Financial Resources Analysis Report for Swipe Wire Production Company

VerifiedAdded on 2021/02/19

|13

|3204

|117

Report

AI Summary

This report provides a financial analysis of Swipe Wire, a small production company planning for expansion. It explores management and financial accounting techniques, comparing their differences and respective users. The report utilizes capital budgeting techniques like NPV, ARR, and IRR to evaluate investment options and calculate various financial ratios to assess the company's performance. Recommendations are made regarding the utilization of external funding sources to improve the debt ratio. The analysis includes a cost-benefit analysis, payback period calculation, accounting rate of return, net present value, and internal rate of return for different projects. Finally, the report calculates and compares financial ratios, offering suggestions for improvement and concluding with a recommendation for the most beneficial project for Swipe Wire. This analysis helps in making informed investment decisions and understanding the financial health of the company.

Financial Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The following report is based upon a small production company Swipe Wire which is

planning for expansion. For the purpose of analysis management and financial accounting

techniques with their difference and respective users are discussed in this project. With the help

of different capital budgeting techniques such as NPV, ARR, IRR etc. the organisation can make

investment in best option. In order to evaluate performance of the company different ratios are

calculated in present report. The enterprise is recommended to formulate strategies for utilising

external sources more than internal funds for business execution so that debt ratio could be

increased.

The following report is based upon a small production company Swipe Wire which is

planning for expansion. For the purpose of analysis management and financial accounting

techniques with their difference and respective users are discussed in this project. With the help

of different capital budgeting techniques such as NPV, ARR, IRR etc. the organisation can make

investment in best option. In order to evaluate performance of the company different ratios are

calculated in present report. The enterprise is recommended to formulate strategies for utilising

external sources more than internal funds for business execution so that debt ratio could be

increased.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Explanation of management and financial accounting................................................................1

Difference between management and financial accounting with respective users......................1

QUESTION2....................................................................................................................................2

Cost benefit analysis....................................................................................................................2

Payback period.............................................................................................................................3

Accounting rate of return.............................................................................................................4

Net present value and internal rate of return................................................................................5

Analysis and conclusion..............................................................................................................6

QUESTION 3...................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Comparison of ratios....................................................................................................................8

Suggestions for improvement......................................................................................................9

CONCLUSION................................................................................................................................9

REFRENCES.................................................................................................................................10

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Explanation of management and financial accounting................................................................1

Difference between management and financial accounting with respective users......................1

QUESTION2....................................................................................................................................2

Cost benefit analysis....................................................................................................................2

Payback period.............................................................................................................................3

Accounting rate of return.............................................................................................................4

Net present value and internal rate of return................................................................................5

Analysis and conclusion..............................................................................................................6

QUESTION 3...................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Comparison of ratios....................................................................................................................8

Suggestions for improvement......................................................................................................9

CONCLUSION................................................................................................................................9

REFRENCES.................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial resources can be defined as the funds which are required by all the

organisations to execute all the operational activities in systematic manner. If an enterprise is not

having sufficient finance to conduct business processes then it will be difficult for it to reach

predetermined organisation (Anselmi, Lagarde and Hanson, 2014). This report is based upon the

entity Swipe Wire which is a small production company and set up by James. Currently the

organisation is planning for expansion and incorporation of the business. This assignment covers

various topics such as management and financial accounting, their functions, respective user,

differences, calculation of payback period, NPV, IRR, ARR etc. Along with this, in order to

determine performance of the business different ratios are also calculated.

QUESTION 1

Explanation of management and financial accounting

Management accounting: It can be defined as the process of monitoring, analysing,

evaluating and controlling organisational processes so that strategic decisions could be

formulated according to actual situation of business. Main purpose of it is to determine that the

operational activities which were performed by company in a specific time period are resulting

positively or negatively. In Swipe Wire it is conducted every year to determine that the plan

which were formulated are being executed properly or not. It's primary function is to assist

managing officials in planning, controlling, organising and decision-making.

Financial accounting: The process which is followed by business entities to formulate

final accounts such as income statement, balance sheet and cash flow statement is known as

financial accounting. It helps to analyse that organisation is able to meet the finance related

objectives or not. Financial analyst of Swipe Wire focuses on it to evaluate financial status of the

company and formulate strategic decisions for future (Guerra, Magni and Stefanini, 2014). It's

core function is recording, summarising, classifying, communicating and interpreting financial

data.

