Detailed Financial Analysis and Performance of Sainsbury's PLC (GM707)

VerifiedAdded on 2023/04/23

|22

|7929

|135

Report

AI Summary

This report presents a comprehensive financial analysis of Sainsbury's PLC, evaluating its performance through various financial ratios including Operating Profit Margin, Price to Equity Ratio, Gearing Ratio, Asset Turnover Ratio, Return on Capital Employed (ROCE), and Interest Cover Ratio for the years 2016 and 2017. The analysis delves into the implications of these ratios, discussing trends and potential underlying factors impacting Sainsbury's financial health. Furthermore, the report explores potential financing options to support future investments in areas like R&D, innovation, and technological upgrades. The report also examines the relevance of the budgeting process in the modern environment, discusses various performance management tools for large global companies, and evaluates capital investment appraisal techniques. The analysis includes a discussion of financial reporting standards (IFRS, GAAP) and their impact on assessing an organization's value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Brief/Task

The detailed requirements for this task are as follows:

There are four equally weighted parts to this assignment

Part 1

You are to select a PLC that has a listing on any recognized stock exchange of your choice and agree this with

the module tutor.

You are required to produce a Financial Analysis of the company based upon the following ratios for the

company for the years 2017 and 2016

1. Operating Profit Margin Ratio

2. Price to Equity [P/e] Ratio

3. Gearing Ratio

4. Asset Turnover Ratio

5. Return on Capital Employed (ROCE).

6. Interest Cover Ratio

(you will need to show all relevant workings and supporting documentation). Your analysis will be based

upon the ratios calculated and utilizing any background industry/company information you think is relevant.

Now examine the typical sources of finance options available to justify a 20% Net Asset investment in

meeting future management priorities of the chosen PLC w.r.t addressing its competitive and leadership

edge of staying invested in either :- R&D or Innovation or Debt Issuance {repayments}/ Restructuring / Re-

engineering or Technological upgrades or Divestitures or M&A/ JV’s or any other suitable Asset Purchase

constituting Capex requirements by integrating the management discussion & analysis from the Ratios

evaluated

# R&D – Research & Development, M&A – Mergers & Acquisitions, JV’s – Joint Venture, Capex- Capital

Expenditure.

Part 2

You are to discuss the question whether the budgeting process is still fit for purpose in the modern

environment from a planning and control dimension? How can scalable technologies such as cloud

computing, big data and predictive analysis software prove ‘reliable’ in strengthening the planning,

budgeting and forecasting exercise to be fully automated in the next five years.

Part 3

Discuss the different types of performance management tools and techniques which can be deployed in

large global companies for evaluating its suitability across a range of business and economic environments.

Part 4

Imagine you are a CEO of a large global corporation and one of your Group Directors has approached with a

business plan requiring significant capital expenditure. What types of capital investment appraisal

techniques would you deploy to arrive at, while examining the fiscal viability of business proposal?

Assessment Criteria

The proportions of the assignment should be

The detailed requirements for this task are as follows:

There are four equally weighted parts to this assignment

Part 1

You are to select a PLC that has a listing on any recognized stock exchange of your choice and agree this with

the module tutor.

You are required to produce a Financial Analysis of the company based upon the following ratios for the

company for the years 2017 and 2016

1. Operating Profit Margin Ratio

2. Price to Equity [P/e] Ratio

3. Gearing Ratio

4. Asset Turnover Ratio

5. Return on Capital Employed (ROCE).

6. Interest Cover Ratio

(you will need to show all relevant workings and supporting documentation). Your analysis will be based

upon the ratios calculated and utilizing any background industry/company information you think is relevant.

Now examine the typical sources of finance options available to justify a 20% Net Asset investment in

meeting future management priorities of the chosen PLC w.r.t addressing its competitive and leadership

edge of staying invested in either :- R&D or Innovation or Debt Issuance {repayments}/ Restructuring / Re-

engineering or Technological upgrades or Divestitures or M&A/ JV’s or any other suitable Asset Purchase

constituting Capex requirements by integrating the management discussion & analysis from the Ratios

evaluated

# R&D – Research & Development, M&A – Mergers & Acquisitions, JV’s – Joint Venture, Capex- Capital

Expenditure.

Part 2

You are to discuss the question whether the budgeting process is still fit for purpose in the modern

environment from a planning and control dimension? How can scalable technologies such as cloud

computing, big data and predictive analysis software prove ‘reliable’ in strengthening the planning,

budgeting and forecasting exercise to be fully automated in the next five years.

Part 3

Discuss the different types of performance management tools and techniques which can be deployed in

large global companies for evaluating its suitability across a range of business and economic environments.

Part 4

Imagine you are a CEO of a large global corporation and one of your Group Directors has approached with a

business plan requiring significant capital expenditure. What types of capital investment appraisal

techniques would you deploy to arrive at, while examining the fiscal viability of business proposal?

Assessment Criteria

The proportions of the assignment should be

1. How does understanding the concepts of financial reporting help in appreciating the of

accounting standards (IFRS , GAAP), when judging true value of organizations (25%).

2. Comparison of company performance with industry based upon ratios calculated (25%)

3. Analytical discussion of the relevance of the budgeting process to the current commercial and

industrial/technology environment (25%)

4. Evaluate the various performance management tools and investment appraisal techniques of its

suitability and relevance in the evolving business and economic environment.(25%)

Assessment limits: No more than: 6500 words, excluding appendices

Assessment (For further details see the Module Guide)

Assessment 1: Coursework (weightage 50%, not Exceeding 3000 Words)

Assessment 2: Coursework (weightage 50%, not Exceeding 3000Words)

Special Assessment Requirements

Both elements of assessment must be passed in order to pass the module

ASSIGNMENT INFORMATION

Full/ Part Assignment Full

Date Assignment Issued

Date Assignment Due

accounting standards (IFRS , GAAP), when judging true value of organizations (25%).

