Financial and Management Accounting Report: Stell Co. Ltd Review

VerifiedAdded on 2023/06/11

|11

|2541

|70

Report

AI Summary

This financial and management accounting report analyzes the performance of Stell Co. Ltd, comparing financial data from 2020 and 2021. It calculates gross profit and net profit ratios, identifies reasons for declining profits and increasing cash flow problems, and recommends strategies to improve the company's financial position. The report also includes a break-even analysis for DK Machines, discussing its utilization for setting profitability targets and the adaptation of activity-based costing. Furthermore, it computes variances for Concorde Construction, explores potential causes and consequences, and suggests corrective strategies, along with a comparison of incremental-based budgeting and zero-based budgeting. Desklib is a platform where you can find this and many other solved assignments.

FINANCIAL and

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1 ..................................................................................................................................3

1. Calculation of Gross Profit and Net Profit...............................................................................3

2. Calculation of Gross Profit and Net profit ratio ......................................................................4

3. Reasons for declining profits and increasing cash flow problems...........................................4

4. Three strategies for recommendations to improve financial position and increasing profit....5

QUESTION 2 ..................................................................................................................................6

1. Calculation of Break-even point..............................................................................................6

2. Utilization of break-even analysis for setting profitability targets..........................................6

3. Adaptation of activity based costing and more accurate management accounting information

......................................................................................................................................................7

QUESTION 3 ..................................................................................................................................7

1. Computation of variances........................................................................................................7

2. Possible causes of variances identified....................................................................................8

3. Projection of likely consequences of variances.......................................................................8

4. Strategies for correcting variances...........................................................................................9

5. Presenting advantages disadvantages of switching from Incremental Based Budgeting to

Zero Based Budgeting................................................................................................................10

REFERENCES..............................................................................................................................11

QUESTION 1 ..................................................................................................................................3

1. Calculation of Gross Profit and Net Profit...............................................................................3

2. Calculation of Gross Profit and Net profit ratio ......................................................................4

3. Reasons for declining profits and increasing cash flow problems...........................................4

4. Three strategies for recommendations to improve financial position and increasing profit....5

QUESTION 2 ..................................................................................................................................6

1. Calculation of Break-even point..............................................................................................6

2. Utilization of break-even analysis for setting profitability targets..........................................6

3. Adaptation of activity based costing and more accurate management accounting information

......................................................................................................................................................7

QUESTION 3 ..................................................................................................................................7

1. Computation of variances........................................................................................................7

2. Possible causes of variances identified....................................................................................8

3. Projection of likely consequences of variances.......................................................................8

4. Strategies for correcting variances...........................................................................................9

5. Presenting advantages disadvantages of switching from Incremental Based Budgeting to

Zero Based Budgeting................................................................................................................10

REFERENCES..............................................................................................................................11

