Business Finance Project: Financial Management of Shower pak Ltd.

VerifiedAdded on 2021/02/21

|8

|2332

|47

Project

AI Summary

This business finance project provides a comprehensive analysis of Shower pak Limited, a family-owned manufacturer of molded shower units. The project delves into key aspects of financial management, including the accounting equation and its application, evaluating changes in balance sheet components, and explaining the reasons for capital changes. It further examines revenue and capital expenditures, contrasting gross and net profit, and differentiating between cost of sales and turnover. The project also explores the purpose of the cash flow statement and the discrepancies between bank and cash statements. Additionally, it assesses the use of benchmarking for performance measurement and analyzes the company's efficiency. The analysis includes detailed interpretations of financial data and concludes with a summary of the findings, supported by relevant academic references. The project highlights the importance of effective financial decision-making for business success.

BUSINESS FINANCE

PROJECT- FINANCIAL

MANAGEMENT

PROJECT- FINANCIAL

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1........................................................................................................................................................1

a. Explaining the accounting equation and its application..........................................................1

b. Evaluating the changes in the components of balance sheet with explanation of their effects.

.....................................................................................................................................................1

c. Explaining the reasons for the change in the capital for an accounting period.......................2

2. ......................................................................................................................................................2

a. Analysing the effect of the revenue expenditure on the profits and the impact of the

incorrect evaluation of the revenue expenditure and capital expenditure...................................2

b. Explaining the contrast between the gross and the net profit..................................................3

c. Explaining the contrast in between the cost of the sales and the turnover..............................3

3........................................................................................................................................................3

a. Explaining the purpose of the cash flow statement ................................................................3

b. Explaining the grounds for the discrepancy in between the bank and the cash statement .....4

4........................................................................................................................................................4

a. Assessing the ways in which the business uses the benchmarking in respect of measuring

the performance with evaluation of its benefits and the limitations...........................................4

b. Analysing the efficiency in the performance of the company ...............................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

1........................................................................................................................................................1

a. Explaining the accounting equation and its application..........................................................1

b. Evaluating the changes in the components of balance sheet with explanation of their effects.

.....................................................................................................................................................1

c. Explaining the reasons for the change in the capital for an accounting period.......................2

2. ......................................................................................................................................................2

a. Analysing the effect of the revenue expenditure on the profits and the impact of the

incorrect evaluation of the revenue expenditure and capital expenditure...................................2

b. Explaining the contrast between the gross and the net profit..................................................3

c. Explaining the contrast in between the cost of the sales and the turnover..............................3

3........................................................................................................................................................3

a. Explaining the purpose of the cash flow statement ................................................................3

b. Explaining the grounds for the discrepancy in between the bank and the cash statement .....4

4........................................................................................................................................................4

a. Assessing the ways in which the business uses the benchmarking in respect of measuring

the performance with evaluation of its benefits and the limitations...........................................4

b. Analysing the efficiency in the performance of the company ...............................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Business finance means the money and the credit that are employed in the business. It

includes the acquisition and the utilization of the funds optimally for attaining the smooth

functioning of the business operations. The present study is based on the Shower pak Limited,

family owned manufacturer, produces moulded shower for the room units. Furthermore, the

study throws deep insights relating to the accounting equation, components of the balance sheet

and the grounds of discrepancy in the bank and cash statement.

1.

