Financial Decision Making Report: SKANSA PLC Financial Analysis

VerifiedAdded on 2023/01/04

|12

|3685

|81

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making within SKANSA PLC. It begins with an introduction to financial decision-making and its importance for effective business investment. The report then explores the critical roles and functions of accounting and finance within the company, including financial planning, managerial accounting, financial accounting, and revenue management. A significant portion of the report is dedicated to the calculation and interpretation of key financial ratios, such as Return on Capital Employed (ROCE), to assess SKANSA PLC's financial performance. The report examines the company's performance in 2018 and 2019, offering insights into its profitability and efficiency. The report also covers aspects like investment valuation, budgeting, and fraud prevention, highlighting their significance in sound financial management. The conclusion summarizes the key findings and reinforces the importance of effective financial decision-making for the success of SKANSA PLC.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:.............3

TASK 2............................................................................................................................................7

Calculation of ratios for the company and comment on performance of company.....................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:.............3

TASK 2............................................................................................................................................7

Calculation of ratios for the company and comment on performance of company.....................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial decision-making refers to a collection of actions or a process for determining the

benefits and disadvantages of actions in relation to the use of resources. The main purpose of this

latest study is to illustrate all the important factors that need to be taken into account by all

companies in an effort to make effective business investment decisions (Agarwal and Mazumder,

2013). Business decision provides help to maximise the financial capital needed to meet the

company's priorities before a sufficient level of corporate financial success is reached. It provides

both a practical and philosophical framework for the financial judgement phase. Advertising,

acquisitions, distributions and control of net-working capital are the core facets of all business

decision. The current thesis is focused primarily on SKANSA PLC, who was founded in 1984 as

a UK-based building company. The research report covers a detailed assessment of the financial

plan of the company using accounting ratios.

TASK 1

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:

In order to accomplish organisational purposes, accounting and funding all these principles play

an overall primary function for the organisation that is used to operate in a way. The manner in

which a company's financial results are recognised, acquired, classified and published is known

to be finance that is necessary for making the required strategic decisions (Lusardi, 2012). The

financial activities and the details that provide the necessary details and to monitor the activities

must be analysed by every company. In the case of SKANSKA PLC, the main roles of both

corporate finance are being used by the management to track their business by measuring both

company-relevant revenues and expenditures to increase performance.

Financial planning: This is defined as the main business feature for the financial management

and preparing of the company and also creating expenditures with the aid of this. In the

SKANSKA business, managers are responsible for executing the financial management system

by understanding both business and audit activities.

Managerial Accounting: Which is the method of audit formulation, accounting and financial

process control and company reports collection. These tasks are carried out by the SKANSKA

government to help effective management decisions through the collection of monetary and

essential documents.

Financial decision-making refers to a collection of actions or a process for determining the

benefits and disadvantages of actions in relation to the use of resources. The main purpose of this

latest study is to illustrate all the important factors that need to be taken into account by all

companies in an effort to make effective business investment decisions (Agarwal and Mazumder,

2013). Business decision provides help to maximise the financial capital needed to meet the

company's priorities before a sufficient level of corporate financial success is reached. It provides

both a practical and philosophical framework for the financial judgement phase. Advertising,

acquisitions, distributions and control of net-working capital are the core facets of all business

decision. The current thesis is focused primarily on SKANSA PLC, who was founded in 1984 as

a UK-based building company. The research report covers a detailed assessment of the financial

plan of the company using accounting ratios.

TASK 1

Importance of Accounting and Finance functions, duties and roles in SKANSA PLC:

In order to accomplish organisational purposes, accounting and funding all these principles play

an overall primary function for the organisation that is used to operate in a way. The manner in

which a company's financial results are recognised, acquired, classified and published is known

to be finance that is necessary for making the required strategic decisions (Lusardi, 2012). The

financial activities and the details that provide the necessary details and to monitor the activities

must be analysed by every company. In the case of SKANSKA PLC, the main roles of both

corporate finance are being used by the management to track their business by measuring both

company-relevant revenues and expenditures to increase performance.

Financial planning: This is defined as the main business feature for the financial management

and preparing of the company and also creating expenditures with the aid of this. In the

SKANSKA business, managers are responsible for executing the financial management system

by understanding both business and audit activities.

Managerial Accounting: Which is the method of audit formulation, accounting and financial

process control and company reports collection. These tasks are carried out by the SKANSKA

government to help effective management decisions through the collection of monetary and

essential documents.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting: it involves the keeping of accounting documents on all payments, use of

the dual accounting information system and the preparing of final reports which are necessary for

regulatory reporting, brokerage firm and regulatory agencies to meet the different governmental

requirements.

Supporting corporate policy and developing financial policies: The financial manager is

responsible for managing a financial climate that promotes financial and business planning (Nga,

and Yien, 2013). In order to accomplish the mission of the company to have the organization

performance needed to seize the opportunities, the best mix of shortened and lengthier financing

and capital tools should be made available. Both management have the primary role of producing

value, and the financial police's key points are to help them to do this.

Earnings and expense monitoring: accounting finance is a crucial feature of the organization that

wants it to track the income and losses incurred or currently generated in the company.

Classification of expenses and control of the purpose is essential for the agency. Administration

hires accounting & financial systems in the SKANSKA Organization to track profits and also

costs that lead to improving competitiveness.

Sound and productive business planning: in the organisation, finances and accounting procedures

are needed as they help to create effective strategies and techniques that can enhance the

operation of the competitive environment and meet the goals. In SKANSKA PLC, there is a

substantial need for the multiple administrative functions to be successfully executed.

Administration focuses mainly on fund management, sales, market growth, the establishment of

planned performance and stock level calculation in this sense, which helps to assess the

inventory levels.

Business utilization of resources: multiple tasks are carried out in the organisation, so

management need to employ accountant elements that help them to handle corporate assets and

assign resources to these various actions in order to accomplish the business goal. SKANSKA

PLC management use accounting & financial data to identify and distribute all available business

tools to maximise productivity with optimum resource utilization (Brahmana, Hooy and Ahmad,

2012).

