Analysis of Cash Budget and Zero-Based Budgeting for St Brides Group

VerifiedAdded on 2023/01/09

|10

|2673

|35

Report

AI Summary

This report provides a financial analysis of the St Brides Group, a hotel and accommodation provider. It begins with an introduction to the company and then delves into two key tasks. The first task focuses on preparing a cash budget, outlining the advantages and disadvantages of this budgeting method and presenting a detailed cash budget for the group. The second task explores zero-based budgeting (ZBB), including its process, decision units, decision packages, and the advantages of ZBB over traditional budgeting, alongside a discussion on how an organization can implement ZBB practically. The report concludes with a summary of the key findings and provides references to the sources used.

St Brides Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Preparing the budget in cash...................................................................................................3

TASK 2............................................................................................................................................6

Details of Zero based Budgeting............................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Preparing the budget in cash...................................................................................................3

TASK 2............................................................................................................................................6

Details of Zero based Budgeting............................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

The analysis of the project is dependent on the group of hotel and accommodation provided

company "St Brides group" which controls and operates a massive resort in UK. This is

comprised of 46 spaces with 26 views to the harbour (Pinheiro, 2014). The work is split into two

assignments that consist of knowledge of various kinds. A cash budget is basically dependent on

provided financial details regarding financial transactions which are covered in first section of

report. Although a thorough review of zero-based budgeting was conducted in an appropriate

way in second part.

TASK 1

Preparing the budget in cash.

A cash budget represents a timeline or policy for expected year-round cash sales and

payments. These flows of cash include imposed income, paid savings and debt returns and

distributions. It presumes that even a cash prediction is an assessment of the businesses' future

financial position. Management usually determines the financial statement because after sales,

investments and capital spending expenses have been already made. These calculations will be

made before the distribution of the currency, such that the currency has a reasonable effect over

time. For instance, until manager can tell how often cash an income amount the mangers gets to

understand. Executives use the financial budget to manage cash flows for a business. It means

the board can ensure the company has ample cash to cover the bills. For example, the payroll has

to be paid every two weeks and the utilities have to be paid every month. The financial spending

allows administrators to anticipate deficiencies in the operating cash flow as well as to address

issues in advance of payments. In some other words, the Money Budget is a calculation in

writing about an organization's future financial situation.

It is also a detailed study of the enterprise's expected annual cash flow. The average estimation

time for cash budgets is one year, divided by monthly or annual intervals. This facilitates

convergence of the daily fluctuations of cash flow. For circumstances where cash balances are

fairly stable, the financial planner will prepare plans for just a complete year. If perceptions are

fairly volatile, he would only need a quarterly forecast. Thus the currency allocation lets the

government predict large monetary amounts. For companies it is not ideal to have large amounts

of cash left in bank accounts (Mariana, 2018). At least some money will be retained for equal

The analysis of the project is dependent on the group of hotel and accommodation provided

company "St Brides group" which controls and operates a massive resort in UK. This is

comprised of 46 spaces with 26 views to the harbour (Pinheiro, 2014). The work is split into two

assignments that consist of knowledge of various kinds. A cash budget is basically dependent on

provided financial details regarding financial transactions which are covered in first section of

report. Although a thorough review of zero-based budgeting was conducted in an appropriate

way in second part.

TASK 1

Preparing the budget in cash.

A cash budget represents a timeline or policy for expected year-round cash sales and

payments. These flows of cash include imposed income, paid savings and debt returns and

distributions. It presumes that even a cash prediction is an assessment of the businesses' future

financial position. Management usually determines the financial statement because after sales,

investments and capital spending expenses have been already made. These calculations will be

made before the distribution of the currency, such that the currency has a reasonable effect over

time. For instance, until manager can tell how often cash an income amount the mangers gets to

understand. Executives use the financial budget to manage cash flows for a business. It means

the board can ensure the company has ample cash to cover the bills. For example, the payroll has

to be paid every two weeks and the utilities have to be paid every month. The financial spending

allows administrators to anticipate deficiencies in the operating cash flow as well as to address

issues in advance of payments. In some other words, the Money Budget is a calculation in

writing about an organization's future financial situation.

