ACC97003M: Financial Analysis of Tuuli Plc - Performance and Options

VerifiedAdded on 2023/05/10

|11

|2492

|274

Report

AI Summary

This report presents a financial analysis of Tuuli Plc, focusing on its performance in 2020 and 2021. The analysis begins with an executive summary, followed by an introduction that outlines the company's background and the report's structure. Part A delves into a critical analysis of financial ratios, including liquidity, solvency, and profitability ratios, to assess the company's financial position. The report calculates and interprets current, quick, debt-to-equity, interest coverage, ROCE, ROE, gross profit margin, and net profit margin ratios. Part B evaluates three strategic options for a clearance sale, recommending Option 2 (participation in a UK show) as the most suitable, supported by detailed calculations and estimated values. The report concludes with a summary of findings and recommendations, emphasizing Tuuli Plc's overall financial health and potential for future growth. The appendix includes detailed calculations and references.

ACC97003M

Financial Analysis, Appraisal & Decision Making

Financial Analysis, Appraisal & Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMAR SHAHZAD

26211752

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

Introduction..............................................................................................................................................3

PART-A......................................................................................................................................................3

CRITICAL ANALYSIS OF RATIOS.......................................................................................................3

LIQUIDITY RATIOS.............................................................................................................................3

SOLVENCY RATIOS...........................................................................................................................4

PROFITABILITY RATIOS...................................................................................................................4

PART-B......................................................................................................................................................5

Option 1.................................................................................................................................................5

Option 2.................................................................................................................................................5

Option 3.................................................................................................................................................5

Recommendations for Option 2..........................................................................................................5

CONCLUSION..........................................................................................................................................6

APPENDIX................................................................................................................................................6

References...............................................................................................................................................8

1

26211752

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

Introduction..............................................................................................................................................3

PART-A......................................................................................................................................................3

CRITICAL ANALYSIS OF RATIOS.......................................................................................................3

LIQUIDITY RATIOS.............................................................................................................................3

SOLVENCY RATIOS...........................................................................................................................4

PROFITABILITY RATIOS...................................................................................................................4

PART-B......................................................................................................................................................5

Option 1.................................................................................................................................................5

Option 2.................................................................................................................................................5

Option 3.................................................................................................................................................5

Recommendations for Option 2..........................................................................................................5

CONCLUSION..........................................................................................................................................6

APPENDIX................................................................................................................................................6

References...............................................................................................................................................8

1

UMAR SHAHZAD

26211752

EXECUTIVE SUMMARY

This reports is based in facts and figures taken from Tuuli Plc as calculations done on

the basis of provided financial statement of the company for the year 2020 and 2021.

Report is comprised of two parts and in part one analysis of ratios is done on the basis

of results to know the financial position of the company, for this liquidity, solvency and

profitability and other ratios are calculated which shows company’s overall performance

is good and Tuuli Plc is a stable company.

In part two of the report three given options are discussed to for clearance sale and

most suitable options is recommend on the basis of facts and figures.

Recommendations are made for future betterment of the company by analysing the

current situation from the available options. In first option one profit and loss is

discussed but as per evaluation company can face loss if it adopt option 1 so company

has two more options of UK show and investment in social housing project and as per

calculations these both methods are suitable for company and recommendation are

also made on the basis of selected option.

2

26211752

EXECUTIVE SUMMARY

This reports is based in facts and figures taken from Tuuli Plc as calculations done on

the basis of provided financial statement of the company for the year 2020 and 2021.

Report is comprised of two parts and in part one analysis of ratios is done on the basis

of results to know the financial position of the company, for this liquidity, solvency and

profitability and other ratios are calculated which shows company’s overall performance

is good and Tuuli Plc is a stable company.

In part two of the report three given options are discussed to for clearance sale and

most suitable options is recommend on the basis of facts and figures.

Recommendations are made for future betterment of the company by analysing the

current situation from the available options. In first option one profit and loss is

discussed but as per evaluation company can face loss if it adopt option 1 so company

has two more options of UK show and investment in social housing project and as per

calculations these both methods are suitable for company and recommendation are

also made on the basis of selected option.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UMAR SHAHZAD

26211752

Introduction

Tuuli Plc is a growing organisation in energy sector which has started in 2000 as a wind

turbine company but later on expanded business to energy sector. As a new employee

in organisation under graduate scheme company’s financial statement is elaborated in

detail to know the scenario of Tuuli Plc and its future. Based on different calculations

and current issues or opportunities recommendations will be made at the end of the

report.

This report is based on two parts; part A and part B. In part A, financial Ratio analysis

will be done in the report to know the current position of company in different

perspectives along with comparison with previous year. Liquidity ratios will be calculated

to know about short term obligations of company (Sherman, 2015) in year 2020 and

2021. Solvency ratios will also be discussed to know the profitability status of Tuuli Plc

and investment or earnings ratios will also be discussed to know performance of

company in investor’s point of view. In part B different optioned will be discussed and

one best fit option will be chosen for company along with its recommendations.

