Comprehensive Financial Management and Analysis of Starbucks Coffee

VerifiedAdded on 2020/10/20

|21

|4466

|116

Report

AI Summary

This report presents a comprehensive financial analysis of Starbucks Coffee Company, examining its performance through various financial ratios. It begins with an introduction to financial management and the company background of Starbucks. The analysis covers liquidity ratios (current and quick ratios), long-term solvency ratios (debt-to-equity ratio), profitability ratios (gross profit ratio, return on equity), asset management ratios (inventory turnover, asset turnover), and market value ratios (earnings per share, dividend per share). The report calculates and interprets these ratios over a five-year period, providing insights into Starbucks' financial health, operational efficiency, and ability to manage its debts and generate profits. The analysis also includes graphical representations for easy understanding and discusses the limitations of ratio analysis. The report concludes with a summary of the findings and references used.

An Assignment on

Financial Management and Analysis

Financial Management and Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................... 2

Company background of Starbuck Coffee.....................................................................................3

Financial performance and ratio analysis.....................................................................................................3

2 Analysis of Liquidity Ratio......................................................................................................................4

2.1 Current ratio......................................................................................................................................4

2.2 Quick ratio or acid test.......................................................................................................................5

3. Analysis of long term solvency ratio.......................................................................................................7

3.1 debt to equity ratio.............................................................................................................................7

4. Analysis of profitability ratio...................................................................................................................9

4.1 Gross profit ratio..............................................................................................................................10

4.2 Return on Equity (ROE) ratio..........................................................................................................11

5. Analysis of asset management ratio.......................................................................................................13

5.1 Inventory turnover ratio...................................................................................................................13

5.2 Asset turnover ratio.........................................................................................................................14

6. Analysis of market value ratios.............................................................................................................16

6.1 Earnings per share...........................................................................................................................16

6.2 Dividend Per Share..........................................................................................................................17

7. Limitations of ratio analysis..................................................................................................................18

Conclusion.................................................................................................................................................19

References.................................................................................................................................................20

Page 2 of 21

Introduction................................................................................................................................... 2

Company background of Starbuck Coffee.....................................................................................3

Financial performance and ratio analysis.....................................................................................................3

2 Analysis of Liquidity Ratio......................................................................................................................4

2.1 Current ratio......................................................................................................................................4

2.2 Quick ratio or acid test.......................................................................................................................5

3. Analysis of long term solvency ratio.......................................................................................................7

3.1 debt to equity ratio.............................................................................................................................7

4. Analysis of profitability ratio...................................................................................................................9

4.1 Gross profit ratio..............................................................................................................................10

4.2 Return on Equity (ROE) ratio..........................................................................................................11

5. Analysis of asset management ratio.......................................................................................................13

5.1 Inventory turnover ratio...................................................................................................................13

5.2 Asset turnover ratio.........................................................................................................................14

6. Analysis of market value ratios.............................................................................................................16

6.1 Earnings per share...........................................................................................................................16

6.2 Dividend Per Share..........................................................................................................................17

7. Limitations of ratio analysis..................................................................................................................18

Conclusion.................................................................................................................................................19

References.................................................................................................................................................20

Page 2 of 21

Introduction

Finance is called the lifeline of business and requires efficient management to be used properly.

The concerned activities on planning, controlling, monitoring and administering the available

funds in business are called financial management. Joy Thomas , & Rabiyathulbasariya, (2017)

stated that financial management in any organization intended to achieve the reduction in finance

cost, sufficient funds availability to operate business, and efficient funds utilization and proper

procurement.

The main objective of financial management analysis and reporting is to provide useful financial

and non-financial information to existing and potential users about the financial health,

performance, continuous changing environment and performance of corporate firms to make

investing, financing and other economic decisions (Iatridis, 2010). To assess risk level against

expected returns analyzing financial statement and management process yields all valuable

information about the firm’s earning quality, co-relationships and trends, as well as the

weaknesses and strength in financial position as well as operational process to interest parties

(Peterson Drake, and Fabozzi, 2012). Management hierarchy of corporate firms are highly

concern about documentation, preparation and presentation of financial statements, relevant

notes and disclosers in reliable and understanding manner to information users such as investors,

creditors, legal authorities, government and corporate media. Also, Iatridis, (2010) demonstrated

that fulfilling the requirement of financial management and corporate reporting, business firms

fulfill the target of utilization of economic and other resources, satisfactory fulfillment of

regulations and laws, updating the cash flow and financial position, exploring future business

opportunities and most importantly satisfy user’s information needs.

Going to present in this paper, through extensive and deeper calculation and analysis of financial

and non-financial information of Starbucks Coffee Company the business strategy and policy

making, operational efficiency and performance growth or changes over couple of years.

Starbuck Coffee is a publically listed coffee shop in coffee industry, serving all over the world

with products in the category of coffee, smoothies, tea, backed products, beverages and

sandwiches and enjoy a major portion of quality minded coffee drinker’s expenditure in its own

Page 3 of 21

Finance is called the lifeline of business and requires efficient management to be used properly.

The concerned activities on planning, controlling, monitoring and administering the available

funds in business are called financial management. Joy Thomas , & Rabiyathulbasariya, (2017)

stated that financial management in any organization intended to achieve the reduction in finance

cost, sufficient funds availability to operate business, and efficient funds utilization and proper

procurement.

