Financial Decision-Making: Analysis of Skanska PLC's Performance

VerifiedAdded on 2022/12/26

|11

|3315

|90

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making, focusing on the case of Skanska PLC, a UK-based construction and engineering corporation. The report begins by exploring the importance, duties, and roles of accounting and finance functions within a company, emphasizing their significance in strategic decision-making, especially as Skanska plans its expansion into European markets. It then delves into a detailed examination of financial ratios, including Return on Capital Employed (ROCE), net profit margin, and the current ratio, analyzing their trends from 2018 to 2019. The analysis highlights the implications of these ratios on the company's financial health and performance. The report concludes by summarizing the key findings and their impact on Skanska's financial strategy and overall business operations.

Financial Decision-Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles:...........................................3

TASK 2............................................................................................................................................7

Ratio computation and analysis:..................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Importance of Accounting and Finance functions, duties and roles:...........................................3

TASK 2............................................................................................................................................7

Ratio computation and analysis:..................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial decision-making is a mechanism by which the administration of a company is

enabled to make various kinds of actions swiftly and appropriately. This allows us to ensure that

organizations are equipped to understand how they could evaluate and view financial statistical

data, figures and facts such that multiple sorts of shorter-term, medium-term and longer-term

decisions could be made. Financial decision-making is procedure of assessing the pluses and

minuses of decision when it applies to the use of capital (Klačmer Čalopa, 2017). Effective

financial decision-making is crucial prerequisite for performance in investing. This study is

focused on the Skanska PLC, a UK based Construction and Engineering Corporation

headquartered in Hertfordshire, UK. The business plans to spread to European nations within the

coming 10 years as well as to increase their market share. This study would concentrate in depth

on assessing the value of accounting as well as finance tasks. In addition, a detailed study of the

various ratios would be carried out as aspect of the project.

TASK 1

Importance of Accounting and Finance functions, duties and roles:

A specialized group of professionals who oversee a firm's financial activities is known

as accounting division. Although not every staff member will be certified public accountant, staff

members will usually be trained in accounting systems and practices. By establishing an

accounting division, a corporation could assist to ensure complete disclosure in its monetary

transactions while offering specialized, streamlined assistance to other departments and

executives. Accounting team will help ensure continued health of company. Accounting division

of a company offers finance and monetary assistance to the company. Trade payable, and trade-

receivable, stock, wages, capital assets and other such fiscal aspects are all held in this division.

In this division, accountants look through each division's reports to assess the corporation 's

fiscal status and any adjustments that are expected to manage the entity efficiently (Ziolo,

Filipiak, Bąk and Cheba, 2019).

Accounting division is base of enterprise finance department. This is in charge of all

accounting, accounts payables, and receivables, as well as the planning of business's balance

sheets, banking data, cash-flow analyses, and day-to-day bookkeeping and supervising. This also

monitors and oversees all business's internal audits and safeguards, as well as taxation and

3

Financial decision-making is a mechanism by which the administration of a company is

enabled to make various kinds of actions swiftly and appropriately. This allows us to ensure that

organizations are equipped to understand how they could evaluate and view financial statistical

data, figures and facts such that multiple sorts of shorter-term, medium-term and longer-term

decisions could be made. Financial decision-making is procedure of assessing the pluses and

minuses of decision when it applies to the use of capital (Klačmer Čalopa, 2017). Effective

financial decision-making is crucial prerequisite for performance in investing. This study is

focused on the Skanska PLC, a UK based Construction and Engineering Corporation

headquartered in Hertfordshire, UK. The business plans to spread to European nations within the

coming 10 years as well as to increase their market share. This study would concentrate in depth

on assessing the value of accounting as well as finance tasks. In addition, a detailed study of the

various ratios would be carried out as aspect of the project.

TASK 1

Importance of Accounting and Finance functions, duties and roles:

A specialized group of professionals who oversee a firm's financial activities is known

as accounting division. Although not every staff member will be certified public accountant, staff

members will usually be trained in accounting systems and practices. By establishing an

accounting division, a corporation could assist to ensure complete disclosure in its monetary

transactions while offering specialized, streamlined assistance to other departments and

executives. Accounting team will help ensure continued health of company. Accounting division

of a company offers finance and monetary assistance to the company. Trade payable, and trade-

receivable, stock, wages, capital assets and other such fiscal aspects are all held in this division.

