Financial Performance Analysis of Tesco and Sainsbury's (MAN7040)

VerifiedAdded on 2022/09/01

|17

|2641

|22

Report

AI Summary

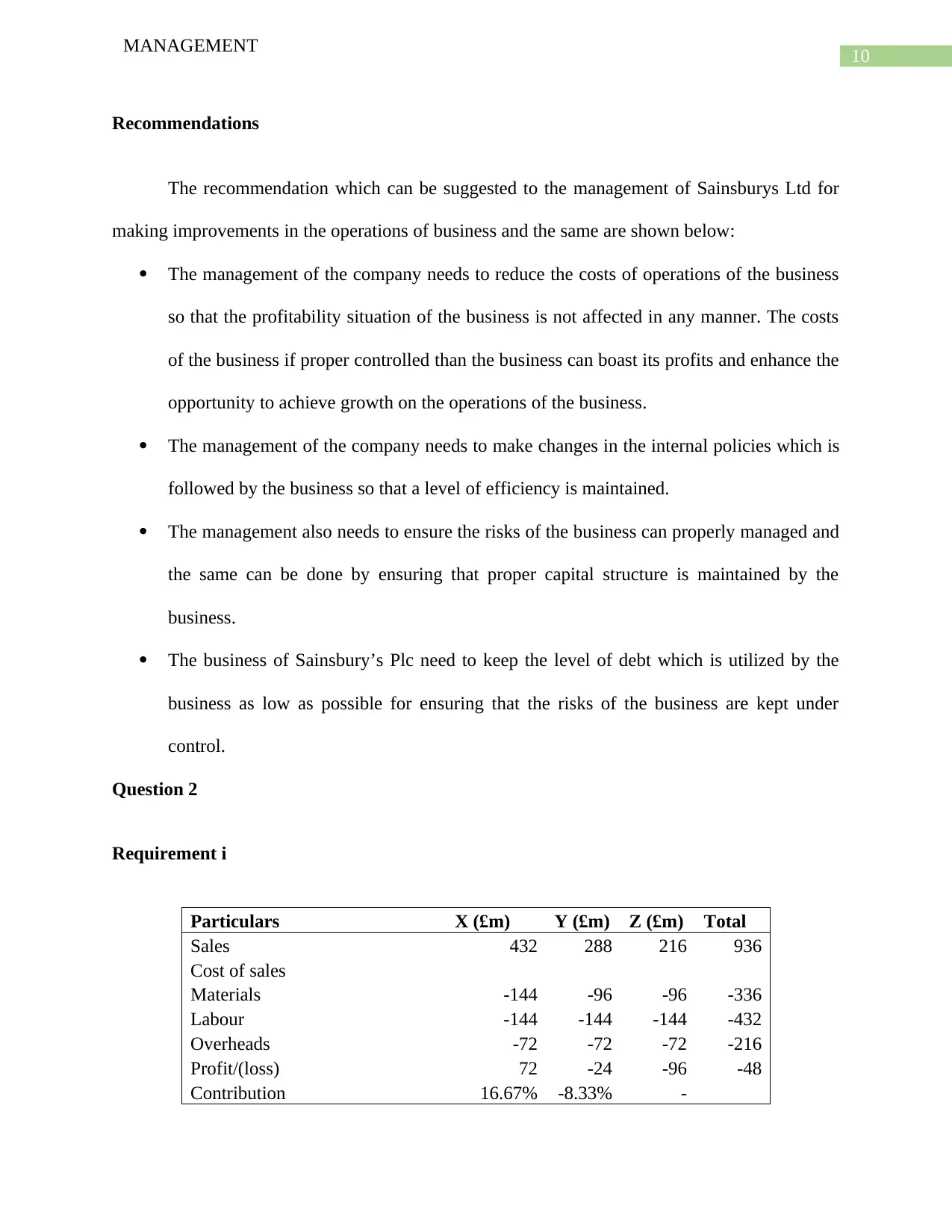

This report presents a comprehensive financial analysis of Tesco and Sainsbury's, evaluating their performance over a five-year period. It begins with an introduction outlining the objectives, followed by an in-depth examination of key financial ratios, including profitability, liquidity, efficiency, and gearing ratios. The analysis compares the performance of both companies, highlighting their strengths and weaknesses. The report then delves into specific financial scenarios, applying marginal costing techniques to determine optimal production strategies. Investment appraisal techniques, such as NPV, IRR, and payback period, are utilized to assess the viability of potential projects. The report also discusses the increasing convergence of corporate governance and corporate social responsibility (CSR), and the relevant legislation. Finally, the report concludes with recommendations for improving the operational structure and financial performance of both companies, offering insights into cost management, efficiency improvements, and risk mitigation strategies. The report is a comprehensive evaluation, including financial data analysis, recommendations, and a discussion of relevant business concepts.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.