Financial Management: Analysis, Budgeting & Sainsbury Plc Proposal

VerifiedAdded on 2023/06/08

|21

|4786

|478

Report

AI Summary

This report provides a comprehensive financial analysis of Sainsbury Plc, a leading UK retailer, focusing on data acquisition, validity assessment, and the application of analytical tools like ratio analysis to financial documents from 2017 and 2018. It evaluates Sainsbury's financial performance, strengths, and weaknesses in terms of profitability, liquidity, and efficiency, offering recommendations for improvement. The report also examines the budgeting process, considering financial barriers, legal needs, and accounting conventions, and analyzes budget outcomes against organizational objectives. Furthermore, it identifies criteria for judging investment proposals, assesses their viability, and evaluates their impact on Sainsbury's strategic objectives. The analysis uses both internal and external data sources, highlighting the importance of internal and external audits for data validation. This detailed financial management report provides valuable insights into Sainsbury Plc's financial strategies and performance.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Task 1:.............................................................................................................................................3

AC 1.1 Ways of obtaining financial data and assessment of its validity:....................................3

AC 1.4 Review and question of financial data:...........................................................................4

Task 2:.............................................................................................................................................4

AC 1.2 Application of different types of analytical tools and techniques to a range of financial

documents:...................................................................................................................................4

AC 1.3 Comparative analyses of financial data:.........................................................................6

Task 3:.............................................................................................................................................8

AC 2.1 Financial barriers and target accomplishments, legal needs and accounting conventions

at the time of budget formulation:...............................................................................................8

Task 4:...........................................................................................................................................10

AC 2.2 Analysis of the budget outcomes against organisational objectives and identification of

alternatives:................................................................................................................................10

Task 5:...........................................................................................................................................12

AC 3.1 Identification of criteria for judging proposals:............................................................12

AC 3.2 Viability of the proposal for expenditure:.....................................................................13

AC 3.3 Identification of the strengths and weaknesses and feedback on the financial proposal:

...................................................................................................................................................15

AC 3.4 Impact of the proposal on the strategic objectives of the organisation:........................16

Table of Contents

Task 1:.............................................................................................................................................3

AC 1.1 Ways of obtaining financial data and assessment of its validity:....................................3

AC 1.4 Review and question of financial data:...........................................................................4

Task 2:.............................................................................................................................................4

AC 1.2 Application of different types of analytical tools and techniques to a range of financial

documents:...................................................................................................................................4

AC 1.3 Comparative analyses of financial data:.........................................................................6

Task 3:.............................................................................................................................................8

AC 2.1 Financial barriers and target accomplishments, legal needs and accounting conventions

at the time of budget formulation:...............................................................................................8

Task 4:...........................................................................................................................................10

AC 2.2 Analysis of the budget outcomes against organisational objectives and identification of

alternatives:................................................................................................................................10

Task 5:...........................................................................................................................................12

AC 3.1 Identification of criteria for judging proposals:............................................................12

AC 3.2 Viability of the proposal for expenditure:.....................................................................13

AC 3.3 Identification of the strengths and weaknesses and feedback on the financial proposal:

...................................................................................................................................................15

AC 3.4 Impact of the proposal on the strategic objectives of the organisation:........................16

2FINANCIAL MANAGEMENT

References:....................................................................................................................................18

References:....................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Task 1:

AC 1.1 Ways of obtaining financial data and assessment of its validity:

For this section, Sainsbury Plc is chosen as the organisation, which is one of the leading

retailers holding 16.9% of the market share in the retail industry of UK (About.sainsburys.co.uk

2018). Financial data provide raw materials for driving conclusion of the financial position of the

business. Primarily, an organisation could obtain financial data from internal resources as well as

external resources (Bekaert and Hodrick 2017). The internal resources denote the records

generated by the business, while the external resources imply the sources available from the third

parties.

The internal financial data could be obtained from the accounting system of the

organisation, control function reports like sales department reports, other departmental

managerial reports and reports prepared by the suppliers, customers and staffs. These reports

provide details of the financial aspects of the departmental operations and thus, the accounts and

finance division of Sainsbury could be provided with information regarding revenue details and

necessary expenditure generated over a year (Cornwall, Vang and Hartman 2016). By combining

these reports, the financial department could accumulate and interpret data for developing

information to infer about its financial position. The other sources from which Sainsbury Plc

could obtain financial data include company house, company website, financial information

database and research reports, which are external data sources.