The main objective of financial management analysis and reporting is to provide useful financial

and non-financial information to existing and potential users about the financial health,

performance, continuous changing environment and performance of corporate firms to make

investing, financing and other economic decisions (Iatridis, 2010). To assess risk level against

expected returns analyzing financial statement and management process yields all valuable

information about the firm’s earning quality, co-relationships and trends, as well as the

weaknesses and strength in financial position as well as operational process to interest parties

(Peterson Drake, and Fabozzi, 2012). Management hierarchy of corporate firms are highly

concern about documentation, preparation and presentation of financial statements, relevant

notes and disclosers in reliable and understanding manner to information users such as investors,

creditors, legal authorities, government and corporate media. Also, Iatridis, (2010) demonstrated

that fulfilling the requirement of financial management and corporate reporting, business firms

fulfill the target of utilization of economic and other resources, satisfactory fulfillment of

regulations and laws, updating the cash flow and financial position, exploring future business

opportunities and most importantly satisfy user’s information needs.

Going to present in this paper, through extensive and deeper calculation and analysis of financial

and non-financial information of Starbucks Coffee Company the business strategy and policy

making, operational efficiency and performance growth or changes over couple of years.

Starbuck Coffee is a publically listed coffee shop in coffee industry, serving all over the world

with products in the category of coffee, smoothies, tea, backed products, beverages and

sandwiches and enjoy a major portion of quality minded coffee drinker’s expenditure in its own

Page 3 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pocket. The firm is following IFRS and IAS to measure, prepare and present its financial

statements and reports to interested information seekers.

Company background of Starbuck Coffee

Financial management analysis reflects information and disclosures about how Starbuck Coffee

is utilizing financial and non-financial resources to increase profitability and enhance firm value

in long-run.

Starbuck is an America based china coffee house founded in 1971, at Seattle, Washington DC.

Starbuck coffee is called the representative of second wave coffee and after 2000s it targeted the

quality seeking coffee drinker with artisanal coffee especially with dark roasted coffee. As

Starbuck is a public company, it’s traded at New York stock exchange and spreading business all

over the world with around 29,500 outlets or franchisee locations and creating employment

opportunities for 295,000 employees (Starbucks.com. 2019).

Away from home and work place, Starbuck coffee successfully positioned itself as a third place,

with long-term focus extending business in emerging economic countries. Interestingly, the

revenue portion of Starbuck is increased from 7% to 12% in 2018 from Asian market segment

and opened 2839 stores more in the last two years (Starbucks.com. 2019). Starbuck is upgrading

with innovative technology not only in business communication, easy ordering and payment

system but also updates its production and procedures for safety and efficiency reasons such as

automated espresso coffee making machines. Myron. E. Ullman is currently serving as the

chairman and it attained in 2018 $24.71 billion as total revenue, from which $4.15 billion was

net profit (Starbucks.com. 2019). Starbuck has other subsidiaries such as ethos water, Hear

Music, Evolution Fresh, Torrefazione Italia and others.

Financial performance and ratio analysis

Ratio analysis means to reckon or calculate, the term had come from Latin word (Joy Thomas, &

Rabiyathulbasariya, 2017). So, financial performance and ratio analysis is significantly

advantageous as it generates useful information on historical performance of the specific firm

about liquidity, solvency, market performance, capitalization and efficiency on operations

through identification, measuring, analyzing and evaluating prepared financial statements of the

company (Green, 2013).

Page 4 of 21

statements and reports to interested information seekers.

Company background of Starbuck Coffee

Financial management analysis reflects information and disclosures about how Starbuck Coffee

is utilizing financial and non-financial resources to increase profitability and enhance firm value

in long-run.

Starbuck is an America based china coffee house founded in 1971, at Seattle, Washington DC.

Starbuck coffee is called the representative of second wave coffee and after 2000s it targeted the

quality seeking coffee drinker with artisanal coffee especially with dark roasted coffee. As

Starbuck is a public company, it’s traded at New York stock exchange and spreading business all

over the world with around 29,500 outlets or franchisee locations and creating employment

opportunities for 295,000 employees (Starbucks.com. 2019).

Away from home and work place, Starbuck coffee successfully positioned itself as a third place,

with long-term focus extending business in emerging economic countries. Interestingly, the

revenue portion of Starbuck is increased from 7% to 12% in 2018 from Asian market segment

and opened 2839 stores more in the last two years (Starbucks.com. 2019). Starbuck is upgrading

with innovative technology not only in business communication, easy ordering and payment

system but also updates its production and procedures for safety and efficiency reasons such as

automated espresso coffee making machines. Myron. E. Ullman is currently serving as the

chairman and it attained in 2018 $24.71 billion as total revenue, from which $4.15 billion was

net profit (Starbucks.com. 2019). Starbuck has other subsidiaries such as ethos water, Hear

Music, Evolution Fresh, Torrefazione Italia and others.

Financial performance and ratio analysis

Ratio analysis means to reckon or calculate, the term had come from Latin word (Joy Thomas, &

Rabiyathulbasariya, 2017). So, financial performance and ratio analysis is significantly

advantageous as it generates useful information on historical performance of the specific firm

about liquidity, solvency, market performance, capitalization and efficiency on operations

through identification, measuring, analyzing and evaluating prepared financial statements of the

company (Green, 2013).

Page 4 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 Analysis of Liquidity Ratio.

Liquidity ratio analysis reflects the company’s financial ability to pay off long-term debts and

current debts from the balance of current assets in a specific financial time period (Peterson

Drake, and Fabozzi, 2012). These ratios are highly dependent on firm’s performance to generate

cash or cash equivalent items in the cash emergency or crisis time not bother about cash balance

on that time period.

2.1 Current ratio

Current ratio is called the efficiency ratio as it measures the company’s ability to pay its short-

term liabilities off with the balance of current assets (MANISHA B, 2012). It’s important to

measure as short-term liabilities are due in the running accounting year.

