Financial Analysis of Superdry: Finance in Management and Leadership

VerifiedAdded on 2020/10/22

|10

|2931

|83

Report

AI Summary

This report provides a comprehensive financial analysis of Superdry, a UK-based clothing company. It begins with an executive summary outlining the importance of financial information for stakeholders and its role in decision-making. The report identifies key stakeholders like customers, employees, investors, and suppliers, detailing their respective interests in Superdry's financial performance. It explains the communication methods used to disseminate financial information, including meetings, conferences, and formal reports. The report then delves into the different types of financial data crucial for managerial decisions, such as cash flow statements and income statements, with specific examples from Superdry's 2017 and 2018 financial data. Furthermore, the report critically evaluates and compares Superdry's financial statements, highlighting the application of accounting concepts like business entity, money measurement, accrual, consistency, and going concern. It also discusses the accounting frameworks, including GAAP, IFRS, and IAS, used in preparing the financial statements, and concludes with an evaluation and comparison of the financial position of the company.

Finance In Management

And Leadership

And Leadership

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Finance in management and leadership ensures proper utilisation of resources and

provides a framework for decision making that assist in achievement of organisation's objectives

and goals. This report summarises importance of financial information for stakeholders and way

in which company can communicate its financial information to users, different types of

financial data and information required for decision making in respect of Superdry, UK's

clothing company. It also describes comparison of financial statements of company by

considering framework and concept applied. Financial data and information required in

Superdry organisation for taking important decisions. Managers use these reports to take

important decisions for the benefits of company. These data show clear picture of the current

organisations growth and its financial position. Financial management help organisation to find

out actual position and areas where an organisation should focus upon to increase in growth and

stay in the competition. Following are the different types of financial data required by mangers to

make important decisions:

Cash Flow Statement: Company requires cash flow statements to check the out flow and in flow

of funds. Cash flow statement show the actual usage of cash in an organisation. This data is

required by the company

Finance in management and leadership ensures proper utilisation of resources and

provides a framework for decision making that assist in achievement of organisation's objectives

and goals. This report summarises importance of financial information for stakeholders and way

in which company can communicate its financial information to users, different types of

financial data and information required for decision making in respect of Superdry, UK's

clothing company. It also describes comparison of financial statements of company by

considering framework and concept applied. Financial data and information required in

Superdry organisation for taking important decisions. Managers use these reports to take

important decisions for the benefits of company. These data show clear picture of the current

organisations growth and its financial position. Financial management help organisation to find

out actual position and areas where an organisation should focus upon to increase in growth and

stay in the competition. Following are the different types of financial data required by mangers to

make important decisions:

Cash Flow Statement: Company requires cash flow statements to check the out flow and in flow

of funds. Cash flow statement show the actual usage of cash in an organisation. This data is

required by the company

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Users (stakeholders) interested in receiving financial information of Superdry:....................1

2. Communication of financial information with all organisational stakeholders:......................2

3. Different types of financial data and information required for decision making....................3

4. Critical evaluation and comparison of financial statements along with accounting concept

and framework:............................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Users (stakeholders) interested in receiving financial information of Superdry:....................1

2. Communication of financial information with all organisational stakeholders:......................2

3. Different types of financial data and information required for decision making....................3

4. Critical evaluation and comparison of financial statements along with accounting concept

and framework:............................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance refers to management of funds and combines functions such as borrowing,

lending, investing, budgeting etc. Management and leadership are vital aspect of an organisation

and both are interlinked with finance and related activities (Renz, 2016). This report describes

users of financial information and extent of interest, circulation of financial information to

stakeholders and information required for decision making in the context of Superdry. It is an

UK based company engaged in selling clothings under its own name label. This report also

provides a critical evaluation and comparison of financial statements while discussing

appropriate accounting concepts and framework used in producing them.

TASK

1. Users (stakeholders) interested in receiving financial information of Superdry:

Stakeholders are individuals who influence and influenced by actions of organisation,

objectives and different policies. Stakeholders' support is necessary for organisation to attain

objectives and goals. Some of the major stakeholders are investors, employees, directors,

creditors etc. All these stakeholders have their own interest in organisation. For example

organisation's customers always demands fair practices and good quality products but customers

are not have same kind of interest as organisation's employees holds. Stakeholders are classified

as internal stakeholders and external stakeholders as per nature and extent of concern or interest

in organisation (Boyd, 2017). Internal stakeholders are individuals working in organisation or

having direct relation with organisation. Where as external stakeholders are those individual who

do not have direct relationship with company. In this context Superdry has following

stakeholders who are interested in receiving financial information of company:

Customers: Customers are real stakeholders of company as they are get affected by brand

value and quality of products, company is selling. Superdry is clothing brand and selling its

products by its name label so customer are interested in receiving financial information to

analyse the brand value and popularity of company in market.

