Financial Analysis Report: Sky Cafe Budget and Variance Analysis

VerifiedAdded on 2021/09/15

|11

|2163

|61

Report

AI Summary

This report provides a comprehensive financial analysis of Sky Cafe's budget, focusing on the month of July. It begins by outlining the objectives of budgeting for the company, including cash flow estimation, resource allocation, scenario modeling, and performance measurement. The report then delves into a detailed analysis of revenue and spending variances, comparing budgeted figures with actual results. Key variances are identified, such as unfavorable revenue variance due to lower sales volume and increased expenses in areas like insurance, fuel, and facility rent. The analysis explores the potential causes of these variances, considering market factors, pricing, and operational efficiency. Finally, the report offers recommendations to Sky Cafe's management to support its corporate objectives, including minimizing the selling price per unit and cutting production costs to improve financial performance and address the identified variances.

Running head: ACCOUNTS AND FINANCE

Accounts and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounts and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTS AND FINANCE

Table of Contents

Introduction:....................................................................................................................................2

Requirement 1:.................................................................................................................................2

Requirement 2:.................................................................................................................................3

Requirement 3:.................................................................................................................................5

Requirement 4:.................................................................................................................................7

Conclusion:......................................................................................................................................7

References:......................................................................................................................................9

Table of Contents

Introduction:....................................................................................................................................2

Requirement 1:.................................................................................................................................2

Requirement 2:.................................................................................................................................3

Requirement 3:.................................................................................................................................5

Requirement 4:.................................................................................................................................7

Conclusion:......................................................................................................................................7

References:......................................................................................................................................9

2ACCOUNTS AND FINANCE

Introduction:

In the current global competitive business environment, any organisation that does not

prepare budget paves the path for a number of financial issues. This idea holds good for all types

of business organisations irrespective of their sizes and ages (Armitage, Webb and Glynn 2016).

On the contrary, an organisation that establishes short-term and long-term business goals through

detailed business plan could develop a roadmap in order to ensure financial success and

expansion opportunities. Budgeting is a procedure involving a series of activities conducted for

preparing a budget. Thus, budget could be defined as a quantitative plan for determining the

activities to be selected for future. The paper would intend to explore the objectives of

developing budget for Sky Cafe. The next section would involve analysis of revenue variance as

well as spending variance of the organisation for July. The next segment would emphasise on

identifying those activity variances needing management concern. Finally, the paper would shed

light on providing recommendations to the organisation so that it could support its objectives

effectively.

Requirement 1:

Sky Cafe is a firm located near an airport engaged in preparing meals for the citizens and

tourists visiting the nation. Hence, it is crucial for the management of Sky Cafe in developing

budget by taking into consideration the following objectives:

Estimation of cash flows:

As Sky Cafe is assumed to be in the growing stage, budget is deemed to be valuable. This

is because the organisation is dependent on seasonal sales. Moreover, this type of organisation

Introduction:

In the current global competitive business environment, any organisation that does not

prepare budget paves the path for a number of financial issues. This idea holds good for all types

of business organisations irrespective of their sizes and ages (Armitage, Webb and Glynn 2016).

On the contrary, an organisation that establishes short-term and long-term business goals through

detailed business plan could develop a roadmap in order to ensure financial success and

expansion opportunities. Budgeting is a procedure involving a series of activities conducted for

preparing a budget. Thus, budget could be defined as a quantitative plan for determining the

activities to be selected for future. The paper would intend to explore the objectives of

developing budget for Sky Cafe. The next section would involve analysis of revenue variance as

well as spending variance of the organisation for July. The next segment would emphasise on

identifying those activity variances needing management concern. Finally, the paper would shed

light on providing recommendations to the organisation so that it could support its objectives

effectively.

Requirement 1:

Sky Cafe is a firm located near an airport engaged in preparing meals for the citizens and

tourists visiting the nation. Hence, it is crucial for the management of Sky Cafe in developing

budget by taking into consideration the following objectives:

Estimation of cash flows:

As Sky Cafe is assumed to be in the growing stage, budget is deemed to be valuable. This

is because the organisation is dependent on seasonal sales. Moreover, this type of organisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTS AND FINANCE

faces issues in predicting the amount of likely cash needed in future and this might result in

periodic cash crises (Ax and Greve 2017). With the help of budget, it becomes easy to estimate

cash flows, which is considered as a reasonable budgeting goal.

Allocation of resources:

Sky Cafe could use the budgeting process as a method for determining the areas, in which

the funds would be allocated to different activities like purchase of fixed assets. With the help of

a suitable objective, it needs to be combined with capacity constraint analysis for ascertaining the

areas of resource allocation (Fullerton, Kennedy and Widener 2014).

