Financial Decision Making: Detailed Analysis of SKANSA PLC Performance

VerifiedAdded on 2023/01/03

|12

|3716

|72

Report

AI Summary

This report provides a detailed analysis of financial decision-making within a business context, focusing on the roles of accounting and finance departments. It begins with an introduction to financial decision-making processes and their importance, followed by an examination of the accounting and finance departments, their responsibilities, and their significance within an organization. The main body of the report includes a case study of SKANSA PLC, a construction corporation, analyzing its financial performance through ratio analysis, including Return on Capital Employed (ROCE), net profit margin, current ratio, debtors collection period, and creditors collection period. The report compares SKANSA's performance over two years, highlighting key financial metrics and providing insights into its financial health. The report concludes with a summary of the findings and their implications for effective financial decision-making.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Accounting and Finance Department:.........................................................................................3

Importance of Accounting and Finance Department:..................................................................4

Role of Accounts Department.....................................................................................................4

Role of Finance Department:.......................................................................................................5

TASK 2............................................................................................................................................7

a. Calculation of of ratios for the company.................................................................................7

b. Comments on actual performance of company SKANSA and position for two years:..........9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Accounting and Finance Department:.........................................................................................3

Importance of Accounting and Finance Department:..................................................................4

Role of Accounts Department.....................................................................................................4

Role of Finance Department:.......................................................................................................5

TASK 2............................................................................................................................................7

a. Calculation of of ratios for the company.................................................................................7

b. Comments on actual performance of company SKANSA and position for two years:..........9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial decision-making within business context may be explained as the processes/set of

activities attributable to devising financial decisions for an entity by considering annual reports,

interim financial reports and business's other financial reports. It is extremely important for all

business to ensure that their accounting-personnel are concentrating on productive business

decisions because it will enable the fulfilment of all longer-term and shorter-term organizational

goals. The principal aim of this project is to strengthen the comprehension of the essential

aspects that all enterprises need to consider for formulate efficient financial decisions (Black,

2019). The current study is centred on the SKANSA PLC i.e. construction corporation

incorporated in 1984. Company is UK based and operating its business in multiple nations. This

report discusses multiple points regarding value of the accounting and finance tasks,

responsibilities and obligations within corporation.

MAIN BODY

TASK 1

Accounting and Finance Department:

Accounting Department: An accounting department is particular division/unit

within firm/business enterprise that is accountable for tracking and monitoring cash ins or

out flows of organisation. The accounting division is accountable for a vast variety

of accounting as well as tasks within the enterprise. This department not only responsible for

recording and reporting of financial reports but also formulate processes and policies for

controlling flow of funds within entity as well as safeguards financial resources. It is component

of administration of organization liable for filing the annual statements, managing the corporate

accounts, collecting bills, billing buyers, payrolls, expense monitoring, financial reporting, and

much more. The top of accounting department also carries the designation of controller (Kim,

Gutter and Spangler, 2017).

Finance Department: A finance Department/unit in an entity is characterised as component

of an entity which is accountable for obtaining funding for the enterprise, administering funds

inside the organisation and scheduling the spending of funding on different asset classes. It is

component of an entity which facilitates the effective financial reporting and fiscal surveillance

requisite to finance all operational processes. The input of finance department/unit of every

Financial decision-making within business context may be explained as the processes/set of

activities attributable to devising financial decisions for an entity by considering annual reports,

interim financial reports and business's other financial reports. It is extremely important for all

business to ensure that their accounting-personnel are concentrating on productive business

decisions because it will enable the fulfilment of all longer-term and shorter-term organizational

goals. The principal aim of this project is to strengthen the comprehension of the essential

aspects that all enterprises need to consider for formulate efficient financial decisions (Black,

2019). The current study is centred on the SKANSA PLC i.e. construction corporation

incorporated in 1984. Company is UK based and operating its business in multiple nations. This

report discusses multiple points regarding value of the accounting and finance tasks,

responsibilities and obligations within corporation.

MAIN BODY

TASK 1

Accounting and Finance Department:

Accounting Department: An accounting department is particular division/unit

within firm/business enterprise that is accountable for tracking and monitoring cash ins or

out flows of organisation. The accounting division is accountable for a vast variety

of accounting as well as tasks within the enterprise. This department not only responsible for

recording and reporting of financial reports but also formulate processes and policies for

controlling flow of funds within entity as well as safeguards financial resources. It is component

of administration of organization liable for filing the annual statements, managing the corporate

accounts, collecting bills, billing buyers, payrolls, expense monitoring, financial reporting, and

much more. The top of accounting department also carries the designation of controller (Kim,

Gutter and Spangler, 2017).

Finance Department: A finance Department/unit in an entity is characterised as component

of an entity which is accountable for obtaining funding for the enterprise, administering funds

inside the organisation and scheduling the spending of funding on different asset classes. It is

component of an entity which facilitates the effective financial reporting and fiscal surveillance

requisite to finance all operational processes. The input of finance department/unit of every

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enterprise including how these inputs have a significant influence on corporate results would rely

heavily on considerations like the level to which owner/manager is engaged with the corporation.

Importance of Accounting and Finance Department:

Accounting Department: The everyday bookkeeping and preparing of financial records is

the responsibility of accounting staff. To take higher decisions regarding financial strategy,

one first need to determine where the business is based. Everyday record keeping involves

billing and salaries, and production of financial reporting involves synthesising and finalising

these details in budget statements, annual fiscal statements and cash-flows accounts at routine

periods, normally annually. Accounting department/unit is liable for tracking and

reporting company's cash flow activities. This unit has a range of core functions and duties,

including trade receivables, current liabilities, accounting, financial statements and the

management of financial standards (Elbayoumi, Awadallah and Basuony, 2019).