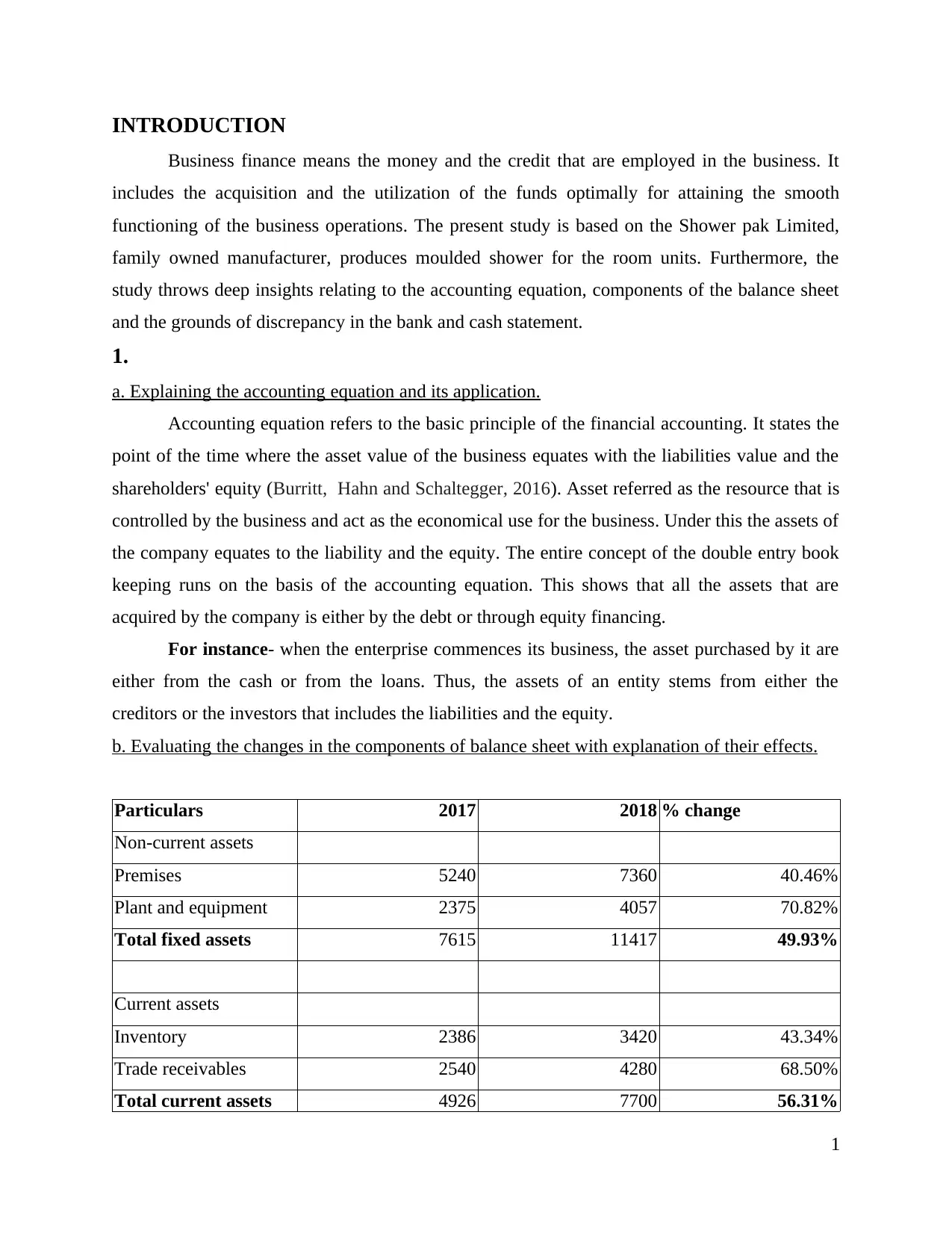

a. Explaining the accounting equation and its application.

Accounting equation refers to the basic principle of the financial accounting. It states the

point of the time where the asset value of the business equates with the liabilities value and the

shareholders' equity (Burritt, Hahn and Schaltegger, 2016). Asset referred as the resource that is

controlled by the business and act as the economical use for the business. Under this the assets of

the company equates to the liability and the equity. The entire concept of the double entry book

keeping runs on the basis of the accounting equation. This shows that all the assets that are

acquired by the company is either by the debt or through equity financing.

For instance- when the enterprise commences its business, the asset purchased by it are

either from the cash or from the loans. Thus, the assets of an entity stems from either the

creditors or the investors that includes the liabilities and the equity.

b. Evaluating the changes in the components of balance sheet with explanation of their effects.

