Financial Decision Making Report: Roast Ltd Case Study Analysis

VerifiedAdded on 2023/01/11

|14

|4302

|63

Report

AI Summary

This report presents a financial analysis of Roast Ltd, focusing on its performance and investment appraisal. It begins with an industry overview, highlighting the competitive landscape of the UK coffee market and Roast Ltd's position within it. The report then delves into the business performance analysis, utilizing financial statements such as the statement of profit and loss, statement of financial position, and statement of cash flows to assess profitability, liquidity, and solvency. Ratio analysis is employed to evaluate key financial metrics, including profitability, efficiency, and solvency ratios. Furthermore, the report examines investment appraisal techniques, including management forecasts and various methods like payback period, accounting rate of return, and net present value. Finally, it explores different sources of finance, comparing their advantages and disadvantages in the context of a potential investment of £400,000. The analysis aims to provide a comprehensive understanding of Roast Ltd's financial health and decision-making processes.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report has considered the case study of Roast Ltd in this report. This report has

presented the overview of industry in which the organization used to deal. Overview of the

company includes the position of the business in the industry and amount of competition present

in the industry in which organization is dealing. After that the report has highlighted the business

performance analysis of the business. This has been presented with the help of statement of profit

and loss which has helped in analysing the profitability position of the business. After that the

report has highlighted the statement of financial position as well as of cash flow this statement

used to help in understanding the cash and cash equivalent present with the company in the

current scenario. After that in the third part of the report the report has highlighted the

investment appraisal of the company which generally includes the management forecast,

different investment Appraisal technique i.e. Payback period, accounting rate of the return and

net present value of the company in the market. After that these report goes on to explain the

comparison between two source of the finance in the organization on the basis of advantage and

disadvantage of different source of the finance which can be used by the organization at the time

of making the investment of 400,000 pounds in coming future.

This report has considered the case study of Roast Ltd in this report. This report has

presented the overview of industry in which the organization used to deal. Overview of the

company includes the position of the business in the industry and amount of competition present

in the industry in which organization is dealing. After that the report has highlighted the business

performance analysis of the business. This has been presented with the help of statement of profit

and loss which has helped in analysing the profitability position of the business. After that the

report has highlighted the statement of financial position as well as of cash flow this statement

used to help in understanding the cash and cash equivalent present with the company in the

current scenario. After that in the third part of the report the report has highlighted the

investment appraisal of the company which generally includes the management forecast,

different investment Appraisal technique i.e. Payback period, accounting rate of the return and

net present value of the company in the market. After that these report goes on to explain the

comparison between two source of the finance in the organization on the basis of advantage and

disadvantage of different source of the finance which can be used by the organization at the time

of making the investment of 400,000 pounds in coming future.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................3

INTRODUCTION...........................................................................................................................1

Industry Overview.......................................................................................................................1

Part 2 Business Performance Analysis............................................................................................1

2.1 Statement of Profit or Loss....................................................................................................1

2.2 Statement of Financial Position.............................................................................................4

2.3 Statement of Cash Flows.......................................................................................................6

PART 3 INVESTMENT APPRAISAL...........................................................................................8

3.1 a. Management forecast.........................................................................................................8

3.1 b. Investment appraisal technique..........................................................................................8

3.2 Sources of finance................................................................................................................10

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................3

INTRODUCTION...........................................................................................................................1

Industry Overview.......................................................................................................................1

Part 2 Business Performance Analysis............................................................................................1

2.1 Statement of Profit or Loss....................................................................................................1

2.2 Statement of Financial Position.............................................................................................4

2.3 Statement of Cash Flows.......................................................................................................6

PART 3 INVESTMENT APPRAISAL...........................................................................................8

3.1 a. Management forecast.........................................................................................................8

3.1 b. Investment appraisal technique..........................................................................................8

3.2 Sources of finance................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Industry Overview

Roast Ltd used to operate in the food and beverage industry of the UK. Roast Ltd. Is an

independent coffee house chain established in the UK in the year 2008. Specifically

Roast. Ltd used to operate in the coffee industry of UK. Coffee market is the fifth largest

coffee consumer market in Market.

As a result it is one of the strongest industries of the UK and used to provide good

contribution in the economy of the UK as a whole. Coffee market is very competitive

industry as there are many different organizations that used to operate in the industry.

As a result Roast Ltd used to face variety of the competition from the market, Star buck is

one of the biggest competitors of the company in the market. Starbuck generally used to

attract huge number of the customer in the market with the quality of product offered by

them.

Coffee industry is one of the successful industry of UK reason behind the same is

identified that there are good number of the consumer in the UK who used to drink

coffee. Looking at the scope of this industry it can be said that coffee industry is well

developed in the UK as there are few oligopoly company who used to run almost whole

the market of the UK.

At the same time preference of different consumer are changing on regular basis as a

result many different organization used to enter in the market by bringing variety of

different product in the market to attract the eye of the consumer.

Part 2 Business Performance Analysis

2.1 Statement of Profit or Loss

Financial statement of profit or loss statement refers to the financial performance of the

company. This represents the financial performance of the company during the year and this

helps the company to take effective measures for improving the financial position of the

company. Financial performance of the Roast ltd will be analysed using ratio analysis. it will be

used for knowing the internal functioning of the company. it used for assessing whether it was

profitable or not for the company. financial statement of the company are required to be prepared

as per the financial statements of company.

1

Industry Overview

Roast Ltd used to operate in the food and beverage industry of the UK. Roast Ltd. Is an

independent coffee house chain established in the UK in the year 2008. Specifically

Roast. Ltd used to operate in the coffee industry of UK. Coffee market is the fifth largest

coffee consumer market in Market.

