Financial Ratio Analysis of Smart Resort Ltd: A Performance Review

VerifiedAdded on 2023/06/16

|11

|3440

|400

Report

AI Summary

This report provides a comprehensive analysis of Smart Resort Ltd.'s financial performance, focusing on the application of financial ratios to interpret the company's financial statements for the years 2018 and 2019. It begins by explaining Generally Accepted Accounting Principles (GAAP) and their importance in financial reporting, along with identifying various users of financial statements and their specific information needs. The report then discusses the relevance of income statements, balance sheets, and cash flow statements to different stakeholders, such as loan creditors and trade creditors. Further, it outlines the components that supplement financial statements in an annual report and explains key financial reporting concepts like matching, business entity, and going concern. Finally, as the finance director of Smart Resort Ltd, the report interprets financial statements using ratios like net profit margin, return on assets, return on equity, and current ratio, comparing the company's performance across both years to provide insights into its financial health and operational efficiency. Desklib offers a wealth of study tools and solved assignments for students seeking to deepen their understanding of financial analysis.

Managing Financial

Resources in

Hospitality Industry

Resources in

Hospitality Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question 1. Explain the concept of generally accepted accounting principles? Discuss various

users of financial statements and assess the financial information that they need.................3

Question 2. The annual financial statements of companies are used by various parties for a

wide variety of purposes. Discuss which of the three statements of income, financial position

and cash flows would be of most interest to the following:...................................................5

Question 3. Describe the components that supplement the financial statements in an annual

report. Discuss financial reporting concepts?.........................................................................6

Question 4. Assume you are the finance director of Smart Resort Ltd. Using the information

provided below, interpret financial statements using appropriate financial ratios and compare

both year performances..........................................................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question 1. Explain the concept of generally accepted accounting principles? Discuss various

users of financial statements and assess the financial information that they need.................3

Question 2. The annual financial statements of companies are used by various parties for a

wide variety of purposes. Discuss which of the three statements of income, financial position

and cash flows would be of most interest to the following:...................................................5

Question 3. Describe the components that supplement the financial statements in an annual

report. Discuss financial reporting concepts?.........................................................................6

Question 4. Assume you are the finance director of Smart Resort Ltd. Using the information

provided below, interpret financial statements using appropriate financial ratios and compare

both year performances..........................................................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial Accounting is a kind of accounting which is concerned with summary, analysis

and reporting of financial transactions related to a business. This type of accounting requires the

accountants to carefully prepare the accounts that are required to make financial statements.

These statements are then reported to the various stakeholders that have interests in the working

of the company (Monahan, 2018). Just like other professions, these are also governed by a set of

bodies and principles that form basis for governing the accounting statements made by the

companies. These principles help accountants work smoothly and present the data accordingly.

Accounting concepts are the foundation that lay an organized accounting system in an

organisation. This report helps know-how the need for economic control and accounting and the

way those help extraordinary users of accounting statistics. The report highlights the concept of

GAAP and one-of-a-kind financial statements. Calculations of various ratios and analysis of

those ratios is also finished following a brief reporting of same. The company taken for this

report is Smart Resort Ltd.

TASK

Question 1. Explain the concept of generally accepted accounting principles? Discuss various

users of financial statements and assess the financial information that they need.

There are different standards that are designed by different accounting bodies which can

be applied while preparation and reporting of the financial information. Generally Accepted

Accounting Principles (GAAP) are common set of accounting rules which includes the

conventions, rules and procedures necessary to followed while preparation of accounting

statements and reporting of same. GAAP mentions the accepted accounting practice at a

particular time (Ariyawansa, and Nanayakkara, 2021). These provide a standard to measure and

make financial presentations. US securities exchange board has adopted these principles which

means all the companies registered there have to follow these principles while reporting the

financial information. GAAP follows the rule-based accounting which means these are set of

rules which are required to be taken as they are and no amendments are allowed in this. Federal

Accounting Standards Advisory Board (FASAB) is the body which makes and regulates GAAP

all around the world.

Financial Accounting is a kind of accounting which is concerned with summary, analysis

and reporting of financial transactions related to a business. This type of accounting requires the

accountants to carefully prepare the accounts that are required to make financial statements.

These statements are then reported to the various stakeholders that have interests in the working

of the company (Monahan, 2018). Just like other professions, these are also governed by a set of

bodies and principles that form basis for governing the accounting statements made by the

companies. These principles help accountants work smoothly and present the data accordingly.

Accounting concepts are the foundation that lay an organized accounting system in an

organisation. This report helps know-how the need for economic control and accounting and the

way those help extraordinary users of accounting statistics. The report highlights the concept of

GAAP and one-of-a-kind financial statements. Calculations of various ratios and analysis of

those ratios is also finished following a brief reporting of same. The company taken for this

report is Smart Resort Ltd.

TASK

Question 1. Explain the concept of generally accepted accounting principles? Discuss various

users of financial statements and assess the financial information that they need.