It is also a detailed study of the enterprise's expected annual cash flow. The average estimation

time for cash budgets is one year, divided by monthly or annual intervals. This facilitates

convergence of the daily fluctuations of cash flow. For circumstances where cash balances are

fairly stable, the financial planner will prepare plans for just a complete year. If perceptions are

fairly volatile, he would only need a quarterly forecast. Thus the currency allocation lets the

government predict large monetary amounts. For companies it is not ideal to have large amounts

of cash left in bank accounts (Mariana, 2018). At least some money will be retained for equal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

benefit. Excessive money is indeed suitable to increasing and making new transactions, rather

than remaining untouched in customer accounts. The financial distribution allows management

to properly track and adjust the economic rates. There are certain disadvantages and merits to

this budget such as:

Advantages Disadvantages

A cash-only strategy enforces smart decisions

for families and businesses. Either businesses

hit ends and live easily, or they don't have to

work to handle cash if they really needed. This

is a process that needs a great deal of

commitment to detail, monitoring of individual

expenditure and diligent handling even as

enough money is provided to satisfy any

necessity.

Manager of company should manage the Cash

Budgets properly otherwise figures may be

changed. For instance, making an impressive

transaction between 1 or 2 days even before

closing of the month which may be confusing

rather than after the start of the monthly period.

This eliminates one cash flow period and

places pressure on another activities.

The accompanying cash budget is prepared and presented below in compliance with the

provided financial data relating to the St Brids Group:

Particulars

Jan

uar

y

Feb

ruar

y

Mar

ch

Apr

il

Ma

y

Jun

e July

Aug

ust

Sept

emb

er

Oct

obe

r

Nov

emb

er

Dec

emb

er

Cash sales

117

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash balance

120

00

Total cash

received

129

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash payments

Spent on new

hybrid motor

220

00

than remaining untouched in customer accounts. The financial distribution allows management

to properly track and adjust the economic rates. There are certain disadvantages and merits to

this budget such as:

Advantages Disadvantages

A cash-only strategy enforces smart decisions

for families and businesses. Either businesses

hit ends and live easily, or they don't have to

work to handle cash if they really needed. This

is a process that needs a great deal of

commitment to detail, monitoring of individual

expenditure and diligent handling even as

enough money is provided to satisfy any

necessity.

Manager of company should manage the Cash

Budgets properly otherwise figures may be

changed. For instance, making an impressive

transaction between 1 or 2 days even before

closing of the month which may be confusing

rather than after the start of the monthly period.

This eliminates one cash flow period and

places pressure on another activities.

The accompanying cash budget is prepared and presented below in compliance with the

provided financial data relating to the St Brids Group:

Particulars

Jan

uar

y

Feb

ruar

y

Mar

ch

Apr

il

Ma

y

Jun

e July

Aug

ust

Sept

emb

er

Oct

obe

r

Nov

emb

er

Dec

emb

er

Cash sales

117

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash balance

120

00

Total cash

received

129

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash payments

Spent on new

hybrid motor

220

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

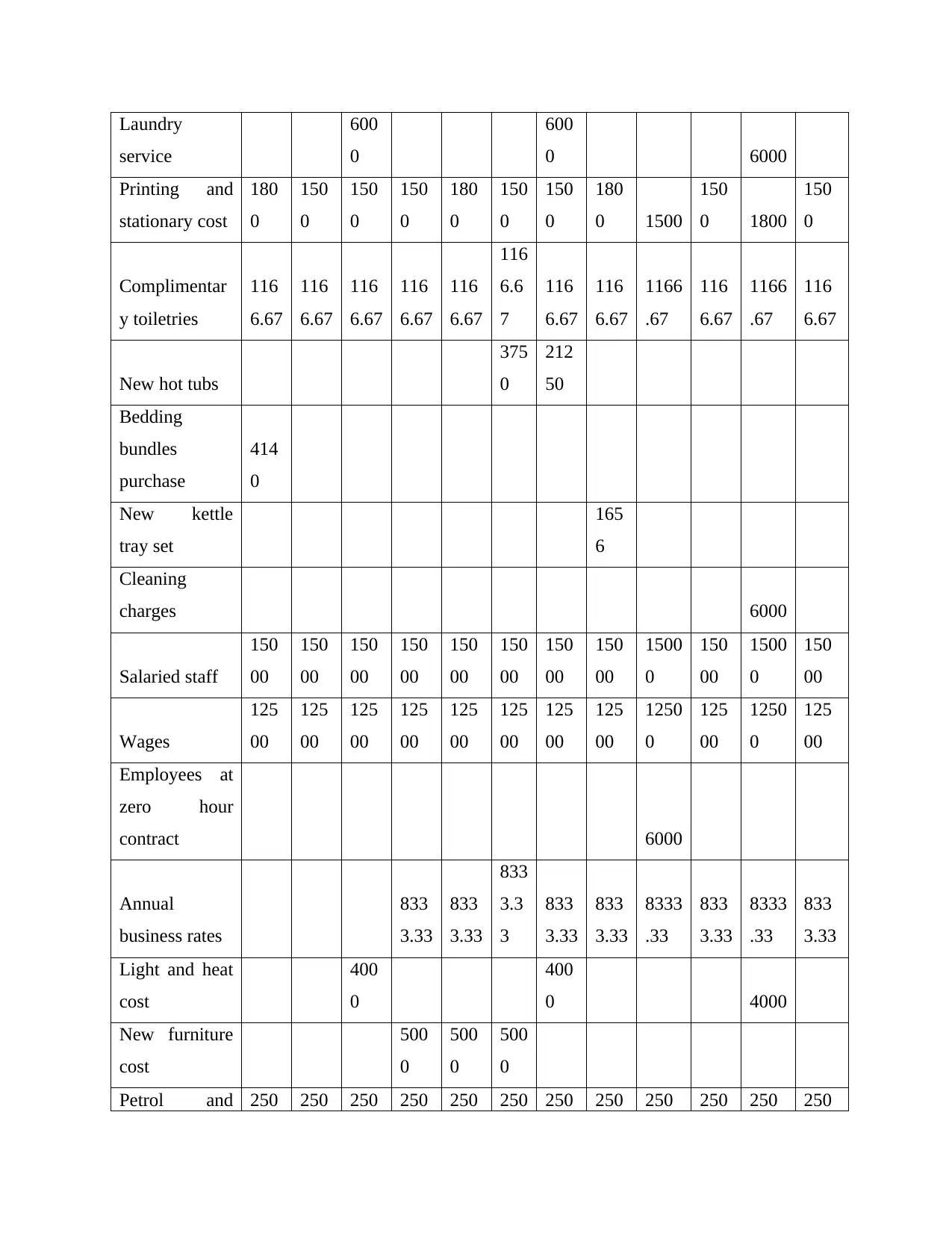

Laundry

service

600

0

600

0 6000

Printing and

stationary cost

180

0

150

0

150

0

150

0

180

0

150

0

150

0

180

0 1500

150

0 1800

150

0

Complimentar

y toiletries

116

6.67

116

6.67

116

6.67

116

6.67

116

6.67

116

6.6

7

116

6.67

116

6.67

1166

.67

116

6.67

1166

.67

116

6.67

New hot tubs

375

0

212

50

Bedding

bundles

purchase

414

0

New kettle

tray set

165

6

Cleaning

charges 6000

Salaried staff

150

00

150

00

150

00

150

00

150

00

150

00

150

00

150

00

1500

0

150

00

1500

0

150

00

Wages

125

00

125

00

125

00

125

00

125

00

125

00

125

00

125

00

1250

0

125

00

1250

0

125

00

Employees at

zero hour

contract 6000

Annual

business rates

833

3.33

833

3.33

833

3.3

3

833

3.33

833

3.33

8333

.33

833

3.33

8333

.33

833

3.33

Light and heat

cost

400

0

400

0 4000

New furniture

cost

500

0

500

0

500

0

Petrol and 250 250 250 250 250 250 250 250 250 250 250 250

service

600

0

600

0 6000

Printing and

stationary cost

180

0

150

0

150

0

150

0

180

0

150

0

150

0

180

0 1500

150

0 1800

150

0

Complimentar