Current assets such as cash, cash equivalents, market securities are easy to convert into cash in

short time and pay off all current liabilities as they become due and without selling off revenue

generating long term assets (Needles, and Powers, 2010). So, current ratio helps creditors and

inventors of Starbucks to understand the liquidity position and efficient of paying current

liabilities. The formula to calculate current ratio is as follows:

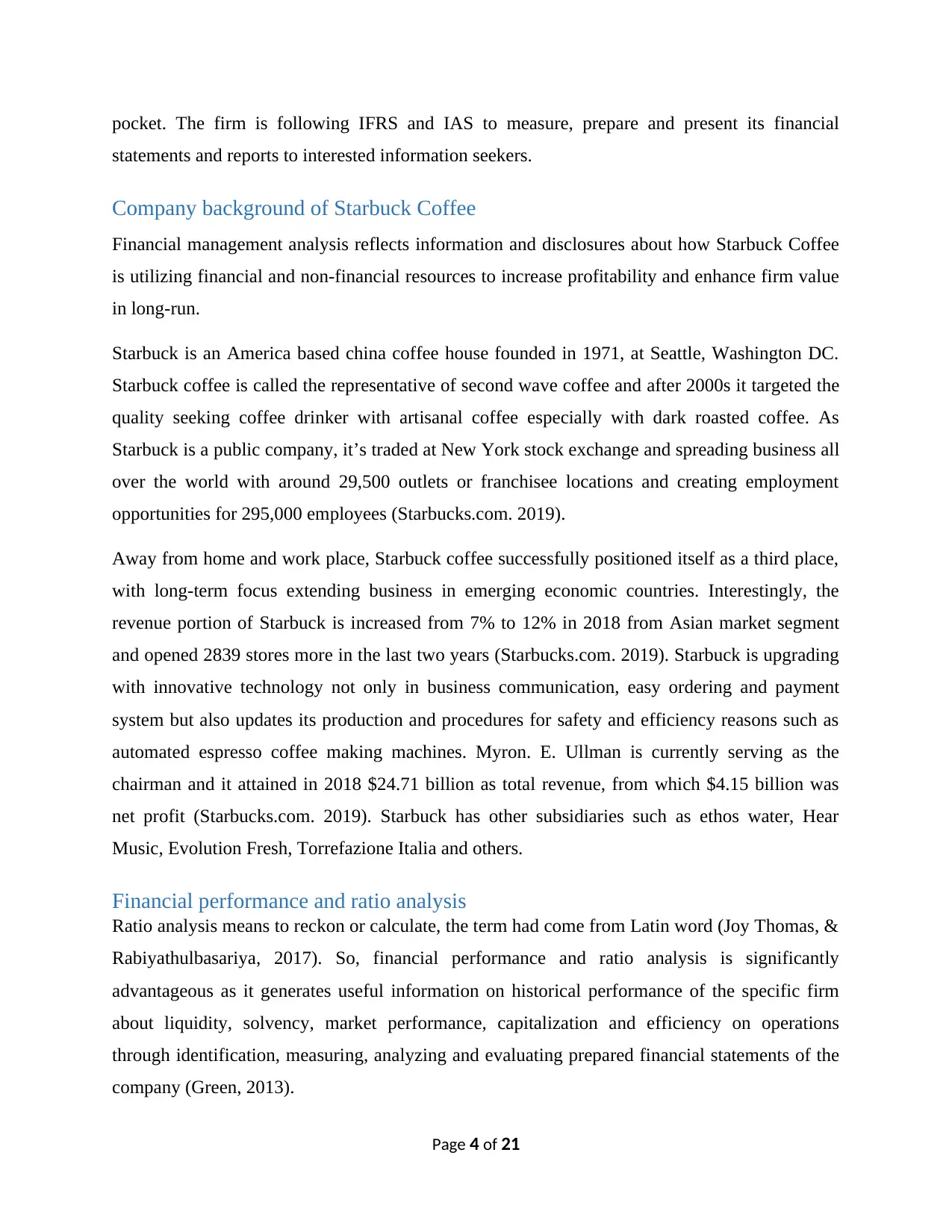

So, analyzing the current ratio for Starbucks Coffee Company limited as follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Total current

assets

4168700000 3971000000 4757900000 5283400000 12494200000

Total current

liabilities

3038700000 3648100000 4546800000 4220700000 5684200000

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Current Ratio 1.372 1.089 1.046 1.252 2.198

Page 5 of 21

Liquidity ratio analysis reflects the company’s financial ability to pay off long-term debts and

current debts from the balance of current assets in a specific financial time period (Peterson

Drake, and Fabozzi, 2012). These ratios are highly dependent on firm’s performance to generate

cash or cash equivalent items in the cash emergency or crisis time not bother about cash balance

on that time period.

2.1 Current ratio

Current ratio is called the efficiency ratio as it measures the company’s ability to pay its short-

term liabilities off with the balance of current assets (MANISHA B, 2012). It’s important to

measure as short-term liabilities are due in the running accounting year.

Current assets such as cash, cash equivalents, market securities are easy to convert into cash in

short time and pay off all current liabilities as they become due and without selling off revenue

generating long term assets (Needles, and Powers, 2010). So, current ratio helps creditors and

inventors of Starbucks to understand the liquidity position and efficient of paying current

liabilities. The formula to calculate current ratio is as follows:

So, analyzing the current ratio for Starbucks Coffee Company limited as follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Total current

assets

4168700000 3971000000 4757900000 5283400000 12494200000

Total current

liabilities

3038700000 3648100000 4546800000 4220700000 5684200000

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Current Ratio 1.372 1.089 1.046 1.252 2.198

Page 5 of 21

Table – 01 current ratio analysis of Starbucks Coffee Limited

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

1.372

1.089 1.046

1.252

2.198

Current Ratio

Current Ratio

The graph will make investors easy understanding of the current ratio and financial position of

Starbucks Coffee.

