Financial Management: Cost, Volume, Profit Analysis in Tourism

VerifiedAdded on 2023/04/10

|20

|4575

|219

Report

AI Summary

This report provides a comprehensive analysis of financial management within the travel and tourism industry, using Thomas Cook Group Plc as a case study. It explores the importance of cost and volume in financial management, analyzing different types of costs (direct, indirect, fixed, variable) and the significance of break-even analysis and cost-volume-profit analysis. The report also examines pricing methods used in the sector, such as commission, package deals, premium pricing, seasonal variation, and price lining, along with factors influencing profit, including commissions, discounting, and package deals. Furthermore, it discusses various types of management accounting information, including cash flow forecasts, statistical sales data, variance analysis, budget analysis, and marginal costing, assessing their use as decision-making tools. The report includes a ratio-based analysis of Thomas Cook Group PLC Limited and an analysis of funding sources and distribution for public and non-public tourism development.

Contents

Introduction.................................................................................................................................................2

Task 1...........................................................................................................................................................3

P1.1 explain the importance of costs and volume in financial management of travel and tourism

businesses using International Airlines Group (IAG) or Thomas Cook as your case study.......................3

P1.2 analyse pricing methods used in the travel and tourism sector using International Airlines Group

(IAG) or Thomas Cook Group Plc as your case study................................................................................5

P1.3 analyse factors influencing profit for travel and tourism businesses using International Airlines

Group (IAG) or Thomas Cook Group as your case study..........................................................................6

Task 2...........................................................................................................................................................8

P2.1 explain different types of management accounting information that could be used in travel and

tourism businesses using International Airlines Group (IAG) or Thomas Cook Group Plc as your case

study........................................................................................................................................................8

P2.2 assess the use of management accounting information as a decision-making tool for International

Airlines Group (IAG) or Thomas Cook Group Plc......................................................................................9

Task 3.........................................................................................................................................................10

P3.1. Ratio based analysis of Thomas Cook Group PLC Limited.............................................................10

Task 4.........................................................................................................................................................13

P4.1 Analyse sources and distribution of funding for public and non-public tourism development......13

Conclusion.................................................................................................................................................17

References.................................................................................................................................................18

1

Introduction.................................................................................................................................................2

Task 1...........................................................................................................................................................3

P1.1 explain the importance of costs and volume in financial management of travel and tourism

businesses using International Airlines Group (IAG) or Thomas Cook as your case study.......................3

P1.2 analyse pricing methods used in the travel and tourism sector using International Airlines Group

(IAG) or Thomas Cook Group Plc as your case study................................................................................5

P1.3 analyse factors influencing profit for travel and tourism businesses using International Airlines

Group (IAG) or Thomas Cook Group as your case study..........................................................................6

Task 2...........................................................................................................................................................8

P2.1 explain different types of management accounting information that could be used in travel and

tourism businesses using International Airlines Group (IAG) or Thomas Cook Group Plc as your case

study........................................................................................................................................................8

P2.2 assess the use of management accounting information as a decision-making tool for International

Airlines Group (IAG) or Thomas Cook Group Plc......................................................................................9

Task 3.........................................................................................................................................................10

P3.1. Ratio based analysis of Thomas Cook Group PLC Limited.............................................................10

Task 4.........................................................................................................................................................13

P4.1 Analyse sources and distribution of funding for public and non-public tourism development......13

Conclusion.................................................................................................................................................17

References.................................................................................................................................................18

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

A travel and tourism company has been taken into consideration according to this assignment,

named as Thomas Cook Group Plc which has started its operations in the year of 1841,

headquartered at Peterborough, having current employee strength of 27000 employees and the

shares are being traded on London Stock Exchange. The organization provides a range of

products and services which includes cruise lines and passenger airlines, hotels and resorts and

holiday packages. It holds the position of leading market globally with a sales figure of about

£8.5 billion in the year of 2014. It operates from the main markets like Airlines Germany,

Northern Europe, Greater parts of United Kingdom, Continental Europe and other fifteen sources

of markets globally.

2

A travel and tourism company has been taken into consideration according to this assignment,

named as Thomas Cook Group Plc which has started its operations in the year of 1841,

headquartered at Peterborough, having current employee strength of 27000 employees and the

shares are being traded on London Stock Exchange. The organization provides a range of

products and services which includes cruise lines and passenger airlines, hotels and resorts and

holiday packages. It holds the position of leading market globally with a sales figure of about

£8.5 billion in the year of 2014. It operates from the main markets like Airlines Germany,

Northern Europe, Greater parts of United Kingdom, Continental Europe and other fifteen sources

of markets globally.