There are different standards that are designed by different accounting bodies which can

be applied while preparation and reporting of the financial information. Generally Accepted

Accounting Principles (GAAP) are common set of accounting rules which includes the

conventions, rules and procedures necessary to followed while preparation of accounting

statements and reporting of same. GAAP mentions the accepted accounting practice at a

particular time (Ariyawansa, and Nanayakkara, 2021). These provide a standard to measure and

make financial presentations. US securities exchange board has adopted these principles which

means all the companies registered there have to follow these principles while reporting the

financial information. GAAP follows the rule-based accounting which means these are set of

rules which are required to be taken as they are and no amendments are allowed in this. Federal

Accounting Standards Advisory Board (FASAB) is the body which makes and regulates GAAP

all around the world.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are different users of accounting information. These may be within the

organisation or outside it. These users use the information for diverse purposes. Thus the

statements should be made successful in such a way that provide to the needs of these users.

These users are discussed below.

Users of Accounting Information

Management: These are the those who formulate and make plans for the future. They

plan consistent with the goals of the corporation. These users of the accounting data make

use of it to devise, manipulate and selection making. It allows them compare the overall

performance of the organization and function (Zeller, Kostolansky and Bozoudis, 2019).

It essentially allows them do their task better. Managers of an enterprise makes use of the

financial facts to track overall performance through budgets, and variances to check the

viability of standards set.

Employees: These are the people working within the company with the goal to earn

profits and fulfil the organisational objectives. They use the accounting statistics to

decide the economic health and profitability of the business to guarantee their activity

protection, destiny remuneration, retirement advantages and other opportunities. They

particularly search for profitability of the enterprise in response to paintings performed.

Owners: They are the people who have invested in the enterprise to earn dividends. They

are the vital factors of a business enterprise and groups usually look for ways to

maximize their income. They use this information to analyse the profitability of the

agency and returns on their investments. It gives them insights about the commercial

enterprise and its capability to pay dividends for his or her investments. It also facilitates

them determine future direction of action.

Creditors: These are users who've given mortgage to the business. They are fascinated to

determine credit score worthiness of the commercial enterprise. These includes providers,

banks, creditors of finance. It helps them examine financial function of the business and

if they could amplify any loans to them (Lessambo, 2018). Trade lenders only want facts

related to short time frame than lenders.

Investors: They need the accounting information as they want to ascertain the risk in

investing and the returns and plan accordingly how much amount and where they should

invest for better returns.

organisation or outside it. These users use the information for diverse purposes. Thus the

statements should be made successful in such a way that provide to the needs of these users.

These users are discussed below.

Users of Accounting Information

Management: These are the those who formulate and make plans for the future. They

plan consistent with the goals of the corporation. These users of the accounting data make

use of it to devise, manipulate and selection making. It allows them compare the overall

performance of the organization and function (Zeller, Kostolansky and Bozoudis, 2019).

It essentially allows them do their task better. Managers of an enterprise makes use of the

financial facts to track overall performance through budgets, and variances to check the

viability of standards set.

Employees: These are the people working within the company with the goal to earn

profits and fulfil the organisational objectives. They use the accounting statistics to

decide the economic health and profitability of the business to guarantee their activity

protection, destiny remuneration, retirement advantages and other opportunities. They

particularly search for profitability of the enterprise in response to paintings performed.

Owners: They are the people who have invested in the enterprise to earn dividends. They

are the vital factors of a business enterprise and groups usually look for ways to

maximize their income. They use this information to analyse the profitability of the

agency and returns on their investments. It gives them insights about the commercial

enterprise and its capability to pay dividends for his or her investments. It also facilitates

them determine future direction of action.

Creditors: These are users who've given mortgage to the business. They are fascinated to

determine credit score worthiness of the commercial enterprise. These includes providers,

banks, creditors of finance. It helps them examine financial function of the business and

if they could amplify any loans to them (Lessambo, 2018). Trade lenders only want facts

related to short time frame than lenders.

Investors: They need the accounting information as they want to ascertain the risk in

investing and the returns and plan accordingly how much amount and where they should

invest for better returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Customers: They need the accounting information to ascertain the financial position of a

business, when they have long involvement in the business.

Regulatory Authorities: They need to ascertain that the accounting information is in

accordance with the rules and complies with the law of state where the business is taking

place.

Question 2. The annual financial statements of companies are used by various parties for a wide

variety of purposes. Discuss which of the three statements of income, financial position

and cash flows would be of most interest to the following:

a) A loan creditor

A loan creditor is someone who expand loans and advances to the commercial enterprise

that's required to be paid back with the aid of the enterprise after the predetermined time period.

