Management Accounting Report: Analysis of TECH (UK) LTD's Financials

VerifiedAdded on 2020/11/23

|19

|3932

|344

Report

AI Summary

This report offers a comprehensive analysis of management accounting, focusing on its application within TECH (UK) LTD. It begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its essential requirements, including financial analysis, investment decisions, and resource allocation. The report then explores various techniques such as activity-based costing, relevant costing analysis, and different costing systems (actual, normal, and standard). It also covers inventory management and job costing systems. Furthermore, the report delves into presenting financial information through different management accounting reports like budgeting reports, job cost reports, and performance reports, emphasizing their importance in evaluating the company's financial position and decision-making processes. The report also discusses the benefits of management systems for TECH (UK) LTD and how these systems integrate within the company's processes.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................. 2

a). Management accounting and the essential requirements of management accounting system

............................................................................................................................................... 3

B). Presenting financial information:...................................................................................... 7

M1 Benefits of management systems under the TECH (UK) LTD..........................................9

TASK 2.................................................................................................................................. 9

Calculation of net profit under marginal and absorption costing:-..........................................9

M2. Application of techniques:............................................................................................. 13

D2. Data interpretation:........................................................................................................ 13

TASK 3................................................................................................................................ 13

A). Budget and its advantage and disadvantage....................................................................13

b).Different types of common costing systems which can be used for budgetary control:.....14

c) Importance of budget as a method for planning and controlling purpose:.........................15

M3. Use of various planning tools for making budget:.........................................................15

M4 How financial tools are used for evaluating the financial problems:...............................15

TASK 4................................................................................................................................ 16

D3 How planning tools for accounting respond for solving financial problems:...................16

CONCLUSION.................................................................................................................... 16

REFERENCES..................................................................................................................... 18

·

INTRODUCTION.................................................................................................................. 2

a). Management accounting and the essential requirements of management accounting system

............................................................................................................................................... 3

B). Presenting financial information:...................................................................................... 7

M1 Benefits of management systems under the TECH (UK) LTD..........................................9

TASK 2.................................................................................................................................. 9

Calculation of net profit under marginal and absorption costing:-..........................................9

M2. Application of techniques:............................................................................................. 13

D2. Data interpretation:........................................................................................................ 13

TASK 3................................................................................................................................ 13

A). Budget and its advantage and disadvantage....................................................................13

b).Different types of common costing systems which can be used for budgetary control:.....14

c) Importance of budget as a method for planning and controlling purpose:.........................15

M3. Use of various planning tools for making budget:.........................................................15

M4 How financial tools are used for evaluating the financial problems:...............................15

TASK 4................................................................................................................................ 16

D3 How planning tools for accounting respond for solving financial problems:...................16

CONCLUSION.................................................................................................................... 16

REFERENCES..................................................................................................................... 18

·

·INTRODUCTION

According to this report a system of Accounting for management, which provide

necessary and important information to the management for discharge of its function. This

function includes planning, directing, controlling and decision making it assist management

to carry out these function more effectively and efficiently in a systematic manner for

company in brief. Under this report, TECH (UK) Ltd. Produce a special Headphone and it

consider that, this accounting for management introduce betterment in communication

between various department about level of acknowledgement about which it is available to

all departments for the improvement in discussion (Wickramasinghe and Alawattage, 2012).

in this accounting report company will create the management accounting reports for making

decision in a manner that is appropriate for company. There are various type of and

techniques which are use to evaluate overall performance of company to achieve business

goals in efficient and effective way.

TASK 1

l壱a). Management accounting and the essential requirements of management accounting

system

This is a process of determination, intimation and demonstrate of information about

accounting that is incurred with the method of financial accounting method and cost

accounting method (Lavia López and Hiebl, 2014). Management accounting is use in

regulating policies of company and making decision and also provides appropriate discussion

about operation of company to the manager and accountant of organization.