Employees: Employees are direct stakeholders of company and holds their stake in

company in form of salary and employment safety. They have direct impact of growth and

performance of company. In Superdry there are thousands of employees operating company's

1

Finance refers to management of funds and combines functions such as borrowing,

lending, investing, budgeting etc. Management and leadership are vital aspect of an organisation

and both are interlinked with finance and related activities (Renz, 2016). This report describes

users of financial information and extent of interest, circulation of financial information to

stakeholders and information required for decision making in the context of Superdry. It is an

UK based company engaged in selling clothings under its own name label. This report also

provides a critical evaluation and comparison of financial statements while discussing

appropriate accounting concepts and framework used in producing them.

TASK

1. Users (stakeholders) interested in receiving financial information of Superdry:

Stakeholders are individuals who influence and influenced by actions of organisation,

objectives and different policies. Stakeholders' support is necessary for organisation to attain

objectives and goals. Some of the major stakeholders are investors, employees, directors,

creditors etc. All these stakeholders have their own interest in organisation. For example

organisation's customers always demands fair practices and good quality products but customers

are not have same kind of interest as organisation's employees holds. Stakeholders are classified

as internal stakeholders and external stakeholders as per nature and extent of concern or interest

in organisation (Boyd, 2017). Internal stakeholders are individuals working in organisation or

having direct relation with organisation. Where as external stakeholders are those individual who

do not have direct relationship with company. In this context Superdry has following

stakeholders who are interested in receiving financial information of company:

Customers: Customers are real stakeholders of company as they are get affected by brand

value and quality of products, company is selling. Superdry is clothing brand and selling its

products by its name label so customer are interested in receiving financial information to

analyse the brand value and popularity of company in market.

Employees: Employees are direct stakeholders of company and holds their stake in

company in form of salary and employment safety. They have direct impact of growth and

performance of company. In Superdry there are thousands of employees operating company's

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stores and offices, they require financial information to evaluate growth of company, in order to

make assurance about their employment safety concerns.

Investors: Investors are real stakeholders of company as they bear risks by investing

funds and money in company and always having concern about return from funds invested. In

Superdry investors make investment by purchasing company's securities and, they require

financial information to assess the viability of such investment made by them in company.

Government: Government is a kind of external stakeholder and holds their stake in form

of taxes and duties. Government collects taxes on income earned by companies. Government

requires various information and details from Superdry in form of various return to assess the

actual amount of tax payable by them (Chisholm-Burns, Vaillancourt and Shepherd, 2012).

Suppliers and vendors: Suppliers and vendors provides goods and services. Generally in

corporate world they provides goods or services on credit. They can affect supply of product or

services. Superdry has suppliers and they require company's financial information to analyse

company's liquidity and profitability positions, to know whether company is able to make

payments against supplies.

2. Communication of financial information with all organisational stakeholders:

In corporates financial information includes financial statement, income statements, cash

flow statement and other financial news or information related to company. Using these

information various internal or external stakeholders take vital decisions and such decisions of

stakeholders affects organisation performance and growth. So in corporates such information is

communicated to stakeholders in formal manner. Effectively communication of financial

information to all internal and external stakeholder is necessary for organisation to take financial

decisions. Financial information are used by stakeholders to different-different purpose but

communication of such information helps to develop trust in these stakeholders. Communication

of financial information also act as a golden chance to attract new customers and investors which

leads to enhancement of brand value (Frich, 2015).

In Superdry in order to communicate the financial information like balance sheet, income

statement or profit and loss account, statement of cash flow etc., company conducts meetings,

conferences, send written or formal letters, email etc. Communication of financial information is

some times is necessary due to law and regulations such company is required to file tax returns

and annual accounts to regulatory authorities. Beside this company organise annual general

2

make assurance about their employment safety concerns.

Investors: Investors are real stakeholders of company as they bear risks by investing

funds and money in company and always having concern about return from funds invested. In

Superdry investors make investment by purchasing company's securities and, they require

financial information to assess the viability of such investment made by them in company.