These finances are vital for the enterprise as those are used in day-to-day activities and

operations of the commercial enterprise (Pouliasis, Papapostolou and Visvikis, 2018). These

creditors need to significantly examine the performance of the commercial enterprise and how

they will be rewarded with the hobby and in what period will the main quantity be paid again. To

reduce the hazard of horrific money owed in the future these creditors perform a chance

assessment based on the monetary statements of the corporation. For analysing they take help of

the financial statements of the business and ascertain the performance of the business. Statement

of performance or balance sheet is one of the critical tool used by them to check the current

liabilities that the organisation holds and also the statement of cash flows to see at what rate the

company is able to pay back its obligations.

b) A trade creditor

A trade creditor is a person who supplies goods and services to the organisation which is

not yet paid for them. The company owes this amount to this supplier which is required to be

paid back in time. Trade creditor provide goods and services on credit after having known the

working of the business and in what time these amount will be paid (Reinganum, 1999). These

are generally paid within a year and forms the short-term liabilities of the business. Trade

creditors make use of the financial statements like statement of profit or loss and cash flows to

ascertain if the company is in position to be given goods on credit or not.

business, when they have long involvement in the business.

Regulatory Authorities: They need to ascertain that the accounting information is in

accordance with the rules and complies with the law of state where the business is taking

place.

Question 2. The annual financial statements of companies are used by various parties for a wide

variety of purposes. Discuss which of the three statements of income, financial position

and cash flows would be of most interest to the following:

a) A loan creditor

A loan creditor is someone who expand loans and advances to the commercial enterprise

that's required to be paid back with the aid of the enterprise after the predetermined time period.

These finances are vital for the enterprise as those are used in day-to-day activities and

operations of the commercial enterprise (Pouliasis, Papapostolou and Visvikis, 2018). These

creditors need to significantly examine the performance of the commercial enterprise and how

they will be rewarded with the hobby and in what period will the main quantity be paid again. To

reduce the hazard of horrific money owed in the future these creditors perform a chance

assessment based on the monetary statements of the corporation. For analysing they take help of

the financial statements of the business and ascertain the performance of the business. Statement

of performance or balance sheet is one of the critical tool used by them to check the current

liabilities that the organisation holds and also the statement of cash flows to see at what rate the

company is able to pay back its obligations.

b) A trade creditor

A trade creditor is a person who supplies goods and services to the organisation which is

not yet paid for them. The company owes this amount to this supplier which is required to be

paid back in time. Trade creditor provide goods and services on credit after having known the

working of the business and in what time these amount will be paid (Reinganum, 1999). These

are generally paid within a year and forms the short-term liabilities of the business. Trade

creditors make use of the financial statements like statement of profit or loss and cash flows to

ascertain if the company is in position to be given goods on credit or not.

Question 3. Describe the components that supplement the financial statements in an annual

report. Discuss financial reporting concepts?

Annual report of any enterprises consists of various additives that gives specific insights to the

customers of those reviews. The most important issue of those report are the financial statements.

These statements consist of statement of earnings or loss, statement of financial overall

performance/ stability sheet and announcement of coins flows (Beaver, 1966). These vital

components are supplemented by some other issue that are notes to money owed. Notes to

financial statements elaborates the facts and figures that are written in a concise way in the

statements. These provide detailed information on the figures written in the statements.

Financial concepts are required to be in mind of any business while recording and

preparing the accounts for an organisation. If an organisation follows the concepts and have in

depth understanding about the same, it creates trust among the stakeholders and they would want

to engage with its business. Following are the accounting concepts that helps accountants work

effectively:

Matching Concept helps in calculating profit or loss in the given period, it needs

to record all the expenses and equivalent incomes to establish accurate profit or

loss (Talha, 2021).

Business Entity Concept says that by law, a business is a separate entity from its

owners. It can be sued and sue by its name. It prevents mixing of assets and

liabilities among business and its owners.

Dual Aspect Concept says that for every debit, there is a corresponding debit.

The recording of transaction is done in dual aspect.

Going Concern Concept says that the business is going to do its business for a

fairly long time and accounting should be done over a period of time. This

assumes that a business will not be forced to stop its business (Çelik and Arslanli,

2021).

Cost Concept says that business assets are required to be shown at the cost price,

that is the price they were purchased in the books of accounts (Meiryani and et. al.

2021). The depreciation is reduced over a period but no account is given to

market growth.

report. Discuss financial reporting concepts?

Annual report of any enterprises consists of various additives that gives specific insights to the

customers of those reviews. The most important issue of those report are the financial statements.

These statements consist of statement of earnings or loss, statement of financial overall

performance/ stability sheet and announcement of coins flows (Beaver, 1966). These vital

components are supplemented by some other issue that are notes to money owed. Notes to

financial statements elaborates the facts and figures that are written in a concise way in the

statements. These provide detailed information on the figures written in the statements.

Financial concepts are required to be in mind of any business while recording and

preparing the accounts for an organisation. If an organisation follows the concepts and have in

depth understanding about the same, it creates trust among the stakeholders and they would want

to engage with its business. Following are the accounting concepts that helps accountants work

effectively:

Matching Concept helps in calculating profit or loss in the given period, it needs

to record all the expenses and equivalent incomes to establish accurate profit or

loss (Talha, 2021).