QUESTION 1

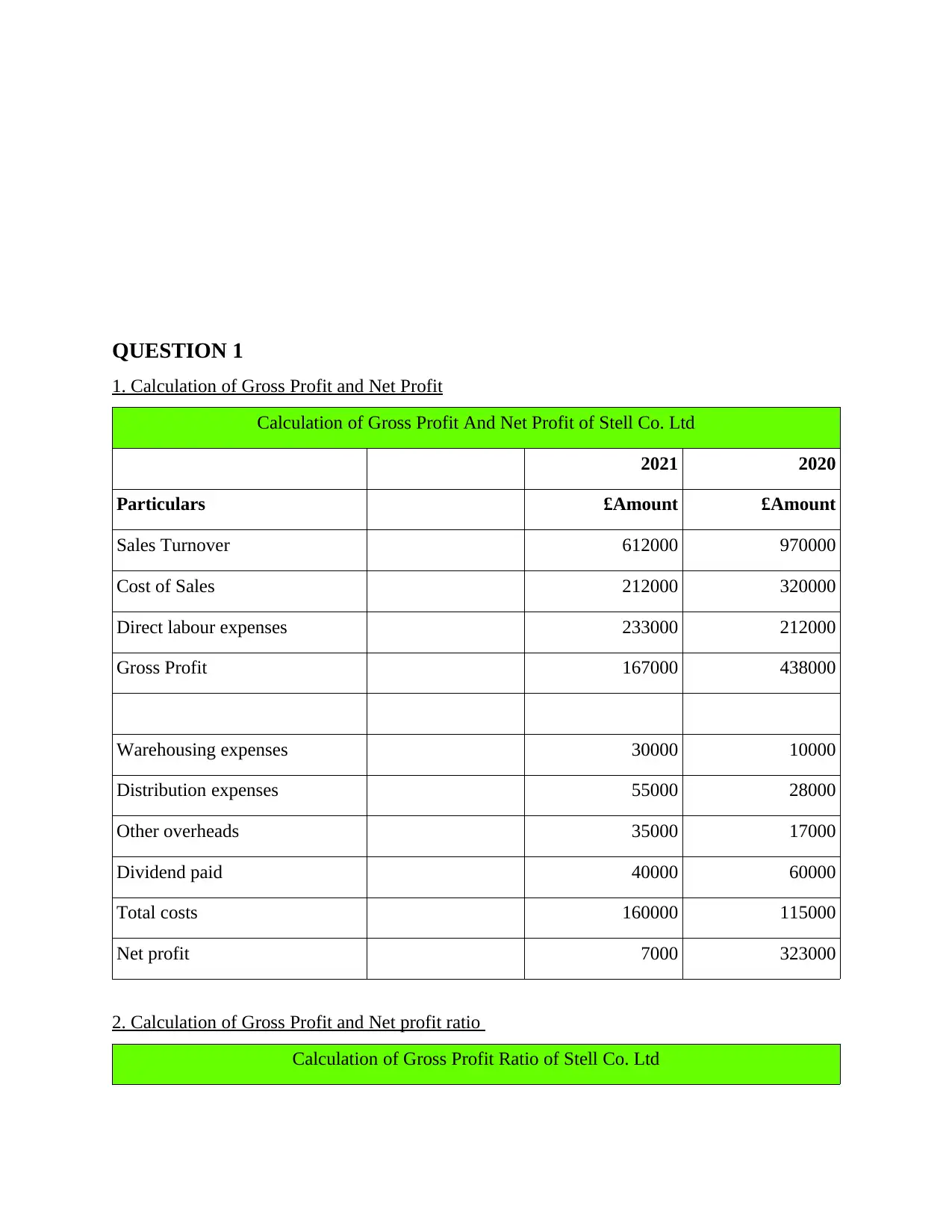

1. Calculation of Gross Profit and Net Profit

Calculation of Gross Profit And Net Profit of Stell Co. Ltd

2021 2020

Particulars £Amount £Amount

Sales Turnover 612000 970000

Cost of Sales 212000 320000

Direct labour expenses 233000 212000

Gross Profit 167000 438000

Warehousing expenses 30000 10000

Distribution expenses 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total costs 160000 115000

Net profit 7000 323000

2. Calculation of Gross Profit and Net profit ratio

Calculation of Gross Profit Ratio of Stell Co. Ltd

1. Calculation of Gross Profit and Net Profit

Calculation of Gross Profit And Net Profit of Stell Co. Ltd

2021 2020

Particulars £Amount £Amount

Sales Turnover 612000 970000

Cost of Sales 212000 320000

Direct labour expenses 233000 212000

Gross Profit 167000 438000

Warehousing expenses 30000 10000

Distribution expenses 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total costs 160000 115000

Net profit 7000 323000

2. Calculation of Gross Profit and Net profit ratio

Calculation of Gross Profit Ratio of Stell Co. Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