PART-A

CRITICAL ANALYSIS OF RATIOS

Financial ratios gives the best picture of company’s overall performance and it helps to

analyses that how company is performing currently and how it performed in past

(Manzler, 2004).

LIQUIDITY RATIOS

Liquidity is very important for any company because a company can survive in loss but

can never survive without liquidity (Rashid, 2021). Liquidity ratios shows ability of

company to pay its debts and short term obligations (Sherman, 2015). Short term

coverage for the company is essential (Davies & Crawford, 2012). As it can see in

calculations that current ratio of Tuuli Plc in 2020 is 1.55 and in 2021 is 1.75 so it means

company is strong enough to pay its debts and it even stronger in 2021 as compared to

2020 which is a good sign. In 2020 it seems company was short in cash to its short term

obligations but in 2021 company had enough cash to meet its short term obligations.

3

26211752

Introduction

Tuuli Plc is a growing organisation in energy sector which has started in 2000 as a wind

turbine company but later on expanded business to energy sector. As a new employee

in organisation under graduate scheme company’s financial statement is elaborated in

detail to know the scenario of Tuuli Plc and its future. Based on different calculations

and current issues or opportunities recommendations will be made at the end of the

report.

This report is based on two parts; part A and part B. In part A, financial Ratio analysis

will be done in the report to know the current position of company in different

perspectives along with comparison with previous year. Liquidity ratios will be calculated

to know about short term obligations of company (Sherman, 2015) in year 2020 and

2021. Solvency ratios will also be discussed to know the profitability status of Tuuli Plc

and investment or earnings ratios will also be discussed to know performance of

company in investor’s point of view. In part B different optioned will be discussed and

one best fit option will be chosen for company along with its recommendations.

PART-A

CRITICAL ANALYSIS OF RATIOS

Financial ratios gives the best picture of company’s overall performance and it helps to

analyses that how company is performing currently and how it performed in past

(Manzler, 2004).

LIQUIDITY RATIOS

Liquidity is very important for any company because a company can survive in loss but

can never survive without liquidity (Rashid, 2021). Liquidity ratios shows ability of

company to pay its debts and short term obligations (Sherman, 2015). Short term

coverage for the company is essential (Davies & Crawford, 2012). As it can see in

calculations that current ratio of Tuuli Plc in 2020 is 1.55 and in 2021 is 1.75 so it means

company is strong enough to pay its debts and it even stronger in 2021 as compared to

2020 which is a good sign. In 2020 it seems company was short in cash to its short term

obligations but in 2021 company had enough cash to meet its short term obligations.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMAR SHAHZAD

26211752

Quick ratio of company in 2020 is 1.18 and in 2021 is 1.38 and that is good sign for

Tuuli Plc in paying off its liabilities.

SOLVENCY RATIOS

Solvency ratios generally measures the company’s profitability and it shows a clear view

to investors that how company can pay its debts in long term. Entrepreneurs look at

solvency ratios of the most of the times to check cash flows and management flexibility

(Vasiu & Gheorghe, 2014).

Debt to equity ratio of Tuuli Plc in 2020 is 3.22 and in 2021 is 2.43 It indicates in 2020

more of business was funded by equity. And in 2020 company was more dependent on

equity as compared to 2021. So it is a good sign for company as their debt is

decreasing as compared to previous year. Here it can be analyzed that high debt to

equity ratio show more investment in loan capital as compared to equity (Patel, 2015).

Interest coverage ratio depicts how strong is firm to pay interest on debt so according to

results of Calculation, Company in both years 2020 and 2021 is good enough to pay the

interest on debt. In 2020 company was 5.22 times stronger to pay interest and in 2021 it

is 4.45 times stronger in paying off interest on debts.

PROFITABILITY RATIOS

Profitability ratios depicts that how efficient is the company in generating profit as it

investigates the profitability of company in different perspectives with net profit and

gross profit margin and ROCE (return on capital employed) & ROE ( return of equity)

depicts how company is valuable for its shareholders. Profitability indicates that how

much capital is invested (Rashid, 2021).

ROCE ratio in 2020 is 7.40% and in 2021 is 6.85%, it shows how well company is

generating profit from capital so according to calculations in 2020 ratio was higher but in

2021 it has decreased which is indicates little decrease in growth of company and it also

shows less return on investment. High value in return on capital employed indicates

competitive advantage of company (Singh & Yadav, 2013). ROE in 2020 was 26.20%

and in 2021 it is 20.2%, this shows decrease in ability of company in profit generation

and growing the value of shareholders.

