Analysis of Financial Management in Tesco's Operations

VerifiedAdded on 2023/01/11

|16

|5610

|47

Report

AI Summary

This financial management report analyzes the financial and management accounting practices of Tesco, a major supermarket chain. The report is divided into two scenarios. Scenario 1 evaluates techniques and factors influencing organizational decision-making, including brainstorming and SWOT analysis, alongside stakeholder management and the management of conflicting objectives. It also examines the value of management accounting techniques for cost control and maximizing stakeholder value, and techniques for fraud detection and prevention. Scenario 2 focuses on how data informs operational and strategic decisions, compares and contrasts investment appraisal techniques, and demonstrates techniques used in financial decision making. The report analyzes how financial decisions support long-term sustainability and provides recommendations for management accountants to improve financial stability. The report covers various techniques like marginal costing, capital budgeting, standard costing, and historical costing, alongside auditing for fraud detection and prevention. The analysis provides a comprehensive overview of Tesco's financial management strategies, providing insights into decision-making, cost control, and stakeholder management.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

1. Evaluation of the range of techniques and factors which are contributing in the decision

making of the organisation..........................................................................................................1

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups.......................................................................................................................2

3. The value of management accounting techniques in cost control and maximising

stakeholder value.........................................................................................................................3

4. Techniques for fraud detection and prevention and the approach to ethical decision making5

5. Reflection for the understanding of above questions..............................................................6

SCENARIO 2..................................................................................................................................6

1. Identify how data helps to inform operational or strategic decisions for the company...........6

2. Compare and contrast the three investment appraisal techniques...........................................9

3. Demonstrate the value of techniques which helps in financial decision making..................10

4. Analyse that how financial decisions support the long term sustainability...........................11

5. Recommendations regarding the way in which management accountants can help to

improve financial sustainability.................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

SCENARIO 1..................................................................................................................................1

1. Evaluation of the range of techniques and factors which are contributing in the decision

making of the organisation..........................................................................................................1

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups.......................................................................................................................2

3. The value of management accounting techniques in cost control and maximising

stakeholder value.........................................................................................................................3

4. Techniques for fraud detection and prevention and the approach to ethical decision making5

5. Reflection for the understanding of above questions..............................................................6

SCENARIO 2..................................................................................................................................6

1. Identify how data helps to inform operational or strategic decisions for the company...........6

2. Compare and contrast the three investment appraisal techniques...........................................9

3. Demonstrate the value of techniques which helps in financial decision making..................10

4. Analyse that how financial decisions support the long term sustainability...........................11

5. Recommendations regarding the way in which management accountants can help to

improve financial sustainability.................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial accounting principles can be defined as various types of rules and regulations

that are required to be followed by all the organisations while generating final accounts. Some of

the financial statements that are formulated by entities on yearly basis are profit and loss account,

balance sheet and cash flow statement. All of them are used to analyse actual position and

performance of company. While formulating decisions for future all of them are used to evaluate

the past year’s situation and then effective strategies are formed to make sure that highly

effective policies for upcoming years could be formed (Dauderies and Annand, 2019). In order to

meet strategic objectives such as increased profits, higher customer engagement and enhanced

revenues it is essential or all the enterprises to make sure that they are able to formulate the final

accounts on the basis of financial accounting principles. Present report is based upon analysis of

management as well as financial accounting of a company. The organisation which is selected

for this report is Tesco which is one of the largest supermarket chains around the world. It was

founded in year 1919 by Jack Cohen. Its headquarter is in London, United Kingdom. This

assignment is segregated in two parts. First scenario covers topics such as evaluation of range of

approaches, techniques and actors contributing in effective decisions making, stakeholder

management, value of management accounting in cost control and techniques of fraud detection

and prevention. Second scenario is based upon calculation of ratios, comparison and contrasting

of investment appraisal techniques, value of BEP and cash flow to inform decisions making etc.

Apart from this, analysis of financial decision making and recommendations for management

accountants to improve financial stability are also covered in this assignment.

SCENARIO 1

1. Evaluation of the range of techniques and factors which are contributing in the decision

making of the organisation

Effective decision making is very important for all the organisations and the managers

are required to make sure that they are using effective techniques and approaches for the same

purpose. In Tesco the management team is using various types of them and all of them are

facilitating effective decision making. Description of them is as follows:

Brain storming: It is one of the common approaches of decision making in which all the

team members sit together and try to analyse the position of business so that effective ways to

1

Financial accounting principles can be defined as various types of rules and regulations

that are required to be followed by all the organisations while generating final accounts. Some of

the financial statements that are formulated by entities on yearly basis are profit and loss account,

balance sheet and cash flow statement. All of them are used to analyse actual position and

performance of company. While formulating decisions for future all of them are used to evaluate

the past year’s situation and then effective strategies are formed to make sure that highly

effective policies for upcoming years could be formed (Dauderies and Annand, 2019). In order to

meet strategic objectives such as increased profits, higher customer engagement and enhanced

revenues it is essential or all the enterprises to make sure that they are able to formulate the final

accounts on the basis of financial accounting principles. Present report is based upon analysis of

management as well as financial accounting of a company. The organisation which is selected

for this report is Tesco which is one of the largest supermarket chains around the world. It was

founded in year 1919 by Jack Cohen. Its headquarter is in London, United Kingdom. This

assignment is segregated in two parts. First scenario covers topics such as evaluation of range of

approaches, techniques and actors contributing in effective decisions making, stakeholder

management, value of management accounting in cost control and techniques of fraud detection

and prevention. Second scenario is based upon calculation of ratios, comparison and contrasting

of investment appraisal techniques, value of BEP and cash flow to inform decisions making etc.

Apart from this, analysis of financial decision making and recommendations for management

accountants to improve financial stability are also covered in this assignment.