Government: Government is a kind of external stakeholder and holds their stake in form

of taxes and duties. Government collects taxes on income earned by companies. Government

requires various information and details from Superdry in form of various return to assess the

actual amount of tax payable by them (Chisholm-Burns, Vaillancourt and Shepherd, 2012).

Suppliers and vendors: Suppliers and vendors provides goods and services. Generally in

corporate world they provides goods or services on credit. They can affect supply of product or

services. Superdry has suppliers and they require company's financial information to analyse

company's liquidity and profitability positions, to know whether company is able to make

payments against supplies.

2. Communication of financial information with all organisational stakeholders:

In corporates financial information includes financial statement, income statements, cash

flow statement and other financial news or information related to company. Using these

information various internal or external stakeholders take vital decisions and such decisions of

stakeholders affects organisation performance and growth. So in corporates such information is

communicated to stakeholders in formal manner. Effectively communication of financial

information to all internal and external stakeholder is necessary for organisation to take financial

decisions. Financial information are used by stakeholders to different-different purpose but

communication of such information helps to develop trust in these stakeholders. Communication

of financial information also act as a golden chance to attract new customers and investors which

leads to enhancement of brand value (Frich, 2015).

In Superdry in order to communicate the financial information like balance sheet, income

statement or profit and loss account, statement of cash flow etc., company conducts meetings,

conferences, send written or formal letters, email etc. Communication of financial information is

some times is necessary due to law and regulations such company is required to file tax returns

and annual accounts to regulatory authorities. Beside this company organise annual general

2

meetings, interim general meetings and extraordinary general meetings to circulate and

communicate annual performance and results of company. For communication with suppliers

company conducts meetings on quarterly and monthly basis. However sometimes to

communicates with its large number of small suppliers company hold seminars and conference.

Any communication of financial information with employees company send emails or hold

meetings. Communication with customers is difficult and costly but necessary so company

adopts adversing methods to communicate financial information relevant for them (Elloker,

2012).

3. Different types of financial data and information required for decision making

Financial data and information required in Superdry organisation for taking important

decisions. Managers use these reports to take important decisions for the benefits of company.

These data show clear picture of the current organisations growth and its financial position.

Financial management help organisation to find out actual position and areas where an

organisation should focus upon to increase in growth and stay in the competition. Following are

the different types of financial data required by mangers to make important decisions:

Cash Flow Statement: Company requires cash flow statements to check the out flow

and in flow of funds (Hoch and Dulebohn, 2013). Cash flow statement show the actual

usage of cash in an organisation. This data is required by the company to control its cash

expenses and increase the circulation of cash in company. Superdry use its cashflow

statement to measure its inflows and outflows and make new and better strategies.

Statements of Income: Statements of income is required by the company to see its

revenue and expenses incurred to earn those revenue (Austin and et.al., 2013). Superdry

also uses its statements of income to check its efficiency and formulate new strategies to

increase its growth and revenue and also control its unnecessary expenses.

Income Statements (Profit and Loss account): As per income statement of Superdry it

is evaluated that company is enjoying profitability position in year 2018. Company's net profit is

increased to £ 76.3 million in year 2018 which was £ 68.7 million in year 2017 exhibits overall

increase of 11.06%. Company has reported overall revenue of £ 872 million in 2018 which was £

752 million in year 2017 which represent that gross sales of company is increased by 15.96%.

Cash Flow statement: As per cash flow statement of Superdry, company's overall cash

obtained through operating activities are increased from £62.3 million to £80.1 million which

3

communicate annual performance and results of company. For communication with suppliers

company conducts meetings on quarterly and monthly basis. However sometimes to

communicates with its large number of small suppliers company hold seminars and conference.

Any communication of financial information with employees company send emails or hold

meetings. Communication with customers is difficult and costly but necessary so company

adopts adversing methods to communicate financial information relevant for them (Elloker,

2012).

3. Different types of financial data and information required for decision making

Financial data and information required in Superdry organisation for taking important

decisions. Managers use these reports to take important decisions for the benefits of company.

These data show clear picture of the current organisations growth and its financial position.

Financial management help organisation to find out actual position and areas where an

organisation should focus upon to increase in growth and stay in the competition. Following are

the different types of financial data required by mangers to make important decisions:

Cash Flow Statement: Company requires cash flow statements to check the out flow

and in flow of funds (Hoch and Dulebohn, 2013). Cash flow statement show the actual

usage of cash in an organisation. This data is required by the company to control its cash

expenses and increase the circulation of cash in company. Superdry use its cashflow

statement to measure its inflows and outflows and make new and better strategies.