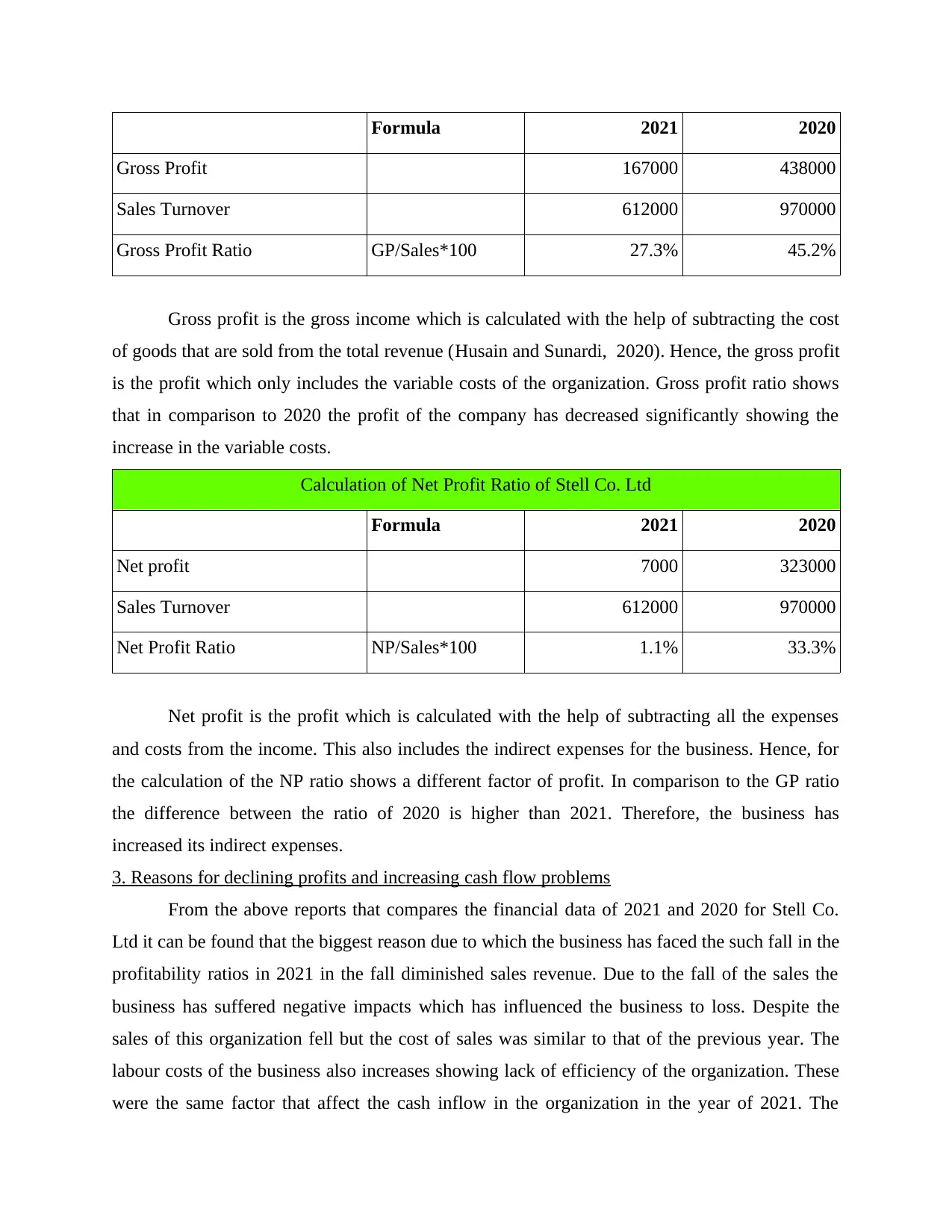

Formula 2021 2020

Gross Profit 167000 438000

Sales Turnover 612000 970000

Gross Profit Ratio GP/Sales*100 27.3% 45.2%

Gross profit is the gross income which is calculated with the help of subtracting the cost

of goods that are sold from the total revenue (Husain and Sunardi, 2020). Hence, the gross profit

is the profit which only includes the variable costs of the organization. Gross profit ratio shows

that in comparison to 2020 the profit of the company has decreased significantly showing the

increase in the variable costs.

Calculation of Net Profit Ratio of Stell Co. Ltd

Formula 2021 2020

Net profit 7000 323000

Sales Turnover 612000 970000

Net Profit Ratio NP/Sales*100 1.1% 33.3%

Net profit is the profit which is calculated with the help of subtracting all the expenses

and costs from the income. This also includes the indirect expenses for the business. Hence, for

the calculation of the NP ratio shows a different factor of profit. In comparison to the GP ratio

the difference between the ratio of 2020 is higher than 2021. Therefore, the business has

increased its indirect expenses.

3. Reasons for declining profits and increasing cash flow problems

From the above reports that compares the financial data of 2021 and 2020 for Stell Co.

Ltd it can be found that the biggest reason due to which the business has faced the such fall in the

profitability ratios in 2021 in the fall diminished sales revenue. Due to the fall of the sales the

business has suffered negative impacts which has influenced the business to loss. Despite the

sales of this organization fell but the cost of sales was similar to that of the previous year. The

labour costs of the business also increases showing lack of efficiency of the organization. These

were the same factor that affect the cash inflow in the organization in the year of 2021. The

Gross Profit 167000 438000

Sales Turnover 612000 970000

Gross Profit Ratio GP/Sales*100 27.3% 45.2%

Gross profit is the gross income which is calculated with the help of subtracting the cost

of goods that are sold from the total revenue (Husain and Sunardi, 2020). Hence, the gross profit

is the profit which only includes the variable costs of the organization. Gross profit ratio shows

that in comparison to 2020 the profit of the company has decreased significantly showing the

increase in the variable costs.

Calculation of Net Profit Ratio of Stell Co. Ltd

Formula 2021 2020

Net profit 7000 323000

Sales Turnover 612000 970000

Net Profit Ratio NP/Sales*100 1.1% 33.3%

Net profit is the profit which is calculated with the help of subtracting all the expenses

and costs from the income. This also includes the indirect expenses for the business. Hence, for

the calculation of the NP ratio shows a different factor of profit. In comparison to the GP ratio

the difference between the ratio of 2020 is higher than 2021. Therefore, the business has

increased its indirect expenses.

3. Reasons for declining profits and increasing cash flow problems

From the above reports that compares the financial data of 2021 and 2020 for Stell Co.

