Strategic Finance: Samsung PLC Financial Statement Analysis Report

VerifiedAdded on 2023/01/20

|29

|4354

|95

Report

AI Summary

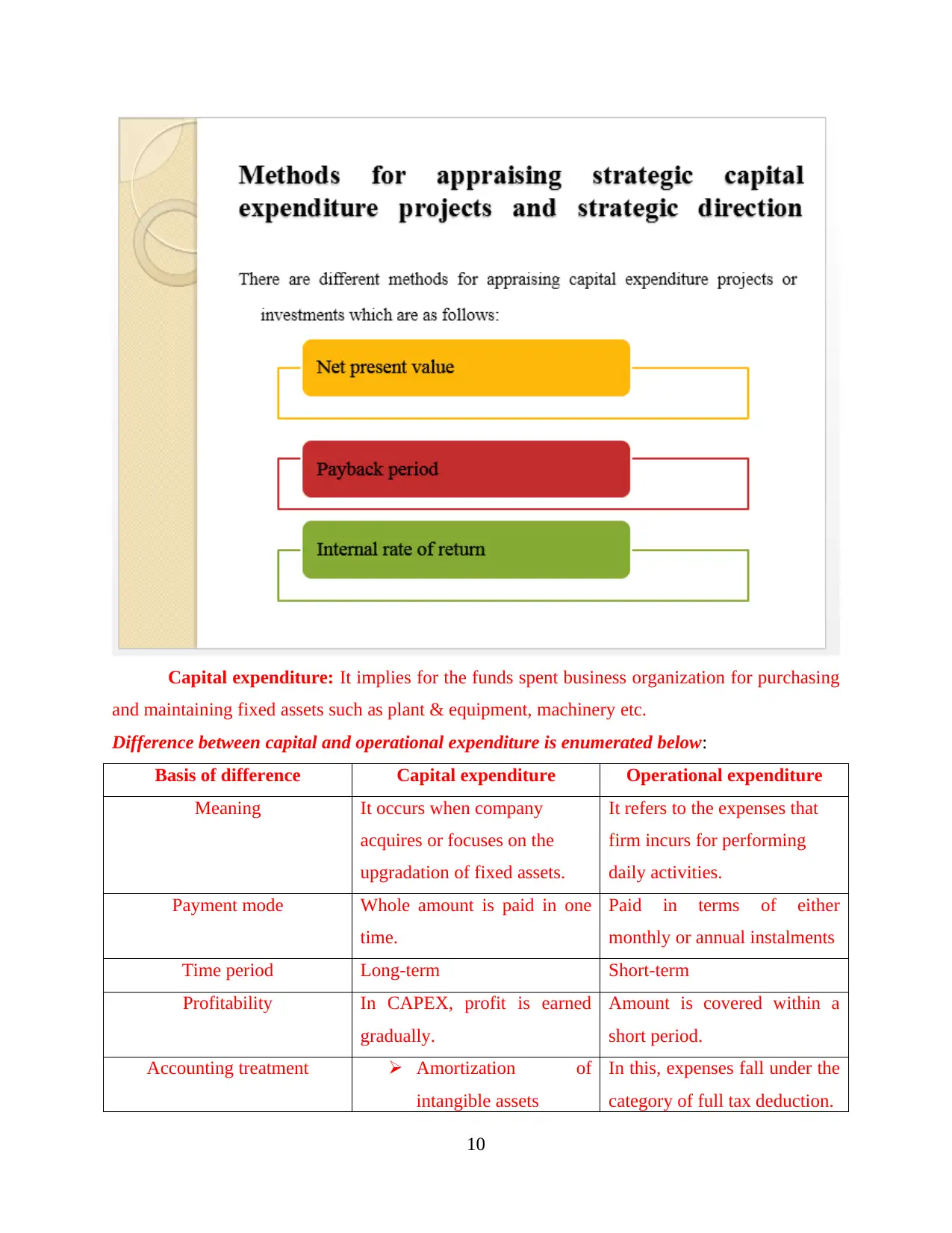

This report presents a comprehensive financial analysis of Samsung PLC, examining various aspects of its financial performance and strategic decision-making. It begins with an introduction discussing the role of financial data in business strategy and risk analysis. Task 1 delves into profitability, capital efficiency, and solvency ratios, emphasizing the importance of external information from suppliers, government, and customers. It explores cash flow management, risk assessment (market, credit, liquidity, operational, and interest risks), and the distinction between capital and operational expenditure. Task 2 focuses on interpreting and comparing Samsung PLC's financial statements using ratios, providing recommendations based on the analysis. Task 3 addresses the impact of 'creative accounting' techniques, the importance of cash flow management in capital expenditure evaluation, and the limitations of ratio analysis. Finally, Task 4 reviews capital expenditure appraisal methods. The report highlights the importance of financial metrics in assessing the company's current viability and making strategic recommendations. It also includes an analysis of investment ratios and the overall growth of Samsung, concluding with the company's financial performance from 2017 to 2018.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.