Statements of Income: Statements of income is required by the company to see its

revenue and expenses incurred to earn those revenue (Austin and et.al., 2013). Superdry

also uses its statements of income to check its efficiency and formulate new strategies to

increase its growth and revenue and also control its unnecessary expenses.

Income Statements (Profit and Loss account): As per income statement of Superdry it

is evaluated that company is enjoying profitability position in year 2018. Company's net profit is

increased to £ 76.3 million in year 2018 which was £ 68.7 million in year 2017 exhibits overall

increase of 11.06%. Company has reported overall revenue of £ 872 million in 2018 which was £

752 million in year 2017 which represent that gross sales of company is increased by 15.96%.

Cash Flow statement: As per cash flow statement of Superdry, company's overall cash

obtained through operating activities are increased from £62.3 million to £80.1 million which

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

points towards increased efficiency of company to generate cash from its operating activities.

Due to purchase of capital assets company's cash flow from investing activities is negative and

increased as compared to past year (Middlehurst, 2013). However overall cash flow of company

from all activities is positive in both year and increased to £ 75.8 million.

4. Critical evaluation and comparison of financial statements along with accounting concept and

framework:

Accounting concepts: Accounting concepts is core and essential rules, assumptions and

principles that act as a groundwork for entering financial transaction and preparing financial

statements (Rickards, 2012). Accounting concepts are applied and followed by business

organisation across the world which helps to create uniformity in financial information

worldwide. It also helps to maintain consistency in accounting records. Following are the major

accounting concepts that are used by Superdry to formulate financial statements:

Business entity concept: This concept state that business is considered as separate legal

entity. The capital or money invested by business owner of Superdry is considered as the liability

of respective company to pay back its owner.

Money measurement concept: Herein, Superdry only those transaction are recorded

which can be measured in term of money. There are other factors also which affect the business

like honesty and sincerity that affect the business but can not be recorded as they cannot be

measured in form of money.

Accrual Concept: Superdry by following this concept recognise revenue or income

when earned and received but expenses or liabilities are recorded as they occur. This concept

provides actual result of company by considering probable expenses and liabilities.

Consistency Concept: It ensures that accounting methods applied or adopted by

Superdry should be followed consistently from one period to other period which lead to

reliability of information while doing comparison of data of two or more year.

Going Concern concept: As per this concept Superdy prepare their financial statement

on the basis of assumption that company will operate for foreseeable future.

Accounting Framework: Accounting framework is systematic collection of criteria that

is applied to assess, identify, disclose and provide information stated in financial statements.

Financial statement of organisation should be prepared as accounting framework because such

financial statement provides true and fair view of financial informations. Most common and

4

Due to purchase of capital assets company's cash flow from investing activities is negative and

increased as compared to past year (Middlehurst, 2013). However overall cash flow of company

from all activities is positive in both year and increased to £ 75.8 million.

4. Critical evaluation and comparison of financial statements along with accounting concept and

framework:

Accounting concepts: Accounting concepts is core and essential rules, assumptions and

principles that act as a groundwork for entering financial transaction and preparing financial

statements (Rickards, 2012). Accounting concepts are applied and followed by business

organisation across the world which helps to create uniformity in financial information

worldwide. It also helps to maintain consistency in accounting records. Following are the major

accounting concepts that are used by Superdry to formulate financial statements:

Business entity concept: This concept state that business is considered as separate legal

entity. The capital or money invested by business owner of Superdry is considered as the liability

of respective company to pay back its owner.

Money measurement concept: Herein, Superdry only those transaction are recorded

which can be measured in term of money. There are other factors also which affect the business

like honesty and sincerity that affect the business but can not be recorded as they cannot be

measured in form of money.

Accrual Concept: Superdry by following this concept recognise revenue or income

when earned and received but expenses or liabilities are recorded as they occur. This concept

provides actual result of company by considering probable expenses and liabilities.

Consistency Concept: It ensures that accounting methods applied or adopted by

Superdry should be followed consistently from one period to other period which lead to

reliability of information while doing comparison of data of two or more year.

Going Concern concept: As per this concept Superdy prepare their financial statement

on the basis of assumption that company will operate for foreseeable future.

Accounting Framework: Accounting framework is systematic collection of criteria that

is applied to assess, identify, disclose and provide information stated in financial statements.

