Financial Decision Making Report: Comprehensive Skanska Plc Analysis

VerifiedAdded on 2023/01/03

|11

|3397

|53

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making within Skanska Plc, a UK-based construction company. It begins with an overview of financial and accounting activities, emphasizing their importance in achieving organizational goals and making informed decisions. The report then delves into the specific responsibilities and tasks associated with financial management, including final accounts generation, performance assessment, regulatory compliance, and strategic decision-making. Furthermore, the study computes and analyzes various financial ratios, such as return on capital employed, net profit margin, current ratio, and debt collection periods, to evaluate Skanska Plc's financial performance. The analysis reveals trends in financial metrics, offering insights into the company's efficiency and suggesting areas for improvement. The report concludes with a discussion on the implications of the findings, highlighting the significance of financial management in driving business success and the need for strategic planning to enhance performance.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

Detailed analysis of the meaning, responsibilities and tasks of the organisation of financial and

accounting activities....................................................................................................................3

TASK 2............................................................................................................................................6

Computation of various ratios of Skanska Plc.............................................................................6

Comment on the performance.....................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

Detailed analysis of the meaning, responsibilities and tasks of the organisation of financial and

accounting activities....................................................................................................................3

TASK 2............................................................................................................................................6

Computation of various ratios of Skanska Plc.............................................................................6

Comment on the performance.....................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Introduction

It is similarly actual important among all financial management to confirm they are capable

of making successful decisions as well as to identify financial decisions mostly as mechanism

which will rely on the development of multiple potential decisions. Financial control is very

important for businesses to ensure that they evaluate each and almost every part of company

financial action while preparing to make changes in their results. It is the determination of

straight the creation of highly effective upcoming proposal of the organization. In accomplishing

the long-term economic targets and benefit of higher wages, for firms to ensure this strategy is

achieved in a systemic way, greater sales (Barth, Papageorge and Thom, 2017). The present

study focuses through an overview of Skanska Plc, a building business based primarily in the

UK. It remained established in 1984 in addition to has remained running methodically. This role

addresses multiple aspects grounded scheduled the entity. These are essential to the

organization's financial accounting functions, activities and responsibilities. In addition, to assess

the company's results, different metrics are measured and in this article, an overview of the

results is included to provide recommendations to investors on investing.

TASK 1

Detailed analysis of the meaning, responsibilities and tasks of the organisation of financial and

accounting activities

It is really relevant to any and all companies, such as Skanska, to ensure that they all pay

more attention to that same decision-making process. Each of the corporation's executive

committee is required to design a company paper, focusing on the measurement and funding of

the organization's financial accounts, tasks and responsibilities. In terms of entity, both of them

are confirmed in this study below:

Accounting and financial activities: they are the primary reporting and control tasks that all

companies must undertake to effectively achieve potential objectives (Chen, 2018). The Finance

Group in Skanska Plc concentrates mostly on following requirements:

Final accounts generation: The primary transparency and financial features. It

would be very hard to evaluate if the actions made in recent years have produced

good or negative outcomes if the company cannot publish financial statements.

Throughout this feature, there have been 3 main types with final accounts. This

It is similarly actual important among all financial management to confirm they are capable

of making successful decisions as well as to identify financial decisions mostly as mechanism

which will rely on the development of multiple potential decisions. Financial control is very

important for businesses to ensure that they evaluate each and almost every part of company

financial action while preparing to make changes in their results. It is the determination of

straight the creation of highly effective upcoming proposal of the organization. In accomplishing

the long-term economic targets and benefit of higher wages, for firms to ensure this strategy is

achieved in a systemic way, greater sales (Barth, Papageorge and Thom, 2017). The present

study focuses through an overview of Skanska Plc, a building business based primarily in the

UK. It remained established in 1984 in addition to has remained running methodically. This role

addresses multiple aspects grounded scheduled the entity. These are essential to the

organization's financial accounting functions, activities and responsibilities. In addition, to assess

the company's results, different metrics are measured and in this article, an overview of the

results is included to provide recommendations to investors on investing.

TASK 1

Detailed analysis of the meaning, responsibilities and tasks of the organisation of financial and

accounting activities

It is really relevant to any and all companies, such as Skanska, to ensure that they all pay

more attention to that same decision-making process. Each of the corporation's executive

committee is required to design a company paper, focusing on the measurement and funding of

the organization's financial accounts, tasks and responsibilities. In terms of entity, both of them

are confirmed in this study below:

Accounting and financial activities: they are the primary reporting and control tasks that all

companies must undertake to effectively achieve potential objectives (Chen, 2018). The Finance

Group in Skanska Plc concentrates mostly on following requirements:

Final accounts generation: The primary transparency and financial features. It

would be very hard to evaluate if the actions made in recent years have produced

good or negative outcomes if the company cannot publish financial statements.

