Financial Analysis Assignment: Detailed Analysis and Calculations

VerifiedAdded on 2020/05/28

|38

|7207

|71

Homework Assignment

AI Summary

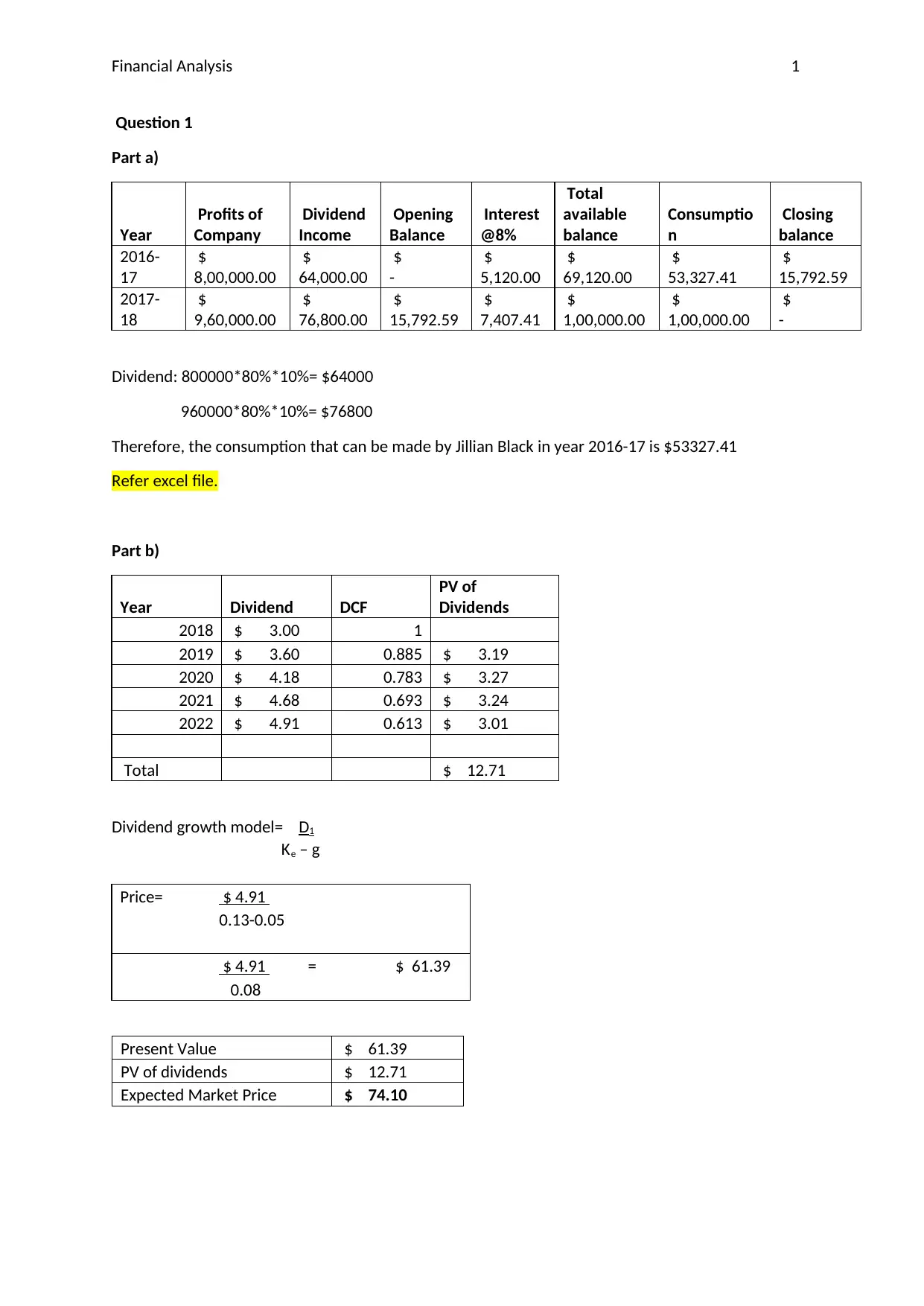