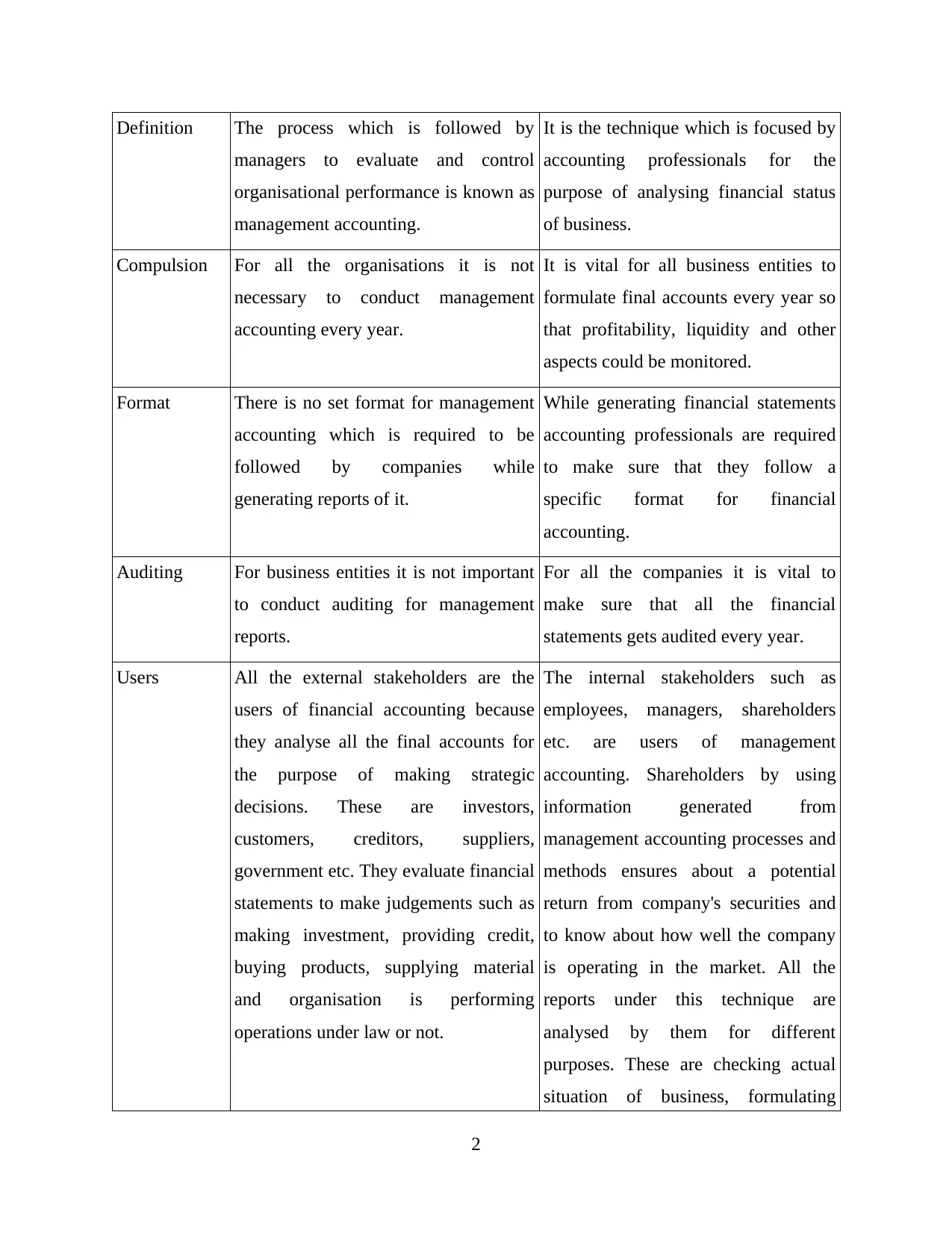

Difference between management and financial accounting with respective users

Difference between financial and management accounting:

Basis Management accounting Financial accounting

1

Financial resources can be defined as the funds which are required by all the

organisations to execute all the operational activities in systematic manner. If an enterprise is not

having sufficient finance to conduct business processes then it will be difficult for it to reach

predetermined organisation (Anselmi, Lagarde and Hanson, 2014). This report is based upon the

entity Swipe Wire which is a small production company and set up by James. Currently the

organisation is planning for expansion and incorporation of the business. This assignment covers

various topics such as management and financial accounting, their functions, respective user,

differences, calculation of payback period, NPV, IRR, ARR etc. Along with this, in order to

determine performance of the business different ratios are also calculated.

QUESTION 1

Explanation of management and financial accounting

Management accounting: It can be defined as the process of monitoring, analysing,

evaluating and controlling organisational processes so that strategic decisions could be

formulated according to actual situation of business. Main purpose of it is to determine that the

operational activities which were performed by company in a specific time period are resulting

positively or negatively. In Swipe Wire it is conducted every year to determine that the plan

which were formulated are being executed properly or not. It's primary function is to assist

managing officials in planning, controlling, organising and decision-making.

Financial accounting: The process which is followed by business entities to formulate

final accounts such as income statement, balance sheet and cash flow statement is known as

financial accounting. It helps to analyse that organisation is able to meet the finance related

objectives or not. Financial analyst of Swipe Wire focuses on it to evaluate financial status of the

company and formulate strategic decisions for future (Guerra, Magni and Stefanini, 2014). It's

core function is recording, summarising, classifying, communicating and interpreting financial

data.

Difference between management and financial accounting with respective users

Difference between financial and management accounting:

Basis Management accounting Financial accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Definition The process which is followed by

managers to evaluate and control

organisational performance is known as

management accounting.

It is the technique which is focused by

accounting professionals for the

purpose of analysing financial status

of business.

Compulsion For all the organisations it is not

necessary to conduct management

accounting every year.

It is vital for all business entities to

formulate final accounts every year so

that profitability, liquidity and other

aspects could be monitored.

Format There is no set format for management

accounting which is required to be

followed by companies while

generating reports of it.

While generating financial statements

accounting professionals are required

to make sure that they follow a

specific format for financial

accounting.

Auditing For business entities it is not important

to conduct auditing for management

reports.

For all the companies it is vital to

make sure that all the financial

statements gets audited every year.

Users All the external stakeholders are the

users of financial accounting because

they analyse all the final accounts for

the purpose of making strategic

decisions. These are investors,

customers, creditors, suppliers,

government etc. They evaluate financial

statements to make judgements such as

making investment, providing credit,

buying products, supplying material

and organisation is performing

operations under law or not.

The internal stakeholders such as

employees, managers, shareholders

etc. are users of management

accounting. Shareholders by using

information generated from

management accounting processes and

methods ensures about a potential

return from company's securities and

to know about how well the company

is operating in the market. All the

reports under this technique are

analysed by them for different

purposes. These are checking actual

situation of business, formulating

2

managers to evaluate and control

organisational performance is known as

management accounting.

It is the technique which is focused by

accounting professionals for the

purpose of analysing financial status

of business.

Compulsion For all the organisations it is not

necessary to conduct management

accounting every year.

It is vital for all business entities to

formulate final accounts every year so

that profitability, liquidity and other

aspects could be monitored.

Format There is no set format for management

accounting which is required to be

followed by companies while

generating reports of it.

While generating financial statements

accounting professionals are required

to make sure that they follow a

specific format for financial

accounting.

Auditing For business entities it is not important

to conduct auditing for management

reports.

For all the companies it is vital to

make sure that all the financial

statements gets audited every year.