Gross profit margin generally shows how successful is the company in generating

revenue and in case of Tuuli Plc gross profit margin in 2020 was 26.7 and in 2021 it

decreased to 28.3 % which is a healthy sign for the company as its gross profit margin

is increased by 1.6%.

4

26211752

Quick ratio of company in 2020 is 1.18 and in 2021 is 1.38 and that is good sign for

Tuuli Plc in paying off its liabilities.

SOLVENCY RATIOS

Solvency ratios generally measures the company’s profitability and it shows a clear view

to investors that how company can pay its debts in long term. Entrepreneurs look at

solvency ratios of the most of the times to check cash flows and management flexibility

(Vasiu & Gheorghe, 2014).

Debt to equity ratio of Tuuli Plc in 2020 is 3.22 and in 2021 is 2.43 It indicates in 2020

more of business was funded by equity. And in 2020 company was more dependent on

equity as compared to 2021. So it is a good sign for company as their debt is

decreasing as compared to previous year. Here it can be analyzed that high debt to

equity ratio show more investment in loan capital as compared to equity (Patel, 2015).

Interest coverage ratio depicts how strong is firm to pay interest on debt so according to

results of Calculation, Company in both years 2020 and 2021 is good enough to pay the

interest on debt. In 2020 company was 5.22 times stronger to pay interest and in 2021 it

is 4.45 times stronger in paying off interest on debts.

PROFITABILITY RATIOS

Profitability ratios depicts that how efficient is the company in generating profit as it

investigates the profitability of company in different perspectives with net profit and

gross profit margin and ROCE (return on capital employed) & ROE ( return of equity)

depicts how company is valuable for its shareholders. Profitability indicates that how

much capital is invested (Rashid, 2021).

ROCE ratio in 2020 is 7.40% and in 2021 is 6.85%, it shows how well company is

generating profit from capital so according to calculations in 2020 ratio was higher but in

2021 it has decreased which is indicates little decrease in growth of company and it also

shows less return on investment. High value in return on capital employed indicates

competitive advantage of company (Singh & Yadav, 2013). ROE in 2020 was 26.20%

and in 2021 it is 20.2%, this shows decrease in ability of company in profit generation

and growing the value of shareholders.

Gross profit margin generally shows how successful is the company in generating

revenue and in case of Tuuli Plc gross profit margin in 2020 was 26.7 and in 2021 it

decreased to 28.3 % which is a healthy sign for the company as its gross profit margin

is increased by 1.6%.

4

UMAR SHAHZAD

26211752

Net profit margin measures that how much net income or profit is received and Tuuli Plc

in 2020 generated the net profit margin of 13.9% and in 2021 it slightly increased to

14.05% and this increase shows that gross profit margin is also increased so overall

profit of company is increased.

PART-B

Option 1

In option one company has opportunity to advertise their sales on website but sales

director is not happy with the plan and as per him it can effect negatively on company’s

profit because it will show we are in trouble with our sales so it is not recommended to

use this option.

Option 2

In this options supervisor suggested to participate in UK show where their competitors

will also market their products but there a some risks involved that if company offers too

much discount it will lose its profit and if company offers low discount customers can go

anywhere else so based on these risk event manager has provided some suggestions

and based on calculations done according to these figure provided by the event

manager to company, it can get maximum profit from parity with competitors. While

making decisions like campaigns companies always look at estimated value of the

company and as per calculations this is recommended method.

Option 3

NPV is calculated on the basis of given facts and figures and total NPV is 1,114,000

which is also suitable for company but I have recommended option 2 and according to

calculation both options 2 and option 3 are suitable for company. NPV is basically used

to know the difference between present value of cash inflows and outflows ( Artill &

McLaney, 2018) and higher NPV is always better than lower.

Recommendations for Option 2

Among three available options, option 2 is most suitable for the company to clear their

items with profit because it can give maximum profit to company when company go for

sale of 600 units of Inti with the probability of 45% and with maximum 2000 units of Ra

5

26211752

Net profit margin measures that how much net income or profit is received and Tuuli Plc

in 2020 generated the net profit margin of 13.9% and in 2021 it slightly increased to

14.05% and this increase shows that gross profit margin is also increased so overall

profit of company is increased.

PART-B

Option 1

In option one company has opportunity to advertise their sales on website but sales

director is not happy with the plan and as per him it can effect negatively on company’s

profit because it will show we are in trouble with our sales so it is not recommended to

use this option.

Option 2

In this options supervisor suggested to participate in UK show where their competitors

will also market their products but there a some risks involved that if company offers too

much discount it will lose its profit and if company offers low discount customers can go

anywhere else so based on these risk event manager has provided some suggestions

and based on calculations done according to these figure provided by the event

manager to company, it can get maximum profit from parity with competitors. While

making decisions like campaigns companies always look at estimated value of the

company and as per calculations this is recommended method.