Long-term priorities action plan: the organisation aims to develop and develop its activities to a

wide extent as well as to fulfil a vision. Managers are expected to formulate long-term plans in

the dual accounting information system and the preparing of final reports which are necessary for

regulatory reporting, brokerage firm and regulatory agencies to meet the different governmental

requirements.

Supporting corporate policy and developing financial policies: The financial manager is

responsible for managing a financial climate that promotes financial and business planning (Nga,

and Yien, 2013). In order to accomplish the mission of the company to have the organization

performance needed to seize the opportunities, the best mix of shortened and lengthier financing

and capital tools should be made available. Both management have the primary role of producing

value, and the financial police's key points are to help them to do this.

Earnings and expense monitoring: accounting finance is a crucial feature of the organization that

wants it to track the income and losses incurred or currently generated in the company.

Classification of expenses and control of the purpose is essential for the agency. Administration

hires accounting & financial systems in the SKANSKA Organization to track profits and also

costs that lead to improving competitiveness.

Sound and productive business planning: in the organisation, finances and accounting procedures

are needed as they help to create effective strategies and techniques that can enhance the

operation of the competitive environment and meet the goals. In SKANSKA PLC, there is a

substantial need for the multiple administrative functions to be successfully executed.

Administration focuses mainly on fund management, sales, market growth, the establishment of

planned performance and stock level calculation in this sense, which helps to assess the

inventory levels.

Business utilization of resources: multiple tasks are carried out in the organisation, so

management need to employ accountant elements that help them to handle corporate assets and

assign resources to these various actions in order to accomplish the business goal. SKANSKA

PLC management use accounting & financial data to identify and distribute all available business

tools to maximise productivity with optimum resource utilization (Brahmana, Hooy and Ahmad,

2012).

Long-term priorities action plan: the organisation aims to develop and develop its activities to a

wide extent as well as to fulfil a vision. Managers are expected to formulate long-term plans in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

order to achieve the same. But in industry, a lengthy plan may be executed by an efficient action

plan that incorporates finance and business procedures and gathers information for this purpose.

Supervisors use financial data in SKANSKA to help their task plan to meet longer-term targets.

Managing and raising finances: funds are necessary for beginning and continuing to run an

operation, so corporate administrators have to assess the adequacy of company funds to

efficiently operate business processes. In this situation, financial management are essential for

them to identify the precise need of funds, monitor the distribution of funds inside the

organisation and identify the successful sources of funds. SKANSKA's management uses

financial and accounting systems to efficiently track finances, preserve the corporation's

appropriate liquidity status, and determine the best way to collect funds when possible.

Revenue Management: This technique is a key programme for those related to money or

marketable securities implemented by the accounting department. The sales management

technique requires the amount of obligation that can be undertaken at any given time period or

length by the company (MacLean and Ziemba, 2013). In general revenue activities and

management are handled by Assistant Finance Manager or Junior Accountant, while any aspect

of FA is managed by Chief Financial Officer. As a building company to ensure that any

infrastructure project has the expected revenue volume, SKANSKA PLC must have sufficient

sales power. SKANSKA PLC will also need appropriate protocols of revenue forecasting to be

accurate and less reliant on expectations.

Method of investment valuation: this is a methodology developed by the finance and accounting

section, a very valuable marketing process. As it helps the shareholder to decide the results of the

portfolio, the investor may use the investment valuation approach to recognise the right choice

between choices. SKANSKA PLC is a very well building company that retains a significant

investment portfolio. In order to retain large shareholders and recruit new shareholders,

SKANSKA's finance and business divisions must build effective financial analysis advertising to

engage existing investment institutions and investment advisors to the sector.

Establishing Accounting Policies and Procedures Manual: the establishment of inventory

valuation that regulates all accounting and financial activities is the main duties of the finance

and business section. These measures would verify that all transactions are carried through

externally and internally through the industry. Since such strategies tend to be approved by

senior management, they are initially established by the division of accounting and finance.

plan that incorporates finance and business procedures and gathers information for this purpose.

Supervisors use financial data in SKANSKA to help their task plan to meet longer-term targets.

Managing and raising finances: funds are necessary for beginning and continuing to run an

operation, so corporate administrators have to assess the adequacy of company funds to

efficiently operate business processes. In this situation, financial management are essential for

them to identify the precise need of funds, monitor the distribution of funds inside the

organisation and identify the successful sources of funds. SKANSKA's management uses

financial and accounting systems to efficiently track finances, preserve the corporation's

appropriate liquidity status, and determine the best way to collect funds when possible.

Revenue Management: This technique is a key programme for those related to money or

marketable securities implemented by the accounting department. The sales management

technique requires the amount of obligation that can be undertaken at any given time period or

length by the company (MacLean and Ziemba, 2013). In general revenue activities and

management are handled by Assistant Finance Manager or Junior Accountant, while any aspect

of FA is managed by Chief Financial Officer. As a building company to ensure that any

infrastructure project has the expected revenue volume, SKANSKA PLC must have sufficient

sales power. SKANSKA PLC will also need appropriate protocols of revenue forecasting to be

accurate and less reliant on expectations.

Method of investment valuation: this is a methodology developed by the finance and accounting

section, a very valuable marketing process. As it helps the shareholder to decide the results of the

portfolio, the investor may use the investment valuation approach to recognise the right choice

between choices. SKANSKA PLC is a very well building company that retains a significant

investment portfolio. In order to retain large shareholders and recruit new shareholders,

SKANSKA's finance and business divisions must build effective financial analysis advertising to

engage existing investment institutions and investment advisors to the sector.

Establishing Accounting Policies and Procedures Manual: the establishment of inventory

valuation that regulates all accounting and financial activities is the main duties of the finance

and business section. These measures would verify that all transactions are carried through

externally and internally through the industry. Since such strategies tend to be approved by

senior management, they are initially established by the division of accounting and finance.

Financial reporting political choices are guidelines established by the division of corporate

finance. For SKANSKA, accounting standards are very important, as they would help the

organisation to keep track on its revenue. The most important things to note to manage include

tracking transfers, because losing track of such a single transaction would mess with the

corporation's whole financial sector.