Throughout this feature, there have been 3 main types with final accounts. This

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provides a statement on gains and expenses, balance sheets and cash flow. All

will help to assess not whether the business can achieve its monetary goals.

Mostly with aid of them who benefit future judgement and the execution of

challenging activities, the sustainability, the profitability, the true role etc. may be

calculated. It is really essential to be oriented; as it lets the company retain

accurate records on all operations.

Performance assessment: This is among the key accounting and financial features.

This helps one to evaluate the good or negative results of the methods that have

already been developed, which makes it quite applicable for the business. If the

company cannot measure its actual outcomes, it may be quite stable to regulate

whether or not possible expectations are extended. Analysis of the present

condition will also assist in predicting the adverse effects of any efforts taken in

the potential. If Skanska Plc's management is unable to achieve however it is very

hard for customers, lenders and so on to fulfil their demands.

Observance of the rules: it is also very essential for the accounting department to

ensure consistency with all laws when drawing up final reports, and it will afford

to disregard legal impairments. It cannot work systematically in Skanska to play

this task; it will be really hard to guarantee the prejudice in financial declarations.

Unless the standards are followed, the accountability and exactness of the

financial reports can also be impaired. For the company, this role is critical to

disregard any legal impairment in operations as well as other financial enterprises

(Eberhardt, de Bruin and Strough, 2019).

The formulation of major choices based on current situation: this financial and

accounting role notes that the formulation of major choices as per the current

situation of the organisation is from the utmost significance for all companies

such as Skanska. It would improve productivity and accomplish future goals. For

the organisation to expand, administrators or management may need to perform

the role when they are driven to reach their long goals.

Accounting and finance tasks: There are numerous duties relevant to the

department of finance and accounting. They should all be Skanska-focused as it

will help to reach all potential goals:

will help to assess not whether the business can achieve its monetary goals.

Mostly with aid of them who benefit future judgement and the execution of

challenging activities, the sustainability, the profitability, the true role etc. may be

calculated. It is really essential to be oriented; as it lets the company retain

accurate records on all operations.

Performance assessment: This is among the key accounting and financial features.

This helps one to evaluate the good or negative results of the methods that have

already been developed, which makes it quite applicable for the business. If the

company cannot measure its actual outcomes, it may be quite stable to regulate

whether or not possible expectations are extended. Analysis of the present

condition will also assist in predicting the adverse effects of any efforts taken in

the potential. If Skanska Plc's management is unable to achieve however it is very

hard for customers, lenders and so on to fulfil their demands.

Observance of the rules: it is also very essential for the accounting department to

ensure consistency with all laws when drawing up final reports, and it will afford

to disregard legal impairments. It cannot work systematically in Skanska to play

this task; it will be really hard to guarantee the prejudice in financial declarations.

Unless the standards are followed, the accountability and exactness of the

financial reports can also be impaired. For the company, this role is critical to

disregard any legal impairment in operations as well as other financial enterprises

(Eberhardt, de Bruin and Strough, 2019).

The formulation of major choices based on current situation: this financial and

accounting role notes that the formulation of major choices as per the current

situation of the organisation is from the utmost significance for all companies

such as Skanska. It would improve productivity and accomplish future goals. For

the organisation to expand, administrators or management may need to perform

the role when they are driven to reach their long goals.

Accounting and finance tasks: There are numerous duties relevant to the

department of finance and accounting. They should all be Skanska-focused as it

will help to reach all potential goals:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Future expense and income forecasting: it is among the key financial and transparency

activities that must be targeted more by Skanska auditors, as it will assist them in

assessing all future expenses. It would allow them to be able to face everything and have

their funds apart to meet them adequately. In addition, sales may also be calculated using

the accountancy to build potential budgets (Greenberg and Hershfield, 2019).

Routinely carrying out all operations: this task is to be applied in systematic fashion to

the financial accounting services of the company. Sufficiency may be allocated to all

teams required for implementing the operations by allocating appropriate funds. Skanska

Plc can help ensure that all its potential targets, including higher earnings and sales,

highly happy consumers etc., are accomplished.

Compliance with the organisational specifications: it is necessary for all organisations to

fulfil all specifications to carrying out certain operations correctly. One is financing, that

is an oversight and finance responsibility. This will help manager meet all lengthy goals

if it is handled correctly. It is among the biggest tasks and it would be very hard to carry

out the activities and to reach potential goals and targets if this is not cantered. To breach

damage in the future, it would be very relevant for managers to actually listen towards

this role (Hershfield, John and Reiff, 2018).