2

Task 1

P1.1 explain the importance of costs and volume in financial management of

travel and tourism businesses using International Airlines Group (IAG) or

Thomas Cook as your case study

The type and nature of cost and the relationship with the volume enables a manager to measure

the risk and take the necessary actions accordingly, both the cost and volume are important in

order to manage the financial operations of the company.

Cost: The expense that has been incurred by an organization for the production of goods is

considered as cost. In case of travel and tourism company the cost is incurred for the products

and services provided to the customers. In order to take decisions, a travel and tourism company

can use various types of cost. Based on various elements like traceability and form of activity, a

cost is divided (Brigham and Houston, 2004).

Degree of traceability:

1. Direct cost: The cost included in products and services which are easily recognized and

measured are termed as direct costs as the costs are related to the production directly and

are included in the product price. Direct cost is the complete accumulation of direct

labour, direct material and direct expenses. For a travel and tourism company the direct

costs are like the salary of the crew line members (Yu-Lee, 2001).

2. Indirect costs: indirect costs are the costs which are related indirectly to the production

and hence, cannot recognize or identified directly. Indirect cost is the accumulation of

indirect material, indirect labour and indirect expenses. Advertisement expenses are an

example of indirect expenses for a travel and tourism company (Ansari, 1997).

.Change in activity:

3

P1.1 explain the importance of costs and volume in financial management of

travel and tourism businesses using International Airlines Group (IAG) or

Thomas Cook as your case study

The type and nature of cost and the relationship with the volume enables a manager to measure

the risk and take the necessary actions accordingly, both the cost and volume are important in

order to manage the financial operations of the company.

Cost: The expense that has been incurred by an organization for the production of goods is

considered as cost. In case of travel and tourism company the cost is incurred for the products

and services provided to the customers. In order to take decisions, a travel and tourism company

can use various types of cost. Based on various elements like traceability and form of activity, a

cost is divided (Brigham and Houston, 2004).

Degree of traceability:

1. Direct cost: The cost included in products and services which are easily recognized and

measured are termed as direct costs as the costs are related to the production directly and

are included in the product price. Direct cost is the complete accumulation of direct

labour, direct material and direct expenses. For a travel and tourism company the direct

costs are like the salary of the crew line members (Yu-Lee, 2001).

2. Indirect costs: indirect costs are the costs which are related indirectly to the production

and hence, cannot recognize or identified directly. Indirect cost is the accumulation of

indirect material, indirect labour and indirect expenses. Advertisement expenses are an

example of indirect expenses for a travel and tourism company (Ansari, 1997).

.Change in activity:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Fixed cost: fixed costs are the cost which doesn’t change throughout the year according

to the production and remains constant or fixed. Even the company is running in loss, in

that situation also the company has to bear the related fixed costs. Office expenses like

rent, electricity bills, etc. comes under the heading of fixed costs.

2. Variable costs: variable costs are the cost which changes according to the changes occur

in the production process as this cost is variable in nature. For a travel and tourism

company, the fuel used for the airlines comes under the variable cost heading (Mowen,

1986).

Volume: The volume includes the following:

1. Break Even Analysis: The breakeven point is regarded as the level where the cost and

the revenue are equal. The percentage filled up seats is taken into consideration as load

factors while measuring the breakeven of Airlines Company. A company needs the break

even analysis in order to calculate the margin of safety as it reflects the stronger part of

the organization in terms of the amount of gain or loss being incurred by the company. As

the break even analysis only analyses the related cost of sales and ignores the demand

side, it can be considered as the supply side analysis (Cafferky and Wentworth, 2010).

There are several variables on which the break even analysis is based on, such as:

A. Total variable cost: It is the cost which changes with the extra unit production.

B. Selling price per unit: The costs which are provided by the customers against the

services they are provided with.

C. Total fixed cost: The costs which are related to the first unit of production.

D. Forecasted net profit: The difference between the total cost and total revenue.

2. Cost volume profit analysis: In case of taking short run decisions the cost volume

profits are necessary. The utilization of information being provided by the break even

4

to the production and remains constant or fixed. Even the company is running in loss, in

that situation also the company has to bear the related fixed costs. Office expenses like

rent, electricity bills, etc. comes under the heading of fixed costs.