Finance Department: This is amongst the most critical of all company operations. Finance

department performs a pivotal function in the organisation. Correspondingly, finance department

of the company must provide all other divisions (operations) with the requisite funds to carrying

out their operations. The finance division is accountable for maintaining this routine so that the

business does not really run-out of funds to cover its bills, nor does it cost too high for finance

costs. Financial departments can also use existing records and analyses to forecast the

corporation's progress and future developments. Finance Team designs growth projections and

plans, handles and minimises costs, aims for opportunities to raise resources, oversees budgets

and funding options, and links with stakeholders. A sensible finance team has complete image of

the corporation 's activities and understands how each feature and task impacts the corporation 's

overall financial situation.

Role of Accounts Department

o Financial accounting: Financial accounting is primary feature/role of accounting

department which includes the task of monitoring, summing up and publishing a range of

transactions arising from company activities over a length of term. Such transactions are outlined

in the preparing of financial reports/accounts, along with balance sheet, profit/loss statement

and cash-flows statement, which document the organization's business 's financial results

for given duration. Financial accounting functions should provide financial reports in a way that

enables the interpretation of corporate results (Klačmer Čalopa, 2017). Company owner, can

heavily on considerations like the level to which owner/manager is engaged with the corporation.

Importance of Accounting and Finance Department:

Accounting Department: The everyday bookkeeping and preparing of financial records is

the responsibility of accounting staff. To take higher decisions regarding financial strategy,

one first need to determine where the business is based. Everyday record keeping involves

billing and salaries, and production of financial reporting involves synthesising and finalising

these details in budget statements, annual fiscal statements and cash-flows accounts at routine

periods, normally annually. Accounting department/unit is liable for tracking and

reporting company's cash flow activities. This unit has a range of core functions and duties,

including trade receivables, current liabilities, accounting, financial statements and the

management of financial standards (Elbayoumi, Awadallah and Basuony, 2019).

Finance Department: This is amongst the most critical of all company operations. Finance

department performs a pivotal function in the organisation. Correspondingly, finance department

of the company must provide all other divisions (operations) with the requisite funds to carrying

out their operations. The finance division is accountable for maintaining this routine so that the

business does not really run-out of funds to cover its bills, nor does it cost too high for finance

costs. Financial departments can also use existing records and analyses to forecast the

corporation's progress and future developments. Finance Team designs growth projections and

plans, handles and minimises costs, aims for opportunities to raise resources, oversees budgets

and funding options, and links with stakeholders. A sensible finance team has complete image of

the corporation 's activities and understands how each feature and task impacts the corporation 's

overall financial situation.

Role of Accounts Department

o Financial accounting: Financial accounting is primary feature/role of accounting

department which includes the task of monitoring, summing up and publishing a range of

transactions arising from company activities over a length of term. Such transactions are outlined

in the preparing of financial reports/accounts, along with balance sheet, profit/loss statement

and cash-flows statement, which document the organization's business 's financial results

for given duration. Financial accounting functions should provide financial reports in a way that

enables the interpretation of corporate results (Klačmer Čalopa, 2017). Company owner, can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

apply financial accounting functions of accounting department to build ratio analytics and use

these ratios to do a more thorough review of the different facets of your business. With this

functions business may calculate the cash condition of your company or evaluate their earnings

or revenue ratio and equate it with their previous results or performance of their rivals. Financial

accounting allows them to formulate their potential course of operation or policy and to assess

the progress of this approach using financial reports from another time.

o Management accounting: Management accounting and related processes are also another

important task for accounting department that includes planning and presenting timely finance

and analytical reports to corporate owners such that they could undertake daily as well as

shorter-term managerial decisions. Accounting management inputs into costs and availability of

supply are important considerations in buying decisions. Information from management

accounting functions empowers decision-making at either an organisational and a tactical stage.

o Tax function: These functions of accounting department comprises ensuring timely

payments of taxes and duties to avoid any penalties. These functions also involve calculation of

taxes (including direct and indirect taxes), filing of tax returns, assessment of advance tax and

other key tax related functions. The duties of taxation are manifestation of their essentially; they

are way of reflecting the features of taxation. The duties of taxes reflect the social intent of the

allocation and allocation of income on basis of value. Each work performed by tax instruments is

a representation of internal attribute, predictor or characteristic, or of that economic class (James,

2019).

o Auditing function: The audit role of business's accounting department consists of

unbiased and impartial consulting procedures intended to bring value to company and enhance

the activity of the organisation. It offers a comprehensive and structured framework to

risks management evaluation and assessment, performance monitoring and regulatory

compliance. Auditing operations are typically based on three main fields, not all of which are

restricted to, internal monitoring over financial statements, time worth of capital, and

enforcement evaluation.

Role of Finance Department:

o Investment function: In ordinary terms, the investment functions within an entity of the

finance department involve the acquisition of shares, options, bonds and assets that already trade

on the capital exchange. Yet that's not true investment, precisely since it is a redistribution of

these ratios to do a more thorough review of the different facets of your business. With this

functions business may calculate the cash condition of your company or evaluate their earnings

or revenue ratio and equate it with their previous results or performance of their rivals. Financial

accounting allows them to formulate their potential course of operation or policy and to assess

the progress of this approach using financial reports from another time.

o Management accounting: Management accounting and related processes are also another

important task for accounting department that includes planning and presenting timely finance

and analytical reports to corporate owners such that they could undertake daily as well as

shorter-term managerial decisions. Accounting management inputs into costs and availability of

supply are important considerations in buying decisions. Information from management

accounting functions empowers decision-making at either an organisational and a tactical stage.

o Tax function: These functions of accounting department comprises ensuring timely

payments of taxes and duties to avoid any penalties. These functions also involve calculation of

taxes (including direct and indirect taxes), filing of tax returns, assessment of advance tax and

other key tax related functions. The duties of taxation are manifestation of their essentially; they

are way of reflecting the features of taxation. The duties of taxes reflect the social intent of the

allocation and allocation of income on basis of value. Each work performed by tax instruments is

a representation of internal attribute, predictor or characteristic, or of that economic class (James,

2019).

o Auditing function: The audit role of business's accounting department consists of

unbiased and impartial consulting procedures intended to bring value to company and enhance

the activity of the organisation. It offers a comprehensive and structured framework to

risks management evaluation and assessment, performance monitoring and regulatory

compliance. Auditing operations are typically based on three main fields, not all of which are

restricted to, internal monitoring over financial statements, time worth of capital, and

enforcement evaluation.