Option 3

NPV is calculated on the basis of given facts and figures and total NPV is 1,114,000

which is also suitable for company but I have recommended option 2 and according to

calculation both options 2 and option 3 are suitable for company. NPV is basically used

to know the difference between present value of cash inflows and outflows ( Artill &

McLaney, 2018) and higher NPV is always better than lower.

Recommendations for Option 2

Among three available options, option 2 is most suitable for the company to clear their

items with profit because it can give maximum profit to company when company go for

sale of 600 units of Inti with the probability of 45% and with maximum 2000 units of Ra

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UMAR SHAHZAD

26211752

by using probability of 45% and these sales can give the highest profit of £210,357 for

Inti and £410,400 for Ra and collectively it can give profit of £620,757 so this is most

recommended and suggested method according to my calculations. Another reason of

suggesting this method is it involves both old and new panels Ra and Inti so it can help

company to clear old stock and to promote new product as well.

Estimated value is calculated and excel is attached in appendix.

Reason of recommending this option is during the show company has opportunity to

advertise and introduce their products to new people so there they will make new

customers along with financial benefits they will also get brand promotion.

CONCLUSION

Liquidity, solvency and performance ratios are calculated and results are analyzed as

well in the report After the analysis of ratios and discussing available options it can be

concluded that Tuuli Plc is a decent company with a good performance and it can be

more profitable in future if work on given recommendation made on the basis of

calculations in all three options. Company has opportunity to grow in future and earn the

profit. In Part B of assignment three options are discussed and best suited options is

recommended as well for the future growth of company.

APPENDIX

PART A Calculations

Ratios Formula 2021 2020

LIQUIDITY RATIOS

Current Ratio

Current

Assets/Current

Liabilities

8038/4584=1.75 6577/4245=1.55

Quick Ratio

Current Assets-

Inventory/Curre

nt Liabilities

8038-1685/4584=1.38 6577-1574/4245=1.18

SOLVENCY RATIOS

Debt to

Equity Ratio

Total Debt/Total

Equity 23141/9516= 2.43 20645/6416=3.21

Interest

Coverage

Ratio

EBIT/Interest

Payble 1924/432= 4.45 times 1693/324= 5.22 times

6

26211752

by using probability of 45% and these sales can give the highest profit of £210,357 for

Inti and £410,400 for Ra and collectively it can give profit of £620,757 so this is most

recommended and suggested method according to my calculations. Another reason of

suggesting this method is it involves both old and new panels Ra and Inti so it can help

company to clear old stock and to promote new product as well.

Estimated value is calculated and excel is attached in appendix.

Reason of recommending this option is during the show company has opportunity to

advertise and introduce their products to new people so there they will make new

customers along with financial benefits they will also get brand promotion.

CONCLUSION

Liquidity, solvency and performance ratios are calculated and results are analyzed as

well in the report After the analysis of ratios and discussing available options it can be

concluded that Tuuli Plc is a decent company with a good performance and it can be

more profitable in future if work on given recommendation made on the basis of

calculations in all three options. Company has opportunity to grow in future and earn the

profit. In Part B of assignment three options are discussed and best suited options is

recommended as well for the future growth of company.