Business Entity Concept says that by law, a business is a separate entity from its

owners. It can be sued and sue by its name. It prevents mixing of assets and

liabilities among business and its owners.

Dual Aspect Concept says that for every debit, there is a corresponding debit.

The recording of transaction is done in dual aspect.

Going Concern Concept says that the business is going to do its business for a

fairly long time and accounting should be done over a period of time. This

assumes that a business will not be forced to stop its business (Çelik and Arslanli,

2021).

Cost Concept says that business assets are required to be shown at the cost price,

that is the price they were purchased in the books of accounts (Meiryani and et. al.

2021). The depreciation is reduced over a period but no account is given to

market growth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Realisation Concept states that profit should only be recorded when it is earned.

Advancement of any such profits should not be realised and should be shown as

liability. Profits should always be realised before going into the accounts.

Money Measurement Concept says that only those business transactions, that

can be expressed in terms of money are recorded in the books of accounts.

Recording of other kind may be kept separately (Ustinova, 2020).

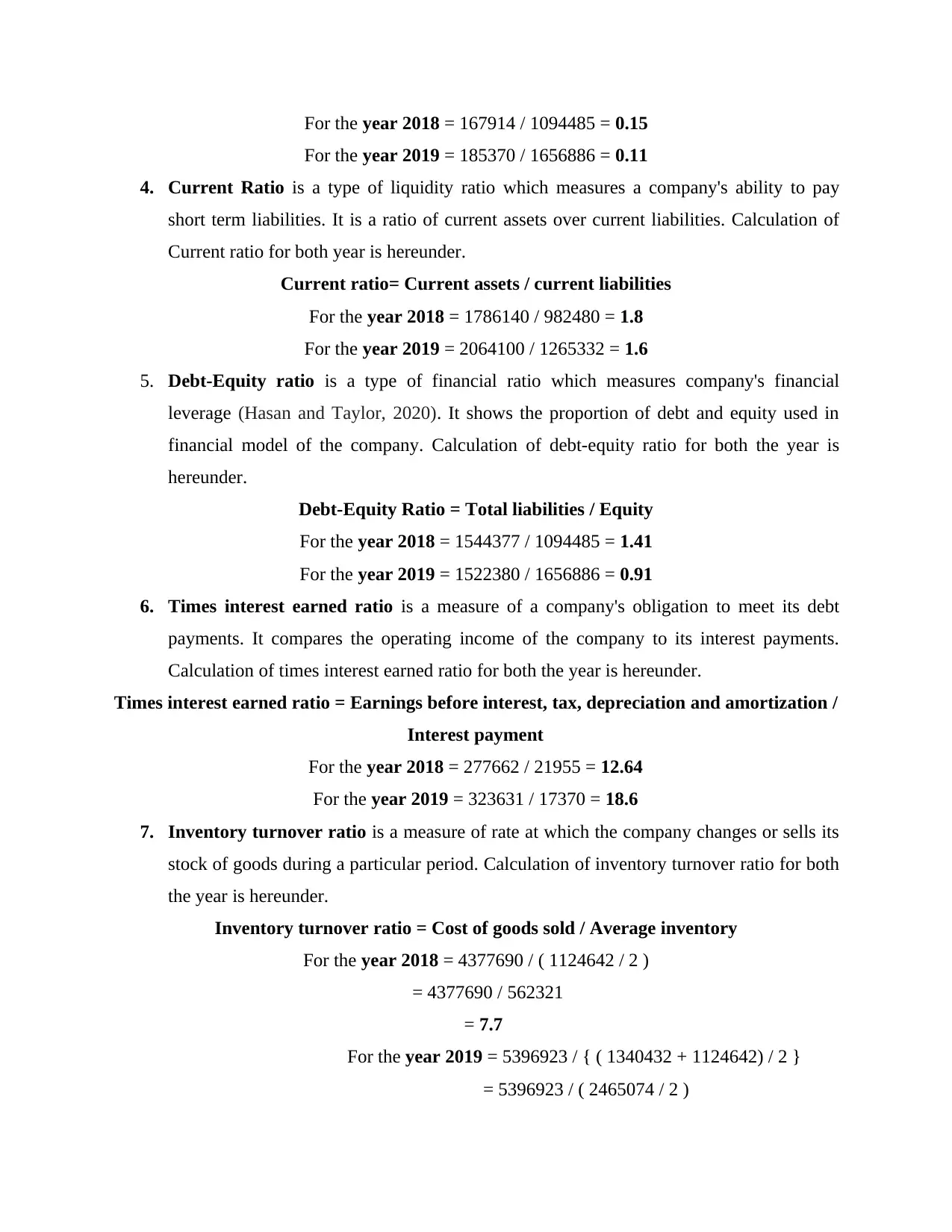

Question 4. Assume you are the finance director of Smart Resort Ltd. Using the information

provided below, interpret financial statements using appropriate financial ratios and

compare both year performances.