Users All the external stakeholders are the

users of financial accounting because

they analyse all the final accounts for

the purpose of making strategic

decisions. These are investors,

customers, creditors, suppliers,

government etc. They evaluate financial

statements to make judgements such as

making investment, providing credit,

buying products, supplying material

and organisation is performing

operations under law or not.

The internal stakeholders such as

employees, managers, shareholders

etc. are users of management

accounting. Shareholders by using

information generated from

management accounting processes and

methods ensures about a potential

return from company's securities and

to know about how well the company

is operating in the market. All the

reports under this technique are

analysed by them for different

purposes. These are checking actual

situation of business, formulating

2

strategic decisions for future and

making sure that they are a part of a

profitable company (Hasan and Habib,

2017)

QUESTION 2

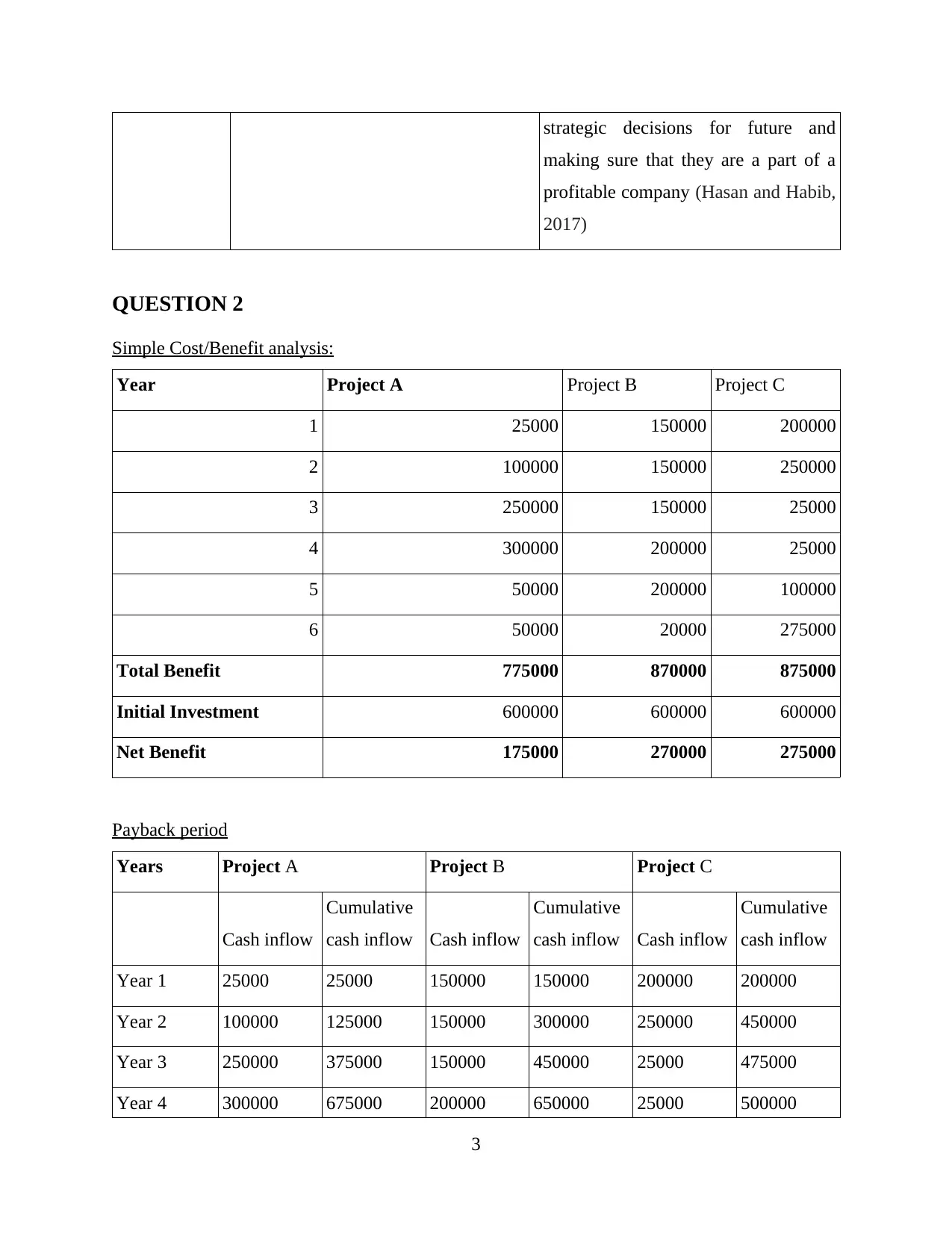

Simple Cost/Benefit analysis:

Year Project A Project B Project C

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 20000 275000

Total Benefit 775000 870000 875000

Initial Investment 600000 600000 600000

Net Benefit 175000 270000 275000

Payback period

Years Project A Project B Project C

Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow

Year 1 25000 25000 150000 150000 200000 200000

Year 2 100000 125000 150000 300000 250000 450000

Year 3 250000 375000 150000 450000 25000 475000

Year 4 300000 675000 200000 650000 25000 500000

3

making sure that they are a part of a

profitable company (Hasan and Habib,

2017)

QUESTION 2

Simple Cost/Benefit analysis:

Year Project A Project B Project C

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 20000 275000

Total Benefit 775000 870000 875000

Initial Investment 600000 600000 600000

Net Benefit 175000 270000 275000

Payback period

Years Project A Project B Project C

Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow

Year 1 25000 25000 150000 150000 200000 200000

Year 2 100000 125000 150000 300000 250000 450000

Year 3 250000 375000 150000 450000 25000 475000

Year 4 300000 675000 200000 650000 25000 500000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