SCENARIO 1

1. Evaluation of the range of techniques and factors which are contributing in the decision

making of the organisation

Effective decision making is very important for all the organisations and the managers

are required to make sure that they are using effective techniques and approaches for the same

purpose. In Tesco the management team is using various types of them and all of them are

facilitating effective decision making. Description of them is as follows:

Brain storming: It is one of the common approaches of decision making in which all the

team members sit together and try to analyse the position of business so that effective ways to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

improve it could be determined. In order to analyse creative ways to meet the business goals it is

used by managers of Tesco so that they can find solution for the problems that are faced by the

organisation. It facilitates effective decision making because it guides them to determine the

steps that could be taken by them for betterment of business (Hayoun, 2018). It is beneficial for

the enterprise because it provides spontaneous solutions for difficult problems faced by the

organisation.

SWOT analysis: It is a technique which is also used in effective decision making by all

the entities like Tesco because with the help of it the managers get aware of strengths,

weaknesses, opportunities and threats for business. By analysing all of them, they determine

position of the company and then formulate effective decisions for upcoming period. It facilitates

in strategy formulation because when the management team will be aware of all the positive and

negative aspects of business then it can help to form effective decisions. This technique is mainly

used for strategic management so that performance of business could be improved.

While planning to formulate effective decisions for future different factors are also

focused by the managers. Description of them is as follows:

Risk: It is one of the main factors which is focused by the managers of Tesco while

formulating effective decisions. They determine all the risks for business which are currently

affecting the business or may leave adverse impacts in future. It helps them to be aware of all the

positive as well as negative situations for the organisation which guides them to make effective

decisions for betterment of the enterprise (Kimmel, Weygandt and Kieso, 2018).

Market situations: For all the managers it is very important to determine the market

situation so that it could be determined that business will be able to grow positively or not. The

management teams in Tesco analyse the market conditions and then formulate decisions for

business so that possibility of attainment of future goals could be enhanced. All the managers of

the organisation try to make sure that they are having accurate information about the market

situations as it helps to form effective strategic decisions for development of business.

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups

Stakeholder management can be defined as the procedure which is mainly focused with

organisation, monitoring, improving and maintaining relations with the stakeholders. It also pays

attention towards assessment of needs and expectations of all the groups of them so that effective

2

used by managers of Tesco so that they can find solution for the problems that are faced by the

organisation. It facilitates effective decision making because it guides them to determine the

steps that could be taken by them for betterment of business (Hayoun, 2018). It is beneficial for

the enterprise because it provides spontaneous solutions for difficult problems faced by the

organisation.

SWOT analysis: It is a technique which is also used in effective decision making by all

the entities like Tesco because with the help of it the managers get aware of strengths,

weaknesses, opportunities and threats for business. By analysing all of them, they determine

position of the company and then formulate effective decisions for upcoming period. It facilitates

in strategy formulation because when the management team will be aware of all the positive and

negative aspects of business then it can help to form effective decisions. This technique is mainly

used for strategic management so that performance of business could be improved.

While planning to formulate effective decisions for future different factors are also

focused by the managers. Description of them is as follows:

Risk: It is one of the main factors which is focused by the managers of Tesco while

formulating effective decisions. They determine all the risks for business which are currently

affecting the business or may leave adverse impacts in future. It helps them to be aware of all the

positive as well as negative situations for the organisation which guides them to make effective

decisions for betterment of the enterprise (Kimmel, Weygandt and Kieso, 2018).

Market situations: For all the managers it is very important to determine the market

situation so that it could be determined that business will be able to grow positively or not. The

management teams in Tesco analyse the market conditions and then formulate decisions for

business so that possibility of attainment of future goals could be enhanced. All the managers of

the organisation try to make sure that they are having accurate information about the market

situations as it helps to form effective strategic decisions for development of business.

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups

Stakeholder management can be defined as the procedure which is mainly focused with

organisation, monitoring, improving and maintaining relations with the stakeholders. It also pays

attention towards assessment of needs and expectations of all the groups of them so that effective

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

plans for meeting them could be formulated by the company. All the managers of Tesco are

focused with management of stakeholders such as employees, customers, government,

shareholders, creditors, investors etc. There are two main groups of the for the enterprise. These

are internal and external stakeholders.

Internal stakeholders are the individuals who internal part of the enterprise. Some of the

examples of them for Tesco are employees, shareholders board members etc. All of them are

focused with enhancement in profitability of the organisation and the main, objective of them is

to make sure that the profits and revenues of the enterprise are increasing continuously

(Mullinova, 2016).

External stakeholders are the parties who are the outsiders but having interest in the

business and its performance. It is very important for all companies like Tesco to make sure that

they are satisfied with the services that are rendered to them because it is very important to keep

them engaged in the business processes. Some of the examples of them are investors, creditors,

customers etc. Main purpose of them is to get higher returns on their funds and buy good quality

of products.

The objectives of internal and external group of stakeholders are conflicting and it may

create difficulties for the managers to manage their interests and objectives. In order to managing

their aims the managers try to formulate effective decisions for business as it can help to improve

the performance of business which will help to fulfil requirements of all of them. The managers

try to make sure that all the products are made with good quality so that profits could be

increased with higher sales. It will help to provide good returns to the investors. All these

activities are performed by the organisation to manage conflicting objectives of different

stakeholder groups (Narayanaswamy, 2017).

3. The value of management accounting techniques in cost control and maximising stakeholder

value

Management accounting is a process of analysing progress of operational activities and

then formulate effective decisions to make improvements in it. For large as well as small entities

it is very important to make sure that they are able to manage the operations as it is linked with

long-term goals. The managers in Tesco are also conducting it on yearly basis so that they can

control the cost and maximise the value of shareholders. Some of the key techniques of

management accounting which are used by them for these purposes are described below:

3

focused with management of stakeholders such as employees, customers, government,

shareholders, creditors, investors etc. There are two main groups of the for the enterprise. These

are internal and external stakeholders.