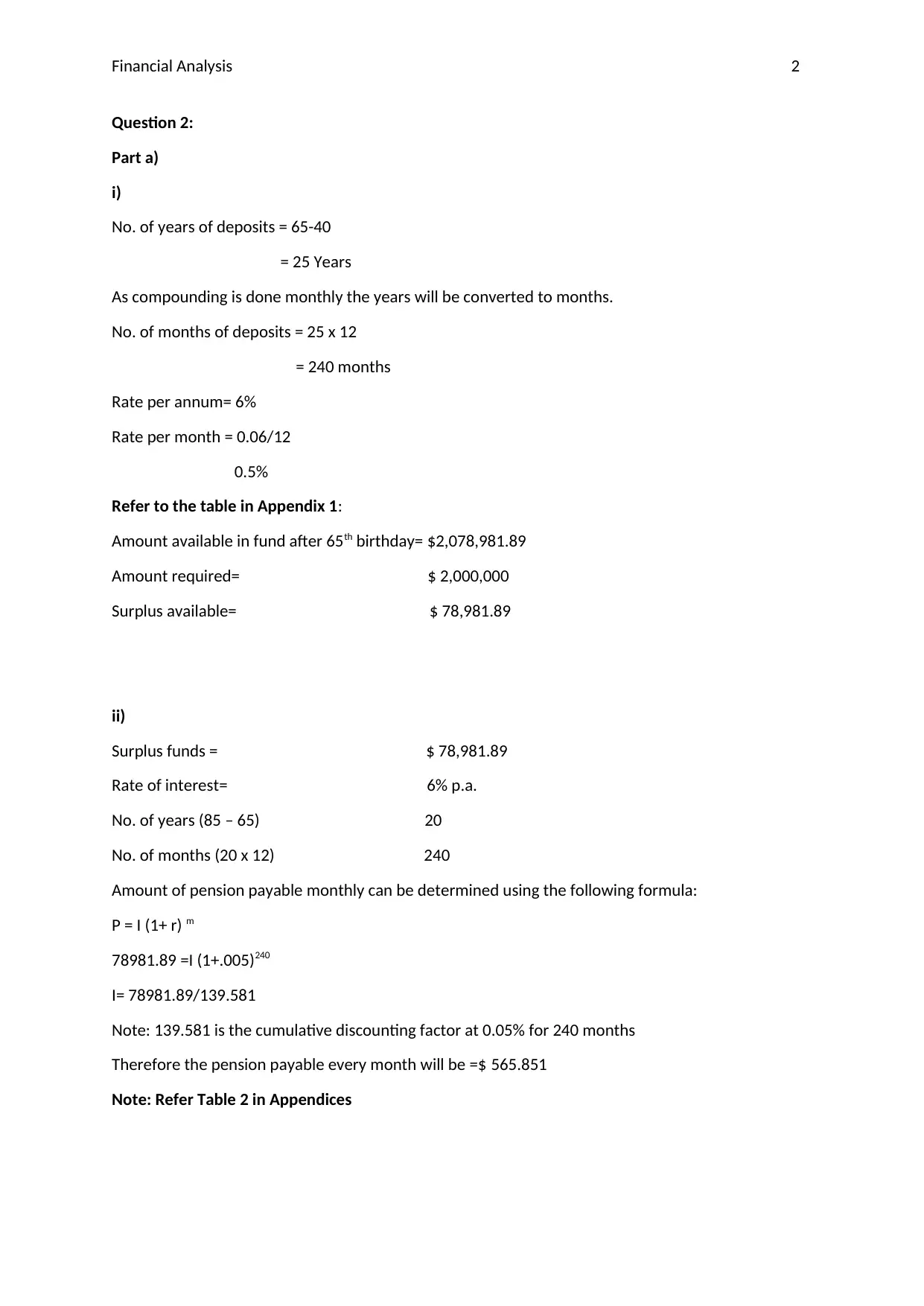

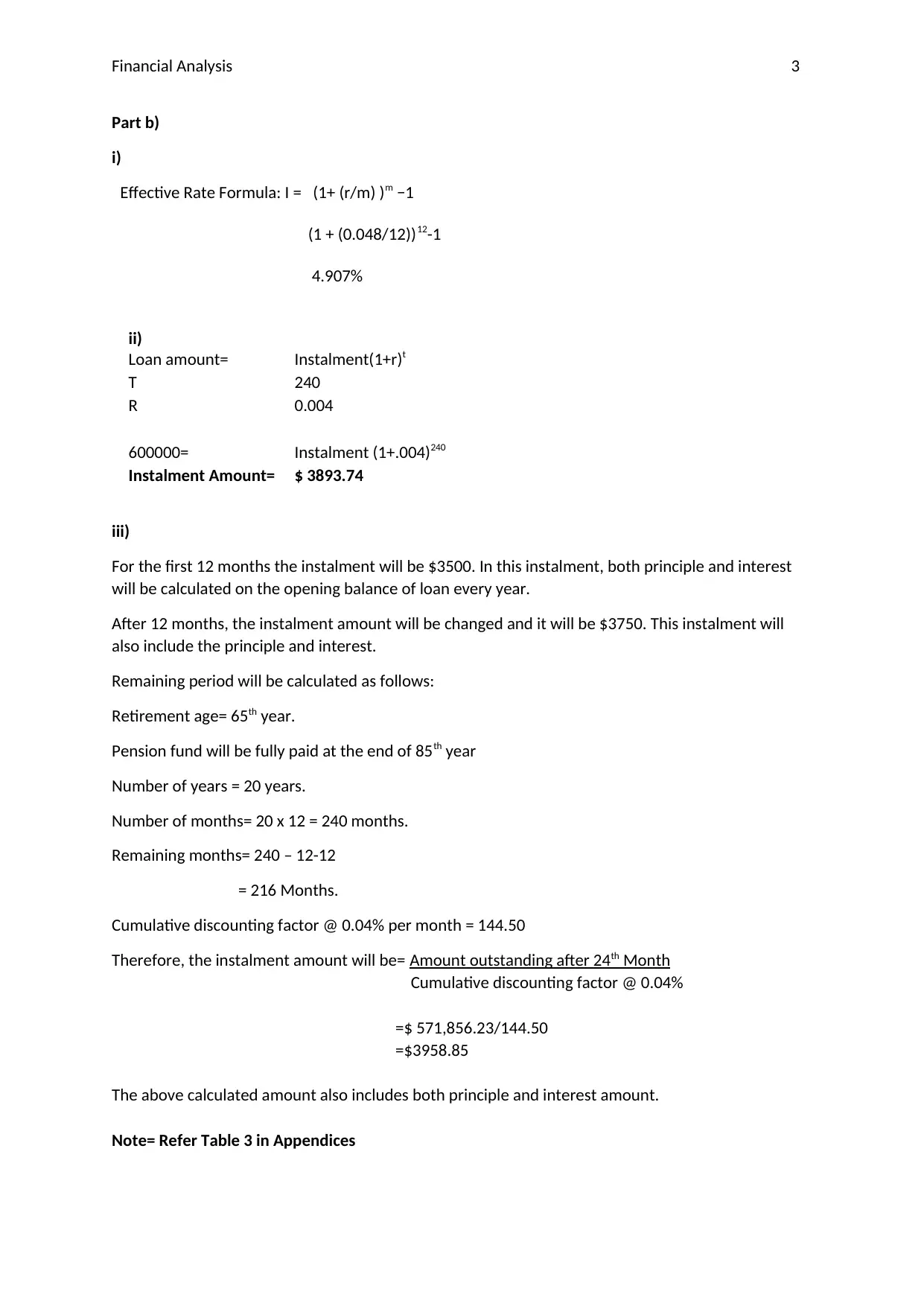

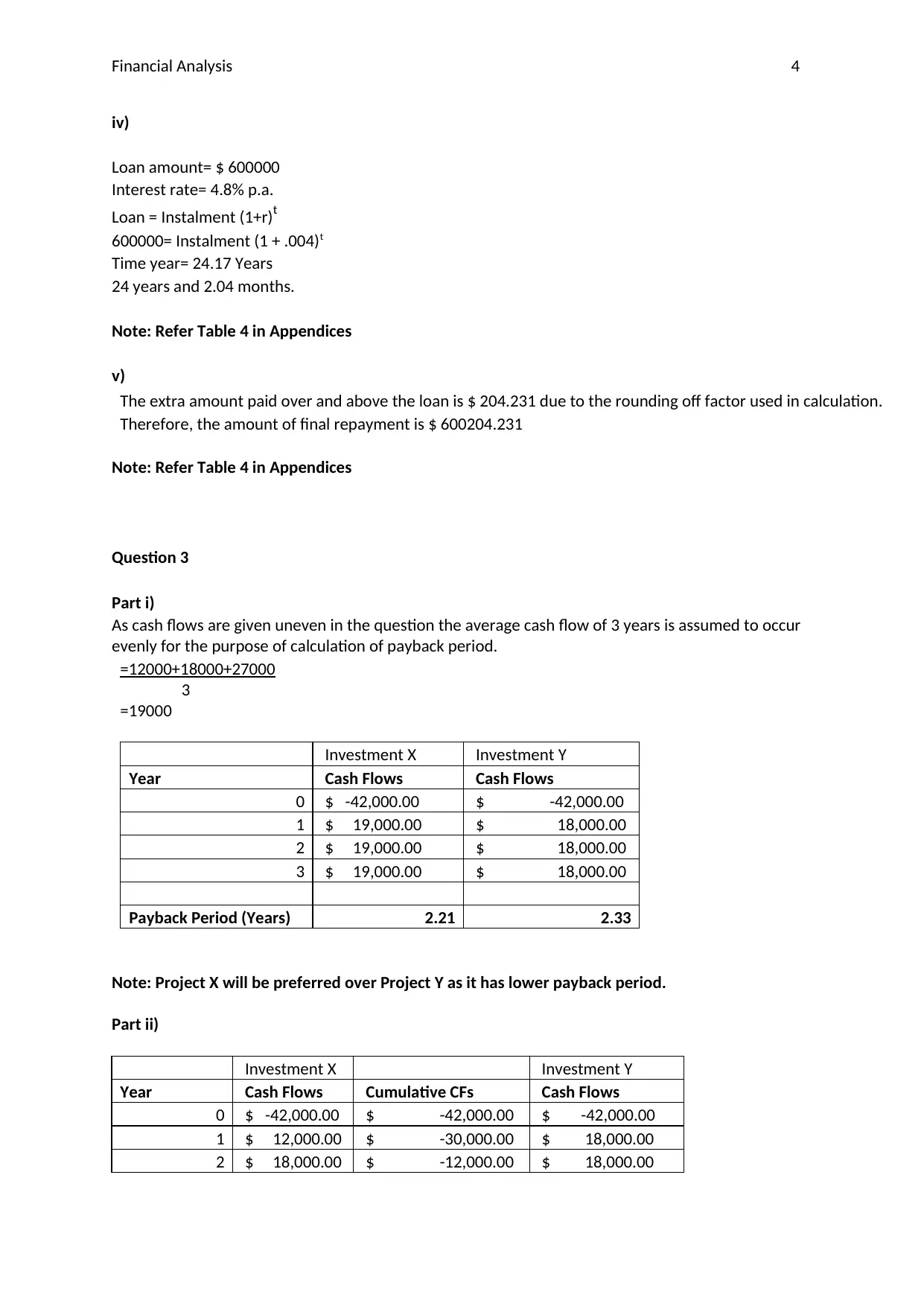

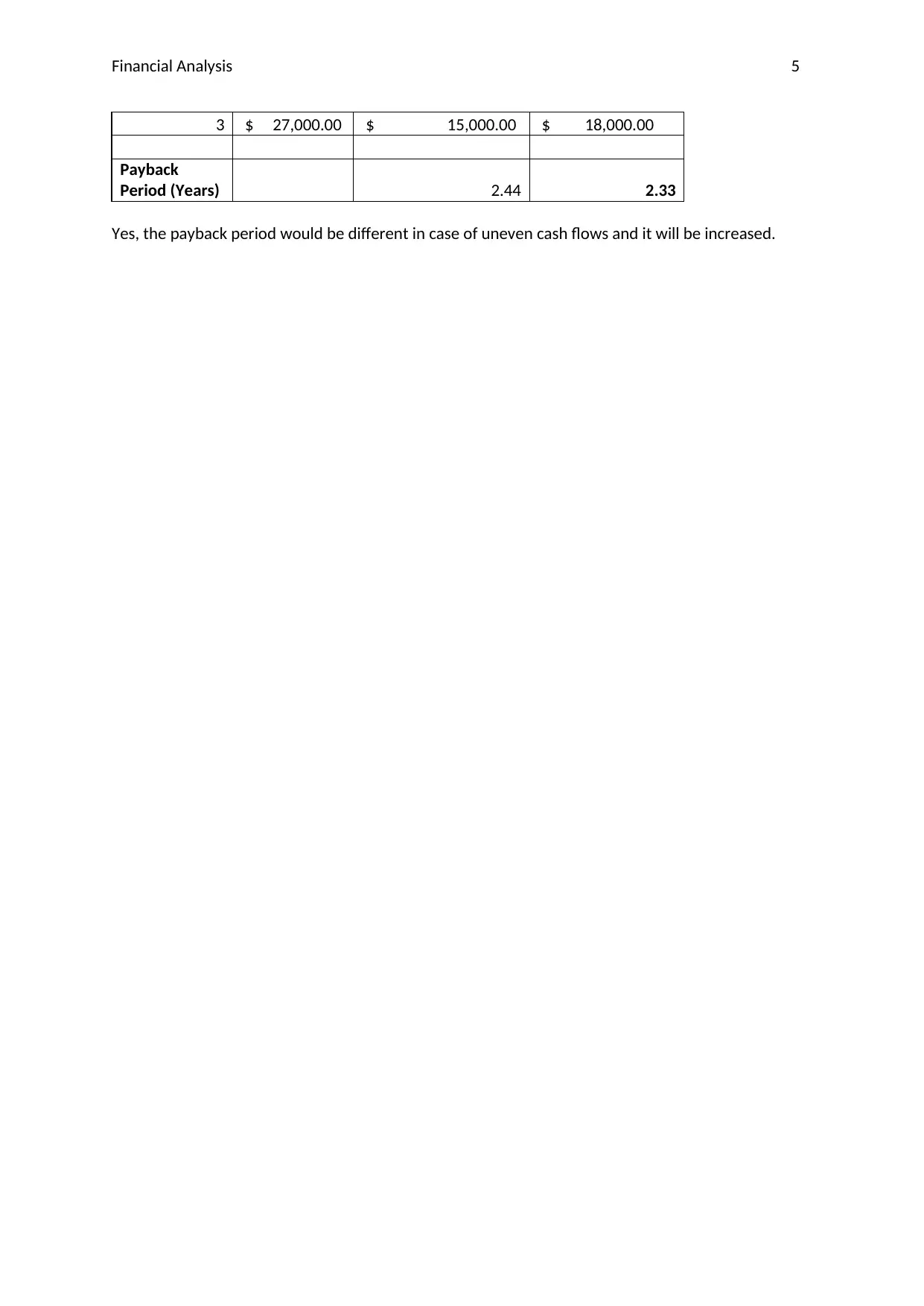