Particulars 2017 2018 % change

Non-current assets

Premises 5240 7360 40.46%

Plant and equipment 2375 4057 70.82%

Total fixed assets 7615 11417 49.93%

Current assets

Inventory 2386 3420 43.34%

Trade receivables 2540 4280 68.50%

Total current assets 4926 7700 56.31%

1

Business finance means the money and the credit that are employed in the business. It

includes the acquisition and the utilization of the funds optimally for attaining the smooth

functioning of the business operations. The present study is based on the Shower pak Limited,

family owned manufacturer, produces moulded shower for the room units. Furthermore, the

study throws deep insights relating to the accounting equation, components of the balance sheet

and the grounds of discrepancy in the bank and cash statement.

1.

a. Explaining the accounting equation and its application.

Accounting equation refers to the basic principle of the financial accounting. It states the

point of the time where the asset value of the business equates with the liabilities value and the

shareholders' equity (Burritt, Hahn and Schaltegger, 2016). Asset referred as the resource that is

controlled by the business and act as the economical use for the business. Under this the assets of

the company equates to the liability and the equity. The entire concept of the double entry book

keeping runs on the basis of the accounting equation. This shows that all the assets that are

acquired by the company is either by the debt or through equity financing.

For instance- when the enterprise commences its business, the asset purchased by it are

either from the cash or from the loans. Thus, the assets of an entity stems from either the

creditors or the investors that includes the liabilities and the equity.

b. Evaluating the changes in the components of balance sheet with explanation of their effects.

Particulars 2017 2018 % change

Non-current assets

Premises 5240 7360 40.46%

Plant and equipment 2375 4057 70.82%

Total fixed assets 7615 11417 49.93%

Current assets

Inventory 2386 3420 43.34%

Trade receivables 2540 4280 68.50%

Total current assets 4926 7700 56.31%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