Role of Finance Department:

o Investment function: In ordinary terms, the investment functions within an entity of the

finance department involve the acquisition of shares, options, bonds and assets that already trade

on the capital exchange. Yet that's not true investment, precisely since it is a redistribution of

current properties. This is also considered capital investment, and does not impact net

expenditure. Investment roles also involve the procurement of new plants and machinery,

development of public projects such as bridges, bridges, buildings etc., total foreign direct

investment, inventory levels and stocks, investments in new businesses (Eberhardt, de Bruin and

Strough, 2019).

o Financing function: The financial function of entity's finance department could clearly be

seen as the job of supplying the finances required by the company on favorable terms, taking into

account the goals of the business. This implies that the funding role is associated exclusively

with the purchase (or sourcing) of shorter-term and longer-term resources. The financial role can

clearly be seen as the job of supplying the funds required by an organization on reasonable

terms, taking into account the goals of the business. This suggests that the funding role is

connected exclusively with the purchase (or sourcing) of shorter-term and longer-term finances.

o Dividend function: A finance department which determines how much of profits received

by the business should be allocated among investors (dividends) including how much can be

preserved for potential contingency plans (internal funds) are regarded as dividend functions.

Dividend applies to the portion of the earnings that is paid to the owners. The

decisions on dividend should be made in the light of the ultimate goal of optimising shareholder

capital. The preferences of shareholders are often taken into consideration when agreeing on a

dividend. Within event that the shareholder wants to obtain a dividend, company will continue to

declare same. In this case, the size of the dividend relies on the extent of aspirations of the

owners. such all the tasks are carried out by finance department (Kaur and Lodhia, 2019).

o Working capital function: Working capital corresponds to funds used to fund all shorter-

term costs of a corporation, comprising stock, shorter-term loan payments, and daily expenses—

called running expenditures. Working capital functions important role of finance department as

this is used to ensure that a company runs efficiently and meets all its financial/debt obligations

in coming period. Finance department track their trade receivables to decide whether they're

scheduled to collect payment from their clients. On other hand, businesses often track their

accounts payables/creditor to assess the days about which transactions are owed to vendors.

If accounts payables are overdue earlier than money due from accounts receivables, the business

will suffer a deficit in the working capital.

expenditure. Investment roles also involve the procurement of new plants and machinery,

development of public projects such as bridges, bridges, buildings etc., total foreign direct

investment, inventory levels and stocks, investments in new businesses (Eberhardt, de Bruin and

Strough, 2019).

o Financing function: The financial function of entity's finance department could clearly be

seen as the job of supplying the finances required by the company on favorable terms, taking into

account the goals of the business. This implies that the funding role is associated exclusively

with the purchase (or sourcing) of shorter-term and longer-term resources. The financial role can

clearly be seen as the job of supplying the funds required by an organization on reasonable

terms, taking into account the goals of the business. This suggests that the funding role is

connected exclusively with the purchase (or sourcing) of shorter-term and longer-term finances.

o Dividend function: A finance department which determines how much of profits received

by the business should be allocated among investors (dividends) including how much can be

preserved for potential contingency plans (internal funds) are regarded as dividend functions.

Dividend applies to the portion of the earnings that is paid to the owners. The

decisions on dividend should be made in the light of the ultimate goal of optimising shareholder

capital. The preferences of shareholders are often taken into consideration when agreeing on a

dividend. Within event that the shareholder wants to obtain a dividend, company will continue to

declare same. In this case, the size of the dividend relies on the extent of aspirations of the

owners. such all the tasks are carried out by finance department (Kaur and Lodhia, 2019).

o Working capital function: Working capital corresponds to funds used to fund all shorter-

term costs of a corporation, comprising stock, shorter-term loan payments, and daily expenses—

called running expenditures. Working capital functions important role of finance department as

this is used to ensure that a company runs efficiently and meets all its financial/debt obligations

in coming period. Finance department track their trade receivables to decide whether they're

scheduled to collect payment from their clients. On other hand, businesses often track their

accounts payables/creditor to assess the days about which transactions are owed to vendors.

If accounts payables are overdue earlier than money due from accounts receivables, the business

will suffer a deficit in the working capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