2. Comparison of company performance with industry based upon ratios calculated (25%)

3. Analytical discussion of the relevance of the budgeting process to the current commercial and

industrial/technology environment (25%)

4. Evaluate the various performance management tools and investment appraisal techniques of its

suitability and relevance in the evolving business and economic environment.(25%)

Assessment limits: No more than: 6500 words, excluding appendices

Assessment (For further details see the Module Guide)

Assessment 1: Coursework (weightage 50%, not Exceeding 3000 Words)

Assessment 2: Coursework (weightage 50%, not Exceeding 3000Words)

Special Assessment Requirements

Both elements of assessment must be passed in order to pass the module

ASSIGNMENT INFORMATION

Full/ Part Assignment Full

Date Assignment Issued

Date Assignment Due

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assignment IV by Col. Anil Ahluwalia

TO BE FILLED BY THE FACULTY

Faculty Name Mr Shahid A Wani

Contact No.

Email ID shahid@ebsedu.org

TO BE FILLED BY THE SUTDENT

Student Name

Student ID

Email ID

Turinitin ID 17975395

Turnitin Enrollment key GM707

Course

Date Submitted

TO BE FILLED BY THE ASSESSOR

Assessment types Marks Marks

Awarded

Understanding the concepts of financial reporting help 25

Comparison of company performance 25

Analytical discussion 25

Evaluate various performance management tools and investment

appraisal techniques

25

Overall Marks 100

Overall Grade

Faculty Name

Summative Feedback by Faculty for further improvement

Table of Contents

Introduction..........................................................................................................................

TO BE FILLED BY THE FACULTY

Faculty Name Mr Shahid A Wani

Contact No.

Email ID shahid@ebsedu.org

TO BE FILLED BY THE SUTDENT

Student Name

Student ID

Email ID

Turinitin ID 17975395

Turnitin Enrollment key GM707

Course

Date Submitted

TO BE FILLED BY THE ASSESSOR

Assessment types Marks Marks

Awarded

Understanding the concepts of financial reporting help 25

Comparison of company performance 25

Analytical discussion 25

Evaluate various performance management tools and investment

appraisal techniques

25

Overall Marks 100

Overall Grade

Faculty Name

Summative Feedback by Faculty for further improvement

Table of Contents

Introduction..........................................................................................................................

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment 1.......................................................................................................................

Answer to Part 1..............................................................................................................

Answer to Part 2..............................................................................................................

Answer to Part 3............................................................................................................

Answer to Part 4............................................................................................................

Assessment 2.....................................................................................................................

Answer to Part 1............................................................................................................

Answer to Part 2............................................................................................................

Answer to Part 3............................................................................................................

Answer to Part 4............................................................................................................

Conclusion.........................................................................................................................

References..........................................................................................................................

Answer to Part 1..............................................................................................................

Answer to Part 2..............................................................................................................

Answer to Part 3............................................................................................................

Answer to Part 4............................................................................................................

Assessment 2.....................................................................................................................

Answer to Part 1............................................................................................................

Answer to Part 2............................................................................................................

Answer to Part 3............................................................................................................

Answer to Part 4............................................................................................................

Conclusion.........................................................................................................................

References..........................................................................................................................

Part1

The scope of the study has provided the assessment of ratios for Sainsbury’s PLC during

2017 and 2016. Some of the main ratios considered for the report includes “Operating Profit

Margin Ratio, Price to Equity [P/e] Ratio, Gearing Ratio, Asset Turnover Ratio, Return on

Capital Employed (ROCE) and Interest Coverage Ratio”. This section of the report has also

discussed on the typical sources of finance options available to justify a 20% net asset

investment for meeting future management priorities. The next part of the study has focused

on the necessity of including budgeting process as per planning and control dimension. The

third segment of the study has highlighted on the inclusion of performance management tools

which are depicted to be deployed in large global companies and discern the suitability of the

range of business and economic environments. The next section of the study has focused on

the understanding the concepts listed under the financial reporting beneficial in appreciating

the various types of the accounting standards listed as per IFRS and GAAP. This will be done

for judging the true value of the selected organization. The second part of assessment 2 has

provided the comparison of the company performance as per the industry-based standards as

per the ratios computed for the company. The significant nature of the analytical decision has

been able to provide the relevance of the budgeting process as per the present commercial and

industrial technology environment. The final section of this section has been conducive in

addressing the various techniques used as per the performance management with application

of the relevant management tools relevant with the suitability of the evolving business and

economic environment (Renz 2016).

Assessment 1

Answer to Part 1

Ratio Analysis of Sainsbury for 2017 and 2016

1. Operating Profit Margin Ratio

The operating profit margin is computed by dividing the total operating income with total

sales. As per the depictions of the profitability ratios it can be seen that the operating profit

margin has reduced from 3.01% in 2016 to 2.45% in 2017. This shows that Sainsbury’s PLC

was not able to maintain a sufficient short-term profit pertaining to increased reliance on short

term debt financing. It needs to be also ascertained that the operating income of the company

was reduced from $ 707m in 2016 to $ 642m in 2017 (Barr and McClellan 2018).

Particulars` 2017 2016

$m $m

Operating Income A 642.0 707.0

Revenue B 26224.0 23506.0

The scope of the study has provided the assessment of ratios for Sainsbury’s PLC during

2017 and 2016. Some of the main ratios considered for the report includes “Operating Profit

Margin Ratio, Price to Equity [P/e] Ratio, Gearing Ratio, Asset Turnover Ratio, Return on

Capital Employed (ROCE) and Interest Coverage Ratio”. This section of the report has also

discussed on the typical sources of finance options available to justify a 20% net asset

investment for meeting future management priorities. The next part of the study has focused

on the necessity of including budgeting process as per planning and control dimension. The

third segment of the study has highlighted on the inclusion of performance management tools

which are depicted to be deployed in large global companies and discern the suitability of the

range of business and economic environments. The next section of the study has focused on

the understanding the concepts listed under the financial reporting beneficial in appreciating

the various types of the accounting standards listed as per IFRS and GAAP. This will be done

for judging the true value of the selected organization. The second part of assessment 2 has

provided the comparison of the company performance as per the industry-based standards as

per the ratios computed for the company. The significant nature of the analytical decision has

been able to provide the relevance of the budgeting process as per the present commercial and

industrial technology environment. The final section of this section has been conducive in

addressing the various techniques used as per the performance management with application

of the relevant management tools relevant with the suitability of the evolving business and

economic environment (Renz 2016).