Ratio analysis is an important tool to interpret the financial statements of the business

(Mohammed and et. al., 2020). Financial Ratio Analysis is a tool in accounting which helps

managers analyse the financial information. Following are the calculations of accounting ratios

in response to Smart Resort Ltd.

1. Net Profit Margin measures how much net profit is generated as a percentage of

sales/revenue. The calculation of net profit for both the year is hereunder.

Net Profit= Net Income / Net sales * 100

For the year 2018 = 167914 / 5732145 * 100

= 0.029 * 100 = 2.92 %

For the year 2019 = 185370 / 7123189 * 100

= 0.026 * 100 = 2.60 %

2. Return on Assets is a profitability ratio which measures how much profit the company is

able to generate over its assets. The calculation of of Return on Assets for both the year is

hereunder.

Return on Assets = Net Income / Total Assets

For the year 2018 = 167914 / 2638862 =0.06

For the year 2019 = 185370 / 3179266 = 0.05

3. Return on Equity is a measure of company's financial performance, it gives insights as

to how much profits is it able to generate over the invested amount of shareholders'. The

calculation of Return on Equity for both the year is hereunder.

Return on Equity= Net Income / Equity

Advancement of any such profits should not be realised and should be shown as

liability. Profits should always be realised before going into the accounts.

Money Measurement Concept says that only those business transactions, that

can be expressed in terms of money are recorded in the books of accounts.

Recording of other kind may be kept separately (Ustinova, 2020).

Question 4. Assume you are the finance director of Smart Resort Ltd. Using the information

provided below, interpret financial statements using appropriate financial ratios and

compare both year performances.

Ratio analysis is an important tool to interpret the financial statements of the business

(Mohammed and et. al., 2020). Financial Ratio Analysis is a tool in accounting which helps

managers analyse the financial information. Following are the calculations of accounting ratios

in response to Smart Resort Ltd.

1. Net Profit Margin measures how much net profit is generated as a percentage of

sales/revenue. The calculation of net profit for both the year is hereunder.

Net Profit= Net Income / Net sales * 100

For the year 2018 = 167914 / 5732145 * 100

= 0.029 * 100 = 2.92 %

For the year 2019 = 185370 / 7123189 * 100

= 0.026 * 100 = 2.60 %

2. Return on Assets is a profitability ratio which measures how much profit the company is

able to generate over its assets. The calculation of of Return on Assets for both the year is

hereunder.

Return on Assets = Net Income / Total Assets

For the year 2018 = 167914 / 2638862 =0.06

For the year 2019 = 185370 / 3179266 = 0.05

3. Return on Equity is a measure of company's financial performance, it gives insights as

to how much profits is it able to generate over the invested amount of shareholders'. The

calculation of Return on Equity for both the year is hereunder.

Return on Equity= Net Income / Equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For the year 2018 = 167914 / 1094485 = 0.15

For the year 2019 = 185370 / 1656886 = 0.11

4. Current Ratio is a type of liquidity ratio which measures a company's ability to pay

short term liabilities. It is a ratio of current assets over current liabilities. Calculation of

Current ratio for both year is hereunder.

Current ratio= Current assets / current liabilities

For the year 2018 = 1786140 / 982480 = 1.8

For the year 2019 = 2064100 / 1265332 = 1.6

5. Debt-Equity ratio is a type of financial ratio which measures company's financial

leverage (Hasan and Taylor, 2020). It shows the proportion of debt and equity used in

financial model of the company. Calculation of debt-equity ratio for both the year is

hereunder.

Debt-Equity Ratio = Total liabilities / Equity

For the year 2018 = 1544377 / 1094485 = 1.41

For the year 2019 = 1522380 / 1656886 = 0.91

6. Times interest earned ratio is a measure of a company's obligation to meet its debt

payments. It compares the operating income of the company to its interest payments.

Calculation of times interest earned ratio for both the year is hereunder.

Times interest earned ratio = Earnings before interest, tax, depreciation and amortization /

Interest payment

For the year 2018 = 277662 / 21955 = 12.64

For the year 2019 = 323631 / 17370 = 18.6

7. Inventory turnover ratio is a measure of rate at which the company changes or sells its

stock of goods during a particular period. Calculation of inventory turnover ratio for both

the year is hereunder.

Inventory turnover ratio = Cost of goods sold / Average inventory

For the year 2018 = 4377690 / ( 1124642 / 2 )

= 4377690 / 562321

= 7.7

For the year 2019 = 5396923 / { ( 1340432 + 1124642) / 2 }

= 5396923 / ( 2465074 / 2 )

For the year 2019 = 185370 / 1656886 = 0.11

4. Current Ratio is a type of liquidity ratio which measures a company's ability to pay

short term liabilities. It is a ratio of current assets over current liabilities. Calculation of

Current ratio for both year is hereunder.