Financial statement of organisation should be prepared as accounting framework because such

financial statement provides true and fair view of financial informations. Most common and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

widely accepted accounting framework is GAAP, IAS and IFRS. GAAP s are generally accepted

accounting principles which provide general guidelines about preparation and presentation of

financial statements. IFRS are intentional financial reporting standards which are internationally

accepted accounting standards that provide a set of standards that are required to be followed by

entities to frame financial statements (Javadi, Rezaee and Salehzadeh, 2013). GAAP is mostly

applied by companies in United States, whereas IFRS are used by business organisation all over

the world. Superdry follows GAAP and IFRS while preparing financial statements. For example

company fulfils disclosure requirement as per IFRS-1. Such Conceptual Framework provides a

basis for application of fundamental concepts for the purpose of financial reporting that provide

guidance to board of directors. It assist to give assurance that Standards applied are consistently

and conceptually right. Beside this IAS( international accounting standards) are also followed by

company. IAS are now replaced with IFRS but some standards are not replaced yet so company

follows such old IAS. The overall objective of these frameworks is to make uniformity and

equalities in accounting across the world.

Evaluation and comparison of financial statements of Superdry:

Following is a critical evaluation and comparison of financial statements such as balance

sheet, income statement and cash flow of Superdry for the year 2018 and 2017, as follows:

Statement of financial position (Balance Sheet): Superdry's balance sheet is prepared as per

GAAP, IFRS and IAS. Company has reported net assets or shareholder's fund of £408.5 million

and £372.5 million in year 2018 and 2017 respectively. Which indicates that company's net asset

is increased by 9.66%. In year 2018 company has reported non current assets of £236.6 million,

and total current assets of £378.1 million which in year 2017 was 212.7 million and 340.1

million respectively. That is indication that company is overall assets are increased and

company's ability to generate assets is enhanced. However company's long term debt has been

increased by £10.6 million. It is also notable that company's current liabilities is increased to

£148 million in year 2018 which was 132.1 in year 2017.

5

accounting principles which provide general guidelines about preparation and presentation of

financial statements. IFRS are intentional financial reporting standards which are internationally

accepted accounting standards that provide a set of standards that are required to be followed by

entities to frame financial statements (Javadi, Rezaee and Salehzadeh, 2013). GAAP is mostly

applied by companies in United States, whereas IFRS are used by business organisation all over

the world. Superdry follows GAAP and IFRS while preparing financial statements. For example

company fulfils disclosure requirement as per IFRS-1. Such Conceptual Framework provides a

basis for application of fundamental concepts for the purpose of financial reporting that provide

guidance to board of directors. It assist to give assurance that Standards applied are consistently

and conceptually right. Beside this IAS( international accounting standards) are also followed by

company. IAS are now replaced with IFRS but some standards are not replaced yet so company

follows such old IAS. The overall objective of these frameworks is to make uniformity and

equalities in accounting across the world.

Evaluation and comparison of financial statements of Superdry:

Following is a critical evaluation and comparison of financial statements such as balance

sheet, income statement and cash flow of Superdry for the year 2018 and 2017, as follows:

Statement of financial position (Balance Sheet): Superdry's balance sheet is prepared as per

GAAP, IFRS and IAS. Company has reported net assets or shareholder's fund of £408.5 million

and £372.5 million in year 2018 and 2017 respectively. Which indicates that company's net asset

is increased by 9.66%. In year 2018 company has reported non current assets of £236.6 million,

and total current assets of £378.1 million which in year 2017 was 212.7 million and 340.1

million respectively. That is indication that company is overall assets are increased and

company's ability to generate assets is enhanced. However company's long term debt has been

increased by £10.6 million. It is also notable that company's current liabilities is increased to

£148 million in year 2018 which was 132.1 in year 2017.