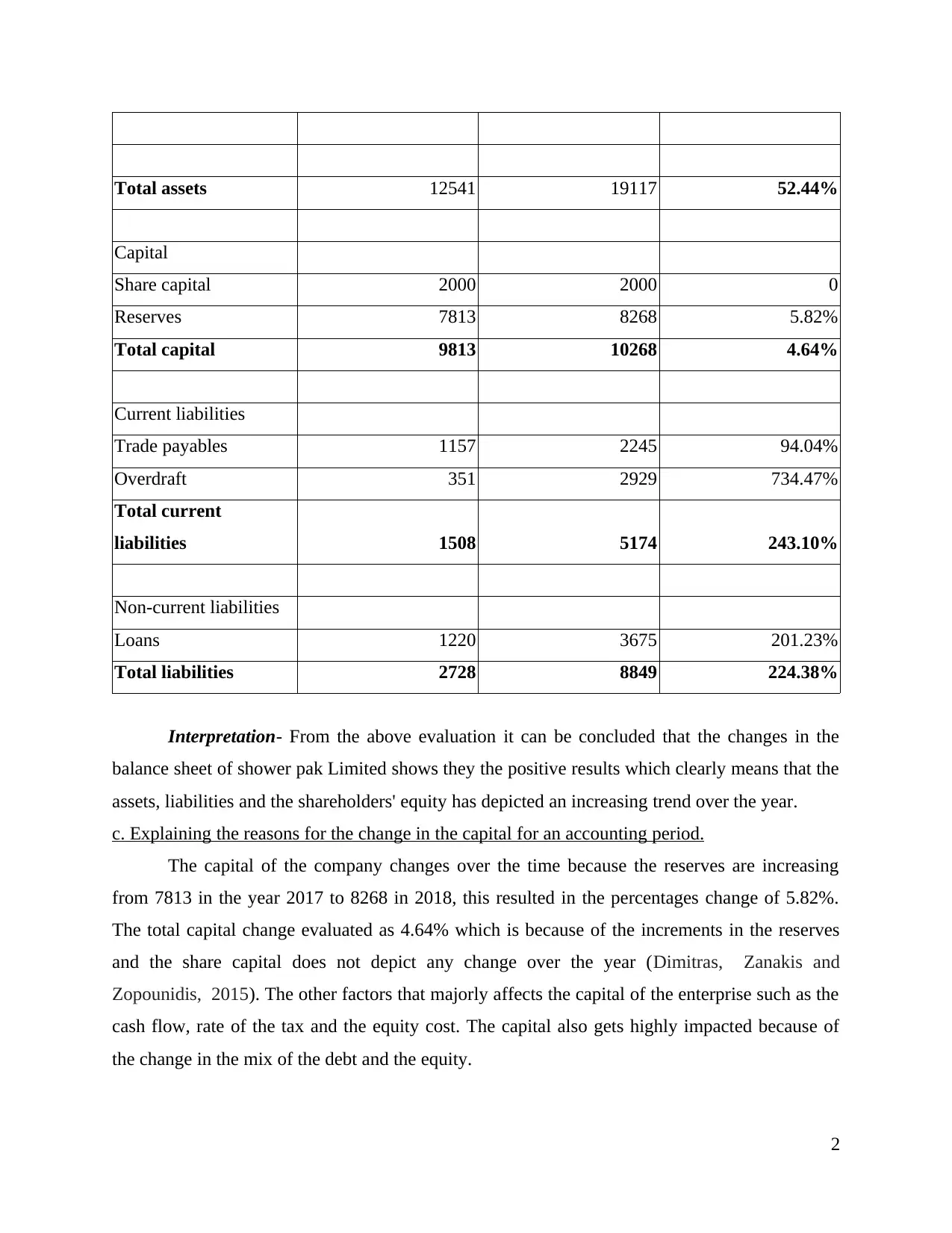

Total assets 12541 19117 52.44%

Capital

Share capital 2000 2000 0

Reserves 7813 8268 5.82%

Total capital 9813 10268 4.64%

Current liabilities

Trade payables 1157 2245 94.04%

Overdraft 351 2929 734.47%

Total current

liabilities 1508 5174 243.10%

Non-current liabilities

Loans 1220 3675 201.23%

Total liabilities 2728 8849 224.38%

Interpretation- From the above evaluation it can be concluded that the changes in the

balance sheet of shower pak Limited shows they the positive results which clearly means that the

assets, liabilities and the shareholders' equity has depicted an increasing trend over the year.

c. Explaining the reasons for the change in the capital for an accounting period.

The capital of the company changes over the time because the reserves are increasing

from 7813 in the year 2017 to 8268 in 2018, this resulted in the percentages change of 5.82%.

The total capital change evaluated as 4.64% which is because of the increments in the reserves

and the share capital does not depict any change over the year (Dimitras, Zanakis and

Zopounidis, 2015). The other factors that majorly affects the capital of the enterprise such as the

cash flow, rate of the tax and the equity cost. The capital also gets highly impacted because of

the change in the mix of the debt and the equity.

2

Capital

Share capital 2000 2000 0

Reserves 7813 8268 5.82%

Total capital 9813 10268 4.64%

Current liabilities

Trade payables 1157 2245 94.04%

Overdraft 351 2929 734.47%

Total current

liabilities 1508 5174 243.10%

Non-current liabilities

Loans 1220 3675 201.23%

Total liabilities 2728 8849 224.38%

Interpretation- From the above evaluation it can be concluded that the changes in the

balance sheet of shower pak Limited shows they the positive results which clearly means that the

assets, liabilities and the shareholders' equity has depicted an increasing trend over the year.

c. Explaining the reasons for the change in the capital for an accounting period.

The capital of the company changes over the time because the reserves are increasing

from 7813 in the year 2017 to 8268 in 2018, this resulted in the percentages change of 5.82%.

The total capital change evaluated as 4.64% which is because of the increments in the reserves

and the share capital does not depict any change over the year (Dimitras, Zanakis and

Zopounidis, 2015). The other factors that majorly affects the capital of the enterprise such as the

cash flow, rate of the tax and the equity cost. The capital also gets highly impacted because of

the change in the mix of the debt and the equity.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.

a. Analysing the effect of the revenue expenditure on the profits and the impact of the incorrect

evaluation of the revenue expenditure and capital expenditure.