Validity implies the reasonableness and accuracy of financial data producing suitable

quality information for ascertaining financial condition of a specific organisation. Thus, it is

necessary for Sainsbury to evaluate the data collected based on regular sampling for validity to

Task 1:

AC 1.1 Ways of obtaining financial data and assessment of its validity:

For this section, Sainsbury Plc is chosen as the organisation, which is one of the leading

retailers holding 16.9% of the market share in the retail industry of UK (About.sainsburys.co.uk

2018). Financial data provide raw materials for driving conclusion of the financial position of the

business. Primarily, an organisation could obtain financial data from internal resources as well as

external resources (Bekaert and Hodrick 2017). The internal resources denote the records

generated by the business, while the external resources imply the sources available from the third

parties.

The internal financial data could be obtained from the accounting system of the

organisation, control function reports like sales department reports, other departmental

managerial reports and reports prepared by the suppliers, customers and staffs. These reports

provide details of the financial aspects of the departmental operations and thus, the accounts and

finance division of Sainsbury could be provided with information regarding revenue details and

necessary expenditure generated over a year (Cornwall, Vang and Hartman 2016). By combining

these reports, the financial department could accumulate and interpret data for developing

information to infer about its financial position. The other sources from which Sainsbury Plc

could obtain financial data include company house, company website, financial information

database and research reports, which are external data sources.

Validity implies the reasonableness and accuracy of financial data producing suitable

quality information for ascertaining financial condition of a specific organisation. Thus, it is

necessary for Sainsbury to evaluate the data collected based on regular sampling for validity to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

be conducted by internal as well as external auditors. The validity of financial data could be

evaluated by reviewing and questioning financial data, which is presented in the below section.

AC 1.4 Review and question of financial data:

The internal auditors are the employees of the organisation and they assess business

operations and accounting for bringing disciplined and systematic approach to analyse and

enhance risk management effectiveness along with processes of governance and control.

However, due to lack of independence, they are sometimes limited to report any error or fraud to

the top management due to perceived threats of their employment (Dyckman, Magee and Pfeiffer

2014). These auditors are not normal staffs and they are hired by the organisation, who are

responsible to report to the top management.

The external auditors give reasonable assurance that the financial reports do not contain

material misstatements, errors or frauds for providing unqualified audit opinion. In this context it

is noteworthy to mention that the external auditors are not and need not be expected to provide

complete assurance about validity and reliability of the financial statements. However, they audit

only published accounts by ensuring that certain rules are followed and they do not assure that

the company information is published in a comparable format.

Task 2:

AC 1.2 Application of different types of analytical tools and techniques to a range of

financial documents:

Ratio analysis is considered as the most powerful tool of analysing the financial

statements, as it ascertains the levels of financial performance along with formulating

be conducted by internal as well as external auditors. The validity of financial data could be

evaluated by reviewing and questioning financial data, which is presented in the below section.

AC 1.4 Review and question of financial data:

The internal auditors are the employees of the organisation and they assess business

operations and accounting for bringing disciplined and systematic approach to analyse and

enhance risk management effectiveness along with processes of governance and control.

However, due to lack of independence, they are sometimes limited to report any error or fraud to

the top management due to perceived threats of their employment (Dyckman, Magee and Pfeiffer

2014). These auditors are not normal staffs and they are hired by the organisation, who are

responsible to report to the top management.

The external auditors give reasonable assurance that the financial reports do not contain

material misstatements, errors or frauds for providing unqualified audit opinion. In this context it

is noteworthy to mention that the external auditors are not and need not be expected to provide

complete assurance about validity and reliability of the financial statements. However, they audit

only published accounts by ensuring that certain rules are followed and they do not assure that

the company information is published in a comparable format.