Internal stakeholders are the individuals who internal part of the enterprise. Some of the

examples of them for Tesco are employees, shareholders board members etc. All of them are

focused with enhancement in profitability of the organisation and the main, objective of them is

to make sure that the profits and revenues of the enterprise are increasing continuously

(Mullinova, 2016).

External stakeholders are the parties who are the outsiders but having interest in the

business and its performance. It is very important for all companies like Tesco to make sure that

they are satisfied with the services that are rendered to them because it is very important to keep

them engaged in the business processes. Some of the examples of them are investors, creditors,

customers etc. Main purpose of them is to get higher returns on their funds and buy good quality

of products.

The objectives of internal and external group of stakeholders are conflicting and it may

create difficulties for the managers to manage their interests and objectives. In order to managing

their aims the managers try to formulate effective decisions for business as it can help to improve

the performance of business which will help to fulfil requirements of all of them. The managers

try to make sure that all the products are made with good quality so that profits could be

increased with higher sales. It will help to provide good returns to the investors. All these

activities are performed by the organisation to manage conflicting objectives of different

stakeholder groups (Narayanaswamy, 2017).

3. The value of management accounting techniques in cost control and maximising stakeholder

value

Management accounting is a process of analysing progress of operational activities and

then formulate effective decisions to make improvements in it. For large as well as small entities

it is very important to make sure that they are able to manage the operations as it is linked with

long-term goals. The managers in Tesco are also conducting it on yearly basis so that they can

control the cost and maximise the value of shareholders. Some of the key techniques of

management accounting which are used by them for these purposes are described below:

3

Marginal costing: This technique is mainly focused with charging the variable cost per

unit and write off the fixed cost for all the items. It is used in Tesco by the managers to make

sure that they are able to analyse the cost of selling one additional unit to the clients. With the

help of it, they try to control the cost because when they will have detailed information of cost

then it will be beneficial for them to find ways to control it. It is also used to maintain

stakeholder’s value because it guides, management to get aware of factors which are resulting in

higher cost and if they will be controlled then value of shareholders will be increased (Pratt,

2016).

Capital budgeting: This technique of management accounting is used in investment

appraisal. With the help of it, managers of Tesco analyse different proposed projects so that one

of the which is best for growth of business could be selected. For example, if the entity is willing

to expand its business in a new location and it is having different alternatives for the same then

capital budgeting could be used to select the best option. With the help of it, the managers try to

maximise the value of shareholders because it will help to select the best project which will help

to grow the business. When The best project will be selected then it will provide benefits to

business and also help to increase value of shareholders.

Standard costing: This technique of management accounting is focused with the

analysis of variation between the actual and budgeted costs. In Tesco it is used by the managers

for the purpose of controlling the cost. It guides them to analyse that the estimations that were

made by them are able to meet the actual figures or not. Apart from this, the managers also try to

control the cost with the help of it because it guides them to determine future costs on the basis

of previous years. When the cost of operations will be controlled then it can help to increase the

value of shareholders within the enterprise.

Historical costing: This technique of management accounting is also focused with

recording all the assets and liabilities on their actual value in the balance sheet. They should not

be recorded on the basis of the market price in the statement of financial position. It is used in

Tesco by the managers for the purpose of making sure that value of shareholders will be

maximised (Rutherford, 2016). When all the assets and liabilities will be recorded on the basis of

their actual cost then it will help to reduce the possibility of negative impacts of changes in

market prices of them.

4

unit and write off the fixed cost for all the items. It is used in Tesco by the managers to make

sure that they are able to analyse the cost of selling one additional unit to the clients. With the

help of it, they try to control the cost because when they will have detailed information of cost

then it will be beneficial for them to find ways to control it. It is also used to maintain

stakeholder’s value because it guides, management to get aware of factors which are resulting in

higher cost and if they will be controlled then value of shareholders will be increased (Pratt,

2016).

Capital budgeting: This technique of management accounting is used in investment

appraisal. With the help of it, managers of Tesco analyse different proposed projects so that one

of the which is best for growth of business could be selected. For example, if the entity is willing

to expand its business in a new location and it is having different alternatives for the same then

capital budgeting could be used to select the best option. With the help of it, the managers try to

maximise the value of shareholders because it will help to select the best project which will help

to grow the business. When The best project will be selected then it will provide benefits to

business and also help to increase value of shareholders.

Standard costing: This technique of management accounting is focused with the

analysis of variation between the actual and budgeted costs. In Tesco it is used by the managers

for the purpose of controlling the cost. It guides them to analyse that the estimations that were

made by them are able to meet the actual figures or not. Apart from this, the managers also try to

control the cost with the help of it because it guides them to determine future costs on the basis

of previous years. When the cost of operations will be controlled then it can help to increase the

value of shareholders within the enterprise.

Historical costing: This technique of management accounting is also focused with

recording all the assets and liabilities on their actual value in the balance sheet. They should not

be recorded on the basis of the market price in the statement of financial position. It is used in

Tesco by the managers for the purpose of making sure that value of shareholders will be

maximised (Rutherford, 2016). When all the assets and liabilities will be recorded on the basis of

their actual cost then it will help to reduce the possibility of negative impacts of changes in

market prices of them.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Techniques for fraud detection and prevention and the approach to ethical decision making

Fraud Detection can be defined as the process which is followed to analyse the frauds in

the final account on the other hand, fraud prevention is focused with the ignorance of any type of

fraud in the books of accounting. It is very important for all the organisations to make sure that

they are focused with both of them so that the possibility of mistakes in the records could be

ignored. There are various types of techniques that are used in Tesco for both the purposes.