Useful and essential factor of management accounting system are:

Financial analysis and planning

Investment decision

Allocation and management of financial resources

Protecting management

Financial and structure decision for raising goals in favourable terms

1. Differences between management accounting and financial accounting:-

According to this report a system of Accounting for management, which provide

necessary and important information to the management for discharge of its function. This

function includes planning, directing, controlling and decision making it assist management

to carry out these function more effectively and efficiently in a systematic manner for

company in brief. Under this report, TECH (UK) Ltd. Produce a special Headphone and it

consider that, this accounting for management introduce betterment in communication

between various department about level of acknowledgement about which it is available to

all departments for the improvement in discussion (Wickramasinghe and Alawattage, 2012).

in this accounting report company will create the management accounting reports for making

decision in a manner that is appropriate for company. There are various type of and

techniques which are use to evaluate overall performance of company to achieve business

goals in efficient and effective way.

TASK 1

l壱a). Management accounting and the essential requirements of management accounting

system

This is a process of determination, intimation and demonstrate of information about

accounting that is incurred with the method of financial accounting method and cost

accounting method (Lavia López and Hiebl, 2014). Management accounting is use in

regulating policies of company and making decision and also provides appropriate discussion

about operation of company to the manager and accountant of organization.

Useful and essential factor of management accounting system are:

Financial analysis and planning

Investment decision

Allocation and management of financial resources

Protecting management

Financial and structure decision for raising goals in favourable terms

1. Differences between management accounting and financial accounting:-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

No.BaseManagement accountingFinancial accountingobjectiveManagement accounting is

a system of giving proper knowledge about the execution of its function for managementIt is

recording of transaction and event or evaluate business results and financial position in

appropriate manner.Set of rules and regulationThere is no any Application of accounting

principles and convention are imply in this accounting system (Christ, 2014). This system is

concerned with a various type of rules and regulations or prescribed manner as applicable to

the organization PeriodReports and financial statement for management accounting can be

prepared in intervals or periodically throughout the yearIn financial accounting accounts are

made at end of financial yearResources Management accounting use financing data as well

as non-financial data both for the purpose of overall performance of companyFinancial

accounting use the financial data for preparation of final accounts.Criteria In this

accounting system criteria of allocation is separate for every department Criteria for

allocation is only the organization as complete for accounting.

2. Importance of management accounting information as a decision- making technique

for the department managers which are given below:-

Activity based costing:- (ABC) is an accounting function that identifies and assimilate

costs to overhead activity and assimilate those costs to product. An activity based costing

system recognises the relation among costs, overhead activity and manufacturing produce

with this relationship, it assigns indirect cost to product less arbitrarily than traditional

methods (Moser, 2012). (ABC) helps to reduce overhead cost which is targeted by the

company and also this costing system is used in targeting costing, process costing, product

line profitability analysis customer, profitability analysis in the company. Activity based

costing enhance the costing process in three ways. First, it expands the number of cost pools

that can be used to be assemble overhead cost. It also create new bases for assigning

overhead cost to such that cost allocated based on the activities that generate cost instead of

on volumes measure, such as machine hours or direct labour cost .

Relevant costing analysis:- Relevant costing is analysis of managerial accounting term that

refer avoidable costs that are incurred when making business decision. It is useful in short

term cause any decision should be approached by using relevant costing principles. Relevant

cost for company means that cost or charges which do not reflect additional cash spending

(such as depreciation and notional cost) should be ignore for the purpose of decision making.

Relevant cost are also incremental cost for the company which increase in cost and revenues.

a system of giving proper knowledge about the execution of its function for managementIt is

recording of transaction and event or evaluate business results and financial position in

appropriate manner.Set of rules and regulationThere is no any Application of accounting

principles and convention are imply in this accounting system (Christ, 2014). This system is

concerned with a various type of rules and regulations or prescribed manner as applicable to

the organization PeriodReports and financial statement for management accounting can be

prepared in intervals or periodically throughout the yearIn financial accounting accounts are

made at end of financial yearResources Management accounting use financing data as well

as non-financial data both for the purpose of overall performance of companyFinancial

accounting use the financial data for preparation of final accounts.Criteria In this

accounting system criteria of allocation is separate for every department Criteria for

allocation is only the organization as complete for accounting.