a. Calculation of of ratios for the company

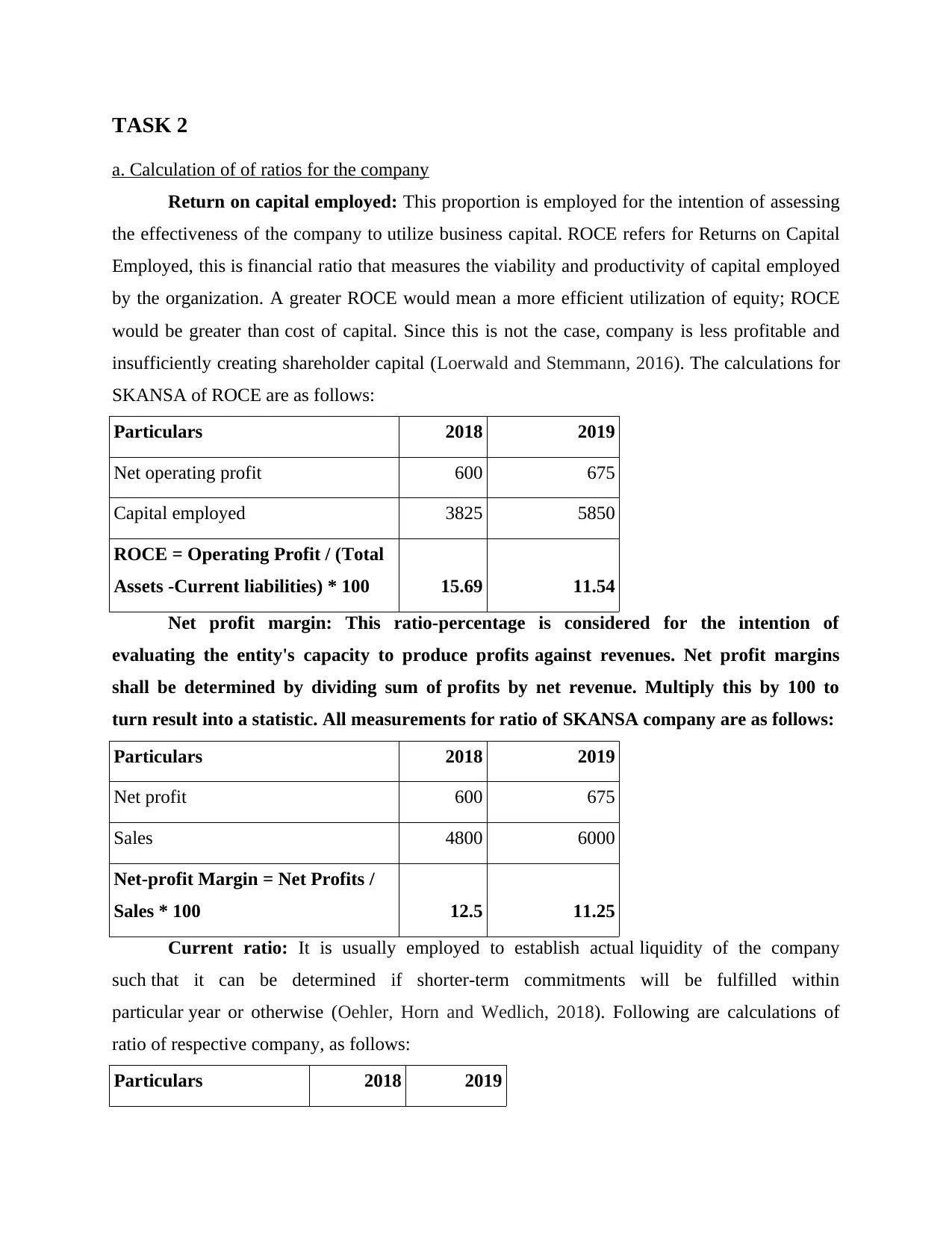

Return on capital employed: This proportion is employed for the intention of assessing

the effectiveness of the company to utilize business capital. ROCE refers for Returns on Capital

Employed, this is financial ratio that measures the viability and productivity of capital employed

by the organization. A greater ROCE would mean a more efficient utilization of equity; ROCE

would be greater than cost of capital. Since this is not the case, company is less profitable and

insufficiently creating shareholder capital (Loerwald and Stemmann, 2016). The calculations for

SKANSA of ROCE are as follows:

Particulars 2018 2019

Net operating profit 600 675

Capital employed 3825 5850

ROCE = Operating Profit / (Total

Assets -Current liabilities) * 100 15.69 11.54

Net profit margin: This ratio-percentage is considered for the intention of

evaluating the entity's capacity to produce profits against revenues. Net profit margins

shall be determined by dividing sum of profits by net revenue. Multiply this by 100 to

turn result into a statistic. All measurements for ratio of SKANSA company are as follows:

Particulars 2018 2019

Net profit 600 675

Sales 4800 6000

Net-profit Margin = Net Profits /

Sales * 100 12.5 11.25

Current ratio: It is usually employed to establish actual liquidity of the company

such that it can be determined if shorter-term commitments will be fulfilled within

particular year or otherwise (Oehler, Horn and Wedlich, 2018). Following are calculations of

ratio of respective company, as follows:

Particulars 2018 2019

a. Calculation of of ratios for the company

Return on capital employed: This proportion is employed for the intention of assessing

the effectiveness of the company to utilize business capital. ROCE refers for Returns on Capital

Employed, this is financial ratio that measures the viability and productivity of capital employed

by the organization. A greater ROCE would mean a more efficient utilization of equity; ROCE

would be greater than cost of capital. Since this is not the case, company is less profitable and

insufficiently creating shareholder capital (Loerwald and Stemmann, 2016). The calculations for

SKANSA of ROCE are as follows:

Particulars 2018 2019

Net operating profit 600 675

Capital employed 3825 5850

ROCE = Operating Profit / (Total

Assets -Current liabilities) * 100 15.69 11.54

Net profit margin: This ratio-percentage is considered for the intention of

evaluating the entity's capacity to produce profits against revenues. Net profit margins

shall be determined by dividing sum of profits by net revenue. Multiply this by 100 to

turn result into a statistic. All measurements for ratio of SKANSA company are as follows:

Particulars 2018 2019

Net profit 600 675

Sales 4800 6000

Net-profit Margin = Net Profits /

Sales * 100 12.5 11.25

Current ratio: It is usually employed to establish actual liquidity of the company

such that it can be determined if shorter-term commitments will be fulfilled within

particular year or otherwise (Oehler, Horn and Wedlich, 2018). Following are calculations of

ratio of respective company, as follows:

Particulars 2018 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current assets 1515 2070

Current liabilities 645 2220

Current Ratio =

Current Assets /

Current Liabilities 2.35 0.93

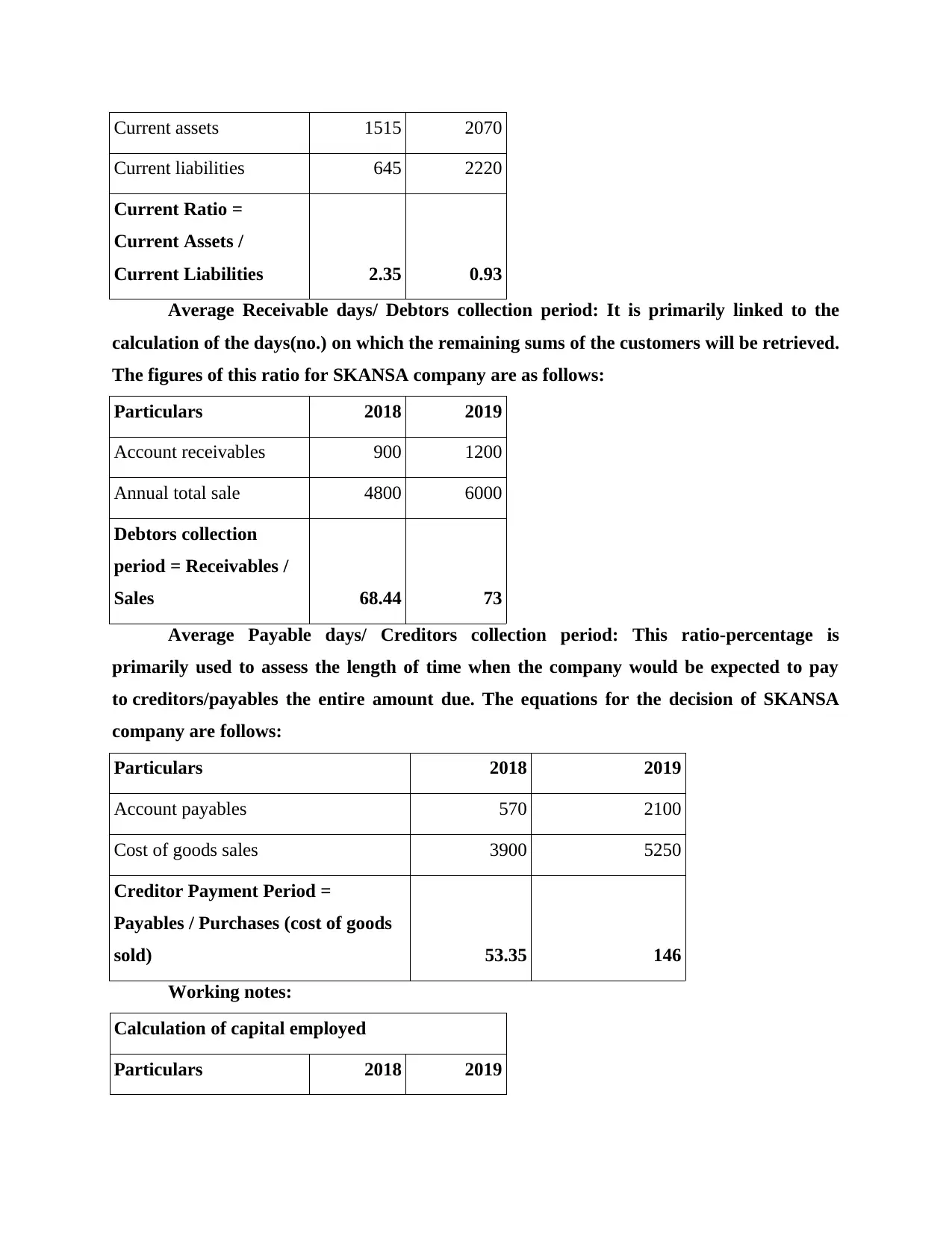

Average Receivable days/ Debtors collection period: It is primarily linked to the

calculation of the days(no.) on which the remaining sums of the customers will be retrieved.

The figures of this ratio for SKANSA company are as follows:

Particulars 2018 2019

Account receivables 900 1200

Annual total sale 4800 6000

Debtors collection

period = Receivables /

Sales 68.44 73

Average Payable days/ Creditors collection period: This ratio-percentage is

primarily used to assess the length of time when the company would be expected to pay

to creditors/payables the entire amount due. The equations for the decision of SKANSA

company are follows:

Particulars 2018 2019

Account payables 570 2100

Cost of goods sales 3900 5250

Creditor Payment Period =

Payables / Purchases (cost of goods

sold) 53.35 146

Working notes:

Calculation of capital employed

Particulars 2018 2019

Current liabilities 645 2220

Current Ratio =

Current Assets /

Current Liabilities 2.35 0.93

Average Receivable days/ Debtors collection period: It is primarily linked to the

calculation of the days(no.) on which the remaining sums of the customers will be retrieved.