Ltd it can be found that the biggest reason due to which the business has faced the such fall in the

profitability ratios in 2021 in the fall diminished sales revenue. Due to the fall of the sales the

business has suffered negative impacts which has influenced the business to loss. Despite the

sales of this organization fell but the cost of sales was similar to that of the previous year. The

labour costs of the business also increases showing lack of efficiency of the organization. These

were the same factor that affect the cash inflow in the organization in the year of 2021. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business had to pay extra for all the expenses that had a negative impact on cash inflow of the

organization. This lead to the business facing cash out flow more than the cash inflow. Total

costs of the organization increased by 45000 and its sales decreased by 358000. This shows the

actual reason for the fall of profit and poor cash flow for Stell Co. Ltd.

4. Three strategies for recommendations to improve financial position and increasing profit

In order to increase the business operations Stell Co. Ltd needs to utilize the following

strategies that will lift up the financial positioning of the organization.

Lowering Expenses :

The business of this organization has been affected negatively due to the increased

expenses in 2021. Hence, the best practices for this organization would be the decrease the total

costs of the organization in order to improve the financial position. It is going to be very

important for the business to find cheap alternatives from the suppliers, equipments and services.

This is the factor that is helpful for the arranging the periodic deferred payments.

Selling unused or Unwanted Assets :

In general it has been seen that the business pay more and earn less when they have an

asset which underperforms. Hence, for the organization it will be very important to sell this asset

and buy new for achieving the operational efficiency.

Lowering prices :

This organization needs to increase its sales in order to improve the sales turnover this is

due to the customers tendency to buy more if the price of the product is less. Hence, it is going to

be very important for the organization to manage the prices and keep it lower and competitive.

For increasing the profit of the organization there are multiple ways for the business to

adapt such as,

Increasing the sales needs to be the biggest priority for this business.

Improving on the operational efficiency of the resources of this business. This would

allow the organization to be more cost-efficient.

Increasing the productivity of the employees can allow the business to develop new

strategies and influence the growth in the organization (Atoyebi, Bello and Owolarafe,

2022).

Utilization of methods like bench-marketing and KPI for monitoring the operations of the

resources will allow the business achieve the growth that is required.

organization. This lead to the business facing cash out flow more than the cash inflow. Total

costs of the organization increased by 45000 and its sales decreased by 358000. This shows the

actual reason for the fall of profit and poor cash flow for Stell Co. Ltd.

4. Three strategies for recommendations to improve financial position and increasing profit

In order to increase the business operations Stell Co. Ltd needs to utilize the following

strategies that will lift up the financial positioning of the organization.

Lowering Expenses :

The business of this organization has been affected negatively due to the increased

expenses in 2021. Hence, the best practices for this organization would be the decrease the total

costs of the organization in order to improve the financial position. It is going to be very

important for the business to find cheap alternatives from the suppliers, equipments and services.

This is the factor that is helpful for the arranging the periodic deferred payments.

Selling unused or Unwanted Assets :

In general it has been seen that the business pay more and earn less when they have an

asset which underperforms. Hence, for the organization it will be very important to sell this asset

and buy new for achieving the operational efficiency.

Lowering prices :

This organization needs to increase its sales in order to improve the sales turnover this is

due to the customers tendency to buy more if the price of the product is less. Hence, it is going to

be very important for the organization to manage the prices and keep it lower and competitive.

For increasing the profit of the organization there are multiple ways for the business to

adapt such as,

Increasing the sales needs to be the biggest priority for this business.

Improving on the operational efficiency of the resources of this business. This would

allow the organization to be more cost-efficient.

Increasing the productivity of the employees can allow the business to develop new

strategies and influence the growth in the organization (Atoyebi, Bello and Owolarafe,

2022).

Utilization of methods like bench-marketing and KPI for monitoring the operations of the

resources will allow the business achieve the growth that is required.