Budgeting: This is one of the key pillars of every enterprise. This needs to be done successfully,

and the brand growth ultimately depends on how expenditures are generated efficiently. As it

keeps a comprehensive list of estimates within the business, financial planning is a key function

of the accounting & financial division (Kramer and Weber, 2012). The Financial Department

was able to review the numbers and analyse the actual condition of the business. Budgets help

clients to foresee a potential vision in such a manner that the organisation needs to be efficient

enough to work properly. For all smaller or larger businesses, finance is essential, so SKANSKA

PLC, as the well big company, needs much more financial planning to meet the demands of

market competition. SKANSKA PLC. The goals to be set, together with the rival's position, must

be calculated in compliance with current industry evaluations. Accurate forecasting is not

possible without appropriate budgeting strategies.

Eradicating fraud: Avoiding fraud and stressing transparency in all dealings is one of the main

duties of auditors within a business. For top management, it is difficult to stop fraud under their

own. For the prevention of theft, upper management depends heavily on finance and business

departments. As the finance department manages inflows and outflows, the department should be

solely responsible as higher oversight brings significant obligations. The bigger the company's

size, the higher the employees and the greater the corporation's risk of corruption. SKANSKA

PLC is an immense business, and it is much tougher for a major corporation to deal with fraud.

To help SKANSKA PLC to eliminate bribery as a whole, control and tax departments must hold

a close eye on transparency.

In order to stay an efficient business unit, the accounting & finance department of SKANSKA

PLC should accept the duties and responsibilities listed. For the development of business, the

Finance Department has a strong degree of importance. It's why it has a greater responsibility to

develop the best tactics and approaches to ensure that the aim of the business is accomplished as

necessary. SKANSKA is more capable of retaining its position or raising it to a whole new level

finance. For SKANSKA, accounting standards are very important, as they would help the

organisation to keep track on its revenue. The most important things to note to manage include

tracking transfers, because losing track of such a single transaction would mess with the

corporation's whole financial sector.

Budgeting: This is one of the key pillars of every enterprise. This needs to be done successfully,

and the brand growth ultimately depends on how expenditures are generated efficiently. As it

keeps a comprehensive list of estimates within the business, financial planning is a key function

of the accounting & financial division (Kramer and Weber, 2012). The Financial Department

was able to review the numbers and analyse the actual condition of the business. Budgets help

clients to foresee a potential vision in such a manner that the organisation needs to be efficient

enough to work properly. For all smaller or larger businesses, finance is essential, so SKANSKA

PLC, as the well big company, needs much more financial planning to meet the demands of

market competition. SKANSKA PLC. The goals to be set, together with the rival's position, must

be calculated in compliance with current industry evaluations. Accurate forecasting is not

possible without appropriate budgeting strategies.

Eradicating fraud: Avoiding fraud and stressing transparency in all dealings is one of the main

duties of auditors within a business. For top management, it is difficult to stop fraud under their

own. For the prevention of theft, upper management depends heavily on finance and business

departments. As the finance department manages inflows and outflows, the department should be

solely responsible as higher oversight brings significant obligations. The bigger the company's

size, the higher the employees and the greater the corporation's risk of corruption. SKANSKA

PLC is an immense business, and it is much tougher for a major corporation to deal with fraud.

To help SKANSKA PLC to eliminate bribery as a whole, control and tax departments must hold

a close eye on transparency.

In order to stay an efficient business unit, the accounting & finance department of SKANSKA

PLC should accept the duties and responsibilities listed. For the development of business, the

Finance Department has a strong degree of importance. It's why it has a greater responsibility to

develop the best tactics and approaches to ensure that the aim of the business is accomplished as

necessary. SKANSKA is more capable of retaining its position or raising it to a whole new level

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by accurately applying the techniques and procedures recommended by the accounting &

financial department. Accounting-and-finance activities are important for the analysis,

maintenance and control of all business-related financial processes and for the efficiency of all

operations (McLaughlin and Somerville, 2013). In order to create and run a business, it is

necessary to have a good understanding of facets of financial management that take place when

operating within the company, so that they can be properly handled.

TASK 2

Calculation of ratios for the company and comment on performance of company

Ratio analysis: - Through analysing the financial statements including the financial statements,

risk assessment is a systematic way of obtaining insight into to the stability, operating

performance, and profitability of the business (Samanez-Larkin, 2013). A foundation of

quantitative equity valuation is profitability ratios. Ratios are points of reference between

businesses. Inside a market, they measure stocks. Similarly, they measure a corporation against

the historic events today. In most situations, knowing the guiding ratios of factors is also

essential, as administration has the versatility to adjust its approach at times to make the portfolio

and business ratios more appealing. In addition, ratios are not usually used in isolation, or in

conjunction with other proportions. In any of the four generally listed categories, getting a clear

idea of the ratios would give you a detailed view of the business from multiple angles and help

you spot possible red flags. Through scrutinising previous and present financial accounts,

investors and analysts use ratio research to assess the financial performance of businesses.

Comparison statistics can indicate how a corporation operates over time which can be used to

predict possible future results. This information will also correlate the fiscal status of an

organisation with market trends when assessing how a company matches up against firms in the

same sector. Below ratio analysis of SKANSKA plc is done below in such manner:

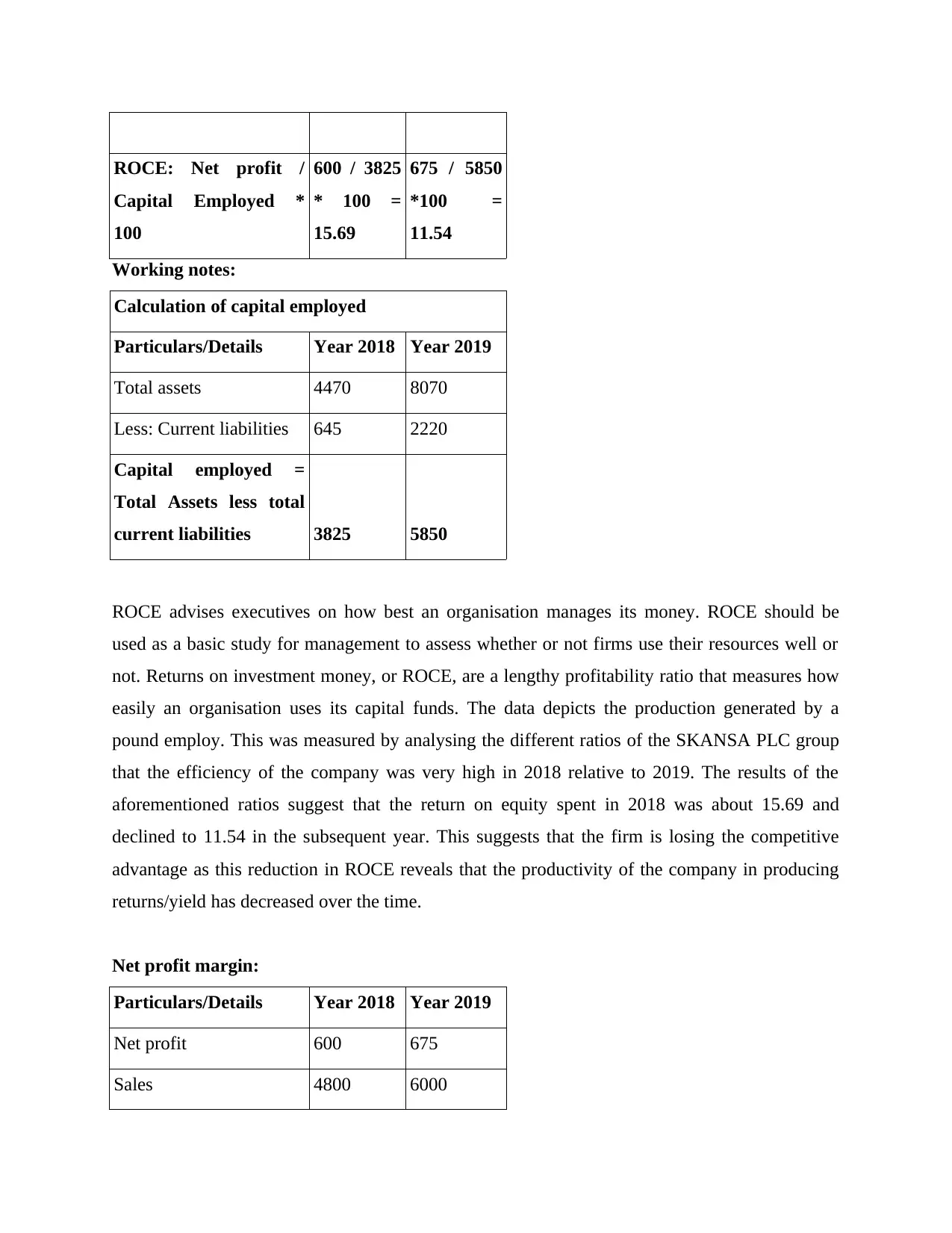

Return on capital employed:

Particulars/Details Year 2018 Year 2019

Net profits 600 675

Capital employed 3825 5850

financial department. Accounting-and-finance activities are important for the analysis,

maintenance and control of all business-related financial processes and for the efficiency of all

operations (McLaughlin and Somerville, 2013). In order to create and run a business, it is

necessary to have a good understanding of facets of financial management that take place when

operating within the company, so that they can be properly handled.

TASK 2

Calculation of ratios for the company and comment on performance of company

Ratio analysis: - Through analysing the financial statements including the financial statements,

risk assessment is a systematic way of obtaining insight into to the stability, operating

performance, and profitability of the business (Samanez-Larkin, 2013). A foundation of

quantitative equity valuation is profitability ratios. Ratios are points of reference between

businesses. Inside a market, they measure stocks. Similarly, they measure a corporation against

the historic events today. In most situations, knowing the guiding ratios of factors is also

essential, as administration has the versatility to adjust its approach at times to make the portfolio

and business ratios more appealing. In addition, ratios are not usually used in isolation, or in

conjunction with other proportions. In any of the four generally listed categories, getting a clear

idea of the ratios would give you a detailed view of the business from multiple angles and help

you spot possible red flags. Through scrutinising previous and present financial accounts,

investors and analysts use ratio research to assess the financial performance of businesses.

Comparison statistics can indicate how a corporation operates over time which can be used to

predict possible future results. This information will also correlate the fiscal status of an

organisation with market trends when assessing how a company matches up against firms in the

same sector. Below ratio analysis of SKANSKA plc is done below in such manner:

Return on capital employed:

Particulars/Details Year 2018 Year 2019

Net profits 600 675

Capital employed 3825 5850

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ROCE: Net profit /

Capital Employed *

100

600 / 3825

* 100 =

15.69

675 / 5850

*100 =

11.54

Working notes:

Calculation of capital employed

Particulars/Details Year 2018 Year 2019

Total assets 4470 8070

Less: Current liabilities 645 2220

Capital employed =

Total Assets less total

current liabilities 3825 5850

ROCE advises executives on how best an organisation manages its money. ROCE should be

used as a basic study for management to assess whether or not firms use their resources well or

not. Returns on investment money, or ROCE, are a lengthy profitability ratio that measures how

easily an organisation uses its capital funds. The data depicts the production generated by a

pound employ. This was measured by analysing the different ratios of the SKANSA PLC group

that the efficiency of the company was very high in 2018 relative to 2019. The results of the

aforementioned ratios suggest that the return on equity spent in 2018 was about 15.69 and

declined to 11.54 in the subsequent year. This suggests that the firm is losing the competitive

advantage as this reduction in ROCE reveals that the productivity of the company in producing

returns/yield has decreased over the time.

Net profit margin:

Particulars/Details Year 2018 Year 2019

Net profit 600 675

Sales 4800 6000

Capital Employed *

100

600 / 3825

* 100 =

15.69

675 / 5850

*100 =

11.54

Working notes:

Calculation of capital employed

Particulars/Details Year 2018 Year 2019

Total assets 4470 8070

Less: Current liabilities 645 2220

Capital employed =

Total Assets less total

current liabilities 3825 5850

ROCE advises executives on how best an organisation manages its money. ROCE should be

used as a basic study for management to assess whether or not firms use their resources well or

not. Returns on investment money, or ROCE, are a lengthy profitability ratio that measures how

easily an organisation uses its capital funds. The data depicts the production generated by a

pound employ. This was measured by analysing the different ratios of the SKANSA PLC group

that the efficiency of the company was very high in 2018 relative to 2019. The results of the

aforementioned ratios suggest that the return on equity spent in 2018 was about 15.69 and

declined to 11.54 in the subsequent year. This suggests that the firm is losing the competitive

advantage as this reduction in ROCE reveals that the productivity of the company in producing

returns/yield has decreased over the time.