5

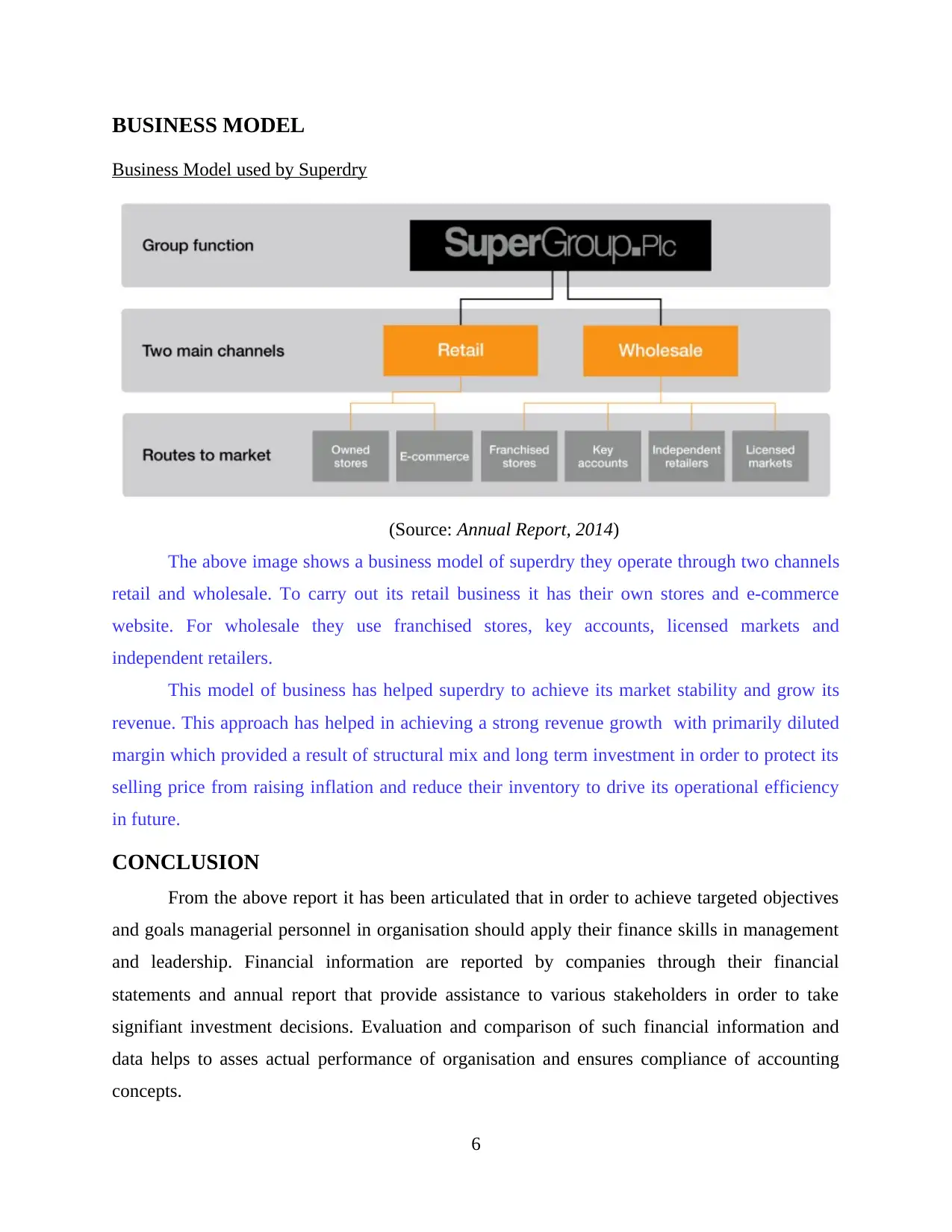

BUSINESS MODEL

Business Model used by Superdry

(Source: Annual Report, 2014)

The above image shows a business model of superdry they operate through two channels

retail and wholesale. To carry out its retail business it has their own stores and e-commerce

website. For wholesale they use franchised stores, key accounts, licensed markets and

independent retailers.

This model of business has helped superdry to achieve its market stability and grow its

revenue. This approach has helped in achieving a strong revenue growth with primarily diluted

margin which provided a result of structural mix and long term investment in order to protect its

selling price from raising inflation and reduce their inventory to drive its operational efficiency

in future.

CONCLUSION

From the above report it has been articulated that in order to achieve targeted objectives

and goals managerial personnel in organisation should apply their finance skills in management

and leadership. Financial information are reported by companies through their financial

statements and annual report that provide assistance to various stakeholders in order to take

signifiant investment decisions. Evaluation and comparison of such financial information and

data helps to asses actual performance of organisation and ensures compliance of accounting

concepts.

6

Business Model used by Superdry

(Source: Annual Report, 2014)

The above image shows a business model of superdry they operate through two channels

retail and wholesale. To carry out its retail business it has their own stores and e-commerce

website. For wholesale they use franchised stores, key accounts, licensed markets and

independent retailers.