Revenue expenditure refers to the cost incurred relating to the expenses of the Shower

pak Limited. These expenditures are considered as essential in respect of maintaining the earning

capacity of the company. Revenue expenditure has a greater impact on the profits of an entity as

higher expenses leads to lower profitability so it is important for the company to ensure adequate

control over its spending in order to earn higher profitability (Bowman, 2017). Incorrect

treatment or evaluation of the revenue and the capital expenditure has a direct impact on the

profits and the fixed assets which in turn relates with the performance and the position of Shower

pak Limited. If in case the capital expenditure is been treated as the revenue expenditure than the

expenses shown are of higher amount and the fixed asset will be of lower amount and this affects

the final results of the enterprise.

b. Explaining the contrast between the gross and the net profit.

Gross profit Net profit

It is the difference in between the net sales and

the cost of sales.

It depicts the difference in between the gross

profit and all the indirect expenses or losses.

Gross profits are been transferred to the profits

and the loss account (Amit and Livnat, 2015).

Net profits is been transferred directly to the

capital account.

It does involve any income that is generated

from the other sources.

It might include the income that is been

generated from the other sources.

It is been evaluated by preparing the trading

account.

It is been ascertained by the preparation of the

P&L account.

Gross profit does not depend upon the net

profit amount.

However, net profit depends upon the gross

profit amount.

c. Explaining the contrast in between the cost of the sales and the turnover.

Cost of sales Turnover

It refers to direct cost that is attributable It refers to the net sales that is been achieved

3

a. Analysing the effect of the revenue expenditure on the profits and the impact of the incorrect

evaluation of the revenue expenditure and capital expenditure.

Revenue expenditure refers to the cost incurred relating to the expenses of the Shower

pak Limited. These expenditures are considered as essential in respect of maintaining the earning

capacity of the company. Revenue expenditure has a greater impact on the profits of an entity as

higher expenses leads to lower profitability so it is important for the company to ensure adequate

control over its spending in order to earn higher profitability (Bowman, 2017). Incorrect

treatment or evaluation of the revenue and the capital expenditure has a direct impact on the

profits and the fixed assets which in turn relates with the performance and the position of Shower

pak Limited. If in case the capital expenditure is been treated as the revenue expenditure than the

expenses shown are of higher amount and the fixed asset will be of lower amount and this affects

the final results of the enterprise.

b. Explaining the contrast between the gross and the net profit.

Gross profit Net profit

It is the difference in between the net sales and

the cost of sales.

It depicts the difference in between the gross

profit and all the indirect expenses or losses.

Gross profits are been transferred to the profits

and the loss account (Amit and Livnat, 2015).

Net profits is been transferred directly to the

capital account.

It does involve any income that is generated

from the other sources.

It might include the income that is been

generated from the other sources.

It is been evaluated by preparing the trading

account.

It is been ascertained by the preparation of the

P&L account.

Gross profit does not depend upon the net

profit amount.

However, net profit depends upon the gross

profit amount.

c. Explaining the contrast in between the cost of the sales and the turnover.

Cost of sales Turnover

It refers to direct cost that is attributable It refers to the net sales that is been achieved

3

towards the production of goods that is been

sold within the company (Holthausen, 2019).

by the business of Shower pak Limited.

It is computed by deducting the gross profit

from the sales.

It is calculated by adding the cost and the profit

amount of the company.

3.

a. Explaining the purpose of the cash flow statement

Cash flow statement is referred as the financial statements which facilitates aggregate

data relating to the cash inflows that the company receives through its operations and the

external sources of the investment. It also involves the outflows of the cash that the business

pays and the investments at a given time period (Mohamed and Lashine, 2015). The foremost

purpose of the cash flow statement is to facilitate the information in relation to the cash receipts,

payment of cash and the resultant changes in the cash from the activities of Shower pak business.

Cash flow statement is prepared with the objective of making the assessment of the change in the

operating, investing and the financing activity of the organization.

b. Explaining the grounds for the discrepancy in between the bank and the cash statement

There are various grounds that results in the difference between the cash book and the

pass book such as non-presentment of the cheque issued for the payment, cheque deposited but

yet not collected by bank, the interest that is credited by bank but wrongly entered in the cash

book, bank charges debited by the bank and not entered in the cash book, expenses paid and the

income collected by bank on the behalf of the customer but is not recorded in the cash book, any

amount that is deposited by the debtors directly into bank and thus not recorded in the cash book,

dishonour of the cheque and the bill (Zimmerman, 2018). Thus, theses were the main reasons

for the resultant discrepancy in the bank and the cash statement.