y toiletries

116

6.67

116

6.67

116

6.67

116

6.67

116

6.67

116

6.6

7

116

6.67

116

6.67

1166

.67

116

6.67

1166

.67

116

6.67

New hot tubs

375

0

212

50

Bedding

bundles

purchase

414

0

New kettle

tray set

165

6

Cleaning

charges 6000

Salaried staff

150

00

150

00

150

00

150

00

150

00

150

00

150

00

150

00

1500

0

150

00

1500

0

150

00

Wages

125

00

125

00

125

00

125

00

125

00

125

00

125

00

125

00

1250

0

125

00

1250

0

125

00

Employees at

zero hour

contract 6000

Annual

business rates

833

3.33

833

3.33

833

3.3

3

833

3.33

833

3.33

8333

.33

833

3.33

8333

.33

833

3.33

Light and heat

cost

400

0

400

0 4000

New furniture

cost

500

0

500

0

500

0

Petrol and 250 250 250 250 250 250 250 250 250 250 250 250

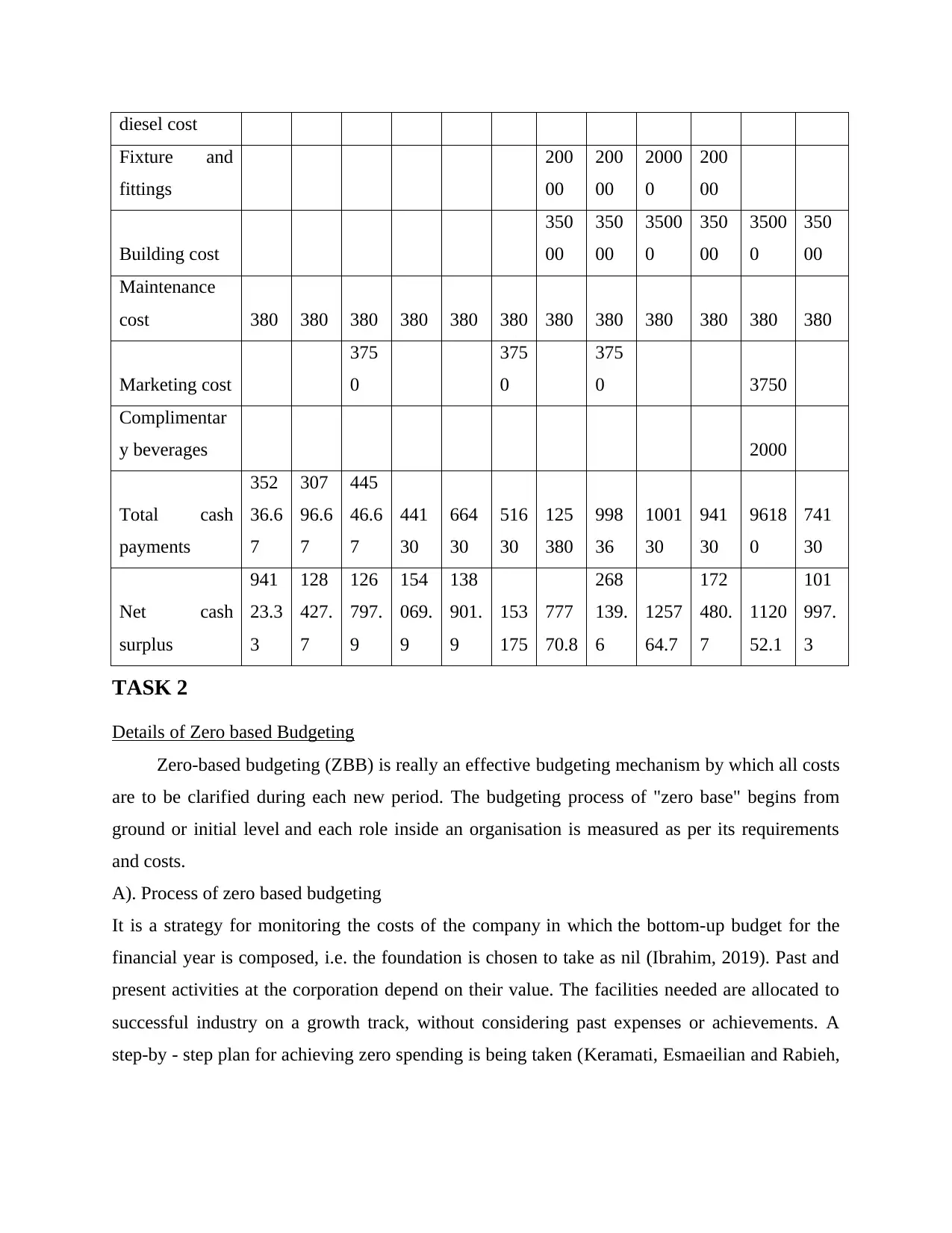

diesel cost

Fixture and

fittings

200

00

200

00

2000

0

200

00

Building cost

350

00

350

00

3500

0

350

00

3500

0

350

00

Maintenance

cost 380 380 380 380 380 380 380 380 380 380 380 380

Marketing cost

375

0

375

0

375

0 3750

Complimentar

y beverages 2000

Total cash

payments

352

36.6

7

307

96.6

7

445

46.6

7

441

30

664

30

516

30

125

380

998

36

1001

30

941

30

9618

0

741

30

Net cash

surplus

941

23.3

3

128

427.

7

126

797.

9

154

069.

9

138

901.

9

153

175

777

70.8

268

139.

6

1257

64.7

172

480.

7

1120

52.1

101

997.

3

TASK 2

Details of Zero based Budgeting

Zero-based budgeting (ZBB) is really an effective budgeting mechanism by which all costs