As a result it is one of the strongest industries of the UK and used to provide good

contribution in the economy of the UK as a whole. Coffee market is very competitive

industry as there are many different organizations that used to operate in the industry.

As a result Roast Ltd used to face variety of the competition from the market, Star buck is

one of the biggest competitors of the company in the market. Starbuck generally used to

attract huge number of the customer in the market with the quality of product offered by

them.

Coffee industry is one of the successful industry of UK reason behind the same is

identified that there are good number of the consumer in the UK who used to drink

coffee. Looking at the scope of this industry it can be said that coffee industry is well

developed in the UK as there are few oligopoly company who used to run almost whole

the market of the UK.

At the same time preference of different consumer are changing on regular basis as a

result many different organization used to enter in the market by bringing variety of

different product in the market to attract the eye of the consumer.

Part 2 Business Performance Analysis

2.1 Statement of Profit or Loss

Financial statement of profit or loss statement refers to the financial performance of the

company. This represents the financial performance of the company during the year and this

helps the company to take effective measures for improving the financial position of the

company. Financial performance of the Roast ltd will be analysed using ratio analysis. it will be

used for knowing the internal functioning of the company. it used for assessing whether it was

profitable or not for the company. financial statement of the company are required to be prepared

as per the financial statements of company.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

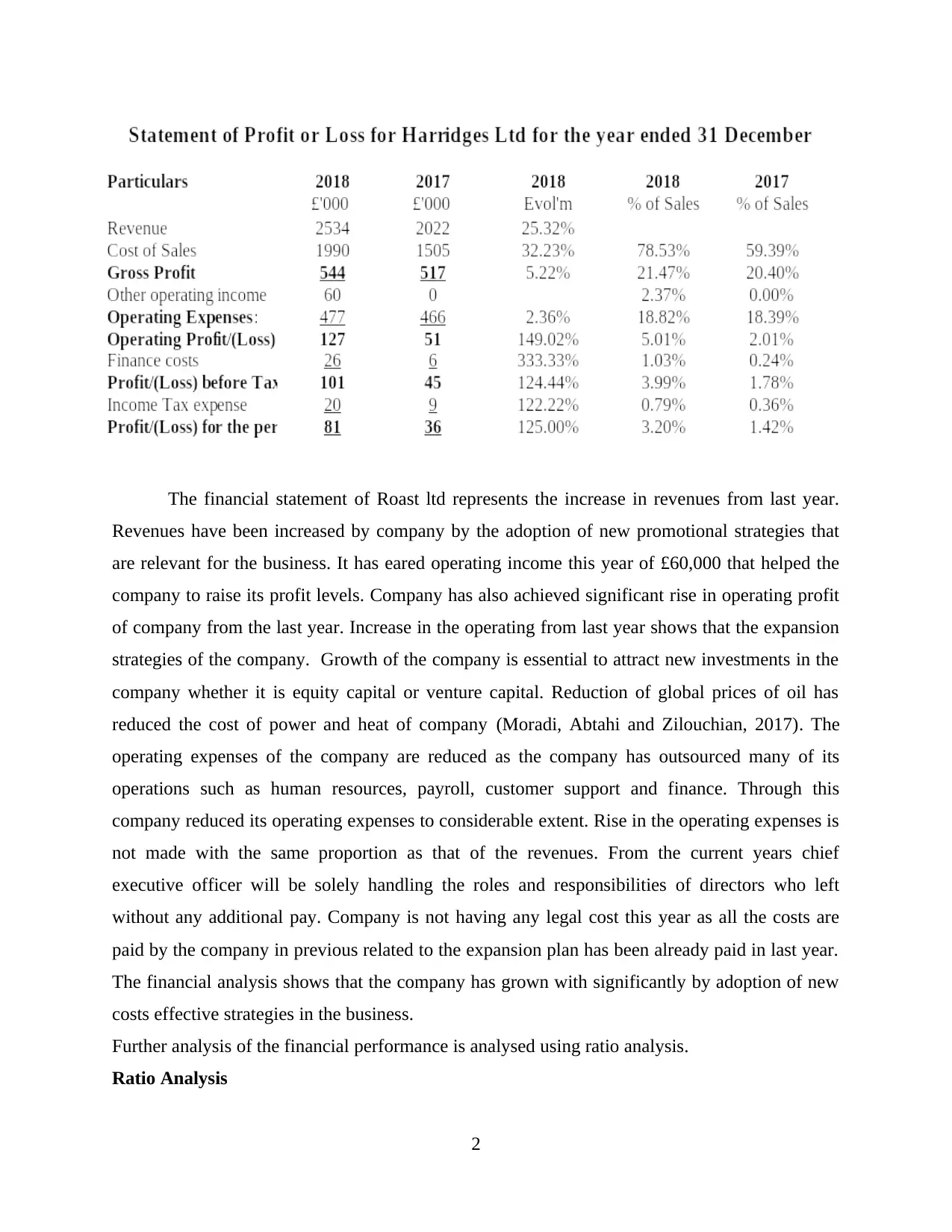

The financial statement of Roast ltd represents the increase in revenues from last year.