2. Importance of management accounting information as a decision- making technique

for the department managers which are given below:-

Activity based costing:- (ABC) is an accounting function that identifies and assimilate

costs to overhead activity and assimilate those costs to product. An activity based costing

system recognises the relation among costs, overhead activity and manufacturing produce

with this relationship, it assigns indirect cost to product less arbitrarily than traditional

methods (Moser, 2012). (ABC) helps to reduce overhead cost which is targeted by the

company and also this costing system is used in targeting costing, process costing, product

line profitability analysis customer, profitability analysis in the company. Activity based

costing enhance the costing process in three ways. First, it expands the number of cost pools

that can be used to be assemble overhead cost. It also create new bases for assigning

overhead cost to such that cost allocated based on the activities that generate cost instead of

on volumes measure, such as machine hours or direct labour cost .

Relevant costing analysis:- Relevant costing is analysis of managerial accounting term that

refer avoidable costs that are incurred when making business decision. It is useful in short

term cause any decision should be approached by using relevant costing principles. Relevant

cost for company means that cost or charges which do not reflect additional cash spending

(such as depreciation and notional cost) should be ignore for the purpose of decision making.

Relevant cost are also incremental cost for the company which increase in cost and revenues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The exercise of useful and important data:- Management accounting provide data that is

useful in preparation of financial reports and final accounts for company. Information and the

data provided by management accounting is used to formulate policies or strategies for the

development of company. The manager use data and exercise these data for the future

planning of the business sand future forecasting on the important data and also makes

strategies for the improvement of productivity of business in future or help to achieve pre set

data in pre-determined period for the company.

Buying decision:- Buying decision is the decision making process used by company

regarding market transaction before, during and after the purchasing. It can be seen as

particular form of cost-benefits analysis in the presence of multiple alternative (Hilton and

Platt, 2013). It is important action for management to select the best one between external

supplier or market. The manager doing this analysis is able to ascertain which option is

profitable for company.

3. Cost accounting system (actual, normal and standard costing):- This system is

framework used by the firms for the estimate of cost of the product for profit analysis,

inventory valuation or controlling cost. A company should know which product are profitable

and which one are not company as per the requirement of, and this can be ascertained only

when there is correct estimation of cost..

Difference between the NORMAL COSTING, ACTUAL COSTING AND STANDARD

COSTING:-

1NO.NORMAL COSTINGACTUAL COSTINGSTANDARD COSTINGActual direct

cost which are directly assigned with particular job as it is incurredActual direct costs are

assigned to job as incurredStandard direct costs are assigned to job as incurred.

1

1Manufacturing overhead is apportioned by using predetermined rate of overhead (Becker,

Ulrich and Staffel, 2011).Actual manufacture overhead apportioned only when actual costs

are knownManufacturing overhead rate is apportioned by using standard overhead rate.In this

costing actual cost are used to determine normal costingIn this costing actual cost are usedIn

this costing standard cost of actual cost is usedThis costing is accurate and fair method when

budgeted numbers for standard overhead is betterIn this method the cost control and

measurement of performance is not in the hand of companyThis method is useful for cost

useful in preparation of financial reports and final accounts for company. Information and the

data provided by management accounting is used to formulate policies or strategies for the

development of company. The manager use data and exercise these data for the future

planning of the business sand future forecasting on the important data and also makes

strategies for the improvement of productivity of business in future or help to achieve pre set

data in pre-determined period for the company.

Buying decision:- Buying decision is the decision making process used by company

regarding market transaction before, during and after the purchasing. It can be seen as

particular form of cost-benefits analysis in the presence of multiple alternative (Hilton and

Platt, 2013). It is important action for management to select the best one between external

supplier or market. The manager doing this analysis is able to ascertain which option is

profitable for company.

3. Cost accounting system (actual, normal and standard costing):- This system is

framework used by the firms for the estimate of cost of the product for profit analysis,

inventory valuation or controlling cost. A company should know which product are profitable

and which one are not company as per the requirement of, and this can be ascertained only

when there is correct estimation of cost..

Difference between the NORMAL COSTING, ACTUAL COSTING AND STANDARD

COSTING:-

1NO.NORMAL COSTINGACTUAL COSTINGSTANDARD COSTINGActual direct

cost which are directly assigned with particular job as it is incurredActual direct costs are

assigned to job as incurredStandard direct costs are assigned to job as incurred.