Net profit margin:

Particulars/Details Year 2018 Year 2019

Net profit 600 675

Sales 4800 6000

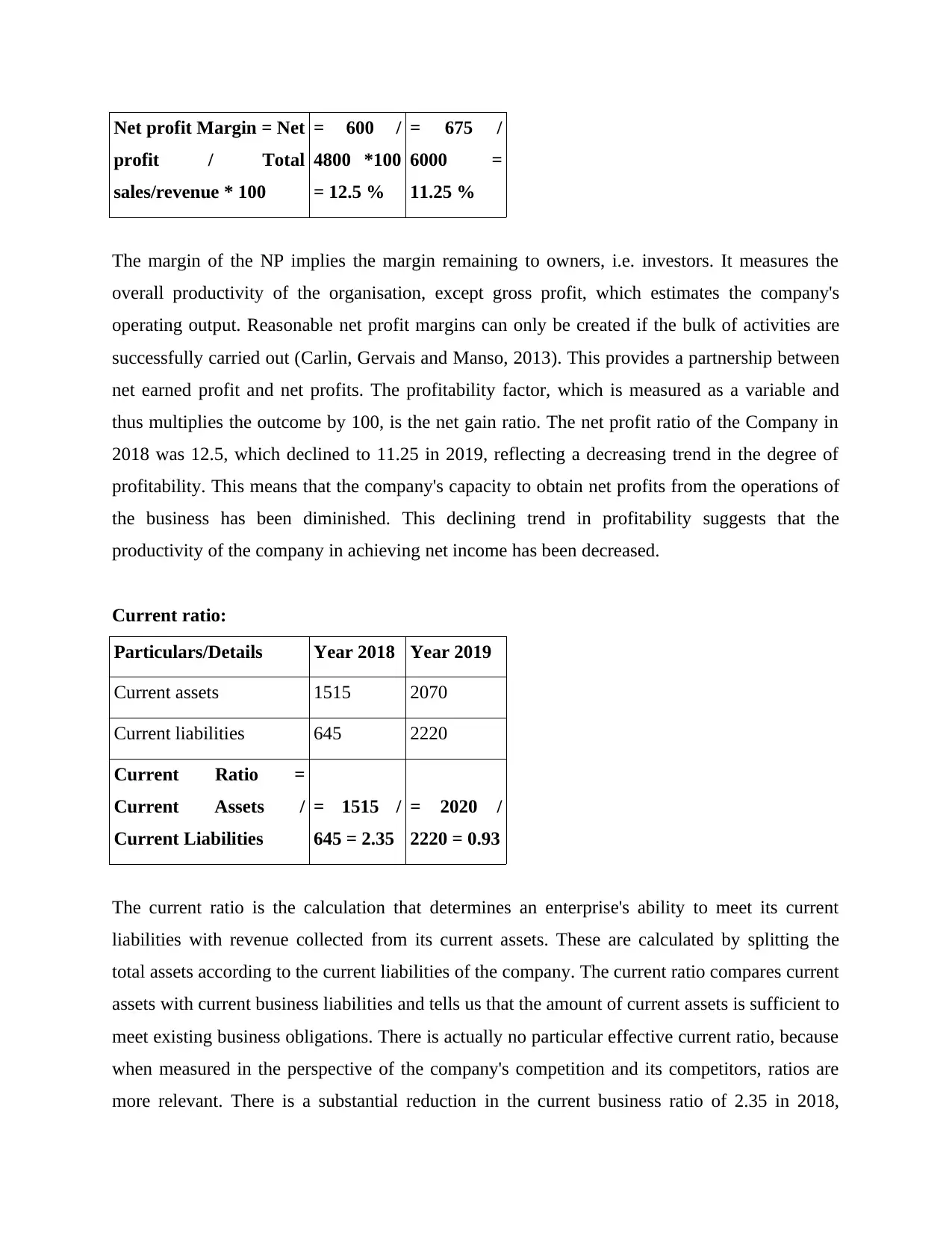

Net profit Margin = Net

profit / Total

sales/revenue * 100

= 600 /

4800 *100

= 12.5 %

= 675 /

6000 =

11.25 %

The margin of the NP implies the margin remaining to owners, i.e. investors. It measures the

overall productivity of the organisation, except gross profit, which estimates the company's

operating output. Reasonable net profit margins can only be created if the bulk of activities are

successfully carried out (Carlin, Gervais and Manso, 2013). This provides a partnership between

net earned profit and net profits. The profitability factor, which is measured as a variable and

thus multiplies the outcome by 100, is the net gain ratio. The net profit ratio of the Company in

2018 was 12.5, which declined to 11.25 in 2019, reflecting a decreasing trend in the degree of

profitability. This means that the company's capacity to obtain net profits from the operations of

the business has been diminished. This declining trend in profitability suggests that the

productivity of the company in achieving net income has been decreased.