Assessment 1

Answer to Part 1

Ratio Analysis of Sainsbury for 2017 and 2016

1. Operating Profit Margin Ratio

The operating profit margin is computed by dividing the total operating income with total

sales. As per the depictions of the profitability ratios it can be seen that the operating profit

margin has reduced from 3.01% in 2016 to 2.45% in 2017. This shows that Sainsbury’s PLC

was not able to maintain a sufficient short-term profit pertaining to increased reliance on short

term debt financing. It needs to be also ascertained that the operating income of the company

was reduced from $ 707m in 2016 to $ 642m in 2017 (Barr and McClellan 2018).

Particulars` 2017 2016

$m $m

Operating Income A 642.0 707.0

Revenue B 26224.0 23506.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

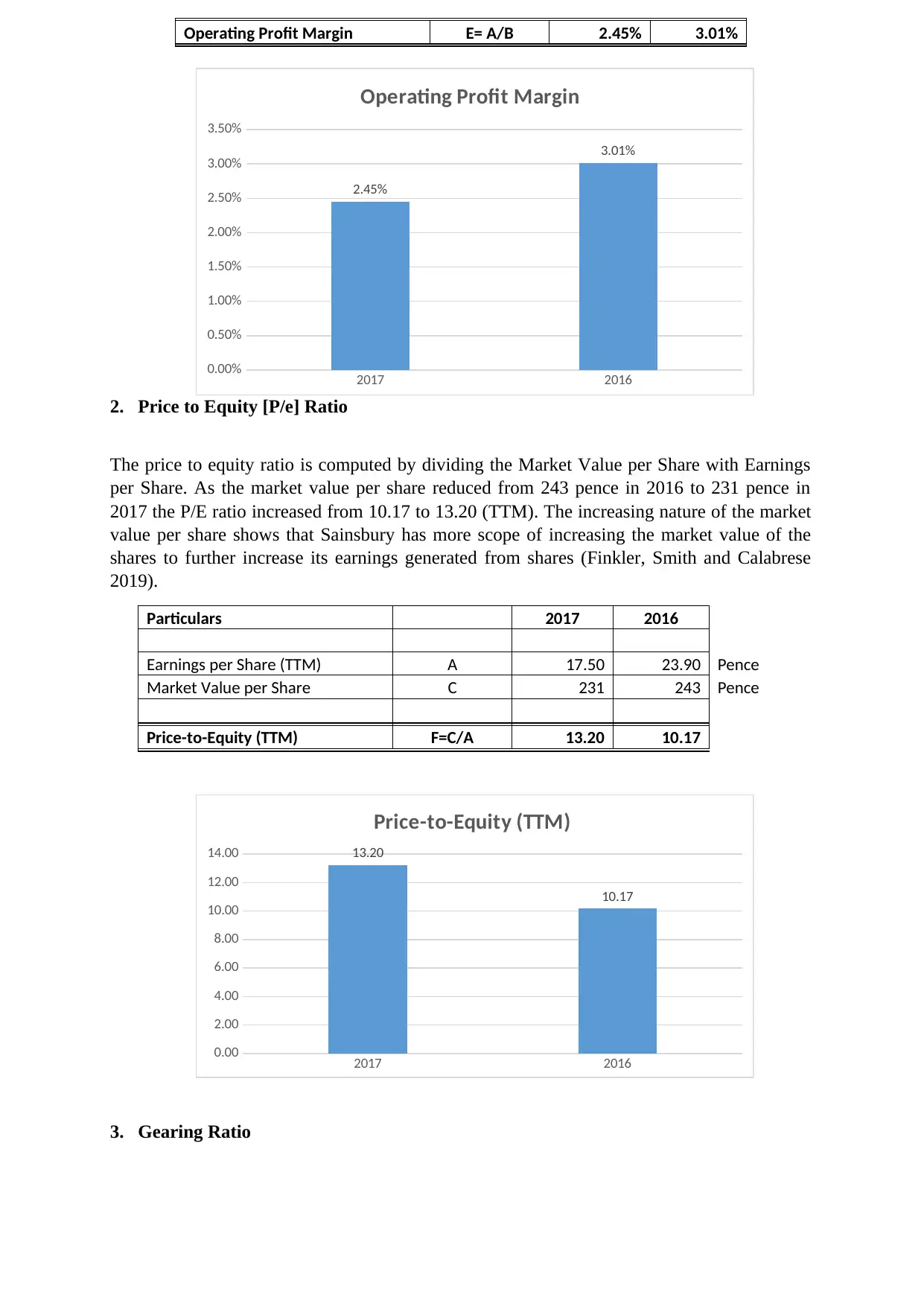

Operating Profit Margin E= A/B 2.45% 3.01%

2017 2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

2.45%

3.01%

Operating Profit Margin

2. Price to Equity [P/e] Ratio

The price to equity ratio is computed by dividing the Market Value per Share with Earnings

per Share. As the market value per share reduced from 243 pence in 2016 to 231 pence in

2017 the P/E ratio increased from 10.17 to 13.20 (TTM). The increasing nature of the market

value per share shows that Sainsbury has more scope of increasing the market value of the

shares to further increase its earnings generated from shares (Finkler, Smith and Calabrese

2019).