Description of them is as follows:

Auditing: It is one of the main techniques of fraud detection because when all the

records of accounting will be audited in regular basis then it can help to analyse any type of fraud

which is being made by the accountants while recording information. With the help of it, the

managers in Tesco try to make sure that they are bale to determine all the frauds so that the

possibility of inaccurate financial statements could be ignored. By using it, on random basis it

will be very easy to detect the frauds and formulate strategies for resolution of them (Schroeder,

Clark and Cathey, 2019).

Assessment of records: It is also a technique which could be used by the organisations

for the purpose of detecting frauds. When all the records will be assessed then it will be very

easy to detect all the frauds which are made in the reports. In Tesco it is used by the managers to

make sure that they are able to analyse all the frauds that are made in the books and for this

purpose they assess each and every transaction which is recorded in the reports. Proper

assessment guides to analyse the mistakes.

Some of the specific techniques which are used by Tesco for the purpose of fraud

prevention are as follows:

Implementation of internal controls: It is one of the main techniques which are used

for the purpose preventing the frauds. It is used in Tesco by the managers by taking control over

all the activities so that they can reduce the possibility of frauds in the books. They also make

sure they check all the reports personally so that all the frauds could be prevented and transparent

report could be generated.

Hiring trustworthy staff members: It is also a technique which is focused by Tesco for

preventing the possibility of fraud. All the employees who are hired by it are trustworthy so that

the information of business could be shared by them without any specific restriction. With the

help of it, the organisation ignores the frauds in the books of accounting.

5

Fraud Detection can be defined as the process which is followed to analyse the frauds in

the final account on the other hand, fraud prevention is focused with the ignorance of any type of

fraud in the books of accounting. It is very important for all the organisations to make sure that

they are focused with both of them so that the possibility of mistakes in the records could be

ignored. There are various types of techniques that are used in Tesco for both the purposes.

Description of them is as follows:

Auditing: It is one of the main techniques of fraud detection because when all the

records of accounting will be audited in regular basis then it can help to analyse any type of fraud

which is being made by the accountants while recording information. With the help of it, the

managers in Tesco try to make sure that they are bale to determine all the frauds so that the

possibility of inaccurate financial statements could be ignored. By using it, on random basis it

will be very easy to detect the frauds and formulate strategies for resolution of them (Schroeder,

Clark and Cathey, 2019).

Assessment of records: It is also a technique which could be used by the organisations

for the purpose of detecting frauds. When all the records will be assessed then it will be very

easy to detect all the frauds which are made in the reports. In Tesco it is used by the managers to

make sure that they are able to analyse all the frauds that are made in the books and for this

purpose they assess each and every transaction which is recorded in the reports. Proper

assessment guides to analyse the mistakes.

Some of the specific techniques which are used by Tesco for the purpose of fraud

prevention are as follows:

Implementation of internal controls: It is one of the main techniques which are used

for the purpose preventing the frauds. It is used in Tesco by the managers by taking control over

all the activities so that they can reduce the possibility of frauds in the books. They also make

sure they check all the reports personally so that all the frauds could be prevented and transparent

report could be generated.

Hiring trustworthy staff members: It is also a technique which is focused by Tesco for

preventing the possibility of fraud. All the employees who are hired by it are trustworthy so that

the information of business could be shared by them without any specific restriction. With the

help of it, the organisation ignores the frauds in the books of accounting.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tesco is one of the largest entities which are carrying out operations at global level. The

managers of it are using various ethical approaches to formulate ethical decisions. Description of

them is as follows:

Fairness or justice approach: This approach is focused with formulation of fair

decisions and it guides managers of Tesco to be fair with all the staff members so that they can

work with higher engagement. It guides all the members in management team to unbiased with

all the employees and formulate ethical decisions for betterment of business (Sithole, 2016).

Rights approach: It is also focused with ethical decision making. It states that all the

managers in organisations such as Tesco are required to make sure that they are providing all the

rights to the employees and carrying out operations ethically.

5. Reflection for the understanding of above questions

All the above questions are mainly focused with management accounting which is required

to be conducted on yearly basis to analyse accuracy of internal records. While completing the

first question my knowledge regarding the approaches and techniques of effective decision

making was enhanced. Some of them which are used in Tesco are SWOT analysis and brain

storming. The factors that are focused by the organisation while formulating decisions are risk

and market situations. While answering second question I understood that there are various types

of stakeholders and all of them are having different objectives It is very important for the

companies to make efforts so that their expectations could be met. Third question is mainly

based upon management accounting techniques and it helped me to improve the understanding

regarding the approaches which could be used to control cost and maximise shareholder value.

The examples of them are marginal costing, standard costing, capital budgeting and historical

costing. Last question is based upon fraud detection and prevention (Suryanto and Ridwansyah,

2016). It helped me to understand the importance of them and the techniques which could be

used for them. Apart from this, I also gained knowledge of ethical decision making for an

organisation and importance of it.