In this division, accountants look through each division's reports to assess the corporation 's

fiscal status and any adjustments that are expected to manage the entity efficiently (Ziolo,

Filipiak, Bąk and Cheba, 2019).

Accounting division is base of enterprise finance department. This is in charge of all

accounting, accounts payables, and receivables, as well as the planning of business's balance

sheets, banking data, cash-flow analyses, and day-to-day bookkeeping and supervising. This also

monitors and oversees all business's internal audits and safeguards, as well as taxation and

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

disclosure. It ensures that the company complies with all legislation as well as is in effective

financial position.

Both departments are a vital division in every enterprise. As a result, it is expected of

organisations to utilize it persistently and properly in order to properly assess their financial

status As Skanska corporation plans to extend into European nations over the next ten years, its

executives must analyse the various positions of both divisions in order to undertake productive

decisions (Esch, Schulze and Wald, 2019). In the context of SKANSA PLC, following is

evaluation of importance, duties and roles of the Accounting and Finance-division, as follows:

Bookkeeping: This is finance and accounting department's most fundamental function. This

entails the documentation, review, and understanding of a corporation 's financial activities on a

daily basis. This will entail keeping track of all spending (investments, transactions, and so forth)

as well as completed merchandise transactions. This position is mostly filled by bookkeeper in

an enterprise, but as the organization develops and evolves, it can be substituted by more

skilled staff.

Treasury management: The accounting and financing division develops specific treasury

management strategy on all personnel who work with currency or cash equivalents. Stuff about

the amount of risk that the company will take on at any given time are part of treasury planning.

Finance/accounting manager is generally in charge of treasury activities, while finance officer

or chief financial officers is in charge of financial accounting (Rasheed and Siddiqui, 2019).

Controlling and Managing the Inventory: The accounts and finance division is also often in

responsibility of monitoring and administering the company's stocks and supplies. Other than

finance unit, no other team is well prepared to deal with stockholdings. The stocks must be

recorded and managed using a variety of statistical procedures. To supervise and preserve the

inventory levels that describe finance department's competitive edge, special methods are being

used. SKANSKA corporation's accounting and finances department has to be competent of

properly handling and controlling inventory operations. Stock planning can assist SKANSKA

PLC in determining whether it is necessary to restock whether inventories are running short. This

would also aid in ensuring correct leading period of materials when they are needed.

Managing company’s cash flow: The financial and accounts department is responsible for

managing all cash-flows through as well as out of organization and ensuring that sufficient funds

are available to fulfill the corporation's daily operations desires. This division also includes the

4

financial position.

Both departments are a vital division in every enterprise. As a result, it is expected of

organisations to utilize it persistently and properly in order to properly assess their financial

status As Skanska corporation plans to extend into European nations over the next ten years, its

executives must analyse the various positions of both divisions in order to undertake productive

decisions (Esch, Schulze and Wald, 2019). In the context of SKANSA PLC, following is

evaluation of importance, duties and roles of the Accounting and Finance-division, as follows:

Bookkeeping: This is finance and accounting department's most fundamental function. This

entails the documentation, review, and understanding of a corporation 's financial activities on a

daily basis. This will entail keeping track of all spending (investments, transactions, and so forth)

as well as completed merchandise transactions. This position is mostly filled by bookkeeper in

an enterprise, but as the organization develops and evolves, it can be substituted by more

skilled staff.

Treasury management: The accounting and financing division develops specific treasury

management strategy on all personnel who work with currency or cash equivalents. Stuff about

the amount of risk that the company will take on at any given time are part of treasury planning.

Finance/accounting manager is generally in charge of treasury activities, while finance officer

or chief financial officers is in charge of financial accounting (Rasheed and Siddiqui, 2019).

Controlling and Managing the Inventory: The accounts and finance division is also often in

responsibility of monitoring and administering the company's stocks and supplies. Other than

finance unit, no other team is well prepared to deal with stockholdings. The stocks must be

recorded and managed using a variety of statistical procedures. To supervise and preserve the

inventory levels that describe finance department's competitive edge, special methods are being

used. SKANSKA corporation's accounting and finances department has to be competent of

properly handling and controlling inventory operations. Stock planning can assist SKANSKA

PLC in determining whether it is necessary to restock whether inventories are running short. This

would also aid in ensuring correct leading period of materials when they are needed.