Particulars 2017 2016

Earnings per Share (TTM) A 17.50 23.90 Pence

Market Value per Share C 231 243 Pence

Price-to-Equity (TTM) F=C/A 13.20 10.17

2017 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00 13.20

10.17

Price-to-Equity (TTM)

3. Gearing Ratio

2017 2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

2.45%

3.01%

Operating Profit Margin

2. Price to Equity [P/e] Ratio

The price to equity ratio is computed by dividing the Market Value per Share with Earnings

per Share. As the market value per share reduced from 243 pence in 2016 to 231 pence in

2017 the P/E ratio increased from 10.17 to 13.20 (TTM). The increasing nature of the market

value per share shows that Sainsbury has more scope of increasing the market value of the

shares to further increase its earnings generated from shares (Finkler, Smith and Calabrese

2019).

Particulars 2017 2016

Earnings per Share (TTM) A 17.50 23.90 Pence

Market Value per Share C 231 243 Pence

Price-to-Equity (TTM) F=C/A 13.20 10.17

2017 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00 13.20

10.17

Price-to-Equity (TTM)

3. Gearing Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

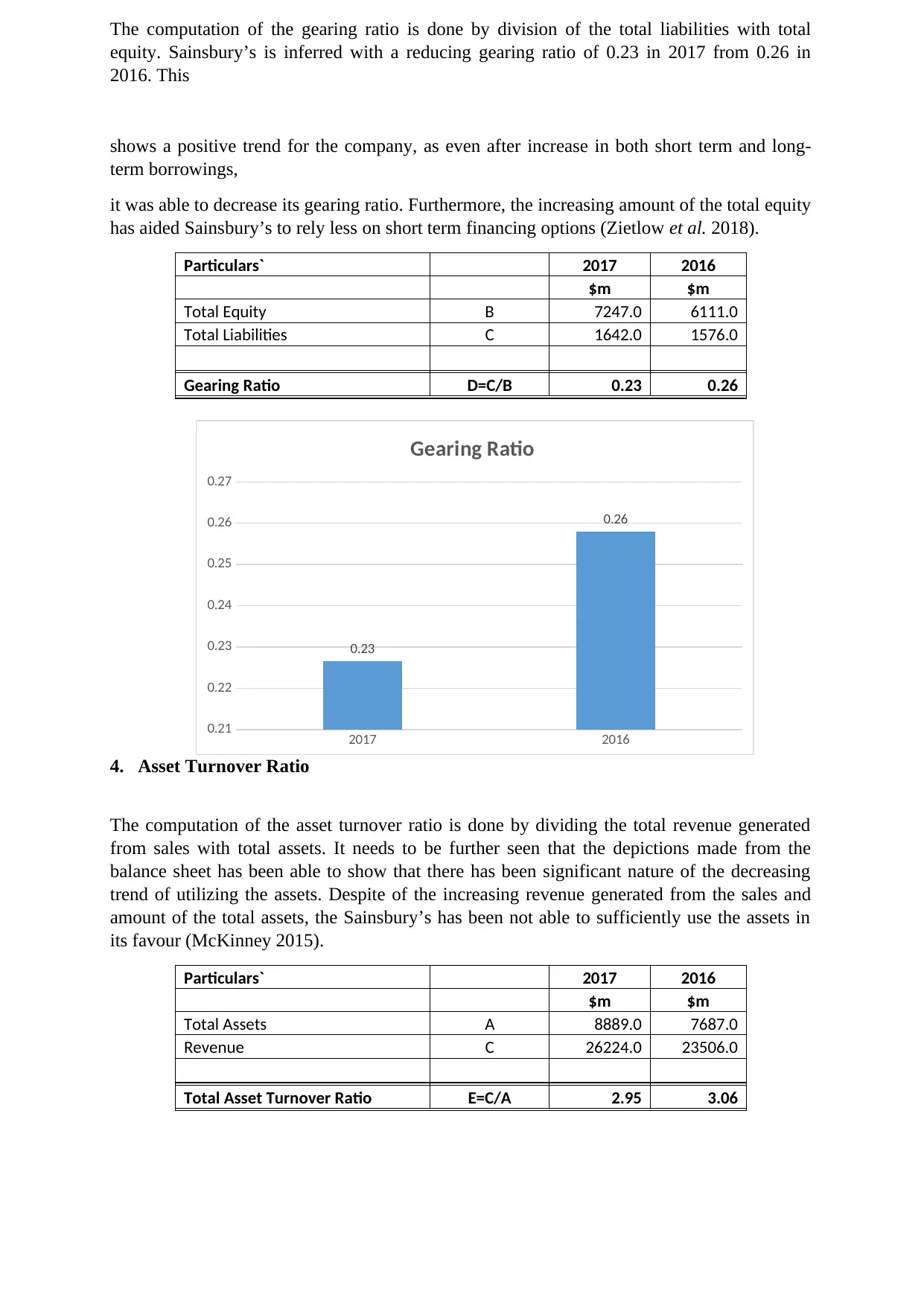

The computation of the gearing ratio is done by division of the total liabilities with total

equity. Sainsbury’s is inferred with a reducing gearing ratio of 0.23 in 2017 from 0.26 in

2016. This

shows a positive trend for the company, as even after increase in both short term and long-

term borrowings,

it was able to decrease its gearing ratio. Furthermore, the increasing amount of the total equity

has aided Sainsbury’s to rely less on short term financing options (Zietlow et al. 2018).