Accounting and finance positions: ensuring that all companies pay more attention to their

operational and finance positions such that financial operations are routinely carried out is

extremely important. A few of the major business and audit functions are discussed as follows:

Report both sales and expenditures: This principal functions of accounts and finance is to

record reports on revenue and expenses that exist throughout the year. The study of the

potential payment of all its costs, by means of income produced during the year, could be

beneficial for the company such as Skanska. It will be very hard to complete future

objectives unless the evidence is not systemtically registered. (Hirshleifer, Jian and

Zhang, 2018).

Managing money balance: Financial management have a duty to manage every working

capital such that the true cash flow as well as outflow can be calculated during the

financial statement. It would be very impossible to maintain that potential targets in

Skanska Plc can be completed effectively if managements are not capable of controlling

activities that must be targeted more by Skanska auditors, as it will assist them in

assessing all future expenses. It would allow them to be able to face everything and have

their funds apart to meet them adequately. In addition, sales may also be calculated using

the accountancy to build potential budgets (Greenberg and Hershfield, 2019).

Routinely carrying out all operations: this task is to be applied in systematic fashion to

the financial accounting services of the company. Sufficiency may be allocated to all

teams required for implementing the operations by allocating appropriate funds. Skanska

Plc can help ensure that all its potential targets, including higher earnings and sales,

highly happy consumers etc., are accomplished.

Compliance with the organisational specifications: it is necessary for all organisations to

fulfil all specifications to carrying out certain operations correctly. One is financing, that

is an oversight and finance responsibility. This will help manager meet all lengthy goals

if it is handled correctly. It is among the biggest tasks and it would be very hard to carry

out the activities and to reach potential goals and targets if this is not cantered. To breach

damage in the future, it would be very relevant for managers to actually listen towards

this role (Hershfield, John and Reiff, 2018).

Accounting and finance positions: ensuring that all companies pay more attention to their

operational and finance positions such that financial operations are routinely carried out is

extremely important. A few of the major business and audit functions are discussed as follows:

Report both sales and expenditures: This principal functions of accounts and finance is to

record reports on revenue and expenses that exist throughout the year. The study of the

potential payment of all its costs, by means of income produced during the year, could be

beneficial for the company such as Skanska. It will be very hard to complete future

objectives unless the evidence is not systemtically registered. (Hirshleifer, Jian and

Zhang, 2018).

Managing money balance: Financial management have a duty to manage every working

capital such that the true cash flow as well as outflow can be calculated during the

financial statement. It would be very impossible to maintain that potential targets in

Skanska Plc can be completed effectively if managements are not capable of controlling

the flow of capital. This is one of the principal functions that can continue to coordinate

all the company's operations and can accomplish all long-term objectives.

Accountability: Its accounting and financial function sets out that the company can

produce all reports of revenue and expenditures so they are capable of helping to

accomplish future goals. In the assistance of individuals and teams, the current role of the

company can be understood and future decisions made. For the managers the financial

division of Skanska, this task is very critical as it will assist them to secure the success

efforts of the company succeed.

The debate is based on the study of multiple forms of accounts, responsibilities and financial

positions at Skanska Plc. They all play an essential part for the firm in addition to they resolve

help achieve all possible goals, like management, financial condition, higher earnings and

incomes. It would be very difficult for management to respond to the advancement of the

company and its success if they cannot actually listen to them. In Skanska each management

committee takes on most of the tasks, obligations and responsibilities of finance and accounting

because they concentrate more on the creation and success of the company (Jetter and Walker,

2017). It is crucial for the accounting department to ensure that all rules are followed when

reviewing the final reports and it will help to avoid legal interventions. It cannot work

systematically in Skanska to play this task; it will be very hard to guarantee the prejudice in

financial declarations. If the requirements are monitored, the transparency and exactness of the

financial documents can also be impaired. This purpose is right useful for the industry to

disregard some sort of legal inference in activities as well as other practices of company.

TASK 2

Computation of various ratios of Skanska Plc

Ratio analysis may be described as an examination of that same corporation's current

financial situation in order to assess its actual results. It is also very hard to make potential

decisions unless the organisations are unable to evaluate the current position. The managers

throughout Skanska Plc measure various kinds of ratios that administrators use to assess the

current market situation. The formulas together with the proportion definition are the following:

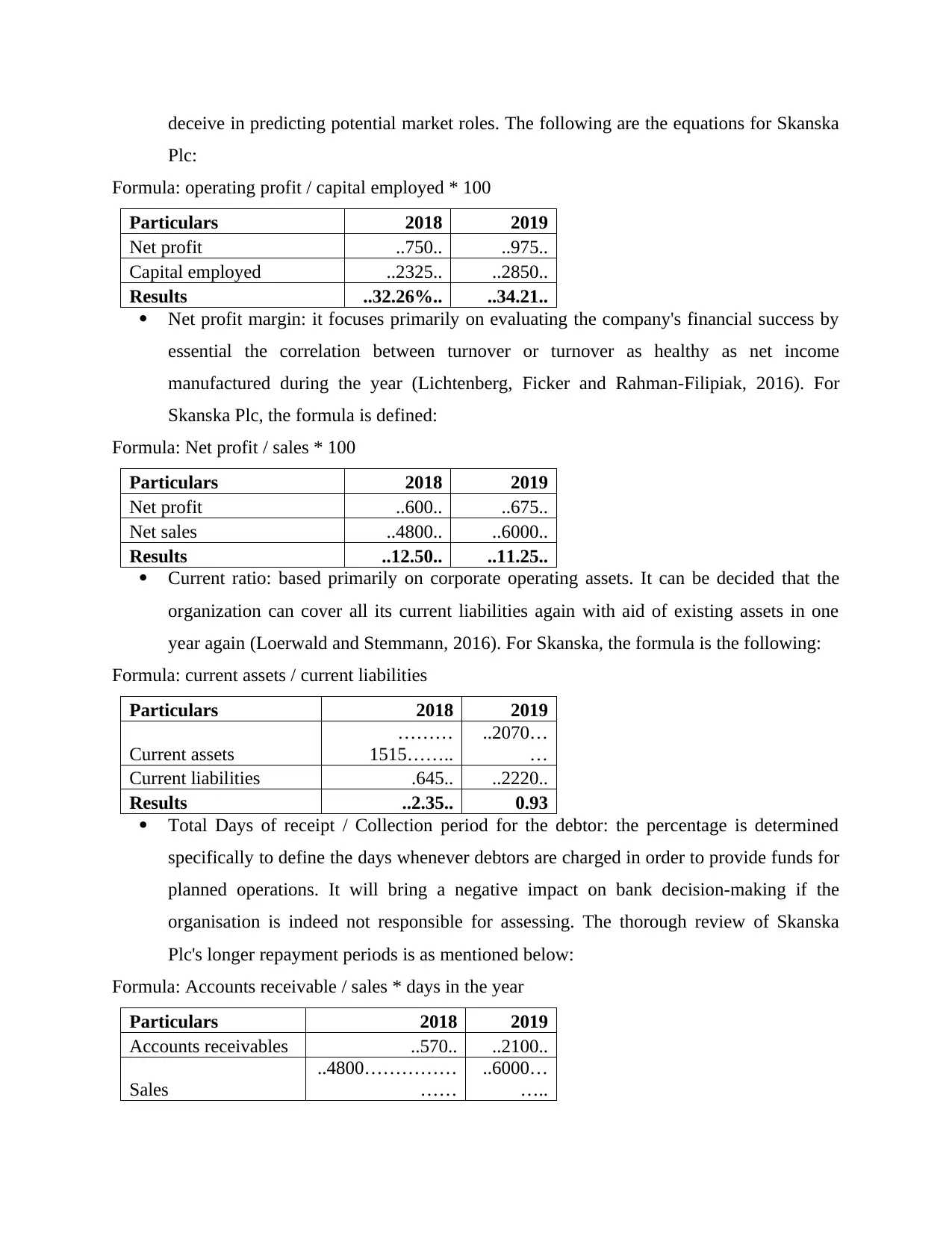

Return on capital employed: This is used principally to receive money and to determine

company capital performance. If it is not correctly measured, the management will

all the company's operations and can accomplish all long-term objectives.

Accountability: Its accounting and financial function sets out that the company can

produce all reports of revenue and expenditures so they are capable of helping to

accomplish future goals. In the assistance of individuals and teams, the current role of the

company can be understood and future decisions made. For the managers the financial

division of Skanska, this task is very critical as it will assist them to secure the success

efforts of the company succeed.

The debate is based on the study of multiple forms of accounts, responsibilities and financial

positions at Skanska Plc. They all play an essential part for the firm in addition to they resolve

help achieve all possible goals, like management, financial condition, higher earnings and

incomes. It would be very difficult for management to respond to the advancement of the

company and its success if they cannot actually listen to them. In Skanska each management

committee takes on most of the tasks, obligations and responsibilities of finance and accounting

because they concentrate more on the creation and success of the company (Jetter and Walker,

2017). It is crucial for the accounting department to ensure that all rules are followed when

reviewing the final reports and it will help to avoid legal interventions. It cannot work

systematically in Skanska to play this task; it will be very hard to guarantee the prejudice in

financial declarations. If the requirements are monitored, the transparency and exactness of the

financial documents can also be impaired. This purpose is right useful for the industry to

disregard some sort of legal inference in activities as well as other practices of company.