2. Variable costs: variable costs are the cost which changes according to the changes occur

in the production process as this cost is variable in nature. For a travel and tourism

company, the fuel used for the airlines comes under the variable cost heading (Mowen,

1986).

Volume: The volume includes the following:

1. Break Even Analysis: The breakeven point is regarded as the level where the cost and

the revenue are equal. The percentage filled up seats is taken into consideration as load

factors while measuring the breakeven of Airlines Company. A company needs the break

even analysis in order to calculate the margin of safety as it reflects the stronger part of

the organization in terms of the amount of gain or loss being incurred by the company. As

the break even analysis only analyses the related cost of sales and ignores the demand

side, it can be considered as the supply side analysis (Cafferky and Wentworth, 2010).

There are several variables on which the break even analysis is based on, such as:

A. Total variable cost: It is the cost which changes with the extra unit production.

B. Selling price per unit: The costs which are provided by the customers against the

services they are provided with.

C. Total fixed cost: The costs which are related to the first unit of production.

D. Forecasted net profit: The difference between the total cost and total revenue.

2. Cost volume profit analysis: In case of taking short run decisions the cost volume

profits are necessary. The utilization of information being provided by the break even

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analysis is enhanced by the cost volume profit analysis (Shim and Siegel, 2000). The cost

volume profit analysis is calculated with the help of the following formula:

Profit = (P – V) x Q – F

Where

P= selling price per unit

V=Variable cost per unit

F=total fixed costs

Q= quantity

The Thomas Cook group can calculate its profit with the help of this analysis by evaluating the

number of unit along with its cost.

P1.2 analyse pricing methods used in the travel and tourism sector using

International Airlines Group (IAG) or Thomas Cook Group Plc as your case

study

As the pricing strategy allows the organization for earning more profits with more attracting

customers, it is necessary for the organization. For this reason the Thomas Cook Group used the

pricing strategy which is as follows:

Commission:

Recently in order to make bookings on behalf of the tourism organizations, a third party is hired.

The charges for the bookings on behalf of the organization which the third party makes are called

as commissions. In order to earn this amount from the customers, the Thomas Cook Group Plc

adds the charges being made for the third party with its products and services.

5

volume profit analysis is calculated with the help of the following formula:

Profit = (P – V) x Q – F

Where

P= selling price per unit

V=Variable cost per unit

F=total fixed costs

Q= quantity

The Thomas Cook group can calculate its profit with the help of this analysis by evaluating the

number of unit along with its cost.

P1.2 analyse pricing methods used in the travel and tourism sector using

International Airlines Group (IAG) or Thomas Cook Group Plc as your case

study

As the pricing strategy allows the organization for earning more profits with more attracting

customers, it is necessary for the organization. For this reason the Thomas Cook Group used the

pricing strategy which is as follows:

Commission:

Recently in order to make bookings on behalf of the tourism organizations, a third party is hired.

The charges for the bookings on behalf of the organization which the third party makes are called

as commissions. In order to earn this amount from the customers, the Thomas Cook Group Plc

adds the charges being made for the third party with its products and services.

5

Package deals:

This strategy is recently used in order to earn more profits. Thomas Cook Group has also adopted

this strategy with sharing hands with the local business concerns in order to provide the

customers full package. This strategy is used as the extra service added with the actual services

being provided which provides more comfort for the employees and full satisfaction for the

customers. A company can earn profit without being providing any discount for the customers.

This adds to one of the main advantages of the strategy.

Premium pricing:

This strategy is used in order to earn more profits as this strategy includes pricing the products

and services at a premium price as the customers think that the costly services are qualitative and

the cheaper services are of low quality. So this strategy is considered to be the best strategy for a

company to earn more profits (Lewis, 2011).

Seasonal variation:

In order to cope up with the rising demand of customers, companies generally adopts this kind of

strategies. According to this strategy the company mixes its products and services according to

the needs and choices of customers’ changes. For this reason Thomas Cook Group has adopted

this strategy in order to satisfy the customers fully.

Price lining:

It is done with a stable set of product and service price for creating the level of quality in the

mind of the customers.