are to be clarified during each new period. The budgeting process of "zero base" begins from

ground or initial level and each role inside an organisation is measured as per its requirements

and costs.

A). Process of zero based budgeting

It is a strategy for monitoring the costs of the company in which the bottom-up budget for the

financial year is composed, i.e. the foundation is chosen to take as nil (Ibrahim, 2019). Past and

present activities at the corporation depend on their value. The facilities needed are allocated to

successful industry on a growth track, without considering past expenses or achievements. A

step-by - step plan for achieving zero spending is being taken (Keramati, Esmaeilian and Rabieh,

Fixture and

fittings

200

00

200

00

2000

0

200

00

Building cost

350

00

350

00

3500

0

350

00

3500

0

350

00

Maintenance

cost 380 380 380 380 380 380 380 380 380 380 380 380

Marketing cost

375

0

375

0

375

0 3750

Complimentar

y beverages 2000

Total cash

payments

352

36.6

7

307

96.6

7

445

46.6

7

441

30

664

30

516

30

125

380

998

36

1001

30

941

30

9618

0

741

30

Net cash

surplus

941

23.3

3

128

427.

7

126

797.

9

154

069.

9

138

901.

9

153

175

777

70.8

268

139.

6

1257

64.7

172

480.

7

1120

52.1

101

997.

3

TASK 2

Details of Zero based Budgeting

Zero-based budgeting (ZBB) is really an effective budgeting mechanism by which all costs

are to be clarified during each new period. The budgeting process of "zero base" begins from

ground or initial level and each role inside an organisation is measured as per its requirements

and costs.

