Financial Analysis and Performance Review of SMART IT: Case Study

VerifiedAdded on 2021/05/31

|14

|2176

|83

Case Study

AI Summary

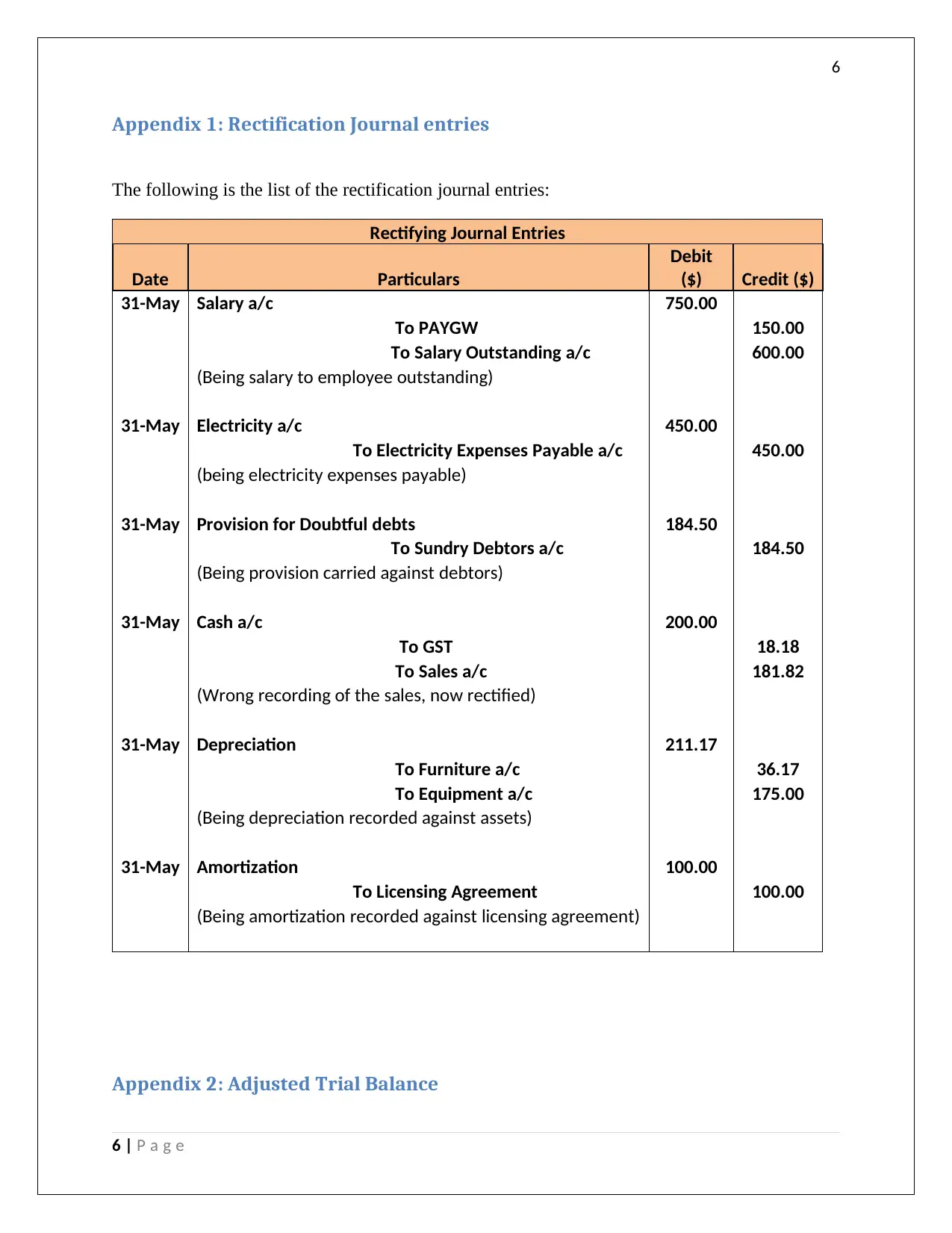

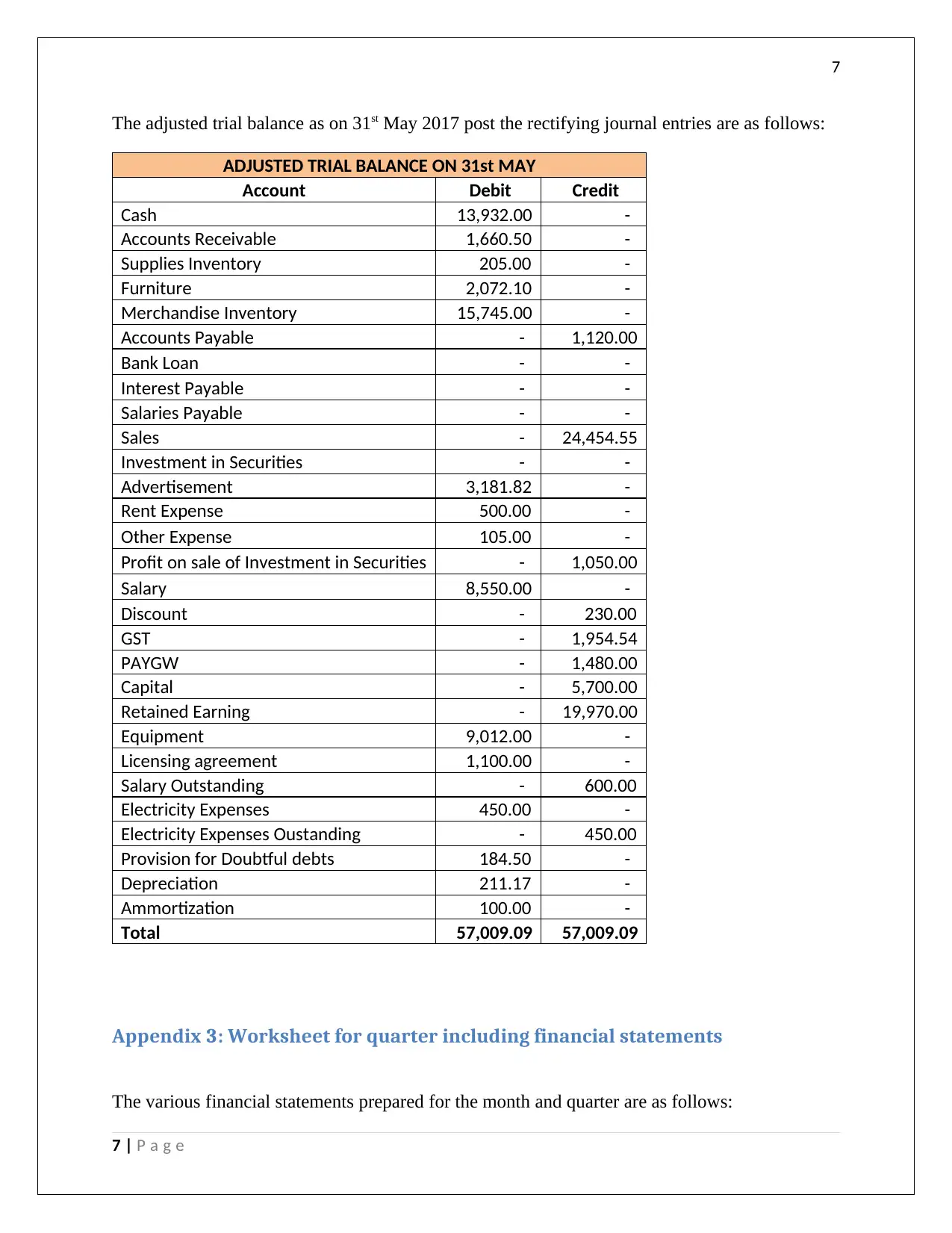

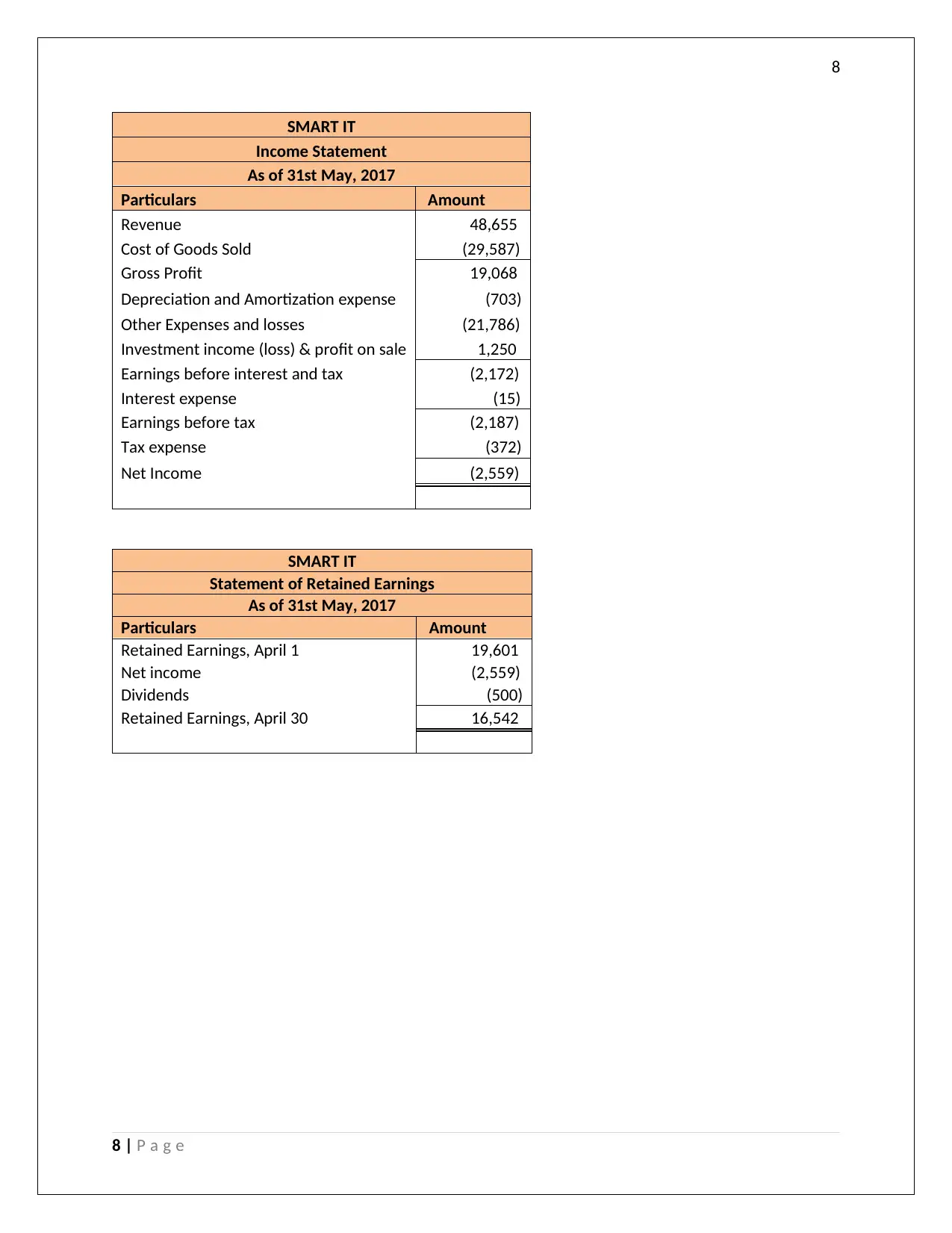