Task 2:

AC 1.2 Application of different types of analytical tools and techniques to a range of

financial documents:

Ratio analysis is considered as the most powerful tool of analysing the financial

statements, as it ascertains the levels of financial performance along with formulating

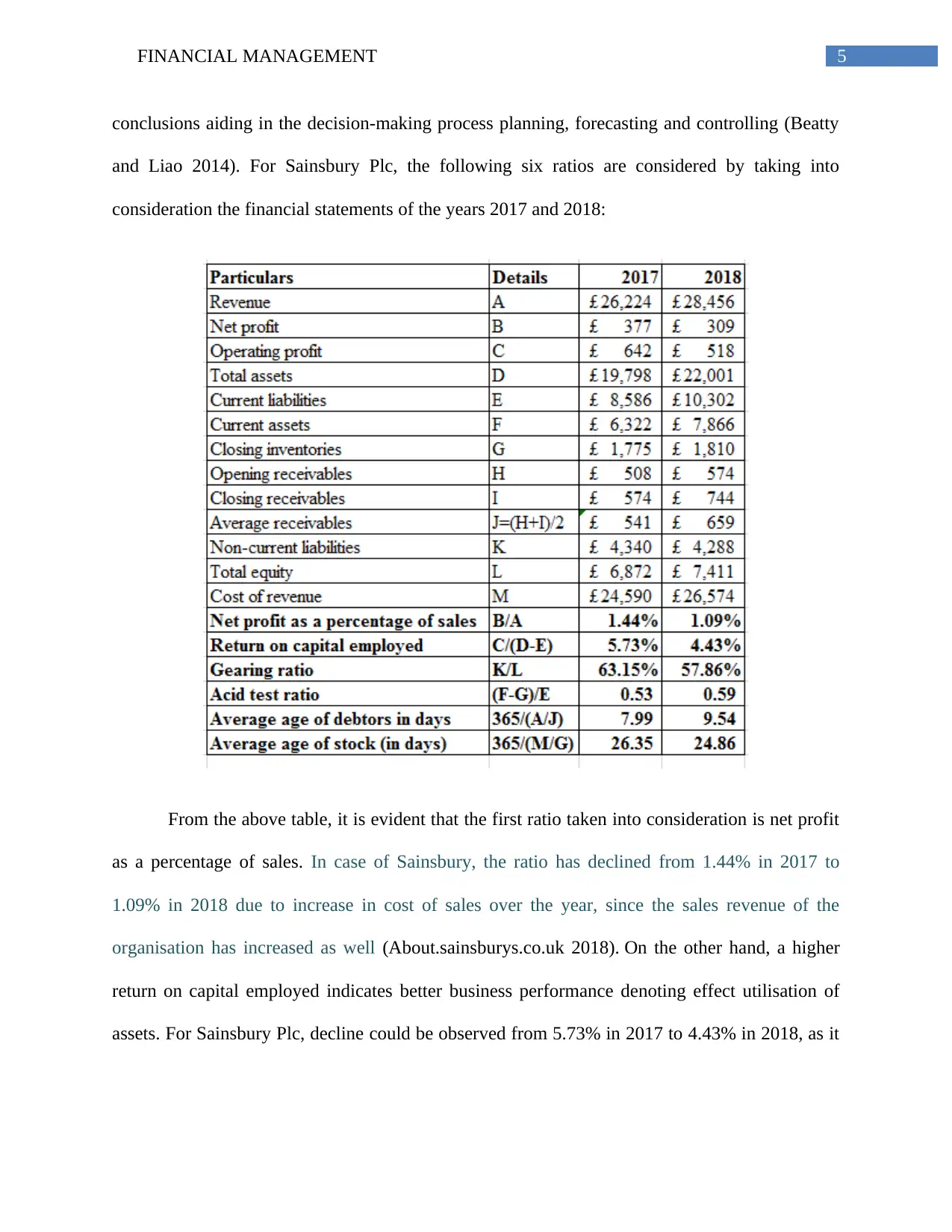

5FINANCIAL MANAGEMENT

conclusions aiding in the decision-making process planning, forecasting and controlling (Beatty

and Liao 2014). For Sainsbury Plc, the following six ratios are considered by taking into

consideration the financial statements of the years 2017 and 2018:

From the above table, it is evident that the first ratio taken into consideration is net profit

as a percentage of sales. In case of Sainsbury, the ratio has declined from 1.44% in 2017 to

1.09% in 2018 due to increase in cost of sales over the year, since the sales revenue of the

organisation has increased as well (About.sainsburys.co.uk 2018). On the other hand, a higher

return on capital employed indicates better business performance denoting effect utilisation of

assets. For Sainsbury Plc, decline could be observed from 5.73% in 2017 to 4.43% in 2018, as it

conclusions aiding in the decision-making process planning, forecasting and controlling (Beatty

and Liao 2014). For Sainsbury Plc, the following six ratios are considered by taking into

consideration the financial statements of the years 2017 and 2018:

From the above table, it is evident that the first ratio taken into consideration is net profit

as a percentage of sales. In case of Sainsbury, the ratio has declined from 1.44% in 2017 to

1.09% in 2018 due to increase in cost of sales over the year, since the sales revenue of the

organisation has increased as well (About.sainsburys.co.uk 2018). On the other hand, a higher

return on capital employed indicates better business performance denoting effect utilisation of

assets. For Sainsbury Plc, decline could be observed from 5.73% in 2017 to 4.43% in 2018, as it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

fails to generate adequate profit from its long-term funding. Thus, in terms of profitability,

Sainsbury Plc is not placed in a favourable position in the UK retail market (Elliott 2017).

For Sainsbury Plc, gearing ratio is observed to decline from 63.15% in 2017 to 57.86% in

2018, as it has focused on raising additional funds through equity by minimising its long-term

liabilities. Thus, the organisation has managed to minimise its exposure to financial risk over the

years (Finkler et al. 2016).

Acid test ratio helps in evaluating the liquidity position of an organisation by not

including few current assets like inventories and prepaid expenses, as they could not be

converted into cash within shorter timeframe. Even though Sainsbury Plc has managed to

increase its acid test ratio from 0.53 in 2017 to 0.59 in 2018, it is below the industrial standard of

1. This is because it has been collecting amounts from the debtors lately due to which the cash

balance has not increased over the years.

In terms of average age of debtors in days, it could be observed that Sainsbury Plc has

increased its debtor terms from 7.99 days in 2017 to 9.54 days in 2018, as it is facing difficulties

in collecting from its customers. However, a decline in average age of stock in days is observed

from 26.35 days in 2017 to 24.86 days in 2018, as it has aligned its inventory base in accordance

with the market demand. Thus, in terms of efficiency, Sainsbury Plc is placed in a slightly

favourable position in the UK retail market.

AC 1.3 Comparative analyses of financial data:

Based on the above evaluation, the major strengths of Sainsbury Plc could be listed down as

follows:

fails to generate adequate profit from its long-term funding. Thus, in terms of profitability,

Sainsbury Plc is not placed in a favourable position in the UK retail market (Elliott 2017).

For Sainsbury Plc, gearing ratio is observed to decline from 63.15% in 2017 to 57.86% in

2018, as it has focused on raising additional funds through equity by minimising its long-term

liabilities. Thus, the organisation has managed to minimise its exposure to financial risk over the

years (Finkler et al. 2016).

Acid test ratio helps in evaluating the liquidity position of an organisation by not

including few current assets like inventories and prepaid expenses, as they could not be

converted into cash within shorter timeframe. Even though Sainsbury Plc has managed to

increase its acid test ratio from 0.53 in 2017 to 0.59 in 2018, it is below the industrial standard of

1. This is because it has been collecting amounts from the debtors lately due to which the cash

balance has not increased over the years.

In terms of average age of debtors in days, it could be observed that Sainsbury Plc has

increased its debtor terms from 7.99 days in 2017 to 9.54 days in 2018, as it is facing difficulties

in collecting from its customers. However, a decline in average age of stock in days is observed

from 26.35 days in 2017 to 24.86 days in 2018, as it has aligned its inventory base in accordance

with the market demand. Thus, in terms of efficiency, Sainsbury Plc is placed in a slightly

favourable position in the UK retail market.

AC 1.3 Comparative analyses of financial data:

Based on the above evaluation, the major strengths of Sainsbury Plc could be listed down as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

A slight improvement in liquidity could be observed due to minimised time of inventory

turnover in days.

The capital structure of the organisation is effectively balanced, as it has concentrated on

raising funds through equity, instead of relying too much on debt funding.

However, there are certain weaknesses evident from the above analysis for Sainsbury Plc,

which could be listed down as follows:

The organisation is struggling in terms of profitability due to its minimised earnings from

the banking subsidiary and as a result, it has failed to generate adequate returns from

investments made.

The organisation is following a lenient policy in collecting amounts from the debtors due

to which the working capital availability has fallen over the years.