P1.3 analyse factors influencing profit for travel and tourism businesses using

International Airlines Group (IAG) or Thomas Cook Group as your case study

The Thomas Cook Group Plc is determined by the influencing factors which are as follows:

6

This strategy is recently used in order to earn more profits. Thomas Cook Group has also adopted

this strategy with sharing hands with the local business concerns in order to provide the

customers full package. This strategy is used as the extra service added with the actual services

being provided which provides more comfort for the employees and full satisfaction for the

customers. A company can earn profit without being providing any discount for the customers.

This adds to one of the main advantages of the strategy.

Premium pricing:

This strategy is used in order to earn more profits as this strategy includes pricing the products

and services at a premium price as the customers think that the costly services are qualitative and

the cheaper services are of low quality. So this strategy is considered to be the best strategy for a

company to earn more profits (Lewis, 2011).

Seasonal variation:

In order to cope up with the rising demand of customers, companies generally adopts this kind of

strategies. According to this strategy the company mixes its products and services according to

the needs and choices of customers’ changes. For this reason Thomas Cook Group has adopted

this strategy in order to satisfy the customers fully.

Price lining:

It is done with a stable set of product and service price for creating the level of quality in the

mind of the customers.

P1.3 analyse factors influencing profit for travel and tourism businesses using

International Airlines Group (IAG) or Thomas Cook Group as your case study

The Thomas Cook Group Plc is determined by the influencing factors which are as follows:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Commission: The inbound tour operators, the travel agents are always paid by the Thomas Cook

Group Plc as commissions for the services they have provided and is also discussed in pricing

strategy for the customers. The pricing strategy of different channels varies from each other

which affects the profitability of the business, this inclusion creates problem for the company.

With the help of the management information the company makes policies and takes proper

decisions. The management information help the company also in making important decisions

like budgeting, cash flowed, etc. (Adongo, Stork and Hasheela, 2005).

Discounting: As the company can gain profit and even face loss in this strategy, this is

considered to be the most important and crucial factor and this requires an accurate decision. The

main twist in this factor is if the company doesn’t offer any discount then it doesn’t look

attractive for the customers and if the company avails more than required discount then it may

lead to incur loss. So while finalizing the decisions regarding this factor, the conditions should be

taken into account and planning should be done accordingly (Adongo, Stork and Hasheela,

2005).

Package deals: Generally the airway companies provide the deals which cover the packaging

system to the hotels. This system or deal includes the number of days stayed, food facilities, the

tourist places being visited by the customers, etc. the net rate of placing better package pricing

can be availed by providing the facilities to the tourism company dealing other complementary

tourism agencies (Adongo, Stork and Hasheela, 2005).

7

Group Plc as commissions for the services they have provided and is also discussed in pricing

strategy for the customers. The pricing strategy of different channels varies from each other

which affects the profitability of the business, this inclusion creates problem for the company.

With the help of the management information the company makes policies and takes proper

decisions. The management information help the company also in making important decisions

like budgeting, cash flowed, etc. (Adongo, Stork and Hasheela, 2005).

Discounting: As the company can gain profit and even face loss in this strategy, this is

considered to be the most important and crucial factor and this requires an accurate decision. The

main twist in this factor is if the company doesn’t offer any discount then it doesn’t look

attractive for the customers and if the company avails more than required discount then it may

lead to incur loss. So while finalizing the decisions regarding this factor, the conditions should be

taken into account and planning should be done accordingly (Adongo, Stork and Hasheela,

2005).

Package deals: Generally the airway companies provide the deals which cover the packaging

system to the hotels. This system or deal includes the number of days stayed, food facilities, the

tourist places being visited by the customers, etc. the net rate of placing better package pricing

can be availed by providing the facilities to the tourism company dealing other complementary

tourism agencies (Adongo, Stork and Hasheela, 2005).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2

P2.1 explain different types of management accounting information that could

be used in travel and tourism businesses using International Airlines Group

(IAG) or Thomas Cook Group Plc as your case study

In order to take proper decisions for the organization a management accounting information is

needed. It provides the required financial data needed for decision making.

Cash flow forecast:

For identifying the requirements relating to cash flows in advance for the Thomas Cook Group

for a particular time period, the cash flow forecast is needed. The process of cash flow

forecasting enables an organization to recognize the future decrease in cash balance in advance

8

P2.1 explain different types of management accounting information that could

be used in travel and tourism businesses using International Airlines Group

(IAG) or Thomas Cook Group Plc as your case study

In order to take proper decisions for the organization a management accounting information is

needed. It provides the required financial data needed for decision making.