1

1Manufacturing overhead is apportioned by using predetermined rate of overhead (Becker,

Ulrich and Staffel, 2011).Actual manufacture overhead apportioned only when actual costs

are knownManufacturing overhead rate is apportioned by using standard overhead rate.In this

costing actual cost are used to determine normal costingIn this costing actual cost are usedIn

this costing standard cost of actual cost is usedThis costing is accurate and fair method when

budgeted numbers for standard overhead is betterIn this method the cost control and

measurement of performance is not in the hand of companyThis method is useful for cost

controlling and the performance of standard. 4. Inventory management system:- inventory

management system basically a system of managing stock of company by using corrective

method of managing inventory. Inventory management has various option to balance

inventory of the organization. Inventory management system used by both who sell product

and produce the product. This system helps to prevent bugs in flow of inventoey.

The two important essential are:

· Planning and replenishing strategies (Jalaludin, sulaiman and nazil, 2011)

·Physically and monetarily both type of management of inventory.

5. Job costing system:-

Job costing system involves the process of collecting cost for each job specifically

related to that job (Eierle and Schultze, 2013). Each job is separate and independent of each

job. The information provided by job costing is useful in determination of accurate

estimation of company.

Job costing process inclusive of ;-

·Information about job order

·Pre-determined price of each job unit

·Period of completion of each job

·Job order

·Cost recognising

·Determination of cost for each job

·Production order

·B). Presenting financial information:

1. Following are the different types of management accounting reports:-

(MAS) are tools for understanding the TECH(UK) LTD. What is happening in the company

in quanty. in accordance to the standard accounting reports that the company must complish

for tax purpose, managerial reporting includes all type of collection of data that can give

useful information about operations. The various type of managerial accounting reports help

management system basically a system of managing stock of company by using corrective

method of managing inventory. Inventory management has various option to balance

inventory of the organization. Inventory management system used by both who sell product

and produce the product. This system helps to prevent bugs in flow of inventoey.

The two important essential are:

· Planning and replenishing strategies (Jalaludin, sulaiman and nazil, 2011)

·Physically and monetarily both type of management of inventory.

5. Job costing system:-

Job costing system involves the process of collecting cost for each job specifically

related to that job (Eierle and Schultze, 2013). Each job is separate and independent of each

job. The information provided by job costing is useful in determination of accurate

estimation of company.

Job costing process inclusive of ;-

·Information about job order

·Pre-determined price of each job unit

·Period of completion of each job

·Job order

·Cost recognising

·Determination of cost for each job

·Production order

·B). Presenting financial information:

1. Following are the different types of management accounting reports:-

(MAS) are tools for understanding the TECH(UK) LTD. What is happening in the company

in quanty. in accordance to the standard accounting reports that the company must complish

for tax purpose, managerial reporting includes all type of collection of data that can give

useful information about operations. The various type of managerial accounting reports help

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the management in preparation of effective management reports. The various type of reports

prepared by the management and advantage are given below:-

·Budgeting reports:- these report are prepared for planning to measure

performance of company while making analysis about the determination of

performance of company and also controlling cost. The past data are used in

preparation of financial budget that is actually incurred in past (Akbar, 2010). These

reports are useful to give bonus and more incentives to employees and also motivate

them to achieve the standard goals of company. The budget which are forecasting

based on reports which assist business to consolidate data and information.

·Job cost reports:- job cost are those cost which are associated with specific job,

work and contract of company. Each job cost will treated as single cost with

accordance of costing job costing also known as single costing. Job cost may be

inclusive of all similar job with same cost but single costing is applied on these job

cost.

·Inventory and manufacturing reports:- Company use this report to become more

efficient process of manufacturing and also company involve these kind of reports in

manufacturing so that it will better than previous. These report has overall

information about the cost per unit, labour overhead which are concerned with the

stock and helpful in distinguish between assigned cost or opportunity cost.

·Performance report:- these reports have overall preview of performance of

company which is concerned with the managerial accounting data and information.

These reports are prepared for the comparison between planned budget and actual

cost of the company. These reports are made whenever needed by the company for

evaluating performance either half-yearly or quarterly.

2. Importance of using these reporting system:-

All above given reports are useful for management accounting to evaluate financial

position of company and reflecting effects of these reports in business. All above discussed

reporting tools are used to recording of all essential transaction and event which are

concerned with set-format. Exactly the same reports of receivable and payable will used to

prepared by the management and advantage are given below:-

·Budgeting reports:- these report are prepared for planning to measure

performance of company while making analysis about the determination of

performance of company and also controlling cost. The past data are used in

preparation of financial budget that is actually incurred in past (Akbar, 2010). These

reports are useful to give bonus and more incentives to employees and also motivate

them to achieve the standard goals of company. The budget which are forecasting

based on reports which assist business to consolidate data and information.