APPENDIX

PART A Calculations

Ratios Formula 2021 2020

LIQUIDITY RATIOS

Current Ratio

Current

Assets/Current

Liabilities

8038/4584=1.75 6577/4245=1.55

Quick Ratio

Current Assets-

Inventory/Curre

nt Liabilities

8038-1685/4584=1.38 6577-1574/4245=1.18

SOLVENCY RATIOS

Debt to

Equity Ratio

Total Debt/Total

Equity 23141/9516= 2.43 20645/6416=3.21

Interest

Coverage

Ratio

EBIT/Interest

Payble 1924/432= 4.45 times 1693/324= 5.22 times

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMAR SHAHZAD

26211752

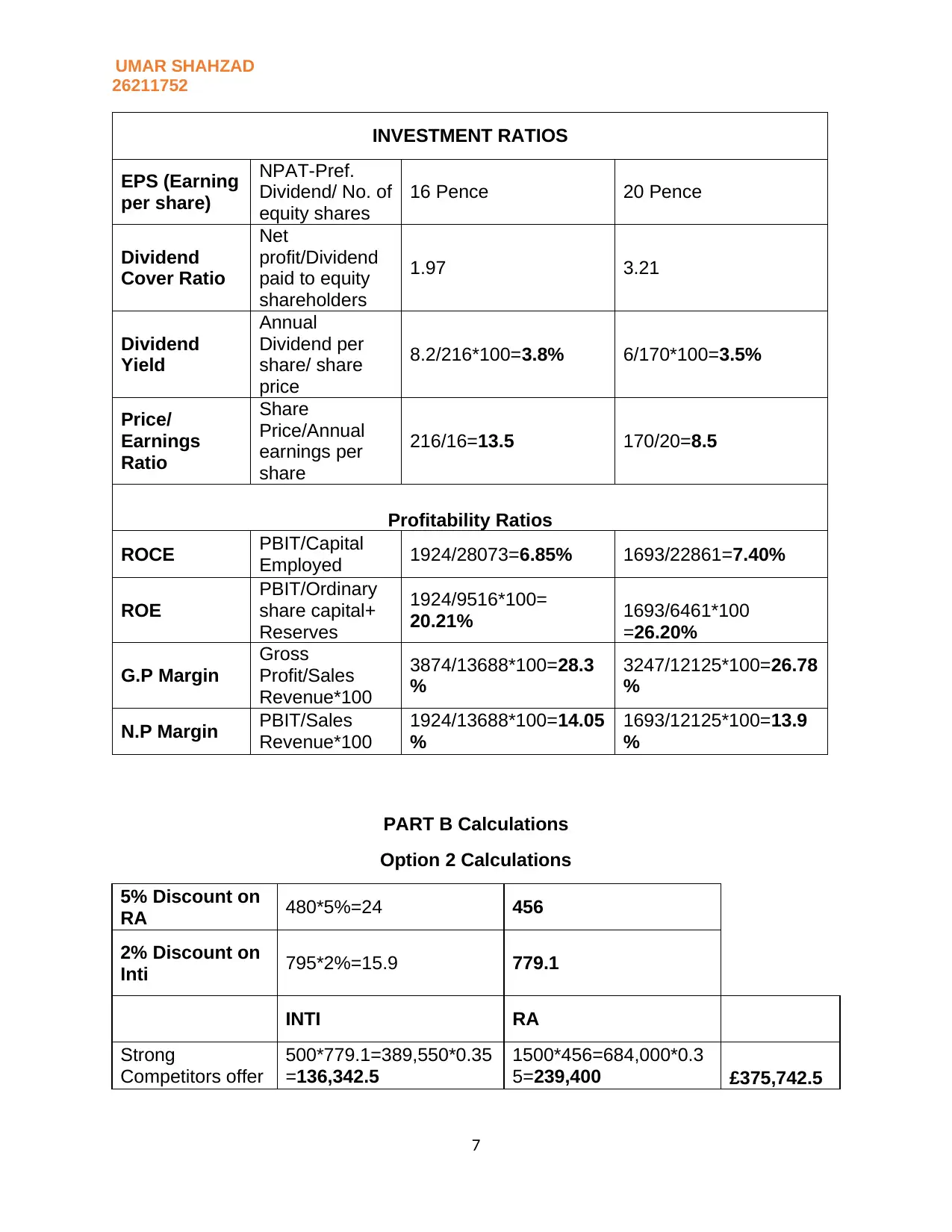

INVESTMENT RATIOS

EPS (Earning

per share)

NPAT-Pref.

Dividend/ No. of

equity shares

16 Pence 20 Pence

Dividend

Cover Ratio

Net

profit/Dividend

paid to equity

shareholders

1.97 3.21

Dividend

Yield

Annual

Dividend per

share/ share

price

8.2/216*100=3.8% 6/170*100=3.5%

Price/

Earnings

Ratio

Share

Price/Annual

earnings per

share

216/16=13.5 170/20=8.5

Profitability Ratios

ROCE PBIT/Capital

Employed 1924/28073=6.85% 1693/22861=7.40%

ROE

PBIT/Ordinary

share capital+

Reserves

1924/9516*100=

20.21% 1693/6461*100

=26.20%

G.P Margin

Gross

Profit/Sales

Revenue*100

3874/13688*100=28.3

%

3247/12125*100=26.78

%

N.P Margin PBIT/Sales

Revenue*100

1924/13688*100=14.05

%

1693/12125*100=13.9

%

PART B Calculations

Option 2 Calculations

5% Discount on

RA 480*5%=24 456

2% Discount on

Inti 795*2%=15.9 779.1

INTI RA

Strong

Competitors offer

500*779.1=389,550*0.35

=136,342.5

1500*456=684,000*0.3

5=239,400 £375,742.5

7

26211752

INVESTMENT RATIOS

EPS (Earning

per share)

NPAT-Pref.