Cash flow forecast:

For identifying the requirements relating to cash flows in advance for the Thomas Cook Group

for a particular time period, the cash flow forecast is needed. The process of cash flow

forecasting enables an organization to recognize the future decrease in cash balance in advance

8

and regarding the pricing strategies as well, the employees will be paid correctly or not. Though

the Thomas Cook Group is able to run its business smoothly without any obstacle, the

forecasting helps in planning upcoming expenses, purchases and also the areas where investment

of excess cash can be made (Dropkin and Hayden, 2001).

Statistical information about sales cost and profit:

In order to stay competitive in the market, the future planning must be done accordingly.

Planning for the operations of an organization to be taken place in the future can be done through

anticipating this process. The outcomes of the future operations are forecasted in advance with

the help of trend analysis. Past revenue, sales and growth statistics are taken into consideration

while calculating with the help of trend analysis.

Variance analysis:

Actual realized expenses and the budget expenses are compared while calculating the variance

analysis. The variance is used for the correction if there is any mistake. Raw material

consumption, material hours, man hours, production time, etc. is included in variance analysis

(Harris and West, 1997).

Budget analysis:

Budgeting takes place after forecasting and helps in framing an appropriate plan for the future.

Allocation of capital money for different operations for carrying out in future is called as

budgeting. Through budgeting the future costs and budgeting are estimated.

Marginal costing:

9

the Thomas Cook Group is able to run its business smoothly without any obstacle, the

forecasting helps in planning upcoming expenses, purchases and also the areas where investment

of excess cash can be made (Dropkin and Hayden, 2001).

Statistical information about sales cost and profit:

In order to stay competitive in the market, the future planning must be done accordingly.

Planning for the operations of an organization to be taken place in the future can be done through

anticipating this process. The outcomes of the future operations are forecasted in advance with

the help of trend analysis. Past revenue, sales and growth statistics are taken into consideration

while calculating with the help of trend analysis.

Variance analysis:

Actual realized expenses and the budget expenses are compared while calculating the variance

analysis. The variance is used for the correction if there is any mistake. Raw material

consumption, material hours, man hours, production time, etc. is included in variance analysis

(Harris and West, 1997).

Budget analysis:

Budgeting takes place after forecasting and helps in framing an appropriate plan for the future.

Allocation of capital money for different operations for carrying out in future is called as

budgeting. Through budgeting the future costs and budgeting are estimated.

Marginal costing:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With the production of one more unit of a product, the increase or decrease of the total cost

which a business incurs is defined as the marginal cost. The calculation of the relation between a

change in cost and a change in quantity is termed as marginal cost. This computation doesn’t

include the fixed costs (Lucey, 2002).

P2.2 assess the use of management accounting information as a decision-

making tool for International Airlines Group (IAG) or Thomas Cook Group Plc.

The management accounting system is important in decision making for an organization. The

organization takes the following decision depending on the management accounting system:

1. In order to stay competitive in the market in future the organization needs to forecast

sales, revenue and cost. The future policies and goals are also can be determined with the

help of the management accounting system.

2. The management accounting system helps in allocating the resources accordingly. The

management accounting system also helps in making decisions regarding the optimum

product mix and the investment plans for new plants and properties.

3. The decisions regarding the raising of funds are also made with the help of management

accounting information. The future financial needs are determined by the budget forecast

and variance analysis.

4. In order to finance the daily operations the funds that are used are termed as working

capital. The proper arrangement of working capital is done with the help of the

management accounting system (Epstein and Lee, 2007).

.

10

which a business incurs is defined as the marginal cost. The calculation of the relation between a

change in cost and a change in quantity is termed as marginal cost. This computation doesn’t

include the fixed costs (Lucey, 2002).

P2.2 assess the use of management accounting information as a decision-

making tool for International Airlines Group (IAG) or Thomas Cook Group Plc.

The management accounting system is important in decision making for an organization. The

organization takes the following decision depending on the management accounting system:

1. In order to stay competitive in the market in future the organization needs to forecast

sales, revenue and cost. The future policies and goals are also can be determined with the

help of the management accounting system.

2. The management accounting system helps in allocating the resources accordingly. The

management accounting system also helps in making decisions regarding the optimum

product mix and the investment plans for new plants and properties.

3. The decisions regarding the raising of funds are also made with the help of management

accounting information. The future financial needs are determined by the budget forecast

and variance analysis.