QUESTION 2

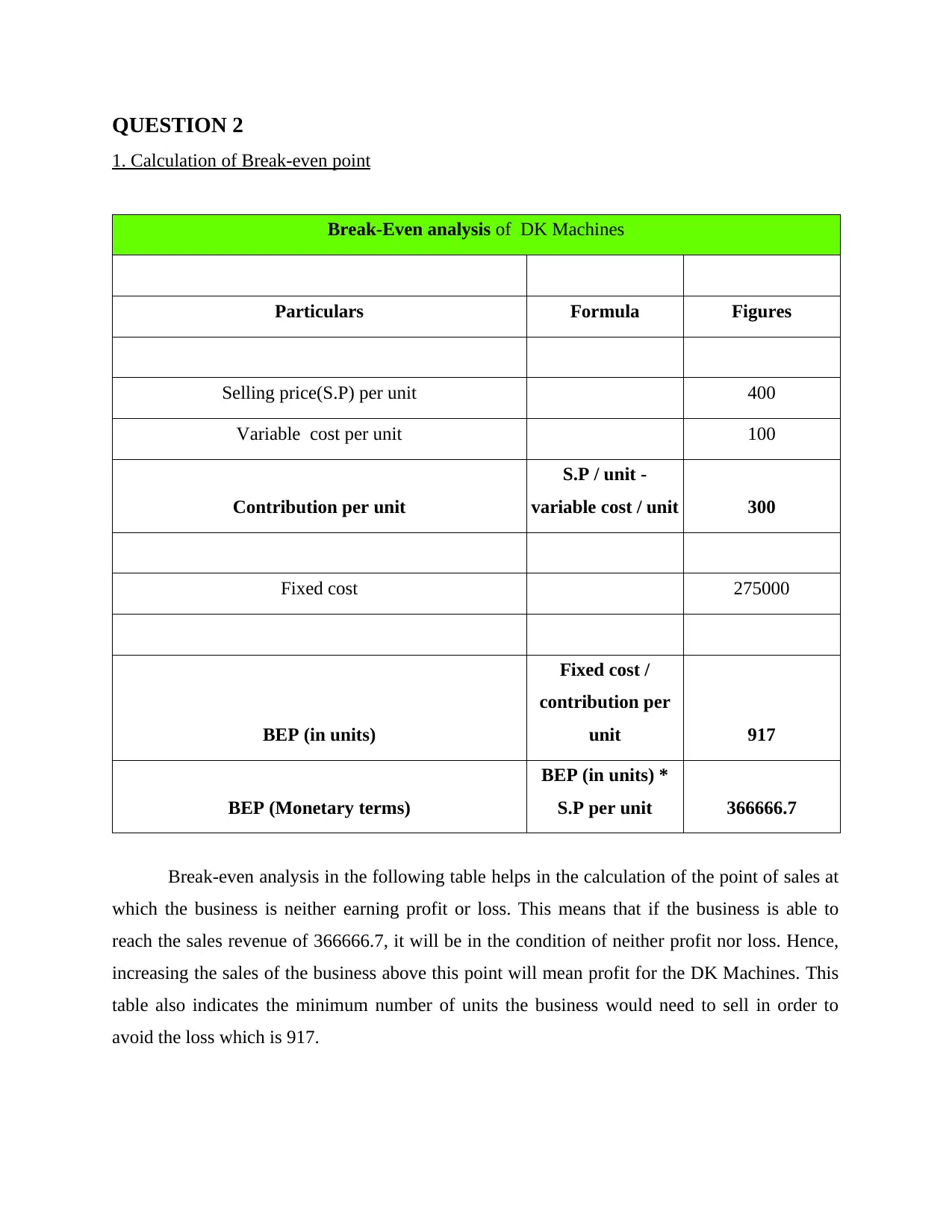

1. Calculation of Break-even point

Break-Even analysis of DK Machines

Particulars Formula Figures

Selling price(S.P) per unit 400

Variable cost per unit 100

Contribution per unit

S.P / unit -

variable cost / unit 300

Fixed cost 275000

BEP (in units)

Fixed cost /

contribution per

unit 917

BEP (Monetary terms)

BEP (in units) *

S.P per unit 366666.7

Break-even analysis in the following table helps in the calculation of the point of sales at

which the business is neither earning profit or loss. This means that if the business is able to

reach the sales revenue of 366666.7, it will be in the condition of neither profit nor loss. Hence,

increasing the sales of the business above this point will mean profit for the DK Machines. This

table also indicates the minimum number of units the business would need to sell in order to

avoid the loss which is 917.

1. Calculation of Break-even point

Break-Even analysis of DK Machines

Particulars Formula Figures

Selling price(S.P) per unit 400

Variable cost per unit 100

Contribution per unit

S.P / unit -

variable cost / unit 300

Fixed cost 275000

BEP (in units)

Fixed cost /

contribution per

unit 917

BEP (Monetary terms)

BEP (in units) *

S.P per unit 366666.7

Break-even analysis in the following table helps in the calculation of the point of sales at

which the business is neither earning profit or loss. This means that if the business is able to

reach the sales revenue of 366666.7, it will be in the condition of neither profit nor loss. Hence,

increasing the sales of the business above this point will mean profit for the DK Machines. This

table also indicates the minimum number of units the business would need to sell in order to

avoid the loss which is 917.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Utilization of break-even analysis for setting profitability targets

Break-even analysis is the calculation of the examination that is the margin of safety for

the entity that collects and associates costs. This method has been considered to be very effective

for the analysation of the sales that pays the costs for doing business. Break-even analysis can

help the company establish a product price for better results that changes the sales prices. This is

helpful for DK Machines to achieve maximum profit without having to increase the price. Break-

even analysis is used for the determination of the unused capacity of the company after it reaches

the break-even point. Business can use this point as the point which it needs to reach before

thinking of earning any kind of profit. Hence, this is the best way in which the business can set

its target for the profit it wants to earn with the projected revenue (Wegmann, 2019). This is

helpful for the determination of the changes in the profits in the price of product that is being

altered at the same time.