Current ratio= Current assets / current liabilities

For the year 2018 = 1786140 / 982480 = 1.8

For the year 2019 = 2064100 / 1265332 = 1.6

5. Debt-Equity ratio is a type of financial ratio which measures company's financial

leverage (Hasan and Taylor, 2020). It shows the proportion of debt and equity used in

financial model of the company. Calculation of debt-equity ratio for both the year is

hereunder.

Debt-Equity Ratio = Total liabilities / Equity

For the year 2018 = 1544377 / 1094485 = 1.41

For the year 2019 = 1522380 / 1656886 = 0.91

6. Times interest earned ratio is a measure of a company's obligation to meet its debt

payments. It compares the operating income of the company to its interest payments.

Calculation of times interest earned ratio for both the year is hereunder.

Times interest earned ratio = Earnings before interest, tax, depreciation and amortization /

Interest payment

For the year 2018 = 277662 / 21955 = 12.64

For the year 2019 = 323631 / 17370 = 18.6

7. Inventory turnover ratio is a measure of rate at which the company changes or sells its

stock of goods during a particular period. Calculation of inventory turnover ratio for both

the year is hereunder.

Inventory turnover ratio = Cost of goods sold / Average inventory

For the year 2018 = 4377690 / ( 1124642 / 2 )

= 4377690 / 562321

= 7.7

For the year 2019 = 5396923 / { ( 1340432 + 1124642) / 2 }

= 5396923 / ( 2465074 / 2 )

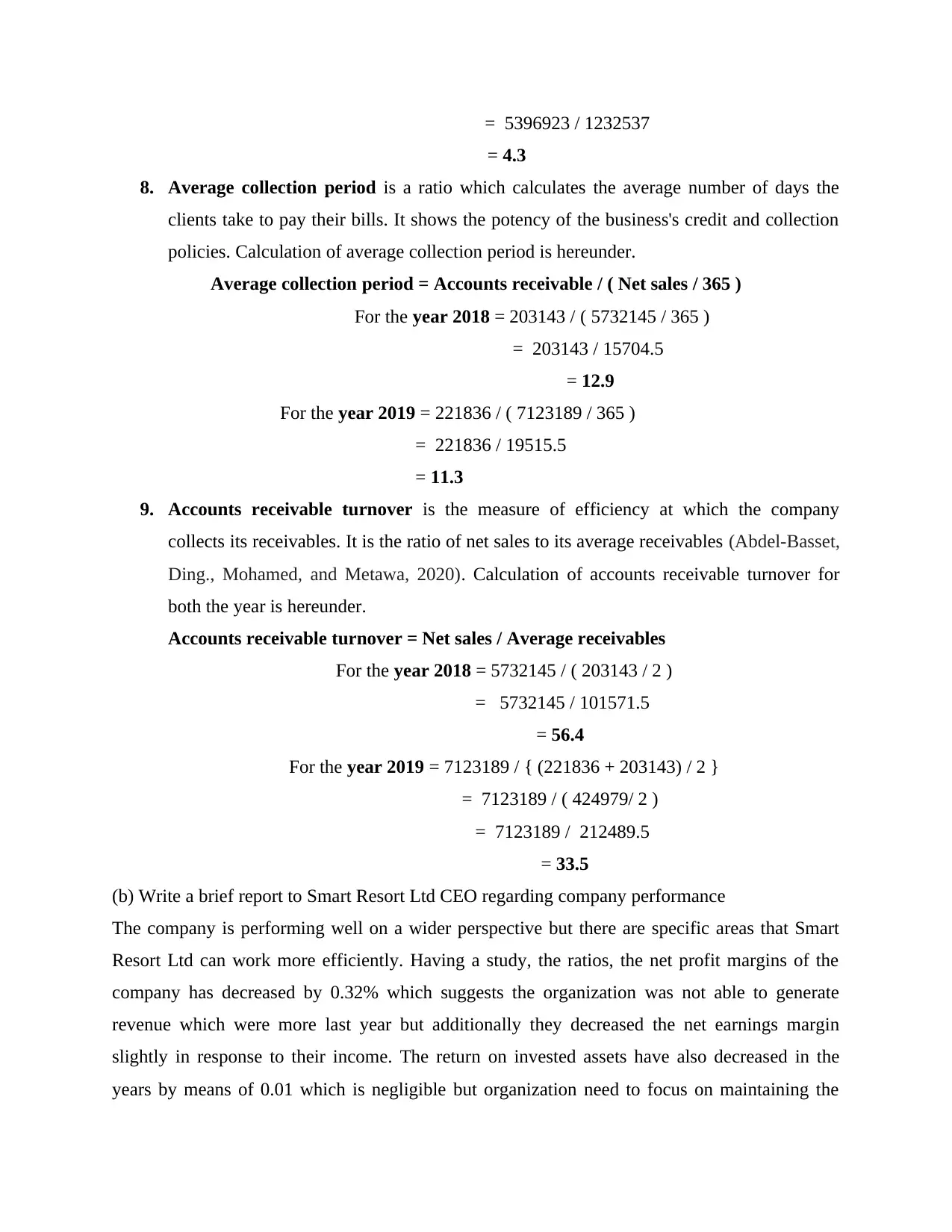

= 5396923 / 1232537

= 4.3

8. Average collection period is a ratio which calculates the average number of days the

clients take to pay their bills. It shows the potency of the business's credit and collection

policies. Calculation of average collection period is hereunder.