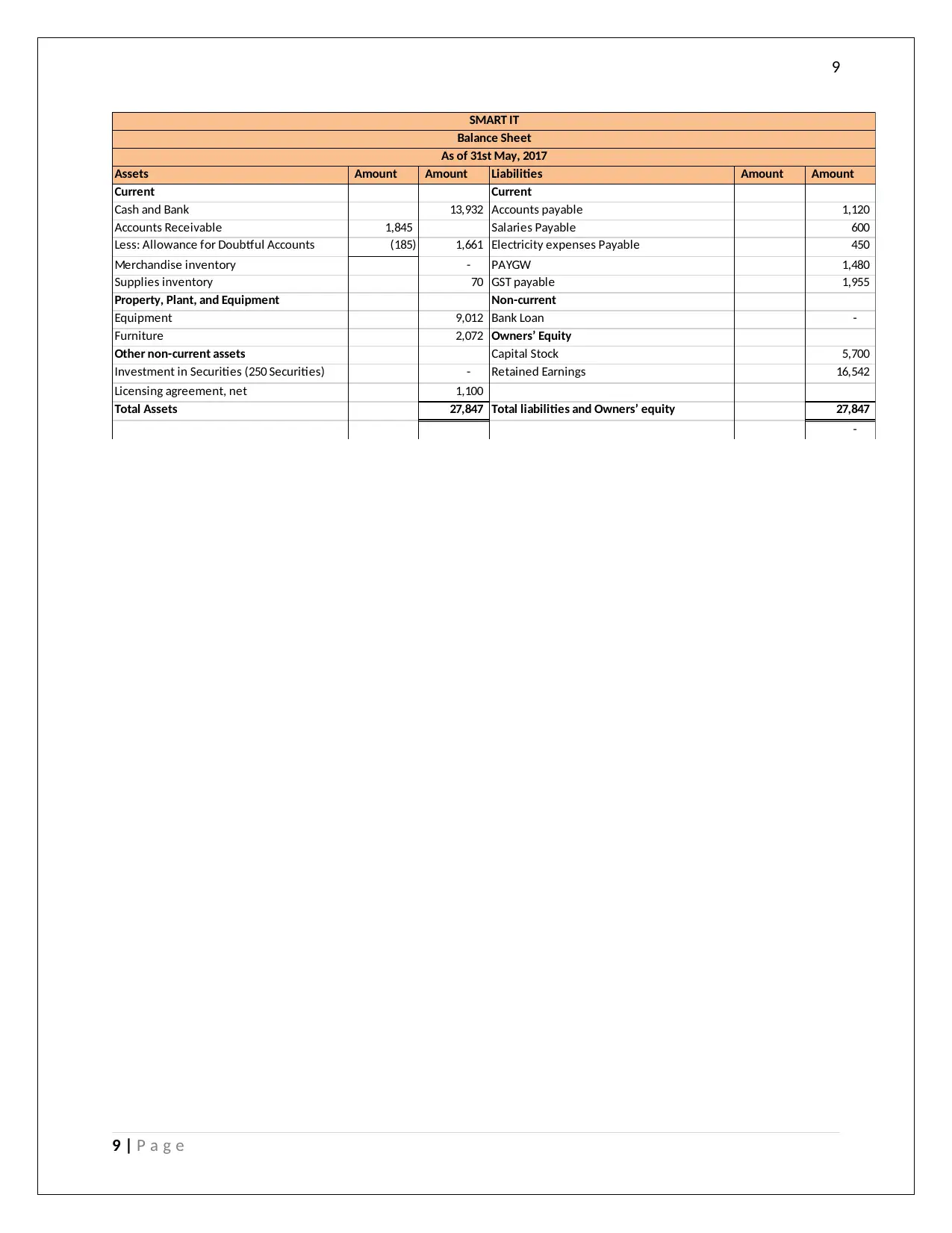

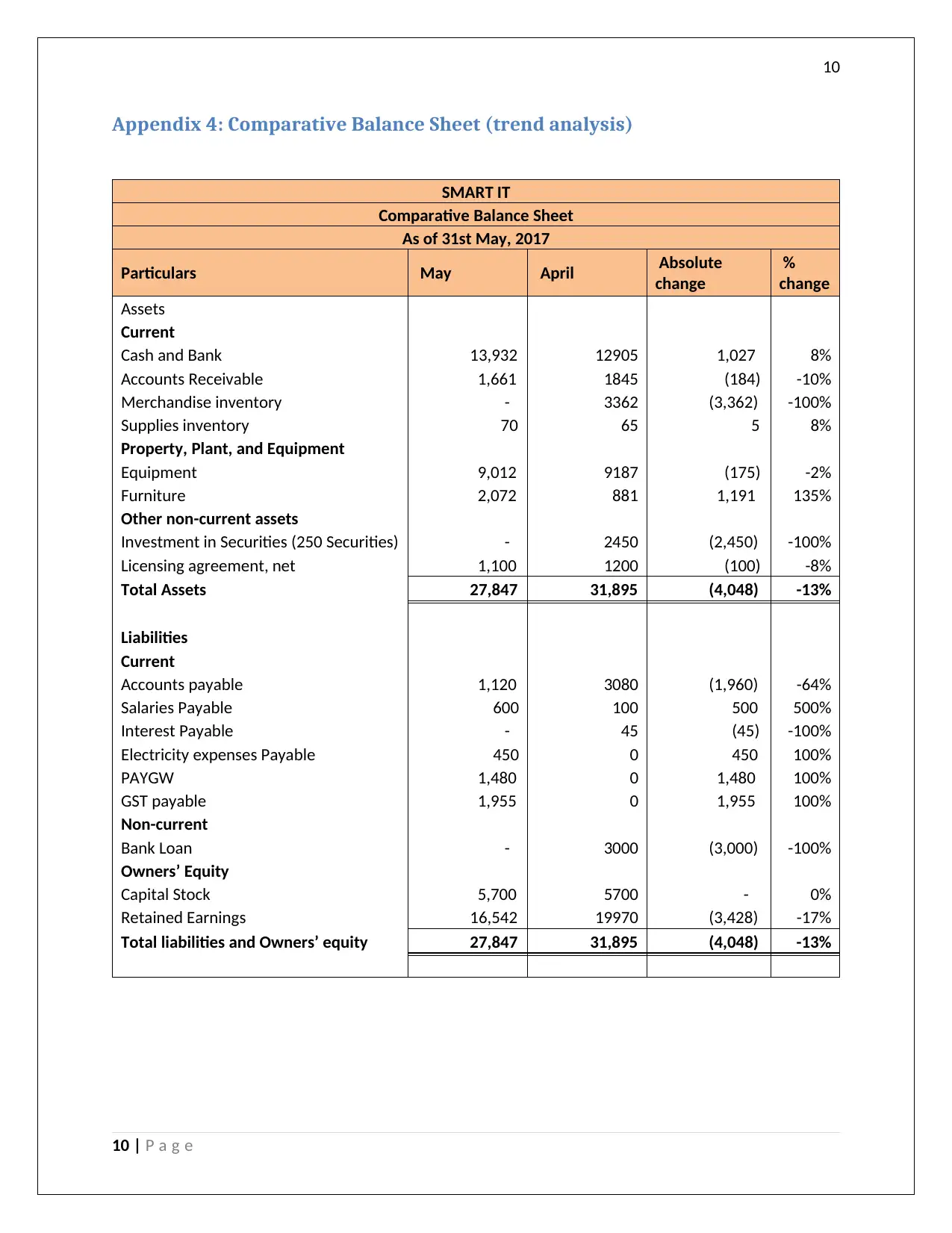

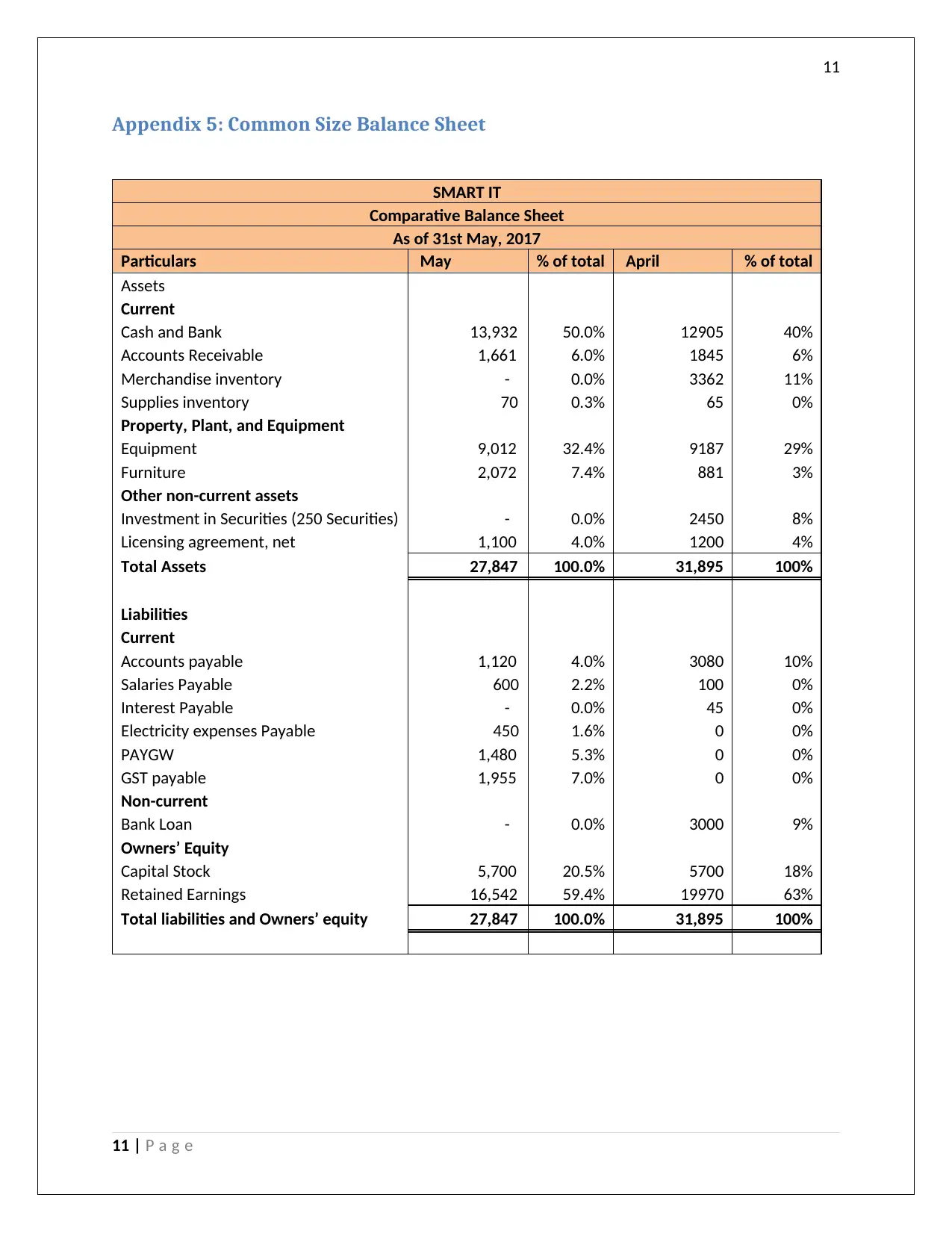

This case study analyzes the financial performance of SMART IT, focusing on the preparation of financial statements. It examines various aspects, including alternative accounting approaches, such as the written down value method for depreciation and perpetual inventory systems, and also explores strategies to address uncollectible debts. The report delves into ratio analysis, revealing a net profit ratio of -5.3%, a return on assets of -8.6%, and a return on equity of -11.5%, indicating financial losses. Comparative and common-size balance sheets are presented, highlighting changes in cash, accounts receivable, and liabilities. The study also includes rectification journal entries, an adjusted trial balance, and financial statements like the income statement and statement of retained earnings. Furthermore, the case study provides a comparative balance sheet for trend analysis and ratio analysis, along with a conclusion and recommendations for improving the company's financial position. References are included at the end.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.