4.

a. Assessing the ways in which the business uses the benchmarking in respect of measuring the

performance with evaluation of its benefits and the limitations

Bench-marking is the technique that is used by Shower pak in order to discover the best

performance that is being by the industry. This information helps the company in determining

4

sold within the company (Holthausen, 2019).

by the business of Shower pak Limited.

It is computed by deducting the gross profit

from the sales.

It is calculated by adding the cost and the profit

amount of the company.

3.

a. Explaining the purpose of the cash flow statement

Cash flow statement is referred as the financial statements which facilitates aggregate

data relating to the cash inflows that the company receives through its operations and the

external sources of the investment. It also involves the outflows of the cash that the business

pays and the investments at a given time period (Mohamed and Lashine, 2015). The foremost

purpose of the cash flow statement is to facilitate the information in relation to the cash receipts,

payment of cash and the resultant changes in the cash from the activities of Shower pak business.

Cash flow statement is prepared with the objective of making the assessment of the change in the

operating, investing and the financing activity of the organization.

b. Explaining the grounds for the discrepancy in between the bank and the cash statement

There are various grounds that results in the difference between the cash book and the

pass book such as non-presentment of the cheque issued for the payment, cheque deposited but

yet not collected by bank, the interest that is credited by bank but wrongly entered in the cash

book, bank charges debited by the bank and not entered in the cash book, expenses paid and the

income collected by bank on the behalf of the customer but is not recorded in the cash book, any

amount that is deposited by the debtors directly into bank and thus not recorded in the cash book,

dishonour of the cheque and the bill (Zimmerman, 2018). Thus, theses were the main reasons

for the resultant discrepancy in the bank and the cash statement.

4.

a. Assessing the ways in which the business uses the benchmarking in respect of measuring the

performance with evaluation of its benefits and the limitations

Bench-marking is the technique that is used by Shower pak in order to discover the best

performance that is being by the industry. This information helps the company in determining

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the gaps if any present in the process of the organization which in turn helps in achieving the

competitive edge for the enterprise in the overall market.

Benefits Limitations

Bench-marking provides for the improvement

in the performance and in enhancing the

competitiveness as it helps in setting out the

standards and the strategies for performing the

task.

It enables Shower pak in respect of focusing on

the change and also provides direction for

executing the change process(Power, 2019).

This technique remains inadequate in

measuring overall effectiveness of the metrics

and only measures the efficiency relating to

operational metrics (Gray, 2016).

In benchmarking there exist a certain level of

the complacency when the business exceeds

the standards relating to their competition.

b. Analysing the efficiency in the performance of the company

The computed efficiency ratios of Shower pak depicts that the days for collecting the

receivables and the paying to the creditors is increasing which in turn reflects that more sales

could be made and more purchases can be ascertained (Gray and Bebbington, 2015). The

inventory turnover period and the cash operating cycle also showing the increasing trend over the

years which indicates that more time is taken by the company in converting its inventory into

sales and the time in producing the product is also increasing. The assets turnover ratio decreases

because sales are less in comparison of the total assets of an entity.

CONCLUSION

From the above report it can be summarized that business finance is the crucial part of the

organization that helps in making the financial decisions efficiently and leads the company

towards growing success. It involves the effective management of the financial activities and

also the financial resources of the enterprise.

5

competitive edge for the enterprise in the overall market.

Benefits Limitations

Bench-marking provides for the improvement

in the performance and in enhancing the

competitiveness as it helps in setting out the

standards and the strategies for performing the

task.

It enables Shower pak in respect of focusing on

the change and also provides direction for

executing the change process(Power, 2019).

This technique remains inadequate in

measuring overall effectiveness of the metrics

and only measures the efficiency relating to

operational metrics (Gray, 2016).