4. In order to finance the daily operations the funds that are used are termed as working

capital. The proper arrangement of working capital is done with the help of the

management accounting system (Epstein and Lee, 2007).

.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

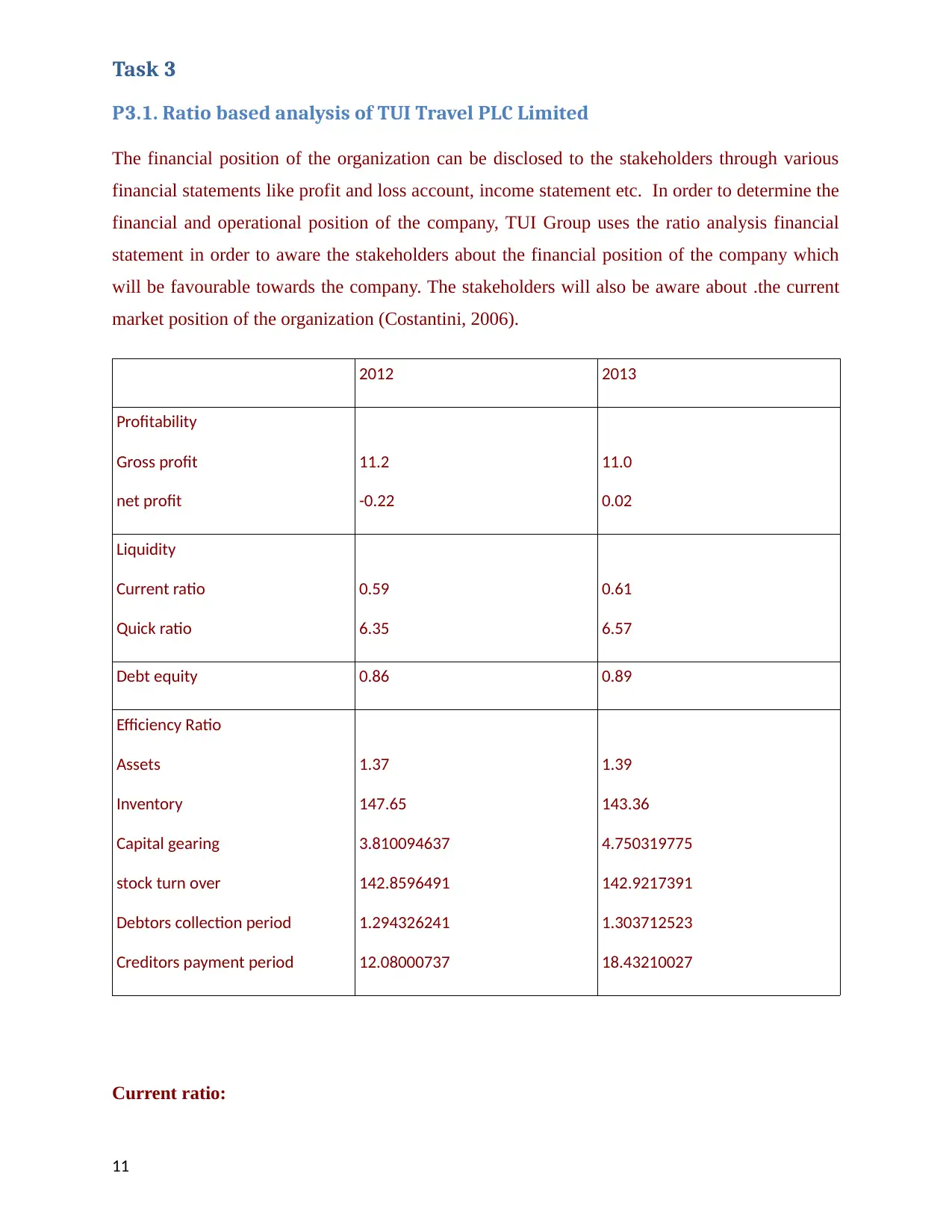

P3.1. Ratio based analysis of TUI Travel PLC Limited

The financial position of the organization can be disclosed to the stakeholders through various

financial statements like profit and loss account, income statement etc. In order to determine the

financial and operational position of the company, TUI Group uses the ratio analysis financial

statement in order to aware the stakeholders about the financial position of the company which

will be favourable towards the company. The stakeholders will also be aware about .the current

market position of the organization (Costantini, 2006).