In order to overcome these challenges, the following recommendations would be extremely

beneficial for Sainsbury Plc to improve its financial performance:

It needs to appoint a specialised market research firm in order to assess the changes in the

tastes and preferences of the customers towards the retail products. Accordingly, new

product lines could be added and they need to be marketed effectively, which would help

in increasing the overall revenues.

It needs to formulate stringent policy for its debtors in collecting amounts from them

within a shorter timeframe by providing discounts for timely payments, which would

help in increasing the availability of working capital.

However, it is to be borne in mind that the ratios are subject to certain limitations, which are

demonstrated briefly as follows:

A slight improvement in liquidity could be observed due to minimised time of inventory

turnover in days.

The capital structure of the organisation is effectively balanced, as it has concentrated on

raising funds through equity, instead of relying too much on debt funding.

However, there are certain weaknesses evident from the above analysis for Sainsbury Plc,

which could be listed down as follows:

The organisation is struggling in terms of profitability due to its minimised earnings from

the banking subsidiary and as a result, it has failed to generate adequate returns from

investments made.

The organisation is following a lenient policy in collecting amounts from the debtors due

to which the working capital availability has fallen over the years.

In order to overcome these challenges, the following recommendations would be extremely

beneficial for Sainsbury Plc to improve its financial performance:

It needs to appoint a specialised market research firm in order to assess the changes in the

tastes and preferences of the customers towards the retail products. Accordingly, new

product lines could be added and they need to be marketed effectively, which would help

in increasing the overall revenues.

It needs to formulate stringent policy for its debtors in collecting amounts from them

within a shorter timeframe by providing discounts for timely payments, which would

help in increasing the availability of working capital.

However, it is to be borne in mind that the ratios are subject to certain limitations, which are

demonstrated briefly as follows:

8FINANCIAL MANAGEMENT

Ratios are derived from past results and the same results are not expected to remain the

same in future.

Due to the difference in accounting policies concerning inventory valuation and

depreciation, the accounting data as well as ratios of the two organisations could not be

compared.

No particular standards are laid down for ideal ratios. For instance, current ratio is

considered to be ideal, if current assets are greater than current liabilities. However, this

standard might not be justified for those concerns having considerable agreements with

bankers to provide funds, as needed. Under such situation, it might be perfectly ideal if

current assets are slightly more or identical to current liabilities (Hoskin, Fizzell and

Cherry 2014).

Task 3:

AC 2.1 Financial barriers and target accomplishments, legal needs and accounting

conventions at the time of budget formulation:

Budget helps in providing comprehensive financial insight of planned company

operation. The budgets are prepared with the intent so that the incomes could be planned and the

expenses could be controlled by the organisation. The objectives of Sainsbury Plc drive its

budget preparation so that it could be compared with the actual outcomes (Barr and McClellan

2018). Many business variables could be budgeted including output, sales, variable and fixed

cost, cash flow, profits and capital investment. Budget needs to be SMART, which is specific,

measurable, achievable, realistic and time bound; whereas, in opposition, budget would not be

effective.

Ratios are derived from past results and the same results are not expected to remain the

same in future.

Due to the difference in accounting policies concerning inventory valuation and

depreciation, the accounting data as well as ratios of the two organisations could not be

compared.

No particular standards are laid down for ideal ratios. For instance, current ratio is

considered to be ideal, if current assets are greater than current liabilities. However, this

standard might not be justified for those concerns having considerable agreements with

bankers to provide funds, as needed. Under such situation, it might be perfectly ideal if

current assets are slightly more or identical to current liabilities (Hoskin, Fizzell and

Cherry 2014).

Task 3:

AC 2.1 Financial barriers and target accomplishments, legal needs and accounting

conventions at the time of budget formulation:

Budget helps in providing comprehensive financial insight of planned company

operation. The budgets are prepared with the intent so that the incomes could be planned and the

expenses could be controlled by the organisation. The objectives of Sainsbury Plc drive its

budget preparation so that it could be compared with the actual outcomes (Barr and McClellan