Average collection period = Accounts receivable / ( Net sales / 365 )

For the year 2018 = 203143 / ( 5732145 / 365 )

= 203143 / 15704.5

= 12.9

For the year 2019 = 221836 / ( 7123189 / 365 )

= 221836 / 19515.5

= 11.3

9. Accounts receivable turnover is the measure of efficiency at which the company

collects its receivables. It is the ratio of net sales to its average receivables (Abdel-Basset,

Ding., Mohamed, and Metawa, 2020). Calculation of accounts receivable turnover for

both the year is hereunder.

Accounts receivable turnover = Net sales / Average receivables

For the year 2018 = 5732145 / ( 203143 / 2 )

= 5732145 / 101571.5

= 56.4

For the year 2019 = 7123189 / { (221836 + 203143) / 2 }

= 7123189 / ( 424979/ 2 )

= 7123189 / 212489.5

= 33.5

(b) Write a brief report to Smart Resort Ltd CEO regarding company performance

The company is performing well on a wider perspective but there are specific areas that Smart

Resort Ltd can work more efficiently. Having a study, the ratios, the net profit margins of the

company has decreased by 0.32% which suggests the organization was not able to generate

revenue which were more last year but additionally they decreased the net earnings margin

slightly in response to their income. The return on invested assets have also decreased in the

years by means of 0.01 which is negligible but organization need to focus on maintaining the

= 4.3

8. Average collection period is a ratio which calculates the average number of days the

clients take to pay their bills. It shows the potency of the business's credit and collection

policies. Calculation of average collection period is hereunder.

Average collection period = Accounts receivable / ( Net sales / 365 )

For the year 2018 = 203143 / ( 5732145 / 365 )

= 203143 / 15704.5

= 12.9

For the year 2019 = 221836 / ( 7123189 / 365 )

= 221836 / 19515.5

= 11.3

9. Accounts receivable turnover is the measure of efficiency at which the company

collects its receivables. It is the ratio of net sales to its average receivables (Abdel-Basset,

Ding., Mohamed, and Metawa, 2020). Calculation of accounts receivable turnover for

both the year is hereunder.

Accounts receivable turnover = Net sales / Average receivables

For the year 2018 = 5732145 / ( 203143 / 2 )

= 5732145 / 101571.5

= 56.4

For the year 2019 = 7123189 / { (221836 + 203143) / 2 }

= 7123189 / ( 424979/ 2 )

= 7123189 / 212489.5

= 33.5

(b) Write a brief report to Smart Resort Ltd CEO regarding company performance

The company is performing well on a wider perspective but there are specific areas that Smart

Resort Ltd can work more efficiently. Having a study, the ratios, the net profit margins of the

company has decreased by 0.32% which suggests the organization was not able to generate

revenue which were more last year but additionally they decreased the net earnings margin

slightly in response to their income. The return on invested assets have also decreased in the

years by means of 0.01 which is negligible but organization need to focus on maintaining the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

return in order that the difference does not go wider. Company has done wonders in decreasing

their debt-equity ratio this year they have issued more equity to the public. This has reduced

tensions on surviving on extra debt than equity. The interest earning ratio were elevated

significantly over the last 12 months which means that the interest paid by means of the

organization has decreased because of reduction money owed and rise in operating profit this

year. Overall, the corporation is performing nicely within the market but there are a few points

that wishes to be addressed like increasing the dependence on equity rather than debt or

recuperating extra from the assets of the firm.

CONCLUSION

From the above report it has been concluded that managing financial resources in a hospitality

industry is an important concept. The report highlights how accounting concepts help in

maintaining and reporting the financial information. The report has also highlighted how

different users of accounting information analyses and make use of different ratios in decision-

making. Different accounting ratios have also been calculated and reported to the CEO of Smart

Resort Ltd.

their debt-equity ratio this year they have issued more equity to the public. This has reduced

tensions on surviving on extra debt than equity. The interest earning ratio were elevated

significantly over the last 12 months which means that the interest paid by means of the

organization has decreased because of reduction money owed and rise in operating profit this

year. Overall, the corporation is performing nicely within the market but there are a few points

that wishes to be addressed like increasing the dependence on equity rather than debt or

recuperating extra from the assets of the firm.

CONCLUSION

From the above report it has been concluded that managing financial resources in a hospitality

industry is an important concept. The report highlights how accounting concepts help in

maintaining and reporting the financial information. The report has also highlighted how

different users of accounting information analyses and make use of different ratios in decision-

making. Different accounting ratios have also been calculated and reported to the CEO of Smart

Resort Ltd.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Monahan, S.J., 2018. Financial statement analysis and earnings forecasting. Foundations and

Trends® in Accounting. 12(2). pp.105-215.