Dividend/ No. of

equity shares

16 Pence 20 Pence

Dividend

Cover Ratio

Net

profit/Dividend

paid to equity

shareholders

1.97 3.21

Dividend

Yield

Annual

Dividend per

share/ share

price

8.2/216*100=3.8% 6/170*100=3.5%

Price/

Earnings

Ratio

Share

Price/Annual

earnings per

share

216/16=13.5 170/20=8.5

Profitability Ratios

ROCE PBIT/Capital

Employed 1924/28073=6.85% 1693/22861=7.40%

ROE

PBIT/Ordinary

share capital+

Reserves

1924/9516*100=

20.21% 1693/6461*100

=26.20%

G.P Margin

Gross

Profit/Sales

Revenue*100

3874/13688*100=28.3

%

3247/12125*100=26.78

%

N.P Margin PBIT/Sales

Revenue*100

1924/13688*100=14.05

%

1693/12125*100=13.9

%

PART B Calculations

Option 2 Calculations

5% Discount on

RA 480*5%=24 456

2% Discount on

Inti 795*2%=15.9 779.1

INTI RA

Strong

Competitors offer

500*779.1=389,550*0.35

=136,342.5

1500*456=684,000*0.3

5=239,400 £375,742.5

7

UMAR SHAHZAD

26211752

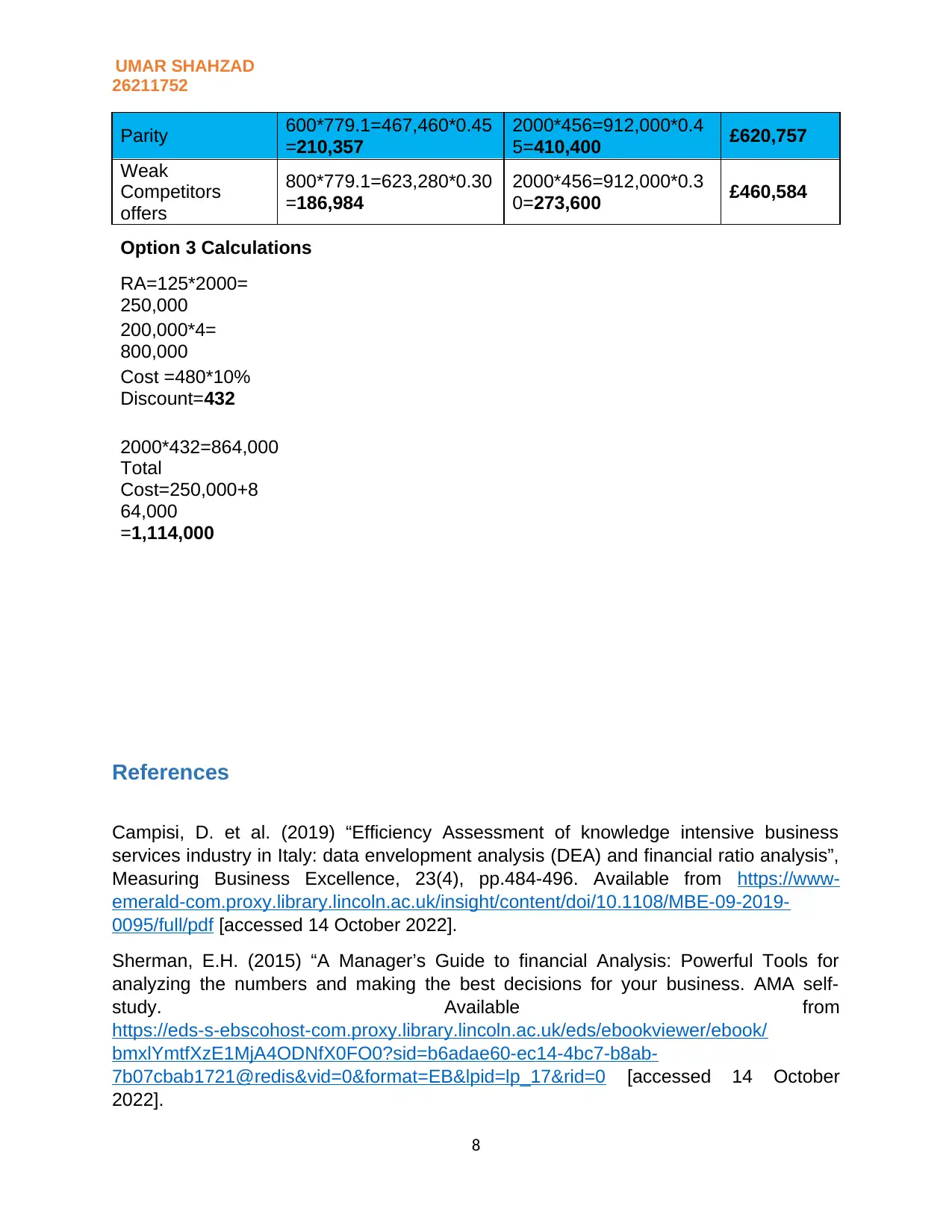

Parity 600*779.1=467,460*0.45

=210,357

2000*456=912,000*0.4

5=410,400 £620,757

Weak

Competitors

offers

800*779.1=623,280*0.30

=186,984

2000*456=912,000*0.3

0=273,600 £460,584

Option 3 Calculations

RA=125*2000=

250,000

200,000*4=

800,000

Cost =480*10%

Discount=432

2000*432=864,000

Total

Cost=250,000+8

64,000

=1,114,000

References

Campisi, D. et al. (2019) “Efficiency Assessment of knowledge intensive business

services industry in Italy: data envelopment analysis (DEA) and financial ratio analysis”,