Revenues have been increased by company by the adoption of new promotional strategies that

are relevant for the business. It has eared operating income this year of £60,000 that helped the

company to raise its profit levels. Company has also achieved significant rise in operating profit

of company from the last year. Increase in the operating from last year shows that the expansion

strategies of the company. Growth of the company is essential to attract new investments in the

company whether it is equity capital or venture capital. Reduction of global prices of oil has

reduced the cost of power and heat of company (Moradi, Abtahi and Zilouchian, 2017). The

operating expenses of the company are reduced as the company has outsourced many of its

operations such as human resources, payroll, customer support and finance. Through this

company reduced its operating expenses to considerable extent. Rise in the operating expenses is

not made with the same proportion as that of the revenues. From the current years chief

executive officer will be solely handling the roles and responsibilities of directors who left

without any additional pay. Company is not having any legal cost this year as all the costs are

paid by the company in previous related to the expansion plan has been already paid in last year.

The financial analysis shows that the company has grown with significantly by adoption of new

costs effective strategies in the business.

Further analysis of the financial performance is analysed using ratio analysis.

Ratio Analysis

2

Revenues have been increased by company by the adoption of new promotional strategies that

are relevant for the business. It has eared operating income this year of £60,000 that helped the

company to raise its profit levels. Company has also achieved significant rise in operating profit

of company from the last year. Increase in the operating from last year shows that the expansion

strategies of the company. Growth of the company is essential to attract new investments in the

company whether it is equity capital or venture capital. Reduction of global prices of oil has

reduced the cost of power and heat of company (Moradi, Abtahi and Zilouchian, 2017). The

operating expenses of the company are reduced as the company has outsourced many of its

operations such as human resources, payroll, customer support and finance. Through this

company reduced its operating expenses to considerable extent. Rise in the operating expenses is

not made with the same proportion as that of the revenues. From the current years chief

executive officer will be solely handling the roles and responsibilities of directors who left

without any additional pay. Company is not having any legal cost this year as all the costs are

paid by the company in previous related to the expansion plan has been already paid in last year.

The financial analysis shows that the company has grown with significantly by adoption of new

costs effective strategies in the business.

Further analysis of the financial performance is analysed using ratio analysis.

Ratio Analysis

2

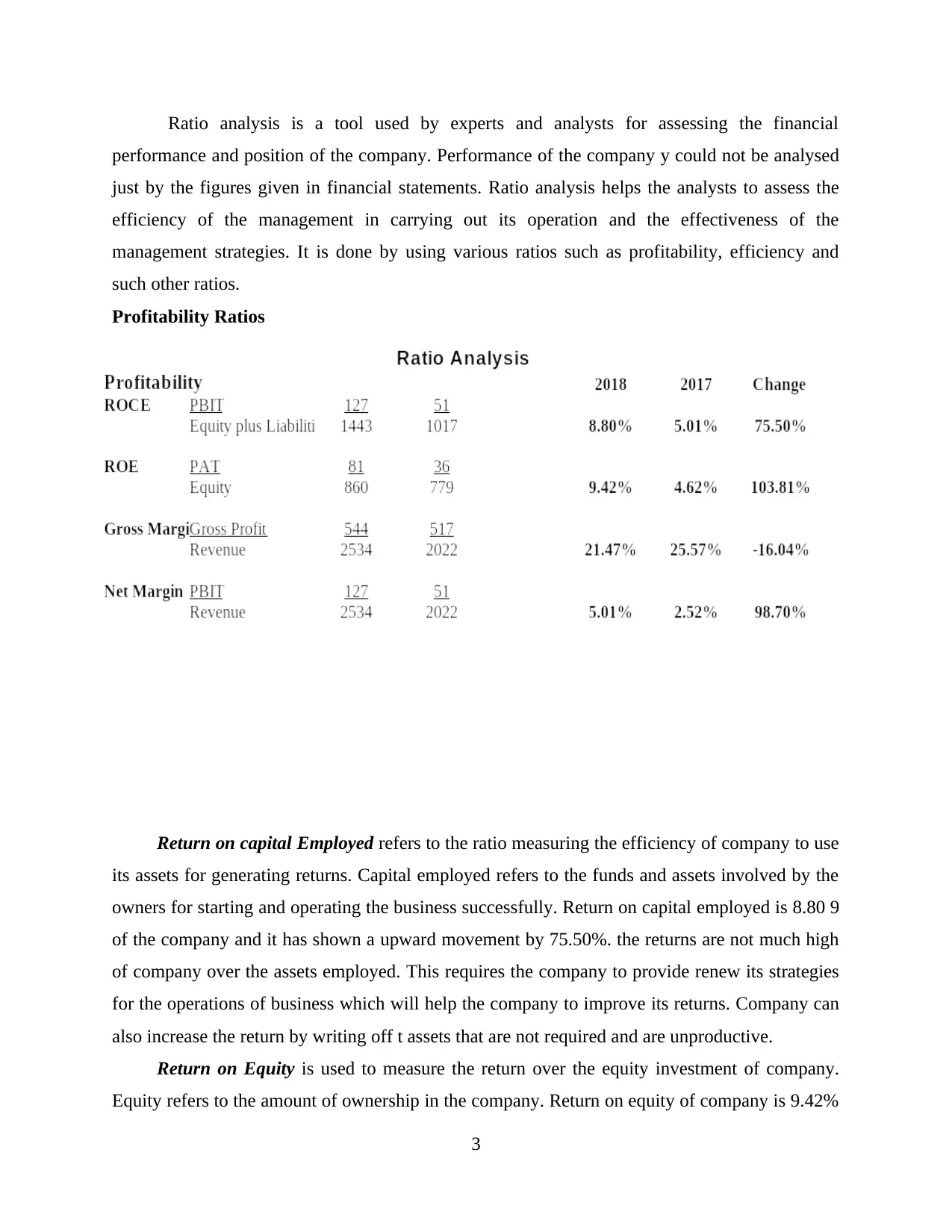

Ratio analysis is a tool used by experts and analysts for assessing the financial

performance and position of the company. Performance of the company y could not be analysed

just by the figures given in financial statements. Ratio analysis helps the analysts to assess the

efficiency of the management in carrying out its operation and the effectiveness of the

management strategies. It is done by using various ratios such as profitability, efficiency and

such other ratios.