Here, a higher ratio is favorable over a lower ratio as it shows the ability and efficiency to make

payment to current liabilities too fast. A current ratio of less than 1.0 reflects that business isn’t

placed debts successfully and need to raise more finance to pay off creditors. While a ratio

between 1.0-3.0 is enough encouraging and suggested that enough cash and other current assets

to pay its all current debts (Needles, and Powers, 2010). So, the increasing current ratio of

Starbucks reflects its healthy financial position and ability to pay off current liabilities within the

running financial year.

The possible ways to improve the current ratio of Starbucks coffee more can be such as selling

off the unproductive assets, fasting the receivables and cash conversion cycle and sweeping the

bank accounts properly.

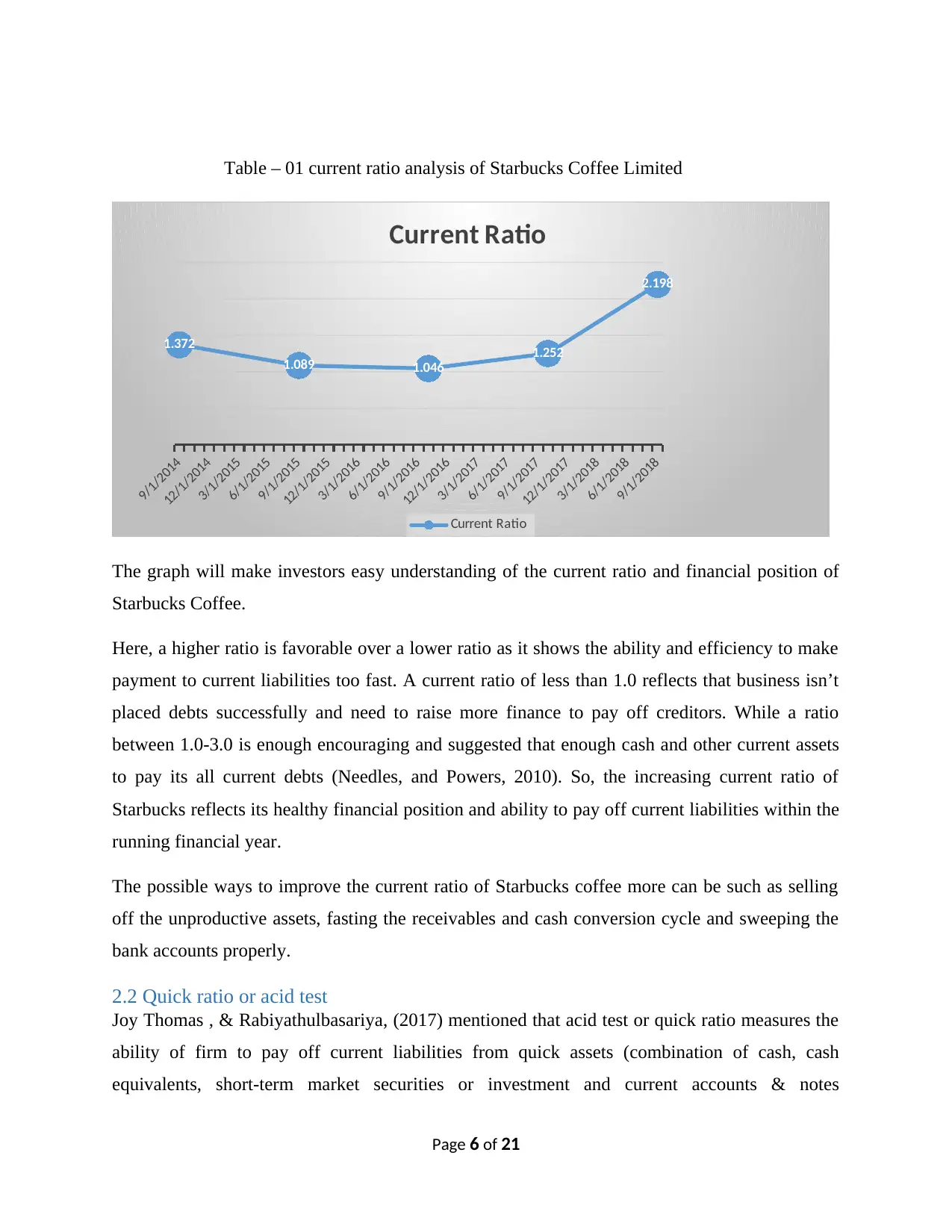

2.2 Quick ratio or acid test

Joy Thomas , & Rabiyathulbasariya, (2017) mentioned that acid test or quick ratio measures the

ability of firm to pay off current liabilities from quick assets (combination of cash, cash

equivalents, short-term market securities or investment and current accounts & notes

Page 6 of 21

9/1/2014

12/1/2014

3/1/2015

6/1/2015

9/1/2015

12/1/2015

3/1/2016

6/1/2016

9/1/2016

12/1/2016

3/1/2017

6/1/2017

9/1/2017

12/1/2017

3/1/2018

6/1/2018

9/1/2018

1.372

1.089 1.046

1.252

2.198

Current Ratio

Current Ratio

The graph will make investors easy understanding of the current ratio and financial position of

Starbucks Coffee.

Here, a higher ratio is favorable over a lower ratio as it shows the ability and efficiency to make

payment to current liabilities too fast. A current ratio of less than 1.0 reflects that business isn’t

placed debts successfully and need to raise more finance to pay off creditors. While a ratio

between 1.0-3.0 is enough encouraging and suggested that enough cash and other current assets

to pay its all current debts (Needles, and Powers, 2010). So, the increasing current ratio of

Starbucks reflects its healthy financial position and ability to pay off current liabilities within the

running financial year.