Managing company’s cash flow: The financial and accounts department is responsible for

managing all cash-flows through as well as out of organization and ensuring that sufficient funds

are available to fulfill the corporation's daily operations desires. This division also includes the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

corporation's credits and collections practices, which guarantee that retailers and suppliers are

charged timely and accurately, as well as that the organization is paid accurately and

within reasonable time (Vitale and Cull, 2018).

Managing Company’s Investments: The finances and accounts department is also responsible

for handling the corporation 's current holdings in addition to reviewing and choosing new

acquisitions. Apart from capital assets, finance department must be concentrated towards current

assets. Because it has larger effect on corporation's liquidity instead of its fixed

assets, corporation's working capital must be handled effectively in order to optimize profits

compared to the sum of funding tied up.

Financial Reporting and analysis: The function of fiscal reporting and evaluation is to convert

raw accounts entries into relevant, accessible, and equivalent financial statements. The finances

and accounts department leads to corporate progress by consistently monitoring and publishing

crucial statistics that are essential to the corporation 's performance This will almost certainly

provide a list of all funding sources, investments, and reserves allocated for potential usage (with

exception of all those allocated and planned for the current cycle), as well as any non-financial

data. And they're normally presented to administrators in a reasonable and understandable

manner.

Help managers in taking key strategic decisions: The finances and accounts department offers

information to corporate managers to help them make financial choices including which sectors

or ventures to enter, payback dates for major capital acquisitions, assessing how much of the

corporation 's profits should be paid as dividends and how much should be reinvested in the firm,

assessing the right funding combination that will yield the corporation the most benefit, and so

forth (Venter, Gordon and Street, 2018).

Budgeting Processes: Budgeting is key important aspects of any corporation. This must be

achieved quickly since the sustainability of the company is entirely dependent on how

well budgets are designed. Since they possess the entire list of figures within the company, the

accounts and finance division is also responsible for budgeting. Just the financial department has

the ability to analyze statistics to assess the company's actual situation. Budgets enable

stakeholders to envision future, so the agency must be productive enough to function in that

direction. Budgeting is necessary for all companies, large and small and SKANSKA PLC, as a

known large company, requires a disproportionate amount of financial planning to face the

5

charged timely and accurately, as well as that the organization is paid accurately and

within reasonable time (Vitale and Cull, 2018).

Managing Company’s Investments: The finances and accounts department is also responsible

for handling the corporation 's current holdings in addition to reviewing and choosing new

acquisitions. Apart from capital assets, finance department must be concentrated towards current

assets. Because it has larger effect on corporation's liquidity instead of its fixed

assets, corporation's working capital must be handled effectively in order to optimize profits

compared to the sum of funding tied up.

Financial Reporting and analysis: The function of fiscal reporting and evaluation is to convert

raw accounts entries into relevant, accessible, and equivalent financial statements. The finances

and accounts department leads to corporate progress by consistently monitoring and publishing

crucial statistics that are essential to the corporation 's performance This will almost certainly

provide a list of all funding sources, investments, and reserves allocated for potential usage (with

exception of all those allocated and planned for the current cycle), as well as any non-financial

data. And they're normally presented to administrators in a reasonable and understandable

manner.

Help managers in taking key strategic decisions: The finances and accounts department offers

information to corporate managers to help them make financial choices including which sectors

or ventures to enter, payback dates for major capital acquisitions, assessing how much of the

corporation 's profits should be paid as dividends and how much should be reinvested in the firm,

assessing the right funding combination that will yield the corporation the most benefit, and so

forth (Venter, Gordon and Street, 2018).

Budgeting Processes: Budgeting is key important aspects of any corporation. This must be

achieved quickly since the sustainability of the company is entirely dependent on how

well budgets are designed. Since they possess the entire list of figures within the company, the

accounts and finance division is also responsible for budgeting. Just the financial department has

the ability to analyze statistics to assess the company's actual situation. Budgets enable

stakeholders to envision future, so the agency must be productive enough to function in that

direction. Budgeting is necessary for all companies, large and small and SKANSKA PLC, as a

known large company, requires a disproportionate amount of financial planning to face the

5

industry's difficulties. SKANSKA Corporation must assess what goals can be developed in light

of existing market assessments as well as the status of competing companies. No reliable

prediction is feasible without adequate budgeting strategies.