Profitability Ratios

Return on capital Employed refers to the ratio measuring the efficiency of company to use

its assets for generating returns. Capital employed refers to the funds and assets involved by the

owners for starting and operating the business successfully. Return on capital employed is 8.80 9

of the company and it has shown a upward movement by 75.50%. the returns are not much high

of company over the assets employed. This requires the company to provide renew its strategies

for the operations of business which will help the company to improve its returns. Company can

also increase the return by writing off t assets that are not required and are unproductive.

Return on Equity is used to measure the return over the equity investment of company.

Equity refers to the amount of ownership in the company. Return on equity of company is 9.42%

3

performance and position of the company. Performance of the company y could not be analysed

just by the figures given in financial statements. Ratio analysis helps the analysts to assess the

efficiency of the management in carrying out its operation and the effectiveness of the

management strategies. It is done by using various ratios such as profitability, efficiency and

such other ratios.

Profitability Ratios

Return on capital Employed refers to the ratio measuring the efficiency of company to use

its assets for generating returns. Capital employed refers to the funds and assets involved by the

owners for starting and operating the business successfully. Return on capital employed is 8.80 9

of the company and it has shown a upward movement by 75.50%. the returns are not much high

of company over the assets employed. This requires the company to provide renew its strategies

for the operations of business which will help the company to improve its returns. Company can

also increase the return by writing off t assets that are not required and are unproductive.

Return on Equity is used to measure the return over the equity investment of company.

Equity refers to the amount of ownership in the company. Return on equity of company is 9.42%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

where it was 4.62% in last year. The returns show whether the equity investors will be earning

enough returns over their investments or not (Hausmann, Kokkinaki and Leng, 2019).. Return of

the company has increased from last but it is required to take steps for maintaining the stability

in returns. Lower returns will affect the company and its value in the market. Company is

required to increase its profits for raising the returns over equity. Lower return may cause the

investors to withdraw fund from the company.

Gross Margin of the company shows how effectively company has managed its cost of

sales for the production of goods and services. Gross profit ratio is 21.475 for the current with a

decline from 25.42% in last year. Decrease in the gross profit is seen even when the revenues of

company has raised. The company has been making imports of raw material and there has been

increase in the raw material prices and labour rates. The rise in cost of sales has the gross profit

to go down it is essential for the company to manage its operation else it may suffer decline in

the returns and profit levels.

Net Profit margin of company is the ration of the profit earned as against its revenues.

Higher profits are desire of every company but it is dependent on the size and nature of the

enterprise. The profit ratio of company is 5.02% which was 2.52% the return of the company has

doubled this year. The increase is not solely due to the raise of revenues but also due the other

operating income which will be not earned every year. Though company has tried to achieve the

profit levels by reducing the cost such as director remuneration and outsourcing of many of the

activities it is required to raise the profit levels. It is required to further take steps that will help

the company to raise the profit levels.

2.2 Statement of Financial Position

Balance sheet is also known as statement of financial position that represents the health

and wealth of the company. it represents the holdings and obligations of the enterprise during the

given financial year. Balance sheet of the company is prepared to represent the financial standing

of the company in comparison with the market. Companies are required to disclose the additional

information related to the assets and liabilities in detail in notes to account. This is used for

assessing the risks associated with the business.