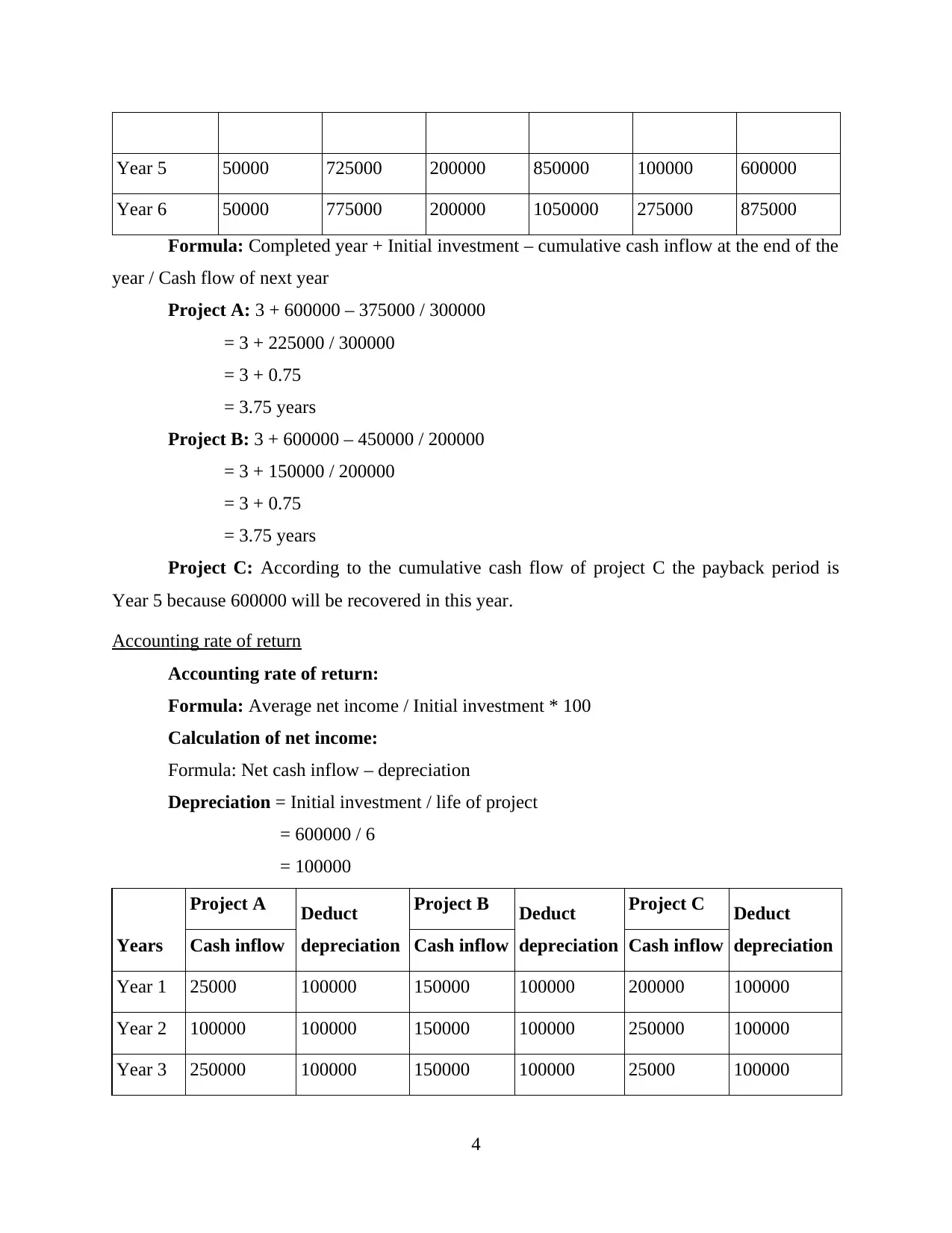

Year 5 50000 725000 200000 850000 100000 600000

Year 6 50000 775000 200000 1050000 275000 875000

Formula: Completed year + Initial investment – cumulative cash inflow at the end of the

year / Cash flow of next year

Project A: 3 + 600000 – 375000 / 300000

= 3 + 225000 / 300000

= 3 + 0.75

= 3.75 years

Project B: 3 + 600000 – 450000 / 200000

= 3 + 150000 / 200000

= 3 + 0.75

= 3.75 years

Project C: According to the cumulative cash flow of project C the payback period is

Year 5 because 600000 will be recovered in this year.

Accounting rate of return

Accounting rate of return:

Formula: Average net income / Initial investment * 100

Calculation of net income:

Formula: Net cash inflow – depreciation

Depreciation = Initial investment / life of project

= 600000 / 6

= 100000

Years

Project A Deduct

depreciation

Project B Deduct

depreciation

Project C Deduct

depreciationCash inflow Cash inflow Cash inflow

Year 1 25000 100000 150000 100000 200000 100000

Year 2 100000 100000 150000 100000 250000 100000

Year 3 250000 100000 150000 100000 25000 100000

4

Year 6 50000 775000 200000 1050000 275000 875000

Formula: Completed year + Initial investment – cumulative cash inflow at the end of the

year / Cash flow of next year

Project A: 3 + 600000 – 375000 / 300000

= 3 + 225000 / 300000

= 3 + 0.75

= 3.75 years

Project B: 3 + 600000 – 450000 / 200000

= 3 + 150000 / 200000

= 3 + 0.75

= 3.75 years

Project C: According to the cumulative cash flow of project C the payback period is

Year 5 because 600000 will be recovered in this year.