Current ratio:

Particulars/Details Year 2018 Year 2019

Current assets 1515 2070

Current liabilities 645 2220

Current Ratio =

Current Assets /

Current Liabilities

= 1515 /

645 = 2.35

= 2020 /

2220 = 0.93

The current ratio is the calculation that determines an enterprise's ability to meet its current

liabilities with revenue collected from its current assets. These are calculated by splitting the

total assets according to the current liabilities of the company. The current ratio compares current

assets with current business liabilities and tells us that the amount of current assets is sufficient to

meet existing business obligations. There is actually no particular effective current ratio, because

when measured in the perspective of the company's competition and its competitors, ratios are

more relevant. There is a substantial reduction in the current business ratio of 2.35 in 2018,

profit / Total

sales/revenue * 100

= 600 /

4800 *100

= 12.5 %

= 675 /

6000 =

11.25 %

The margin of the NP implies the margin remaining to owners, i.e. investors. It measures the

overall productivity of the organisation, except gross profit, which estimates the company's

operating output. Reasonable net profit margins can only be created if the bulk of activities are

successfully carried out (Carlin, Gervais and Manso, 2013). This provides a partnership between

net earned profit and net profits. The profitability factor, which is measured as a variable and

thus multiplies the outcome by 100, is the net gain ratio. The net profit ratio of the Company in

2018 was 12.5, which declined to 11.25 in 2019, reflecting a decreasing trend in the degree of

profitability. This means that the company's capacity to obtain net profits from the operations of

the business has been diminished. This declining trend in profitability suggests that the

productivity of the company in achieving net income has been decreased.

Current ratio:

Particulars/Details Year 2018 Year 2019

Current assets 1515 2070

Current liabilities 645 2220

Current Ratio =

Current Assets /

Current Liabilities

= 1515 /

645 = 2.35

= 2020 /

2220 = 0.93

The current ratio is the calculation that determines an enterprise's ability to meet its current

liabilities with revenue collected from its current assets. These are calculated by splitting the

total assets according to the current liabilities of the company. The current ratio compares current

assets with current business liabilities and tells us that the amount of current assets is sufficient to

meet existing business obligations. There is actually no particular effective current ratio, because

when measured in the perspective of the company's competition and its competitors, ratios are

more relevant. There is a substantial reduction in the current business ratio of 2.35 in 2018,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

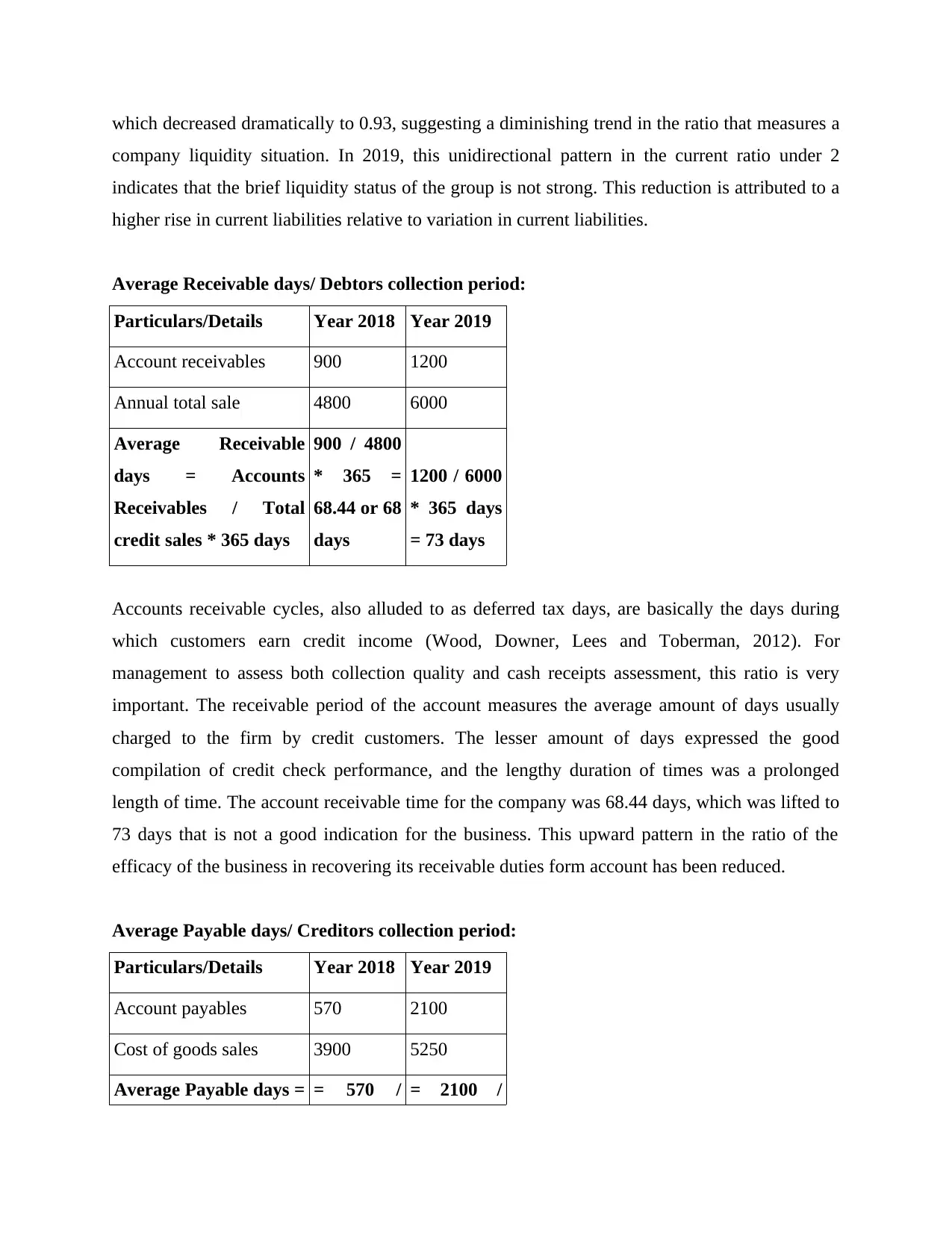

which decreased dramatically to 0.93, suggesting a diminishing trend in the ratio that measures a

company liquidity situation. In 2019, this unidirectional pattern in the current ratio under 2

indicates that the brief liquidity status of the group is not strong. This reduction is attributed to a

higher rise in current liabilities relative to variation in current liabilities.