Advising and sourcing of longer-term financing: The finances and accounting department's

function is to advise businesses on the right funding mix that will yield the most benefit and to

assist them in obtaining longer-term financing at lowest cost in order to maintain a sufficient

scale of liquidity (Eberhardt, de Bruin and Strough, 2019).

Managing Taxes: Taxes are a component of operating a corporation and finance division is in

charge of dealing with them. This involves forming constructive business ties with government

through remitting PAYE to the appropriate authority and ensures that tax issues are implemented

in compliance with existing policies.

Managing Risks: Company's financial and accounts department is also in charge of the risk

management. They are in charge of identifying, analyzing, prioritizing, and mitigating the

corporation's risks. External improvements are predicted by the financial division for new

product that isn't going too well. They reflect global developments such as the economy's

contraction, currency volatility, and so on. They make the most of their ability to mitigate the

effects and keep an eye on the situation for improvements. Risk assessment also assists in the

maximization of project prospects by forecasting and becoming aware of industry developments

and acquisition opportunities.

Capital Budgeting: This is the practice of observing and finding projects and prospects in the

economy that are worth participating in. Land, acquisitions mergers, and the buying of fixed

asset are also exampling of its implementations. The entire concept of the capital budgeting

for business revolves around the primary goal of rising profitability. They want to increase

earnings in order to keep the corporation's capital increasing.

SKANSKA corporation's accounts and finance division would offer a slew of upsides

to corporation. By offering the best image of fiscal stability, the division would be inclined to

convince clients. In addition, the company would be able to establish an appropriate alignment

among risks and profit maximization. Financial managerial concept often helps the company to

make decisions in a structured and well-organized way. SKANSKA Corporation will also

achieve a strategic edge because it will be able to adapt quickly to all financial-related problems.

6

of existing market assessments as well as the status of competing companies. No reliable

prediction is feasible without adequate budgeting strategies.

Advising and sourcing of longer-term financing: The finances and accounting department's

function is to advise businesses on the right funding mix that will yield the most benefit and to

assist them in obtaining longer-term financing at lowest cost in order to maintain a sufficient

scale of liquidity (Eberhardt, de Bruin and Strough, 2019).

Managing Taxes: Taxes are a component of operating a corporation and finance division is in

charge of dealing with them. This involves forming constructive business ties with government

through remitting PAYE to the appropriate authority and ensures that tax issues are implemented

in compliance with existing policies.

Managing Risks: Company's financial and accounts department is also in charge of the risk

management. They are in charge of identifying, analyzing, prioritizing, and mitigating the

corporation's risks. External improvements are predicted by the financial division for new

product that isn't going too well. They reflect global developments such as the economy's

contraction, currency volatility, and so on. They make the most of their ability to mitigate the

effects and keep an eye on the situation for improvements. Risk assessment also assists in the

maximization of project prospects by forecasting and becoming aware of industry developments

and acquisition opportunities.

Capital Budgeting: This is the practice of observing and finding projects and prospects in the

economy that are worth participating in. Land, acquisitions mergers, and the buying of fixed

asset are also exampling of its implementations. The entire concept of the capital budgeting

for business revolves around the primary goal of rising profitability. They want to increase

earnings in order to keep the corporation's capital increasing.

SKANSKA corporation's accounts and finance division would offer a slew of upsides

to corporation. By offering the best image of fiscal stability, the division would be inclined to

convince clients. In addition, the company would be able to establish an appropriate alignment

among risks and profit maximization. Financial managerial concept often helps the company to

make decisions in a structured and well-organized way. SKANSKA Corporation will also

achieve a strategic edge because it will be able to adapt quickly to all financial-related problems.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The division's overall practices will operate smoothly with one of most significant reasons being

the flow of funds to properly finance division's expenditures.