TASK 2

Computation of various ratios of Skanska Plc

Ratio analysis may be described as an examination of that same corporation's current

financial situation in order to assess its actual results. It is also very hard to make potential

decisions unless the organisations are unable to evaluate the current position. The managers

throughout Skanska Plc measure various kinds of ratios that administrators use to assess the

current market situation. The formulas together with the proportion definition are the following:

Return on capital employed: This is used principally to receive money and to determine

company capital performance. If it is not correctly measured, the management will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

deceive in predicting potential market roles. The following are the equations for Skanska

Plc:

Formula: operating profit / capital employed * 100

Particulars 2018 2019

Net profit ..750.. ..975..

Capital employed ..2325.. ..2850..

Results ..32.26%.. ..34.21..

Net profit margin: it focuses primarily on evaluating the company's financial success by

essential the correlation between turnover or turnover as healthy as net income

manufactured during the year (Lichtenberg, Ficker and Rahman-Filipiak, 2016). For

Skanska Plc, the formula is defined:

Formula: Net profit / sales * 100

Particulars 2018 2019

Net profit ..600.. ..675..

Net sales ..4800.. ..6000..

Results ..12.50.. ..11.25..

Current ratio: based primarily on corporate operating assets. It can be decided that the

organization can cover all its current liabilities again with aid of existing assets in one

year again (Loerwald and Stemmann, 2016). For Skanska, the formula is the following:

Formula: current assets / current liabilities

Particulars 2018 2019

Current assets

………

1515……..

..2070…

…

Current liabilities .645.. ..2220..

Results ..2.35.. 0.93

Total Days of receipt / Collection period for the debtor: the percentage is determined

specifically to define the days whenever debtors are charged in order to provide funds for

planned operations. It will bring a negative impact on bank decision-making if the

organisation is indeed not responsible for assessing. The thorough review of Skanska

Plc's longer repayment periods is as mentioned below:

Formula: Accounts receivable / sales * days in the year

Particulars 2018 2019

Accounts receivables ..570.. ..2100..

Sales

..4800……………

……

..6000…

…..

Plc:

Formula: operating profit / capital employed * 100

Particulars 2018 2019

Net profit ..750.. ..975..

Capital employed ..2325.. ..2850..

Results ..32.26%.. ..34.21..

Net profit margin: it focuses primarily on evaluating the company's financial success by

essential the correlation between turnover or turnover as healthy as net income

manufactured during the year (Lichtenberg, Ficker and Rahman-Filipiak, 2016). For

Skanska Plc, the formula is defined:

Formula: Net profit / sales * 100

Particulars 2018 2019

Net profit ..600.. ..675..

Net sales ..4800.. ..6000..

Results ..12.50.. ..11.25..

Current ratio: based primarily on corporate operating assets. It can be decided that the

organization can cover all its current liabilities again with aid of existing assets in one

year again (Loerwald and Stemmann, 2016). For Skanska, the formula is the following:

Formula: current assets / current liabilities

Particulars 2018 2019

Current assets

………

1515……..

..2070…

…

Current liabilities .645.. ..2220..

Results ..2.35.. 0.93

Total Days of receipt / Collection period for the debtor: the percentage is determined

specifically to define the days whenever debtors are charged in order to provide funds for

planned operations. It will bring a negative impact on bank decision-making if the

organisation is indeed not responsible for assessing. The thorough review of Skanska

Plc's longer repayment periods is as mentioned below:

Formula: Accounts receivable / sales * days in the year

Particulars 2018 2019

Accounts receivables ..570.. ..2100..