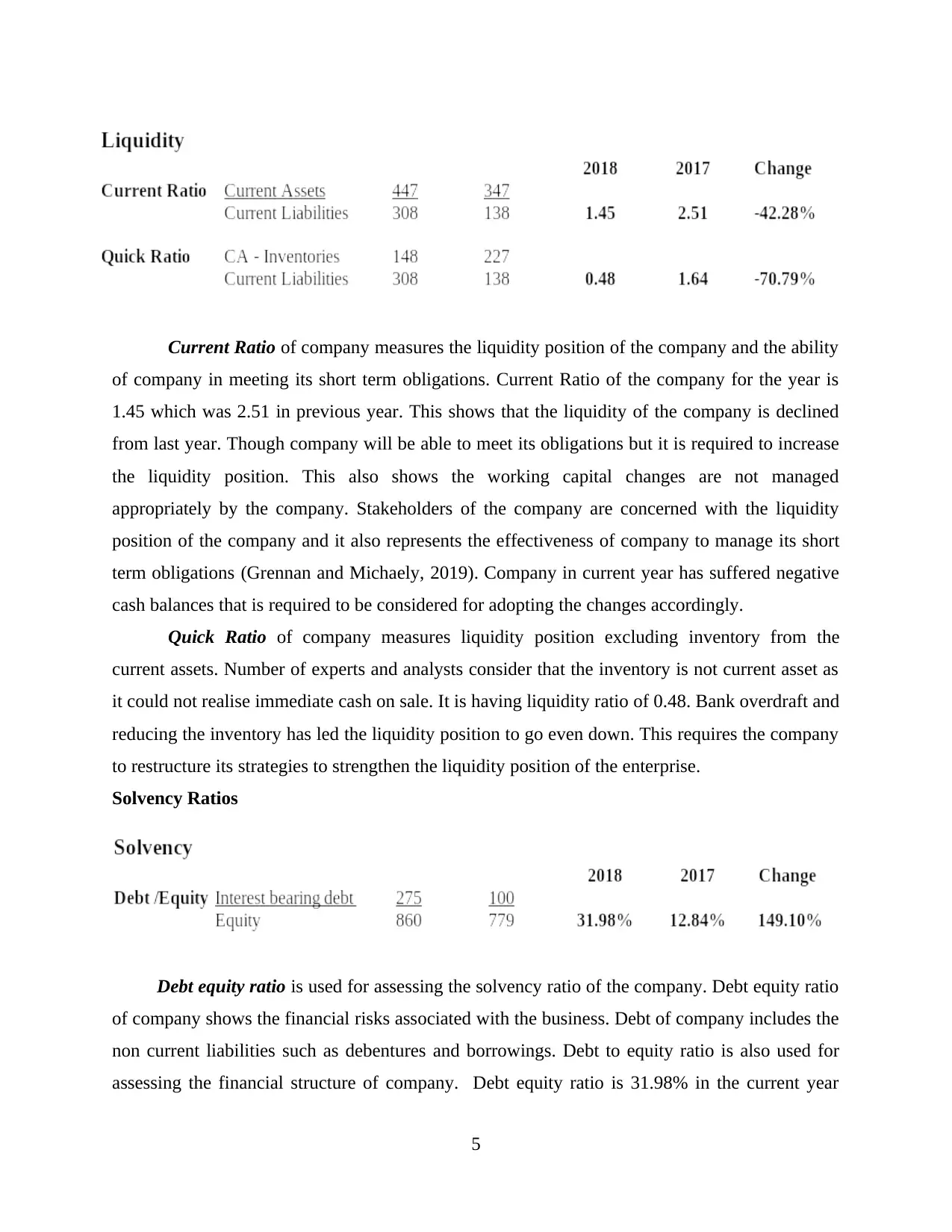

Liquidity Ratio of the company is used for assessing the liquidity position of company.

This is essential for assessing the management of liquid assets and liabilities of company and

ensuring that the company is able to meet its short tern obligation with the available assets.

4

enough returns over their investments or not (Hausmann, Kokkinaki and Leng, 2019).. Return of

the company has increased from last but it is required to take steps for maintaining the stability

in returns. Lower returns will affect the company and its value in the market. Company is

required to increase its profits for raising the returns over equity. Lower return may cause the

investors to withdraw fund from the company.

Gross Margin of the company shows how effectively company has managed its cost of

sales for the production of goods and services. Gross profit ratio is 21.475 for the current with a

decline from 25.42% in last year. Decrease in the gross profit is seen even when the revenues of

company has raised. The company has been making imports of raw material and there has been

increase in the raw material prices and labour rates. The rise in cost of sales has the gross profit

to go down it is essential for the company to manage its operation else it may suffer decline in

the returns and profit levels.

Net Profit margin of company is the ration of the profit earned as against its revenues.

Higher profits are desire of every company but it is dependent on the size and nature of the

enterprise. The profit ratio of company is 5.02% which was 2.52% the return of the company has

doubled this year. The increase is not solely due to the raise of revenues but also due the other

operating income which will be not earned every year. Though company has tried to achieve the

profit levels by reducing the cost such as director remuneration and outsourcing of many of the

activities it is required to raise the profit levels. It is required to further take steps that will help

the company to raise the profit levels.

2.2 Statement of Financial Position

Balance sheet is also known as statement of financial position that represents the health

and wealth of the company. it represents the holdings and obligations of the enterprise during the

given financial year. Balance sheet of the company is prepared to represent the financial standing

of the company in comparison with the market. Companies are required to disclose the additional

information related to the assets and liabilities in detail in notes to account. This is used for

assessing the risks associated with the business.

Liquidity Ratio of the company is used for assessing the liquidity position of company.

This is essential for assessing the management of liquid assets and liabilities of company and

ensuring that the company is able to meet its short tern obligation with the available assets.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Ratio of company measures the liquidity position of the company and the ability

of company in meeting its short term obligations. Current Ratio of the company for the year is

1.45 which was 2.51 in previous year. This shows that the liquidity of the company is declined

from last year. Though company will be able to meet its obligations but it is required to increase

the liquidity position. This also shows the working capital changes are not managed

appropriately by the company. Stakeholders of the company are concerned with the liquidity

position of the company and it also represents the effectiveness of company to manage its short

term obligations (Grennan and Michaely, 2019). Company in current year has suffered negative

cash balances that is required to be considered for adopting the changes accordingly.

Quick Ratio of company measures liquidity position excluding inventory from the

current assets. Number of experts and analysts consider that the inventory is not current asset as

it could not realise immediate cash on sale. It is having liquidity ratio of 0.48. Bank overdraft and

reducing the inventory has led the liquidity position to go even down. This requires the company

to restructure its strategies to strengthen the liquidity position of the enterprise.

Solvency Ratios

Debt equity ratio is used for assessing the solvency ratio of the company. Debt equity ratio

of company shows the financial risks associated with the business. Debt of company includes the

non current liabilities such as debentures and borrowings. Debt to equity ratio is also used for

assessing the financial structure of company. Debt equity ratio is 31.98% in the current year

5

of company in meeting its short term obligations. Current Ratio of the company for the year is

1.45 which was 2.51 in previous year. This shows that the liquidity of the company is declined

from last year. Though company will be able to meet its obligations but it is required to increase

the liquidity position. This also shows the working capital changes are not managed

appropriately by the company. Stakeholders of the company are concerned with the liquidity

position of the company and it also represents the effectiveness of company to manage its short

term obligations (Grennan and Michaely, 2019). Company in current year has suffered negative

cash balances that is required to be considered for adopting the changes accordingly.