TASK 2

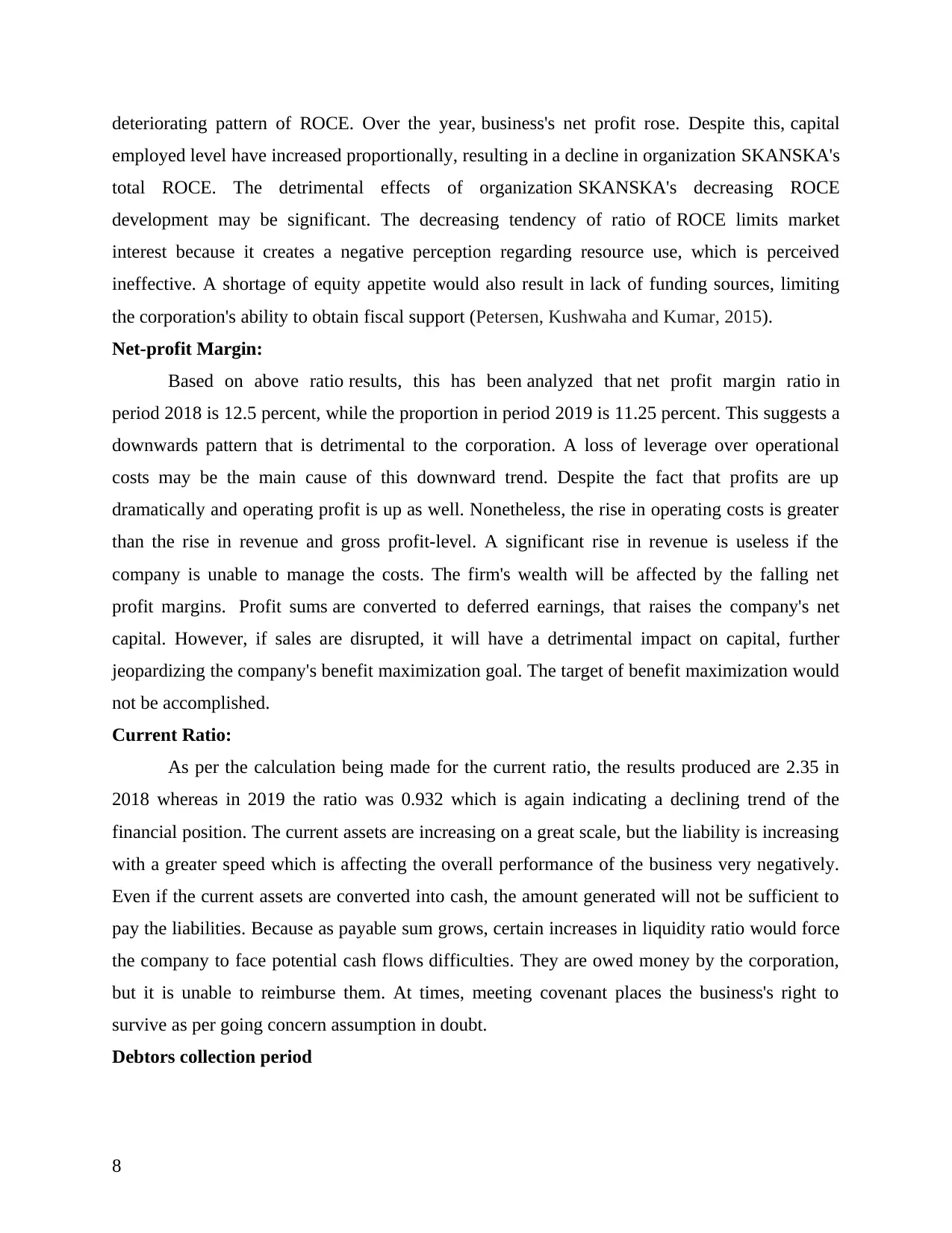

Ratio computation and analysis:

Interpretation of above computed ratios:

ROCE

The findings of the aforementioned measurement of corporation SKANSKA's ROCE for periods

year-2018 and year-2019 show a falling pattern, with the return on capital in 2018 reached

to 34.96% and in year-2019 reached to 18.67%. When analysing efficiency by ratio of ROCE,

the optimal tendency for stakeholders is for results to be stronger or consistent. The inefficient

usage of resources in the sector may be one of the potential factors or explanations for the

7

the flow of funds to properly finance division's expenditures.