Sales

..4800……………

……

..6000…

…..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

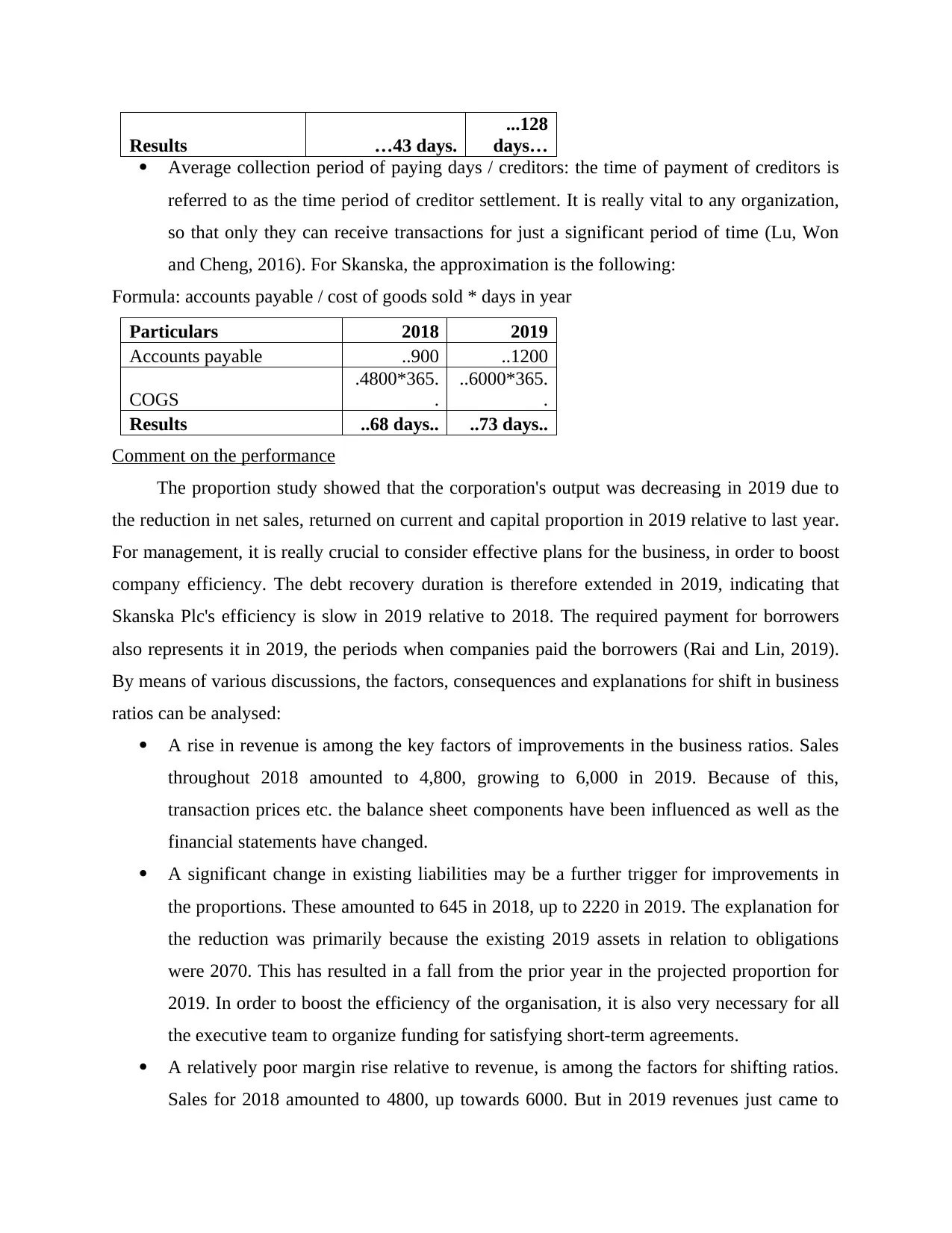

Results …43 days.

...128

days…

Average collection period of paying days / creditors: the time of payment of creditors is

referred to as the time period of creditor settlement. It is really vital to any organization,

so that only they can receive transactions for just a significant period of time (Lu, Won

and Cheng, 2016). For Skanska, the approximation is the following:

Formula: accounts payable / cost of goods sold * days in year

Particulars 2018 2019

Accounts payable ..900 ..1200

COGS

.4800*365.

.

..6000*365.

.

Results ..68 days.. ..73 days..

Comment on the performance

The proportion study showed that the corporation's output was decreasing in 2019 due to

the reduction in net sales, returned on current and capital proportion in 2019 relative to last year.

For management, it is really crucial to consider effective plans for the business, in order to boost

company efficiency. The debt recovery duration is therefore extended in 2019, indicating that

Skanska Plc's efficiency is slow in 2019 relative to 2018. The required payment for borrowers

also represents it in 2019, the periods when companies paid the borrowers (Rai and Lin, 2019).

By means of various discussions, the factors, consequences and explanations for shift in business

ratios can be analysed:

A rise in revenue is among the key factors of improvements in the business ratios. Sales

throughout 2018 amounted to 4,800, growing to 6,000 in 2019. Because of this,

transaction prices etc. the balance sheet components have been influenced as well as the

financial statements have changed.

A significant change in existing liabilities may be a further trigger for improvements in

the proportions. These amounted to 645 in 2018, up to 2220 in 2019. The explanation for

the reduction was primarily because the existing 2019 assets in relation to obligations

were 2070. This has resulted in a fall from the prior year in the projected proportion for

2019. In order to boost the efficiency of the organisation, it is also very necessary for all

the executive team to organize funding for satisfying short-term agreements.

A relatively poor margin rise relative to revenue, is among the factors for shifting ratios.