Particulars` 2017 2016

$m $m

Total Equity B 7247.0 6111.0

Total Liabilities C 1642.0 1576.0

Gearing Ratio D=C/B 0.23 0.26

2017 2016

0.21

0.22

0.23

0.24

0.25

0.26

0.27

0.23

0.26

Gearing Ratio

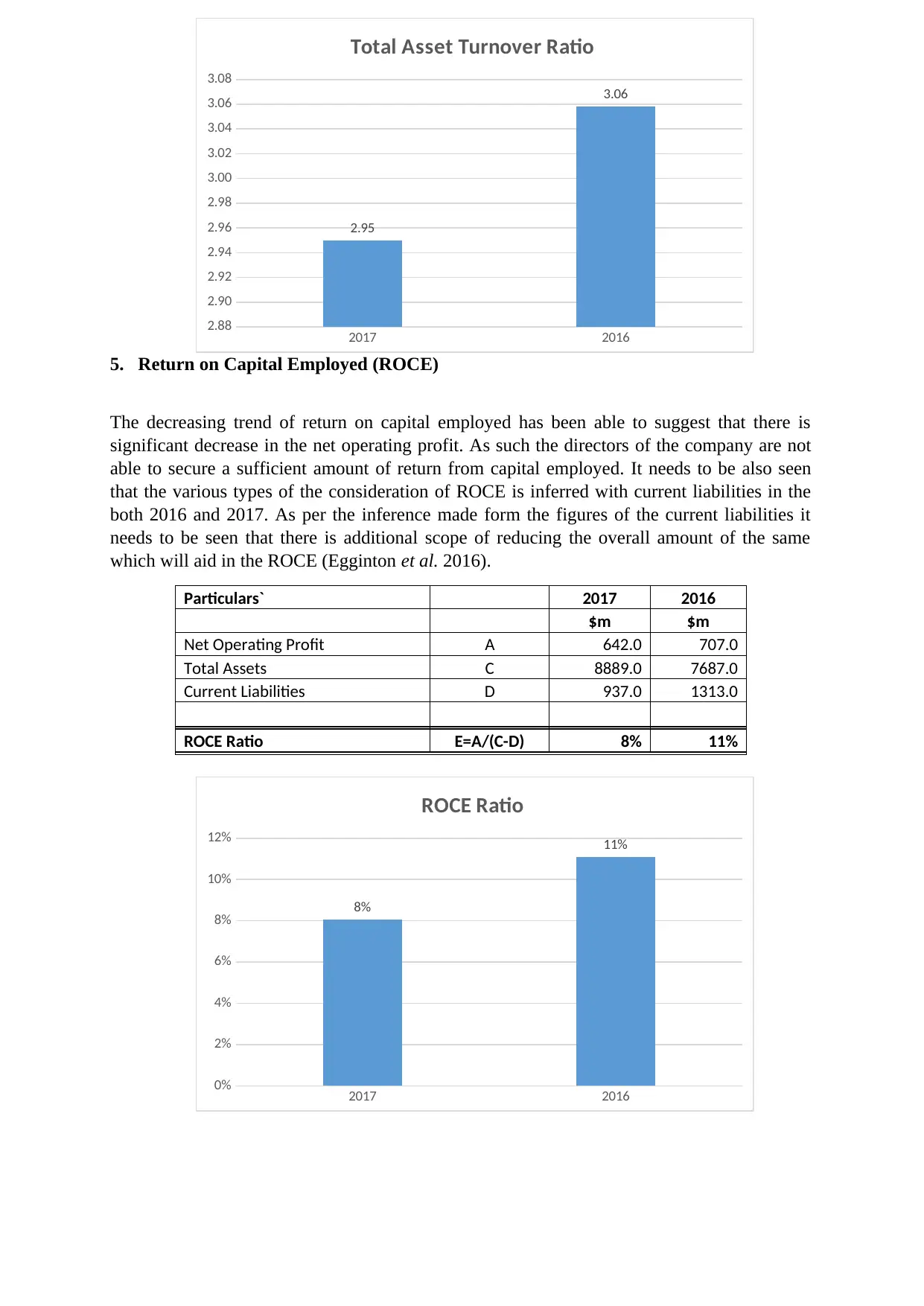

4. Asset Turnover Ratio

The computation of the asset turnover ratio is done by dividing the total revenue generated

from sales with total assets. It needs to be further seen that the depictions made from the

balance sheet has been able to show that there has been significant nature of the decreasing

trend of utilizing the assets. Despite of the increasing revenue generated from the sales and

amount of the total assets, the Sainsbury’s has been not able to sufficiently use the assets in

its favour (McKinney 2015).

Particulars` 2017 2016

$m $m

Total Assets A 8889.0 7687.0

Revenue C 26224.0 23506.0

Total Asset Turnover Ratio E=C/A 2.95 3.06

equity. Sainsbury’s is inferred with a reducing gearing ratio of 0.23 in 2017 from 0.26 in

2016. This

shows a positive trend for the company, as even after increase in both short term and long-

term borrowings,

it was able to decrease its gearing ratio. Furthermore, the increasing amount of the total equity

has aided Sainsbury’s to rely less on short term financing options (Zietlow et al. 2018).

Particulars` 2017 2016

$m $m

Total Equity B 7247.0 6111.0

Total Liabilities C 1642.0 1576.0

Gearing Ratio D=C/B 0.23 0.26

2017 2016

0.21

0.22

0.23

0.24

0.25

0.26

0.27

0.23

0.26

Gearing Ratio

4. Asset Turnover Ratio

The computation of the asset turnover ratio is done by dividing the total revenue generated

from sales with total assets. It needs to be further seen that the depictions made from the

balance sheet has been able to show that there has been significant nature of the decreasing

trend of utilizing the assets. Despite of the increasing revenue generated from the sales and

amount of the total assets, the Sainsbury’s has been not able to sufficiently use the assets in

its favour (McKinney 2015).