This model of business has helped superdry to achieve its market stability and grow its

revenue. This approach has helped in achieving a strong revenue growth with primarily diluted

margin which provided a result of structural mix and long term investment in order to protect its

selling price from raising inflation and reduce their inventory to drive its operational efficiency

in future.

CONCLUSION

From the above report it has been articulated that in order to achieve targeted objectives

and goals managerial personnel in organisation should apply their finance skills in management

and leadership. Financial information are reported by companies through their financial

statements and annual report that provide assistance to various stakeholders in order to take

signifiant investment decisions. Evaluation and comparison of such financial information and

data helps to asses actual performance of organisation and ensures compliance of accounting

concepts.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Boyd, B., et.al., 2017. Hybrid organizations: New business models for environmental leadership.

Routledge.

Chisholm-Burns, M. A., Vaillancourt, A. M. and Shepherd, M., 2012. Pharmacy management,

leadership, marketing, and finance. Jones & Bartlett Publishers.

Elloker, S., et.al., 2012. Crises, routines and innovations: the complexities and possibilities of

sub-district management: leadership and governance. South African health review.

2012(2012/2013). pp.161-173.

Javadi, M. H. M., Rezaee, M. S. and Salehzadeh, R., 2013. Investigating the relationship

between self-leadership strategies and job satisfaction. International Journal of

Academic Research in Accounting, Finance and Management Sciences. 3(3). pp.284-

289.

Middlehurst, R., 2013. Changing Internal Governance: Are Leadership Roles and Management

Structures in United Kingdom Universities Fit for the Future?. Higher Education

Quarterly. 67(3). pp.275-294.

Frich, J. C., et.al., 2015. Leadership development programs for physicians: a systematic review.

Journal of general internal medicine. 30(5). pp.656-674.

Hoch, J. E. and Dulebohn, J. H., 2013. Shared leadership in enterprise resource planning and

human resource management system implementation. Human Resource Management

Review. 23(1). pp.114-125.

Austin, C., et.al., 2013. Application of Project Management in Higher Education. Journal of

Economic Development, Management, IT, Finance & Marketing. 5(2).

Rickards, T., 2012. Dilemmas of leadership. Routledge.

Online

Business Model of superdry group, Annual report, 2014. [Online]. Available through:

<http://annualreport2014.supergroup.co.uk/strategic-report/strategic-report>.

Annual report of Superdry, 2018. [Online]. Available through:

<https://corporate.superdry.com/media/2479/superdry-ar2018-indexed-linked3.pdf>.

7

Books and Journals:

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Boyd, B., et.al., 2017. Hybrid organizations: New business models for environmental leadership.

Routledge.

Chisholm-Burns, M. A., Vaillancourt, A. M. and Shepherd, M., 2012. Pharmacy management,

leadership, marketing, and finance. Jones & Bartlett Publishers.

Elloker, S., et.al., 2012. Crises, routines and innovations: the complexities and possibilities of

sub-district management: leadership and governance. South African health review.

2012(2012/2013). pp.161-173.

Javadi, M. H. M., Rezaee, M. S. and Salehzadeh, R., 2013. Investigating the relationship

between self-leadership strategies and job satisfaction. International Journal of

Academic Research in Accounting, Finance and Management Sciences. 3(3). pp.284-

289.

Middlehurst, R., 2013. Changing Internal Governance: Are Leadership Roles and Management

Structures in United Kingdom Universities Fit for the Future?. Higher Education

Quarterly. 67(3). pp.275-294.

Frich, J. C., et.al., 2015. Leadership development programs for physicians: a systematic review.

Journal of general internal medicine. 30(5). pp.656-674.

Hoch, J. E. and Dulebohn, J. H., 2013. Shared leadership in enterprise resource planning and

human resource management system implementation. Human Resource Management

Review. 23(1). pp.114-125.

Austin, C., et.al., 2013. Application of Project Management in Higher Education. Journal of

Economic Development, Management, IT, Finance & Marketing. 5(2).

Rickards, T., 2012. Dilemmas of leadership. Routledge.

Online

Business Model of superdry group, Annual report, 2014. [Online]. Available through:

<http://annualreport2014.supergroup.co.uk/strategic-report/strategic-report>.

Annual report of Superdry, 2018. [Online]. Available through:

<https://corporate.superdry.com/media/2479/superdry-ar2018-indexed-linked3.pdf>.

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.