Average Receivable days/ Debtors collection period:

Particulars/Details Year 2018 Year 2019

Account receivables 900 1200

Annual total sale 4800 6000

Average Receivable

days = Accounts

Receivables / Total

credit sales * 365 days

900 / 4800

* 365 =

68.44 or 68

days

1200 / 6000

* 365 days

= 73 days

Accounts receivable cycles, also alluded to as deferred tax days, are basically the days during

which customers earn credit income (Wood, Downer, Lees and Toberman, 2012). For

management to assess both collection quality and cash receipts assessment, this ratio is very

important. The receivable period of the account measures the average amount of days usually

charged to the firm by credit customers. The lesser amount of days expressed the good

compilation of credit check performance, and the lengthy duration of times was a prolonged

length of time. The account receivable time for the company was 68.44 days, which was lifted to

73 days that is not a good indication for the business. This upward pattern in the ratio of the

efficacy of the business in recovering its receivable duties form account has been reduced.

Average Payable days/ Creditors collection period:

Particulars/Details Year 2018 Year 2019

Account payables 570 2100

Cost of goods sales 3900 5250

Average Payable days = = 570 / = 2100 /

company liquidity situation. In 2019, this unidirectional pattern in the current ratio under 2

indicates that the brief liquidity status of the group is not strong. This reduction is attributed to a

higher rise in current liabilities relative to variation in current liabilities.

Average Receivable days/ Debtors collection period:

Particulars/Details Year 2018 Year 2019

Account receivables 900 1200

Annual total sale 4800 6000

Average Receivable

days = Accounts

Receivables / Total

credit sales * 365 days

900 / 4800

* 365 =

68.44 or 68

days

1200 / 6000

* 365 days

= 73 days

Accounts receivable cycles, also alluded to as deferred tax days, are basically the days during

which customers earn credit income (Wood, Downer, Lees and Toberman, 2012). For

management to assess both collection quality and cash receipts assessment, this ratio is very

important. The receivable period of the account measures the average amount of days usually

charged to the firm by credit customers. The lesser amount of days expressed the good

compilation of credit check performance, and the lengthy duration of times was a prolonged

length of time. The account receivable time for the company was 68.44 days, which was lifted to

73 days that is not a good indication for the business. This upward pattern in the ratio of the

efficacy of the business in recovering its receivable duties form account has been reduced.

Average Payable days/ Creditors collection period:

Particulars/Details Year 2018 Year 2019

Account payables 570 2100

Cost of goods sales 3900 5250

Average Payable days = = 570 / = 2100 /

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

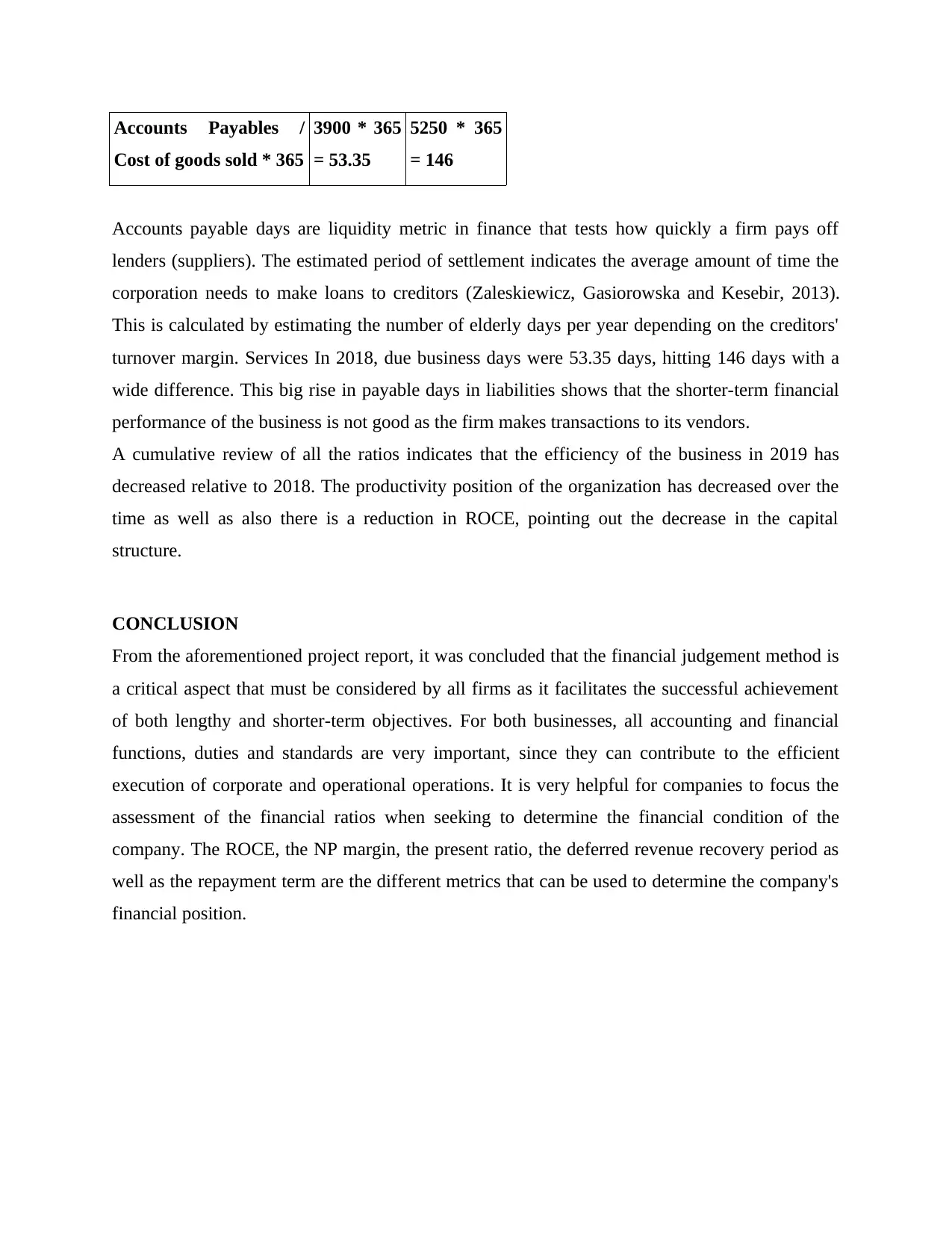

Accounts Payables /

Cost of goods sold * 365

3900 * 365

= 53.35

5250 * 365

= 146

Accounts payable days are liquidity metric in finance that tests how quickly a firm pays off

lenders (suppliers). The estimated period of settlement indicates the average amount of time the

corporation needs to make loans to creditors (Zaleskiewicz, Gasiorowska and Kesebir, 2013).