Quick Ratio of company measures liquidity position excluding inventory from the

current assets. Number of experts and analysts consider that the inventory is not current asset as

it could not realise immediate cash on sale. It is having liquidity ratio of 0.48. Bank overdraft and

reducing the inventory has led the liquidity position to go even down. This requires the company

to restructure its strategies to strengthen the liquidity position of the enterprise.

Solvency Ratios

Debt equity ratio is used for assessing the solvency ratio of the company. Debt equity ratio

of company shows the financial risks associated with the business. Debt of company includes the

non current liabilities such as debentures and borrowings. Debt to equity ratio is also used for

assessing the financial structure of company. Debt equity ratio is 31.98% in the current year

5

where last year it was 12.84%. Debt of the company is increased due to the expansion pan of

entity to the Romania. However even after raising the new borrowings the financial risks has not

risen to a level of attention or high risks. This is due to the high equity capital of company and it

will not affect the financial position of company. The capital structure of company should be

adequate where the cost of capital of the company is least. Cost of equity is high but raising

excessive debts will raise the financial risks of the business, therefore further funds should be

raise by doing effective analysis.

2.3 Statement of Cash Flows

Statement of cash flow is one of the three financial statement prepared by the company to

represent the cash position of entity. This reflects the cash flows of the enterprise throughout the

business year. Cash flow statement of company represents the fiscal position of organisation

during the given period of time. Cash flows during the year from operating activities are negative

of the enterprise amounting -24000. From the negative operating cash flows it could be

interpreted that the company is not in state for paying its trade bills unless the additional capital

is raised by the company.

A company having negative cash flows is considered to be inefficient in managing its

operations and current assets. Investing activities represents the cash flows from the sale or

purchase of investments or assets. It had negative cash flow from investing activities of -358000.

It has made investment in the purchase of equipments of the expansion plan of the business. The

investments made by the company are part of the long term business plan for expanding the

business to new borders (de Assis and et.al., 2017). Financing activities provided cash flows of

175000 during the year. Positive cash flows from this activity show that company has raised new

capital. The funds have flown to the firm increasing the liquidity position of company. However

it is seen that company suffered a net decrease of -207000 in 2018. This could be interpreted that

the outflows of the company are higher than the cash inflows incurred during the year.

6

entity to the Romania. However even after raising the new borrowings the financial risks has not

risen to a level of attention or high risks. This is due to the high equity capital of company and it

will not affect the financial position of company. The capital structure of company should be

adequate where the cost of capital of the company is least. Cost of equity is high but raising

excessive debts will raise the financial risks of the business, therefore further funds should be

raise by doing effective analysis.

2.3 Statement of Cash Flows

Statement of cash flow is one of the three financial statement prepared by the company to

represent the cash position of entity. This reflects the cash flows of the enterprise throughout the

business year. Cash flow statement of company represents the fiscal position of organisation

during the given period of time. Cash flows during the year from operating activities are negative

of the enterprise amounting -24000. From the negative operating cash flows it could be

interpreted that the company is not in state for paying its trade bills unless the additional capital

is raised by the company.

A company having negative cash flows is considered to be inefficient in managing its

operations and current assets. Investing activities represents the cash flows from the sale or

purchase of investments or assets. It had negative cash flow from investing activities of -358000.

It has made investment in the purchase of equipments of the expansion plan of the business. The

investments made by the company are part of the long term business plan for expanding the

business to new borders (de Assis and et.al., 2017). Financing activities provided cash flows of

175000 during the year. Positive cash flows from this activity show that company has raised new

capital. The funds have flown to the firm increasing the liquidity position of company. However

it is seen that company suffered a net decrease of -207000 in 2018. This could be interpreted that

the outflows of the company are higher than the cash inflows incurred during the year.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

