasin, M.L., 2015. Corporate accounting fraud: A case study of Satyam Computers Limited.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brown, P., Beekes, W. and Verhoeven, P., 2011. Corporate governance, accounting and finance:

A review. Accounting & finance. 51(1). pp.96-172.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting:

explaining practice in leading German companies. Australian Accounting Review. 21(1).

pp.80-98.

DU, X.Q. and DU, Y.J., 2010. Charitable Donation, Accounting Performance and Market

Performance: Empirical Evidences from Wenchuan Earthquake [J]. Contemporary

Finance & Economics. 2. p.017.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging practice

in social and ethical accounting and auditing. Routledge.

Online

Finance Lease. 2017.[Online]. Available Through:

<https://www.contracthireandleasing.com/guides/finance-lease/>. [Accessed on 14th

September 2017].

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.