Accounting rate of return

Accounting rate of return:

Formula: Average net income / Initial investment * 100

Calculation of net income:

Formula: Net cash inflow – depreciation

Depreciation = Initial investment / life of project

= 600000 / 6

= 100000

Years

Project A Deduct

depreciation

Project B Deduct

depreciation

Project C Deduct

depreciationCash inflow Cash inflow Cash inflow

Year 1 25000 100000 150000 100000 200000 100000

Year 2 100000 100000 150000 100000 250000 100000

Year 3 250000 100000 150000 100000 25000 100000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

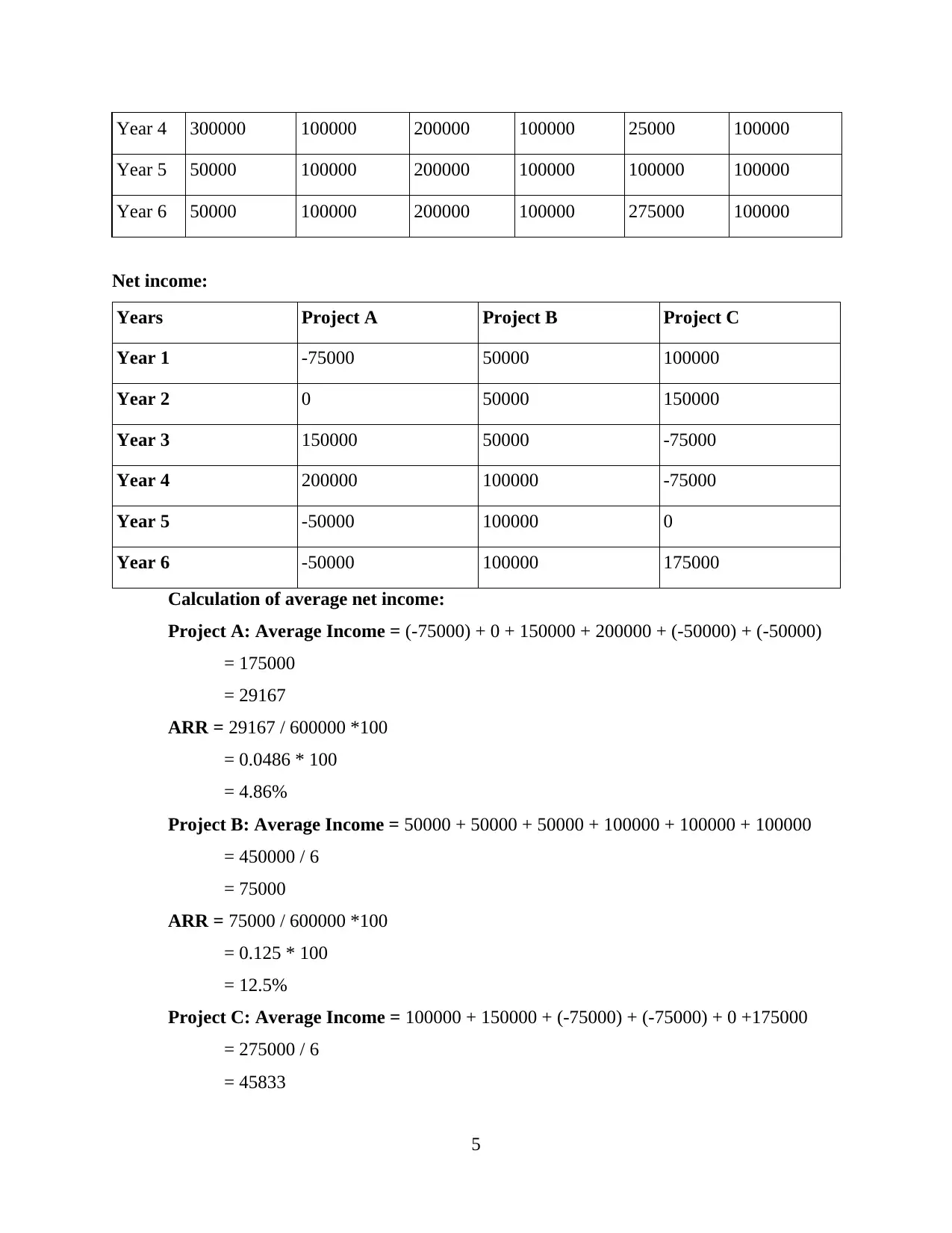

Year 4 300000 100000 200000 100000 25000 100000

Year 5 50000 100000 200000 100000 100000 100000

Year 6 50000 100000 200000 100000 275000 100000

Net income:

Years Project A Project B Project C

Year 1 -75000 50000 100000

Year 2 0 50000 150000

Year 3 150000 50000 -75000

Year 4 200000 100000 -75000

Year 5 -50000 100000 0

Year 6 -50000 100000 175000

Calculation of average net income:

Project A: Average Income = (-75000) + 0 + 150000 + 200000 + (-50000) + (-50000)

= 175000

= 29167

ARR = 29167 / 600000 *100

= 0.0486 * 100

= 4.86%

Project B: Average Income = 50000 + 50000 + 50000 + 100000 + 100000 + 100000

= 450000 / 6

= 75000

ARR = 75000 / 600000 *100

= 0.125 * 100

= 12.5%

Project C: Average Income = 100000 + 150000 + (-75000) + (-75000) + 0 +175000

= 275000 / 6

= 45833

5

Year 5 50000 100000 200000 100000 100000 100000

Year 6 50000 100000 200000 100000 275000 100000

Net income:

Years Project A Project B Project C

Year 1 -75000 50000 100000

Year 2 0 50000 150000

Year 3 150000 50000 -75000

Year 4 200000 100000 -75000

Year 5 -50000 100000 0

Year 6 -50000 100000 175000

Calculation of average net income:

Project A: Average Income = (-75000) + 0 + 150000 + 200000 + (-50000) + (-50000)