2018). Many business variables could be budgeted including output, sales, variable and fixed

cost, cash flow, profits and capital investment. Budget needs to be SMART, which is specific,

measurable, achievable, realistic and time bound; whereas, in opposition, budget would not be

effective.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

The strategic goal of Sainsbury Plc is the initial factor, which requires to be taken into

account at the time of preparing budgets, since failure would be obvious, if the budgets are not

aligned with the strategic objectives. After this step, it is necessary to identify the limiting factor

that the firm is encountered, which is identified as impediment. This might be restriction on the

selling volume of the business or direct labour hours of a specific kind of workforce. At the time

organisation detects the limiting factor, budgetary principle is set. The next step is coordination

and evaluation of internal factors, which are employee resources and capabilities along with draft

department budget (Irimia-Dieguez, Medina-Lopez and Alfalla-Luque 2015). Once when the

step is over, the organisation needs to evaluate the external factors like estimated political,

economic and international environment, which enables in reducing the risk related to budget.

Finally, Sainsbury should coordinate the overall department budget that include production

budget, sales budget, labour budget, material and overhead budget or master budget (Nilsson and

Stockenstrand 2015).

The master budget is an overview of the plans of an organisation for setting particular

targets for financing and distribution activities along with sales production. This is culminated

generally in budgeted profit and loss statement, cash budget and a budgeted balance sheet. The

initiation of master budget is made with sales estimations, which could be conducted by critical

evaluation of the previous selling trend, sales force estimations, actions of the competitors,

general economic conditions, variation in the prices of the organisation, market research along

with promotion plans for sales and advertising (Henderson et al. 2015). Sales estimations results

in sales budget, which is a detailed overview of the estimated sales for the budget period. This

could be represented in the form of currency and units. Thus, one of the significant pillars of

master budget is sales budget.

The strategic goal of Sainsbury Plc is the initial factor, which requires to be taken into

account at the time of preparing budgets, since failure would be obvious, if the budgets are not

aligned with the strategic objectives. After this step, it is necessary to identify the limiting factor

that the firm is encountered, which is identified as impediment. This might be restriction on the

selling volume of the business or direct labour hours of a specific kind of workforce. At the time

organisation detects the limiting factor, budgetary principle is set. The next step is coordination

and evaluation of internal factors, which are employee resources and capabilities along with draft

department budget (Irimia-Dieguez, Medina-Lopez and Alfalla-Luque 2015). Once when the

step is over, the organisation needs to evaluate the external factors like estimated political,

economic and international environment, which enables in reducing the risk related to budget.

Finally, Sainsbury should coordinate the overall department budget that include production

budget, sales budget, labour budget, material and overhead budget or master budget (Nilsson and

Stockenstrand 2015).

The master budget is an overview of the plans of an organisation for setting particular

targets for financing and distribution activities along with sales production. This is culminated

generally in budgeted profit and loss statement, cash budget and a budgeted balance sheet. The

initiation of master budget is made with sales estimations, which could be conducted by critical

evaluation of the previous selling trend, sales force estimations, actions of the competitors,

general economic conditions, variation in the prices of the organisation, market research along

with promotion plans for sales and advertising (Henderson et al. 2015). Sales estimations results

in sales budget, which is a detailed overview of the estimated sales for the budget period. This

could be represented in the form of currency and units. Thus, one of the significant pillars of

master budget is sales budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

After sales budget, production budget is necessary for Sainsbury, since it determines the

production volume based on the expected sales volume along with beginning and ending

inventories (Lafond, McAleer and Wentzel 2016). Another budgeting component is material

budget, which represents the cost and volume of buying materials for planned inventories and

production. Labour budget reflects the budget for both skilled and unskilled labour based on the

production level. Finally, Sainsbury Plc could prepare overhead budget for showing quantities of

a bigger number of cost items. These items include electricity, rent, salary and administrative

expenses (Karadag 2015). When all these budgets are prepared for Sainsbury, it could formulate

projected profit and loss statement, cash budget, cash inflows and outflows and budgeted balance

sheet.