Modelling scenarios:

When there are a number of alternatives for any organisation, a set of budgets could be

created based on varied scenarios for predicting the financial outcomes of the strategic

directions. However, Sky Cafe need not be overly optimistic while inputting assumptions in the

budget model for avoiding unlikely outcomes.

Measurement of performance:

Sky Cafe could prepare budget for using the same as a base in order to judge staff

performance with the help of budgetary variances. However, constant monitoring is needed for

this objective, as the staffs try to alter budget by making their personal goals easy for

accomplishment (Langfield-Smith et al. 2017).

faces issues in predicting the amount of likely cash needed in future and this might result in

periodic cash crises (Ax and Greve 2017). With the help of budget, it becomes easy to estimate

cash flows, which is considered as a reasonable budgeting goal.

Allocation of resources:

Sky Cafe could use the budgeting process as a method for determining the areas, in which

the funds would be allocated to different activities like purchase of fixed assets. With the help of

a suitable objective, it needs to be combined with capacity constraint analysis for ascertaining the

areas of resource allocation (Fullerton, Kennedy and Widener 2014).

Modelling scenarios:

When there are a number of alternatives for any organisation, a set of budgets could be

created based on varied scenarios for predicting the financial outcomes of the strategic

directions. However, Sky Cafe need not be overly optimistic while inputting assumptions in the

budget model for avoiding unlikely outcomes.

Measurement of performance:

Sky Cafe could prepare budget for using the same as a base in order to judge staff

performance with the help of budgetary variances. However, constant monitoring is needed for

this objective, as the staffs try to alter budget by making their personal goals easy for

accomplishment (Langfield-Smith et al. 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTS AND FINANCE