The figures of this ratio for SKANSA company are as follows:

Particulars 2018 2019

Account receivables 900 1200

Annual total sale 4800 6000

Debtors collection

period = Receivables /

Sales 68.44 73

Average Payable days/ Creditors collection period: This ratio-percentage is

primarily used to assess the length of time when the company would be expected to pay

to creditors/payables the entire amount due. The equations for the decision of SKANSA

company are follows:

Particulars 2018 2019

Account payables 570 2100

Cost of goods sales 3900 5250

Creditor Payment Period =

Payables / Purchases (cost of goods

sold) 53.35 146

Working notes:

Calculation of capital employed

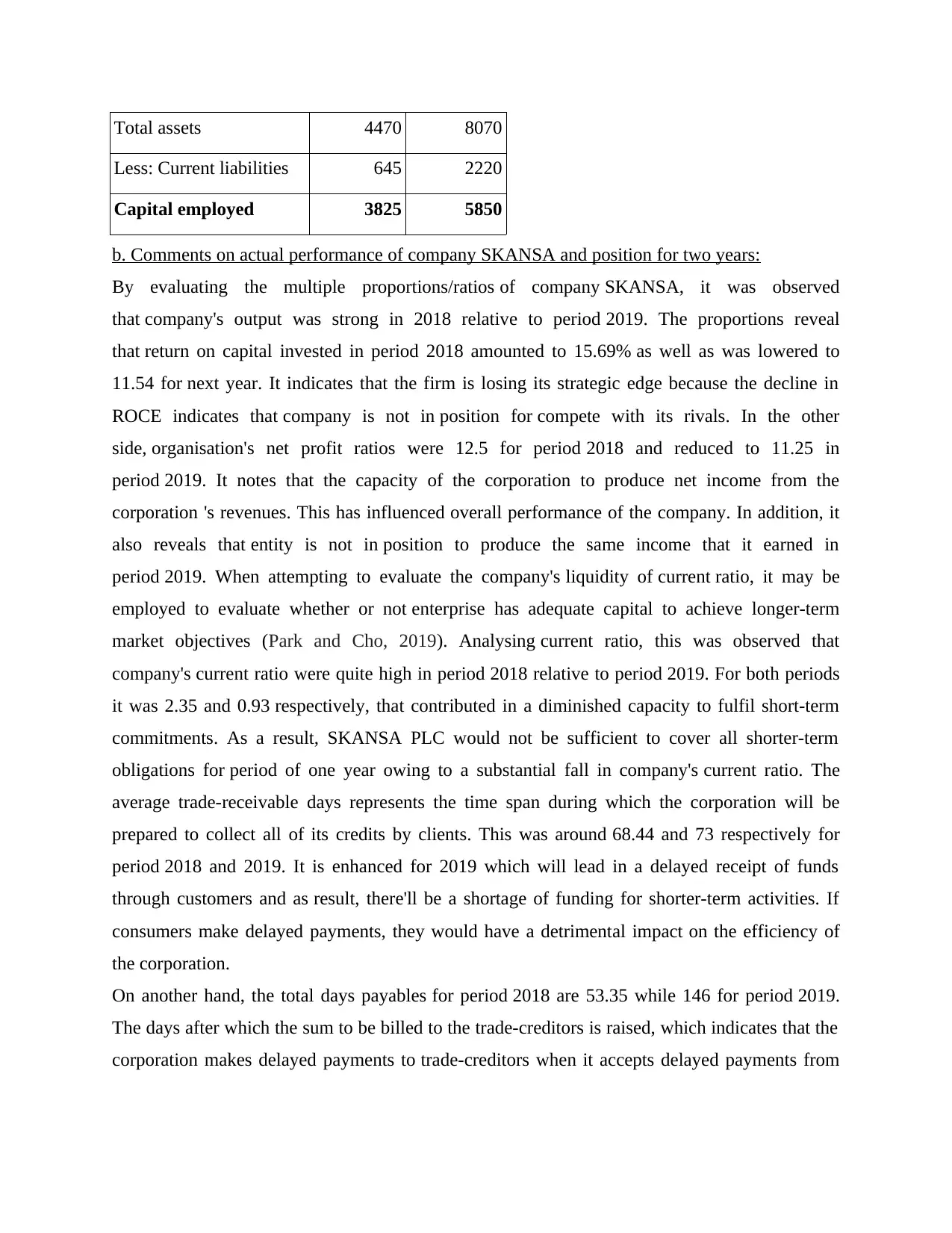

Particulars 2018 2019

Total assets 4470 8070

Less: Current liabilities 645 2220

Capital employed 3825 5850

b. Comments on actual performance of company SKANSA and position for two years:

By evaluating the multiple proportions/ratios of company SKANSA, it was observed

that company's output was strong in 2018 relative to period 2019. The proportions reveal

that return on capital invested in period 2018 amounted to 15.69% as well as was lowered to

11.54 for next year. It indicates that the firm is losing its strategic edge because the decline in

ROCE indicates that company is not in position for compete with its rivals. In the other

side, organisation's net profit ratios were 12.5 for period 2018 and reduced to 11.25 in

period 2019. It notes that the capacity of the corporation to produce net income from the

corporation 's revenues. This has influenced overall performance of the company. In addition, it

also reveals that entity is not in position to produce the same income that it earned in

period 2019. When attempting to evaluate the company's liquidity of current ratio, it may be

employed to evaluate whether or not enterprise has adequate capital to achieve longer-term

market objectives (Park and Cho, 2019). Analysing current ratio, this was observed that

company's current ratio were quite high in period 2018 relative to period 2019. For both periods

it was 2.35 and 0.93 respectively, that contributed in a diminished capacity to fulfil short-term

commitments. As a result, SKANSA PLC would not be sufficient to cover all shorter-term

obligations for period of one year owing to a substantial fall in company's current ratio. The

average trade-receivable days represents the time span during which the corporation will be

prepared to collect all of its credits by clients. This was around 68.44 and 73 respectively for

period 2018 and 2019. It is enhanced for 2019 which will lead in a delayed receipt of funds

through customers and as result, there'll be a shortage of funding for shorter-term activities. If

consumers make delayed payments, they would have a detrimental impact on the efficiency of

the corporation.