3. Adaptation of activity based costing and more accurate management accounting information

The management accounting information are very important as they help in making both

short-term and long-term decisions that involve the financial health of the company. For the

directors it is very important for having the accurate management accounting information as it

helps them to make operational decisions which have the intention to increase the company's

operational efficiency. This is very important for the company for making any kind of long term

investment decisions. It is very important for the business to adapt the activity based costing for

improving their ability to set fir monitoring the abilities and achieving the long term objectives.

The activity based costing is considered to be the one that provides the managers more accurate

production costs that can help the business to make more information that is about the product

and develop new methods of production.

This method is helpful for the realization of the more accurate production costs.

It is also helpful for assigning a specific overhead costs for more expensive products.

This is helpful for the evaluation of the efficiency of production and making

improvements.

Break-even analysis is the calculation of the examination that is the margin of safety for

the entity that collects and associates costs. This method has been considered to be very effective

for the analysation of the sales that pays the costs for doing business. Break-even analysis can

help the company establish a product price for better results that changes the sales prices. This is

helpful for DK Machines to achieve maximum profit without having to increase the price. Break-

even analysis is used for the determination of the unused capacity of the company after it reaches

the break-even point. Business can use this point as the point which it needs to reach before

thinking of earning any kind of profit. Hence, this is the best way in which the business can set

its target for the profit it wants to earn with the projected revenue (Wegmann, 2019). This is

helpful for the determination of the changes in the profits in the price of product that is being

altered at the same time.

3. Adaptation of activity based costing and more accurate management accounting information

The management accounting information are very important as they help in making both

short-term and long-term decisions that involve the financial health of the company. For the

directors it is very important for having the accurate management accounting information as it

helps them to make operational decisions which have the intention to increase the company's

operational efficiency. This is very important for the company for making any kind of long term

investment decisions. It is very important for the business to adapt the activity based costing for

improving their ability to set fir monitoring the abilities and achieving the long term objectives.

The activity based costing is considered to be the one that provides the managers more accurate

production costs that can help the business to make more information that is about the product

and develop new methods of production.

This method is helpful for the realization of the more accurate production costs.

It is also helpful for assigning a specific overhead costs for more expensive products.