The possible ways to improve the current ratio of Starbucks coffee more can be such as selling

off the unproductive assets, fasting the receivables and cash conversion cycle and sweeping the

bank accounts properly.

2.2 Quick ratio or acid test

Joy Thomas , & Rabiyathulbasariya, (2017) mentioned that acid test or quick ratio measures the

ability of firm to pay off current liabilities from quick assets (combination of cash, cash

equivalents, short-term market securities or investment and current accounts & notes

Page 6 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

receivables). The analysis is called quick ratio as the assets can be converted into cash so faster.

At the time of calculating quick ratio or acid test it’s necessary to make comparison with

competitors and measure average industry performance for building strengths and overcoming

the weaknesses with better future perspective in coffee industry (Darmawan, 2017).

The formula to calculate quick ratio or acid test is as follows:

Quick ratio = (Cash+ Cash Equivalent + Short-term marketable securities or investment +

Current Receivables) ÷ Current liabilities

Here, analyzing the quick ratio or acid test for Starbucks Coffee Company limited as follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Total current

assets

4168700000 3971000000 4757900000 5283400000 12494200000

Total current

liabilities

3038700000 3648100000 4546800000 4220700000 5684200000

Inventories 1090900000 1306400000 1378500000 1364000000 1400500000

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Quick Ratios 1.013 0.730 0.743 0.929 1.952

Table – 02 Quick ratio analysis of Starbucks Coffee Limited

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

1/1/2017

3/1/2017

5/1/2017

7/1/2017

9/1/2017

11/1/2017

1/1/2018

3/1/2018

5/1/2018

7/1/2018

9/1/2018

1.013

0.730 0.743 0.929

1.952

Quick Ratio

Quick Ratios

Page 7 of 21

At the time of calculating quick ratio or acid test it’s necessary to make comparison with

competitors and measure average industry performance for building strengths and overcoming

the weaknesses with better future perspective in coffee industry (Darmawan, 2017).

The formula to calculate quick ratio or acid test is as follows:

Quick ratio = (Cash+ Cash Equivalent + Short-term marketable securities or investment +

Current Receivables) ÷ Current liabilities

Here, analyzing the quick ratio or acid test for Starbucks Coffee Company limited as follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Total current

assets

4168700000 3971000000 4757900000 5283400000 12494200000

Total current

liabilities

3038700000 3648100000 4546800000 4220700000 5684200000

Inventories 1090900000 1306400000 1378500000 1364000000 1400500000

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Quick Ratios 1.013 0.730 0.743 0.929 1.952

Table – 02 Quick ratio analysis of Starbucks Coffee Limited

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

1/1/2017

3/1/2017

5/1/2017

7/1/2017

9/1/2017

11/1/2017

1/1/2018

3/1/2018

5/1/2018

7/1/2018

9/1/2018

1.013

0.730 0.743 0.929

1.952

Quick Ratio

Quick Ratios

Page 7 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The graph will help investors to understand the financial condition of Starbuck Coffee easily

with reasonable explanation.

Here, Starbuck Coffee is enjoying increasing quick ratio over the since 2014 to 2018. Higher

ratios are favorable to businesses as it reflects that more quick assets are available than current

liabilities (Jonny, 2016). With a ratio of 1 indicates that firm has quick assets equivalent to

current assets. So, without selling long-term current assets Starbucks can pay off its current

liabilities with quick assets. And the ratio around 2 reflects that Starbucks has twice quick assets

than current liabilities.

The possible ways to Starbucks Coffee to improve quick ratio in an increasing ways can be such

as improving inventory turnover ratio with reduction of cash or receivables collection period.

3. Analysis of long term solvency ratio

The capital structure, long term and short-term solvency can be measured through long-term

solvency ratio. These ratios shows debt-equity mix, assists to evaluate interest payment to total

debt holders and return to equity holders at maturity date (Jonny, 2016). Here, going to present

debt to equity ratio, and times of interest earned are as follows:

3.1 debt to equity ratio

Debt to equity ratio is the result of dividing total debt by total equity to determine the financial

leverage of Starbucks. It measures the level at which a firm can financing its operational

activities through debt as well as shareholder-owned funds (Darmawan, 2017). Also shows the

ability of equity holders to cover outstanding debts in any event of sudden business shutdown.

The formula to calculate debt to equity ratio is presenting as follows:

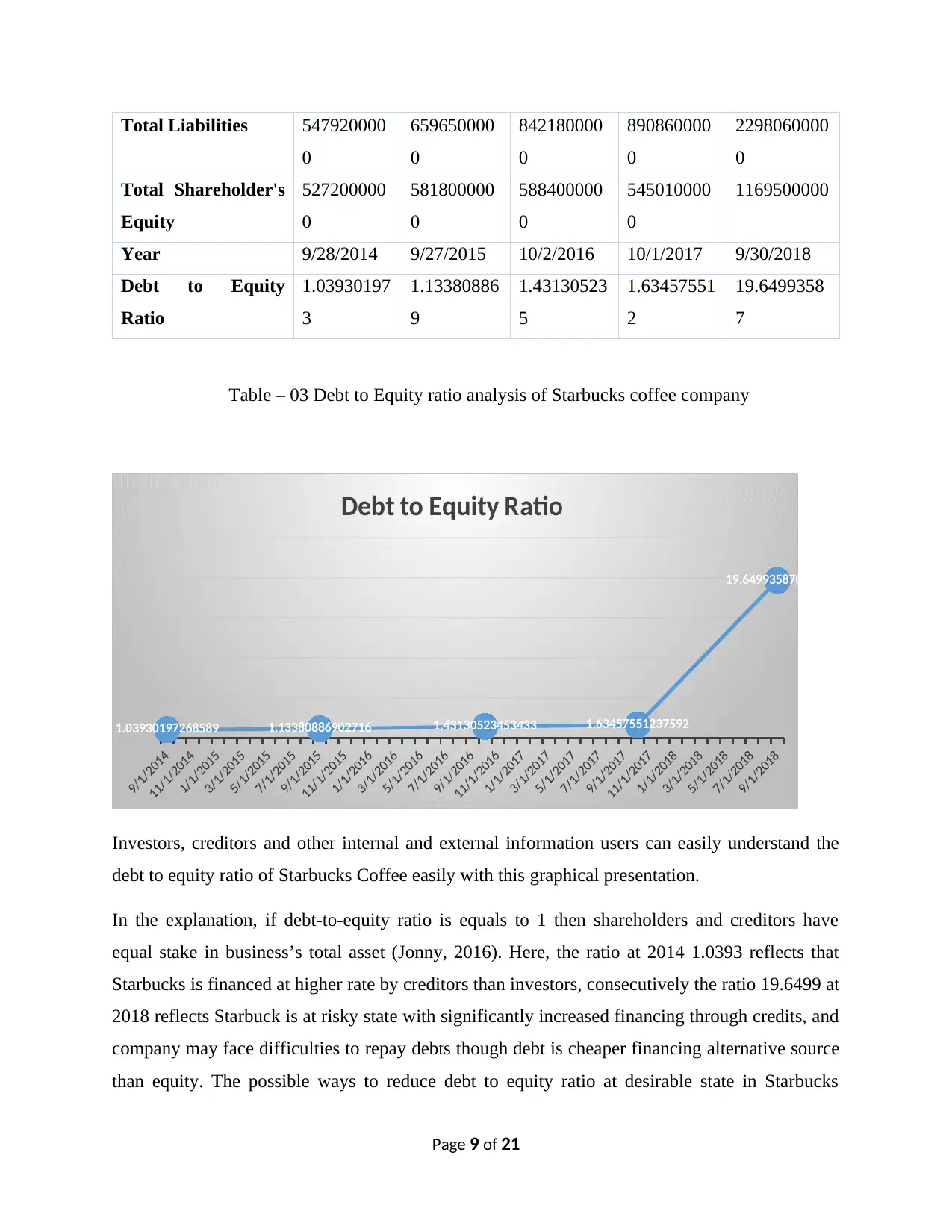

Here, presenting the debt to equity ratio of Starbucks coffee company as follows:

Particulars 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Page 8 of 21

with reasonable explanation.

Here, Starbuck Coffee is enjoying increasing quick ratio over the since 2014 to 2018. Higher

ratios are favorable to businesses as it reflects that more quick assets are available than current

liabilities (Jonny, 2016). With a ratio of 1 indicates that firm has quick assets equivalent to

current assets. So, without selling long-term current assets Starbucks can pay off its current

liabilities with quick assets. And the ratio around 2 reflects that Starbucks has twice quick assets

than current liabilities.

The possible ways to Starbucks Coffee to improve quick ratio in an increasing ways can be such

as improving inventory turnover ratio with reduction of cash or receivables collection period.

3. Analysis of long term solvency ratio

The capital structure, long term and short-term solvency can be measured through long-term

solvency ratio. These ratios shows debt-equity mix, assists to evaluate interest payment to total

debt holders and return to equity holders at maturity date (Jonny, 2016). Here, going to present

debt to equity ratio, and times of interest earned are as follows:

3.1 debt to equity ratio

Debt to equity ratio is the result of dividing total debt by total equity to determine the financial

leverage of Starbucks. It measures the level at which a firm can financing its operational

activities through debt as well as shareholder-owned funds (Darmawan, 2017). Also shows the

ability of equity holders to cover outstanding debts in any event of sudden business shutdown.

The formula to calculate debt to equity ratio is presenting as follows:

Here, presenting the debt to equity ratio of Starbucks coffee company as follows:

Particulars 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Page 8 of 21

Total Liabilities 547920000

0

659650000

0

842180000

0

890860000

0

2298060000

0

Total Shareholder's

Equity

527200000

0

581800000

0

588400000

0

545010000

0

1169500000

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Debt to Equity

Ratio

1.03930197

3

1.13380886

9

1.43130523

5

1.63457551

2

19.6499358

7

Table – 03 Debt to Equity ratio analysis of Starbucks coffee company

1.03930197268589 1.13380886902716 1.43130523453433 1.63457551237592

19.6499358700299

Debt to Equity Ratio

Investors, creditors and other internal and external information users can easily understand the

debt to equity ratio of Starbucks Coffee easily with this graphical presentation.

In the explanation, if debt-to-equity ratio is equals to 1 then shareholders and creditors have

equal stake in business’s total asset (Jonny, 2016). Here, the ratio at 2014 1.0393 reflects that

Starbucks is financed at higher rate by creditors than investors, consecutively the ratio 19.6499 at

2018 reflects Starbuck is at risky state with significantly increased financing through credits, and

company may face difficulties to repay debts though debt is cheaper financing alternative source

than equity. The possible ways to reduce debt to equity ratio at desirable state in Starbucks

Page 9 of 21

0

659650000

0

842180000

0

890860000

0

2298060000

0

Total Shareholder's

Equity

527200000

0

581800000

0

588400000

0

545010000

0

1169500000

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Debt to Equity

Ratio

1.03930197

3

1.13380886

9

1.43130523

5

1.63457551

2

19.6499358

7

Table – 03 Debt to Equity ratio analysis of Starbucks coffee company

1.03930197268589 1.13380886902716 1.43130523453433 1.63457551237592

19.6499358700299

Debt to Equity Ratio

Investors, creditors and other internal and external information users can easily understand the

debt to equity ratio of Starbucks Coffee easily with this graphical presentation.