On another hand, the total days payables for period 2018 are 53.35 while 146 for period 2019.

The days after which the sum to be billed to the trade-creditors is raised, which indicates that the

corporation makes delayed payments to trade-creditors when it accepts delayed payments from

Less: Current liabilities 645 2220

Capital employed 3825 5850

b. Comments on actual performance of company SKANSA and position for two years:

By evaluating the multiple proportions/ratios of company SKANSA, it was observed

that company's output was strong in 2018 relative to period 2019. The proportions reveal

that return on capital invested in period 2018 amounted to 15.69% as well as was lowered to

11.54 for next year. It indicates that the firm is losing its strategic edge because the decline in

ROCE indicates that company is not in position for compete with its rivals. In the other

side, organisation's net profit ratios were 12.5 for period 2018 and reduced to 11.25 in

period 2019. It notes that the capacity of the corporation to produce net income from the

corporation 's revenues. This has influenced overall performance of the company. In addition, it

also reveals that entity is not in position to produce the same income that it earned in

period 2019. When attempting to evaluate the company's liquidity of current ratio, it may be

employed to evaluate whether or not enterprise has adequate capital to achieve longer-term

market objectives (Park and Cho, 2019). Analysing current ratio, this was observed that

company's current ratio were quite high in period 2018 relative to period 2019. For both periods

it was 2.35 and 0.93 respectively, that contributed in a diminished capacity to fulfil short-term

commitments. As a result, SKANSA PLC would not be sufficient to cover all shorter-term

obligations for period of one year owing to a substantial fall in company's current ratio. The

average trade-receivable days represents the time span during which the corporation will be

prepared to collect all of its credits by clients. This was around 68.44 and 73 respectively for

period 2018 and 2019. It is enhanced for 2019 which will lead in a delayed receipt of funds

through customers and as result, there'll be a shortage of funding for shorter-term activities. If

consumers make delayed payments, they would have a detrimental impact on the efficiency of

the corporation.

On another hand, the total days payables for period 2018 are 53.35 while 146 for period 2019.

The days after which the sum to be billed to the trade-creditors is raised, which indicates that the

corporation makes delayed payments to trade-creditors when it accepts delayed payments from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

its customers. Due to the improvement in this proportion, the company will face problems in the

future, as creditors will fail to extend credits to the organisation in the long term.

Potential explanations, factors and results of ratio variations:

• The ROCE of corporation is lowered due to an expansion in overall capital engaged for the

period 2019. This is the primary source and trigger of the decline. Its key consequence on the

firm would be to reduce its capacity to re earnings in the corporation.

• Net profit margins of company SKANSA is lowered due to higher revenues and profits. The

rise in earnings was very poor relative to the increase in revenue which resulting in a decline in

the corporation's net profit ratio level. The biggest impact on the organization was a decline in

earnings for year 2019. As result, the corporation would not be sufficient to fulfil any of its

commitments because of a drop in revenues.

• The decrease in company's current ratio is quite higher and the key explanation for this is a

spike in the total current liabilities, that amounted to 645 in year-2018 and rose to year-2220.

Current assets have also raised, but value of the rise was lower relative to current obligations. As

a consequence of this decline in company's current ratio, company was impaired by the decline

in its willingness to fulfil all shorter-term obligations (Sapkauskiene and Orlovskij, 2017).

• The average trade-receivable days of corporation SKANKA PLC was lowered for 2018 as well

as the key explanation for this reduction is higher gross net revenue and elevated receivables.

This would have an effect on the corporation's existing assets as customers render late payments

to company, which would result in a loss of funds for business operations.

• The total trade-payable days of company are enhanced, which ensures that the corporation

makes overdue payments for all credits it gets. The key explanation for this is the rise in costs of

goods sold as-well-as increase in payables for the year. As a consequence, the brand reputation

could have an effect which would also lead to creditors' reluctance to extend credits to the

organization.

From the aforementioned discussion, this can be interpreted that overall performance

of given company SKANSA PLC was strong in year-2018 and that the company is experiencing

challenges due to improvements in ratios in year-2019. When most of ratios-assessed are

reduced, there is a detrimental effect on the efficiency of the enterprise. In addition, the company

is also faced with the problem of diminished financing for operating operations as its viability

and liquidity drop. As a result of this cut, the company is not in a position to carry out the

future, as creditors will fail to extend credits to the organisation in the long term.

Potential explanations, factors and results of ratio variations:

• The ROCE of corporation is lowered due to an expansion in overall capital engaged for the

period 2019. This is the primary source and trigger of the decline. Its key consequence on the

firm would be to reduce its capacity to re earnings in the corporation.

• Net profit margins of company SKANSA is lowered due to higher revenues and profits. The

rise in earnings was very poor relative to the increase in revenue which resulting in a decline in

the corporation's net profit ratio level. The biggest impact on the organization was a decline in

earnings for year 2019. As result, the corporation would not be sufficient to fulfil any of its

commitments because of a drop in revenues.

• The decrease in company's current ratio is quite higher and the key explanation for this is a

spike in the total current liabilities, that amounted to 645 in year-2018 and rose to year-2220.

Current assets have also raised, but value of the rise was lower relative to current obligations. As

a consequence of this decline in company's current ratio, company was impaired by the decline

in its willingness to fulfil all shorter-term obligations (Sapkauskiene and Orlovskij, 2017).

• The average trade-receivable days of corporation SKANKA PLC was lowered for 2018 as well

as the key explanation for this reduction is higher gross net revenue and elevated receivables.

This would have an effect on the corporation's existing assets as customers render late payments

to company, which would result in a loss of funds for business operations.