This is helpful for the evaluation of the efficiency of production and making

improvements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

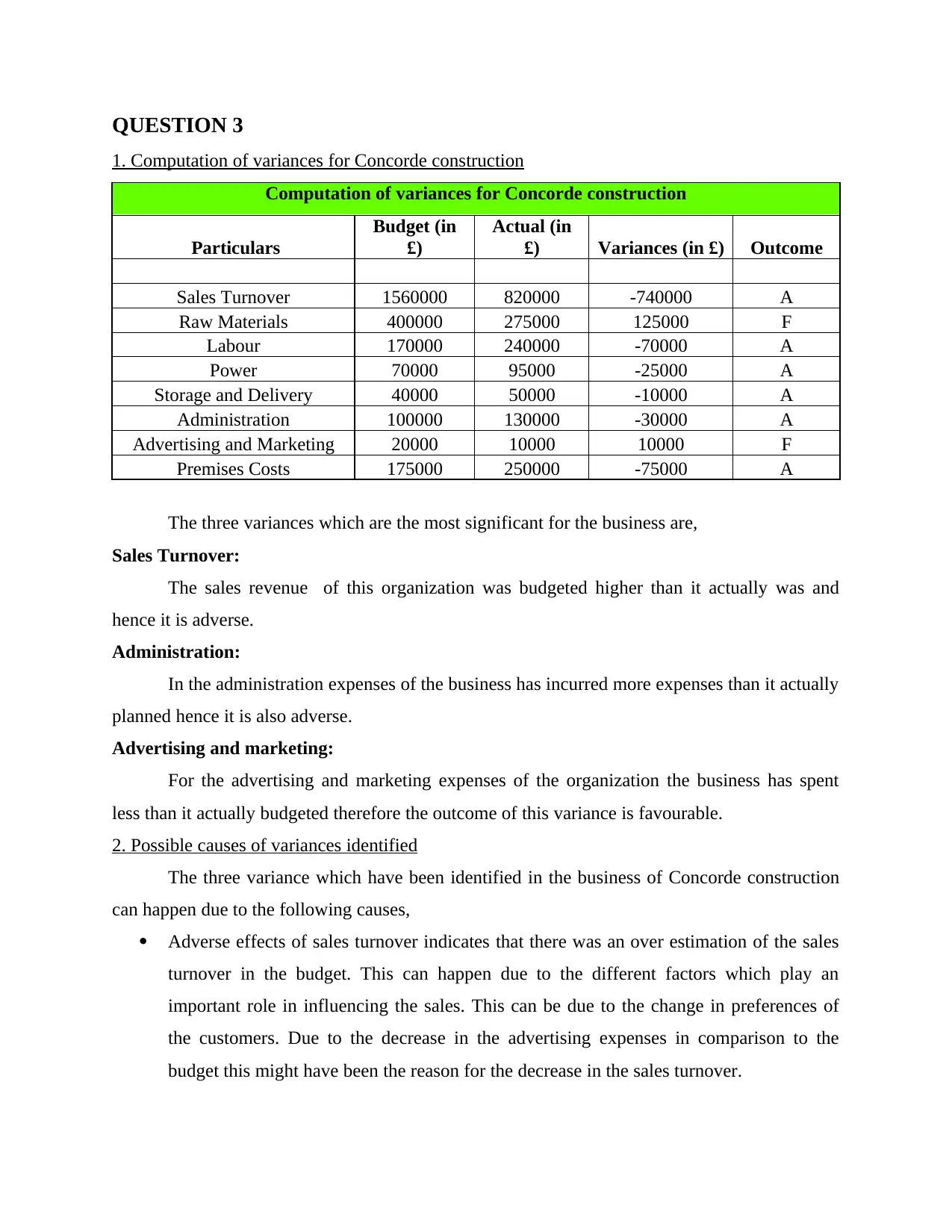

1. Computation of variances for Concorde construction

Computation of variances for Concorde construction

Particulars

Budget (in

£)

Actual (in

£) Variances (in £) Outcome

Sales Turnover 1560000 820000 -740000 A

Raw Materials 400000 275000 125000 F

Labour 170000 240000 -70000 A

Power 70000 95000 -25000 A

Storage and Delivery 40000 50000 -10000 A

Administration 100000 130000 -30000 A

Advertising and Marketing 20000 10000 10000 F

Premises Costs 175000 250000 -75000 A

The three variances which are the most significant for the business are,

Sales Turnover:

The sales revenue of this organization was budgeted higher than it actually was and

hence it is adverse.

Administration:

In the administration expenses of the business has incurred more expenses than it actually

planned hence it is also adverse.

Advertising and marketing:

For the advertising and marketing expenses of the organization the business has spent

less than it actually budgeted therefore the outcome of this variance is favourable.

2. Possible causes of variances identified

The three variance which have been identified in the business of Concorde construction

can happen due to the following causes,

Adverse effects of sales turnover indicates that there was an over estimation of the sales

turnover in the budget. This can happen due to the different factors which play an

important role in influencing the sales. This can be due to the change in preferences of

the customers. Due to the decrease in the advertising expenses in comparison to the

budget this might have been the reason for the decrease in the sales turnover.

1. Computation of variances for Concorde construction

Computation of variances for Concorde construction

Particulars

Budget (in

£)

Actual (in

£) Variances (in £) Outcome

Sales Turnover 1560000 820000 -740000 A

Raw Materials 400000 275000 125000 F

Labour 170000 240000 -70000 A

Power 70000 95000 -25000 A

Storage and Delivery 40000 50000 -10000 A

Administration 100000 130000 -30000 A

Advertising and Marketing 20000 10000 10000 F

Premises Costs 175000 250000 -75000 A

The three variances which are the most significant for the business are,

Sales Turnover:

The sales revenue of this organization was budgeted higher than it actually was and

hence it is adverse.

Administration:

In the administration expenses of the business has incurred more expenses than it actually

planned hence it is also adverse.

Advertising and marketing:

For the advertising and marketing expenses of the organization the business has spent

less than it actually budgeted therefore the outcome of this variance is favourable.

2. Possible causes of variances identified

The three variance which have been identified in the business of Concorde construction

can happen due to the following causes,

Adverse effects of sales turnover indicates that there was an over estimation of the sales

turnover in the budget. This can happen due to the different factors which play an

important role in influencing the sales. This can be due to the change in preferences of

the customers. Due to the decrease in the advertising expenses in comparison to the

budget this might have been the reason for the decrease in the sales turnover.

Administration expenses are expenses when depends on the management and their

efficiency of the work. Hence, it can be a result of poor management which has increased

the estimated expenses.

Lack of capital or liquidity can be the reason for not spending on the advertising

expenses.

3. Projection of likely consequences of variances

The chosen variance can have the following impacts on the business of the organization,

Sales Turnover Due to sales turnover variance having adverse result the business

will face major impacts on its profitability. The decrease in the

sales can also lead the business to the situation of loss. This can

impact the growth of the organization and might affect the future

of this business. Facing losses can have negative impacts to the

employees and management of the organization.

Administration Having adverse affects on the variance of administration

expenses shows that the business has spent more on the

administration/operational activities of the business. This can

help the business to gain efficiency and enhance the productivity

of the organization in the future.

Advertising and Marketing Favourable variance of the marketing and advertising means that

the business has spent less on the organization therefore can

result in decrease in the sales.

4. Strategies for correcting variances

This organization needs to adapt to strategies in-order to rectify the variances that has

occurred in its budget.

Sales turnover:

To increase the marketing expenditure.

To understand the target customers.