Particulars` 2017 2016

$m $m

Total Assets A 8889.0 7687.0

Revenue C 26224.0 23506.0

Total Asset Turnover Ratio E=C/A 2.95 3.06

2017 2016

2.88

2.90

2.92

2.94

2.96

2.98

3.00

3.02

3.04

3.06

3.08

2.95

3.06

Total Asset Turnover Ratio

5. Return on Capital Employed (ROCE)

The decreasing trend of return on capital employed has been able to suggest that there is

significant decrease in the net operating profit. As such the directors of the company are not

able to secure a sufficient amount of return from capital employed. It needs to be also seen

that the various types of the consideration of ROCE is inferred with current liabilities in the

both 2016 and 2017. As per the inference made form the figures of the current liabilities it

needs to be seen that there is additional scope of reducing the overall amount of the same

which will aid in the ROCE (Egginton et al. 2016).

Particulars` 2017 2016

$m $m

Net Operating Profit A 642.0 707.0

Total Assets C 8889.0 7687.0

Current Liabilities D 937.0 1313.0

ROCE Ratio E=A/(C-D) 8% 11%

2017 2016

0%

2%

4%

6%

8%

10%

12%

8%

11%

ROCE Ratio

2.88

2.90

2.92

2.94

2.96

2.98

3.00

3.02

3.04

3.06

3.08

2.95

3.06

Total Asset Turnover Ratio

5. Return on Capital Employed (ROCE)

The decreasing trend of return on capital employed has been able to suggest that there is

significant decrease in the net operating profit. As such the directors of the company are not

able to secure a sufficient amount of return from capital employed. It needs to be also seen

that the various types of the consideration of ROCE is inferred with current liabilities in the

both 2016 and 2017. As per the inference made form the figures of the current liabilities it

needs to be seen that there is additional scope of reducing the overall amount of the same

which will aid in the ROCE (Egginton et al. 2016).

Particulars` 2017 2016

$m $m

Net Operating Profit A 642.0 707.0

Total Assets C 8889.0 7687.0

Current Liabilities D 937.0 1313.0

ROCE Ratio E=A/(C-D) 8% 11%

2017 2016

0%

2%

4%

6%

8%

10%

12%

8%

11%

ROCE Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

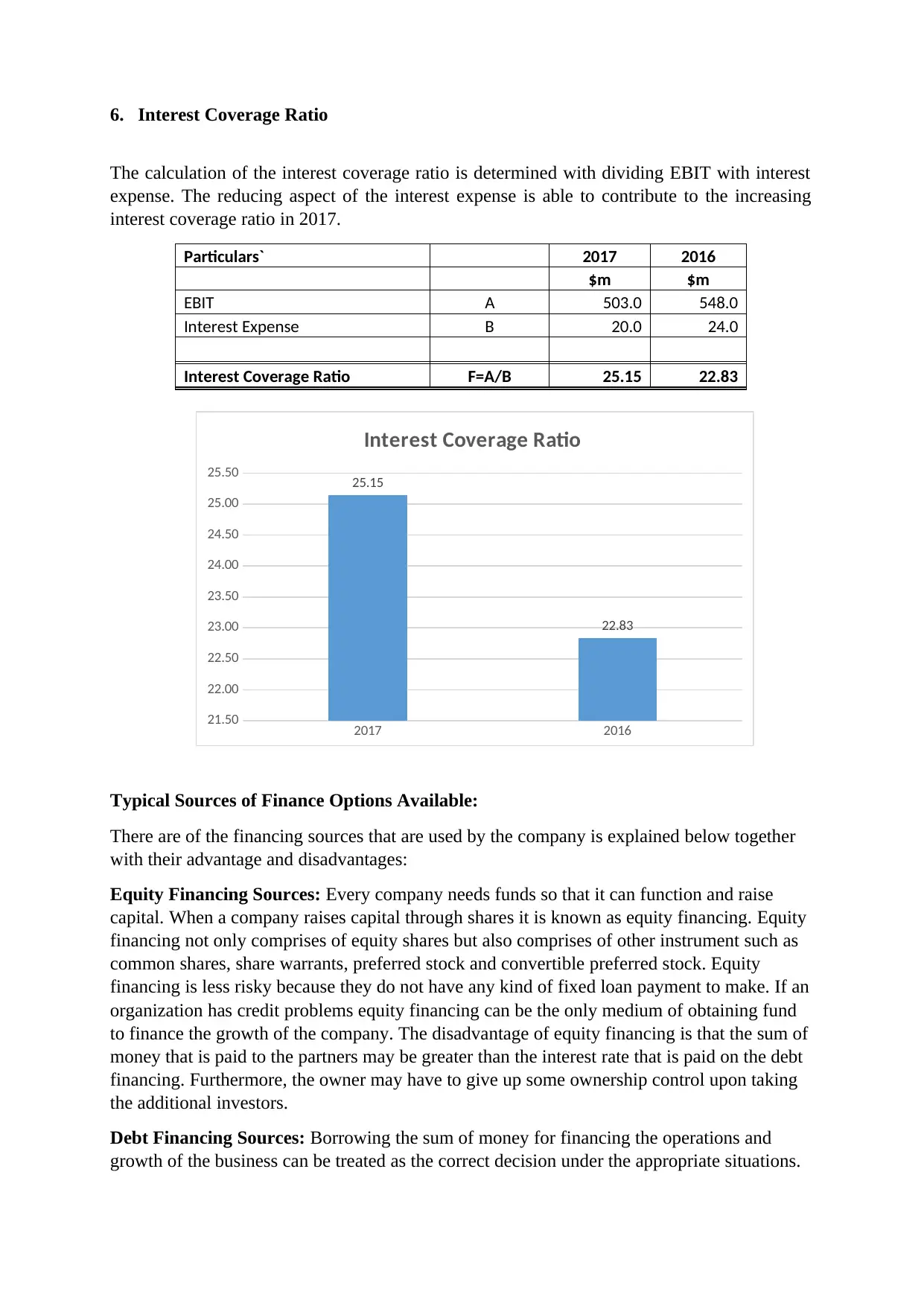

6. Interest Coverage Ratio

The calculation of the interest coverage ratio is determined with dividing EBIT with interest

expense. The reducing aspect of the interest expense is able to contribute to the increasing

interest coverage ratio in 2017.

