Comprehensive Financial Analysis Report: Stock Market Returns and Risk

VerifiedAdded on 2020/05/11

|13

|2153

|57

Report

AI Summary

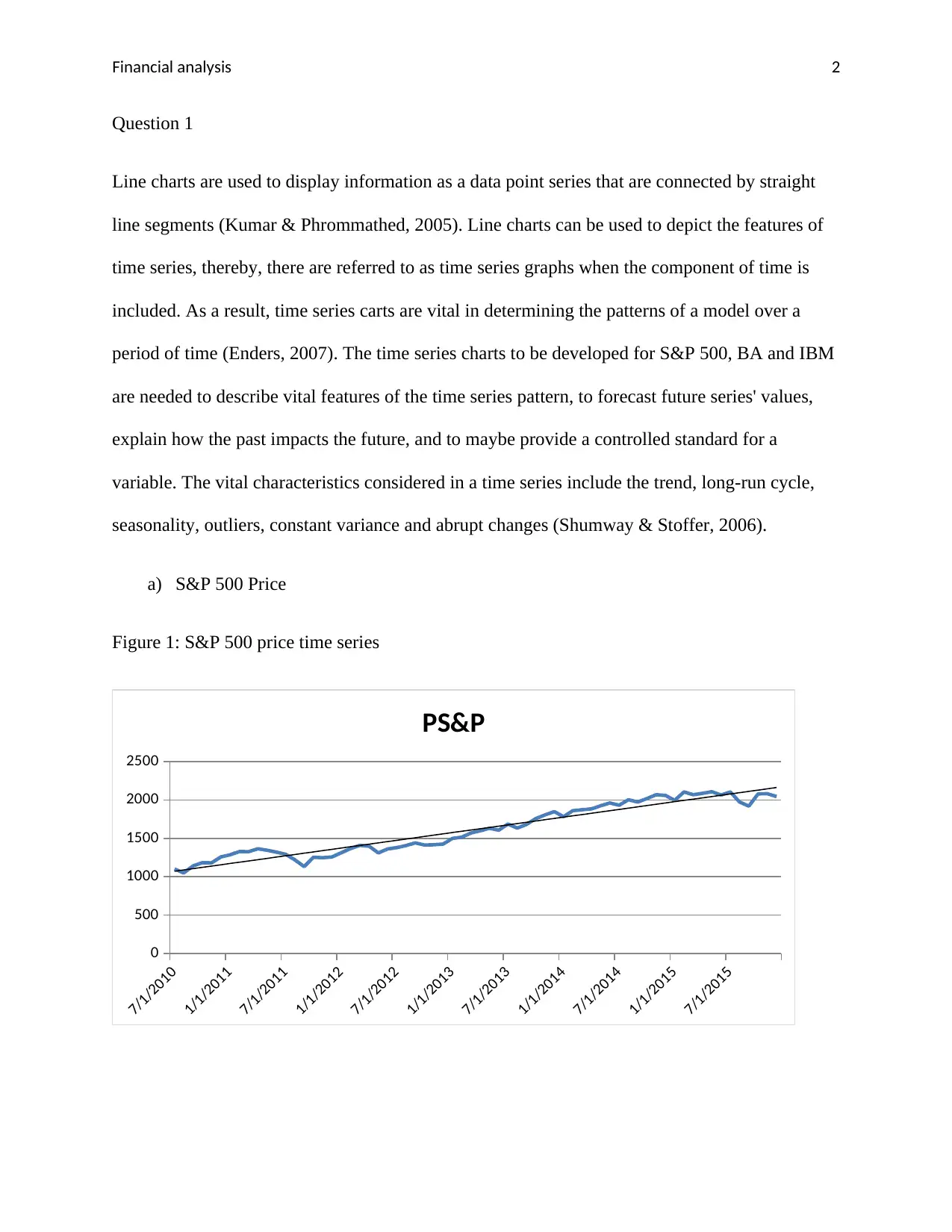

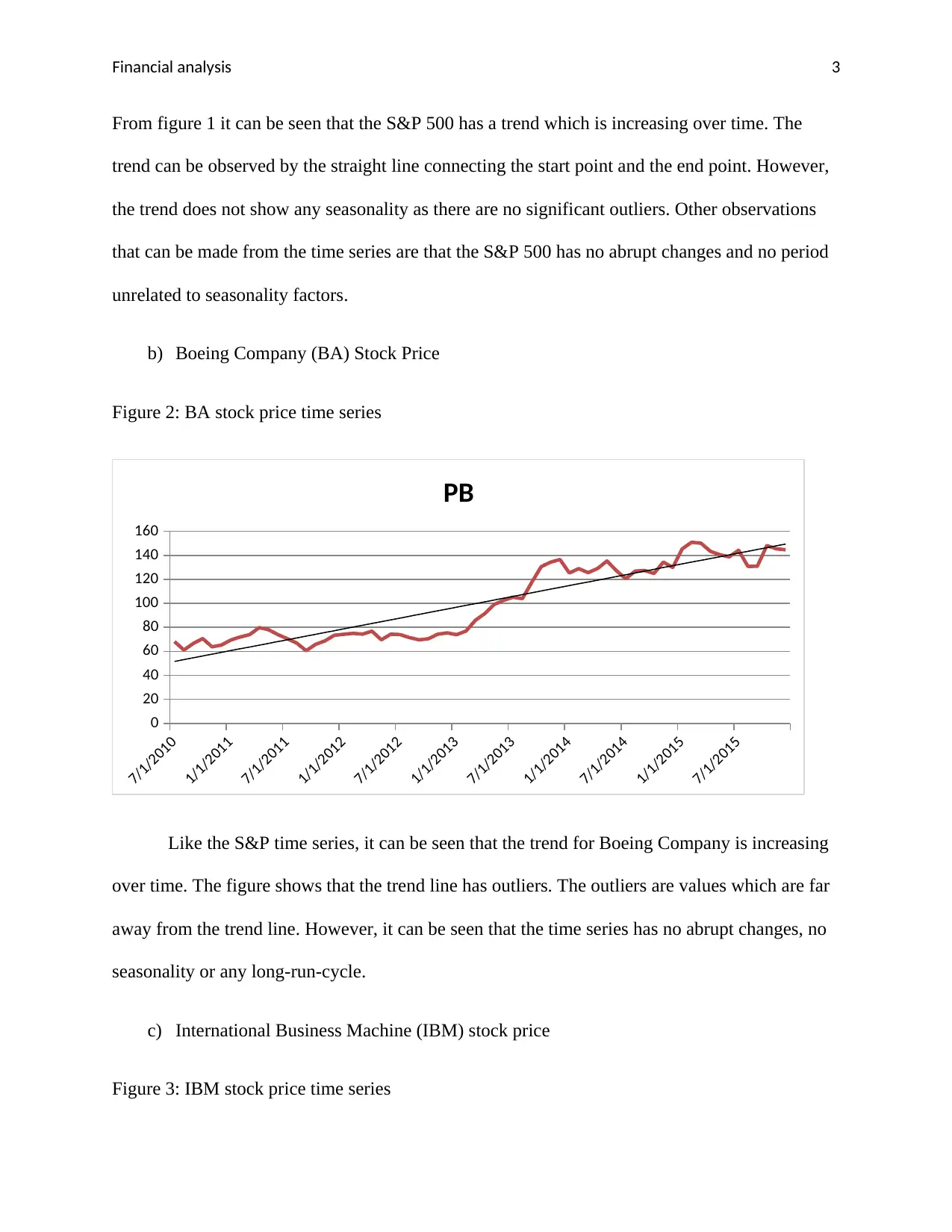

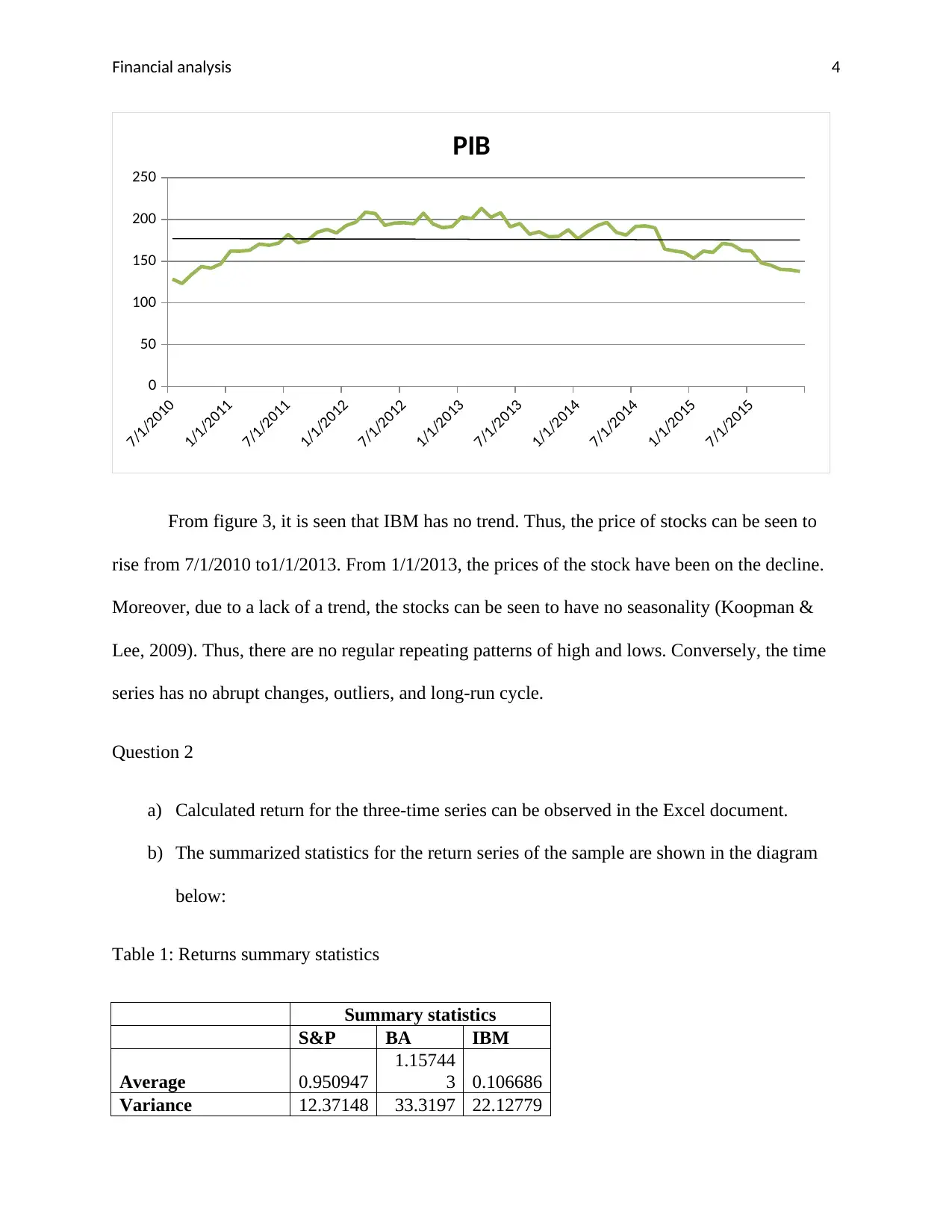

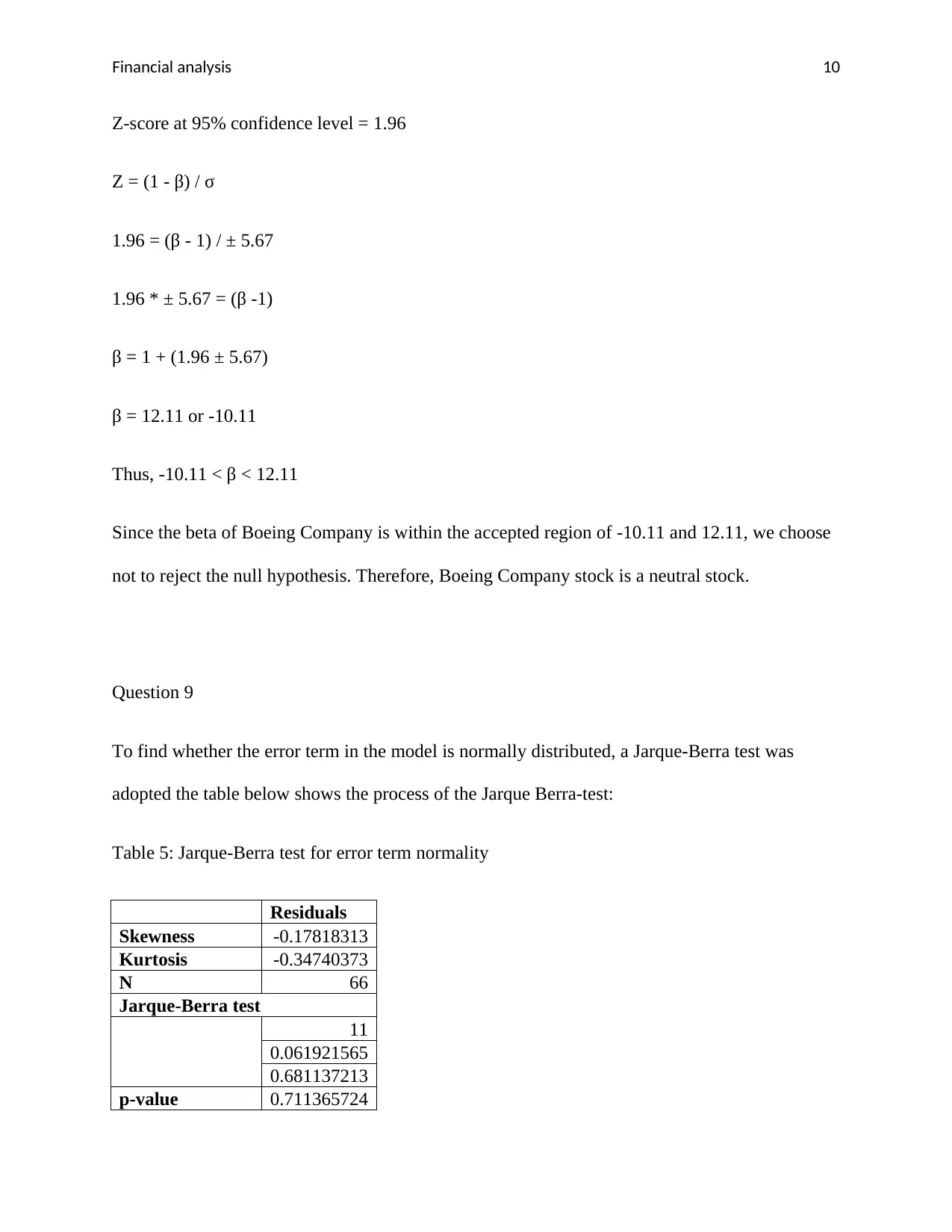

This report presents a comprehensive financial analysis of stock market data, focusing on the S&P 500, Boeing (BA), and IBM. The analysis begins with time series charts to visualize trends, cycles, and outliers in stock prices. Statistical methods are employed to calculate and compare returns, standard deviations, and risks associated with each stock. Hypothesis testing, including the Jarque-Bera test for normality, one-tailed z-tests, chi-square tests, and ANOVA, are used to evaluate stock performance and relationships between variables. The report further delves into regression analysis to determine beta coefficients and assess the volatility of Boeing stock relative to the market. The findings include insights into stock returns, risk assessment, and statistical validation of the results, concluding with a discussion of the preferred stock based on the analysis and the evaluation of the error term normality.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.