Measuring Business Excellence, 23(4), pp.484-496. Available from https://www-

emerald-com.proxy.library.lincoln.ac.uk/insight/content/doi/10.1108/MBE-09-2019-

0095/full/pdf [accessed 14 October 2022].

Sherman, E.H. (2015) “A Manager’s Guide to financial Analysis: Powerful Tools for

analyzing the numbers and making the best decisions for your business. AMA self-

study. Available from

https://eds-s-ebscohost-com.proxy.library.lincoln.ac.uk/eds/ebookviewer/ebook/

bmxlYmtfXzE1MjA4ODNfX0FO0?sid=b6adae60-ec14-4bc7-b8ab-

7b07cbab1721@redis&vid=0&format=EB&lpid=lp_17&rid=0 [accessed 14 October

2022].

8

26211752

Parity 600*779.1=467,460*0.45

=210,357

2000*456=912,000*0.4

5=410,400 £620,757

Weak

Competitors

offers

800*779.1=623,280*0.30

=186,984

2000*456=912,000*0.3

0=273,600 £460,584

Option 3 Calculations

RA=125*2000=

250,000

200,000*4=

800,000

Cost =480*10%

Discount=432

2000*432=864,000

Total

Cost=250,000+8

64,000

=1,114,000

References

Campisi, D. et al. (2019) “Efficiency Assessment of knowledge intensive business

services industry in Italy: data envelopment analysis (DEA) and financial ratio analysis”,

Measuring Business Excellence, 23(4), pp.484-496. Available from https://www-

emerald-com.proxy.library.lincoln.ac.uk/insight/content/doi/10.1108/MBE-09-2019-

0095/full/pdf [accessed 14 October 2022].

Sherman, E.H. (2015) “A Manager’s Guide to financial Analysis: Powerful Tools for

analyzing the numbers and making the best decisions for your business. AMA self-

study. Available from

https://eds-s-ebscohost-com.proxy.library.lincoln.ac.uk/eds/ebookviewer/ebook/

bmxlYmtfXzE1MjA4ODNfX0FO0?sid=b6adae60-ec14-4bc7-b8ab-

7b07cbab1721@redis&vid=0&format=EB&lpid=lp_17&rid=0 [accessed 14 October

2022].

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UMAR SHAHZAD

26211752

Edmister, R.O. (1972) “An Empirical Test of Financial Ratio Analysis for small Business

Failure Prediction,” Journal of Financial & Quantitative Analysis. Cambridge University

Press, 7(2), pp. 1477-1493. Available from

https://www.cambridge.org/core/journals/journal-of-financial-and-quantitative-analysis/

article/abs/an-empirical-test-of-financial-ratio-analysis-for-small-business-failure-

prediction/5B6446728276923EE0657CA4ADD84F83 [Accessed 14 Oct 2022].

Rashid, C.A. (2021) “The Efficiency of financial ratios analysis to evaluate company’s

profitability.” Journal of Global Economic & Business, 2(4), pp.119-132. Available from

https://www.researchgate.net/publication/348686551_THE_EFFICIENCY_OF_FINANCI

AL_RATIOS_ANALYSIS_TO_EVALUATE_COMPANY'S_PROFITABILITY [Accessed

13 Oct 2021].

Manzler, D. (2004) “Liquidity Ratios & Business Performance.” Journal of Financial

Ratios Analysis, 67(45), pp12-16. Available from

https://ictactjournals.in/paper/IJMS_V6_I3_Paper_5_1273_1275.pdf [Accessed 13 Oct

2022].

Suthar, K.U. (2018) “Financial Ratio Analysis: A Theoretical Study.” International journal

of research in all subjects in Multi-languages, 6(3). Available from

http://www.raijmr.com/ijrsml/wp-content/uploads/2018/06/IJRSML_2018_vol06_issue_3

_Eng_09.pdf [Accessed 14 Oct 2022].

Srividhya, S, et al., (2020) “A study on financial ratio Analysis of Planys technologies

Pvt. Ltd. India.” Elementary Education online 19(3), pp. 4642-4652. Available from

https://www.ilkogretim-online.org/fulltext/218-1642781318.pdf [Accessed 14 Oct 2022].