Sales for 2018 amounted to 4800, up towards 6000. But in 2019 revenues just came to

...128

days…

Average collection period of paying days / creditors: the time of payment of creditors is

referred to as the time period of creditor settlement. It is really vital to any organization,

so that only they can receive transactions for just a significant period of time (Lu, Won

and Cheng, 2016). For Skanska, the approximation is the following:

Formula: accounts payable / cost of goods sold * days in year

Particulars 2018 2019

Accounts payable ..900 ..1200

COGS

.4800*365.

.

..6000*365.

.

Results ..68 days.. ..73 days..

Comment on the performance

The proportion study showed that the corporation's output was decreasing in 2019 due to

the reduction in net sales, returned on current and capital proportion in 2019 relative to last year.

For management, it is really crucial to consider effective plans for the business, in order to boost

company efficiency. The debt recovery duration is therefore extended in 2019, indicating that

Skanska Plc's efficiency is slow in 2019 relative to 2018. The required payment for borrowers

also represents it in 2019, the periods when companies paid the borrowers (Rai and Lin, 2019).

By means of various discussions, the factors, consequences and explanations for shift in business

ratios can be analysed:

A rise in revenue is among the key factors of improvements in the business ratios. Sales

throughout 2018 amounted to 4,800, growing to 6,000 in 2019. Because of this,

transaction prices etc. the balance sheet components have been influenced as well as the

financial statements have changed.

A significant change in existing liabilities may be a further trigger for improvements in

the proportions. These amounted to 645 in 2018, up to 2220 in 2019. The explanation for

the reduction was primarily because the existing 2019 assets in relation to obligations

were 2070. This has resulted in a fall from the prior year in the projected proportion for

2019. In order to boost the efficiency of the organisation, it is also very necessary for all

the executive team to organize funding for satisfying short-term agreements.

A relatively poor margin rise relative to revenue, is among the factors for shifting ratios.

Sales for 2018 amounted to 4800, up towards 6000. But in 2019 revenues just came to

75. As a result the organization's performance has been impaired and has declined in

comparison with last year.

Adjustments to the accounting ratios have a huge influence on the company's financial

condition. Since the organization's success in 2019 is not strong compared with 2018,

business funding is very challenging. As a result, future investors' appetite will be

diminished. Furthermore the gradual deterioration in financial results has negative

implications for revenue, earnings and profit margins as well. It would be very necessary

for Skanska Plc to make successful future actions throughout order to boost its money

position.

Investor's Recommendation: Based on Skanska Plc ratio research, it was calculated that future

buyers that are position to finance 1 million pounds in the business will not next year spend the

capital in the enterprise. A development in Skanska must be planned by the shareholder for 2 or

three years, but his success should be analysed (Serrano-Silva, Villuenda-Rey and Yáñez-

Márquez 2018). These will give the researcher larger expected returns if it is successful. The

investor would raise the likelihood of poor returns on each capital that is spent by doing this

investment in 2012.

CONCLUSION

From this concept analysis, financial decision-making was inferred as the implementation

mechanism to make rational management choices in order to meet the financing aims and

outcomes effectively. It would be incredibly difficult for management to accomplish future aims

and objectives if they cannot make successful choices for this next timeline. There remain altered

answerability and investment tasks, tasks and responsibilities that all businesses essential to

essence on. Some of them appear to be closing intelligences, performance assessment, obedience

with all law and possible actions depending on the present situation. Besides all this, it is also a

matter of finance and business responsibilities and commitments to estimate future expenses and

profits, to carry out all activities systematically, to fulfil company criteria, to monitor the transfer

of cash, and to retain accounts, etc. There were various types of proportion determined when

planning for an entity to set its economic viability. Some include returns on employed money,

net profit, current cost, average for account receivables and receivables. It is convenient for

management to evaluate whether or not company is experiencing success by measuring both of

comparison with last year.

Adjustments to the accounting ratios have a huge influence on the company's financial

condition. Since the organization's success in 2019 is not strong compared with 2018,

business funding is very challenging. As a result, future investors' appetite will be

diminished. Furthermore the gradual deterioration in financial results has negative

implications for revenue, earnings and profit margins as well. It would be very necessary

for Skanska Plc to make successful future actions throughout order to boost its money

position.

Investor's Recommendation: Based on Skanska Plc ratio research, it was calculated that future

buyers that are position to finance 1 million pounds in the business will not next year spend the

capital in the enterprise. A development in Skanska must be planned by the shareholder for 2 or

three years, but his success should be analysed (Serrano-Silva, Villuenda-Rey and Yáñez-

Márquez 2018). These will give the researcher larger expected returns if it is successful. The

investor would raise the likelihood of poor returns on each capital that is spent by doing this

investment in 2012.