A). Process of zero based budgeting

It is a strategy for monitoring the costs of the company in which the bottom-up budget for the

financial year is composed, i.e. the foundation is chosen to take as nil (Ibrahim, 2019). Past and

present activities at the corporation depend on their value. The facilities needed are allocated to

successful industry on a growth track, without considering past expenses or achievements. A

step-by - step plan for achieving zero spending is being taken (Keramati, Esmaeilian and Rabieh,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015). Manager of company clarify the efforts made in zero budgeting in greater details as

it consists of a mechanism which is as described underneath:

Identifying decision units: The very first and primary phase throughout the zero-based

budgeting process is the definition of a decision unit. A mechanism for decision-making

might have been an isolated and important distinguishing single event or chain of

operation. The process is separate and does not personally influence any actions. Every

individual that makes decisions is also special. A corporation has many mechanisms for

taking decisions. Any absorption costing, such as marketing, distribution, human

resources, research and development, is a unit of operation. This move is important to

clarify every aspect of spending for the budget. The manager of the decision unit needs to

justify the cost and the distribution of the budget to his decision unit. Steps of Zero

Dependent Budgeting (ZBB) rely on management's justification and on the prior year’s

expenditure or the policy entity’s contribution for the past year. Since zero-based

financial planning is designed for the program from start, it can even be newly explained

for the correct year.

Decision packages: Determination units specified at the early phase are broken up into smaller

packages of decisions. In the method. These collections of acts must comply with the priorities

of the organization. Increasing decision bundle acts as an independent program requiring

distribution of funds (Hernandez, Jonker and Kosse, 2017). Every policy package outlines the

project's functions, responsibilities, and activities, the criteria for suggestions, its financial and

quantitative benefits, the absence of opportunities when the project gets funding, etc. A

structured set of decisions has to include the necessary statement:

1. The reason where the actions are made.

2. The wider decision-making tower's objectives and goals.

3. Decision Package Objectives and Priorities.

4. Role requires review.

5. Evaluation of the technical and operational viability of the mission.

6. Alternative route review.

Items for rating choices: This really is the 3 stage of budgeting process, in which all

judgment packs are grouped in the priority order and choice inside the judgement unit as

well as between specific units of judgment (Abioro, 2013). The reason around focus

it consists of a mechanism which is as described underneath:

Identifying decision units: The very first and primary phase throughout the zero-based

budgeting process is the definition of a decision unit. A mechanism for decision-making

might have been an isolated and important distinguishing single event or chain of

operation. The process is separate and does not personally influence any actions. Every

individual that makes decisions is also special. A corporation has many mechanisms for

taking decisions. Any absorption costing, such as marketing, distribution, human

resources, research and development, is a unit of operation. This move is important to

clarify every aspect of spending for the budget. The manager of the decision unit needs to

justify the cost and the distribution of the budget to his decision unit. Steps of Zero

Dependent Budgeting (ZBB) rely on management's justification and on the prior year’s

expenditure or the policy entity’s contribution for the past year. Since zero-based

financial planning is designed for the program from start, it can even be newly explained

for the correct year.

Decision packages: Determination units specified at the early phase are broken up into smaller

packages of decisions. In the method. These collections of acts must comply with the priorities

of the organization. Increasing decision bundle acts as an independent program requiring

distribution of funds (Hernandez, Jonker and Kosse, 2017). Every policy package outlines the

project's functions, responsibilities, and activities, the criteria for suggestions, its financial and

quantitative benefits, the absence of opportunities when the project gets funding, etc. A

structured set of decisions has to include the necessary statement:

1. The reason where the actions are made.

2. The wider decision-making tower's objectives and goals.

3. Decision Package Objectives and Priorities.

4. Role requires review.

5. Evaluation of the technical and operational viability of the mission.

6. Alternative route review.

Items for rating choices: This really is the 3 stage of budgeting process, in which all

judgment packs are grouped in the priority order and choice inside the judgement unit as

well as between specific units of judgment (Abioro, 2013). The reason around focus

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decision-making processes is for the efficient allocation of finite resources. Decision

services are evaluated according to a cost-benefit analysis. Throughout that step all

options are evaluated to pick the easiest and most cost-effective choices and the higher

authority retains the right to support or reject decision-making. Only certain judgment

bundle which allows the team meet its defined goal is approved.

Distribution of existing resources: The final step will implement the zero-based

budgeting process. Financial support is issued at this point for the decision packages that

are mentioned during the last process. So we should conclude that the financing

judgments are being taken in this process. The distribution of funds and other factors is

directed towards the ranking of the judgment kit. Strengthened assistance is therefore

provided for the most effective packages of decisions. This ensures the important

resources are optimally used to make better results (Cox, 2014).