Increase efficiency for gaining competitive advantages.

efficiency of the work. Hence, it can be a result of poor management which has increased

the estimated expenses.

Lack of capital or liquidity can be the reason for not spending on the advertising

expenses.

3. Projection of likely consequences of variances

The chosen variance can have the following impacts on the business of the organization,

Sales Turnover Due to sales turnover variance having adverse result the business

will face major impacts on its profitability. The decrease in the

sales can also lead the business to the situation of loss. This can

impact the growth of the organization and might affect the future

of this business. Facing losses can have negative impacts to the

employees and management of the organization.

Administration Having adverse affects on the variance of administration

expenses shows that the business has spent more on the

administration/operational activities of the business. This can

help the business to gain efficiency and enhance the productivity

of the organization in the future.

Advertising and Marketing Favourable variance of the marketing and advertising means that

the business has spent less on the organization therefore can

result in decrease in the sales.

4. Strategies for correcting variances

This organization needs to adapt to strategies in-order to rectify the variances that has

occurred in its budget.

Sales turnover:

To increase the marketing expenditure.

To understand the target customers.

Increase efficiency for gaining competitive advantages.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Offering special promotions and discounts can help the business to influence its sales

turnover.

Administration:

Limiting the expenses which are made for unproductive measures.

Elimination of unnecessary subscription and memberships. Utilization of digital methods of storing data for cutting the paper and stationary costs.

Advertising and Marketing:

The marketing of this organization needs to be improved by utilization marketing

campaign.

Utilization of digital marketing practices can bring more efficiency to the marketing

practices of the business.

Increasing the marketing in different platforms for achieving greater results for the

business.

5. Presenting advantages disadvantages of switching from Incremental Based Budgeting to Zero

Based Budgeting

Incremental based budgeting is the process is not as affective because it has been known

to be the method that leads to the organization doing extra spendings. This method is not very

flexible in nature and hence does not consider any kind of change in the organization. It does not

provide a proper review of the budget. Due to this method being based on unreal assumptions

switching to Zero-based budgeting has been considered to be the factor that would help the

business to build on the own cost-benefit analysis that has been known to be justified for an

easier. This method has been known for better and most efficiency allocation of resources. It

provides the organization with the promotion of the business process management (Ibrahim,

2019). It is also the strengths of the strategic growth and transparency that is helpful for

improving the organizational benefits. This method considers the changes and has been known to

be more versatile.

turnover.

Administration:

Limiting the expenses which are made for unproductive measures.

Elimination of unnecessary subscription and memberships. Utilization of digital methods of storing data for cutting the paper and stationary costs.

Advertising and Marketing:

The marketing of this organization needs to be improved by utilization marketing

campaign.

Utilization of digital marketing practices can bring more efficiency to the marketing

practices of the business.

Increasing the marketing in different platforms for achieving greater results for the

business.

5. Presenting advantages disadvantages of switching from Incremental Based Budgeting to Zero

Based Budgeting

Incremental based budgeting is the process is not as affective because it has been known

to be the method that leads to the organization doing extra spendings. This method is not very

flexible in nature and hence does not consider any kind of change in the organization. It does not

provide a proper review of the budget. Due to this method being based on unreal assumptions

switching to Zero-based budgeting has been considered to be the factor that would help the

business to build on the own cost-benefit analysis that has been known to be justified for an

easier. This method has been known for better and most efficiency allocation of resources. It

provides the organization with the promotion of the business process management (Ibrahim,

2019). It is also the strengths of the strategic growth and transparency that is helpful for

improving the organizational benefits. This method considers the changes and has been known to

be more versatile.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Atoyebi, J. O., Bello, S. A. and Owolarafe, O. K., 2022. A case-study approach to profitability

assessment in fermented African locust beans (iru) production using break-even

analysis. Agricultural Engineering International: CIGR Journal. 24(1).

Husain, T. and Sunardi, N., 2020. Firm's Value Prediction Based on Profitability Ratios and

Dividend Policy. Finance & Economics Review. 2(2). pp.13-26.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Wegmann, G., 2019. A typology of cost accounting practices based on activity-based costing-a

strategic cost management approach. Asia-Pacific Management Accounting Journal. 14.

pp.161-184.

Books and Journals

Atoyebi, J. O., Bello, S. A. and Owolarafe, O. K., 2022. A case-study approach to profitability

assessment in fermented African locust beans (iru) production using break-even

analysis. Agricultural Engineering International: CIGR Journal. 24(1).

Husain, T. and Sunardi, N., 2020. Firm's Value Prediction Based on Profitability Ratios and

Dividend Policy. Finance & Economics Review. 2(2). pp.13-26.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Wegmann, G., 2019. A typology of cost accounting practices based on activity-based costing-a

strategic cost management approach. Asia-Pacific Management Accounting Journal. 14.

pp.161-184.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.