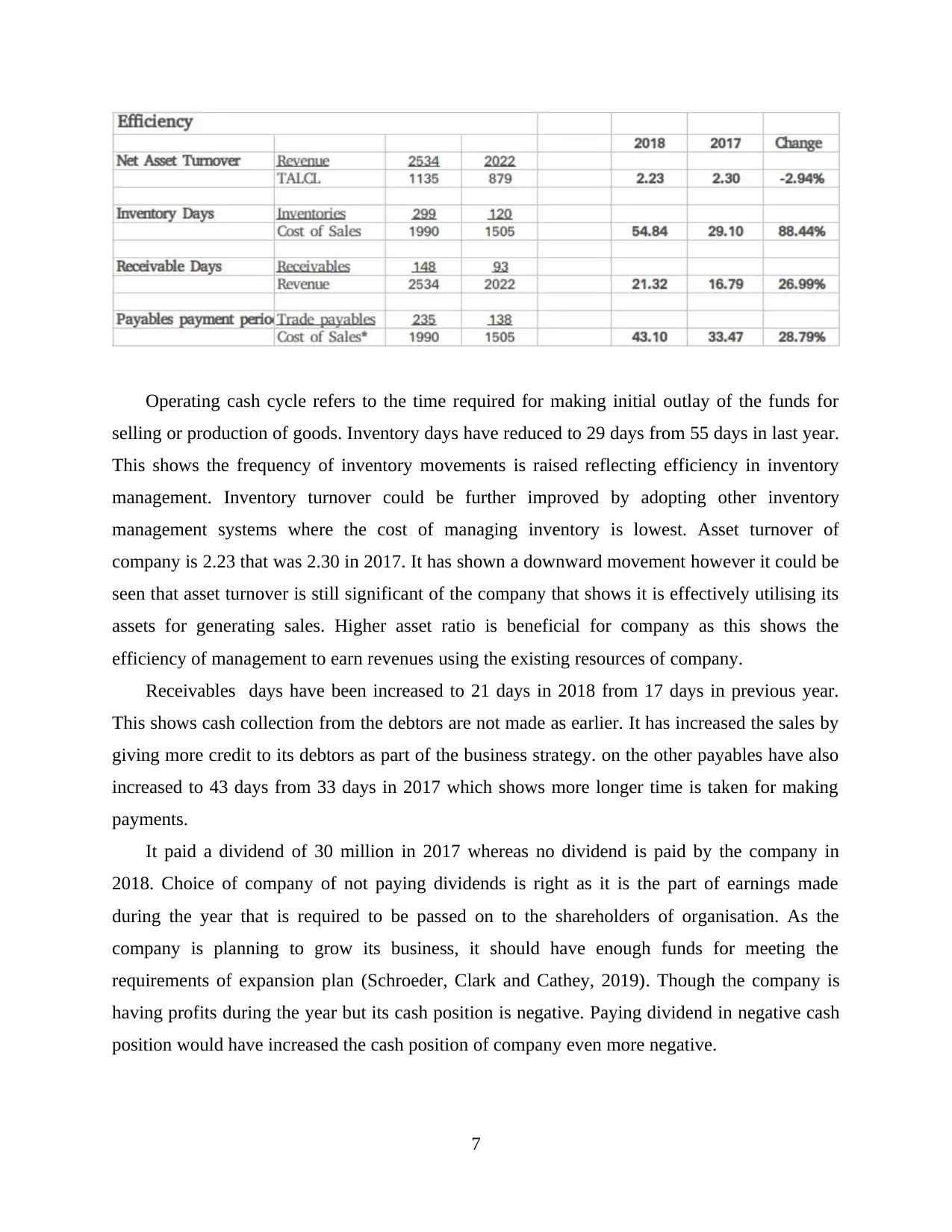

Operating cash cycle refers to the time required for making initial outlay of the funds for

selling or production of goods. Inventory days have reduced to 29 days from 55 days in last year.

This shows the frequency of inventory movements is raised reflecting efficiency in inventory

management. Inventory turnover could be further improved by adopting other inventory

management systems where the cost of managing inventory is lowest. Asset turnover of

company is 2.23 that was 2.30 in 2017. It has shown a downward movement however it could be

seen that asset turnover is still significant of the company that shows it is effectively utilising its

assets for generating sales. Higher asset ratio is beneficial for company as this shows the

efficiency of management to earn revenues using the existing resources of company.

Receivables days have been increased to 21 days in 2018 from 17 days in previous year.

This shows cash collection from the debtors are not made as earlier. It has increased the sales by

giving more credit to its debtors as part of the business strategy. on the other payables have also

increased to 43 days from 33 days in 2017 which shows more longer time is taken for making

payments.

It paid a dividend of 30 million in 2017 whereas no dividend is paid by the company in

2018. Choice of company of not paying dividends is right as it is the part of earnings made

during the year that is required to be passed on to the shareholders of organisation. As the

company is planning to grow its business, it should have enough funds for meeting the

requirements of expansion plan (Schroeder, Clark and Cathey, 2019). Though the company is

having profits during the year but its cash position is negative. Paying dividend in negative cash

position would have increased the cash position of company even more negative.

7

selling or production of goods. Inventory days have reduced to 29 days from 55 days in last year.

This shows the frequency of inventory movements is raised reflecting efficiency in inventory

management. Inventory turnover could be further improved by adopting other inventory

management systems where the cost of managing inventory is lowest. Asset turnover of

company is 2.23 that was 2.30 in 2017. It has shown a downward movement however it could be

seen that asset turnover is still significant of the company that shows it is effectively utilising its

assets for generating sales. Higher asset ratio is beneficial for company as this shows the

efficiency of management to earn revenues using the existing resources of company.

Receivables days have been increased to 21 days in 2018 from 17 days in previous year.

This shows cash collection from the debtors are not made as earlier. It has increased the sales by

giving more credit to its debtors as part of the business strategy. on the other payables have also

increased to 43 days from 33 days in 2017 which shows more longer time is taken for making

payments.

It paid a dividend of 30 million in 2017 whereas no dividend is paid by the company in

2018. Choice of company of not paying dividends is right as it is the part of earnings made

during the year that is required to be passed on to the shareholders of organisation. As the

company is planning to grow its business, it should have enough funds for meeting the

requirements of expansion plan (Schroeder, Clark and Cathey, 2019). Though the company is

having profits during the year but its cash position is negative. Paying dividend in negative cash

position would have increased the cash position of company even more negative.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 3 INVESTMENT APPRAISAL

3.1 a. Management forecast

The management forecast is referred to as the predicting or forecasting of the company in order

to manage or operate the business in proper manner (Harris, 2017). The management need to

forecast the expansion of the project of Romania project using the different capital budgeting

techniques. The capital budgeting technique s the technique which is helpful for Roast Ltd in

analysing the fact that whether the investment in Romania project will be successful or not. The

initial investment proposed by the company is around £500 million. Also, the company and the

management need to analyse the different source of fund for the investment in the other project.