Particulars` 2017 2016

$m $m

EBIT A 503.0 548.0

Interest Expense B 20.0 24.0

Interest Coverage Ratio F=A/B 25.15 22.83

2017 2016

21.50

22.00

22.50

23.00

23.50

24.00

24.50

25.00

25.50 25.15

22.83

Interest Coverage Ratio

Typical Sources of Finance Options Available:

There are of the financing sources that are used by the company is explained below together

with their advantage and disadvantages:

Equity Financing Sources: Every company needs funds so that it can function and raise

capital. When a company raises capital through shares it is known as equity financing. Equity

financing not only comprises of equity shares but also comprises of other instrument such as

common shares, share warrants, preferred stock and convertible preferred stock. Equity

financing is less risky because they do not have any kind of fixed loan payment to make. If an

organization has credit problems equity financing can be the only medium of obtaining fund

to finance the growth of the company. The disadvantage of equity financing is that the sum of

money that is paid to the partners may be greater than the interest rate that is paid on the debt

financing. Furthermore, the owner may have to give up some ownership control upon taking

the additional investors.

Debt Financing Sources: Borrowing the sum of money for financing the operations and

growth of the business can be treated as the correct decision under the appropriate situations.

The calculation of the interest coverage ratio is determined with dividing EBIT with interest

expense. The reducing aspect of the interest expense is able to contribute to the increasing

interest coverage ratio in 2017.

Particulars` 2017 2016

$m $m

EBIT A 503.0 548.0

Interest Expense B 20.0 24.0

Interest Coverage Ratio F=A/B 25.15 22.83

2017 2016

21.50

22.00

22.50

23.00

23.50

24.00

24.50

25.00

25.50 25.15

22.83

Interest Coverage Ratio

Typical Sources of Finance Options Available:

There are of the financing sources that are used by the company is explained below together

with their advantage and disadvantages:

Equity Financing Sources: Every company needs funds so that it can function and raise

capital. When a company raises capital through shares it is known as equity financing. Equity

financing not only comprises of equity shares but also comprises of other instrument such as

common shares, share warrants, preferred stock and convertible preferred stock. Equity

financing is less risky because they do not have any kind of fixed loan payment to make. If an

organization has credit problems equity financing can be the only medium of obtaining fund

to finance the growth of the company. The disadvantage of equity financing is that the sum of

money that is paid to the partners may be greater than the interest rate that is paid on the debt

financing. Furthermore, the owner may have to give up some ownership control upon taking

the additional investors.

Debt Financing Sources: Borrowing the sum of money for financing the operations and

growth of the business can be treated as the correct decision under the appropriate situations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The sources of debt financing include the banks, credit unions, consumer finance company,

trade credit or the leasing companies. The advantage of debt financing is that loan interest is

deductible for tax. Principle and payment of interest are provided in advance therefore it

becomes easy to work in the cash flow of the company. However, the disadvantage is that

taking large amount of debt may make the business vulnerable and may have the problems of

meeting loan payments given the cash flow falls. Payment of principle and interest should be

paid on the specific dates without any failure. Business that have uncertain cash flow may

face the difficulties in making payment of loan.

Retained Earnings: Retained earnings refers to the part of profit that is not distributed

between the shareholders but the same is retained and used for the business purpose. This is a

vital source of finance because it uses the working capital. The retained earnings are the

cheaper source of finance and financial stability and the shareholders may get the sufficient

dividend even though the company does not earn sufficient profit. The disadvantage of

retained earnings is that improper usage of funds may result in careless spending of funds.

Conservative dividend policy may result in over-use of capitalization.

Justification a 20% Net Asset investment in meeting future management priorities

Some of the typical sources available to justify the net asset investment in meeting the future

management priorities can be understood with both short financing options and long-term

financing options. The short-term financing options to justify a 20% Net Asset investment

may be inferred with proceeding with an overdraft agreement. In addition to this, the

company also has the choice of proceeding with short term financing options such as

accounts receivable financing, customer advances and selling goods on instalment. The

available options for the long-term financing needs to be understood with taking long term

loan from the bank at best possible rate of interest. In addition to this, the long-term financing

options are contingent with looking for JV agreements through retained portion of profits

which may be used as the working capital by the company (Cashin et al. 2017).

In extreme situations Sainsbury’s PLC has the option of issuing equities and debentures. This

will be beneficial for the organization in consideration of investments in large-scale ventures.

This can be proceeded by issuing bonds and debentures to the general public and in some

cases when there is a requirement of huge quantum of funds (Braun and Raddatz 2016).

Answer to Part 2

Most leaders are of the opinion that budget process is identified with a considerable problem

of being fit for the modern environment from a planning and control dimension. The budget

in general is supposed to provide a detailed plan in a strategic planning period. Despite of

this, previous experience has shown instances where there has been little constitution made

towards viability of budgeting. The budgeting process is considered as a constraint to the

value adding activities. Some of the different forms of the negative effects generated by the

process of budget needs to be well-thought-out in terms of the fighting for unambitious

targets by the rational managers thereby leading to scope for personal gains. Secondly, as the

budget are always fluctuating, the company may face difficulties in determining its success in

a particular year of operations. Some of the different types of the other constraints of the

process of budgeting needs to be understood in terms of increased cost of implementation and

integration with number of other cost overheads. Even in case the goal of cost budget is met,

there is no assurance for the company in using optimal resources. Therefore, even if the

trade credit or the leasing companies. The advantage of debt financing is that loan interest is

deductible for tax. Principle and payment of interest are provided in advance therefore it

becomes easy to work in the cash flow of the company. However, the disadvantage is that

taking large amount of debt may make the business vulnerable and may have the problems of

meeting loan payments given the cash flow falls. Payment of principle and interest should be

paid on the specific dates without any failure. Business that have uncertain cash flow may

face the difficulties in making payment of loan.