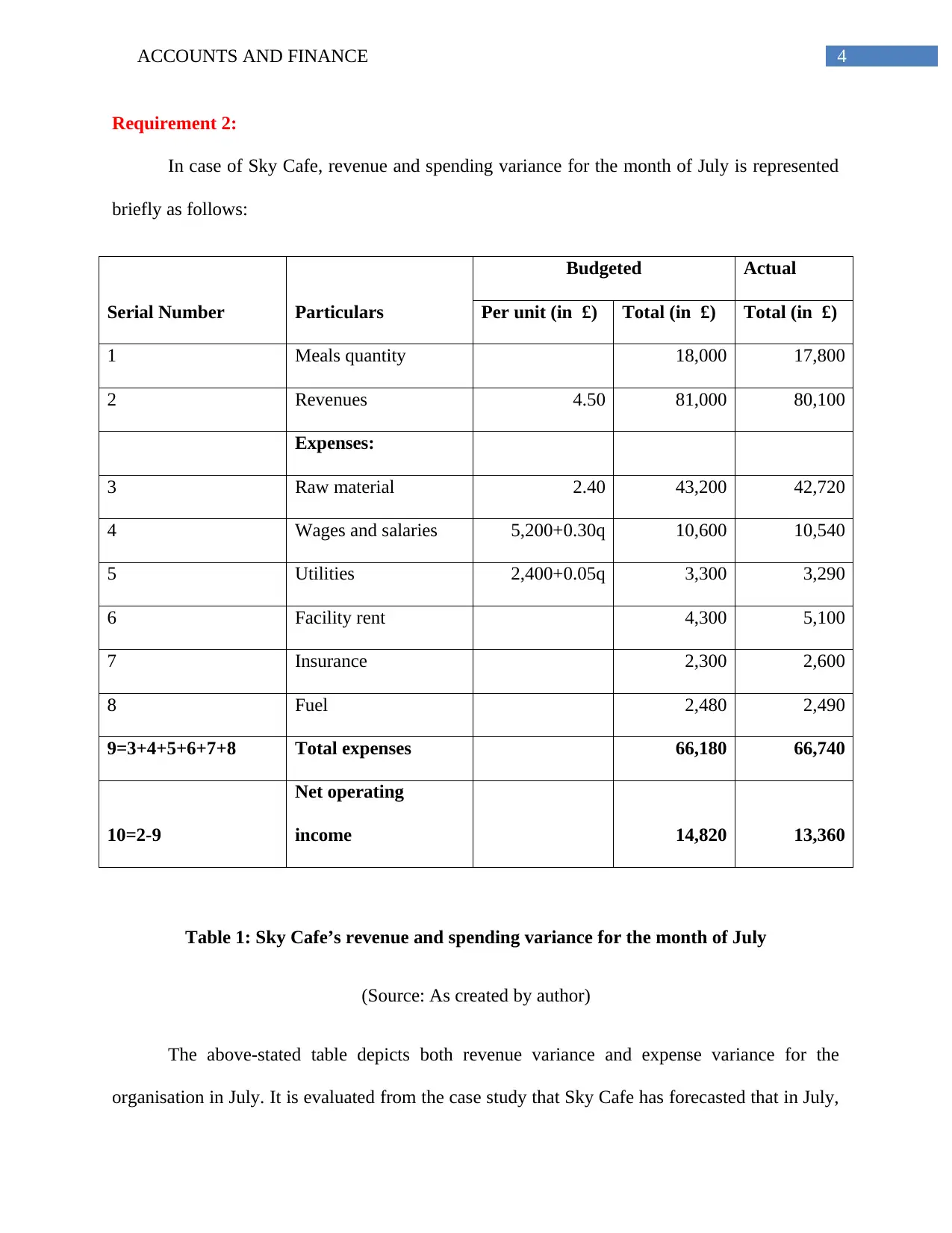

Requirement 2:

In case of Sky Cafe, revenue and spending variance for the month of July is represented

briefly as follows:

Serial Number Particulars

Budgeted Actual

Per unit (in £) Total (in £) Total (in £)

1 Meals quantity 18,000 17,800

2 Revenues 4.50 81,000 80,100

Expenses:

3 Raw material 2.40 43,200 42,720

4 Wages and salaries 5,200+0.30q 10,600 10,540

5 Utilities 2,400+0.05q 3,300 3,290

6 Facility rent 4,300 5,100

7 Insurance 2,300 2,600

8 Fuel 2,480 2,490

9=3+4+5+6+7+8 Total expenses 66,180 66,740

10=2-9

Net operating

income 14,820 13,360

Table 1: Sky Cafe’s revenue and spending variance for the month of July

(Source: As created by author)

The above-stated table depicts both revenue variance and expense variance for the

organisation in July. It is evaluated from the case study that Sky Cafe has forecasted that in July,

Requirement 2:

In case of Sky Cafe, revenue and spending variance for the month of July is represented

briefly as follows:

Serial Number Particulars

Budgeted Actual

Per unit (in £) Total (in £) Total (in £)

1 Meals quantity 18,000 17,800

2 Revenues 4.50 81,000 80,100

Expenses:

3 Raw material 2.40 43,200 42,720

4 Wages and salaries 5,200+0.30q 10,600 10,540

5 Utilities 2,400+0.05q 3,300 3,290

6 Facility rent 4,300 5,100

7 Insurance 2,300 2,600

8 Fuel 2,480 2,490

9=3+4+5+6+7+8 Total expenses 66,180 66,740

10=2-9

Net operating

income 14,820 13,360

Table 1: Sky Cafe’s revenue and spending variance for the month of July

(Source: As created by author)

The above-stated table depicts both revenue variance and expense variance for the

organisation in July. It is evaluated from the case study that Sky Cafe has forecasted that in July,

5ACCOUNTS AND FINANCE

it would be able to sell 18,000 meals. There would not be any change in the selling price per

meal; however, the actual sales volume declined to 17,800 meals. Due to this, the revenue

generated has been lower by £900 compared to the estimated figure. This is considered to be the

revenue variance for the organisation. As remarked by Lavia López and Hiebl (2014), favourable

revenue variance takes place at the time actual revenues are more than budgeted revenues and

vice-versa in case of unfavourable revenue variance. The main reason that this variance occurs is

due to the difference between budgeted amount and actual selling prices, sales volume or a

combination of both.

Based on the provided information, it is evident that Sky Cafe has neither increased nor

decreased its actual selling price for each meal. However, the actual sales volume has fallen short

by 200 meals in comparison to the budgeted figures. As a result, an unfavourable revenue

variance of £900 could be observed in the month of July for the organisation.

In the words of Messner (2016), spending variance usually occurs due to the difference

between the expectations of the management in paying for a product and the amount actually

incurred for that product. However, it is to be borne in mind that the actual expenses rarely

match with the forecasted expenses identically. There always remains a slight variance between

the estimated figure and the actual figure. In case of Sky Cafe, the estimated spending figure has

been lower than the actual spending figure by £560. This is not favourable for the organisation,

as it has to incur higher amounts for maintaining its business expenses. Moreover, the revenue

margin for the month has fallen as well and hence, the situation has worsened further for Sky

Cafe in the same month.

it would be able to sell 18,000 meals. There would not be any change in the selling price per

meal; however, the actual sales volume declined to 17,800 meals. Due to this, the revenue

generated has been lower by £900 compared to the estimated figure. This is considered to be the

revenue variance for the organisation. As remarked by Lavia López and Hiebl (2014), favourable

revenue variance takes place at the time actual revenues are more than budgeted revenues and

vice-versa in case of unfavourable revenue variance. The main reason that this variance occurs is

due to the difference between budgeted amount and actual selling prices, sales volume or a

combination of both.