SCENARIO 2

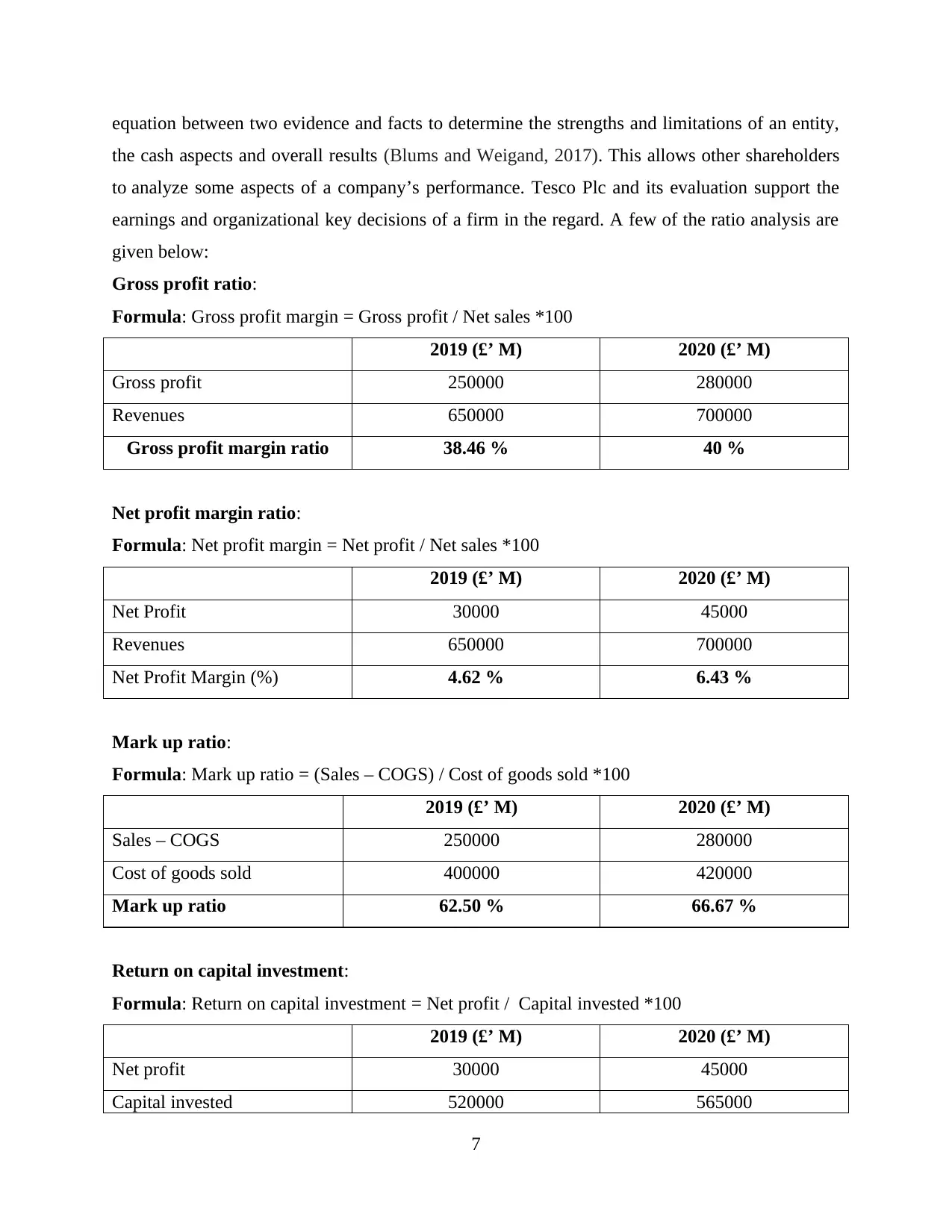

1. Identify how data helps to inform operational or strategic decisions for the company

Ratio analysis is widely used method, it is an essential method to analyze the financial

statement. Based on the financial information, the estimates build a qualitative or quantitative

6

managers of it are using various ethical approaches to formulate ethical decisions. Description of

them is as follows:

Fairness or justice approach: This approach is focused with formulation of fair

decisions and it guides managers of Tesco to be fair with all the staff members so that they can

work with higher engagement. It guides all the members in management team to unbiased with

all the employees and formulate ethical decisions for betterment of business (Sithole, 2016).

Rights approach: It is also focused with ethical decision making. It states that all the

managers in organisations such as Tesco are required to make sure that they are providing all the

rights to the employees and carrying out operations ethically.

5. Reflection for the understanding of above questions

All the above questions are mainly focused with management accounting which is required

to be conducted on yearly basis to analyse accuracy of internal records. While completing the

first question my knowledge regarding the approaches and techniques of effective decision

making was enhanced. Some of them which are used in Tesco are SWOT analysis and brain

storming. The factors that are focused by the organisation while formulating decisions are risk

and market situations. While answering second question I understood that there are various types

of stakeholders and all of them are having different objectives It is very important for the

companies to make efforts so that their expectations could be met. Third question is mainly

based upon management accounting techniques and it helped me to improve the understanding

regarding the approaches which could be used to control cost and maximise shareholder value.

The examples of them are marginal costing, standard costing, capital budgeting and historical

costing. Last question is based upon fraud detection and prevention (Suryanto and Ridwansyah,

2016). It helped me to understand the importance of them and the techniques which could be

used for them. Apart from this, I also gained knowledge of ethical decision making for an

organisation and importance of it.

SCENARIO 2

1. Identify how data helps to inform operational or strategic decisions for the company

Ratio analysis is widely used method, it is an essential method to analyze the financial

statement. Based on the financial information, the estimates build a qualitative or quantitative

6

equation between two evidence and facts to determine the strengths and limitations of an entity,

the cash aspects and overall results (Blums and Weigand, 2017). This allows other shareholders

to analyze some aspects of a company’s performance. Tesco Plc and its evaluation support the

earnings and organizational key decisions of a firm in the regard. A few of the ratio analysis are

given below:

Gross profit ratio:

Formula: Gross profit margin = Gross profit / Net sales *100

2019 (£’ M) 2020 (£’ M)

Gross profit 250000 280000

Revenues 650000 700000

Gross profit margin ratio 38.46 % 40 %

Net profit margin ratio:

Formula: Net profit margin = Net profit / Net sales *100

2019 (£’ M) 2020 (£’ M)

Net Profit 30000 45000

Revenues 650000 700000

Net Profit Margin (%) 4.62 % 6.43 %

Mark up ratio:

Formula: Mark up ratio = (Sales – COGS) / Cost of goods sold *100

2019 (£’ M) 2020 (£’ M)