·Job cost reports:- job cost are those cost which are associated with specific job,

work and contract of company. Each job cost will treated as single cost with

accordance of costing job costing also known as single costing. Job cost may be

inclusive of all similar job with same cost but single costing is applied on these job

cost.

·Inventory and manufacturing reports:- Company use this report to become more

efficient process of manufacturing and also company involve these kind of reports in

manufacturing so that it will better than previous. These report has overall

information about the cost per unit, labour overhead which are concerned with the

stock and helpful in distinguish between assigned cost or opportunity cost.

·Performance report:- these reports have overall preview of performance of

company which is concerned with the managerial accounting data and information.

These reports are prepared for the comparison between planned budget and actual

cost of the company. These reports are made whenever needed by the company for

evaluating performance either half-yearly or quarterly.

2. Importance of using these reporting system:-

All above given reports are useful for management accounting to evaluate financial

position of company and reflecting effects of these reports in business. All above discussed

reporting tools are used to recording of all essential transaction and event which are

concerned with set-format. Exactly the same reports of receivable and payable will used to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

determination of collection and payment from various creditors and debtors. As well as

inventoey reports is used to ascertain the stock held with the company.

l壱M1 Benefits of management systems under the TECH (UK) LTD.

By using all these method or function, TECH (UK) LTD. can operate and run the

organization without any difficulty. There are is various tools which are used by company to

attains business objective and goals in effective or correct manner. Under this it can be seen

that company will able to run its business more effectively by adopting these method and

techniques (Leitner, 2013). Management accounting provides more beneficiary objective to

company when providing important information and data also company will able to increase

in the liquid profitability ratio with the use of management accounting system(MAS).

l壱D1. How management accounting system and management accounting reporting integrates

within the company process

Managerial accounting system help to TECH(UK) LTD. To prepare the managerial

accounting reports within effective and more appropriate decision so that company will be

able to attains business goals in effective manner with budgeted figures and period. This is

correct action taken by the company to achieve their business goals by running their business

smoothly. So the both the system of management accounting reports and management

accounting system is integrated.

·TASK 2

·Calculation of net profit under marginal and absorption costing:-

Marginal costing: marginal costing is system of costing whereby all variable fixed

cost excluded from the total cost and variable cost is inclusive in total cost of product for

costing. It is used to ascertain the change in the volume of activity with the change in

variable cost or profit. The marginal costing requires a clear difference between fixed and

variable cost and this is the widely usable method of costing.

Absorption costing:- absorption costing is method of costing in which direct variable

cost and direct fixed cost both are inclusive in the charging of all cost. It is different from

marginal costing, the main difference is exclusion of fixed cost for costing in marginal

costing method.

inventoey reports is used to ascertain the stock held with the company.

l壱M1 Benefits of management systems under the TECH (UK) LTD.

By using all these method or function, TECH (UK) LTD. can operate and run the

organization without any difficulty. There are is various tools which are used by company to

attains business objective and goals in effective or correct manner. Under this it can be seen

that company will able to run its business more effectively by adopting these method and

techniques (Leitner, 2013). Management accounting provides more beneficiary objective to

company when providing important information and data also company will able to increase

in the liquid profitability ratio with the use of management accounting system(MAS).

l壱D1. How management accounting system and management accounting reporting integrates

within the company process

Managerial accounting system help to TECH(UK) LTD. To prepare the managerial

accounting reports within effective and more appropriate decision so that company will be

able to attains business goals in effective manner with budgeted figures and period. This is

correct action taken by the company to achieve their business goals by running their business

smoothly. So the both the system of management accounting reports and management

accounting system is integrated.

·TASK 2

·Calculation of net profit under marginal and absorption costing:-

Marginal costing: marginal costing is system of costing whereby all variable fixed

cost excluded from the total cost and variable cost is inclusive in total cost of product for

costing. It is used to ascertain the change in the volume of activity with the change in

variable cost or profit. The marginal costing requires a clear difference between fixed and

variable cost and this is the widely usable method of costing.