= 175000

= 29167

ARR = 29167 / 600000 *100

= 0.0486 * 100

= 4.86%

Project B: Average Income = 50000 + 50000 + 50000 + 100000 + 100000 + 100000

= 450000 / 6

= 75000

ARR = 75000 / 600000 *100

= 0.125 * 100

= 12.5%

Project C: Average Income = 100000 + 150000 + (-75000) + (-75000) + 0 +175000

= 275000 / 6

= 45833

5

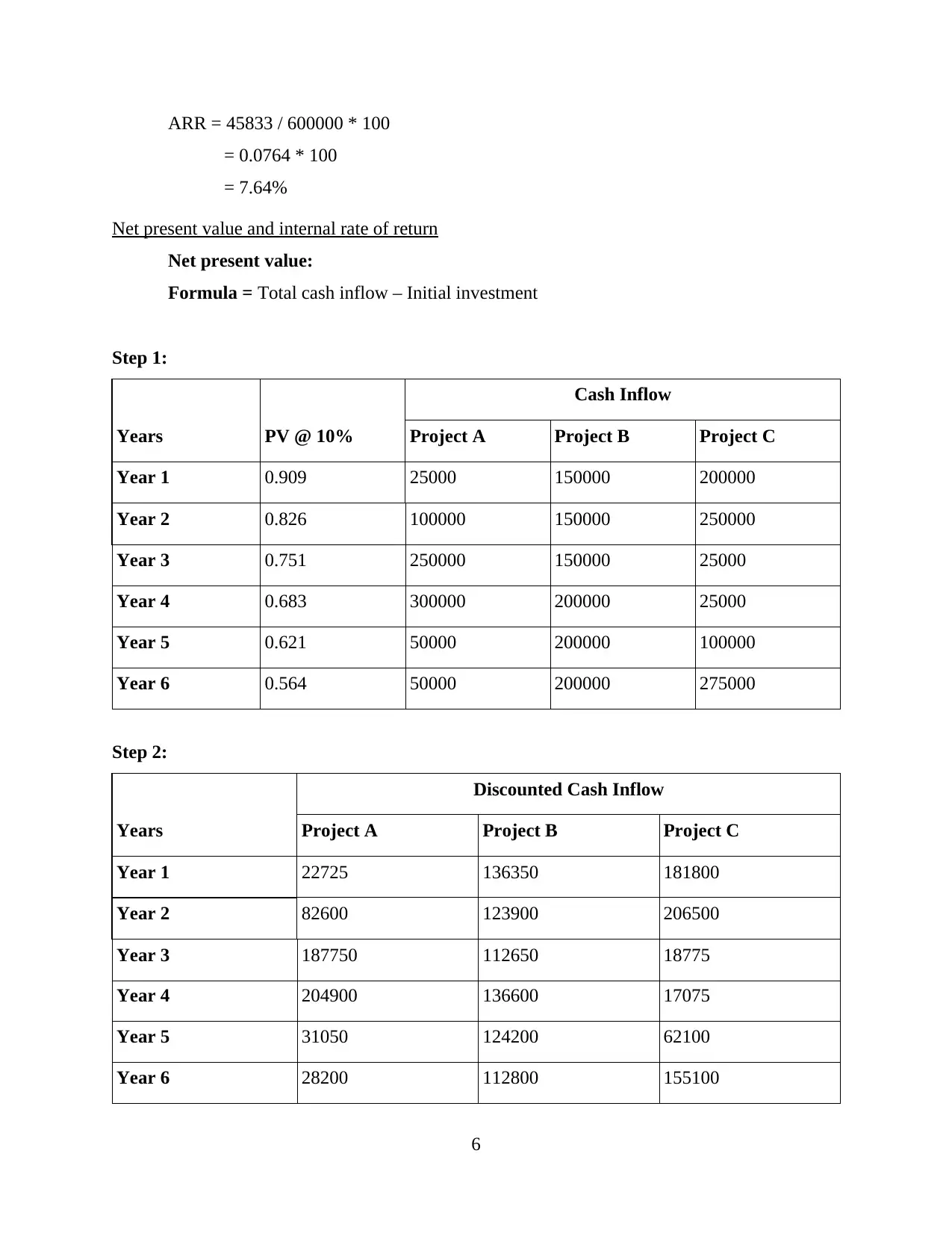

ARR = 45833 / 600000 * 100

= 0.0764 * 100

= 7.64%

Net present value and internal rate of return

Net present value:

Formula = Total cash inflow – Initial investment

Step 1:

Years PV @ 10%

Cash Inflow

Project A Project B Project C

Year 1 0.909 25000 150000 200000

Year 2 0.826 100000 150000 250000

Year 3 0.751 250000 150000 25000

Year 4 0.683 300000 200000 25000

Year 5 0.621 50000 200000 100000

Year 6 0.564 50000 200000 275000

Step 2:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

6

= 0.0764 * 100

= 7.64%

Net present value and internal rate of return

Net present value:

Formula = Total cash inflow – Initial investment

Step 1:

Years PV @ 10%

Cash Inflow

Project A Project B Project C

Year 1 0.909 25000 150000 200000

Year 2 0.826 100000 150000 250000

Year 3 0.751 250000 150000 25000

Year 4 0.683 300000 200000 25000

Year 5 0.621 50000 200000 100000

Year 6 0.564 50000 200000 275000

Step 2:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

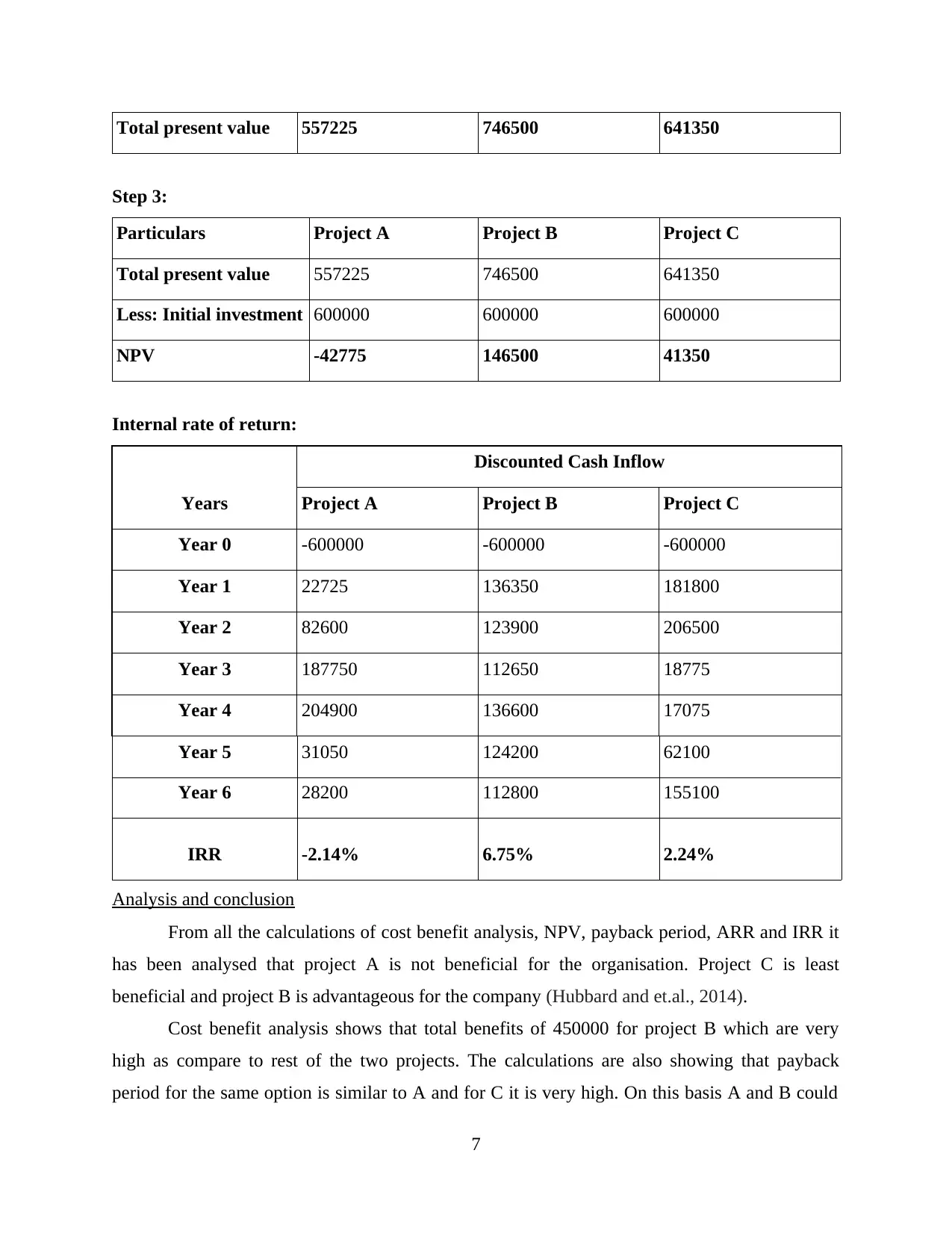

Total present value 557225 746500 641350

Step 3:

Particulars Project A Project B Project C

Total present value 557225 746500 641350

Less: Initial investment 600000 600000 600000

NPV -42775 146500 41350

Internal rate of return:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 0 -600000 -600000 -600000

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

IRR -2.14% 6.75% 2.24%

Analysis and conclusion

From all the calculations of cost benefit analysis, NPV, payback period, ARR and IRR it

has been analysed that project A is not beneficial for the organisation. Project C is least

beneficial and project B is advantageous for the company (Hubbard and et.al., 2014).

Cost benefit analysis shows that total benefits of 450000 for project B which are very

high as compare to rest of the two projects. The calculations are also showing that payback

period for the same option is similar to A and for C it is very high. On this basis A and B could

7

Step 3:

Particulars Project A Project B Project C

Total present value 557225 746500 641350

Less: Initial investment 600000 600000 600000

NPV -42775 146500 41350

Internal rate of return:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 0 -600000 -600000 -600000

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

IRR -2.14% 6.75% 2.24%

Analysis and conclusion

From all the calculations of cost benefit analysis, NPV, payback period, ARR and IRR it

has been analysed that project A is not beneficial for the organisation. Project C is least

beneficial and project B is advantageous for the company (Hubbard and et.al., 2014).

Cost benefit analysis shows that total benefits of 450000 for project B which are very

high as compare to rest of the two projects. The calculations are also showing that payback

period for the same option is similar to A and for C it is very high. On this basis A and B could

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be selected for recovering the investment in a short period. The calculations of accounting rate of

return are showing that the ARR for A, B and C are 4.86%, 12.5% and 7.64% respectively. From

all of them the rate for project B is very high and if investment is made in this project then it will

provide higher returns to the business.

Net present value shows current market value of a project which helps business entities to

select best suitable option to make investment. From the calculations of it, it has been assessed

that project B is having highest NPV as compare to other projects. By making investment in this

project the organisation will be able to attain success. Internal rate of returns for all the projects

are -2.14%, 6.75% and 2.24%. The highest IRR shows higher returns from project in which

investment is made (FKarltorp, 2016).

From the above analysis it has been concluded that by from all the tree project the most

beneficial option for Swipe Wire is project B because in all the calculations it has been identified

that it is the best suitable alternative for the business. On the basis of the analysis it has been

advised to the management that project B should be adopted by the company.

QUESTION 3

Calculation of ratios

Ratio Formula Particulars 2017 2018

Gross profit

margin

Gross profit /

net sales *100

Gross profit 250000 280000

Net sales 650000 700000

Gross profit margin ratio 38.46 40

Net profit

margin ratio

Net profit / net

sales *100

Net profit 30000 45000

Net sales 650000 700000

Net profit ratio 4.62 6.43

Mark up

ratio

(Sales – Cost of

good sold)/ cost

Sales – Cost of good sold 250000 280000

Cost of goods sold 400000 420000

8

return are showing that the ARR for A, B and C are 4.86%, 12.5% and 7.64% respectively. From

all of them the rate for project B is very high and if investment is made in this project then it will

provide higher returns to the business.

Net present value shows current market value of a project which helps business entities to

select best suitable option to make investment. From the calculations of it, it has been assessed

that project B is having highest NPV as compare to other projects. By making investment in this

project the organisation will be able to attain success. Internal rate of returns for all the projects

are -2.14%, 6.75% and 2.24%. The highest IRR shows higher returns from project in which

investment is made (FKarltorp, 2016).

From the above analysis it has been concluded that by from all the tree project the most

beneficial option for Swipe Wire is project B because in all the calculations it has been identified

that it is the best suitable alternative for the business. On the basis of the analysis it has been

advised to the management that project B should be adopted by the company.