TASK 2

Ratio computation and analysis:

Interpretation of above computed ratios:

ROCE

The findings of the aforementioned measurement of corporation SKANSKA's ROCE for periods

year-2018 and year-2019 show a falling pattern, with the return on capital in 2018 reached

to 34.96% and in year-2019 reached to 18.67%. When analysing efficiency by ratio of ROCE,

the optimal tendency for stakeholders is for results to be stronger or consistent. The inefficient

usage of resources in the sector may be one of the potential factors or explanations for the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deteriorating pattern of ROCE. Over the year, business's net profit rose. Despite this, capital

employed level have increased proportionally, resulting in a decline in organization SKANSKA's

total ROCE. The detrimental effects of organization SKANSKA's decreasing ROCE

development may be significant. The decreasing tendency of ratio of ROCE limits market

interest because it creates a negative perception regarding resource use, which is perceived

ineffective. A shortage of equity appetite would also result in lack of funding sources, limiting

the corporation's ability to obtain fiscal support (Petersen, Kushwaha and Kumar, 2015).

Net-profit Margin:

Based on above ratio results, this has been analyzed that net profit margin ratio in

period 2018 is 12.5 percent, while the proportion in period 2019 is 11.25 percent. This suggests a

downwards pattern that is detrimental to the corporation. A loss of leverage over operational

costs may be the main cause of this downward trend. Despite the fact that profits are up

dramatically and operating profit is up as well. Nonetheless, the rise in operating costs is greater

than the rise in revenue and gross profit-level. A significant rise in revenue is useless if the

company is unable to manage the costs. The firm's wealth will be affected by the falling net

profit margins. Profit sums are converted to deferred earnings, that raises the company's net

capital. However, if sales are disrupted, it will have a detrimental impact on capital, further

jeopardizing the company's benefit maximization goal. The target of benefit maximization would

not be accomplished.

Current Ratio:

As per the calculation being made for the current ratio, the results produced are 2.35 in

2018 whereas in 2019 the ratio was 0.932 which is again indicating a declining trend of the

financial position. The current assets are increasing on a great scale, but the liability is increasing

with a greater speed which is affecting the overall performance of the business very negatively.

Even if the current assets are converted into cash, the amount generated will not be sufficient to

pay the liabilities. Because as payable sum grows, certain increases in liquidity ratio would force

the company to face potential cash flows difficulties. They are owed money by the corporation,

but it is unable to reimburse them. At times, meeting covenant places the business's right to

survive as per going concern assumption in doubt.

Debtors collection period

8

employed level have increased proportionally, resulting in a decline in organization SKANSKA's

total ROCE. The detrimental effects of organization SKANSKA's decreasing ROCE

development may be significant. The decreasing tendency of ratio of ROCE limits market

interest because it creates a negative perception regarding resource use, which is perceived

ineffective. A shortage of equity appetite would also result in lack of funding sources, limiting

the corporation's ability to obtain fiscal support (Petersen, Kushwaha and Kumar, 2015).

Net-profit Margin:

Based on above ratio results, this has been analyzed that net profit margin ratio in

period 2018 is 12.5 percent, while the proportion in period 2019 is 11.25 percent. This suggests a

downwards pattern that is detrimental to the corporation. A loss of leverage over operational

costs may be the main cause of this downward trend. Despite the fact that profits are up

dramatically and operating profit is up as well. Nonetheless, the rise in operating costs is greater

than the rise in revenue and gross profit-level. A significant rise in revenue is useless if the

company is unable to manage the costs. The firm's wealth will be affected by the falling net

profit margins. Profit sums are converted to deferred earnings, that raises the company's net

capital. However, if sales are disrupted, it will have a detrimental impact on capital, further

jeopardizing the company's benefit maximization goal. The target of benefit maximization would

not be accomplished.

Current Ratio:

As per the calculation being made for the current ratio, the results produced are 2.35 in

2018 whereas in 2019 the ratio was 0.932 which is again indicating a declining trend of the

financial position. The current assets are increasing on a great scale, but the liability is increasing

with a greater speed which is affecting the overall performance of the business very negatively.

Even if the current assets are converted into cash, the amount generated will not be sufficient to

pay the liabilities. Because as payable sum grows, certain increases in liquidity ratio would force

the company to face potential cash flows difficulties. They are owed money by the corporation,

but it is unable to reimburse them. At times, meeting covenant places the business's right to

survive as per going concern assumption in doubt.