Vasiu, D.E. & Gheorghe, I. (2014) “ Case study regarding solvency analysis, during

2006-2012, of the companies having the business line in Industry and construction,

Listed and Traded on the Bucharest Stock Exchange”. PP. 258-269. Available from

https://www.sciencedirect.com/science/article/pii/S2212567114007990?

ref=pdf_download&fr=RR-2&rr=75c2f824da8d8861 [Accessed 13 Oct 2022].

Patel, M.K.V. (2015) “Analysis of Solvency of selected FMCG Companies in India.”

Journal of research in Humanities and Soc. Sciences, 3(9). Available from

https://www.raijmr.com/ijrhs/wp-content/uploads/2017/11/IJRHS_2015_vol03_issue_09

_06.pdf [Accessed 13 Oct 2022].

Singh, J. & Yadav, P. (2013) “Return on Capital Employed- A tool for analyzing

Profitability of companies.” International Journal of Techno- Management Research,

1(1). Available from https://www.ijtmr.com/docs/vol1/ju2013(5).pdf [Accessed 14 Oct

2022].

Artill, P. & McLaney, E. (2018) “Accounting and Finance for non- specialists, Pearson

Education, Limited, Harlow. Available from https://ebookcentral-proquest-

com.proxy.library.lincoln.ac.uk/lib/ulinc/detail.action?docID=5601284# [Accessed 14 Oct

2022].

9

26211752

Edmister, R.O. (1972) “An Empirical Test of Financial Ratio Analysis for small Business

Failure Prediction,” Journal of Financial & Quantitative Analysis. Cambridge University

Press, 7(2), pp. 1477-1493. Available from

https://www.cambridge.org/core/journals/journal-of-financial-and-quantitative-analysis/

article/abs/an-empirical-test-of-financial-ratio-analysis-for-small-business-failure-

prediction/5B6446728276923EE0657CA4ADD84F83 [Accessed 14 Oct 2022].

Rashid, C.A. (2021) “The Efficiency of financial ratios analysis to evaluate company’s

profitability.” Journal of Global Economic & Business, 2(4), pp.119-132. Available from

https://www.researchgate.net/publication/348686551_THE_EFFICIENCY_OF_FINANCI

AL_RATIOS_ANALYSIS_TO_EVALUATE_COMPANY'S_PROFITABILITY [Accessed

13 Oct 2021].

Manzler, D. (2004) “Liquidity Ratios & Business Performance.” Journal of Financial

Ratios Analysis, 67(45), pp12-16. Available from

https://ictactjournals.in/paper/IJMS_V6_I3_Paper_5_1273_1275.pdf [Accessed 13 Oct

2022].

Suthar, K.U. (2018) “Financial Ratio Analysis: A Theoretical Study.” International journal

of research in all subjects in Multi-languages, 6(3). Available from

http://www.raijmr.com/ijrsml/wp-content/uploads/2018/06/IJRSML_2018_vol06_issue_3

_Eng_09.pdf [Accessed 14 Oct 2022].

Srividhya, S, et al., (2020) “A study on financial ratio Analysis of Planys technologies

Pvt. Ltd. India.” Elementary Education online 19(3), pp. 4642-4652. Available from

https://www.ilkogretim-online.org/fulltext/218-1642781318.pdf [Accessed 14 Oct 2022].

Vasiu, D.E. & Gheorghe, I. (2014) “ Case study regarding solvency analysis, during

2006-2012, of the companies having the business line in Industry and construction,

Listed and Traded on the Bucharest Stock Exchange”. PP. 258-269. Available from

https://www.sciencedirect.com/science/article/pii/S2212567114007990?

ref=pdf_download&fr=RR-2&rr=75c2f824da8d8861 [Accessed 13 Oct 2022].

Patel, M.K.V. (2015) “Analysis of Solvency of selected FMCG Companies in India.”

Journal of research in Humanities and Soc. Sciences, 3(9). Available from

https://www.raijmr.com/ijrhs/wp-content/uploads/2017/11/IJRHS_2015_vol03_issue_09

_06.pdf [Accessed 13 Oct 2022].

Singh, J. & Yadav, P. (2013) “Return on Capital Employed- A tool for analyzing

Profitability of companies.” International Journal of Techno- Management Research,

1(1). Available from https://www.ijtmr.com/docs/vol1/ju2013(5).pdf [Accessed 14 Oct

2022].

Artill, P. & McLaney, E. (2018) “Accounting and Finance for non- specialists, Pearson

Education, Limited, Harlow. Available from https://ebookcentral-proquest-

com.proxy.library.lincoln.ac.uk/lib/ulinc/detail.action?docID=5601284# [Accessed 14 Oct

2022].

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMAR SHAHZAD

26211752

10

26211752

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.