Based on the provided information, it is evident that Sky Cafe has neither increased nor

decreased its actual selling price for each meal. However, the actual sales volume has fallen short

by 200 meals in comparison to the budgeted figures. As a result, an unfavourable revenue

variance of £900 could be observed in the month of July for the organisation.

In the words of Messner (2016), spending variance usually occurs due to the difference

between the expectations of the management in paying for a product and the amount actually

incurred for that product. However, it is to be borne in mind that the actual expenses rarely

match with the forecasted expenses identically. There always remains a slight variance between

the estimated figure and the actual figure. In case of Sky Cafe, the estimated spending figure has

been lower than the actual spending figure by £560. This is not favourable for the organisation,

as it has to incur higher amounts for maintaining its business expenses. Moreover, the revenue

margin for the month has fallen as well and hence, the situation has worsened further for Sky

Cafe in the same month.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTS AND FINANCE

Requirement 3:

There are certain activities identified having unfavourable variances and these activities

require proper management concern in the context of Safe. They are explained briefly as follows:

As evaluated in the previous section, actual revenue for Sky Cafe is lower than the

budgeted revenue by £900. The main reason that revenue has declined for the organisation is due

to the market factor. There are situations when an organisation plans out all moves and there

could be an abrupt shift in the market resulting in loss of sales or sales transposition, since the

customers start preferring a feature or product over another (Otley 2016). In case of Sky Cafe, as

the organisation is mainly dependent on the tourists for revenue generation, a sudden seasonal

change might have lead to fall in overall sales revenue.

Another area of concern is insurance expense, in which Sky Cafe has actually incurred

£2,600, which is £300 more than the budgeted figure. The reason identified behind such increase

in this expense item is that the organisation might not have settled a part of its insurance expense

in the past month due to which the actual amount has exceeded the budgeted amount.

Fuel is another item, in which the actual expense incurred has exceeded the budgeted

expense by £10. The cost of fuel increases with change in governmental policy, as the relevant

authority sets the fuel price of the nation (Shields 2015). In case of Sky Cafe, the fuel price

estimation was not made correctly, as the estimator might have failed to anticipate the sudden

rise in fuel price. As a result, the management of Sky Cafe has to bear additional expenses for

this item.

Finally, facility rent is deemed to be the final expense item having adverse variance in the

context of Sky Cafe. The facility rent is observed to exceed the budgeted amount by £800. The

Requirement 3:

There are certain activities identified having unfavourable variances and these activities

require proper management concern in the context of Safe. They are explained briefly as follows:

As evaluated in the previous section, actual revenue for Sky Cafe is lower than the

budgeted revenue by £900. The main reason that revenue has declined for the organisation is due

to the market factor. There are situations when an organisation plans out all moves and there

could be an abrupt shift in the market resulting in loss of sales or sales transposition, since the

customers start preferring a feature or product over another (Otley 2016). In case of Sky Cafe, as

the organisation is mainly dependent on the tourists for revenue generation, a sudden seasonal

change might have lead to fall in overall sales revenue.

Another area of concern is insurance expense, in which Sky Cafe has actually incurred

£2,600, which is £300 more than the budgeted figure. The reason identified behind such increase

in this expense item is that the organisation might not have settled a part of its insurance expense

in the past month due to which the actual amount has exceeded the budgeted amount.

Fuel is another item, in which the actual expense incurred has exceeded the budgeted

expense by £10. The cost of fuel increases with change in governmental policy, as the relevant

authority sets the fuel price of the nation (Shields 2015). In case of Sky Cafe, the fuel price

estimation was not made correctly, as the estimator might have failed to anticipate the sudden

rise in fuel price. As a result, the management of Sky Cafe has to bear additional expenses for

this item.

Finally, facility rent is deemed to be the final expense item having adverse variance in the

context of Sky Cafe. The facility rent is observed to exceed the budgeted amount by £800. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTS AND FINANCE

reason is that the organisation might have leased additional equipment due to the fact that it has

overestimated its sales volume for the month of July (Smith 2017). The rental expense has

increased compared to the budgeted one and as a result, Sky Cafe has to incur additional overall

expense of £1,460 compared to the budgeted figure.