Debtors collection period

8

Based on above computations of ratio this has been analysed that, the total

receivables days for period 2018 is approx. 68.44 days, while the result for period 2019 is

approx. 73 days. The improvement of the length is unfavorable since it indicates that the money

due from debtors would therefore take longer for the company to obtain. In period 2018, the total

collection period is lower, suggesting that the sum of collecting is accomplished in a smaller

period of time According to the figures for 2019, the number of days has risen, resulting in a

pause in payment receipt. The primary explanation for this rise is that debtors are either unable

or unable to pay due amount. The implication of such a rising amount of days raises the

likelihood of default on the trade debtor's part, resulting in a rise in bad debts cost on income

statement. Total profitability would suffer as a consequence of these outcomes, because this will

be adversely affected. With growing payment defaults, the chance of no redemption rises, and

such account receivables are more likely to default (Yue, Gizem Korkmaz and Zhou, 2020).

Creditors collection period:

Based on the aforementioned compurgation in table, average payable duration is

approx. 43 days during period 2018 as well as 128-days during period 2019 of company. Both

numbers show a significant gap. The longer the pay-outs term, the greater the harm. The key

explanation for the spike in payables days is that the firm doesn't have enough cash to reimburse

its suppliers. This illustrates that the corporation is struggling to pay its suppliers because it's not

making sufficient sales.

The impact of the rise for several days will be unfavourable, because as business would

experience additional cash flows problems as a result of insufficient sales, and the enterprise will

find this impossible to meet its expenditures and obligations at same time. Another result of the

longer average payment time may be a loss of supplier credibility. In the view of manufacturers,

a firm's value or reputation can be questioned. To ensure that their cash is not lost, the vendors

will be unable to deliver any additional products. Any company's foundation is its suppliers, and

disrupting their terms will have a detrimental effect on entire business processes (Cook and

Sadeghein, 2018).

CONCLUSION

From above study this has been ascertained that Accounts and financing are essential

facets of every company's administration. Profits and cash are what businesses strive for

at ending of the day and even if money is mismanaged, the company as a whole is mismanaged.

9

receivables days for period 2018 is approx. 68.44 days, while the result for period 2019 is

approx. 73 days. The improvement of the length is unfavorable since it indicates that the money

due from debtors would therefore take longer for the company to obtain. In period 2018, the total

collection period is lower, suggesting that the sum of collecting is accomplished in a smaller

period of time According to the figures for 2019, the number of days has risen, resulting in a

pause in payment receipt. The primary explanation for this rise is that debtors are either unable

or unable to pay due amount. The implication of such a rising amount of days raises the

likelihood of default on the trade debtor's part, resulting in a rise in bad debts cost on income

statement. Total profitability would suffer as a consequence of these outcomes, because this will

be adversely affected. With growing payment defaults, the chance of no redemption rises, and

such account receivables are more likely to default (Yue, Gizem Korkmaz and Zhou, 2020).

Creditors collection period:

Based on the aforementioned compurgation in table, average payable duration is

approx. 43 days during period 2018 as well as 128-days during period 2019 of company. Both

numbers show a significant gap. The longer the pay-outs term, the greater the harm. The key

explanation for the spike in payables days is that the firm doesn't have enough cash to reimburse

its suppliers. This illustrates that the corporation is struggling to pay its suppliers because it's not

making sufficient sales.

The impact of the rise for several days will be unfavourable, because as business would

experience additional cash flows problems as a result of insufficient sales, and the enterprise will

find this impossible to meet its expenditures and obligations at same time. Another result of the

longer average payment time may be a loss of supplier credibility. In the view of manufacturers,

a firm's value or reputation can be questioned. To ensure that their cash is not lost, the vendors

will be unable to deliver any additional products. Any company's foundation is its suppliers, and

disrupting their terms will have a detrimental effect on entire business processes (Cook and

Sadeghein, 2018).

CONCLUSION

From above study this has been ascertained that Accounts and financing are essential

facets of every company's administration. Profits and cash are what businesses strive for

at ending of the day and even if money is mismanaged, the company as a whole is mismanaged.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The movement of money could be managed and measured by effectively managing the

accounting and financial of the company's expenditure and profits, thus leading the business

direction. To formulate effective financial plan that supports company's goals, efficient finance

management or supervisor must consider and comprehend every part of each business aims.