In benchmarking there exist a certain level of

the complacency when the business exceeds

the standards relating to their competition.

b. Analysing the efficiency in the performance of the company

The computed efficiency ratios of Shower pak depicts that the days for collecting the

receivables and the paying to the creditors is increasing which in turn reflects that more sales

could be made and more purchases can be ascertained (Gray and Bebbington, 2015). The

inventory turnover period and the cash operating cycle also showing the increasing trend over the

years which indicates that more time is taken by the company in converting its inventory into

sales and the time in producing the product is also increasing. The assets turnover ratio decreases

because sales are less in comparison of the total assets of an entity.

CONCLUSION

From the above report it can be summarized that business finance is the crucial part of the

organization that helps in making the financial decisions efficiently and leads the company

towards growing success. It involves the effective management of the financial activities and

also the financial resources of the enterprise.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Amit, R. and Livnat, J., 2015. Diversification strategies, business cycles and economic

performance. Strategic Management Journal. 9(2). pp.99-110.

Bowman, R. G., 2017. The theoretical relationship between systematic risk and financial

(accounting) variables. The Journal of Finance. 34(3). pp.617-630.

Burritt, R. L., Hahn, T. and Schaltegger, S., 2016. Towards a comprehensive framework for

environmental management accounting—Links between business actors and

environmental management accounting tools. Australian Accounting Review. 12(27).

pp.39-50.

Dimitras, A. I., Zanakis, S. H. and Zopounidis, C., 2015. A survey of business failures with an

emphasis on prediction methods and industrial applications. European Journal of

Operational Research. 90(3). pp.487-513.

Gray, R. and Bebbington, J., 2015. Environmental accounting, managerialism and sustainability:

Is the planet safe in the hands of business and accounting?. In Advances in environmental

accounting & management (pp. 1-44). Emerald Group Publishing Limited.

Gray, S. J., 2016. Towards a theory of cultural influence on the development of accounting

systems internationally. Abacus. 24(1). pp.1-15.

Holthausen, R. W., 2019. Accounting standards, financial reporting outcomes, and

enforcement. Journal of Accounting Research. 47(2). pp.447-458.

Mohamed, E. K. and Lashine, S. H., 2015. Accounting knowledge and skills and the challenges

of a global business environment. Managerial finance. 29(7). pp.3-16.

Power, M., 2019. Fair value accounting, financial economics and the transformation of

reliability. Accounting and business research. 40(3). pp.197-210.

Zimmerman, J. L., 2018. Conjectures regarding empirical managerial accounting

research. Journal of accounting and economics. 32(1-3). pp.411-427.

6

Books and Journals

Amit, R. and Livnat, J., 2015. Diversification strategies, business cycles and economic

performance. Strategic Management Journal. 9(2). pp.99-110.

Bowman, R. G., 2017. The theoretical relationship between systematic risk and financial

(accounting) variables. The Journal of Finance. 34(3). pp.617-630.

Burritt, R. L., Hahn, T. and Schaltegger, S., 2016. Towards a comprehensive framework for

environmental management accounting—Links between business actors and

environmental management accounting tools. Australian Accounting Review. 12(27).

pp.39-50.

Dimitras, A. I., Zanakis, S. H. and Zopounidis, C., 2015. A survey of business failures with an

emphasis on prediction methods and industrial applications. European Journal of

Operational Research. 90(3). pp.487-513.

Gray, R. and Bebbington, J., 2015. Environmental accounting, managerialism and sustainability:

Is the planet safe in the hands of business and accounting?. In Advances in environmental

accounting & management (pp. 1-44). Emerald Group Publishing Limited.

Gray, S. J., 2016. Towards a theory of cultural influence on the development of accounting

systems internationally. Abacus. 24(1). pp.1-15.

Holthausen, R. W., 2019. Accounting standards, financial reporting outcomes, and

enforcement. Journal of Accounting Research. 47(2). pp.447-458.

Mohamed, E. K. and Lashine, S. H., 2015. Accounting knowledge and skills and the challenges

of a global business environment. Managerial finance. 29(7). pp.3-16.

Power, M., 2019. Fair value accounting, financial economics and the transformation of

reliability. Accounting and business research. 40(3). pp.197-210.

Zimmerman, J. L., 2018. Conjectures regarding empirical managerial accounting

research. Journal of accounting and economics. 32(1-3). pp.411-427.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.