Absorption costing:- absorption costing is method of costing in which direct variable

cost and direct fixed cost both are inclusive in the charging of all cost. It is different from

marginal costing, the main difference is exclusion of fixed cost for costing in marginal

costing method.

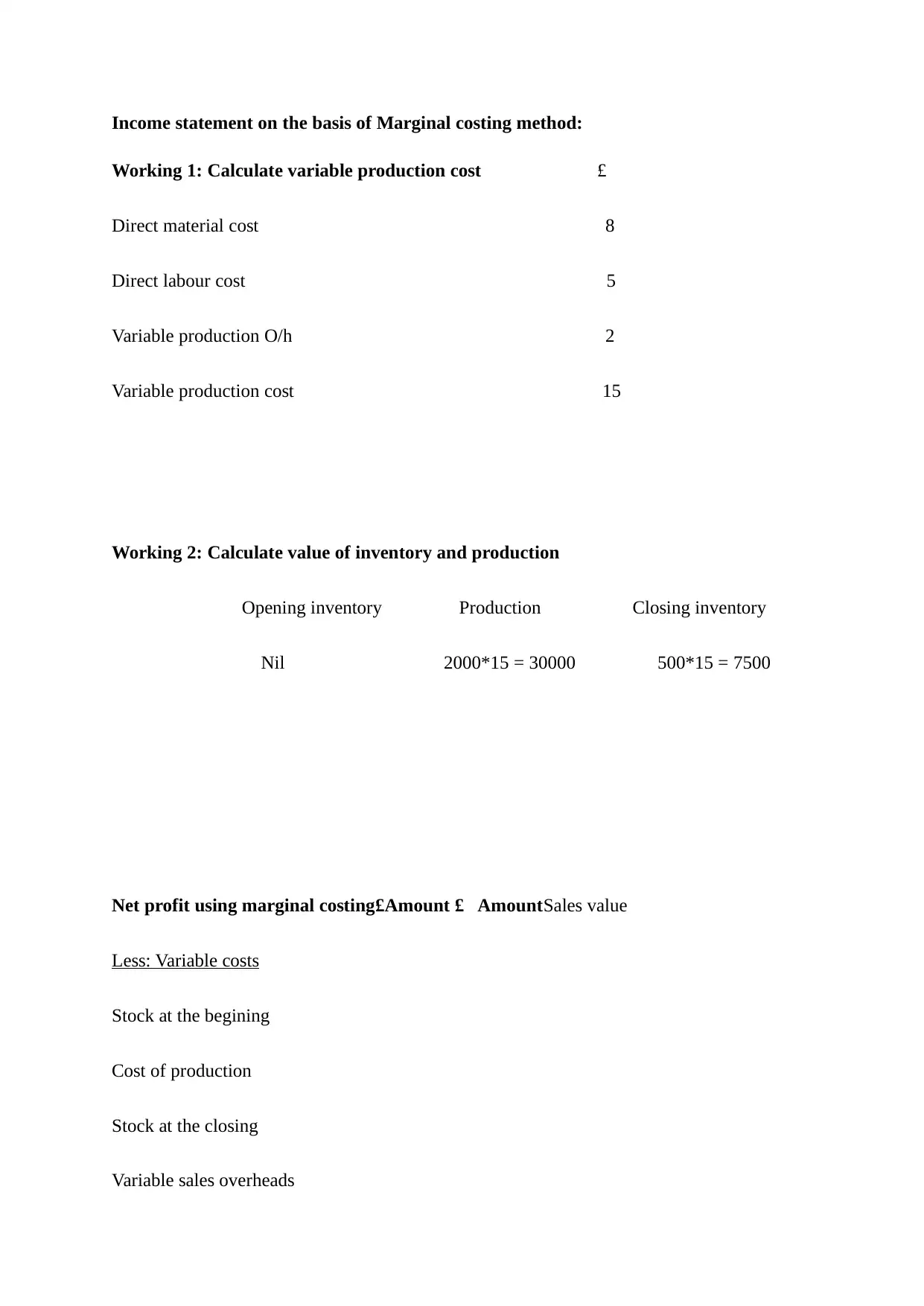

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing£Amount £ AmountSales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing£Amount £ AmountSales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