Sales – COGS 250000 280000

Cost of goods sold 400000 420000

Mark up ratio 62.50 % 66.67 %

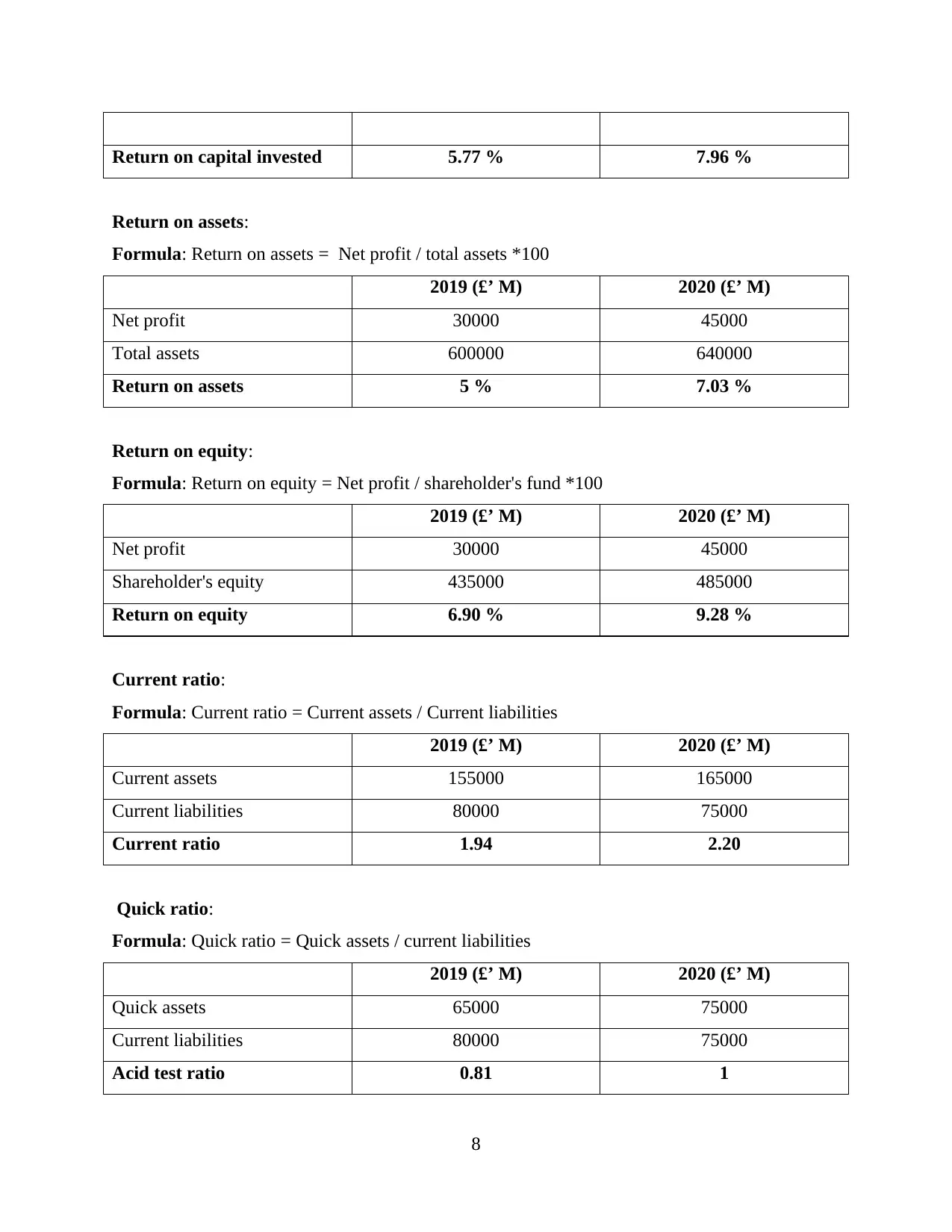

Return on capital investment:

Formula: Return on capital investment = Net profit / Capital invested *100

2019 (£’ M) 2020 (£’ M)

Net profit 30000 45000

Capital invested 520000 565000

7

the cash aspects and overall results (Blums and Weigand, 2017). This allows other shareholders

to analyze some aspects of a company’s performance. Tesco Plc and its evaluation support the

earnings and organizational key decisions of a firm in the regard. A few of the ratio analysis are

given below:

Gross profit ratio:

Formula: Gross profit margin = Gross profit / Net sales *100

2019 (£’ M) 2020 (£’ M)

Gross profit 250000 280000

Revenues 650000 700000

Gross profit margin ratio 38.46 % 40 %

Net profit margin ratio:

Formula: Net profit margin = Net profit / Net sales *100

2019 (£’ M) 2020 (£’ M)

Net Profit 30000 45000

Revenues 650000 700000

Net Profit Margin (%) 4.62 % 6.43 %

Mark up ratio:

Formula: Mark up ratio = (Sales – COGS) / Cost of goods sold *100

2019 (£’ M) 2020 (£’ M)

Sales – COGS 250000 280000

Cost of goods sold 400000 420000

Mark up ratio 62.50 % 66.67 %

Return on capital investment:

Formula: Return on capital investment = Net profit / Capital invested *100

2019 (£’ M) 2020 (£’ M)

Net profit 30000 45000

Capital invested 520000 565000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on capital invested 5.77 % 7.96 %

Return on assets:

Formula: Return on assets = Net profit / total assets *100

2019 (£’ M) 2020 (£’ M)

Net profit 30000 45000

Total assets 600000 640000

Return on assets 5 % 7.03 %

Return on equity:

Formula: Return on equity = Net profit / shareholder's fund *100

2019 (£’ M) 2020 (£’ M)

Net profit 30000 45000

Shareholder's equity 435000 485000

Return on equity 6.90 % 9.28 %

Current ratio:

Formula: Current ratio = Current assets / Current liabilities

2019 (£’ M) 2020 (£’ M)

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

Quick ratio:

Formula: Quick ratio = Quick assets / current liabilities

2019 (£’ M) 2020 (£’ M)

Quick assets 65000 75000

Current liabilities 80000 75000

Acid test ratio 0.81 1

8

Return on assets:

Formula: Return on assets = Net profit / total assets *100

2019 (£’ M) 2020 (£’ M)

Net profit 30000 45000

Total assets 600000 640000

Return on assets 5 % 7.03 %

Return on equity:

Formula: Return on equity = Net profit / shareholder's fund *100

2019 (£’ M) 2020 (£’ M)

Net profit 30000 45000

Shareholder's equity 435000 485000

Return on equity 6.90 % 9.28 %

Current ratio:

Formula: Current ratio = Current assets / Current liabilities

2019 (£’ M) 2020 (£’ M)

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

Quick ratio:

Formula: Quick ratio = Quick assets / current liabilities

2019 (£’ M) 2020 (£’ M)

Quick assets 65000 75000

Current liabilities 80000 75000

Acid test ratio 0.81 1

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

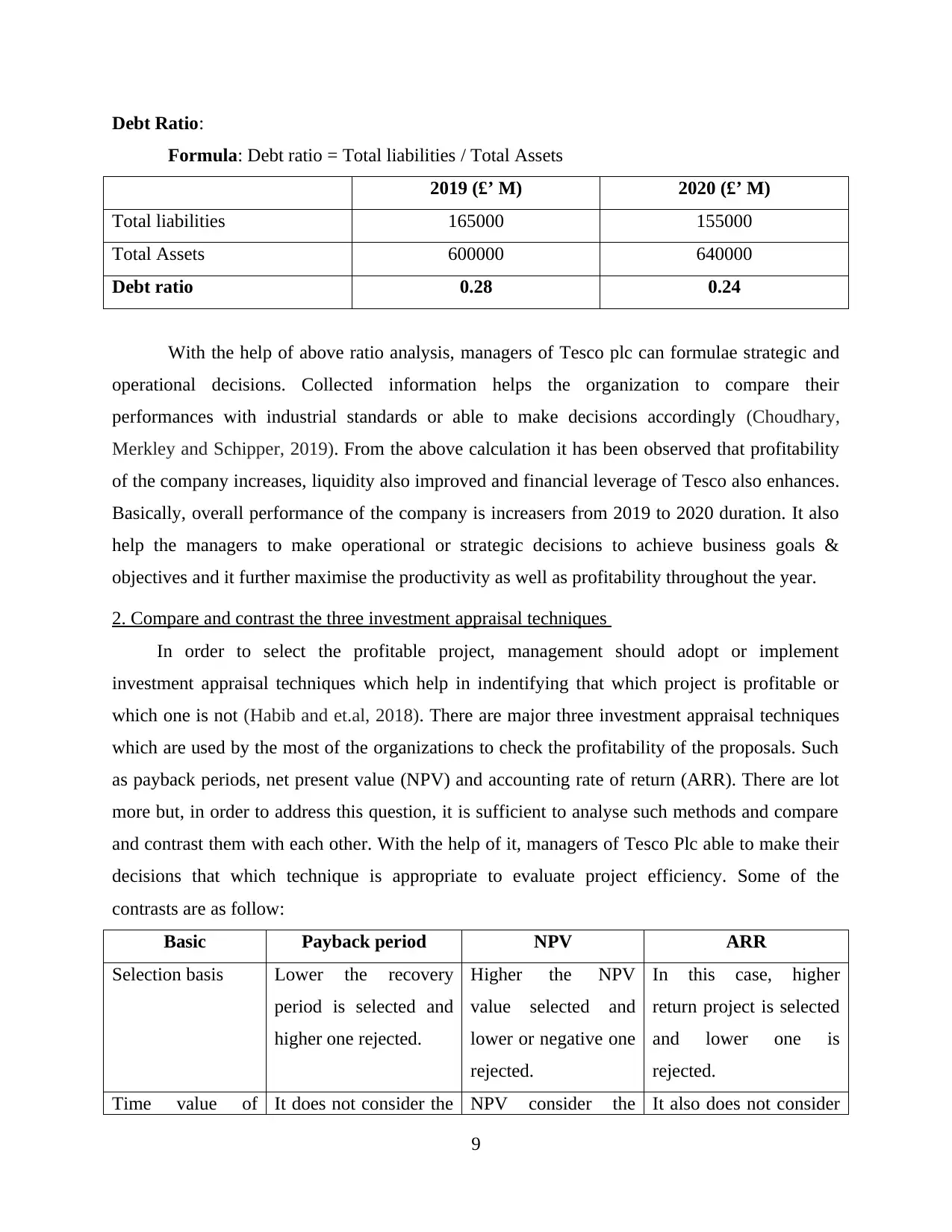

Debt Ratio:

Formula: Debt ratio = Total liabilities / Total Assets

2019 (£’ M) 2020 (£’ M)

Total liabilities 165000 155000

Total Assets 600000 640000

Debt ratio 0.28 0.24

With the help of above ratio analysis, managers of Tesco plc can formulae strategic and

operational decisions. Collected information helps the organization to compare their

performances with industrial standards or able to make decisions accordingly (Choudhary,

Merkley and Schipper, 2019). From the above calculation it has been observed that profitability

of the company increases, liquidity also improved and financial leverage of Tesco also enhances.

Basically, overall performance of the company is increasers from 2019 to 2020 duration. It also

help the managers to make operational or strategic decisions to achieve business goals &

objectives and it further maximise the productivity as well as profitability throughout the year.

2. Compare and contrast the three investment appraisal techniques

In order to select the profitable project, management should adopt or implement

investment appraisal techniques which help in indentifying that which project is profitable or

which one is not (Habib and et.al, 2018). There are major three investment appraisal techniques

which are used by the most of the organizations to check the profitability of the proposals. Such

as payback periods, net present value (NPV) and accounting rate of return (ARR). There are lot

more but, in order to address this question, it is sufficient to analyse such methods and compare

and contrast them with each other. With the help of it, managers of Tesco Plc able to make their

decisions that which technique is appropriate to evaluate project efficiency. Some of the

contrasts are as follow:

Basic Payback period NPV ARR

Selection basis Lower the recovery

period is selected and

higher one rejected.