CONCLUSION

From this concept analysis, financial decision-making was inferred as the implementation

mechanism to make rational management choices in order to meet the financing aims and

outcomes effectively. It would be incredibly difficult for management to accomplish future aims

and objectives if they cannot make successful choices for this next timeline. There remain altered

answerability and investment tasks, tasks and responsibilities that all businesses essential to

essence on. Some of them appear to be closing intelligences, performance assessment, obedience

with all law and possible actions depending on the present situation. Besides all this, it is also a

matter of finance and business responsibilities and commitments to estimate future expenses and

profits, to carry out all activities systematically, to fulfil company criteria, to monitor the transfer

of cash, and to retain accounts, etc. There were various types of proportion determined when

planning for an entity to set its economic viability. Some include returns on employed money,

net profit, current cost, average for account receivables and receivables. It is convenient for

management to evaluate whether or not company is experiencing success by measuring both of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them. Investors might use the percentages to assess whether or not assets can be spent in the

company.

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Barth, D., Papageorge, N. W. and Thom, K., 2017. Genetic ability, wealth, and financial

decision-making.

Chen, T. Y., 2018. An outranking approach using a risk attitudinal assignment model involving

Pythagorean fuzzy information and its application to financial decision making. Applied

Soft Computing. 71. pp.460-487.

Eberhardt, W., de Bruin, W. B. and Strough, J., 2019. Age differences in financial decision

making: The benefits of more experience and less negative emotions. Journal of

Behavioral Decision Making. 32(1). pp.79-93.

Greenberg, A. E. and Hershfield, H. E., 2019. Financial decision making. Consumer Psychology

Review. 2(1). pp.17-29.

Hershfield, H. E., John, E. M. and Reiff, J. S., 2018. Using vividness interventions to improve

financial decision making. Policy Insights from the Behavioral and Brain Sciences.

5(2). pp.209-215.

Hirshleifer, D., Jian, M. and Zhang, H., 2018. Superstition and financial decision

making. Management Science. 64(1). pp.235-252.

Jetter, M. and Walker, J. K., 2017. Anchoring in financial decision-making: Evidence from

Jeopardy!. Journal of Economic Behavior & Organization. 141. pp.164-176.

Lichtenberg, P. A., Ficker, L. J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of

Elder Abuse & Neglect. 28(1). pp.14-33.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International handbook of

financial literacy (pp. 25-38). Springer, Singapore.

Lu, Q., Won, J. and Cheng, J. C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management. 34(1). pp.3-21.

Rai, D. and Lin, C. W. W., 2019. The influence of implicit self-theories on consumer financial

decision making. Journal of Business Research. 95. pp.316-325.

Serrano-Silva, Y. O., Villuendas-Rey, Y. and Yáñez-Márquez, C., 2018. Automatic feature

weighting for improving financial Decision Support Systems. Decision Support

Systems. 107. pp.78-87.

Books and Journals:

Barth, D., Papageorge, N. W. and Thom, K., 2017. Genetic ability, wealth, and financial

decision-making.

Chen, T. Y., 2018. An outranking approach using a risk attitudinal assignment model involving

Pythagorean fuzzy information and its application to financial decision making. Applied

Soft Computing. 71. pp.460-487.

Eberhardt, W., de Bruin, W. B. and Strough, J., 2019. Age differences in financial decision

making: The benefits of more experience and less negative emotions. Journal of

Behavioral Decision Making. 32(1). pp.79-93.

Greenberg, A. E. and Hershfield, H. E., 2019. Financial decision making. Consumer Psychology

Review. 2(1). pp.17-29.

Hershfield, H. E., John, E. M. and Reiff, J. S., 2018. Using vividness interventions to improve

financial decision making. Policy Insights from the Behavioral and Brain Sciences.

5(2). pp.209-215.

Hirshleifer, D., Jian, M. and Zhang, H., 2018. Superstition and financial decision

making. Management Science. 64(1). pp.235-252.

Jetter, M. and Walker, J. K., 2017. Anchoring in financial decision-making: Evidence from

Jeopardy!. Journal of Economic Behavior & Organization. 141. pp.164-176.

Lichtenberg, P. A., Ficker, L. J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of

Elder Abuse & Neglect. 28(1). pp.14-33.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International handbook of

financial literacy (pp. 25-38). Springer, Singapore.

Lu, Q., Won, J. and Cheng, J. C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management. 34(1). pp.3-21.

Rai, D. and Lin, C. W. W., 2019. The influence of implicit self-theories on consumer financial

decision making. Journal of Business Research. 95. pp.316-325.

Serrano-Silva, Y. O., Villuendas-Rey, Y. and Yáñez-Márquez, C., 2018. Automatic feature

weighting for improving financial Decision Support Systems. Decision Support

Systems. 107. pp.78-87.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.