2012 2013

Profitability

Gross profit

net profit

11.2

-0.22

11.0

0.02

Liquidity

Current ratio

Quick ratio

0.59

6.35

0.61

6.57

Debt equity 0.86 0.89

Efficiency Ratio

Assets

Inventory

Capital gearing

stock turn over

Debtors collection period

Creditors payment period

1.37

147.65

3.810094637

142.8596491

1.294326241

12.08000737

1.39

143.36

4.750319775

142.9217391

1.303712523

18.43210027

Current ratio:

11

P3.1. Ratio based analysis of TUI Travel PLC Limited

The financial position of the organization can be disclosed to the stakeholders through various

financial statements like profit and loss account, income statement etc. In order to determine the

financial and operational position of the company, TUI Group uses the ratio analysis financial

statement in order to aware the stakeholders about the financial position of the company which

will be favourable towards the company. The stakeholders will also be aware about .the current

market position of the organization (Costantini, 2006).

2012 2013

Profitability

Gross profit

net profit

11.2

-0.22

11.0

0.02

Liquidity

Current ratio

Quick ratio

0.59

6.35

0.61

6.57

Debt equity 0.86 0.89

Efficiency Ratio

Assets

Inventory

Capital gearing

stock turn over

Debtors collection period

Creditors payment period

1.37

147.65

3.810094637

142.8596491

1.294326241

12.08000737

1.39

143.36

4.750319775

142.9217391

1.303712523

18.43210027

Current ratio:

11

The relation between the current assets and liabilities are shown with the help of current ratio.

The current ratio shows the potential of the company in terms of its liquidity position of the

business and determines the capability to fund the company’s short term obligations and debt

handling. After making the calculation it is realized that the current ratio of TUI group in the year

2013 has increased from 0.61 by 0.59 in comparison with the previous year. It clearly reflects

that the liquidity position of TUI group has enriched in 2013 compared to the previous year.

Acid test ratio:

The acid test ratio is also popularly known as quick ratio. It projects the relation between the

liquid assets which are easily convertible to cash and the current liabilities. This reflects the

ability of the company in order to pay all the debts out of its liquid assets. As per the above

calculation it has ascertained that in 2013 the quick ration has increased by 6.57 by 6.35.

Return on net assets:

The income of the company which is generated from its assets during a financial year is shown

by a profitability ratio which is the return of net assets. The ratio of the annual net incomes and

the total assets of a company are measured as return on net assets. The return on net asset of the

TUI group has remained fixed on both of the years and the operational value of the company also

doesn’t increase.

Debtor’s collection period

The debtor’s collection period ratio helps in gauging the performance of the company. The time

period in which the recovery of the credit is done i.e. the accounts receivable is collected is

determined by this ratio. The debtor’s collection period of this company and the improvement of

the company within a couple of years is determined with the help of this ratio. The debtors

collection period was 12.08000737 in the 2012 which was increased by 18.43210027 in 2013

Creditor’s payment period:

12

The current ratio shows the potential of the company in terms of its liquidity position of the

business and determines the capability to fund the company’s short term obligations and debt

handling. After making the calculation it is realized that the current ratio of TUI group in the year

2013 has increased from 0.61 by 0.59 in comparison with the previous year. It clearly reflects

that the liquidity position of TUI group has enriched in 2013 compared to the previous year.

Acid test ratio:

The acid test ratio is also popularly known as quick ratio. It projects the relation between the

liquid assets which are easily convertible to cash and the current liabilities. This reflects the

ability of the company in order to pay all the debts out of its liquid assets. As per the above

calculation it has ascertained that in 2013 the quick ration has increased by 6.57 by 6.35.

Return on net assets:

The income of the company which is generated from its assets during a financial year is shown

by a profitability ratio which is the return of net assets. The ratio of the annual net incomes and

the total assets of a company are measured as return on net assets. The return on net asset of the

TUI group has remained fixed on both of the years and the operational value of the company also

doesn’t increase.

Debtor’s collection period

The debtor’s collection period ratio helps in gauging the performance of the company. The time

period in which the recovery of the credit is done i.e. the accounts receivable is collected is

determined by this ratio. The debtor’s collection period of this company and the improvement of

the company within a couple of years is determined with the help of this ratio. The debtors

collection period was 12.08000737 in the 2012 which was increased by 18.43210027 in 2013

Creditor’s payment period:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.