Ariyawansa, H.D.G.R. and Nanayakkara, K.G.M., 2021. Financial statement informativeness

and intellectual capital disclosures: with special reference to listed companies in srilanka.

Zeller, T., Kostolansky, J. and Bozoudis, M., 2019. An IFRS-based taxonomy of financial

ratios. Accounting Research Journal.

Lessambo, F.I., 2018. Audit tools: Financial ratios analysis. In Auditing, assurance services, and

forensics (pp. 371-394). Palgrave Macmillan, Cham.

Pouliasis, P.K., Papapostolou, N.C. and Visvikis, I.D., 2018. Investor Sentiment, Earnings

Growth, and Volatility: Strategies for Finance in International Shipping. In Finance and Risk

Management for International Logistics and the Supply Chain (pp. 109-127). Elsevier.

Reinganum, M.R., 1999. The significance of market capitalization in portfolio management over

time. Journal of Portfolio Management. 25(4). p.39.

Beaver, W.H., 1966. Financial ratios as predictors of failure. Journal of accounting research,

pp.71-111.

Çelik, E. and Arslanli, K.Y., 2021. The idiosyncratic characteristics of Turkish REITs: evidence

from financial ratios. Journal of European Real Estate Research.

Mohammed, A., and et. al., 2020. Characterization and modeling the flow behavior and

compression strength of the cement paste modified with silica nano-size at different temperature

conditions. Construction and Building Materials. 257. p.119590.

Hasan, M.M. and Taylor, G., 2020. Financial statement comparability and bank risk-

taking. Journal of Contemporary Accounting & Economics. 16(3). p.100206.

Talha, M., 2021. FINANCIAL STATEMENT ANALYSIS OF ATLAS HONDA MOTORS,

INDUS MOTORS AND PAK SUZUKI MOTORS (EVIDENCE FROM

PAKISTAN). Ilkogretim Online. 20(4).

Meiryani, M., and et. al. 2021, July. Analysis of Technology Acceptance Model (TAM)

Approach to the Quality of Accounting Information Systems. In The 2021 9th International

Conference on Computer and Communications Management (pp. 37-45).

Ustinova, Y., 2020, October. Intellectual Capital of a Company in the Financial Statements: The

Reasons of Information Deficit and the Ways of it Overcoming. In International Conference on

Comprehensible Science (pp. 81-90). Springer, Cham.

Books and Journals

Monahan, S.J., 2018. Financial statement analysis and earnings forecasting. Foundations and

Trends® in Accounting. 12(2). pp.105-215.

Ariyawansa, H.D.G.R. and Nanayakkara, K.G.M., 2021. Financial statement informativeness

and intellectual capital disclosures: with special reference to listed companies in srilanka.

Zeller, T., Kostolansky, J. and Bozoudis, M., 2019. An IFRS-based taxonomy of financial

ratios. Accounting Research Journal.

Lessambo, F.I., 2018. Audit tools: Financial ratios analysis. In Auditing, assurance services, and

forensics (pp. 371-394). Palgrave Macmillan, Cham.

Pouliasis, P.K., Papapostolou, N.C. and Visvikis, I.D., 2018. Investor Sentiment, Earnings

Growth, and Volatility: Strategies for Finance in International Shipping. In Finance and Risk

Management for International Logistics and the Supply Chain (pp. 109-127). Elsevier.

Reinganum, M.R., 1999. The significance of market capitalization in portfolio management over

time. Journal of Portfolio Management. 25(4). p.39.

Beaver, W.H., 1966. Financial ratios as predictors of failure. Journal of accounting research,

pp.71-111.

Çelik, E. and Arslanli, K.Y., 2021. The idiosyncratic characteristics of Turkish REITs: evidence

from financial ratios. Journal of European Real Estate Research.

Mohammed, A., and et. al., 2020. Characterization and modeling the flow behavior and

compression strength of the cement paste modified with silica nano-size at different temperature

conditions. Construction and Building Materials. 257. p.119590.

Hasan, M.M. and Taylor, G., 2020. Financial statement comparability and bank risk-

taking. Journal of Contemporary Accounting & Economics. 16(3). p.100206.

Talha, M., 2021. FINANCIAL STATEMENT ANALYSIS OF ATLAS HONDA MOTORS,

INDUS MOTORS AND PAK SUZUKI MOTORS (EVIDENCE FROM

PAKISTAN). Ilkogretim Online. 20(4).

Meiryani, M., and et. al. 2021, July. Analysis of Technology Acceptance Model (TAM)

Approach to the Quality of Accounting Information Systems. In The 2021 9th International

Conference on Computer and Communications Management (pp. 37-45).

Ustinova, Y., 2020, October. Intellectual Capital of a Company in the Financial Statements: The

Reasons of Information Deficit and the Ways of it Overcoming. In International Conference on

Comprehensible Science (pp. 81-90). Springer, Cham.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.