• The total trade-payable days of company are enhanced, which ensures that the corporation

makes overdue payments for all credits it gets. The key explanation for this is the rise in costs of

goods sold as-well-as increase in payables for the year. As a consequence, the brand reputation

could have an effect which would also lead to creditors' reluctance to extend credits to the

organization.

From the aforementioned discussion, this can be interpreted that overall performance

of given company SKANSA PLC was strong in year-2018 and that the company is experiencing

challenges due to improvements in ratios in year-2019. When most of ratios-assessed are

reduced, there is a detrimental effect on the efficiency of the enterprise. In addition, the company

is also faced with the problem of diminished financing for operating operations as its viability

and liquidity drop. As a result of this cut, the company is not in a position to carry out the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activities adequately. The financial situation of the corporation is quite bad in 2019 relative to

2018, since there are significant variations in the organization's ratios due to various reasons.

That include higher sales expenses, Trade payable, profits, current assets etc.

CONCLUSION

It has been inferred from the aforementioned project study that the financial decision-

making is core factor that must be concentrated on by every organizations as it promotes the

implementation of both long-term and shorter-term projects. Both accountings and finance tasks,

responsibilities and responsibilities are quite relevant to all companies, since they can contribute

in the successful implementation of all operating activities. When preparing to evaluate the

financial condition of the firm, it would be quite essential for organisations to utilize the study of

the proportion. The various measures that may be used to assess the financial condition of the

firm include the return on capital-engaged or invested, the net profits margin, the current ratio,

the total receivables collection and the payable duration.

2018, since there are significant variations in the organization's ratios due to various reasons.

That include higher sales expenses, Trade payable, profits, current assets etc.

CONCLUSION

It has been inferred from the aforementioned project study that the financial decision-

making is core factor that must be concentrated on by every organizations as it promotes the

implementation of both long-term and shorter-term projects. Both accountings and finance tasks,

responsibilities and responsibilities are quite relevant to all companies, since they can contribute

in the successful implementation of all operating activities. When preparing to evaluate the

financial condition of the firm, it would be quite essential for organisations to utilize the study of

the proportion. The various measures that may be used to assess the financial condition of the

firm include the return on capital-engaged or invested, the net profits margin, the current ratio,

the total receivables collection and the payable duration.

REFERENCES

Books and Journals:

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Kim, J., Gutter, M.S. and Spangler, T., 2017. Review of family financial decision making:

Suggestions for future research and implications for financial education. Journal of

Financial Counseling and Planning, 28(2), pp.253-267.

Elbayoumi, A. F., Awadallah, E. A. and Basuony, M. A., 2019. Development of accounting and

auditing in Egypt: Origin, growth, practice and influential factors. The Journal of

Developing Areas. 53(2).

Klačmer Čalopa, M., 2017. Business owner and manager’s attitudes towards financial decision-

making and strategic planning: Evidence from Croatian SMEs. Management: journal of

contemporary management issues, 22(1), pp.103-116.

James, H. L., 2019. Connecting policy with the personal: UK pension reforms and individual

financial decision making. The University of Manchester (United Kingdom).

Eberhardt, W., de Bruin, W.B. and Strough, J., 2019. Age differences in financial decision

making: The benefits of more experience and less negative emotions. Journal of

Behavioral Decision Making, 32(1), pp.79-93.

Kaur, A. and Lodhia, S. K., 2019. Key issues and challenges in stakeholder engagement in

sustainability reporting. Pacific Accounting Review.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International handbook of

financial literacy (pp. 25-38). Springer, Singapore.

Oehler, A., Horn, M. and Wedlich, F., 2018. Young adults’ subjective and objective risk attitude

in financial decision making. Review of Behavioral Finance.

Park, I. and Cho, S., 2019. The influence of number line estimation precision and numeracy on

risky financial decision making. International Journal of Psychology. 54(4). pp.530-

538.

Sapkauskiene, A. and Orlovskij, S., 2017. The usefulness of fair value estimates for financial

decision making–a literature review. Zeszyty Teoretyczne Rachunkowości, (93 (149)),

pp.163-173.

Books and Journals:

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Kim, J., Gutter, M.S. and Spangler, T., 2017. Review of family financial decision making:

Suggestions for future research and implications for financial education. Journal of

Financial Counseling and Planning, 28(2), pp.253-267.

Elbayoumi, A. F., Awadallah, E. A. and Basuony, M. A., 2019. Development of accounting and

auditing in Egypt: Origin, growth, practice and influential factors. The Journal of

Developing Areas. 53(2).

Klačmer Čalopa, M., 2017. Business owner and manager’s attitudes towards financial decision-

making and strategic planning: Evidence from Croatian SMEs. Management: journal of

contemporary management issues, 22(1), pp.103-116.

James, H. L., 2019. Connecting policy with the personal: UK pension reforms and individual

financial decision making. The University of Manchester (United Kingdom).

Eberhardt, W., de Bruin, W.B. and Strough, J., 2019. Age differences in financial decision

making: The benefits of more experience and less negative emotions. Journal of

Behavioral Decision Making, 32(1), pp.79-93.

Kaur, A. and Lodhia, S. K., 2019. Key issues and challenges in stakeholder engagement in

sustainability reporting. Pacific Accounting Review.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International handbook of

financial literacy (pp. 25-38). Springer, Singapore.

Oehler, A., Horn, M. and Wedlich, F., 2018. Young adults’ subjective and objective risk attitude

in financial decision making. Review of Behavioral Finance.

Park, I. and Cho, S., 2019. The influence of number line estimation precision and numeracy on

risky financial decision making. International Journal of Psychology. 54(4). pp.530-

538.

Sapkauskiene, A. and Orlovskij, S., 2017. The usefulness of fair value estimates for financial

decision making–a literature review. Zeszyty Teoretyczne Rachunkowości, (93 (149)),

pp.163-173.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.