In the explanation, if debt-to-equity ratio is equals to 1 then shareholders and creditors have

equal stake in business’s total asset (Jonny, 2016). Here, the ratio at 2014 1.0393 reflects that

Starbucks is financed at higher rate by creditors than investors, consecutively the ratio 19.6499 at

2018 reflects Starbuck is at risky state with significantly increased financing through credits, and

company may face difficulties to repay debts though debt is cheaper financing alternative source

than equity. The possible ways to reduce debt to equity ratio at desirable state in Starbucks

Page 9 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Coffee are increasing profit margin, pay off more risky debts with equity and retained earnings

furthermore after 2018 in Starbucks Coffee.

4. Analysis of profitability ratio

Profitability ratio analysis reflects the generated profit from comprehensive income statements

and evaluate the capacity of firm to earn more profit from business and enhance values of sales

volume, assets value and equity (Omar, and et al 2014). Now, going to analysis net profit margin

and return on equity for Starbucks Coffee Company are as follows:

4.1 Gross profit ratio

The ratios measures the net income earned with each dollar of sales through comparison of net

income and net sales of the firm. So, the profit ratio reflects the left over amount of sales after

paying off all the expenses. The ratio provides information to creditors and investors about

operational efficiency to pay back loans and distributable amount to investors as dividend (Omar,

and et al 2014).

Clemons, (2010) discussed about that though lower ratio indicates firm has higher expenditures

and significantly management requires to cut extra expenses and budgeting the incomes and

expenditures. So, internal management can use the ratio to set performance targets.

To calculate gross profit margin ratio, the formula is as follows:

Here, conducting the analysis of net profit margin ratio of Starbucks Coffee Company is as

follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Net Income 2068100000 2757400000 2817700000 2884700000 4518300000

Page 10 of 21

furthermore after 2018 in Starbucks Coffee.

4. Analysis of profitability ratio

Profitability ratio analysis reflects the generated profit from comprehensive income statements

and evaluate the capacity of firm to earn more profit from business and enhance values of sales

volume, assets value and equity (Omar, and et al 2014). Now, going to analysis net profit margin

and return on equity for Starbucks Coffee Company are as follows:

4.1 Gross profit ratio

The ratios measures the net income earned with each dollar of sales through comparison of net

income and net sales of the firm. So, the profit ratio reflects the left over amount of sales after

paying off all the expenses. The ratio provides information to creditors and investors about

operational efficiency to pay back loans and distributable amount to investors as dividend (Omar,

and et al 2014).

Clemons, (2010) discussed about that though lower ratio indicates firm has higher expenditures

and significantly management requires to cut extra expenses and budgeting the incomes and

expenditures. So, internal management can use the ratio to set performance targets.

To calculate gross profit margin ratio, the formula is as follows:

Here, conducting the analysis of net profit margin ratio of Starbucks Coffee Company is as

follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Net Income 2068100000 2757400000 2817700000 2884700000 4518300000