This involves the use of different budgeting techniques and are used before the investment is

done and this include techniques like NPV, payback period method, IRR and many other

investment appraisal techniques. In accordance to the forecast of the management of Roast Ltd it

was found that the project is viable and it must be adopted in order to get profitability. This

project will involve the buying of different types of machines of coffee and manufacturing as per

the demand of the company and the consumers. Also, this machine will involves the Italian

process of making the coffee and this will bring in more taste and texture to the coffee for the

consumers. If Roast ltd will adopt this project of investment then this will bring in company in

developing and increasing the profitability of the company. Also, the properties and equipment if

the expansion needs to be purchased and this will increase the cost of the company. But this will

also result in the increase in the growth of company by at least 20 % is this Romania project will

be adopted.

3.1 b. Investment appraisal technique

These are the techniques which will help the company in order to analyse the different options

which will help the company in analysing the different types of investment will be present for the

company. There are different techniques of investment appraisal technique which are as follows-

Payback period- this is a method of capital budgeting which is used by Roast Ltd in order to

indentify the viability of the project that is whether the project is viable or not (Hausmann,

Kokkinaki and Leng, 2019). This is calculated due to the reason that this helps the company in

knowing the time which will take the company in recovering the initial cost of the investment

which company is doing in the other business. The present project will recover the cost of

investment in not more than 4 years.

8

3.1 a. Management forecast

The management forecast is referred to as the predicting or forecasting of the company in order

to manage or operate the business in proper manner (Harris, 2017). The management need to

forecast the expansion of the project of Romania project using the different capital budgeting

techniques. The capital budgeting technique s the technique which is helpful for Roast Ltd in

analysing the fact that whether the investment in Romania project will be successful or not. The

initial investment proposed by the company is around £500 million. Also, the company and the

management need to analyse the different source of fund for the investment in the other project.

This involves the use of different budgeting techniques and are used before the investment is

done and this include techniques like NPV, payback period method, IRR and many other

investment appraisal techniques. In accordance to the forecast of the management of Roast Ltd it

was found that the project is viable and it must be adopted in order to get profitability. This

project will involve the buying of different types of machines of coffee and manufacturing as per

the demand of the company and the consumers. Also, this machine will involves the Italian

process of making the coffee and this will bring in more taste and texture to the coffee for the

consumers. If Roast ltd will adopt this project of investment then this will bring in company in

developing and increasing the profitability of the company. Also, the properties and equipment if

the expansion needs to be purchased and this will increase the cost of the company. But this will

also result in the increase in the growth of company by at least 20 % is this Romania project will

be adopted.

3.1 b. Investment appraisal technique

These are the techniques which will help the company in order to analyse the different options

which will help the company in analysing the different types of investment will be present for the

company. There are different techniques of investment appraisal technique which are as follows-

Payback period- this is a method of capital budgeting which is used by Roast Ltd in order to

indentify the viability of the project that is whether the project is viable or not (Hausmann,

Kokkinaki and Leng, 2019). This is calculated due to the reason that this helps the company in

knowing the time which will take the company in recovering the initial cost of the investment

which company is doing in the other business. The present project will recover the cost of

investment in not more than 4 years.

8

Advantage

The major advantage of this is that this is easy and simple method and it is more beneficial in

case of uncertainty activity.

Disadvantage

The major disadvantage of this method is that this ignores the time value of the money and this

also does not cover the cash flow and it will do not take into account the profitability.

Accounting rate of return- this is another financial ration which is used in order to calculate the

capital budgeting. This method is used for calculation of the return which is generated from the

capital investment which is done by the company. The current ARR for the present project is

approximately 18 % and this is enough and adequate for the current project which is accepted by

the company (Kogadeeva and Zamboni, 2016).

Advantage

The major advantage of this method is that this is easy to calculate and this is better for

understanding the total profit for the whole period of economic life cycle.

Disadvantage

The major drawback of this method is that time factor is not considered and this does not involve

external factors which affect the profitability of the company to a great extent.

Net present value- this is another method of capital budgeting which is being used by the

companies in investment appraisal. This method uses the discounting factor which help the

company in knowing the fact that whether the future cash flow from the project form covering

the cost of the project. The negative cash flow depicts that project is not profitable for the

company and if it is positive then this is profitable for the company (Knežević and Mitrović,

2018).

Advantage

The major advantage of this method represents the initial investment of cash and it takes into

consideration the time value of money and other risk.

Disadvantage

This is the major drawback of this method as there is no set guideline for the determination of the

required rate of return and this is not used to compare the project which has different sizes.

9

The major advantage of this is that this is easy and simple method and it is more beneficial in

case of uncertainty activity.

Disadvantage

The major disadvantage of this method is that this ignores the time value of the money and this

also does not cover the cash flow and it will do not take into account the profitability.

Accounting rate of return- this is another financial ration which is used in order to calculate the

capital budgeting. This method is used for calculation of the return which is generated from the

capital investment which is done by the company. The current ARR for the present project is

approximately 18 % and this is enough and adequate for the current project which is accepted by

the company (Kogadeeva and Zamboni, 2016).

Advantage

The major advantage of this method is that this is easy to calculate and this is better for

understanding the total profit for the whole period of economic life cycle.

Disadvantage

The major drawback of this method is that time factor is not considered and this does not involve

external factors which affect the profitability of the company to a great extent.

Net present value- this is another method of capital budgeting which is being used by the

companies in investment appraisal. This method uses the discounting factor which help the

company in knowing the fact that whether the future cash flow from the project form covering

the cost of the project. The negative cash flow depicts that project is not profitable for the

company and if it is positive then this is profitable for the company (Knežević and Mitrović,

2018).

Advantage

The major advantage of this method represents the initial investment of cash and it takes into

consideration the time value of money and other risk.

Disadvantage

This is the major drawback of this method as there is no set guideline for the determination of the

required rate of return and this is not used to compare the project which has different sizes.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.