Higher the NPV

value selected and

lower or negative one

rejected.

In this case, higher

return project is selected

and lower one is

rejected.

Time value of It does not consider the NPV consider the It also does not consider

9

Formula: Debt ratio = Total liabilities / Total Assets

2019 (£’ M) 2020 (£’ M)

Total liabilities 165000 155000

Total Assets 600000 640000

Debt ratio 0.28 0.24

With the help of above ratio analysis, managers of Tesco plc can formulae strategic and

operational decisions. Collected information helps the organization to compare their

performances with industrial standards or able to make decisions accordingly (Choudhary,

Merkley and Schipper, 2019). From the above calculation it has been observed that profitability

of the company increases, liquidity also improved and financial leverage of Tesco also enhances.

Basically, overall performance of the company is increasers from 2019 to 2020 duration. It also

help the managers to make operational or strategic decisions to achieve business goals &

objectives and it further maximise the productivity as well as profitability throughout the year.

2. Compare and contrast the three investment appraisal techniques

In order to select the profitable project, management should adopt or implement

investment appraisal techniques which help in indentifying that which project is profitable or

which one is not (Habib and et.al, 2018). There are major three investment appraisal techniques

which are used by the most of the organizations to check the profitability of the proposals. Such

as payback periods, net present value (NPV) and accounting rate of return (ARR). There are lot

more but, in order to address this question, it is sufficient to analyse such methods and compare

and contrast them with each other. With the help of it, managers of Tesco Plc able to make their

decisions that which technique is appropriate to evaluate project efficiency. Some of the

contrasts are as follow:

Basic Payback period NPV ARR

Selection basis Lower the recovery

period is selected and

higher one rejected.

Higher the NPV

value selected and

lower or negative one

rejected.

In this case, higher

return project is selected

and lower one is

rejected.

Time value of It does not consider the NPV consider the It also does not consider

9

money time of value of money

which can differ the

results.

time value of money

until the project life

cycle is ended.

the time value of money

which can provide

higher returns.

There are some basic similarities among the three investment appraisal techniques that all

are used to identify the profitability of the project and how much worth they provided to the

organization (Liang, Marinovic and Varas, 2018). All are very simple to calculate and further

help the managers to make their investment decisions accordingly. These are the most crucial

techniques which are used by the most of the organization beefier taking any decision in respect

of their future investments. With the help of it, they can easily compare the project or select the

most suitable project which provides more benefits in terms of profitability or higher returns.

3. Demonstrate the value of techniques which helps in financial decision making

There are several management accounting techniques which helps the organizations to

make financial decisions and make sure that it will be appropriate which maximise the overall

efficiency as well as effectiveness of business operations. Use of such techniques create value for

the organizations such as Tesco Plc, it help the managers to formulate financial decisions as per

the financial information by using below mention techniques:

Cash flow statement: It is a financial report which documents cash inflows and cash

outflows at a particular time in a business. It is among the most significant factors of a firm's

earnings management as it is a significant indicator of the company’s liquidity. It statement

supports the organisations in making financial decisions. Predict potential cash shortages, and

then make a spending plan in advance. Establish a sound foundation for taking credit;

incorporate it, for example, into our strategic plan of action by management or organizational

strategy. When in every time frame they have accrued positive balances, part of this surplus will

be deposited in the stock market to produce an extra stream of income. Under one of the income

sections, the money is reported as interest income (Obradović, Čupić and Dimitrijević, 2018). It

could also be investing in technology or machinery to enhance the performance of the firm. The

important aspect of the cash flow statement would be that it allows businesses to know its

liquidity quickly, providing key knowledge that enables to make financial decisions.

Break-even analysis: This is the stage at which the profits of the company provided

sufficient income to offset all of its operating costs and expenditures. At this point, all received

10

which can differ the

results.

time value of money

until the project life

cycle is ended.

the time value of money

which can provide

higher returns.

There are some basic similarities among the three investment appraisal techniques that all

are used to identify the profitability of the project and how much worth they provided to the

organization (Liang, Marinovic and Varas, 2018). All are very simple to calculate and further

help the managers to make their investment decisions accordingly. These are the most crucial

techniques which are used by the most of the organization beefier taking any decision in respect

of their future investments. With the help of it, they can easily compare the project or select the

most suitable project which provides more benefits in terms of profitability or higher returns.

3. Demonstrate the value of techniques which helps in financial decision making

There are several management accounting techniques which helps the organizations to

make financial decisions and make sure that it will be appropriate which maximise the overall

efficiency as well as effectiveness of business operations. Use of such techniques create value for

the organizations such as Tesco Plc, it help the managers to formulate financial decisions as per

the financial information by using below mention techniques:

Cash flow statement: It is a financial report which documents cash inflows and cash

outflows at a particular time in a business. It is among the most significant factors of a firm's

earnings management as it is a significant indicator of the company’s liquidity. It statement

supports the organisations in making financial decisions. Predict potential cash shortages, and

then make a spending plan in advance. Establish a sound foundation for taking credit;

incorporate it, for example, into our strategic plan of action by management or organizational

strategy. When in every time frame they have accrued positive balances, part of this surplus will

be deposited in the stock market to produce an extra stream of income. Under one of the income

sections, the money is reported as interest income (Obradović, Čupić and Dimitrijević, 2018). It

could also be investing in technology or machinery to enhance the performance of the firm. The

important aspect of the cash flow statement would be that it allows businesses to know its

liquidity quickly, providing key knowledge that enables to make financial decisions.

Break-even analysis: This is the stage at which the profits of the company provided

sufficient income to offset all of its operating costs and expenditures. At this point, all received

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.