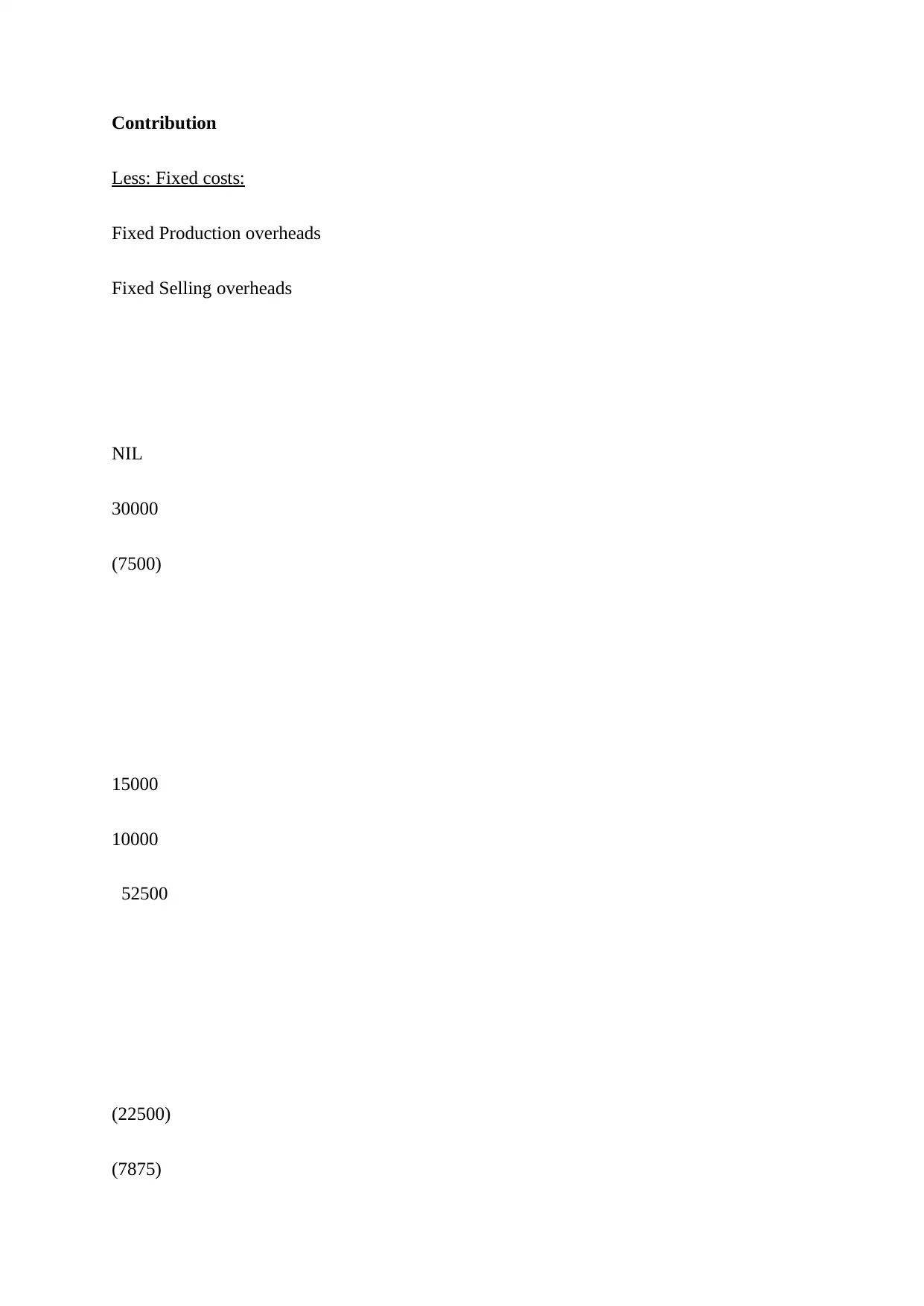

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

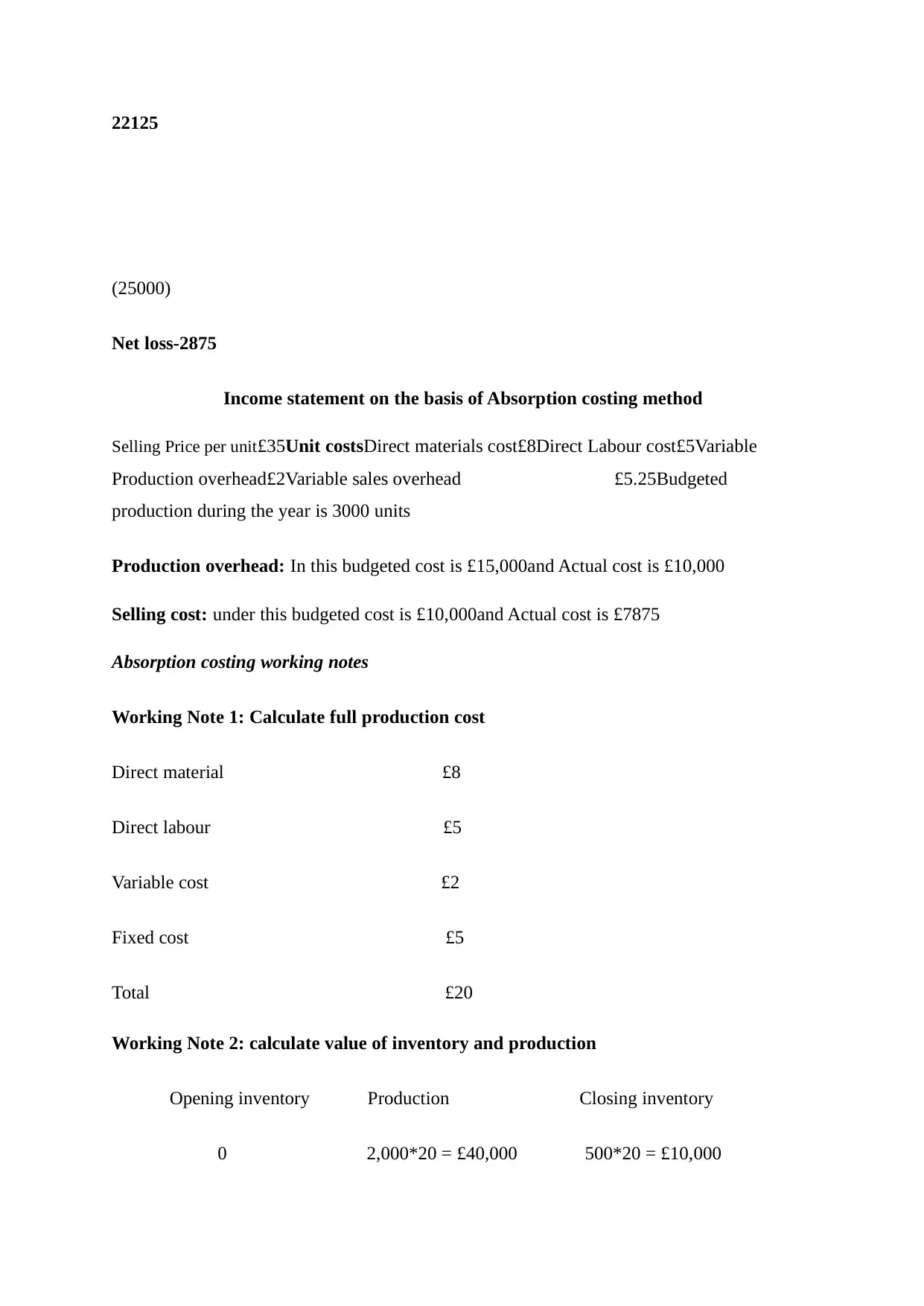

22125

(25000)

Net loss-2875

Income statement on the basis of Absorption costing method

Selling Price per unit£35Unit costsDirect materials cost£8Direct Labour cost£5Variable

Production overhead£2Variable sales overhead £5.25Budgeted

production during the year is 3000 units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

(25000)

Net loss-2875

Income statement on the basis of Absorption costing method

Selling Price per unit£35Unit costsDirect materials cost£8Direct Labour cost£5Variable

Production overhead£2Variable sales overhead £5.25Budgeted

production during the year is 3000 units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings£Amount £AmountSales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings£Amount £AmountSales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.