10

accounting and financial of the company's expenditure and profits, thus leading the business

direction. To formulate effective financial plan that supports company's goals, efficient finance

management or supervisor must consider and comprehend every part of each business aims.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Klačmer Čalopa, M., 2017. Business owner and manager’s attitudes towards financial decision-

making and strategic planning: Evidence from Croatian SMEs. Management: journal of

contemporary management issues, 22(1), pp.103-116.

Ziolo, M., Filipiak, B.Z., Bąk, I. and Cheba, K., 2019. How to design more sustainable financial

systems: the roles of environmental, social, and governance factors in the decision-

making process. Sustainability, 11(20), p.5604.

Esch, M., Schulze, M. and Wald, A., 2019. The dynamics of financial information and non-

financial environmental, social and governance information in the strategic decision-

making process. Journal of Strategy and Management.

Rasheed, R. and Siddiqui, S.H., 2019. Attitude for inclusive finance: influence of owner-

managers’ and firms’ characteristics on SMEs financial decision making. Journal of

Economic and Administrative Sciences.

Vitale, C. and Cull, M., 2018. Modelling the influence of CEO values and leadership styles on

financial decision making. The Journal of New Business Ideas & Trends, 16(1), pp.16-

30.

Venter, E.R., Gordon, E.A. and Street, D.L., 2018. The role of accounting and the accountancy

profession in economic development: A research agenda. Journal of International

Financial Management & Accounting, 29(2), pp.195-218.

Eberhardt, W., de Bruin, W.B. and Strough, J., 2019. Age differences in financial decision

making: The benefits of more experience and less negative emotions. Journal of

behavioral decision making, 32(1), pp.79-93.

Petersen, J.A., Kushwaha, T. and Kumar, V., 2015. Marketing communication strategies and

consumer financial decision making: The role of national culture. Journal of

Marketing, 79(1), pp.44-63.

Yue, P., Gizem Korkmaz, A. and Zhou, H., 2020. Household financial decision making amidst

the COVID-19 pandemic. Emerging Markets Finance and Trade, 56(10), pp.2363-

2377.

Cook, L.A. and Sadeghein, R., 2018. Effects of perceived scarcity on financial decision

making. Journal of Public Policy & Marketing, 37(1), pp.68-87.

11

Books and Journals:

Klačmer Čalopa, M., 2017. Business owner and manager’s attitudes towards financial decision-

making and strategic planning: Evidence from Croatian SMEs. Management: journal of

contemporary management issues, 22(1), pp.103-116.

Ziolo, M., Filipiak, B.Z., Bąk, I. and Cheba, K., 2019. How to design more sustainable financial

systems: the roles of environmental, social, and governance factors in the decision-

making process. Sustainability, 11(20), p.5604.

Esch, M., Schulze, M. and Wald, A., 2019. The dynamics of financial information and non-

financial environmental, social and governance information in the strategic decision-

making process. Journal of Strategy and Management.

Rasheed, R. and Siddiqui, S.H., 2019. Attitude for inclusive finance: influence of owner-

managers’ and firms’ characteristics on SMEs financial decision making. Journal of

Economic and Administrative Sciences.

Vitale, C. and Cull, M., 2018. Modelling the influence of CEO values and leadership styles on

financial decision making. The Journal of New Business Ideas & Trends, 16(1), pp.16-

30.

Venter, E.R., Gordon, E.A. and Street, D.L., 2018. The role of accounting and the accountancy

profession in economic development: A research agenda. Journal of International

Financial Management & Accounting, 29(2), pp.195-218.

Eberhardt, W., de Bruin, W.B. and Strough, J., 2019. Age differences in financial decision

making: The benefits of more experience and less negative emotions. Journal of

behavioral decision making, 32(1), pp.79-93.

Petersen, J.A., Kushwaha, T. and Kumar, V., 2015. Marketing communication strategies and

consumer financial decision making: The role of national culture. Journal of

Marketing, 79(1), pp.44-63.

Yue, P., Gizem Korkmaz, A. and Zhou, H., 2020. Household financial decision making amidst

the COVID-19 pandemic. Emerging Markets Finance and Trade, 56(10), pp.2363-

2377.

Cook, L.A. and Sadeghein, R., 2018. Effects of perceived scarcity on financial decision

making. Journal of Public Policy & Marketing, 37(1), pp.68-87.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.