QUESTION 3

Calculation of ratios

Ratio Formula Particulars 2017 2018

Gross profit

margin

Gross profit /

net sales *100

Gross profit 250000 280000

Net sales 650000 700000

Gross profit margin ratio 38.46 40

Net profit

margin ratio

Net profit / net

sales *100

Net profit 30000 45000

Net sales 650000 700000

Net profit ratio 4.62 6.43

Mark up

ratio

(Sales – Cost of

good sold)/ cost

Sales – Cost of good sold 250000 280000

Cost of goods sold 400000 420000

8

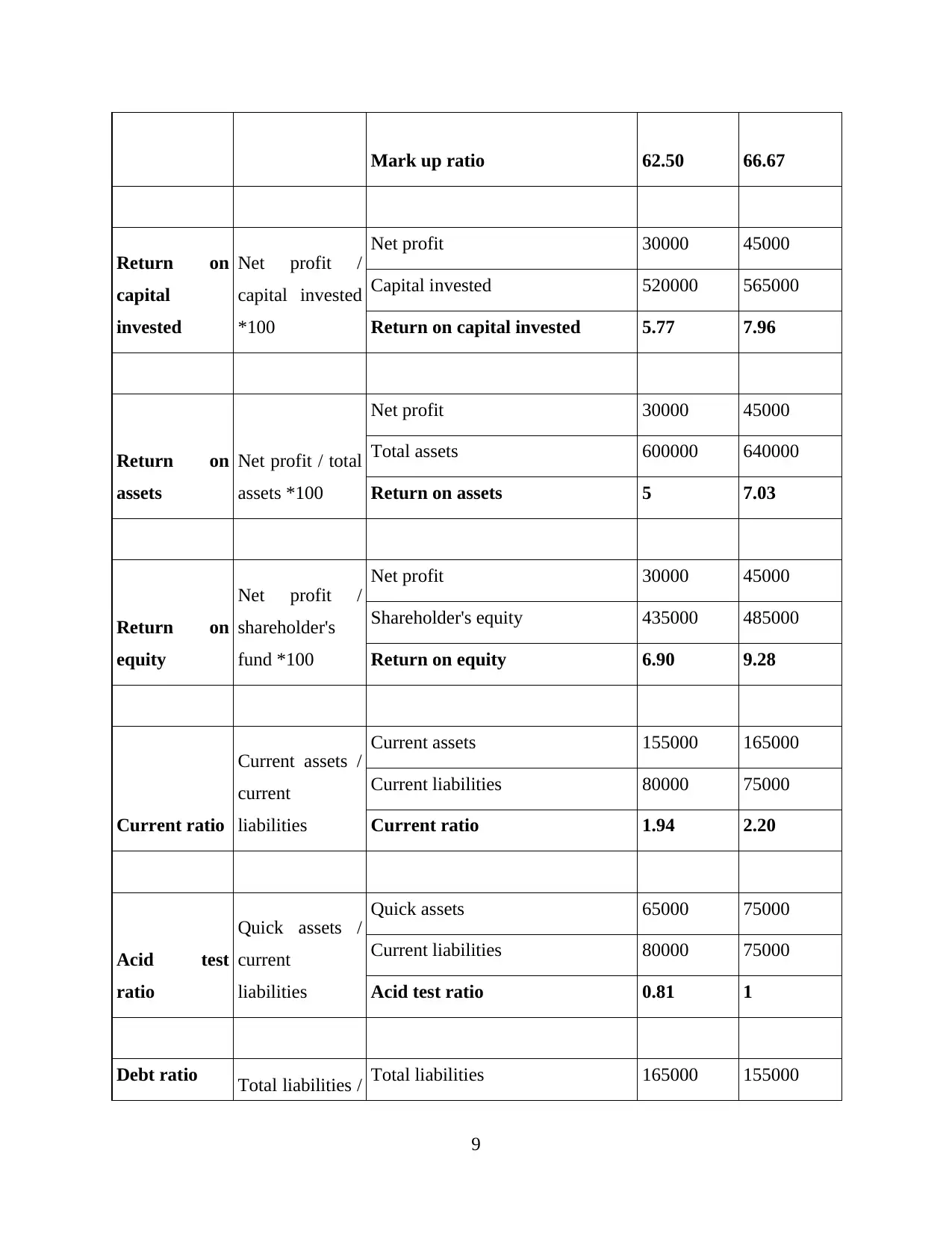

Mark up ratio 62.50 66.67

Return on

capital

invested

Net profit /

capital invested

*100

Net profit 30000 45000

Capital invested 520000 565000

Return on capital invested 5.77 7.96

Return on

assets

Net profit / total

assets *100

Net profit 30000 45000

Total assets 600000 640000

Return on assets 5 7.03

Return on

equity

Net profit /

shareholder's

fund *100

Net profit 30000 45000

Shareholder's equity 435000 485000

Return on equity 6.90 9.28

Current ratio

Current assets /

current

liabilities

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

Acid test

ratio

Quick assets /

current

liabilities

Quick assets 65000 75000

Current liabilities 80000 75000

Acid test ratio 0.81 1

Debt ratio Total liabilities / Total liabilities 165000 155000

9

Return on

capital

invested

Net profit /

capital invested

*100

Net profit 30000 45000

Capital invested 520000 565000

Return on capital invested 5.77 7.96

Return on

assets

Net profit / total

assets *100

Net profit 30000 45000

Total assets 600000 640000

Return on assets 5 7.03

Return on

equity

Net profit /

shareholder's

fund *100

Net profit 30000 45000

Shareholder's equity 435000 485000

Return on equity 6.90 9.28

Current ratio

Current assets /

current

liabilities

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

Acid test

ratio

Quick assets /

current

liabilities

Quick assets 65000 75000

Current liabilities 80000 75000

Acid test ratio 0.81 1

Debt ratio Total liabilities / Total liabilities 165000 155000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.