This is calculated by estimating the number of elderly days per year depending on the creditors'

turnover margin. Services In 2018, due business days were 53.35 days, hitting 146 days with a

wide difference. This big rise in payable days in liabilities shows that the shorter-term financial

performance of the business is not good as the firm makes transactions to its vendors.

A cumulative review of all the ratios indicates that the efficiency of the business in 2019 has

decreased relative to 2018. The productivity position of the organization has decreased over the

time as well as also there is a reduction in ROCE, pointing out the decrease in the capital

structure.

CONCLUSION

From the aforementioned project report, it was concluded that the financial judgement method is

a critical aspect that must be considered by all firms as it facilitates the successful achievement

of both lengthy and shorter-term objectives. For both businesses, all accounting and financial

functions, duties and standards are very important, since they can contribute to the efficient

execution of corporate and operational operations. It is very helpful for companies to focus the

assessment of the financial ratios when seeking to determine the financial condition of the

company. The ROCE, the NP margin, the present ratio, the deferred revenue recovery period as

well as the repayment term are the different metrics that can be used to determine the company's

financial position.

Cost of goods sold * 365

3900 * 365

= 53.35

5250 * 365

= 146

Accounts payable days are liquidity metric in finance that tests how quickly a firm pays off

lenders (suppliers). The estimated period of settlement indicates the average amount of time the

corporation needs to make loans to creditors (Zaleskiewicz, Gasiorowska and Kesebir, 2013).

This is calculated by estimating the number of elderly days per year depending on the creditors'

turnover margin. Services In 2018, due business days were 53.35 days, hitting 146 days with a

wide difference. This big rise in payable days in liabilities shows that the shorter-term financial

performance of the business is not good as the firm makes transactions to its vendors.

A cumulative review of all the ratios indicates that the efficiency of the business in 2019 has

decreased relative to 2018. The productivity position of the organization has decreased over the

time as well as also there is a reduction in ROCE, pointing out the decrease in the capital

structure.

CONCLUSION

From the aforementioned project report, it was concluded that the financial judgement method is

a critical aspect that must be considered by all firms as it facilitates the successful achievement

of both lengthy and shorter-term objectives. For both businesses, all accounting and financial

functions, duties and standards are very important, since they can contribute to the efficient

execution of corporate and operational operations. It is very helpful for companies to focus the

assessment of the financial ratios when seeking to determine the financial condition of the

company. The ROCE, the NP margin, the present ratio, the deferred revenue recovery period as

well as the repayment term are the different metrics that can be used to determine the company's

financial position.

REFERENCES

Agarwal, S. and Mazumder, B., 2013. Cognitive abilities and household financial decision

making. American Economic Journal: Applied Economics, 5(1), pp.193-207.

Lusardi, A., 2012. Numeracy, financial literacy, and financial decision-making (No. w17821).

National Bureau of Economic Research.

Nga, J.K. and Yien, L.K., 2013. The influence of personality trait and demographics on financial

decision making among Generation Y. Young Consumers.

Brahmana, R.K., Hooy, C.W. and Ahmad, Z., 2012. Psychological factors on irrational financial

decision making. Humanomics.

MacLean, L.C. and Ziemba, W.T., 2013. Handbook of the fundamentals of financial decision

making (Vol. 4). World Scientific.

Kramer, L.A. and Weber, J.M., 2012. This is your portfolio on winter: Seasonal affective

disorder and risk aversion in financial decision making. Social Psychological and

Personality Science, 3(2), pp.193-199.

McLaughlin, O. and Somerville, J., 2013. Choice blindness in financial decision

making. Judgment and Decision Making, 8(5), p.577.

Samanez-Larkin, G.R., 2013. Financial decision making and the aging brain. APS

observer, 26(5), p.30.

Carlin, B.I., Gervais, S. and Manso, G., 2013. Libertarian paternalism, information production,

and financial decision making. The Review of Financial Studies, 26(9), pp.2204-2228.

Wood, A., Downer, K., Lees, B. and Toberman, A., 2012. Household financial decision making:

Qualitative research with couples. Department for Work and Pensions Research

Report, 805.

Zaleskiewicz, T., Gasiorowska, A. and Kesebir, P., 2013. Saving can save from death anxiety:

Mortality salience and financial decision-making. PloS one, 8(11), p.e79407.

Agarwal, S. and Mazumder, B., 2013. Cognitive abilities and household financial decision

making. American Economic Journal: Applied Economics, 5(1), pp.193-207.

Lusardi, A., 2012. Numeracy, financial literacy, and financial decision-making (No. w17821).

National Bureau of Economic Research.

Nga, J.K. and Yien, L.K., 2013. The influence of personality trait and demographics on financial

decision making among Generation Y. Young Consumers.

Brahmana, R.K., Hooy, C.W. and Ahmad, Z., 2012. Psychological factors on irrational financial

decision making. Humanomics.

MacLean, L.C. and Ziemba, W.T., 2013. Handbook of the fundamentals of financial decision

making (Vol. 4). World Scientific.

Kramer, L.A. and Weber, J.M., 2012. This is your portfolio on winter: Seasonal affective

disorder and risk aversion in financial decision making. Social Psychological and

Personality Science, 3(2), pp.193-199.

McLaughlin, O. and Somerville, J., 2013. Choice blindness in financial decision

making. Judgment and Decision Making, 8(5), p.577.

Samanez-Larkin, G.R., 2013. Financial decision making and the aging brain. APS

observer, 26(5), p.30.

Carlin, B.I., Gervais, S. and Manso, G., 2013. Libertarian paternalism, information production,

and financial decision making. The Review of Financial Studies, 26(9), pp.2204-2228.

Wood, A., Downer, K., Lees, B. and Toberman, A., 2012. Household financial decision making:

Qualitative research with couples. Department for Work and Pensions Research

Report, 805.

Zaleskiewicz, T., Gasiorowska, A. and Kesebir, P., 2013. Saving can save from death anxiety:

Mortality salience and financial decision-making. PloS one, 8(11), p.e79407.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.