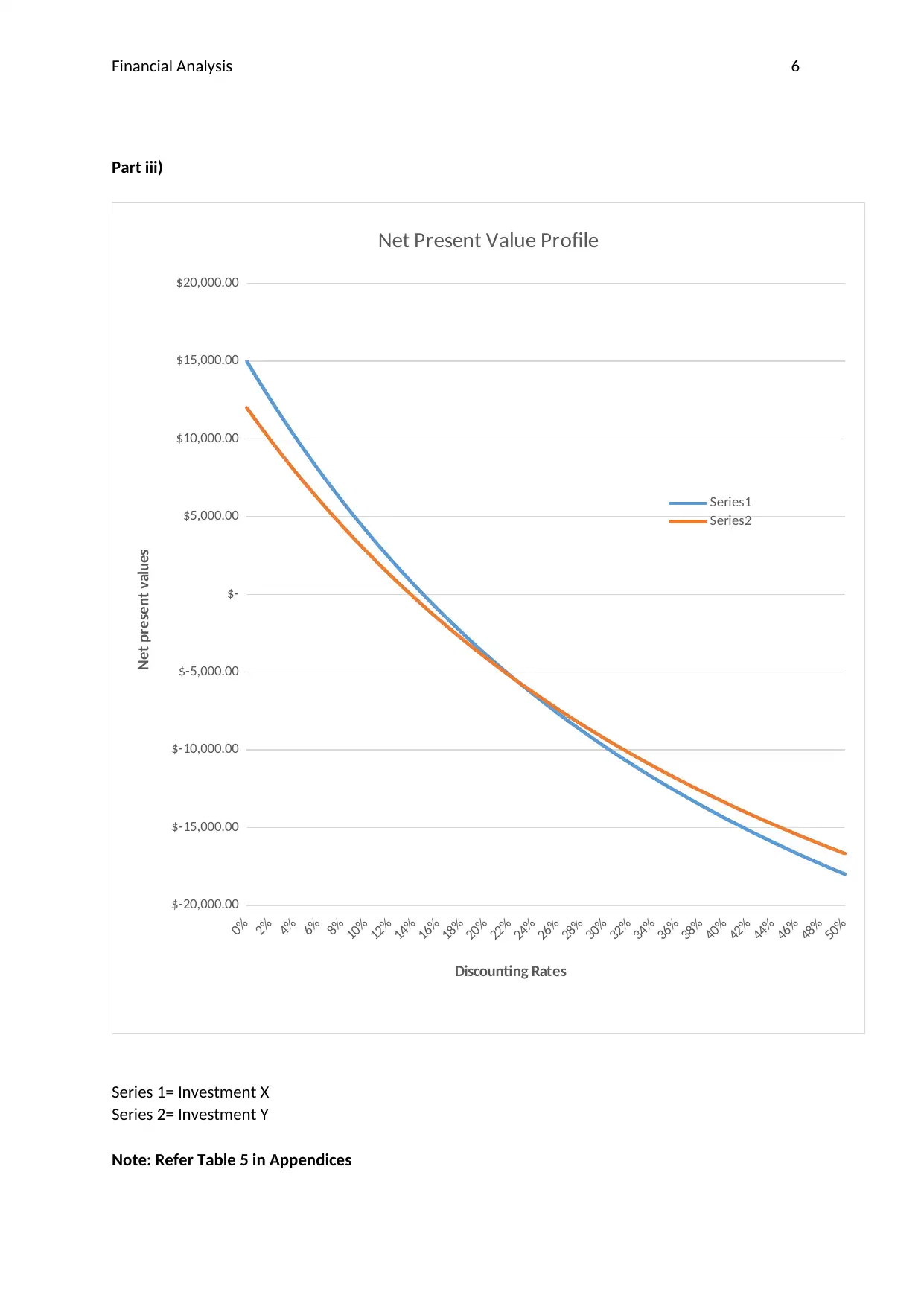

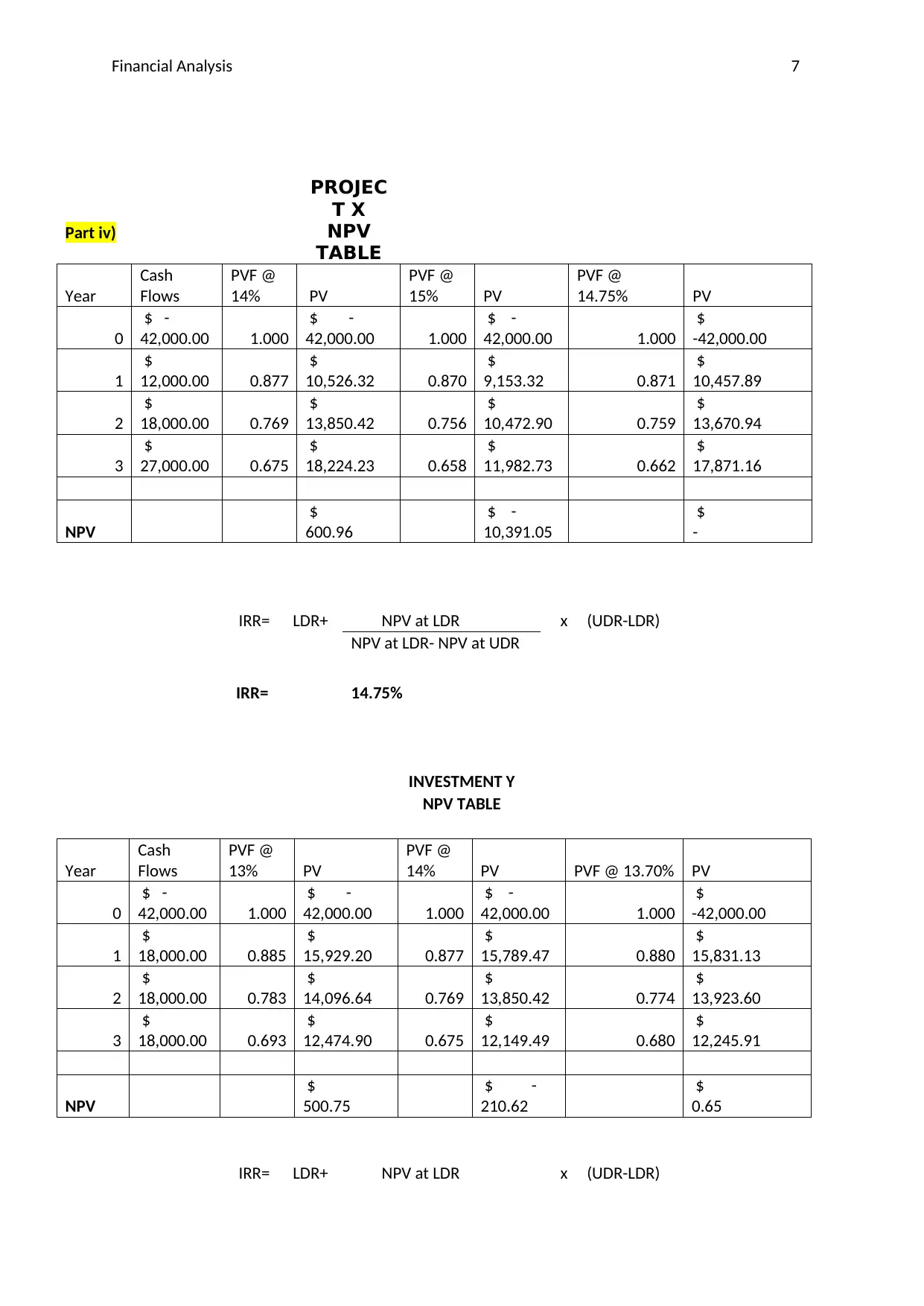

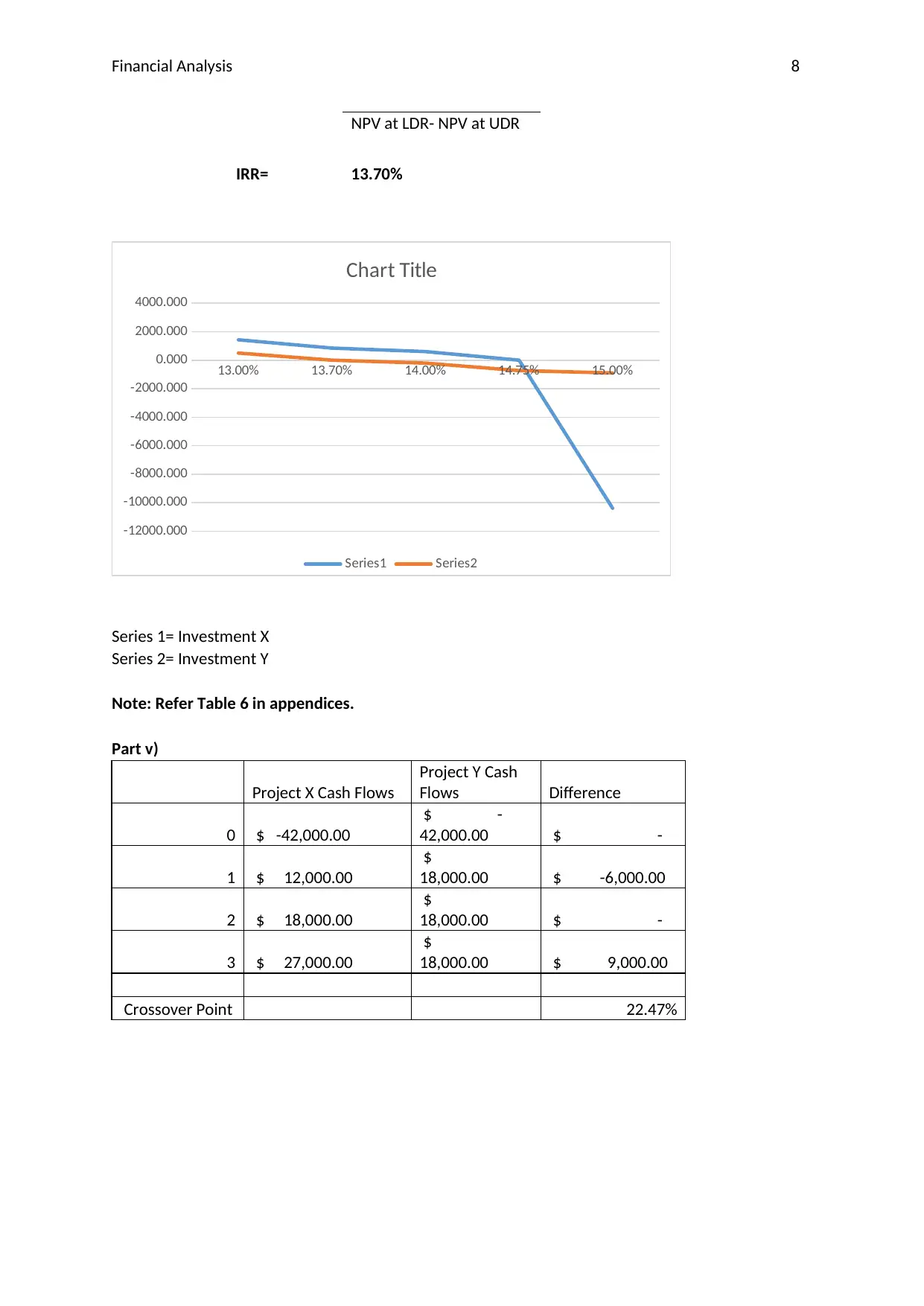

This document presents a comprehensive financial analysis assignment solution. It begins with an analysis of a company's profits, dividend income, and consumption, including calculations for available balance and closing balance over two years. Part B delves into dividend discount models, calculating present values of dividends and expected market prices. The assignment then moves into investment and loan analysis, determining amounts available in funds, pension payments, effective interest rates, and loan installments. It explores payback periods for different investment projects under both even and uneven cash flows, calculating NPV and IRR. The final section analyzes the financial implications of a technology purchase, assessing the impact on labor costs, depreciation, and tax benefits, ultimately determining whether the purchase is financially viable.

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.