Requirement 4:

After identification of the adverse variances for Sky Cafe, it is recommended to the

organisation to undertake certain measures that would assist in supporting its corporate

objectives. These measures are described briefly as follows:

Minimisation in selling price per unit:

It has been analysed that Sky Cafe has not managed to meet its expected sales volume, as

per the budgeted figure. As the competitors are perceived to use similar selling price per unit

with additional features, the organisation could minimise its selling price per unit to £4 per meal.

This is because many tourists prefer to avail food meals at lower prices for saving money

(Thomas 2016). This needs to be supported by additional marketing efforts to provide prior

information to the potential customers.

Cutting production costs:

As Sky Cafe is unable to control its operating costs due to unavoidable external

conditions, it needs to minimise its production costs. This reduction would assist in offsetting the

increased operating expense for the organisation (Van Der Stede 2016).

reason is that the organisation might have leased additional equipment due to the fact that it has

overestimated its sales volume for the month of July (Smith 2017). The rental expense has

increased compared to the budgeted one and as a result, Sky Cafe has to incur additional overall

expense of £1,460 compared to the budgeted figure.

Requirement 4:

After identification of the adverse variances for Sky Cafe, it is recommended to the

organisation to undertake certain measures that would assist in supporting its corporate

objectives. These measures are described briefly as follows:

Minimisation in selling price per unit:

It has been analysed that Sky Cafe has not managed to meet its expected sales volume, as

per the budgeted figure. As the competitors are perceived to use similar selling price per unit

with additional features, the organisation could minimise its selling price per unit to £4 per meal.

This is because many tourists prefer to avail food meals at lower prices for saving money

(Thomas 2016). This needs to be supported by additional marketing efforts to provide prior

information to the potential customers.

Cutting production costs:

As Sky Cafe is unable to control its operating costs due to unavoidable external

conditions, it needs to minimise its production costs. This reduction would assist in offsetting the

increased operating expense for the organisation (Van Der Stede 2016).

8ACCOUNTS AND FINANCE

Conclusion:

From the above discussion, it is inherent that the objective of preparing budget for Sky

Cafe is to allocate resources effectively along with appropriate estimation of market conditions.

When the budgeted expenses and revenue are compared with the actual expenses and revenue,

both revenue and spending variance are found to be adverse. The activities that need

management attention include revenue, insurance, fuel and facility rent. Hence, for combating

with these problems, it is advised to the management of Sky Cafe to minimise its selling price

per unit as well as production cost for increasing revenue and offsetting increase in operating

costs.

Conclusion:

From the above discussion, it is inherent that the objective of preparing budget for Sky

Cafe is to allocate resources effectively along with appropriate estimation of market conditions.

When the budgeted expenses and revenue are compared with the actual expenses and revenue,

both revenue and spending variance are found to be adverse. The activities that need

management attention include revenue, insurance, fuel and facility rent. Hence, for combating

with these problems, it is advised to the management of Sky Cafe to minimise its selling price

per unit as well as production cost for increasing revenue and offsetting increase in operating

costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTS AND FINANCE

References:

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34, pp.59-74.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management, 32(7-8), pp.414-428.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H., 2017. Management

accounting: Information for creating and managing value. McGraw-Hill Education Australia.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research, 31, pp.103-111.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and decision

making: Two case studies of outsourcing. In Accounting Forum, 39(1), pp. 64-82.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

References:

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34, pp.59-74.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management, 32(7-8), pp.414-428.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H., 2017. Management

accounting: Information for creating and managing value. McGraw-Hill Education Australia.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research, 31, pp.103-111.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and decision

making: Two case studies of outsourcing. In Accounting Forum, 39(1), pp. 64-82.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTS AND FINANCE

Shields, M.D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research, 27(1), pp.123-132.

Smith, S.S., 2017. Strategic Management Accounting: Delivering Value in a Changing Business

Environment Through Integrated Reporting. Business Expert Press.

Thomas, T.F., 2016. Motivating revisions of management accounting systems: An examination

of organizational goals and accounting feedback. Accounting, Organizations and Society, 53,

pp.1-16.

Van Der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research, 31, pp.100-102.

Shields, M.D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research, 27(1), pp.123-132.

Smith, S.S., 2017. Strategic Management Accounting: Delivering Value in a Changing Business

Environment Through Integrated Reporting. Business Expert Press.

Thomas, T.F., 2016. Motivating revisions of management accounting systems: An examination

of organizational goals and accounting feedback. Accounting, Organizations and Society, 53,

pp.1-16.

Van Der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research, 31, pp.100-102.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.