Page 10 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

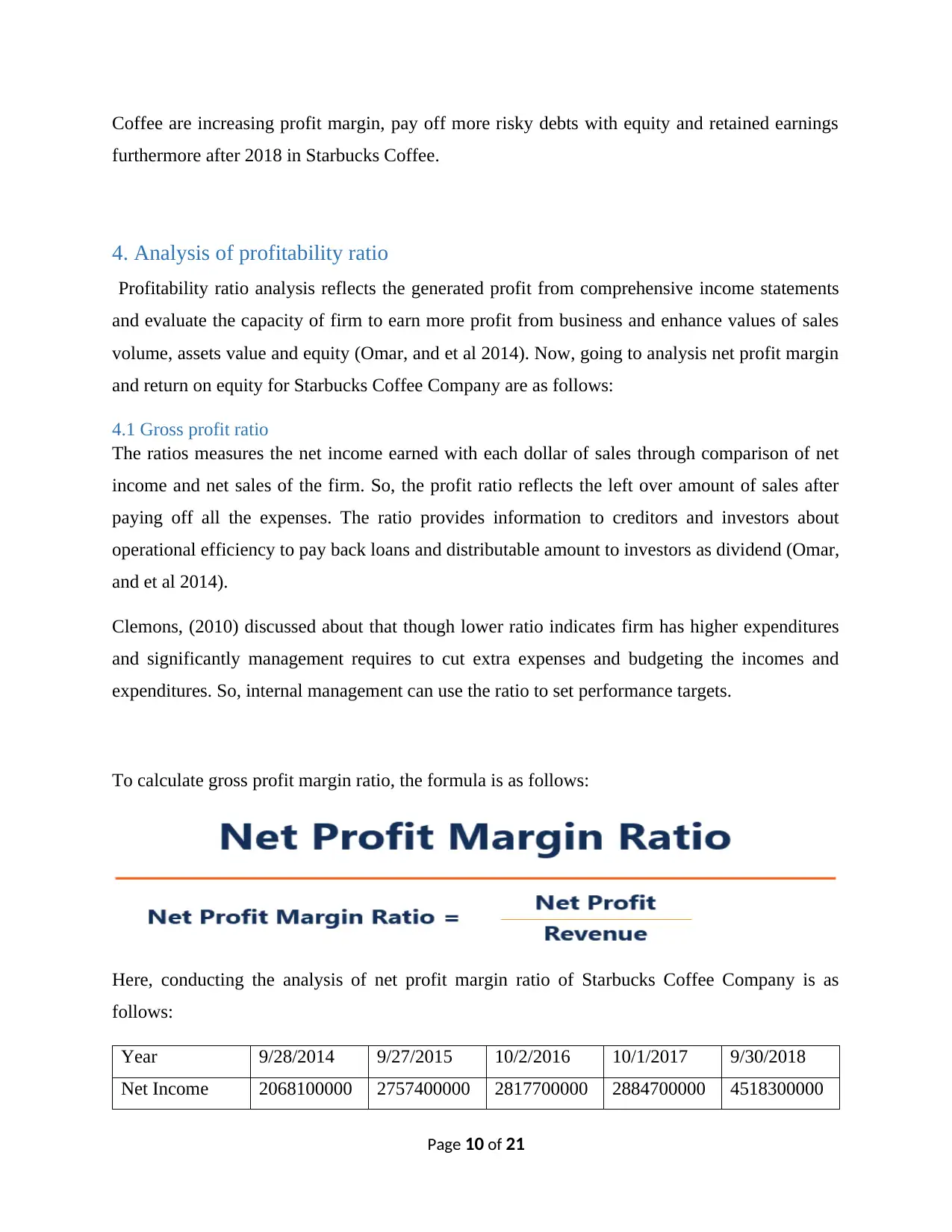

Revenue 1644780000

0

1916270000

0

2131590000

0

2238680000

0

2471950000

0

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Profit Margin 0.126 0.144 0.132 0.129 0.183

Table – 04 Gross profit ratio analysis of Starbucks Coffee Company

Also, making graphical presentation of gross profit ratio for information users’ betterments.

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

1/1/2017

3/1/2017

5/1/2017

7/1/2017

9/1/2017

11/1/2017

1/1/2018

3/1/2018

5/1/2018

7/1/2018

9/1/2018

0.126

0.144 0.132 0.129

0.183

Profit Margin

Profit Margin

So, the increasing profit margin of Starbuck Coffee from 2014 to 2018 shows that Starbuck can

effectively control its operational costs and price of products & services higher than cost. So,

Starbucks ad strong pricing strategies and efficient management team to operate. Also, the ratio

further can be increased with increasing sales proceeds, reducing utilities expenses, mitigating

labor costs and insurance premiums successfully (Omar, and et al 2014).

4.2 Return on Equity (ROE) ratio

ROE is a profitability ratio determines the firm’s ability to utilize shareholder’s equity, ability to

generate profit and grow the firm performance (Darmawan, 2017). ROE is measured through net

income divided by shareholder’s equity. So, investors calculate ROE at the beginning and ending

of financial year to trace Starbucks progress and ability to maintain increasing performance trend

(Clemons, 2010). The formula to calculate return on shareholder’s equity is as follows:

Page 11 of 21

0

1916270000

0

2131590000

0

2238680000

0

2471950000

0

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Profit Margin 0.126 0.144 0.132 0.129 0.183

Table – 04 Gross profit ratio analysis of Starbucks Coffee Company

Also, making graphical presentation of gross profit ratio for information users’ betterments.

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

1/1/2017

3/1/2017

5/1/2017

7/1/2017

9/1/2017

11/1/2017

1/1/2018

3/1/2018

5/1/2018

7/1/2018

9/1/2018

0.126

0.144 0.132 0.129

0.183

Profit Margin

Profit Margin

So, the increasing profit margin of Starbuck Coffee from 2014 to 2018 shows that Starbuck can

effectively control its operational costs and price of products & services higher than cost. So,

Starbucks ad strong pricing strategies and efficient management team to operate. Also, the ratio

further can be increased with increasing sales proceeds, reducing utilities expenses, mitigating

labor costs and insurance premiums successfully (Omar, and et al 2014).

4.2 Return on Equity (ROE) ratio

ROE is a profitability ratio determines the firm’s ability to utilize shareholder’s equity, ability to

generate profit and grow the firm performance (Darmawan, 2017). ROE is measured through net

income divided by shareholder’s equity. So, investors calculate ROE at the beginning and ending

of financial year to trace Starbucks progress and ability to maintain increasing performance trend

(Clemons, 2010). The formula to calculate return on shareholder’s equity is as follows:

Page 11 of 21

Here, performing the return on equity of Starbucks Coffee Company is as follows:

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Net Income 2,068,100,00

0

2,757,400,00

0

2,817,700,00

0

2,884,700,00

0

4,518,300,00

0

Total

shareholders’

equity

5,272,000,00

0

5,818,000,00

0

5,884,000,00

0

5,450,100,00

0

1,169,500,00

0

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Return On

Equity

0.39227997 0.473942936 0.478874915 0.52929304 3.863445917

Table – 05 Return on Equity of Starbucks Coffee Company

Also, the graphical presentation of ROE ratio is presenting:

0.392279969650

986

0.473942935716

741

0.478874915023

793

0.529293040494

67

3.863445917058

57

Return On Equity

Return On Equity

Page 12 of 21

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Net Income 2,068,100,00

0

2,757,400,00

0

2,817,700,00

0

2,884,700,00

0

4,518,300,00

0

Total

shareholders’

equity

5,272,000,00

0

5,818,000,00

0

5,884,000,00

0

5,450,100,00

0

1,169,500,00

0

Year 9/28/2014 9/27/2015 10/2/2016 10/1/2017 9/30/2018

Return On

Equity

0.39227997 0.473942936 0.478874915 0.52929304 3.863445917

Table – 05 Return on Equity of Starbucks Coffee Company

Also, the graphical presentation of ROE ratio is presenting:

0.392279969650

986

0.473942935716

741

0.478874915023

793

0.529293040494

67

3.863445917058

57

Return On Equity

Return On Equity

Page 12 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.