Managing and reporting: This is the final planning step for the ZBB as it

includes decision packages that are monitored and analysed for their efficacy and

performance. Assessing the efficacy of action packages helps administrators to know that

the services are correctly allocated or not.

Advantages of ZBB over traditional budgeting.

The ZBB plays a vital role in different company in different forms that help to make better

results. Throughout the situation of the above-mentioned hotel, they should extend this

expenditure plan which in future will participate in a really way and give various advantages

(Cotter and Fritzsche, 2014). Some of these are discussed below:

Contrary to conventional budgeting methods requiring discretionary budgetary changes

in the intervening year, zero-based budgeting requires all agencies to control and

calculate cash flow operations. It helps to reduce spending in a way that it gives a

straightforward picture of spending against the goal goals.

It also improves departmental trust and collaboration as well as encourages workers to

provide their opinion which ease the decision making process.

The goal is to ensure an optimal distribution of capital (departments-wise), since it does

not evaluate numbers nor addresses existing figures.

It allows finding possible and cost-effective solutions to doing issues by eliminating any

unproductive or destructive activity.

services are evaluated according to a cost-benefit analysis. Throughout that step all

options are evaluated to pick the easiest and most cost-effective choices and the higher

authority retains the right to support or reject decision-making. Only certain judgment

bundle which allows the team meet its defined goal is approved.

Distribution of existing resources: The final step will implement the zero-based

budgeting process. Financial support is issued at this point for the decision packages that

are mentioned during the last process. So we should conclude that the financing

judgments are being taken in this process. The distribution of funds and other factors is

directed towards the ranking of the judgment kit. Strengthened assistance is therefore

provided for the most effective packages of decisions. This ensures the important

resources are optimally used to make better results (Cox, 2014).

Managing and reporting: This is the final planning step for the ZBB as it

includes decision packages that are monitored and analysed for their efficacy and

performance. Assessing the efficacy of action packages helps administrators to know that

the services are correctly allocated or not.

Advantages of ZBB over traditional budgeting.

The ZBB plays a vital role in different company in different forms that help to make better

results. Throughout the situation of the above-mentioned hotel, they should extend this

expenditure plan which in future will participate in a really way and give various advantages

(Cotter and Fritzsche, 2014). Some of these are discussed below:

Contrary to conventional budgeting methods requiring discretionary budgetary changes

in the intervening year, zero-based budgeting requires all agencies to control and

calculate cash flow operations. It helps to reduce spending in a way that it gives a

straightforward picture of spending against the goal goals.

It also improves departmental trust and collaboration as well as encourages workers to

provide their opinion which ease the decision making process.

The goal is to ensure an optimal distribution of capital (departments-wise), since it does

not evaluate numbers nor addresses existing figures.

It allows finding possible and cost-effective solutions to doing issues by eliminating any

unproductive or destructive activity.

How organization can introduce this budget in practical terms.

ZBB promotes the implementation of top-level organizational goals during the budgeting

process by linking them to specific company operating zones, where investments can then be

clustered and measured against historical performance and current objectives (Cox, 2014). These

can be incorporated in the operational life of businesses by determining their needs and

conducting the essence of the activities within the company. In each segment, this can be

extended, as in the instance from the above hotel, if it is division of financing or human resource.

Through applying this strategy, having consistency of financial details would become simpler for

the above-mentioned business management and they will be likely to find better and effective

use of financial capital.

CONCLUSION

In the end of report, it has been founded that hotel must prepare detailed cash budged for

each and every activity so that task can be managed in a way to giver higher results to increase

the productivity of entire company. Budgets are Very much important in terms of effective

financial performance. Budgets offer an outline about the process to make much better use of

financial capital. The study expresses on the financial plan as well as its importance for

companies. In keeping with the financial data provided, an expenditure plan is also planned. It

can be inferred from the 2 part of the study that zero-based budget is really an efficient budget

and can offer consistency in money transfers and also be applied in any company. This help to

save time and cost which can further be used in other term that increase the profitability of St

Brids group.