Task 4:

AC 2.2 Analysis of the budget outcomes against organisational objectives and identification

of alternatives:

The actual performance and the budgeted performance often resemble each other and the

significant budgeting goal is to reduce the gap between actual performance and budgeted

performance. Because of faulty assumptions in budget numbers, mistakes in arithmetic of the

actual results, incorrect budget assumptions and actual results, timing variations and price

variance might take place. With the help of budget, it is possible to gauge the performance for

conducting the comparison between actual performance and budgeted performance (Martin

2016). Variances are utilised for gauging the gap between actual performance and budgeted

performance. This analysis helps the managers in identifying issues requiring additional

After sales budget, production budget is necessary for Sainsbury, since it determines the

production volume based on the expected sales volume along with beginning and ending

inventories (Lafond, McAleer and Wentzel 2016). Another budgeting component is material

budget, which represents the cost and volume of buying materials for planned inventories and

production. Labour budget reflects the budget for both skilled and unskilled labour based on the

production level. Finally, Sainsbury Plc could prepare overhead budget for showing quantities of

a bigger number of cost items. These items include electricity, rent, salary and administrative

expenses (Karadag 2015). When all these budgets are prepared for Sainsbury, it could formulate

projected profit and loss statement, cash budget, cash inflows and outflows and budgeted balance

sheet.

Task 4:

AC 2.2 Analysis of the budget outcomes against organisational objectives and identification

of alternatives:

The actual performance and the budgeted performance often resemble each other and the

significant budgeting goal is to reduce the gap between actual performance and budgeted

performance. Because of faulty assumptions in budget numbers, mistakes in arithmetic of the

actual results, incorrect budget assumptions and actual results, timing variations and price

variance might take place. With the help of budget, it is possible to gauge the performance for

conducting the comparison between actual performance and budgeted performance (Martin

2016). Variances are utilised for gauging the gap between actual performance and budgeted

performance. This analysis helps the managers in identifying issues requiring additional

11FINANCIAL MANAGEMENT

examinations for adopting corrective actions. Variances could be labour variance, material

variance and overhead variance.

In case of the provided budget, increase in sales receipts could be observed over the

months and the organisation has earned loan proceeds due to which the cash receipts are the

highest in the month of January. Positive variance could be observed in wages, as it has declined

over the half-year period. However, fixed costs have increased over the months, as more units

are produced in the later months of the year, due to which there is overall increase in the cost of

goods sold. Another reason that the net cash flow of the organisation has been negative from

February is due to the lease of new building, the payment of which has continued until June.

Advertising fees have been charged from the month of February, which remained same until

April with a slight increase in May; however, no such fees are charged in June. The organisation

has budgeted half-yearly tax payment scheduled to be paid in the month of June. On the other

hand, the most significant reason that the net cash flow of the organisation has been negative in

most of the months is due to the estimated capital expenditure in the month of March. Finally,

loan repayments are projected to begin from April to June due to which the overall payments

have increased. In this case, the closing cash balance is observed to be negative in the months of

May and June. The organisation has a bank overdraft of £750,000, which could help in offsetting

the negative cash flow.

This particular situation could be addressed with the help of variance analysis. In this

respect, labour rate and efficiency variances along with material price and volume variances are

benchmarks of efficiency and economy (Matthew 2017). With the help of selling price and

volume variances, it would become possible for the organisation to signify the effect on

performance due to the change in demand and price levels. The management could detect the

examinations for adopting corrective actions. Variances could be labour variance, material

variance and overhead variance.

In case of the provided budget, increase in sales receipts could be observed over the

months and the organisation has earned loan proceeds due to which the cash receipts are the

highest in the month of January. Positive variance could be observed in wages, as it has declined

over the half-year period. However, fixed costs have increased over the months, as more units

are produced in the later months of the year, due to which there is overall increase in the cost of

goods sold. Another reason that the net cash flow of the organisation has been negative from

February is due to the lease of new building, the payment of which has continued until June.

Advertising fees have been charged from the month of February, which remained same until

April with a slight increase in May; however, no such fees are charged in June. The organisation

has budgeted half-yearly tax payment scheduled to be paid in the month of June. On the other

hand, the most significant reason that the net cash flow of the organisation has been negative in

most of the months is due to the estimated capital expenditure in the month of March. Finally,

loan repayments are projected to begin from April to June due to which the overall payments

have increased. In this case, the closing cash balance is observed to be negative in the months of

May and June. The organisation has a bank overdraft of £750,000, which could help in offsetting

the negative cash flow.

This particular situation could be addressed with the help of variance analysis. In this

respect, labour rate and efficiency variances along with material price and volume variances are

benchmarks of efficiency and economy (Matthew 2017). With the help of selling price and

volume variances, it would become possible for the organisation to signify the effect on

performance due to the change in demand and price levels. The management could detect the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.