Retained Earnings: Retained earnings refers to the part of profit that is not distributed

between the shareholders but the same is retained and used for the business purpose. This is a

vital source of finance because it uses the working capital. The retained earnings are the

cheaper source of finance and financial stability and the shareholders may get the sufficient

dividend even though the company does not earn sufficient profit. The disadvantage of

retained earnings is that improper usage of funds may result in careless spending of funds.

Conservative dividend policy may result in over-use of capitalization.

Justification a 20% Net Asset investment in meeting future management priorities

Some of the typical sources available to justify the net asset investment in meeting the future

management priorities can be understood with both short financing options and long-term

financing options. The short-term financing options to justify a 20% Net Asset investment

may be inferred with proceeding with an overdraft agreement. In addition to this, the

company also has the choice of proceeding with short term financing options such as

accounts receivable financing, customer advances and selling goods on instalment. The

available options for the long-term financing needs to be understood with taking long term

loan from the bank at best possible rate of interest. In addition to this, the long-term financing

options are contingent with looking for JV agreements through retained portion of profits

which may be used as the working capital by the company (Cashin et al. 2017).

In extreme situations Sainsbury’s PLC has the option of issuing equities and debentures. This

will be beneficial for the organization in consideration of investments in large-scale ventures.

This can be proceeded by issuing bonds and debentures to the general public and in some

cases when there is a requirement of huge quantum of funds (Braun and Raddatz 2016).

Answer to Part 2

Most leaders are of the opinion that budget process is identified with a considerable problem

of being fit for the modern environment from a planning and control dimension. The budget

in general is supposed to provide a detailed plan in a strategic planning period. Despite of

this, previous experience has shown instances where there has been little constitution made

towards viability of budgeting. The budgeting process is considered as a constraint to the

value adding activities. Some of the different forms of the negative effects generated by the

process of budget needs to be well-thought-out in terms of the fighting for unambitious

targets by the rational managers thereby leading to scope for personal gains. Secondly, as the

budget are always fluctuating, the company may face difficulties in determining its success in

a particular year of operations. Some of the different types of the other constraints of the

process of budgeting needs to be understood in terms of increased cost of implementation and

integration with number of other cost overheads. Even in case the goal of cost budget is met,

there is no assurance for the company in using optimal resources. Therefore, even if the

revenue budget is met, there is no proof of success and origin of the market share (Xing et al.

2017).

The use of the predictive modelling techniques such as cloud computing and big data will be

useful in understanding the usability of data mining in finance and discerning probability of

the forecasted outcomes for the company. The predictive modeling methodologies are seen

with using logistic regression, time series analysis and decision trees. The predictive

modelling in the next five years may be able to detect the money laundering practices and at

the same time incorporate a linear predictive model. The retail giants may be adopting neural

networks such as machine learning and deep learning and incorporate artificial intelligence to

track the changes in consumer demand which would have not been possible in traditional

budgeting (Ogiela 2015).

Answer to Part 3

In general, the performance management has been beneficial for the organisations in staying

ahead of the competition. The various types of the performance management tools and

techniques to improve the performance of the organization both at corporate and individual

level are listed as follows:

Key performance indicators (KPIs) and metrics- The KPIs are often inferred to be

commonly used as performance management tools. The primary values of the KPIs is

not in measurement per se but in enabling a rich data driven performance which may

be considered with better decision making (Le et al. 2018).

Performance Appraisals: In case these are appropriately used then performance

appraisals will be incredibly powerful and make possibility of alignment of the

strategic aims and goals of individuals. The employees should feel that the appraisal is

fair, regular and honest with a constructive two-way conversation (Ksendzova,

Donnelly and Howell 2017).

Providing a 360-degree feedback: This particular tool is conducive for addressing

the question of how the individuals are performing in the eyes of those who are having

a stake in the business. It is able to provide the individuals with the appropriate

assessment of their performance as per the views of customers, suppliers, supervisor

and manager. The results of such an analysis are significantly tallied with the various

types of the assertions which are depicted to be made by the manager. The

2017).

The use of the predictive modelling techniques such as cloud computing and big data will be

useful in understanding the usability of data mining in finance and discerning probability of

the forecasted outcomes for the company. The predictive modeling methodologies are seen

with using logistic regression, time series analysis and decision trees. The predictive

modelling in the next five years may be able to detect the money laundering practices and at

the same time incorporate a linear predictive model. The retail giants may be adopting neural

networks such as machine learning and deep learning and incorporate artificial intelligence to

track the changes in consumer demand which would have not been possible in traditional

budgeting (Ogiela 2015).

Answer to Part 3

In general, the performance management has been beneficial for the organisations in staying

ahead of the competition. The various types of the performance management tools and

techniques to improve the performance of the organization both at corporate and individual

level are listed as follows:

Key performance indicators (KPIs) and metrics- The KPIs are often inferred to be

commonly used as performance management tools. The primary values of the KPIs is

not in measurement per se but in enabling a rich data driven performance which may

be considered with better decision making (Le et al. 2018).

Performance Appraisals: In case these are appropriately used then performance

appraisals will be incredibly powerful and make possibility of alignment of the

strategic aims and goals of individuals. The employees should feel that the appraisal is

fair, regular and honest with a constructive two-way conversation (Ksendzova,

Donnelly and Howell 2017).

Providing a 360-degree feedback: This particular tool is conducive for addressing

the question of how the individuals are performing in the eyes of those who are having

a stake in the business. It is able to provide the individuals with the appropriate

assessment of their performance as per the views of customers, suppliers, supervisor

and manager. The results of such an analysis are significantly tallied with the various

types of the assertions which are depicted to be made by the manager. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.