ZBB promotes the implementation of top-level organizational goals during the budgeting

process by linking them to specific company operating zones, where investments can then be

clustered and measured against historical performance and current objectives (Cox, 2014). These

can be incorporated in the operational life of businesses by determining their needs and

conducting the essence of the activities within the company. In each segment, this can be

extended, as in the instance from the above hotel, if it is division of financing or human resource.

Through applying this strategy, having consistency of financial details would become simpler for

the above-mentioned business management and they will be likely to find better and effective

use of financial capital.

CONCLUSION

In the end of report, it has been founded that hotel must prepare detailed cash budged for

each and every activity so that task can be managed in a way to giver higher results to increase

the productivity of entire company. Budgets are Very much important in terms of effective

financial performance. Budgets offer an outline about the process to make much better use of

financial capital. The study expresses on the financial plan as well as its importance for

companies. In keeping with the financial data provided, an expenditure plan is also planned. It

can be inferred from the 2 part of the study that zero-based budget is really an efficient budget

and can offer consistency in money transfers and also be applied in any company. This help to

save time and cost which can further be used in other term that increase the profitability of St

Brids group.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abioro, M., 2013. The impact of cash management on the performance of manufacturing

companies in Nigeria. Uncertain Supply chain management, 1(3), pp.177-192.

Cotter, R. V. and Fritzsche, D. J., 2014, March. The business policy game. In Developments in

Business Simulation and Experiential Learning: Proceedings of the Annual ABSEL

conference (Vol. 21).

Cox, P., 2014. Master budget project: Analysis of cash budget report. Strategic Finance, 95(9),

p.52.

Cox, P., 2014. Master budget project: cash budget macro. Strategic Finance, 96(4), pp.54-56.

Hernandez, L., Jonker, N. and Kosse, A., 2017. Cash versus debit card: The role of budget

control. Journal of Consumer Affairs, 51(1), pp.91-112.

Keramati, A., Esmaeilian, M. and Rabieh, M., 2015. Developing a Model for Project Scheduling

with Limited resources and Budget with Considering Discounted Cash Flows through

Fixed Prioritization Method. Asian Journal of Research in Business Economics and

Management, 5(1), pp.212-220.

Mariana, Z., 2018. THE CASH BUDGET–A SHORT-TERM FORECAST TOOL FOR THE

FINANCIAL STATEMENTS OF ECONOMIC ENTITIES. Ecoforum Journal, 7(2).

Pinheiro, J. D. O. G., 2014. Cash budget versus financial budget: advantages and disadvantages:

a case study (Doctoral dissertation).

Books and Journals

Abioro, M., 2013. The impact of cash management on the performance of manufacturing

companies in Nigeria. Uncertain Supply chain management, 1(3), pp.177-192.

Cotter, R. V. and Fritzsche, D. J., 2014, March. The business policy game. In Developments in

Business Simulation and Experiential Learning: Proceedings of the Annual ABSEL

conference (Vol. 21).

Cox, P., 2014. Master budget project: Analysis of cash budget report. Strategic Finance, 95(9),

p.52.

Cox, P., 2014. Master budget project: cash budget macro. Strategic Finance, 96(4), pp.54-56.

Hernandez, L., Jonker, N. and Kosse, A., 2017. Cash versus debit card: The role of budget

control. Journal of Consumer Affairs, 51(1), pp.91-112.

Keramati, A., Esmaeilian, M. and Rabieh, M., 2015. Developing a Model for Project Scheduling

with Limited resources and Budget with Considering Discounted Cash Flows through

Fixed Prioritization Method. Asian Journal of Research in Business Economics and

Management, 5(1), pp.212-220.

Mariana, Z., 2018. THE CASH BUDGET–A SHORT-TERM FORECAST TOOL FOR THE

FINANCIAL STATEMENTS OF ECONOMIC ENTITIES. Ecoforum Journal, 7(2).

Pinheiro, J. D. O. G., 2014. Cash budget versus financial budget: advantages and disadvantages:

a case study (Doctoral dissertation).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.